12 Months' Cash Budget Forecast for Dysonica Plc up to 30 April 2023

VerifiedAdded on 2023/06/11

|14

|4288

|281

AI Summary

This report provides a 12 months' cash budget forecast for Dysonica Plc up to 30 April 2023, including starting cash balance, cash inflows, cash outflows, net cash flow, and ending cash balance for each month. The cash budget forecast is formulated by estimating the cash inflows and outflows for each month and calculating the net cash flow and ending cash balance. The report recommends the use of activity-based costing or marginal costing to control costs involved in the creation of a product.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Business Finance

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Elaborate the cost incurred and the nature of the business.....................................................3

TASK 2............................................................................................................................................7

Suggest on the cost reduction strategy of the Business concern............................................7

TASK 3............................................................................................................................................8

Formulate a 12 months’ cash budget forecast for the business up to 30April 2023..............8

TASK 4..........................................................................................................................................10

Evaluate the forecast and budget of the Dysonica................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

2

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Elaborate the cost incurred and the nature of the business.....................................................3

TASK 2............................................................................................................................................7

Suggest on the cost reduction strategy of the Business concern............................................7

TASK 3............................................................................................................................................8

Formulate a 12 months’ cash budget forecast for the business up to 30April 2023..............8

TASK 4..........................................................................................................................................10

Evaluate the forecast and budget of the Dysonica................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

2

INTRODUCTION

Finance is required for the firm's activities to run smoothly. It is used by a variety of

businesses to help them obtain finance from numerous sources. It is utilised to get raw materials,

assets, and products for the company. A firm that starts with a little amount of money will

constantly require additional finances to carry out its operations. Finance is the bedrock of any

business. It's practically impossible to thrive without a solid financial foundation. The finances

and credit used in a firm are referred to as business finance. Any business relies on monetary

backing. Finance is anticipated to acquire property, products, regular assets, and other business-

related assets. A solid financial management system aids in meeting a company's potential and

financial demands. The case of Dysonica Plc is highlighted in the following report. The report is

broken into four sections, the first of which outlines how the company uses various cost types

such as variable, semi-variable, and fixed costs. It also mentions absorption, marginal costing,

and activity-based costing. The second role is making recommendations to the firm in terms of

cost effectiveness and business operations. The third section is about the company's cash flow

estimate for the fiscal year ending 30 April 2023. Task four describes how the industry works

through assisting company operations through the use of predictions (Alabdullah, 2022).

MAIN BODY

Elaborate the cost incurred and the nature of the business.

Cost refers to any expense made by a company in order to produce or manufacture goods

and services. It is the money spent on selling and acquiring a firm. The firm must incur both

fixed and variable costs in order to make items.

The firm's output, which is created by the firm, determines variable cost. It is possible

that as a result of this, a rise in production leads to an increase in variable costs. It comprises

commissions, raw materials, utility bills, and labour, all of which contribute to an increase in the

firm's variable cost.

Fixed costs are a responsibility that will be included in the firm's expenses regardless of the

firm's size. Property tax, rent, depreciation, and insurance are all costs spent by the corporation

during the production process.

A semi variable cost is a cost that is a combination of variable and fixed costs. These costs are

set at a certain level of output and thereafter vary depending on the amount of production. When

3

Finance is required for the firm's activities to run smoothly. It is used by a variety of

businesses to help them obtain finance from numerous sources. It is utilised to get raw materials,

assets, and products for the company. A firm that starts with a little amount of money will

constantly require additional finances to carry out its operations. Finance is the bedrock of any

business. It's practically impossible to thrive without a solid financial foundation. The finances

and credit used in a firm are referred to as business finance. Any business relies on monetary

backing. Finance is anticipated to acquire property, products, regular assets, and other business-

related assets. A solid financial management system aids in meeting a company's potential and

financial demands. The case of Dysonica Plc is highlighted in the following report. The report is

broken into four sections, the first of which outlines how the company uses various cost types

such as variable, semi-variable, and fixed costs. It also mentions absorption, marginal costing,

and activity-based costing. The second role is making recommendations to the firm in terms of

cost effectiveness and business operations. The third section is about the company's cash flow

estimate for the fiscal year ending 30 April 2023. Task four describes how the industry works

through assisting company operations through the use of predictions (Alabdullah, 2022).

MAIN BODY

Elaborate the cost incurred and the nature of the business.

Cost refers to any expense made by a company in order to produce or manufacture goods

and services. It is the money spent on selling and acquiring a firm. The firm must incur both

fixed and variable costs in order to make items.

The firm's output, which is created by the firm, determines variable cost. It is possible

that as a result of this, a rise in production leads to an increase in variable costs. It comprises

commissions, raw materials, utility bills, and labour, all of which contribute to an increase in the

firm's variable cost.

Fixed costs are a responsibility that will be included in the firm's expenses regardless of the

firm's size. Property tax, rent, depreciation, and insurance are all costs spent by the corporation

during the production process.

A semi variable cost is a cost that is a combination of variable and fixed costs. These costs are

set at a certain level of output and thereafter vary depending on the amount of production. When

3

no units are produced, a fixed sum is charged, which is referred to as fixed cost (Alakaleek and

Cooper, 2018).

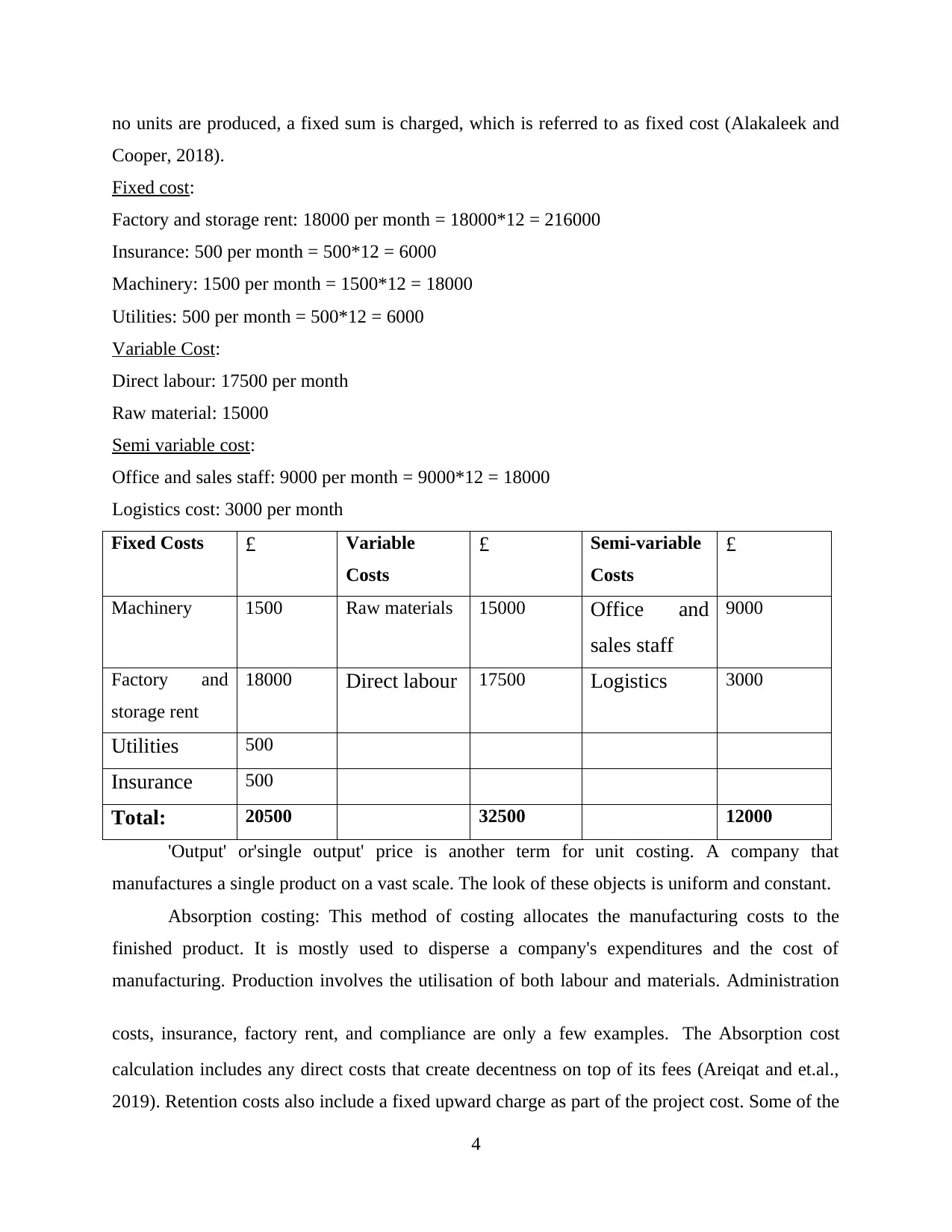

Fixed cost:

Factory and storage rent: 18000 per month = 18000*12 = 216000

Insurance: 500 per month = 500*12 = 6000

Machinery: 1500 per month = 1500*12 = 18000

Utilities: 500 per month = 500*12 = 6000

Variable Cost:

Direct labour: 17500 per month

Raw material: 15000

Semi variable cost:

Office and sales staff: 9000 per month = 9000*12 = 18000

Logistics cost: 3000 per month

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

'Output' or'single output' price is another term for unit costing. A company that

manufactures a single product on a vast scale. The look of these objects is uniform and constant.

Absorption costing: This method of costing allocates the manufacturing costs to the

finished product. It is mostly used to disperse a company's expenditures and the cost of

manufacturing. Production involves the utilisation of both labour and materials. Administration

costs, insurance, factory rent, and compliance are only a few examples. The Absorption cost

calculation includes any direct costs that create decentness on top of its fees (Areiqat and et.al.,

2019). Retention costs also include a fixed upward charge as part of the project cost. Some of the

4

Cooper, 2018).

Fixed cost:

Factory and storage rent: 18000 per month = 18000*12 = 216000

Insurance: 500 per month = 500*12 = 6000

Machinery: 1500 per month = 1500*12 = 18000

Utilities: 500 per month = 500*12 = 6000

Variable Cost:

Direct labour: 17500 per month

Raw material: 15000

Semi variable cost:

Office and sales staff: 9000 per month = 9000*12 = 18000

Logistics cost: 3000 per month

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

'Output' or'single output' price is another term for unit costing. A company that

manufactures a single product on a vast scale. The look of these objects is uniform and constant.

Absorption costing: This method of costing allocates the manufacturing costs to the

finished product. It is mostly used to disperse a company's expenditures and the cost of

manufacturing. Production involves the utilisation of both labour and materials. Administration

costs, insurance, factory rent, and compliance are only a few examples. The Absorption cost

calculation includes any direct costs that create decentness on top of its fees (Areiqat and et.al.,

2019). Retention costs also include a fixed upward charge as part of the project cost. Some of the

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

costs associated with assembling an item include the salary of the representative who actually cut

the item, the natural substances used to create the item, and all ongoing upwards costs (like per-

utility charges). Taking into account the cost associated with this inventory is related to the full

expense of the inventory that is still nearby, the ingestion costing guarantees a more accurate

representation of finished goods inventory. Additionally, more of the cost is reflected in unsold

items, which reduces the true cost detailed in the duration frame in the salary announcement.

This results in higher total compensation calculation comparisons and variable cost estimates.

(Direct material cost – Direct labour cost + Variable manufacturing overhead cost +

Fixed manufacturing overhead) / Number of units produced = absorption costing

The absorption cost formula indicates that in order to estimate the product's margin, the

firm must contribute per unit, which aids in finding the break-even analysis of the company's

sales. The break-even point is the point at which the company's revenues equal the cost of

producing the same number of units. Because a rise in production of an extra unit does not

contribute to the increased fixed cost, absorption costing conforms with GAAP laws and

regulations, resulting in a gain in profit (Bai, C. and et.al., 2021). It's a method of valuing

inventories using expenditure accounting. Every cost of constructing an item, both fixed and

variable, is included or "absorbed" in absorption cost estimates. This implies that all expenses are

remembered as inventory costs, including immediate, similar to material charges, and

roundabout, similar to upward charges. Variable costing methodologies do not offer a

comprehensive and accurate picture of the real cost of delivering items.

For Example:

Assume that ABC is a computer manufacturer. The information provided is about the production

process. The absorption costing method is used to determine profits.

The total number of units made was 10,000, of which 9000 were sold. The selling price for each

device is $50.

Direct labour cost = $5 direct material is $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing:

Marginal costing is a method of assigning factor creation to production units. It is

5

the item, the natural substances used to create the item, and all ongoing upwards costs (like per-

utility charges). Taking into account the cost associated with this inventory is related to the full

expense of the inventory that is still nearby, the ingestion costing guarantees a more accurate

representation of finished goods inventory. Additionally, more of the cost is reflected in unsold

items, which reduces the true cost detailed in the duration frame in the salary announcement.

This results in higher total compensation calculation comparisons and variable cost estimates.

(Direct material cost – Direct labour cost + Variable manufacturing overhead cost +

Fixed manufacturing overhead) / Number of units produced = absorption costing

The absorption cost formula indicates that in order to estimate the product's margin, the

firm must contribute per unit, which aids in finding the break-even analysis of the company's

sales. The break-even point is the point at which the company's revenues equal the cost of

producing the same number of units. Because a rise in production of an extra unit does not

contribute to the increased fixed cost, absorption costing conforms with GAAP laws and

regulations, resulting in a gain in profit (Bai, C. and et.al., 2021). It's a method of valuing

inventories using expenditure accounting. Every cost of constructing an item, both fixed and

variable, is included or "absorbed" in absorption cost estimates. This implies that all expenses are

remembered as inventory costs, including immediate, similar to material charges, and

roundabout, similar to upward charges. Variable costing methodologies do not offer a

comprehensive and accurate picture of the real cost of delivering items.

For Example:

Assume that ABC is a computer manufacturer. The information provided is about the production

process. The absorption costing method is used to determine profits.

The total number of units made was 10,000, of which 9000 were sold. The selling price for each

device is $50.

Direct labour cost = $5 direct material is $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing:

Marginal costing is a method of assigning factor creation to production units. It is

5

characterized by an adjustment to the amount due to the additional costs that come with it. It

takes into account variable and fixed costs. Fixed costs remain consistent with little focus on

creation. Variable fees vary with the number of units created. Variable creative costs include

direct materials, direct hardware, and direct work. Only a few overhead costs can be considered

factor costs. "Determining insignificant expenses and the effect of adjustment amounts or results

on revenue by separating fixed and variable expenses" is a characteristic of peripheral costing.

The idea of optional costing depends on how the fee varies with the degree of creation

(Beaumont, 2019). In semi-variable costing, costs are divided into fixed costs and variable costs.

The minimum cost of creation is an adjustment to the full cost of creation from the manufacture

or delivery of an additional unit. To calculate the minimum fee, divide the adjustment for the

cost of creation by the adjustment for the amount. The motivation behind factoring negligible

fees is to determine when an association can achieve economies of scale to escalate creation and

general tasks. If the small fee for delivering an additional unit is less than the value per unit, the

manufacturer may gain.

In practice, even semi-variable costs are divided into fixed and variable costs. Both work

in progress and finished goods are considered minimum prices. Since expanding a variable-shape

unit would result in an expansion of the component cost within the current creation limits, the

cost to some extent is actually the same as the development of the entire element cost. Fixed

costs remain unchanged. In this approach, component-only costs are considered appropriate risk

costs, while decent expenses are considered period costs that will be remembered as ongoing

revenue. Commitments are revenue from countless exchanges that outperform variable fees.

Change in cost / Change in Quantity = Marginal cost

The change in cost is a result of the change in production level. Regardless of the quantity of

units produced, fixed will stay the same.

Assume that XYZ is a company that produces bottles. The following information is supplied

about its production facilities.

10,000 units produced in the first month 2: 15,000 Units Produced Month 1 Variable Costs =

$50,000 Month 2 Variable Costs = $ 80,000

Changes in price and quantity Equals Marginal Cost = Marginal Cost (80,000 – 50,000)/ (15,000

– 10,000)

As a result, the per-unit marginal cost is $ 6 (30,000/5,000).

6

takes into account variable and fixed costs. Fixed costs remain consistent with little focus on

creation. Variable fees vary with the number of units created. Variable creative costs include

direct materials, direct hardware, and direct work. Only a few overhead costs can be considered

factor costs. "Determining insignificant expenses and the effect of adjustment amounts or results

on revenue by separating fixed and variable expenses" is a characteristic of peripheral costing.

The idea of optional costing depends on how the fee varies with the degree of creation

(Beaumont, 2019). In semi-variable costing, costs are divided into fixed costs and variable costs.

The minimum cost of creation is an adjustment to the full cost of creation from the manufacture

or delivery of an additional unit. To calculate the minimum fee, divide the adjustment for the

cost of creation by the adjustment for the amount. The motivation behind factoring negligible

fees is to determine when an association can achieve economies of scale to escalate creation and

general tasks. If the small fee for delivering an additional unit is less than the value per unit, the

manufacturer may gain.

In practice, even semi-variable costs are divided into fixed and variable costs. Both work

in progress and finished goods are considered minimum prices. Since expanding a variable-shape

unit would result in an expansion of the component cost within the current creation limits, the

cost to some extent is actually the same as the development of the entire element cost. Fixed

costs remain unchanged. In this approach, component-only costs are considered appropriate risk

costs, while decent expenses are considered period costs that will be remembered as ongoing

revenue. Commitments are revenue from countless exchanges that outperform variable fees.

Change in cost / Change in Quantity = Marginal cost

The change in cost is a result of the change in production level. Regardless of the quantity of

units produced, fixed will stay the same.

Assume that XYZ is a company that produces bottles. The following information is supplied

about its production facilities.

10,000 units produced in the first month 2: 15,000 Units Produced Month 1 Variable Costs =

$50,000 Month 2 Variable Costs = $ 80,000

Changes in price and quantity Equals Marginal Cost = Marginal Cost (80,000 – 50,000)/ (15,000

– 10,000)

As a result, the per-unit marginal cost is $ 6 (30,000/5,000).

6

Activity-based costing:

The cost of creating goods and services may be determined using activity-based costing.

This strategy yields precise product or service pricing. It assists managers in determining

overheads and cost drivers, which are used to emphasise the product's cost and value addition, as

well as removing undesirable or unneeded expenditures incurred during manufacturing. It assists

in estimating the effective cost and overhead cost in order to lower the product's per-unit cost. It

is a costing approach that aids in determining the cost and assigning it to the defined basis

(Borgogno and Colangelo, 2020).

This approach aids in assessing the process's worth and relevance in the manufacturing

process. As a result, the items are categorised based on their worth. In three ways, it aids in the

costing process improvement. The goods with the highest value and lowest share are evaluated in

the ABC costing's A list. The product with a lower value than the second requirement is listed in

the 'B' section. In the third section, persons whose worth is low but who are many are evaluated.

TASK 2

Suggest on the cost reduction strategy of the Business concern.

Based on the outcomes of using the aforementioned techniques, they have established that

they should compute expenditures utilising the activity-based costing methodology. The key

reason for choosing this technique is that it evaluates and distributes charges to each department

within the organisation based on the defined drivers. ABC costing will aid them in enabling cost

in each of their business operations, and they will be able to rapidly discover which departments

are cost-beneficial to them and which departments are incurring higher expenses, allowing them

to maintain costs within an acceptable range. The main advantage of ABC costing is that instead

of allocating expenditures to operational departments, it separates them into job activities. It

helps the firm reduce the overall cost of the finished product by allowing it to identify a

reasonable selling price for the product that is not onerous to the customer. As a result of the

above discussions, Dysonica Plc is encouraged to use activity-based costing in their business so

that product costs may be reduced correspondingly (Carè, Trotta and Rizzello, 2018).

From the numerous costing strategies, Dysonica Plc recommends activity based costing or

marginal costing since it aids in identifying how firms control their costs involved in the creation

of a product. This allows businesses to segment expenses depending on their systems and

7

The cost of creating goods and services may be determined using activity-based costing.

This strategy yields precise product or service pricing. It assists managers in determining

overheads and cost drivers, which are used to emphasise the product's cost and value addition, as

well as removing undesirable or unneeded expenditures incurred during manufacturing. It assists

in estimating the effective cost and overhead cost in order to lower the product's per-unit cost. It

is a costing approach that aids in determining the cost and assigning it to the defined basis

(Borgogno and Colangelo, 2020).

This approach aids in assessing the process's worth and relevance in the manufacturing

process. As a result, the items are categorised based on their worth. In three ways, it aids in the

costing process improvement. The goods with the highest value and lowest share are evaluated in

the ABC costing's A list. The product with a lower value than the second requirement is listed in

the 'B' section. In the third section, persons whose worth is low but who are many are evaluated.

TASK 2

Suggest on the cost reduction strategy of the Business concern.

Based on the outcomes of using the aforementioned techniques, they have established that

they should compute expenditures utilising the activity-based costing methodology. The key

reason for choosing this technique is that it evaluates and distributes charges to each department

within the organisation based on the defined drivers. ABC costing will aid them in enabling cost

in each of their business operations, and they will be able to rapidly discover which departments

are cost-beneficial to them and which departments are incurring higher expenses, allowing them

to maintain costs within an acceptable range. The main advantage of ABC costing is that instead

of allocating expenditures to operational departments, it separates them into job activities. It

helps the firm reduce the overall cost of the finished product by allowing it to identify a

reasonable selling price for the product that is not onerous to the customer. As a result of the

above discussions, Dysonica Plc is encouraged to use activity-based costing in their business so

that product costs may be reduced correspondingly (Carè, Trotta and Rizzello, 2018).

From the numerous costing strategies, Dysonica Plc recommends activity based costing or

marginal costing since it aids in identifying how firms control their costs involved in the creation

of a product. This allows businesses to segment expenses depending on their systems and

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

determine which one is the most expensive, helping them to cut costs and improve operations in

the same way. Organizations may use action-based costing as a one-stop shop for cost reduction.

It enables businesses to track expenditures as they arise rather than combining them with other

expenses. As a result, the true source of cost is misunderstood, and the association may

concentrate on proper control of specific expense categories rather than other business drivers.

Because upside consumption is categorised and arranged according to the number of activities,

the dispersion of upside expenses is more targeted and exact. ABC groups expenses by job rather

than aggregating all costs again to provide roundabout measurements of association costs, which

makes things easier. It aids in the separation of costs according to the varied values assigned to

different departments. It also aids management in lowering costs in order to make the product

more accessible to the general population. Activity-based costing offers a foundation for

lowering the firm's product costs. It also aids in identifying the company's true manufacturing

costs. It also aids in the management of costs incurred throughout the product's manufacturing

process. Overhead costs are pooled and controlled at the department where they need to be split.

It must be correctly accessible and handled in accordance with the project's costs. The ABC

technique aids activities in distinct groups based on their value and contribution to the

manufacturing process. The ABC costing approach may also be used to track depreciation. It has

the potential to cut both the cost and the volume of the product. Individual errands are now able

to identify previously unidentified consumptions, such as depreciation, thanks to movement-

based bookkeeping. The ABC method can lower the unit cost of low-volume goods by shifting

management attention from higher-priced goods to lower-priced goods (Chen and et.al., 2020).

TASK 3

Formulate a 12 months’ cash budget forecast for the business up to 30April 2023.

A cash flow statement is a financial statement that shows the sources of funds and where

they are utilised. It is divided into three categories: operational operations, financing activities,

and financing activities. A cash flow statement shows how the company's finances are doing.

These statements are used by businesses to determine the amount of money they have earned,

applied, and received from various sources.

Non-cash expenses are not included in the cash flow statement and are adjusted in the

income statement and balance sheet.

8

the same way. Organizations may use action-based costing as a one-stop shop for cost reduction.

It enables businesses to track expenditures as they arise rather than combining them with other

expenses. As a result, the true source of cost is misunderstood, and the association may

concentrate on proper control of specific expense categories rather than other business drivers.

Because upside consumption is categorised and arranged according to the number of activities,

the dispersion of upside expenses is more targeted and exact. ABC groups expenses by job rather

than aggregating all costs again to provide roundabout measurements of association costs, which

makes things easier. It aids in the separation of costs according to the varied values assigned to

different departments. It also aids management in lowering costs in order to make the product

more accessible to the general population. Activity-based costing offers a foundation for

lowering the firm's product costs. It also aids in identifying the company's true manufacturing

costs. It also aids in the management of costs incurred throughout the product's manufacturing

process. Overhead costs are pooled and controlled at the department where they need to be split.

It must be correctly accessible and handled in accordance with the project's costs. The ABC

technique aids activities in distinct groups based on their value and contribution to the

manufacturing process. The ABC costing approach may also be used to track depreciation. It has

the potential to cut both the cost and the volume of the product. Individual errands are now able

to identify previously unidentified consumptions, such as depreciation, thanks to movement-

based bookkeeping. The ABC method can lower the unit cost of low-volume goods by shifting

management attention from higher-priced goods to lower-priced goods (Chen and et.al., 2020).

TASK 3

Formulate a 12 months’ cash budget forecast for the business up to 30April 2023.

A cash flow statement is a financial statement that shows the sources of funds and where

they are utilised. It is divided into three categories: operational operations, financing activities,

and financing activities. A cash flow statement shows how the company's finances are doing.

These statements are used by businesses to determine the amount of money they have earned,

applied, and received from various sources.

Non-cash expenses are not included in the cash flow statement and are adjusted in the

income statement and balance sheet.

8

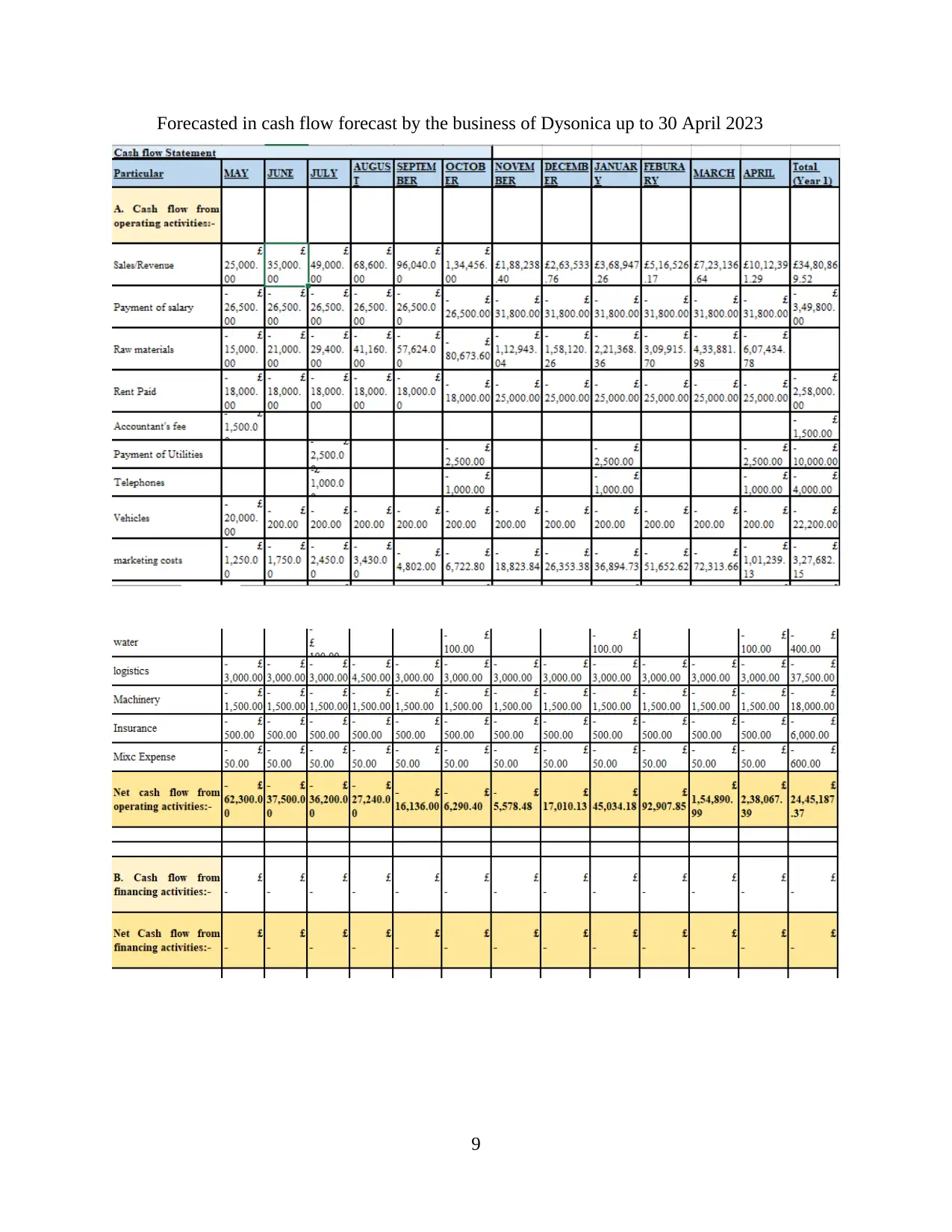

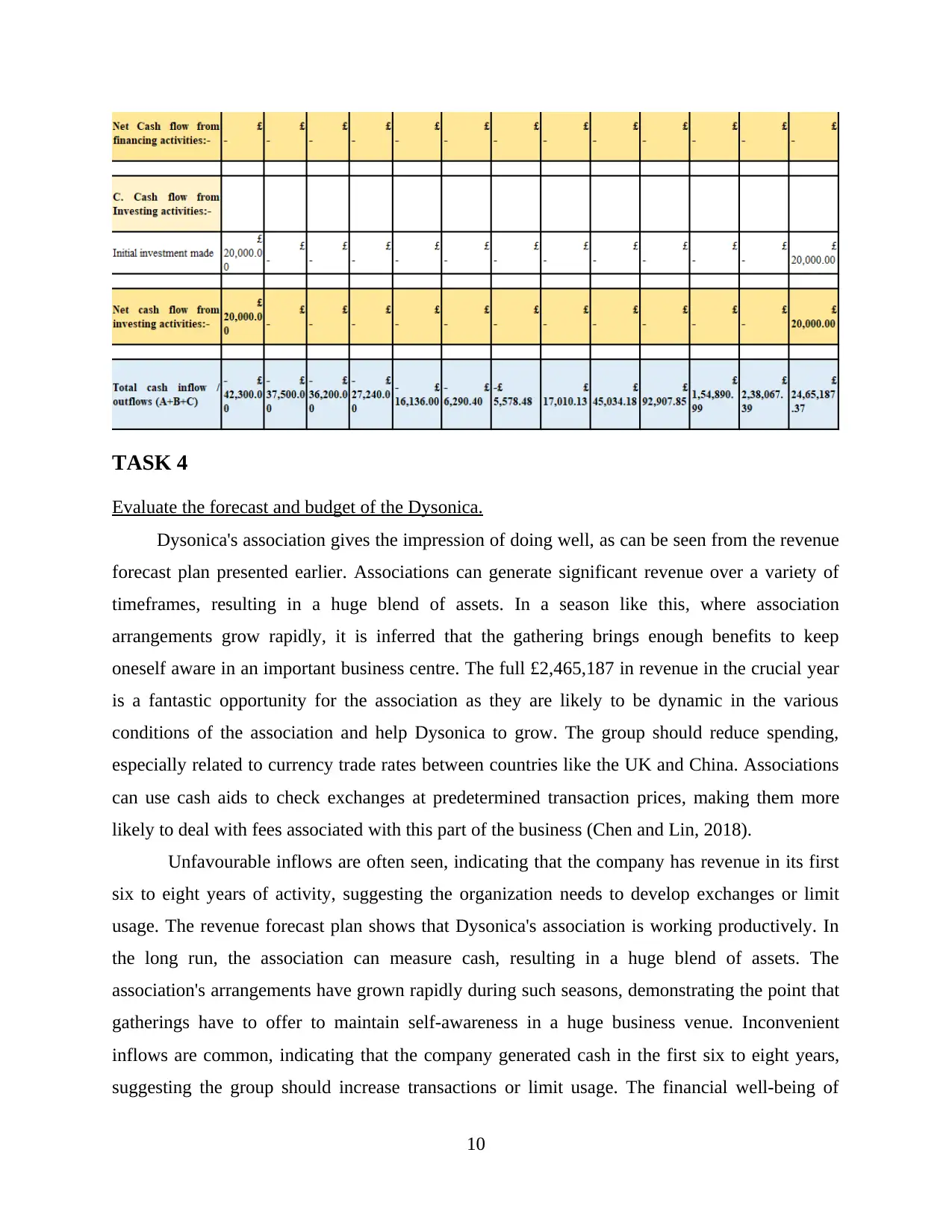

Forecasted in cash flow forecast by the business of Dysonica up to 30 April 2023

9

9

TASK 4

Evaluate the forecast and budget of the Dysonica.

Dysonica's association gives the impression of doing well, as can be seen from the revenue

forecast plan presented earlier. Associations can generate significant revenue over a variety of

timeframes, resulting in a huge blend of assets. In a season like this, where association

arrangements grow rapidly, it is inferred that the gathering brings enough benefits to keep

oneself aware in an important business centre. The full £2,465,187 in revenue in the crucial year

is a fantastic opportunity for the association as they are likely to be dynamic in the various

conditions of the association and help Dysonica to grow. The group should reduce spending,

especially related to currency trade rates between countries like the UK and China. Associations

can use cash aids to check exchanges at predetermined transaction prices, making them more

likely to deal with fees associated with this part of the business (Chen and Lin, 2018).

Unfavourable inflows are often seen, indicating that the company has revenue in its first

six to eight years of activity, suggesting the organization needs to develop exchanges or limit

usage. The revenue forecast plan shows that Dysonica's association is working productively. In

the long run, the association can measure cash, resulting in a huge blend of assets. The

association's arrangements have grown rapidly during such seasons, demonstrating the point that

gatherings have to offer to maintain self-awareness in a huge business venue. Inconvenient

inflows are common, indicating that the company generated cash in the first six to eight years,

suggesting the group should increase transactions or limit usage. The financial well-being of

10

Evaluate the forecast and budget of the Dysonica.

Dysonica's association gives the impression of doing well, as can be seen from the revenue

forecast plan presented earlier. Associations can generate significant revenue over a variety of

timeframes, resulting in a huge blend of assets. In a season like this, where association

arrangements grow rapidly, it is inferred that the gathering brings enough benefits to keep

oneself aware in an important business centre. The full £2,465,187 in revenue in the crucial year

is a fantastic opportunity for the association as they are likely to be dynamic in the various

conditions of the association and help Dysonica to grow. The group should reduce spending,

especially related to currency trade rates between countries like the UK and China. Associations

can use cash aids to check exchanges at predetermined transaction prices, making them more

likely to deal with fees associated with this part of the business (Chen and Lin, 2018).

Unfavourable inflows are often seen, indicating that the company has revenue in its first

six to eight years of activity, suggesting the organization needs to develop exchanges or limit

usage. The revenue forecast plan shows that Dysonica's association is working productively. In

the long run, the association can measure cash, resulting in a huge blend of assets. The

association's arrangements have grown rapidly during such seasons, demonstrating the point that

gatherings have to offer to maintain self-awareness in a huge business venue. Inconvenient

inflows are common, indicating that the company generated cash in the first six to eight years,

suggesting the group should increase transactions or limit usage. The financial well-being of

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

companies is influenced by theoretical constant development, and each association is expected to

thrive in the intricate world of finance and around the world. Selective stock affiliates can help

keep costs down by distinguishing which drives are to blame and spending the association's cash.

They should do practical exercises at a consistent pace to keep up with huge utilitarian profits

over a longer period of time. Indisputably, the main portion of income from work activity for an

accounting period shows a bargain starting in May and ending in April, increasing over time (Dai

and Zhang, 2019).

The association's regular pay announcements reflect an important area of stable currency

conditions. Dysonica can meet its interim commitments without difficulty, and it has sufficient

liquid assets to cover its drawn-down liabilities. Also, a marketable strategy should be visible,

showing that the organization is really doing integrity in selling its items and administration and

generating a lot of benefits from exchange income. A full infusion of £2,465,187 for the current

year is a fantastic opportunity for organizations as it allows them to take an interest in Dysonica's

range of situations and assist with the company's expansion. The association's regular

remuneration announcements reflect an important area of stable monetary conditions. Dysonica

can meet its medium-term commitments without difficulty, and it has sufficient liquid assets to

cover its drawn liabilities. In addition, a marketable strategy should be visible, showing that the

organization is really honest in selling its items and management, and generating a lot of benefits

from exchange income. This year's full capital injection of £2,465,187 is an excellent

opportunity for organizations as it enables them to take an interest in Dysonica's various

situations and assist with the company's expansion (Elkhal, 2019).

The organization's finances have been affected by a recurring uptick in venture capital,

which is critical for any association to win in the deep business world and around the world.

Costs can be reduced by taking advantage of optional inventory associations and finding out

which drives are failing and which are draining the organization's cash (Farooq and Selim,

2019).

CONCLUSION

The organisation of money and the arrangement of these dollars, according to the report

given above, is a vital and crucial aspect in the organisation of exhibits. Organizations like

Dysonica, which operate on a worldwide basis, have faced severe competition. They should

11

thrive in the intricate world of finance and around the world. Selective stock affiliates can help

keep costs down by distinguishing which drives are to blame and spending the association's cash.

They should do practical exercises at a consistent pace to keep up with huge utilitarian profits

over a longer period of time. Indisputably, the main portion of income from work activity for an

accounting period shows a bargain starting in May and ending in April, increasing over time (Dai

and Zhang, 2019).

The association's regular pay announcements reflect an important area of stable currency

conditions. Dysonica can meet its interim commitments without difficulty, and it has sufficient

liquid assets to cover its drawn-down liabilities. Also, a marketable strategy should be visible,

showing that the organization is really doing integrity in selling its items and administration and

generating a lot of benefits from exchange income. A full infusion of £2,465,187 for the current

year is a fantastic opportunity for organizations as it allows them to take an interest in Dysonica's

range of situations and assist with the company's expansion. The association's regular

remuneration announcements reflect an important area of stable monetary conditions. Dysonica

can meet its medium-term commitments without difficulty, and it has sufficient liquid assets to

cover its drawn liabilities. In addition, a marketable strategy should be visible, showing that the

organization is really honest in selling its items and management, and generating a lot of benefits

from exchange income. This year's full capital injection of £2,465,187 is an excellent

opportunity for organizations as it enables them to take an interest in Dysonica's various

situations and assist with the company's expansion (Elkhal, 2019).

The organization's finances have been affected by a recurring uptick in venture capital,

which is critical for any association to win in the deep business world and around the world.

Costs can be reduced by taking advantage of optional inventory associations and finding out

which drives are failing and which are draining the organization's cash (Farooq and Selim,

2019).

CONCLUSION

The organisation of money and the arrangement of these dollars, according to the report

given above, is a vital and crucial aspect in the organisation of exhibits. Organizations like

Dysonica, which operate on a worldwide basis, have faced severe competition. They should

11

lower the multiple costs that businesses confront to keep ahead of the competition in a serious

area. Organizations that work worldwide, such as Dysonica, are up against a lot of competition.

They must reduce the different expenses that firms encounter in order to maintain a competitive

advantage in a highly competitive sector. Income forecasting is a critical tool for anticipating a

company's cash influx or outflow at the conclusion of a certain period, allowing businesses to

make their own budgeting decisions. Minor costing and action based costing are two of the

costing methodologies that a Dysonica company may employ to reduce the risk of error and

calculate each expense that should be taken. It also helps businesses save money by employing

cost pools and cost headers to cut expenditures that don't provide value to the bottom line. When

selecting a specific time period, revenue forecasting is an excellent strategy for projecting floods

or surges of cash going into or out of a firm, and businesses may use it to construct their own

strategies. Minimal and action-based expenditure are two of the most effective costing strategies

that a company may use. Dysonica eliminates the possibility of human mistake and evaluates the

costs that must be expended. It also aids businesses in cost-cutting by utilising entire expenses

and cost headers that do not generate substantial income for the organisation.

12

area. Organizations that work worldwide, such as Dysonica, are up against a lot of competition.

They must reduce the different expenses that firms encounter in order to maintain a competitive

advantage in a highly competitive sector. Income forecasting is a critical tool for anticipating a

company's cash influx or outflow at the conclusion of a certain period, allowing businesses to

make their own budgeting decisions. Minor costing and action based costing are two of the

costing methodologies that a Dysonica company may employ to reduce the risk of error and

calculate each expense that should be taken. It also helps businesses save money by employing

cost pools and cost headers to cut expenditures that don't provide value to the bottom line. When

selecting a specific time period, revenue forecasting is an excellent strategy for projecting floods

or surges of cash going into or out of a firm, and businesses may use it to construct their own

strategies. Minimal and action-based expenditure are two of the most effective costing strategies

that a company may use. Dysonica eliminates the possibility of human mistake and evaluates the

costs that must be expended. It also aids businesses in cost-cutting by utilising entire expenses

and cost headers that do not generate substantial income for the organisation.

12

REFERENCES

Books and Journals

Alabdullah, T.T.Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise, 9(2), pp.244-257.

Alakaleek, W. and Cooper, S.Y., 2018. The female entrepreneur’s financial networks: accessing

finance for the emergence of technology-based firms in Jordan. Venture Capital, 20(2),

pp.137-157.

Areiqat, A.Y. and et.al., 2019. Impact of behavioral finance on stock investment decisions

applied study on a sample of investors at Amman stock exchange. Academy of

Accounting and Financial Studies Journal, 23(2), pp.1-17.

Bai, C. and et.al., 2021. Exploring the development trend of internet finance in China:

Perspective from club convergence. The North American Journal of Economics and

Finance, 58, p.101505.

Beaumont, P.H., 2019. Digital Finance: Big Data, Start-ups, and the Future of Financial

Services. Routledge.

Borgogno, O. and Colangelo, G., 2020. Data, innovation and competition in finance: the case of

the access to account rule. European Business Law Review, 31(4).

Carè, R., Trotta, A. and Rizzello, A., 2018. An alternative finance approach for a more

sustainable financial system. In Designing a Sustainable Financial System (pp. 17-63).

Palgrave Macmillan, Cham.

Chen, R. and et.al., 2020. Linkages and spillovers between internet finance and traditional

finance: Evidence from China. Emerging Markets Finance and Trade, 56(6), pp.1196-

1210.

Chen, S.S. and Lin, Y.H., 2018. The competitive effects of S&P 500 Index revisions. Journal of

Business Finance & Accounting, 45(7-8), pp.997-1027.

Dai, L. and Zhang, B., 2019. Political uncertainty and finance: a survey. Asia‐Pacific Journal of

Financial Studies, 48(3), pp.307-333.

Elkhal, K., 2019. Business uncertainty and financial leverage: should the firm double up on

risk?. Managerial Finance.

Farooq, M.O. and Selim, M., 2019. Conceptualization of the real economy and Islamic finance:

Transformation beyond the asset‐link rhetoric. Thunderbird International Business

Review, 61(5), pp.685-696.

Hajjar, M. ed., 2019. Islamic finance in Europe: a cross analysis of 10 European countries.

Springer.

Ionescu, L., 2021. Corporate Environmental Performance, Climate Change Mitigation, and

Green Innovation Behavior in Sustainable Finance. Economics, Management, and

Financial Markets, 16(3), pp.94-106.

Jiang, S., Li, X. and Wang, S., 2021. Exploring evolution trends in cryptocurrency study: From

underlying technology to economic applications. Finance Research Letters, 38,

p.101532.

Kayal, P. and Rohilla, P., 2019. Bitcoin in the literature of economics and finance: a

survey. Available at SSRN 3441652.

Lee, H. and Park, K., 2018. Advances in the corporate finance literature: a survey of recent

studies on Korea. Managerial Finance.

13

Books and Journals

Alabdullah, T.T.Y., 2022. Management accounting insight via a new perspective on risk

management-companies' profitability relationship. International Journal of Intelligent

Enterprise, 9(2), pp.244-257.

Alakaleek, W. and Cooper, S.Y., 2018. The female entrepreneur’s financial networks: accessing

finance for the emergence of technology-based firms in Jordan. Venture Capital, 20(2),

pp.137-157.

Areiqat, A.Y. and et.al., 2019. Impact of behavioral finance on stock investment decisions

applied study on a sample of investors at Amman stock exchange. Academy of

Accounting and Financial Studies Journal, 23(2), pp.1-17.

Bai, C. and et.al., 2021. Exploring the development trend of internet finance in China:

Perspective from club convergence. The North American Journal of Economics and

Finance, 58, p.101505.

Beaumont, P.H., 2019. Digital Finance: Big Data, Start-ups, and the Future of Financial

Services. Routledge.

Borgogno, O. and Colangelo, G., 2020. Data, innovation and competition in finance: the case of

the access to account rule. European Business Law Review, 31(4).

Carè, R., Trotta, A. and Rizzello, A., 2018. An alternative finance approach for a more

sustainable financial system. In Designing a Sustainable Financial System (pp. 17-63).

Palgrave Macmillan, Cham.

Chen, R. and et.al., 2020. Linkages and spillovers between internet finance and traditional

finance: Evidence from China. Emerging Markets Finance and Trade, 56(6), pp.1196-

1210.

Chen, S.S. and Lin, Y.H., 2018. The competitive effects of S&P 500 Index revisions. Journal of

Business Finance & Accounting, 45(7-8), pp.997-1027.

Dai, L. and Zhang, B., 2019. Political uncertainty and finance: a survey. Asia‐Pacific Journal of

Financial Studies, 48(3), pp.307-333.

Elkhal, K., 2019. Business uncertainty and financial leverage: should the firm double up on

risk?. Managerial Finance.

Farooq, M.O. and Selim, M., 2019. Conceptualization of the real economy and Islamic finance:

Transformation beyond the asset‐link rhetoric. Thunderbird International Business

Review, 61(5), pp.685-696.

Hajjar, M. ed., 2019. Islamic finance in Europe: a cross analysis of 10 European countries.

Springer.

Ionescu, L., 2021. Corporate Environmental Performance, Climate Change Mitigation, and

Green Innovation Behavior in Sustainable Finance. Economics, Management, and

Financial Markets, 16(3), pp.94-106.

Jiang, S., Li, X. and Wang, S., 2021. Exploring evolution trends in cryptocurrency study: From

underlying technology to economic applications. Finance Research Letters, 38,

p.101532.

Kayal, P. and Rohilla, P., 2019. Bitcoin in the literature of economics and finance: a

survey. Available at SSRN 3441652.

Lee, H. and Park, K., 2018. Advances in the corporate finance literature: a survey of recent

studies on Korea. Managerial Finance.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liao, G., Yao, D. and Hu, Z., 2020. The spatial effect of the efficiency of regional financial

resource allocation from the perspective of internet finance: evidence from Chinese

provinces. Emerging Markets Finance and Trade, 56(6), pp.1211-1223.

Sandberg, J., 2018. Toward a theory of sustainable finance. In Designing a Sustainable Financial

System (pp. 329-346). Palgrave Macmillan, Cham.

Shahab, Y. and et.al., 2021. Online feedback and crowdfunding finance in China. International

Journal of Finance & Economics, 26(3), pp.4634-4652.

14

resource allocation from the perspective of internet finance: evidence from Chinese

provinces. Emerging Markets Finance and Trade, 56(6), pp.1211-1223.

Sandberg, J., 2018. Toward a theory of sustainable finance. In Designing a Sustainable Financial

System (pp. 329-346). Palgrave Macmillan, Cham.

Shahab, Y. and et.al., 2021. Online feedback and crowdfunding finance in China. International

Journal of Finance & Economics, 26(3), pp.4634-4652.

14

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.