Detailed Analysis of The Abraaj Group Scandal and Collapse Case Study

VerifiedAdded on 2022/12/28

|9

|2619

|34

Case Study

AI Summary

This case study examines the Abraaj Group, a Dubai-based private equity firm, and its dramatic collapse due to allegations of fraud and financial mismanagement. The report delves into the assessment of risks, including business, compliance, and financial risks, highlighting the firm's failure to effectively manage its market position and maintain accurate financial reporting. It analyzes Abraaj's responses to its risk exposure, the gaps and shortfalls in its approach, and the relevant aspects of risk governance and regulatory failures. The scandal involved accusations of misrepresenting financial performance, misappropriating investor funds, and failing to comply with financial regulations, leading to the arrest of key executives and highlighting significant loopholes in international regulatory oversight. The case study concludes by emphasizing the need for enhanced regulatory scrutiny, internal controls, and transparent financial practices to prevent similar scandals in the future, offering valuable insights into the complexities of financial risk management and corporate governance.

Case Study The Abraaj Group

Scandal and Collapse

Scandal and Collapse

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

ASSESSMENT OF RISK..........................................................................................................3

RISK RESPONSE......................................................................................................................5

Abraaj’s response to its risk exposure....................................................................................5

Gaps and shortfalls in Abraaj’s approach..............................................................................5

Relevant aspects of risk governance and regulatory risk.......................................................6

CONCLUSION..........................................................................................................................7

REFERENCES...........................................................................................................................8

INTRODUCTION......................................................................................................................3

ASSESSMENT OF RISK..........................................................................................................3

RISK RESPONSE......................................................................................................................5

Abraaj’s response to its risk exposure....................................................................................5

Gaps and shortfalls in Abraaj’s approach..............................................................................5

Relevant aspects of risk governance and regulatory risk.......................................................6

CONCLUSION..........................................................................................................................7

REFERENCES...........................................................................................................................8

INTRODUCTION

Abraaj which is a private equity firm based in Dubai, considered to be the most

influential emerging market after sixteen years of its operation having $14 bn in AUM. In the

year 2019, its founder Arif Naqvi and then executive Mustafa Abdel-Wadood were arrested

on the US charges of defrauding the investors (The Abraaj Group Scandal. 2019). Based on

the claim of US prosecutor it is said that the firm has been lying about the performance of the

company since 2014 and hence was rising the value by the more than ½ a billion dollars.

Along with that, charges also pinned the executives in regard to the misappropriation of the

million of dollars of the funds of its investors in the Madoffesque fashion.

The cause behind this scandal is that in 2018 there was an allegation on the firm that

amount in Abraaj’s health fund had been misused and both Naqvi and Abraaj denied to this

and blamed political and regulatory hurdles in regard to delay in the deployment of funds.

Among the investor, in the firm of Abraaj were the large number of US financial institutions,

pension and retirement funds, US government agency and the Bill and Melinda Gates

Foundation. This report provides an insight into the key risk involved in the case and how the

firm responded to its risk exposure. It also covers any gap or shortfall in the approach used by

the company covering key risk governance and regulatory risk. Both Naqvi and Abdel

provided its investors and the potential investors false performance metrics.

ASSESSMENT OF RISK

Assessment of risk is basically the term which is being used to describe the overall

process through the one can identify the risk. It involves various steps starting from

identifying the hazards and the risk factors which are having the potential to cause harm to

the analysing and evaluating the risk associated with that hazard which is simply called as the

risk analysis and evaluation. In order to effectively identify the risk and categorize the risk,

the Enterprise Risk Management Model (ERM) is being used which is based on the

international standards and practices. This framework incorporates the Moncler’s entire

organization along with the governance bodies each acting inside the scope of their individual

competence (Khan and Ali, 2017). In accordance with the field's rules and best acts of

reference, the primary goal of ERM is to guarantee the successful identification of proof,

estimation, the management, and observing of risks. This model incorporates all types of risk

which are having the potential to impact the functioning and of the business and thereby

affecting the accomplishment of the strategic objectives, impair organization resources, and

sabotage the estimation of the brand. ERM is joined into vital choices and key decision-

Abraaj which is a private equity firm based in Dubai, considered to be the most

influential emerging market after sixteen years of its operation having $14 bn in AUM. In the

year 2019, its founder Arif Naqvi and then executive Mustafa Abdel-Wadood were arrested

on the US charges of defrauding the investors (The Abraaj Group Scandal. 2019). Based on

the claim of US prosecutor it is said that the firm has been lying about the performance of the

company since 2014 and hence was rising the value by the more than ½ a billion dollars.

Along with that, charges also pinned the executives in regard to the misappropriation of the

million of dollars of the funds of its investors in the Madoffesque fashion.

The cause behind this scandal is that in 2018 there was an allegation on the firm that

amount in Abraaj’s health fund had been misused and both Naqvi and Abraaj denied to this

and blamed political and regulatory hurdles in regard to delay in the deployment of funds.

Among the investor, in the firm of Abraaj were the large number of US financial institutions,

pension and retirement funds, US government agency and the Bill and Melinda Gates

Foundation. This report provides an insight into the key risk involved in the case and how the

firm responded to its risk exposure. It also covers any gap or shortfall in the approach used by

the company covering key risk governance and regulatory risk. Both Naqvi and Abdel

provided its investors and the potential investors false performance metrics.

ASSESSMENT OF RISK

Assessment of risk is basically the term which is being used to describe the overall

process through the one can identify the risk. It involves various steps starting from

identifying the hazards and the risk factors which are having the potential to cause harm to

the analysing and evaluating the risk associated with that hazard which is simply called as the

risk analysis and evaluation. In order to effectively identify the risk and categorize the risk,

the Enterprise Risk Management Model (ERM) is being used which is based on the

international standards and practices. This framework incorporates the Moncler’s entire

organization along with the governance bodies each acting inside the scope of their individual

competence (Khan and Ali, 2017). In accordance with the field's rules and best acts of

reference, the primary goal of ERM is to guarantee the successful identification of proof,

estimation, the management, and observing of risks. This model incorporates all types of risk

which are having the potential to impact the functioning and of the business and thereby

affecting the accomplishment of the strategic objectives, impair organization resources, and

sabotage the estimation of the brand. ERM is joined into vital choices and key decision-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

making processes. The risk might be inward or outer relying upon whether they are

distinguished inside or outside the company. Specifically, external risks are connected to

industry and market circumstances as well as the stakeholder’s perception to it. In this model,

the risk is divided into 4 categories which are- strategic, business, compliance and financial

risk.

The main objective of this model is to identify the risk and segregate it into different

categories which makes it very easy for the business entity in effectively managing its risks

by undertaking specific prevention and controllable measures. These actions or the measures

can be implemented into the company processes in order to eliminate the risk along with

reducing the likelihood of occurrence of it again, and affecting the business performance. The

risk assessment recognizes all the threats and risks along with the risk owners, answerable for

dealing with the actual risk and the connected control framework, and for actualizing or

improving relief measures (Yang, Ishtiaq and Anwar, 2018). All the threats, the assessment

of the applicable internal control framework and related mitigation activities are recorded in a

Risks Register, which is upgraded consistently with risk owners, based on a yearly

arrangement affirmed by the Board of Directors with the help of the Control, Risks and

Sustainability Committee. The arrangement is occasionally updated to incorporate any new

components of danger as well as to reflect any rise in the probability of events or in the

degree of effects.

Therefore, based upon this framework, the risks pertaining to this case are stated

underneath.

Business risks: Abraaj firm failed to effectively follow the market in which it was

operating which has led to be lose control and reporting system. The company despite its

successful inception, the company started struggling as year on year the accounts of it

displayed a multimillion dollar losses. In addition to this, the revenue of the outweighed the

bloated costs and in order to reduce the gap the company borrowed funds (Saeidi and et.al.,

2019). In the year 2018, the financing cost reached to $41 mn. Two years back, the fir

attempted to divest assets which involves the $1.8 bn stake in Pakistani utility firm in order to

avoid the situation of cash crunch. All these losses were not disclosed and reported in the

financial reports of the company.

Compliance risks: The firm failed to comply with the financial reporting framework

and also used tactics in depicting better financial position and performance. For instance, the

company borrowed money just before the financial reporting dates with the purpose of

distinguished inside or outside the company. Specifically, external risks are connected to

industry and market circumstances as well as the stakeholder’s perception to it. In this model,

the risk is divided into 4 categories which are- strategic, business, compliance and financial

risk.

The main objective of this model is to identify the risk and segregate it into different

categories which makes it very easy for the business entity in effectively managing its risks

by undertaking specific prevention and controllable measures. These actions or the measures

can be implemented into the company processes in order to eliminate the risk along with

reducing the likelihood of occurrence of it again, and affecting the business performance. The

risk assessment recognizes all the threats and risks along with the risk owners, answerable for

dealing with the actual risk and the connected control framework, and for actualizing or

improving relief measures (Yang, Ishtiaq and Anwar, 2018). All the threats, the assessment

of the applicable internal control framework and related mitigation activities are recorded in a

Risks Register, which is upgraded consistently with risk owners, based on a yearly

arrangement affirmed by the Board of Directors with the help of the Control, Risks and

Sustainability Committee. The arrangement is occasionally updated to incorporate any new

components of danger as well as to reflect any rise in the probability of events or in the

degree of effects.

Therefore, based upon this framework, the risks pertaining to this case are stated

underneath.

Business risks: Abraaj firm failed to effectively follow the market in which it was

operating which has led to be lose control and reporting system. The company despite its

successful inception, the company started struggling as year on year the accounts of it

displayed a multimillion dollar losses. In addition to this, the revenue of the outweighed the

bloated costs and in order to reduce the gap the company borrowed funds (Saeidi and et.al.,

2019). In the year 2018, the financing cost reached to $41 mn. Two years back, the fir

attempted to divest assets which involves the $1.8 bn stake in Pakistani utility firm in order to

avoid the situation of cash crunch. All these losses were not disclosed and reported in the

financial reports of the company.

Compliance risks: The firm failed to comply with the financial reporting framework

and also used tactics in depicting better financial position and performance. For instance, the

company borrowed money just before the financial reporting dates with the purpose of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

producing temporarily inflated bank account balances. It also misappropriated money of more

than $250 mn from Abraaj.

Financial risks: Abraaj was dependent upon the multiple level of leverage which

led to highly unstable business model which is not common in private equity firm. After

analysing the documents, the investigators at PwC stated that Abraaj used loans to cover up

its operating expenses which consequently left it sensitive to the volatility and the potential

liquidity crisis.

RISK RESPONSE

Abraaj’s response to its risk exposure

After the exposure of the risk, Abraaj and Mr. Naqvi have stated that they have not

misused the money and there must be some sort of misunderstanding in regard to how the

funds are being operated. Along with this, they have said that there was delay in getting

approval from the relevant regulators in order to build the hospitals in Nigeria. In addition to

this, Pakistan has prevented Abraaj from deployment of funds more quickly. Also, in a

meeting in London, the investors saw that the financial statements show the cash of over

$200 mn and were unaware of the fact that the money has not been invested and asks the fund

manager to show in the bank statement where the money was deployed. Investors also

claimed that the Abraaj as supposed to return the money within 60 days as it was not utilized

in that time. Mr. Naqvi told the investors that the company is buying hospitals in across the

world which requires funds as cash in hand and along with that cited regulatory delays. But

then too, the investors were not convinced and in response to which Mr. Naqvi has to send

more than $100 million back to its investors.

Gaps and shortfalls in Abraaj’s approach

In order to effectively identify the shortfalls and the gaps in the approach being used

by the Abraaj, COSO Control Framework which is having an international recognition. This

model helps the Bard of Directors, management and other top-level personnel in effectively

setting up the strategies across the firm (Rae, Sands and Subramaniam, 2017). This is mainly

designed for identifying the events which are having the potential to affect the business entity

and this supports in managing the risk within its risk appetite. This helps in providing

assurance about the achievement of business objectives. The firm failed to understand and

effectively align its high-level goals with the mission which resulted into failure in effectively

carrying out the business activities. It also failed to comply with the applicable laws and

regulations and protect its organizational assets and maintaining the financial reporting.

than $250 mn from Abraaj.

Financial risks: Abraaj was dependent upon the multiple level of leverage which

led to highly unstable business model which is not common in private equity firm. After

analysing the documents, the investigators at PwC stated that Abraaj used loans to cover up

its operating expenses which consequently left it sensitive to the volatility and the potential

liquidity crisis.

RISK RESPONSE

Abraaj’s response to its risk exposure

After the exposure of the risk, Abraaj and Mr. Naqvi have stated that they have not

misused the money and there must be some sort of misunderstanding in regard to how the

funds are being operated. Along with this, they have said that there was delay in getting

approval from the relevant regulators in order to build the hospitals in Nigeria. In addition to

this, Pakistan has prevented Abraaj from deployment of funds more quickly. Also, in a

meeting in London, the investors saw that the financial statements show the cash of over

$200 mn and were unaware of the fact that the money has not been invested and asks the fund

manager to show in the bank statement where the money was deployed. Investors also

claimed that the Abraaj as supposed to return the money within 60 days as it was not utilized

in that time. Mr. Naqvi told the investors that the company is buying hospitals in across the

world which requires funds as cash in hand and along with that cited regulatory delays. But

then too, the investors were not convinced and in response to which Mr. Naqvi has to send

more than $100 million back to its investors.

Gaps and shortfalls in Abraaj’s approach

In order to effectively identify the shortfalls and the gaps in the approach being used

by the Abraaj, COSO Control Framework which is having an international recognition. This

model helps the Bard of Directors, management and other top-level personnel in effectively

setting up the strategies across the firm (Rae, Sands and Subramaniam, 2017). This is mainly

designed for identifying the events which are having the potential to affect the business entity

and this supports in managing the risk within its risk appetite. This helps in providing

assurance about the achievement of business objectives. The firm failed to understand and

effectively align its high-level goals with the mission which resulted into failure in effectively

carrying out the business activities. It also failed to comply with the applicable laws and

regulations and protect its organizational assets and maintaining the financial reporting.

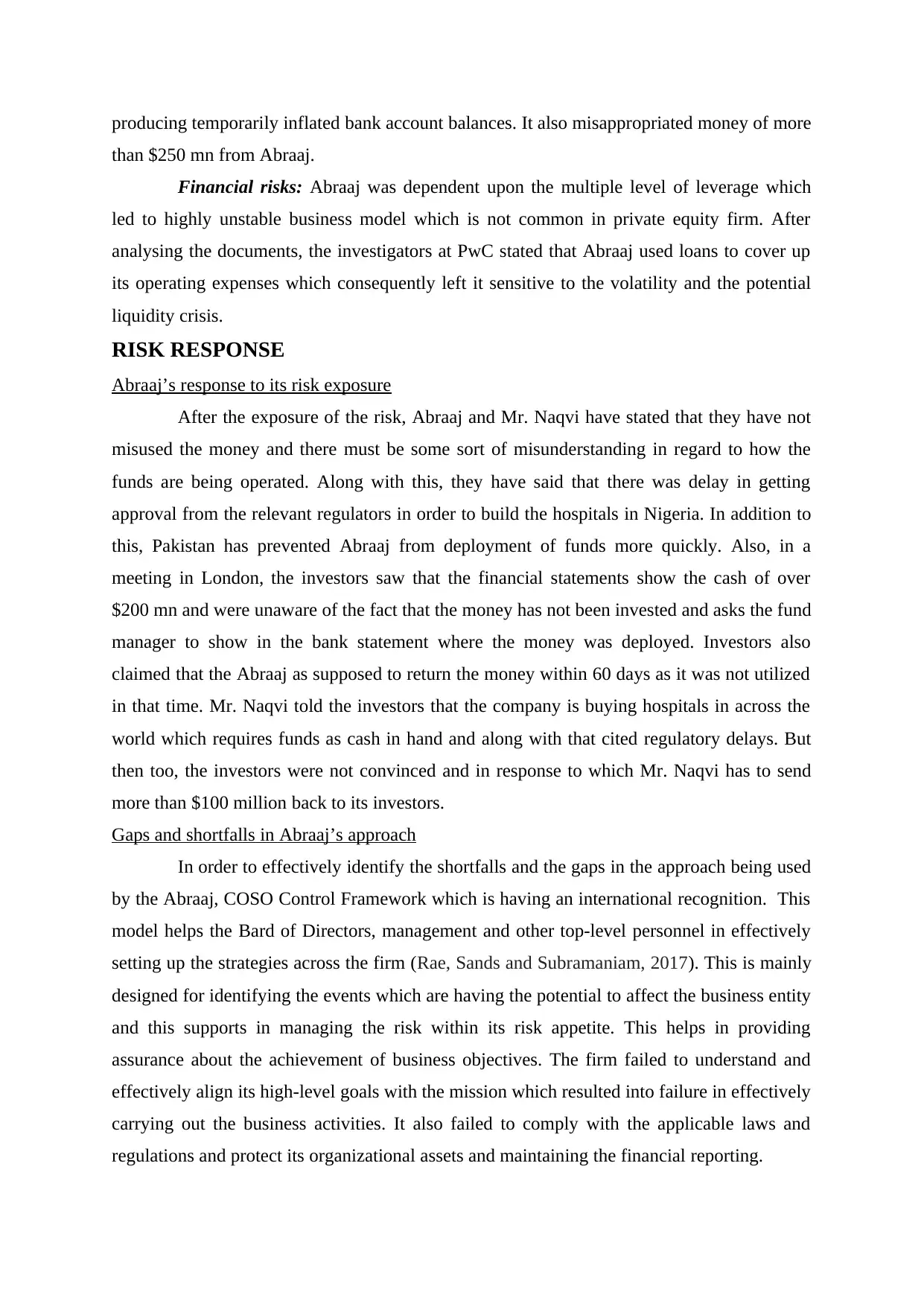

Figure 1 COSO's enterprise risk management framework. (Source: https://www.accaglobal.com/ie/en/student/exam-

support-resources/professional-exams-study-resources/strategic-business-leader/technical-articles/coso-enterprise-risk-

management-framework.html)

On the other side, the company was ineffective in analysing the industry and market

in which it is operating. In addition to this, the organization lacked behind identifying the

events and business activities which is having the potential to affect the business function

which resulted into increment in operating expenditure for the firm (Thabit, 2019). Proper

risk assessment was not done and also determining how an event can respond to the risk that

the company is facing which has resulted into affecting the financial instability of the firm.

Under the control activities, the firm was effective in implementing right set of practices and

policies pertaining to addressing the risk that the entity was exposed to. In the information

and communication, proper practices in regard to the communicating the right information to

the right people like the shareholders or the investors the right information about the financial

position of the company which is the major shortfall on the side of Abraaj. The firm was not

having proper evaluation system in order to ensure that the controls are functioning properly

so that corrective actions can be taken on time if required. All these components were needed

to considered at different levels of the organization instead of a single function or division.

Relevant aspects of risk governance and regulatory risk

It is of the perception that the BODs of Abraaj were unable to prevent the poor

governance which was led by the minority and also greater scrutiny was placed on the

independence of the directors.

support-resources/professional-exams-study-resources/strategic-business-leader/technical-articles/coso-enterprise-risk-

management-framework.html)

On the other side, the company was ineffective in analysing the industry and market

in which it is operating. In addition to this, the organization lacked behind identifying the

events and business activities which is having the potential to affect the business function

which resulted into increment in operating expenditure for the firm (Thabit, 2019). Proper

risk assessment was not done and also determining how an event can respond to the risk that

the company is facing which has resulted into affecting the financial instability of the firm.

Under the control activities, the firm was effective in implementing right set of practices and

policies pertaining to addressing the risk that the entity was exposed to. In the information

and communication, proper practices in regard to the communicating the right information to

the right people like the shareholders or the investors the right information about the financial

position of the company which is the major shortfall on the side of Abraaj. The firm was not

having proper evaluation system in order to ensure that the controls are functioning properly

so that corrective actions can be taken on time if required. All these components were needed

to considered at different levels of the organization instead of a single function or division.

Relevant aspects of risk governance and regulatory risk

It is of the perception that the BODs of Abraaj were unable to prevent the poor

governance which was led by the minority and also greater scrutiny was placed on the

independence of the directors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The Abraaj fallout showed various regulatory regimes which washed their hand

from the responsibility. Both the Dubai Financial Services Authority and the Cayman Islands

Monetary Authority rejected extreme administrative responsibility, referring to citing local

jurisdiction (Prewett and Terry, 2018). The Dubai regulator stated that it is only bore

responsibility for the fund manager headquartered there while the Cayman stated that locally

domiciled entities of the firm were not regulated as they are based on the Dubai HQ. This

makes it appear that the Abraaj have fallen from the gaps in the international regulatory

environment because of which for four years no regulator caught the financial misreporting.

CONCLUSION

It can be summarized from the above that the troubles of Abraaj is considered to be

one of the biggest private equity in the middle East, which occurred in 2018 as the dispute

arose with some of its investors in regard to the usage of the money pertaining to the $1 bn

healthcare fund. The investors involve the large corporates which accused the firm for

mishandling of the funds. Even after the exposure of the scandal, Abraaj was denying the

wrong doings but soon faced the solvency crisis as this scandal became the international

headlines. This scandal has into light the various loopholes in the existing system, regulatory

and compliance system which are required to reviewed again and changes should be

implemented. This scandal happened because Abraaj was able to effective make use of the

funds being collected for the Health care purpose. It lied about the projects and made use of

these funds in managing its operating expenses and highly valued to financial figures by more

than half a billion dollars. In connection to this, in 2019, Naqvi and Mustafa Abdel-Wadood

were arrested on the US charges in regard to the defrauding the investors. It was also found

out the firm making false claim about its financial performance for the last 4 years.

Therefore, in order to minimize such type of scandal it is important for the

regulators to regularly review the standards and regulations set in order to ensure that

everything is working properly. Through this way, it can effectively monitor the working or

the function of the businesses. Also, timely internal checks should be done in order to make

sure that things are going as per the regulation and there is no discrepancy in the financial

reporting as well. It is crucial to make sure that the organization is have implemented relevant

internal control and risk assessment system through which it can easily identify the potential

risk that may occur due to the business events and along with the same, it needs to understand

that proper evaluation of the same should be done for determining the level of its.

from the responsibility. Both the Dubai Financial Services Authority and the Cayman Islands

Monetary Authority rejected extreme administrative responsibility, referring to citing local

jurisdiction (Prewett and Terry, 2018). The Dubai regulator stated that it is only bore

responsibility for the fund manager headquartered there while the Cayman stated that locally

domiciled entities of the firm were not regulated as they are based on the Dubai HQ. This

makes it appear that the Abraaj have fallen from the gaps in the international regulatory

environment because of which for four years no regulator caught the financial misreporting.

CONCLUSION

It can be summarized from the above that the troubles of Abraaj is considered to be

one of the biggest private equity in the middle East, which occurred in 2018 as the dispute

arose with some of its investors in regard to the usage of the money pertaining to the $1 bn

healthcare fund. The investors involve the large corporates which accused the firm for

mishandling of the funds. Even after the exposure of the scandal, Abraaj was denying the

wrong doings but soon faced the solvency crisis as this scandal became the international

headlines. This scandal has into light the various loopholes in the existing system, regulatory

and compliance system which are required to reviewed again and changes should be

implemented. This scandal happened because Abraaj was able to effective make use of the

funds being collected for the Health care purpose. It lied about the projects and made use of

these funds in managing its operating expenses and highly valued to financial figures by more

than half a billion dollars. In connection to this, in 2019, Naqvi and Mustafa Abdel-Wadood

were arrested on the US charges in regard to the defrauding the investors. It was also found

out the firm making false claim about its financial performance for the last 4 years.

Therefore, in order to minimize such type of scandal it is important for the

regulators to regularly review the standards and regulations set in order to ensure that

everything is working properly. Through this way, it can effectively monitor the working or

the function of the businesses. Also, timely internal checks should be done in order to make

sure that things are going as per the regulation and there is no discrepancy in the financial

reporting as well. It is crucial to make sure that the organization is have implemented relevant

internal control and risk assessment system through which it can easily identify the potential

risk that may occur due to the business events and along with the same, it needs to understand

that proper evaluation of the same should be done for determining the level of its.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Khan, S. N. and Ali, E. I. E., 2017. The moderating role of intellectual capital between

enterprise risk management and firm performance: A conceptual review. American

Journal of Social Sciences and Humanities. 2(1). pp.9-15.

Prewett, K. and Terry, A., 2018. COSO's Updated Enterprise Risk Management Framework

—A Quest For Depth And Clarity. Journal of Corporate Accounting &

Finance. 29(3). pp.16-23.

Rae, K., Sands, J. and Subramaniam, N., 2017. Associations among the five components

within COSO internal control-integrated framework as the underpinning of quality

corporate governance. Australasian Accounting, Business and Finance

Journal. 11(1). pp.28-54.

Saeidi, P. and et.al., 2019. The impact of enterprise risk management on competitive

advantage by moderating role of information technology. Computer Standards &

Interfaces. 63. pp.67-82.

Thabit, T., 2019, April. Determining the effectiveness of internal controls in enterprise risk

management based on COSO recommendations. In International Conference on

Accounting, Business Economics and Politics.

Yang, S., Ishtiaq, M. and Anwar, M., 2018. Enterprise risk management practices and firm

performance, the mediating role of competitive advantage and the moderating role of

financial literacy. Journal of Risk and Financial Management. 11(3). p.35.

Online

Abraaj scandal: the world's largest private equity insolvency. 2020. [Online]. Available

Through:< https://www.arabianbusiness.com/video/448252-video-uaes-abraaj-

scandal-the-worlds-largest-private-equity-insolvency#:~:text=The%20Dubai

%20Financial%20Services%20Authority,deceiving%20investors%20and

%20misappropriating%20funds.&text=Abraaj%20had%20borrowed%20to

%20fill,creditors%20more%20than%20%241%20billion. >.

The Abraaj Group Scandal. 2019. [Online]. Available Through:<

https://bspeclub.com/2019/11/19/the-abraaj-group-scandal/ >.

Books and Journals

Khan, S. N. and Ali, E. I. E., 2017. The moderating role of intellectual capital between

enterprise risk management and firm performance: A conceptual review. American

Journal of Social Sciences and Humanities. 2(1). pp.9-15.

Prewett, K. and Terry, A., 2018. COSO's Updated Enterprise Risk Management Framework

—A Quest For Depth And Clarity. Journal of Corporate Accounting &

Finance. 29(3). pp.16-23.

Rae, K., Sands, J. and Subramaniam, N., 2017. Associations among the five components

within COSO internal control-integrated framework as the underpinning of quality

corporate governance. Australasian Accounting, Business and Finance

Journal. 11(1). pp.28-54.

Saeidi, P. and et.al., 2019. The impact of enterprise risk management on competitive

advantage by moderating role of information technology. Computer Standards &

Interfaces. 63. pp.67-82.

Thabit, T., 2019, April. Determining the effectiveness of internal controls in enterprise risk

management based on COSO recommendations. In International Conference on

Accounting, Business Economics and Politics.

Yang, S., Ishtiaq, M. and Anwar, M., 2018. Enterprise risk management practices and firm

performance, the mediating role of competitive advantage and the moderating role of

financial literacy. Journal of Risk and Financial Management. 11(3). p.35.

Online

Abraaj scandal: the world's largest private equity insolvency. 2020. [Online]. Available

Through:< https://www.arabianbusiness.com/video/448252-video-uaes-abraaj-

scandal-the-worlds-largest-private-equity-insolvency#:~:text=The%20Dubai

%20Financial%20Services%20Authority,deceiving%20investors%20and

%20misappropriating%20funds.&text=Abraaj%20had%20borrowed%20to

%20fill,creditors%20more%20than%20%241%20billion. >.

The Abraaj Group Scandal. 2019. [Online]. Available Through:<

https://bspeclub.com/2019/11/19/the-abraaj-group-scandal/ >.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.