CIVMB_AS_v3A3: Detailed Case Study on Finance and Mortgage Broking

VerifiedAdded on 2024/05/20

|55

|13159

|250

Report

AI Summary

This assignment presents a comprehensive solution to a case study focused on finance and mortgage broking, specifically addressing the requirements of Certificate IV in Finance and Mortgage Broking (CIVMB_AS_v3A3). It includes two case studies, the first involving Clinton and Jennifer Andrews seeking to purchase an investment property, and the second focusing on Tony and Lorraine Denton. The solution covers various tasks such as initial disclosures, client information gathering, assessing financial situations, exploring equity usage, conducting reasonable inquiries, providing recommendations, understanding interest rates, and navigating settlement processes. Furthermore, it delves into responsible lending obligations, special considerations for self-employed individuals, advising on financial strategies, assessing the impact of credit history, and understanding external dispute resolution. The document also incorporates practical tools like a client information collection tool and a serviceability calculator, providing a thorough analysis and guidance on the key aspects of finance and mortgage broking. This assignment, contributed by a student, is available on Desklib, a platform offering AI-powered study tools and resources for students.

Assignment

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v3A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10573096

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v3A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number 10573096

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Result summary (assessor to complete)

First submission Resubmission (if required)

Section

1: Case

study 1

—

Clinton

and

Jennifer

Andrew

s

Task 1 — Initial disclosures

Task 2 — Gathering and documenting client

information

Task 3 — Assessing the clients’ situation

Task 4 — Using equity

Task 5 — Reasonable enquiries

Task 6 — Recommendations

Task 7 — Clinton and Jennifer’s professional

network

Task 8 — Interest rates

Task 9 — Settlement

Section

2: Case

study 2

—

Tony

and

Lorraine

Denton

Task 10 — Establishing level of financial knowledge

Task 11 — Responsible lending obligations

Task 12 — Self Employed special considerations

Task 13 — Advising on strategies

Task 14 — Impact of credit history

Task 15 — External dispute resolution

Task 16 — Effective access to files

Feedback (assessor to complete)

[insert assessor feedback]

First submission Resubmission (if required)

Section

1: Case

study 1

—

Clinton

and

Jennifer

Andrew

s

Task 1 — Initial disclosures

Task 2 — Gathering and documenting client

information

Task 3 — Assessing the clients’ situation

Task 4 — Using equity

Task 5 — Reasonable enquiries

Task 6 — Recommendations

Task 7 — Clinton and Jennifer’s professional

network

Task 8 — Interest rates

Task 9 — Settlement

Section

2: Case

study 2

—

Tony

and

Lorraine

Denton

Task 10 — Establishing level of financial knowledge

Task 11 — Responsible lending obligations

Task 12 — Self Employed special considerations

Task 13 — Advising on strategies

Task 14 — Impact of credit history

Task 15 — External dispute resolution

Task 16 — Effective access to files

Feedback (assessor to complete)

[insert assessor feedback]

Before you begin

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v3A3).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Section 1: Case study 1 — Clinton and Jennifer Andrews

– Task 1 — Initial disclosures

– Task 2 — Gathering and documenting client information

– Task 3 — Assessing the clients’ situation

– Task 4 — Using equity

– Task 5 — Reasonable enquiries

– Task 6 — Recommendations

– Task 7 — Clinton and Jennifer’s professional network

– Task 8 — Interest rates

– Task 9 — Settlement

• Section 2: Case study 2 — Tony and Lorraine Denton

– Task 10 — Establishing level of financial knowledge

– Task 11 — Responsible lending obligations

– Task 12 — Self Employed special considerations

– Task 13 — Advising on strategies

– Task 14 — Impact of credit history

– Task 15 — External dispute resolution

– Task 16 — Effective access to files

• Appendix 1: Client information collection tool/Fact Finder.

• Appendix 2: Serviceability calculator.

How to use the study plan

We recommend that you use the study plan for this subject; it will help you manage your time

effectively and complete the assignment within your enrolment period. Your study plan is in the

KapLearn Certificate IV in Finance and Mortgage Broking (CIVMBv3) subject room.

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v3A3).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Section 1: Case study 1 — Clinton and Jennifer Andrews

– Task 1 — Initial disclosures

– Task 2 — Gathering and documenting client information

– Task 3 — Assessing the clients’ situation

– Task 4 — Using equity

– Task 5 — Reasonable enquiries

– Task 6 — Recommendations

– Task 7 — Clinton and Jennifer’s professional network

– Task 8 — Interest rates

– Task 9 — Settlement

• Section 2: Case study 2 — Tony and Lorraine Denton

– Task 10 — Establishing level of financial knowledge

– Task 11 — Responsible lending obligations

– Task 12 — Self Employed special considerations

– Task 13 — Advising on strategies

– Task 14 — Impact of credit history

– Task 15 — External dispute resolution

– Task 16 — Effective access to files

• Appendix 1: Client information collection tool/Fact Finder.

• Appendix 2: Serviceability calculator.

How to use the study plan

We recommend that you use the study plan for this subject; it will help you manage your time

effectively and complete the assignment within your enrolment period. Your study plan is in the

KapLearn Certificate IV in Finance and Mortgage Broking (CIVMBv3) subject room.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1: Instructions for completing and submitting

this assignment

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_CIVMBv3A3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete

all 16 tasks.

The information and data needed to complete Sections 1 and 2 is presented in case studies at the

beginning of those sections.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted,

although they must not be in conflict with the information provided in the Case Study.

this assignment

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_CIVMBv3A3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete

all 16 tasks.

The information and data needed to complete Sections 1 and 2 is presented in case studies at the

beginning of those sections.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted,

although they must not be in conflict with the information provided in the Case Study.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

You may also be required to source additional information from other organisations in the finance

industry to find the right products or services to meet your client’s requirements or to calculate any

service fees that may be applicable.

industry to find the right products or services to meet your client’s requirements or to calculate any

service fees that may be applicable.

Submitting the assignment

You must submit the completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

The assignment marking process

You have 26 weeks from the date of your enrolment in this subject to submit your

completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be given an additional four (4) weeks

to resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv3) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

You must submit the completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

The assignment marking process

You have 26 weeks from the date of your enrolment in this subject to submit your

completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be given an additional four (4) weeks

to resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv3) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

• Assessing your responses to each question (and sub-parts if applicable) then determining whether

you have demonstrated competence in each question.

• Determining if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

you have demonstrated competence in each question.

• Determining if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the

required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

When making changes to your original submission, use a different text colour for your resubmission.

This way, your assessor will be in a better position to gauge the quality and nature of your changes.

Ensure you leave your first assessor’s comments in your assignment, so your second assessor can see

the instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum

in your subject room.

Before you submit your assignment

If you have any queries about the assignment questions, please use the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer from your Tutor within 24 hours of posting your question.

Remember, your online tutor cannot preview or check your assignment answers, or provide specific

answer guidance. Please ensure that your questions are about clarification of the intent of an

assignment question.

After your assignment has been assessed

If you have questions about your assessor’s feedback, please email: <studentadviser@kaplan.edu.au>

and include a copy of your assessed assignment. Never post your assignment answers or assessor

comments in the ‘Ask Your Tutor’ forum.

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the

required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

When making changes to your original submission, use a different text colour for your resubmission.

This way, your assessor will be in a better position to gauge the quality and nature of your changes.

Ensure you leave your first assessor’s comments in your assignment, so your second assessor can see

the instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum

in your subject room.

Before you submit your assignment

If you have any queries about the assignment questions, please use the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer from your Tutor within 24 hours of posting your question.

Remember, your online tutor cannot preview or check your assignment answers, or provide specific

answer guidance. Please ensure that your questions are about clarification of the intent of an

assignment question.

After your assignment has been assessed

If you have questions about your assessor’s feedback, please email: <studentadviser@kaplan.edu.au>

and include a copy of your assessed assignment. Never post your assignment answers or assessor

comments in the ‘Ask Your Tutor’ forum.

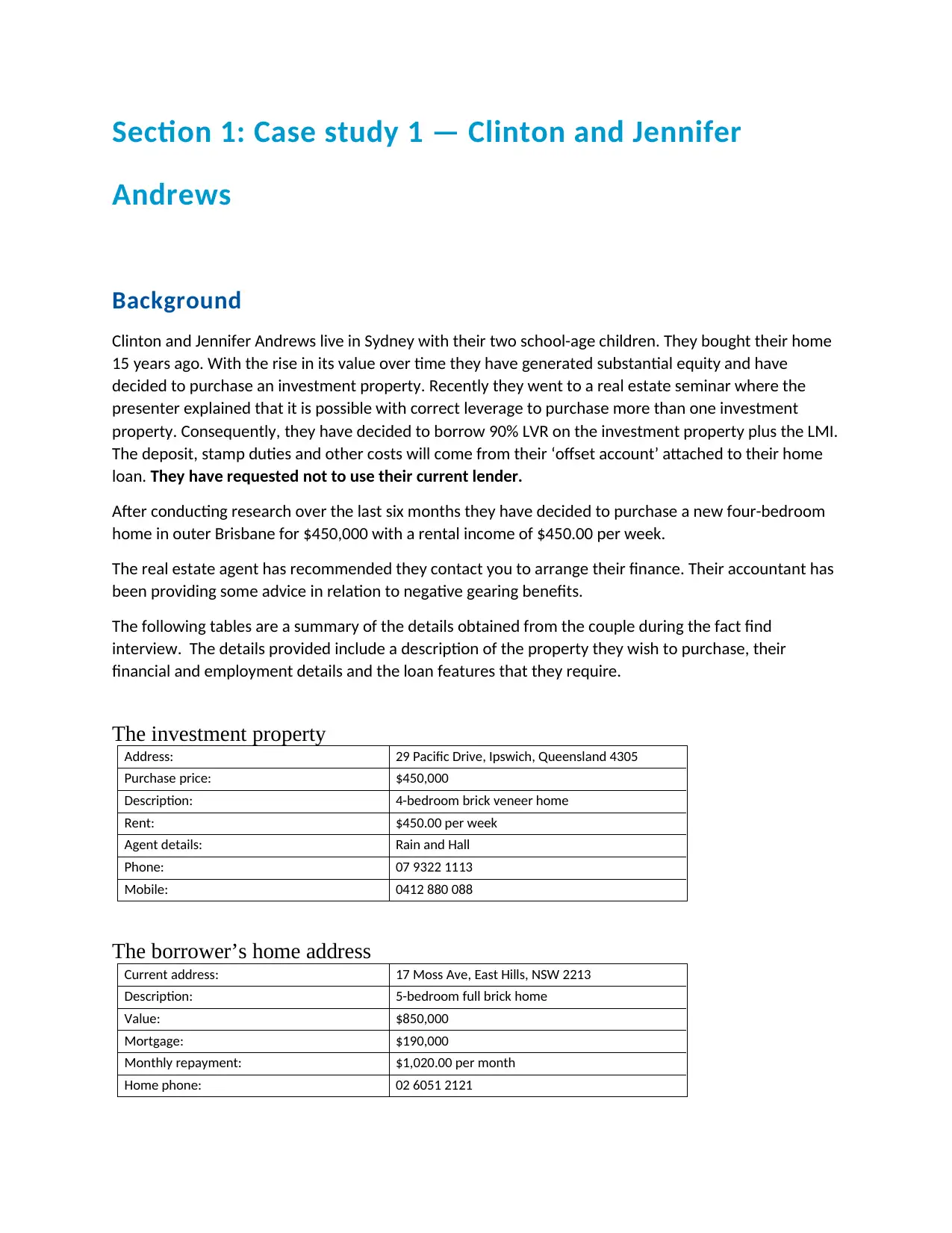

Section 1: Case study 1 — Clinton and Jennifer

Andrews

Background

Clinton and Jennifer Andrews live in Sydney with their two school-age children. They bought their home

15 years ago. With the rise in its value over time they have generated substantial equity and have

decided to purchase an investment property. Recently they went to a real estate seminar where the

presenter explained that it is possible with correct leverage to purchase more than one investment

property. Consequently, they have decided to borrow 90% LVR on the investment property plus the LMI.

The deposit, stamp duties and other costs will come from their ‘offset account’ attached to their home

loan. They have requested not to use their current lender.

After conducting research over the last six months they have decided to purchase a new four-bedroom

home in outer Brisbane for $450,000 with a rental income of $450.00 per week.

The real estate agent has recommended they contact you to arrange their finance. Their accountant has

been providing some advice in relation to negative gearing benefits.

The following tables are a summary of the details obtained from the couple during the fact find

interview. The details provided include a description of the property they wish to purchase, their

financial and employment details and the loan features that they require.

The investment property

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Purchase price: $450,000

Description: 4-bedroom brick veneer home

Rent: $450.00 per week

Agent details: Rain and Hall

Phone: 07 9322 1113

Mobile: 0412 880 088

The borrower’s home address

Current address: 17 Moss Ave, East Hills, NSW 2213

Description: 5-bedroom full brick home

Value: $850,000

Mortgage: $190,000

Monthly repayment: $1,020.00 per month

Home phone: 02 6051 2121

Andrews

Background

Clinton and Jennifer Andrews live in Sydney with their two school-age children. They bought their home

15 years ago. With the rise in its value over time they have generated substantial equity and have

decided to purchase an investment property. Recently they went to a real estate seminar where the

presenter explained that it is possible with correct leverage to purchase more than one investment

property. Consequently, they have decided to borrow 90% LVR on the investment property plus the LMI.

The deposit, stamp duties and other costs will come from their ‘offset account’ attached to their home

loan. They have requested not to use their current lender.

After conducting research over the last six months they have decided to purchase a new four-bedroom

home in outer Brisbane for $450,000 with a rental income of $450.00 per week.

The real estate agent has recommended they contact you to arrange their finance. Their accountant has

been providing some advice in relation to negative gearing benefits.

The following tables are a summary of the details obtained from the couple during the fact find

interview. The details provided include a description of the property they wish to purchase, their

financial and employment details and the loan features that they require.

The investment property

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Purchase price: $450,000

Description: 4-bedroom brick veneer home

Rent: $450.00 per week

Agent details: Rain and Hall

Phone: 07 9322 1113

Mobile: 0412 880 088

The borrower’s home address

Current address: 17 Moss Ave, East Hills, NSW 2213

Description: 5-bedroom full brick home

Value: $850,000

Mortgage: $190,000

Monthly repayment: $1,020.00 per month

Home phone: 02 6051 2121

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

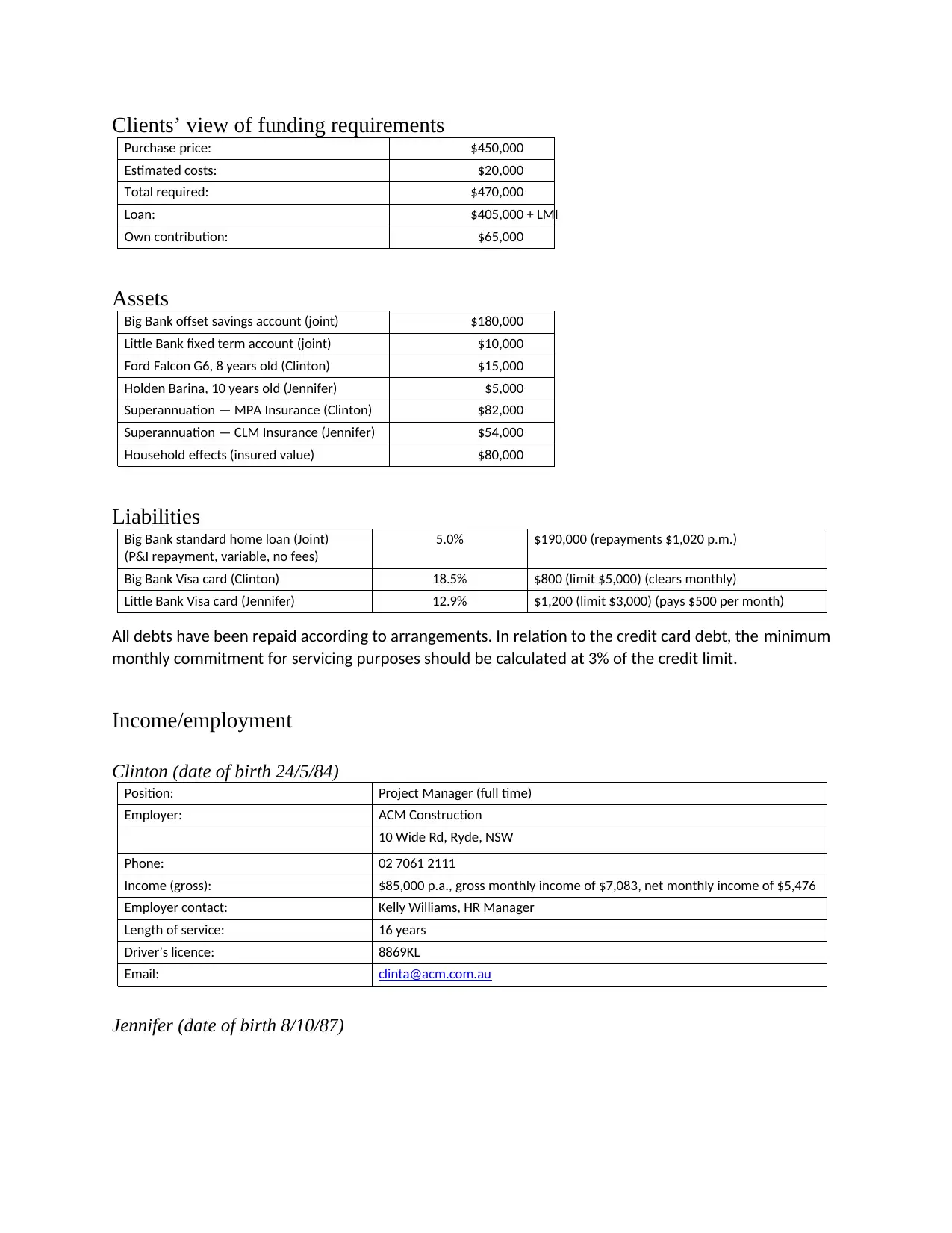

Clients’ view of funding requirements

Purchase price: $450,000

Estimated costs: $20,000

Total required: $470,000

Loan: $405,000 + LMI

Own contribution: $65,000

Assets

Big Bank offset savings account (joint) $180,000

Little Bank fixed term account (joint) $10,000

Ford Falcon G6, 8 years old (Clinton) $15,000

Holden Barina, 10 years old (Jennifer) $5,000

Superannuation — MPA Insurance (Clinton) $82,000

Superannuation — CLM Insurance (Jennifer) $54,000

Household effects (insured value) $80,000

Liabilities

Big Bank standard home loan (Joint)

(P&I repayment, variable, no fees)

5.0% $190,000 (repayments $1,020 p.m.)

Big Bank Visa card (Clinton) 18.5% $800 (limit $5,000) (clears monthly)

Little Bank Visa card (Jennifer) 12.9% $1,200 (limit $3,000) (pays $500 per month)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment for servicing purposes should be calculated at 3% of the credit limit.

Income/employment

Clinton (date of birth 24/5/84)

Position: Project Manager (full time)

Employer: ACM Construction

10 Wide Rd, Ryde, NSW

Phone: 02 7061 2111

Income (gross): $85,000 p.a., gross monthly income of $7,083, net monthly income of $5,476

Employer contact: Kelly Williams, HR Manager

Length of service: 16 years

Driver’s licence: 8869KL

Email: clinta@acm.com.au

Jennifer (date of birth 8/10/87)

Purchase price: $450,000

Estimated costs: $20,000

Total required: $470,000

Loan: $405,000 + LMI

Own contribution: $65,000

Assets

Big Bank offset savings account (joint) $180,000

Little Bank fixed term account (joint) $10,000

Ford Falcon G6, 8 years old (Clinton) $15,000

Holden Barina, 10 years old (Jennifer) $5,000

Superannuation — MPA Insurance (Clinton) $82,000

Superannuation — CLM Insurance (Jennifer) $54,000

Household effects (insured value) $80,000

Liabilities

Big Bank standard home loan (Joint)

(P&I repayment, variable, no fees)

5.0% $190,000 (repayments $1,020 p.m.)

Big Bank Visa card (Clinton) 18.5% $800 (limit $5,000) (clears monthly)

Little Bank Visa card (Jennifer) 12.9% $1,200 (limit $3,000) (pays $500 per month)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment for servicing purposes should be calculated at 3% of the credit limit.

Income/employment

Clinton (date of birth 24/5/84)

Position: Project Manager (full time)

Employer: ACM Construction

10 Wide Rd, Ryde, NSW

Phone: 02 7061 2111

Income (gross): $85,000 p.a., gross monthly income of $7,083, net monthly income of $5,476

Employer contact: Kelly Williams, HR Manager

Length of service: 16 years

Driver’s licence: 8869KL

Email: clinta@acm.com.au

Jennifer (date of birth 8/10/87)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

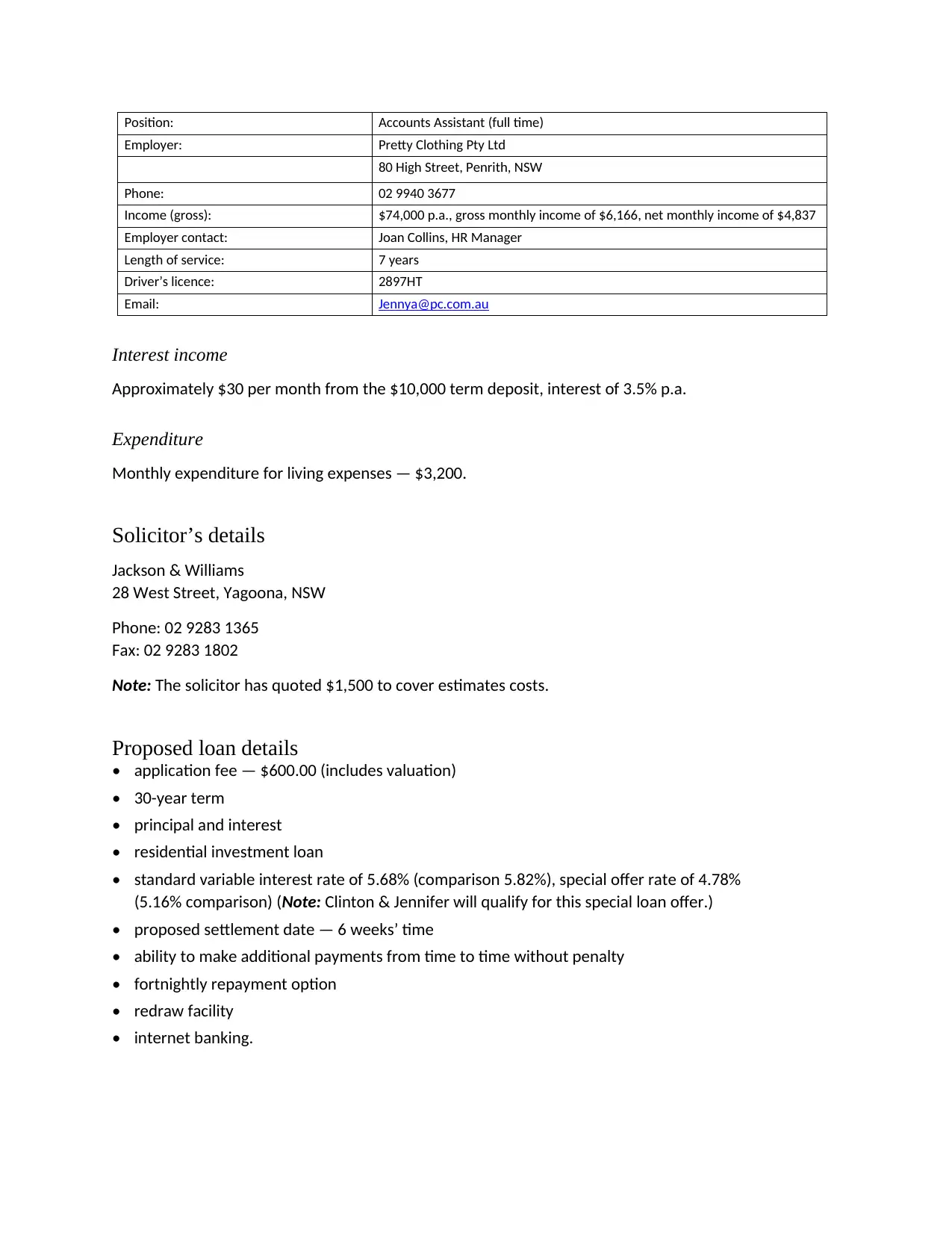

Position: Accounts Assistant (full time)

Employer: Pretty Clothing Pty Ltd

80 High Street, Penrith, NSW

Phone: 02 9940 3677

Income (gross): $74,000 p.a., gross monthly income of $6,166, net monthly income of $4,837

Employer contact: Joan Collins, HR Manager

Length of service: 7 years

Driver’s licence: 2897HT

Email: Jennya@pc.com.au

Interest income

Approximately $30 per month from the $10,000 term deposit, interest of 3.5% p.a.

Expenditure

Monthly expenditure for living expenses — $3,200.

Solicitor’s details

Jackson & Williams

28 West Street, Yagoona, NSW

Phone: 02 9283 1365

Fax: 02 9283 1802

Note: The solicitor has quoted $1,500 to cover estimates costs.

Proposed loan details

• application fee — $600.00 (includes valuation)

• 30-year term

• principal and interest

• residential investment loan

• standard variable interest rate of 5.68% (comparison 5.82%), special offer rate of 4.78%

(5.16% comparison) (Note: Clinton & Jennifer will qualify for this special loan offer.)

• proposed settlement date — 6 weeks’ time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• internet banking.

Employer: Pretty Clothing Pty Ltd

80 High Street, Penrith, NSW

Phone: 02 9940 3677

Income (gross): $74,000 p.a., gross monthly income of $6,166, net monthly income of $4,837

Employer contact: Joan Collins, HR Manager

Length of service: 7 years

Driver’s licence: 2897HT

Email: Jennya@pc.com.au

Interest income

Approximately $30 per month from the $10,000 term deposit, interest of 3.5% p.a.

Expenditure

Monthly expenditure for living expenses — $3,200.

Solicitor’s details

Jackson & Williams

28 West Street, Yagoona, NSW

Phone: 02 9283 1365

Fax: 02 9283 1802

Note: The solicitor has quoted $1,500 to cover estimates costs.

Proposed loan details

• application fee — $600.00 (includes valuation)

• 30-year term

• principal and interest

• residential investment loan

• standard variable interest rate of 5.68% (comparison 5.82%), special offer rate of 4.78%

(5.16% comparison) (Note: Clinton & Jennifer will qualify for this special loan offer.)

• proposed settlement date — 6 weeks’ time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• internet banking.

Assignment tasks (student to complete)

Task 1 — Initial disclosures

Following a personal introduction and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker.

These disclosures include the way you are remunerated and the range and limitation of your services.

1. There are four (4) documents listed in ASIC Information sheet INFO 146 ‘Responsible lending

disclosure obligations – Overview for credit licensees and representatives’ that must be provided to

customers. Refer to this Information sheet and the information contained in your topic notes to

answer part (a) and (b) below.

(a) Identify which of these four (4) documents you must provide your client before

you commence providing credit assistance and explain the main disclosures relevant to that

document. (40 words)

Student response to Task 1: Question 1(a)

Before commencing the provision of credit assistance to the client the documents which must be

provided to the client under National Consumer Credit Protection Act 2009 (National Credit Act) are

pointed out below:

The document for proposal and the disclosure made under section 144 and 121.

The quote and disclosure made under section 137 and 114.

The credit guide and disclosure under section 136 and 113.

Disclosure of preliminary assessment and written assessment under section 143 and section

120.

(b) Identify which of these four documents you will provide the client should you

intend to charge a broker fee and explain what is required for it to be valid. (40 words)

Student response to Task 1: Question 1(b)

For charging a brokerage fees from the client while providing credit assistance it is mandatory to

provide credit guide document to the client. In order to validate that document it is necessary to

make disclosure under section 158 of National Consumer Credit Protection Act 2009 (National

Credit Act).

Assessor feedback: Resubmission required?

Task 1 — Initial disclosures

Following a personal introduction and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker.

These disclosures include the way you are remunerated and the range and limitation of your services.

1. There are four (4) documents listed in ASIC Information sheet INFO 146 ‘Responsible lending

disclosure obligations – Overview for credit licensees and representatives’ that must be provided to

customers. Refer to this Information sheet and the information contained in your topic notes to

answer part (a) and (b) below.

(a) Identify which of these four (4) documents you must provide your client before

you commence providing credit assistance and explain the main disclosures relevant to that

document. (40 words)

Student response to Task 1: Question 1(a)

Before commencing the provision of credit assistance to the client the documents which must be

provided to the client under National Consumer Credit Protection Act 2009 (National Credit Act) are

pointed out below:

The document for proposal and the disclosure made under section 144 and 121.

The quote and disclosure made under section 137 and 114.

The credit guide and disclosure under section 136 and 113.

Disclosure of preliminary assessment and written assessment under section 143 and section

120.

(b) Identify which of these four documents you will provide the client should you

intend to charge a broker fee and explain what is required for it to be valid. (40 words)

Student response to Task 1: Question 1(b)

For charging a brokerage fees from the client while providing credit assistance it is mandatory to

provide credit guide document to the client. In order to validate that document it is necessary to

make disclosure under section 158 of National Consumer Credit Protection Act 2009 (National

Credit Act).

Assessor feedback: Resubmission required?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 55

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.