Oral Assessment: Certificate IV in Finance and Mortgage Broking

VerifiedAdded on 2022/08/21

|7

|1804

|11

Homework Assignment

AI Summary

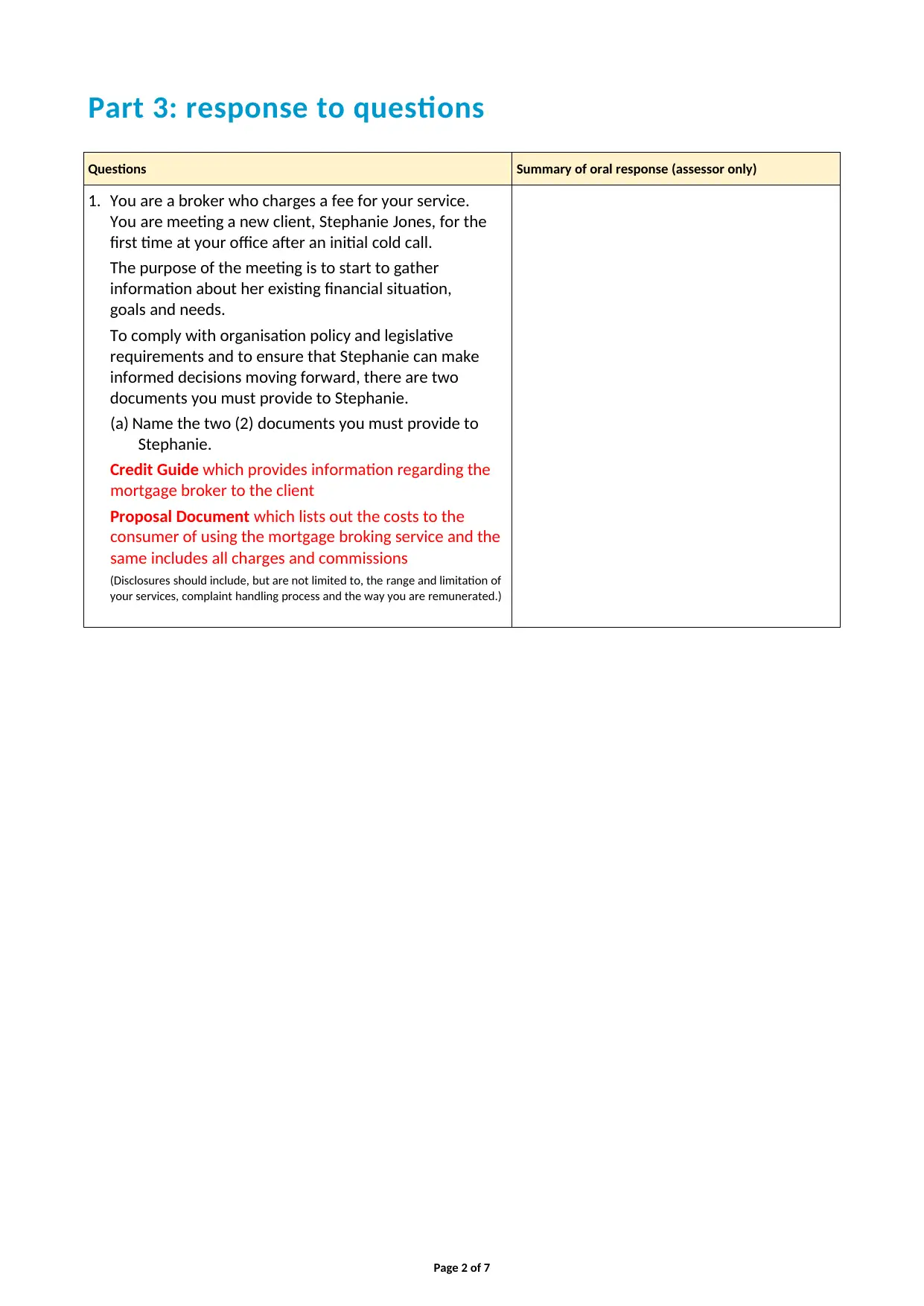

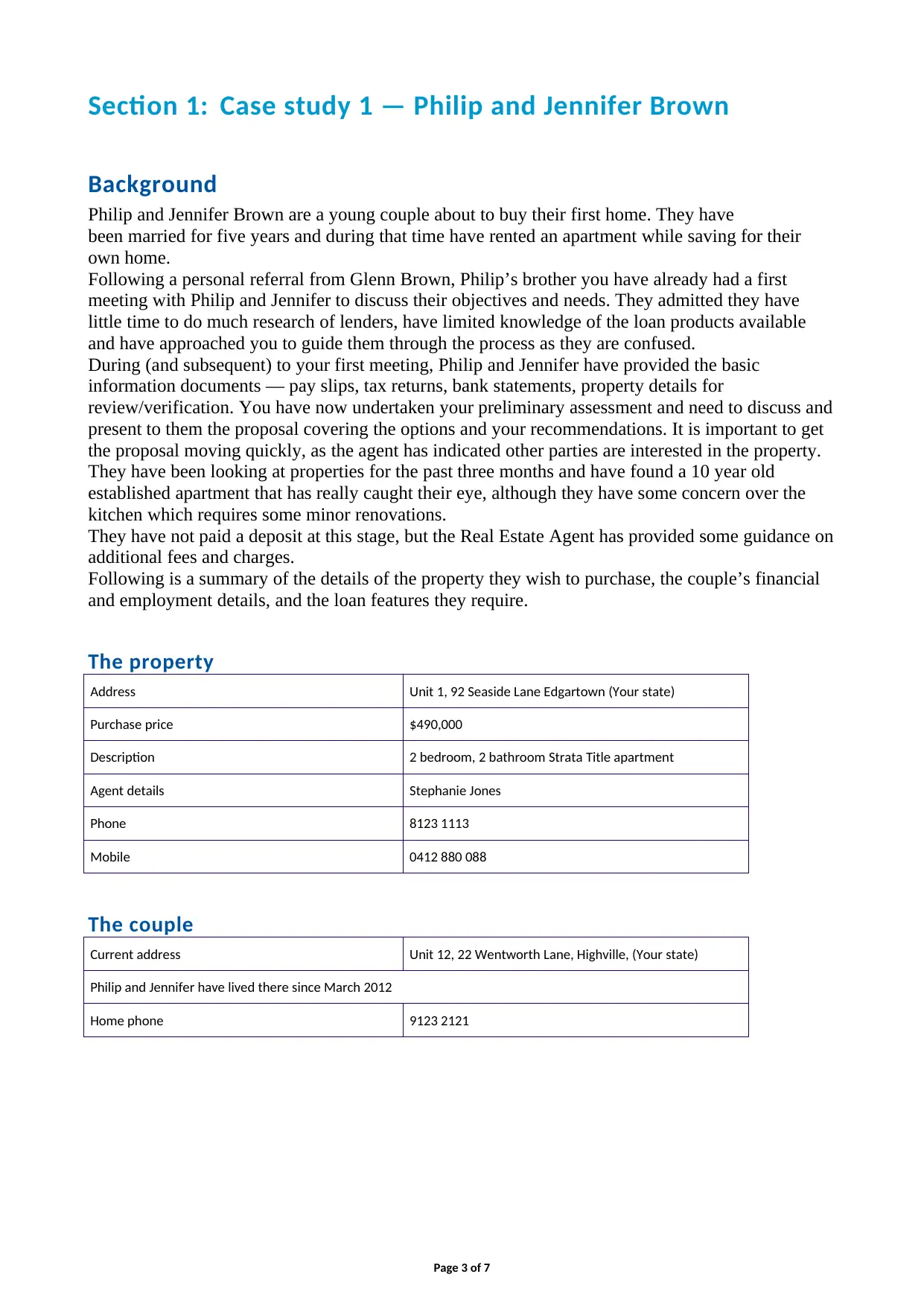

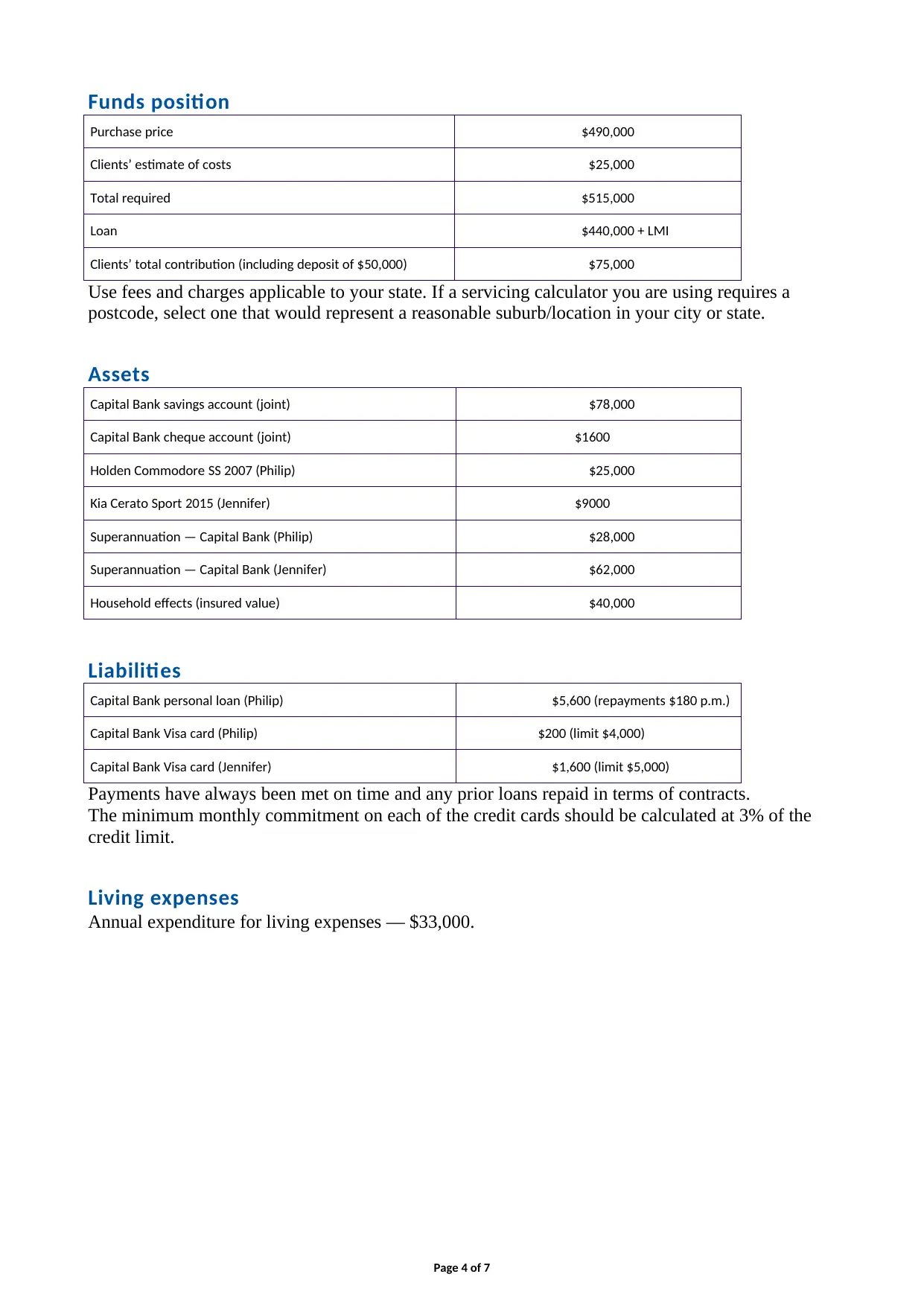

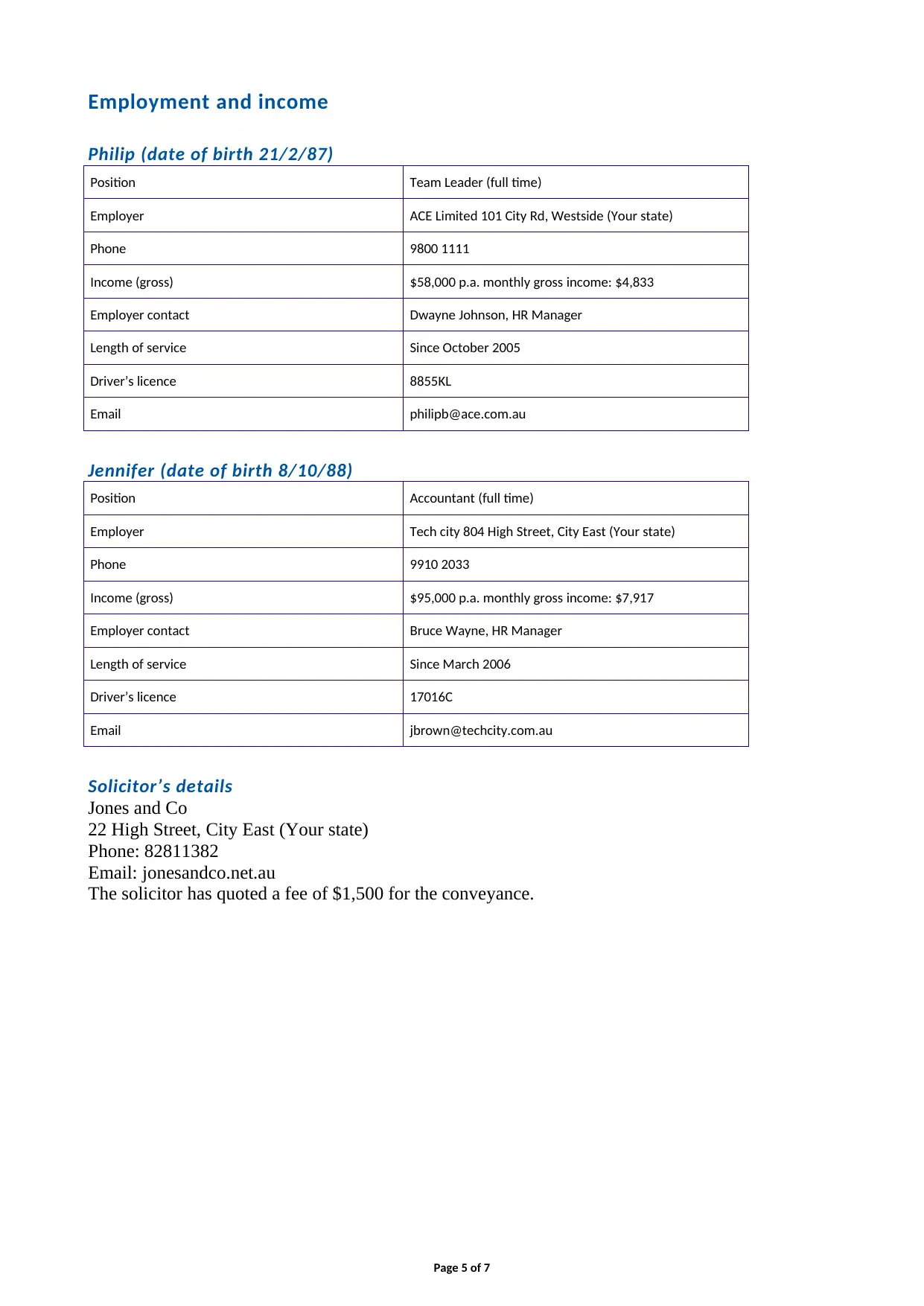

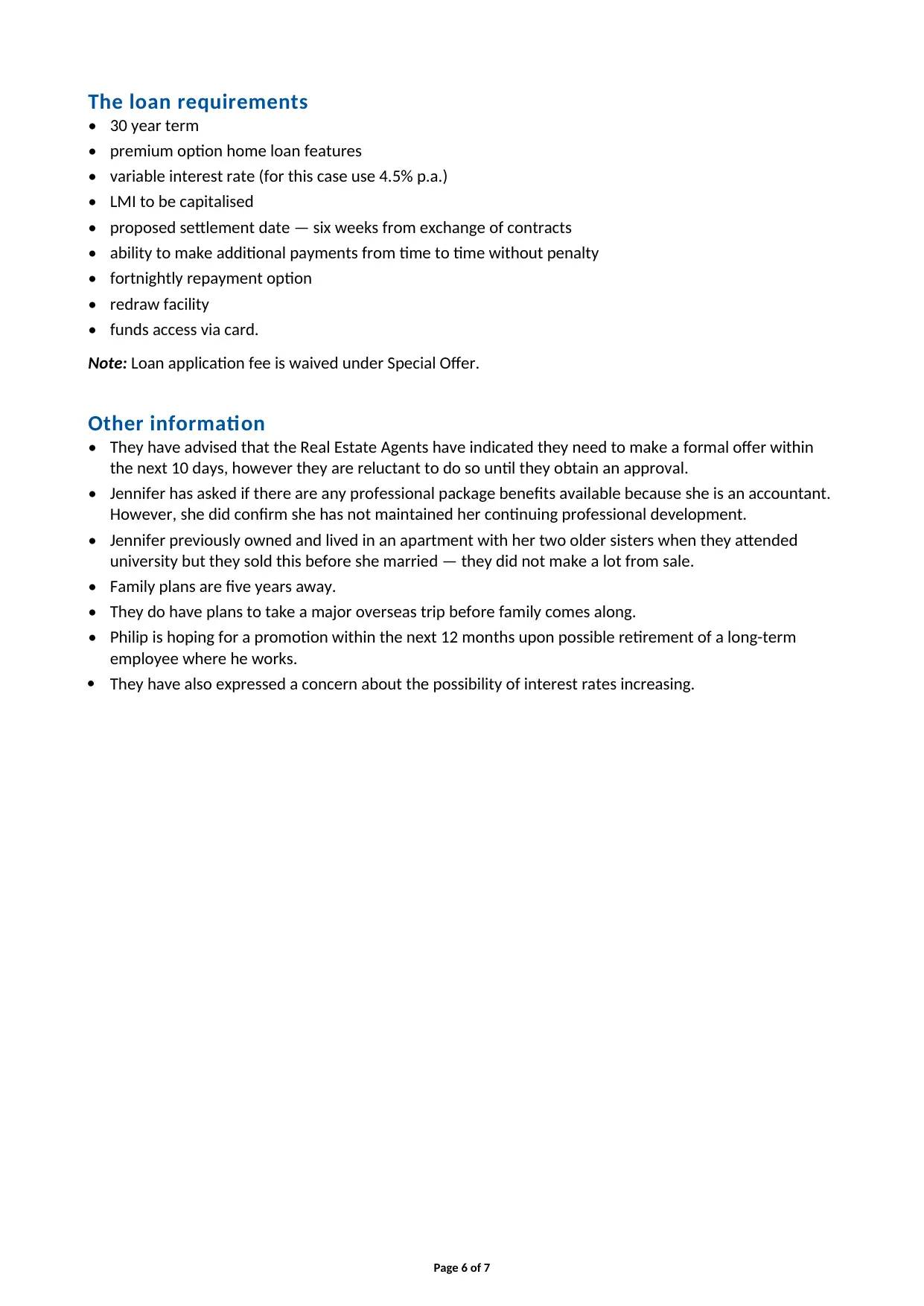

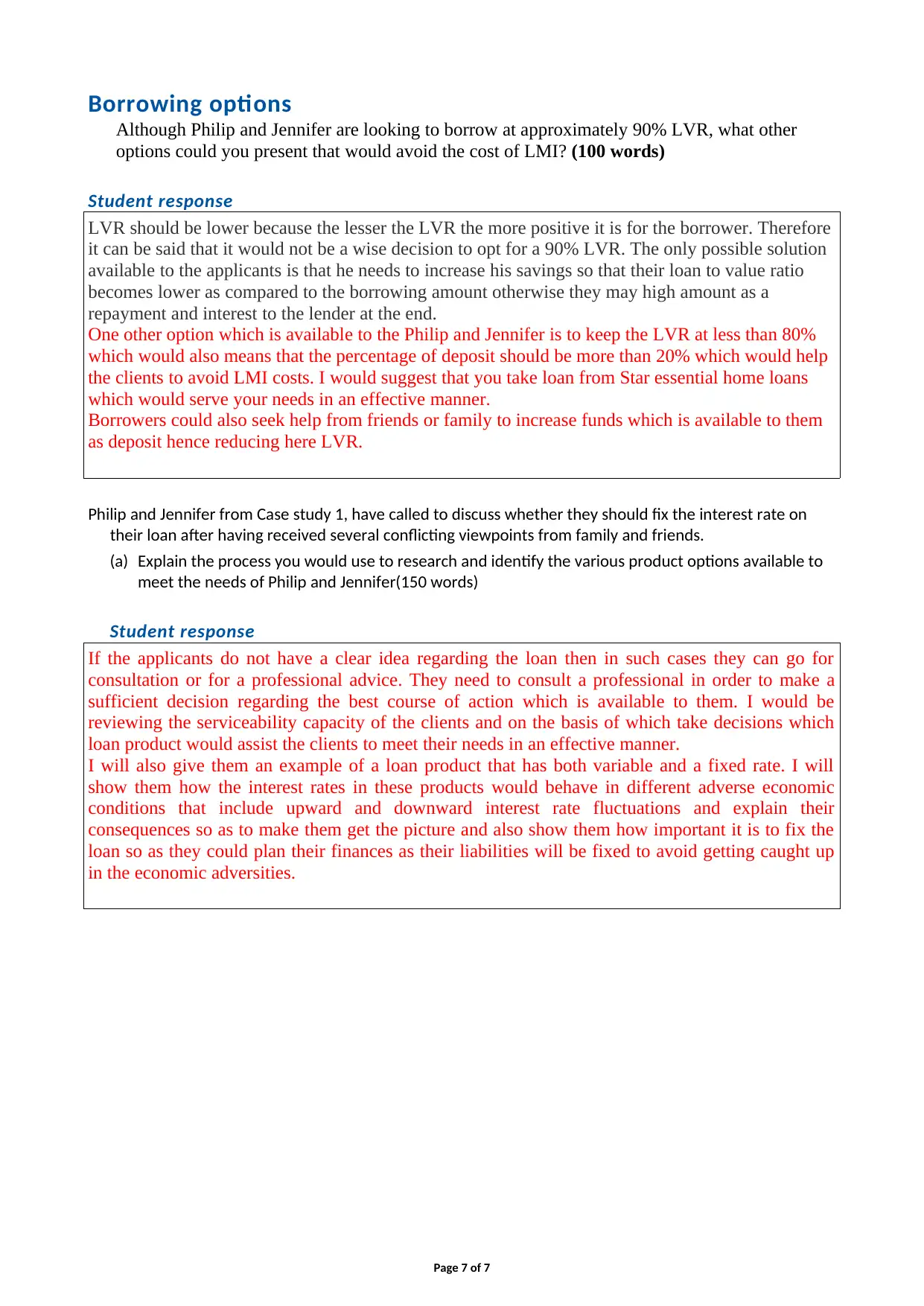

This document provides a solution to an oral assignment for the Certificate IV in Finance and Mortgage Broking (CIVMB) course. The assignment focuses on various aspects of mortgage broking, including client interactions, loan product knowledge, and financial analysis. The solution addresses questions related to providing required documents to clients, analyzing a case study involving a young couple seeking a home loan, and discussing borrowing options to avoid LMI. It also includes a discussion on researching and identifying product options for clients considering fixed interest rates. The assignment assesses the student's understanding of the mortgage broking process, client needs analysis, and financial product knowledge. The student's responses are provided to the questions in the assignment.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.