Issues in Auditing Practice: Report on Cerise Enterprises (BUS000)

VerifiedAdded on 2023/06/03

|10

|2378

|199

Report

AI Summary

This report is an audit planning report prepared for Cerise Enterprises, a small entity. It includes an executive summary, table of contents, introduction, analysis, discussion, conclusion, and recommendations. The report identifies audit risks and assertions in key accounts and proposes audit procedures. The analysis involves a trial balance, determination of materiality, and a preliminary analytical review, including variance analysis of the income statement. The discussion focuses on critical income statement accounts like sales, cost of sales, repair and maintenance, and wages, along with their respective audit assertions and procedures. A fraud risk analysis is also conducted, highlighting potential risks in the accounts. The report recommends additional analysis and offers suggestions for the audit process, including opening balance confirmation and balance sheet analysis.

University of XXXXXXXXXXXXX

Issues in Auditing Practice Assignment

BUS000, Tutor Name, Tutorial Time

Student Name, SID: XXXXXXXXXX

7-7-2017

Issues in Auditing Practice Assignment

BUS000, Tutor Name, Tutorial Time

Student Name, SID: XXXXXXXXXX

7-7-2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

An audit planning report has been prepared for one of the small entities named “Cerise

Enterprises”. The report incorporates the audit risks and the audit assertions in the critical

accounts and the audit procedures to be employed in order to check and verify the same.

Several analysis have been done to identify the critical accounts and the also the fraud risk

analysis has been done towards the end to find the possibility of fraud in accounts, if any.

i

An audit planning report has been prepared for one of the small entities named “Cerise

Enterprises”. The report incorporates the audit risks and the audit assertions in the critical

accounts and the audit procedures to be employed in order to check and verify the same.

Several analysis have been done to identify the critical accounts and the also the fraud risk

analysis has been done towards the end to find the possibility of fraud in accounts, if any.

i

Table of Contents

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................2

3. Discussion on the report................................................................................................................3

3.1. Income statement accounts to be analysed..........................................................................3

3.2. Audit procedures to be undertaken.......................................................................................4

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................2

3. Discussion on the report................................................................................................................3

3.1. Income statement accounts to be analysed..........................................................................3

3.2. Audit procedures to be undertaken.......................................................................................4

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.Introduction

1.1. Authorisation

This report is being prepared as per the directions of the audit partner of the firm to whom

the report will be handed over at the end (Bromwich & Scapens, 2016). Several

recommendations and suggestions have been given by the senior audit partner which has

also been discussed.

1.2. Limitations

The entire report has been prepared on the basis of the trial balance of the entity, however

the debit and the credit totals of the same is not matching and therefore the same can be

assumed to be suspense account but it has not been considered in any of the analysis as the

nature of the account is not known (Bumgarner & Vasarhelyi, 2018).

1.3. Scope

The report will include selection and identification of the key risk account where audit

attention is required, the audit assertions and procedures on the basis of preliminary

analytical procedures. The report will also highlight the selection of materiality limit and

possibility of frauds in any of the accounts mentioned in trial balance.

1

1.1. Authorisation

This report is being prepared as per the directions of the audit partner of the firm to whom

the report will be handed over at the end (Bromwich & Scapens, 2016). Several

recommendations and suggestions have been given by the senior audit partner which has

also been discussed.

1.2. Limitations

The entire report has been prepared on the basis of the trial balance of the entity, however

the debit and the credit totals of the same is not matching and therefore the same can be

assumed to be suspense account but it has not been considered in any of the analysis as the

nature of the account is not known (Bumgarner & Vasarhelyi, 2018).

1.3. Scope

The report will include selection and identification of the key risk account where audit

attention is required, the audit assertions and procedures on the basis of preliminary

analytical procedures. The report will also highlight the selection of materiality limit and

possibility of frauds in any of the accounts mentioned in trial balance.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

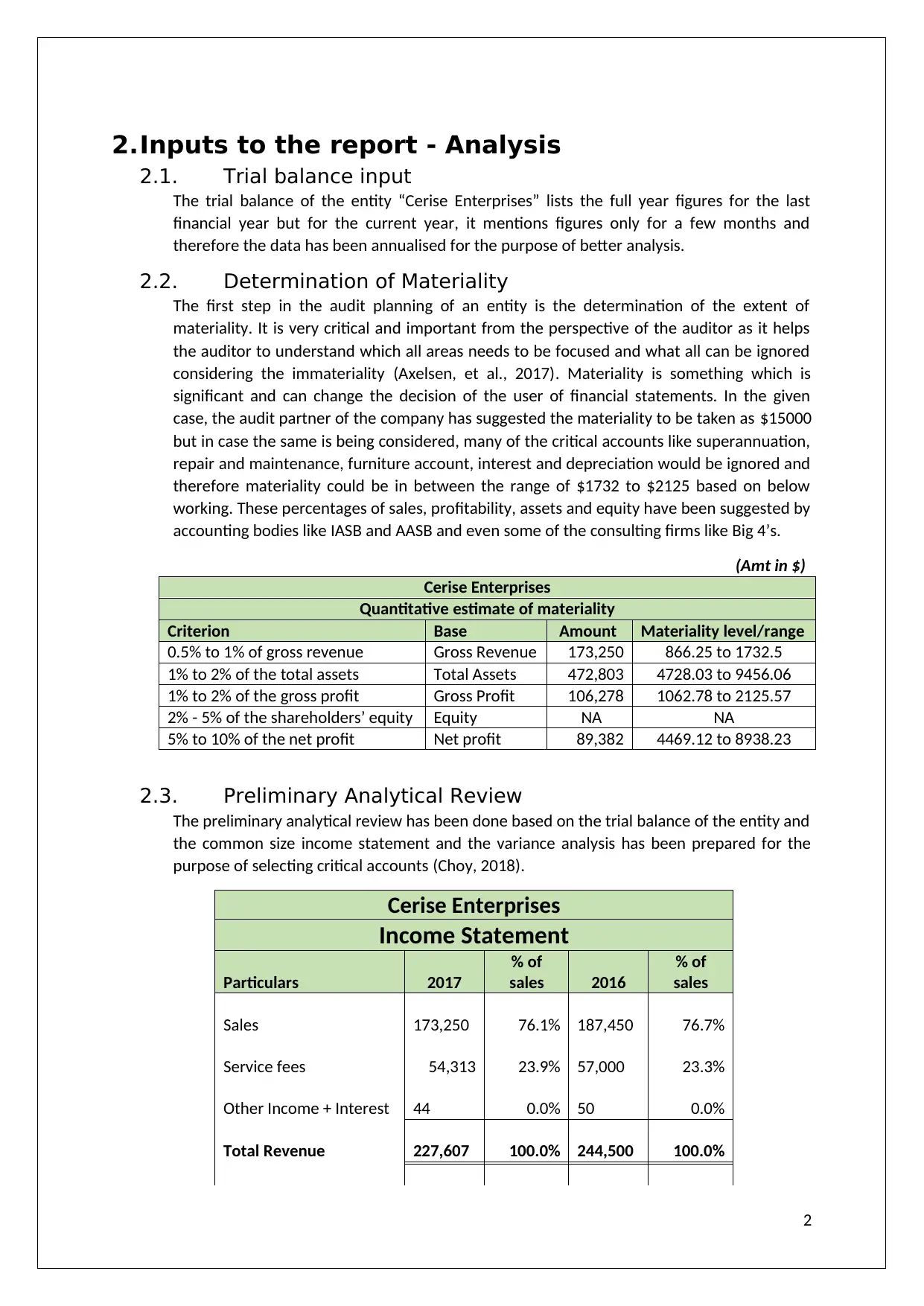

2.Inputs to the report - Analysis

2.1. Trial balance input

The trial balance of the entity “Cerise Enterprises” lists the full year figures for the last

financial year but for the current year, it mentions figures only for a few months and

therefore the data has been annualised for the purpose of better analysis.

2.2. Determination of Materiality

The first step in the audit planning of an entity is the determination of the extent of

materiality. It is very critical and important from the perspective of the auditor as it helps

the auditor to understand which all areas needs to be focused and what all can be ignored

considering the immateriality (Axelsen, et al., 2017). Materiality is something which is

significant and can change the decision of the user of financial statements. In the given

case, the audit partner of the company has suggested the materiality to be taken as $15000

but in case the same is being considered, many of the critical accounts like superannuation,

repair and maintenance, furniture account, interest and depreciation would be ignored and

therefore materiality could be in between the range of $1732 to $2125 based on below

working. These percentages of sales, profitability, assets and equity have been suggested by

accounting bodies like IASB and AASB and even some of the consulting firms like Big 4’s.

(Amt in $)

Cerise Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 173,250 866.25 to 1732.5

1% to 2% of the total assets Total Assets 472,803 4728.03 to 9456.06

1% to 2% of the gross profit Gross Profit 106,278 1062.78 to 2125.57

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 89,382 4469.12 to 8938.23

2.3. Preliminary Analytical Review

The preliminary analytical review has been done based on the trial balance of the entity and

the common size income statement and the variance analysis has been prepared for the

purpose of selecting critical accounts (Choy, 2018).

Cerise Enterprises

Income Statement

Particulars 2017

% of

sales 2016

% of

sales

Sales 173,250 76.1% 187,450 76.7%

Service fees 54,313 23.9% 57,000 23.3%

Other Income + Interest 44 0.0% 50 0.0%

Total Revenue 227,607 100.0% 244,500 100.0%

2

2.1. Trial balance input

The trial balance of the entity “Cerise Enterprises” lists the full year figures for the last

financial year but for the current year, it mentions figures only for a few months and

therefore the data has been annualised for the purpose of better analysis.

2.2. Determination of Materiality

The first step in the audit planning of an entity is the determination of the extent of

materiality. It is very critical and important from the perspective of the auditor as it helps

the auditor to understand which all areas needs to be focused and what all can be ignored

considering the immateriality (Axelsen, et al., 2017). Materiality is something which is

significant and can change the decision of the user of financial statements. In the given

case, the audit partner of the company has suggested the materiality to be taken as $15000

but in case the same is being considered, many of the critical accounts like superannuation,

repair and maintenance, furniture account, interest and depreciation would be ignored and

therefore materiality could be in between the range of $1732 to $2125 based on below

working. These percentages of sales, profitability, assets and equity have been suggested by

accounting bodies like IASB and AASB and even some of the consulting firms like Big 4’s.

(Amt in $)

Cerise Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 173,250 866.25 to 1732.5

1% to 2% of the total assets Total Assets 472,803 4728.03 to 9456.06

1% to 2% of the gross profit Gross Profit 106,278 1062.78 to 2125.57

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 89,382 4469.12 to 8938.23

2.3. Preliminary Analytical Review

The preliminary analytical review has been done based on the trial balance of the entity and

the common size income statement and the variance analysis has been prepared for the

purpose of selecting critical accounts (Choy, 2018).

Cerise Enterprises

Income Statement

Particulars 2017

% of

sales 2016

% of

sales

Sales 173,250 76.1% 187,450 76.7%

Service fees 54,313 23.9% 57,000 23.3%

Other Income + Interest 44 0.0% 50 0.0%

Total Revenue 227,607 100.0% 244,500 100.0%

2

Less: Expenses

Cost of sales 63,708 28.0% 63,595 26.0%

Bank charges 319 0.1% 350 0.1%

Depreciation 14,841 6.5% 15,863 6.5%

Interest expense 10,542 4.6% 11,500 4.7%

Printing 231 0.1% 250 0.1%

Repairs and

Maintenance 1,320 0.6% 5,050 2.1%

Wages 44,000 19.3% 53,000 21.7%

Superannuation 3,263 1.4% 4,770 2.0%

Total Expenses 138,224 60.7% 154,378 63.1%

Net Profit 89,382 39.3% 90,122 36.9%

Cerise Enterprises

Income Statement

Particulars 2017 2016 Variance Variance %

Sales 173,250 187,450 1,550 1%

Consultancy fees 54,313 57,000 2,250 4%

Interest income 44 50 - 2 -4%

Total Revenue 227,607 244,500 3,798 2%

Less: Expenses

Cost of sales 63,708 63,595 5,905 9%

Bank charges 319 350 - 2 -1%

Depreciation 14,841 15,863 327 2%

Interest expense 10,542 11,500 - 0%

Printing 231 250 2 1%

Repairs and

Maintenance 1,320 5,050 - 3,610 -71%

Wages 44,000 53,000 - 5,000 -9%

Superannuation 3,263 4,770 - 1,210 -25%

Total Expenses 138,224 154,378 - 3,588 -2%

Net Profit 89,382 90,122 7,386 8%

Net Profit % 39.27% 36.86%

3

Cost of sales 63,708 28.0% 63,595 26.0%

Bank charges 319 0.1% 350 0.1%

Depreciation 14,841 6.5% 15,863 6.5%

Interest expense 10,542 4.6% 11,500 4.7%

Printing 231 0.1% 250 0.1%

Repairs and

Maintenance 1,320 0.6% 5,050 2.1%

Wages 44,000 19.3% 53,000 21.7%

Superannuation 3,263 1.4% 4,770 2.0%

Total Expenses 138,224 60.7% 154,378 63.1%

Net Profit 89,382 39.3% 90,122 36.9%

Cerise Enterprises

Income Statement

Particulars 2017 2016 Variance Variance %

Sales 173,250 187,450 1,550 1%

Consultancy fees 54,313 57,000 2,250 4%

Interest income 44 50 - 2 -4%

Total Revenue 227,607 244,500 3,798 2%

Less: Expenses

Cost of sales 63,708 63,595 5,905 9%

Bank charges 319 350 - 2 -1%

Depreciation 14,841 15,863 327 2%

Interest expense 10,542 11,500 - 0%

Printing 231 250 2 1%

Repairs and

Maintenance 1,320 5,050 - 3,610 -71%

Wages 44,000 53,000 - 5,000 -9%

Superannuation 3,263 4,770 - 1,210 -25%

Total Expenses 138,224 154,378 - 3,588 -2%

Net Profit 89,382 90,122 7,386 8%

Net Profit % 39.27% 36.86%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

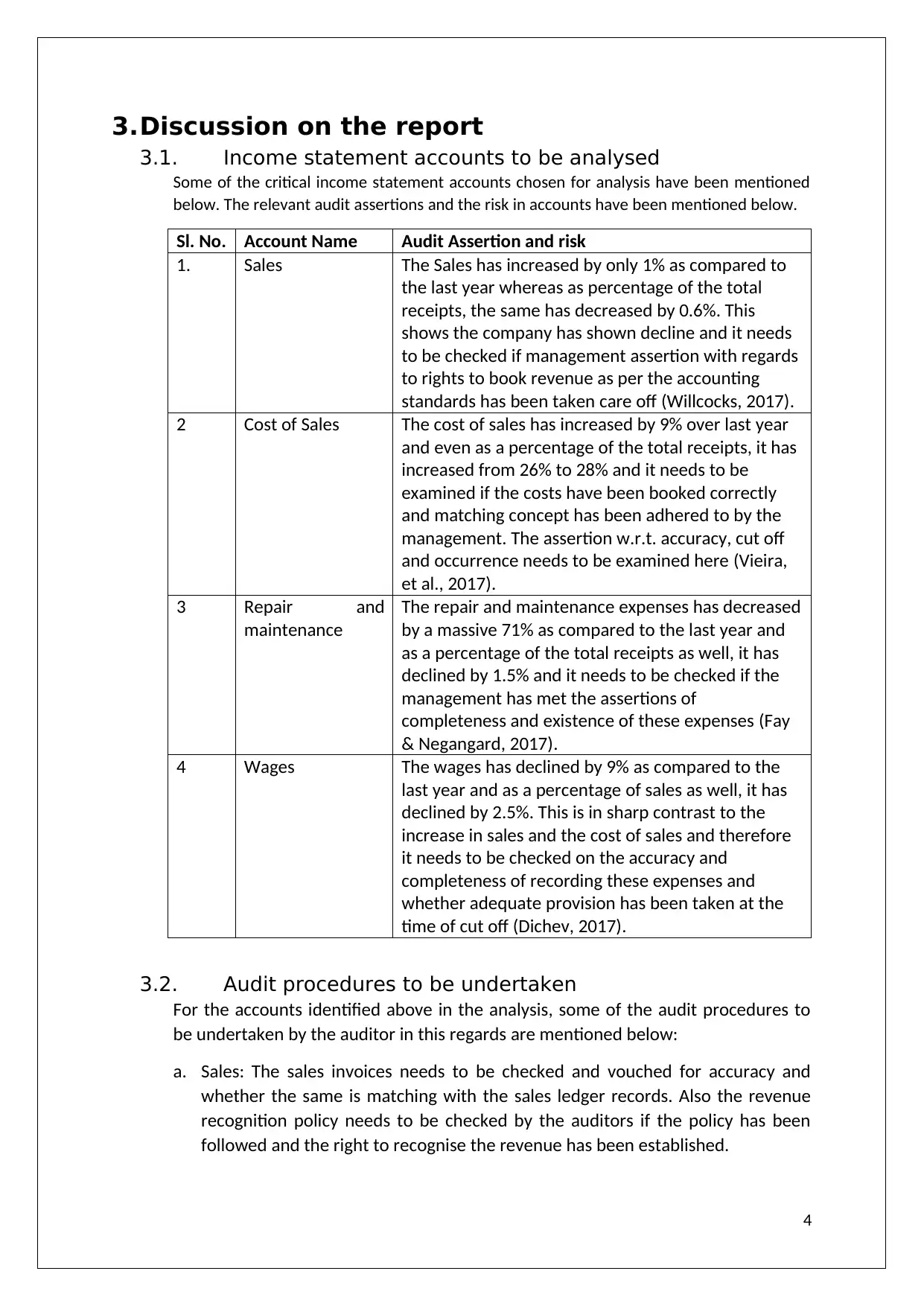

3.Discussion on the report

3.1. Income statement accounts to be analysed

Some of the critical income statement accounts chosen for analysis have been mentioned

below. The relevant audit assertions and the risk in accounts have been mentioned below.

Sl. No. Account Name Audit Assertion and risk

1. Sales The Sales has increased by only 1% as compared to

the last year whereas as percentage of the total

receipts, the same has decreased by 0.6%. This

shows the company has shown decline and it needs

to be checked if management assertion with regards

to rights to book revenue as per the accounting

standards has been taken care off (Willcocks, 2017).

2 Cost of Sales The cost of sales has increased by 9% over last year

and even as a percentage of the total receipts, it has

increased from 26% to 28% and it needs to be

examined if the costs have been booked correctly

and matching concept has been adhered to by the

management. The assertion w.r.t. accuracy, cut off

and occurrence needs to be examined here (Vieira,

et al., 2017).

3 Repair and

maintenance

The repair and maintenance expenses has decreased

by a massive 71% as compared to the last year and

as a percentage of the total receipts as well, it has

declined by 1.5% and it needs to be checked if the

management has met the assertions of

completeness and existence of these expenses (Fay

& Negangard, 2017).

4 Wages The wages has declined by 9% as compared to the

last year and as a percentage of sales as well, it has

declined by 2.5%. This is in sharp contrast to the

increase in sales and the cost of sales and therefore

it needs to be checked on the accuracy and

completeness of recording these expenses and

whether adequate provision has been taken at the

time of cut off (Dichev, 2017).

3.2. Audit procedures to be undertaken

For the accounts identified above in the analysis, some of the audit procedures to

be undertaken by the auditor in this regards are mentioned below:

a. Sales: The sales invoices needs to be checked and vouched for accuracy and

whether the same is matching with the sales ledger records. Also the revenue

recognition policy needs to be checked by the auditors if the policy has been

followed and the right to recognise the revenue has been established.

4

3.1. Income statement accounts to be analysed

Some of the critical income statement accounts chosen for analysis have been mentioned

below. The relevant audit assertions and the risk in accounts have been mentioned below.

Sl. No. Account Name Audit Assertion and risk

1. Sales The Sales has increased by only 1% as compared to

the last year whereas as percentage of the total

receipts, the same has decreased by 0.6%. This

shows the company has shown decline and it needs

to be checked if management assertion with regards

to rights to book revenue as per the accounting

standards has been taken care off (Willcocks, 2017).

2 Cost of Sales The cost of sales has increased by 9% over last year

and even as a percentage of the total receipts, it has

increased from 26% to 28% and it needs to be

examined if the costs have been booked correctly

and matching concept has been adhered to by the

management. The assertion w.r.t. accuracy, cut off

and occurrence needs to be examined here (Vieira,

et al., 2017).

3 Repair and

maintenance

The repair and maintenance expenses has decreased

by a massive 71% as compared to the last year and

as a percentage of the total receipts as well, it has

declined by 1.5% and it needs to be checked if the

management has met the assertions of

completeness and existence of these expenses (Fay

& Negangard, 2017).

4 Wages The wages has declined by 9% as compared to the

last year and as a percentage of sales as well, it has

declined by 2.5%. This is in sharp contrast to the

increase in sales and the cost of sales and therefore

it needs to be checked on the accuracy and

completeness of recording these expenses and

whether adequate provision has been taken at the

time of cut off (Dichev, 2017).

3.2. Audit procedures to be undertaken

For the accounts identified above in the analysis, some of the audit procedures to

be undertaken by the auditor in this regards are mentioned below:

a. Sales: The sales invoices needs to be checked and vouched for accuracy and

whether the same is matching with the sales ledger records. Also the revenue

recognition policy needs to be checked by the auditors if the policy has been

followed and the right to recognise the revenue has been established.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Cost of Sales: Since the cost of sales has increased by huge amount, it needs to

be vouched if all the expenses incurred in the accounting period has been

recorded with accuracy or the future expenses have also been considered. Also,

cut off accounting entries at the month and year end also needs to be checked if

the same has been taken appropriately and extra cost is not accounted in the

current year (Raiborn, et al., 2016).

c. Repair and Maintenance: The repair expenses has come down drastically and

hence it needs to be checked if the management has ensured that all the

expenses pertaining to the accounting year has been recorded in the books and

if the requisite provision has also been taken. All the management estimates as

well as the judgements in this regards also needs to be verified (Meroño-Cerdán,

et al., 2017).

d. Wages: The wages has decreased by 9% and hence it needs to check if the

efficiency of operations has improved or the wage rates have been lowered. The

employee register needs to be checked and also it needs to be checked if the

company has complied with all the labour laws and the appropriate disclosures

have been given in this regard (Kachelmeier, et al., 2018).

5

be vouched if all the expenses incurred in the accounting period has been

recorded with accuracy or the future expenses have also been considered. Also,

cut off accounting entries at the month and year end also needs to be checked if

the same has been taken appropriately and extra cost is not accounted in the

current year (Raiborn, et al., 2016).

c. Repair and Maintenance: The repair expenses has come down drastically and

hence it needs to be checked if the management has ensured that all the

expenses pertaining to the accounting year has been recorded in the books and

if the requisite provision has also been taken. All the management estimates as

well as the judgements in this regards also needs to be verified (Meroño-Cerdán,

et al., 2017).

d. Wages: The wages has decreased by 9% and hence it needs to check if the

efficiency of operations has improved or the wage rates have been lowered. The

employee register needs to be checked and also it needs to be checked if the

company has complied with all the labour laws and the appropriate disclosures

have been given in this regard (Kachelmeier, et al., 2018).

5

4.Conclusion – Fraud Risk Analysis

Fraud risk analysis is analysing the possibility of the fraud in the organization. It is one of the

key steps in auditing and therefore needs to be conducted compulsorily. The same has been

stated in a number of places like APES 110 on ethics of auditing. Besides this, the concept of

professional scepticism also advocates that the fraud risk analysis should be conducted for

all the clients irrespective of anything (Grenier, 2017). In the given case the audit partner

has recommended and suggested that the given client should not be subjected to fraud risk

analysis considering the trustworthiness but his contention is wrong as per the points

already explained above.

Some of the accounts in the given entity do hint towards the possibility of the fraud in the

organization, which are wages account and cost of sales account, for the reasons explained

above. Furthermore, superannuation account also needs to be reviewed as the same has

gone down considerably as compared to the last year and depreciation account which has

increased despite no changes in the asset balances as compared to the last year.

5.Recommendations

Few of the recommendations for the given client’s audit is:

Apart from the income statement analysis, opening balance confirmation also needs

to be done.

Balance sheet analysis can also be considered in case the auditor is not able to

establish sufficient and appropriate audit evidences.

References

6

Fraud risk analysis is analysing the possibility of the fraud in the organization. It is one of the

key steps in auditing and therefore needs to be conducted compulsorily. The same has been

stated in a number of places like APES 110 on ethics of auditing. Besides this, the concept of

professional scepticism also advocates that the fraud risk analysis should be conducted for

all the clients irrespective of anything (Grenier, 2017). In the given case the audit partner

has recommended and suggested that the given client should not be subjected to fraud risk

analysis considering the trustworthiness but his contention is wrong as per the points

already explained above.

Some of the accounts in the given entity do hint towards the possibility of the fraud in the

organization, which are wages account and cost of sales account, for the reasons explained

above. Furthermore, superannuation account also needs to be reviewed as the same has

gone down considerably as compared to the last year and depreciation account which has

increased despite no changes in the asset balances as compared to the last year.

5.Recommendations

Few of the recommendations for the given client’s audit is:

Apart from the income statement analysis, opening balance confirmation also needs

to be done.

Balance sheet analysis can also be considered in case the auditor is not able to

establish sufficient and appropriate audit evidences.

References

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Axelsen, M., Green, P. & Ridley, G., 2017. Explaining the information systems auditor role in the

public sector financial audit. International Journal of Accounting Information Systems, 24(1), pp. 15-

31.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, Volume 31, pp. 1-9.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Willcocks, L. P. L. M. C. &. S. C., 2017. Introduction. In Outsourcing and Offshoring Business Services.

Cham: Palgrave Macmillan,.

7

public sector financial audit. International Journal of Accounting Information Systems, 24(1), pp. 15-

31.

Bromwich, M. & Scapens, R., 2016. Management Accounting Research: 25 years on. Management

Accounting Research, Volume 31, pp. 1-9.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, p. 145.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1).

Willcocks, L. P. L. M. C. &. S. C., 2017. Introduction. In Outsourcing and Offshoring Business Services.

Cham: Palgrave Macmillan,.

7

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.