Challenger Limited: A Comprehensive Analysis of Financial Reporting Practices

VerifiedAdded on 2024/05/31

|9

|2168

|499

AI Summary

This report provides a detailed analysis of Challenger Limited's financial reporting practices, focusing on contingencies, provisions, leased items, and asset valuation. It examines the criteria and measurements used for provisions and contingencies, presents an argument for and against the inclusion of Parent Entity Guarantees and Undertakings, and discusses the classification and presentation requirements for leased items. The report also explores a hypothetical situation for reclassifying leased assets and analyzes the valuation method used for non-current assets, proposing an alternative approach. This comprehensive analysis aims to provide insights into Challenger Limited's financial reporting practices and their impact on the company's overall financial performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TASK2: CHALLENGER LIMITED

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction......................................................................................................................................2

1. Providing details of the contingencies and provisions disclosed.................................................3

2. Discussing the criteria and Measurements for the Provisions and Contingencies......................3

3. Providing an debatary argument on Contingency.......................................................................3

4. Details of Leased Items of the Company.....................................................................................4

5. Discussion on the classification and presentation Requirement Relevant to The Leased Items. 4

6. Explanation and identification of the hypothetical Situation for further reclassification of the

leased asset.......................................................................................................................................5

7. Selection of the nation Current Asset Of the Company and Valuation Method used for it........5

8. Alternative Valuation Method.....................................................................................................6

Conclusion.......................................................................................................................................6

References:......................................................................................................................................7

2

Introduction......................................................................................................................................2

1. Providing details of the contingencies and provisions disclosed.................................................3

2. Discussing the criteria and Measurements for the Provisions and Contingencies......................3

3. Providing an debatary argument on Contingency.......................................................................3

4. Details of Leased Items of the Company.....................................................................................4

5. Discussion on the classification and presentation Requirement Relevant to The Leased Items. 4

6. Explanation and identification of the hypothetical Situation for further reclassification of the

leased asset.......................................................................................................................................5

7. Selection of the nation Current Asset Of the Company and Valuation Method used for it........5

8. Alternative Valuation Method.....................................................................................................6

Conclusion.......................................................................................................................................6

References:......................................................................................................................................7

2

Introduction

In the era of globalization, the accuracy and transparency form the twin factors that augment the

process of attaining higher competitive edge in long run. Challenger Limited is a listed company

on the Australian Securities Exchange (ASE) that follows the rules of the Australian Prudential

Regulation Authority (APRA). Analyzing the provisions along with the contingencies of the

company and renewing its criteria while checking its measures, will build up the first part of the

report. An argument will be provided for and against demonstrating one of the contingencies of

the company has been mentioned in the report. Details on the leased items of the company will

be given and its classification will also be discussed. Choosing a hypothetical situation of

reclassified leased item and discussion on it will be provided. The valuation method used by the

company for its non-current asset and an alternative to it will be provided at the end of the report.

3

In the era of globalization, the accuracy and transparency form the twin factors that augment the

process of attaining higher competitive edge in long run. Challenger Limited is a listed company

on the Australian Securities Exchange (ASE) that follows the rules of the Australian Prudential

Regulation Authority (APRA). Analyzing the provisions along with the contingencies of the

company and renewing its criteria while checking its measures, will build up the first part of the

report. An argument will be provided for and against demonstrating one of the contingencies of

the company has been mentioned in the report. Details on the leased items of the company will

be given and its classification will also be discussed. Choosing a hypothetical situation of

reclassified leased item and discussion on it will be provided. The valuation method used by the

company for its non-current asset and an alternative to it will be provided at the end of the report.

3

1. Providing details of the contingencies and provisions disclosed

The contingencies and the provisions provided by the Challenger group have been always

employee and company friendly. The Retirement Income Plan was one of the contingencies of

the company which would help to increase the standard of the Australian Retirees. A broader and

wider aspect of retirement income solutions was planned in FY2017 of the company, which was

for the oldies of the country. This contingency disclosure has increased the efficiency along with

market leading cost to income ratio. A retirement illustrator was launched in order to deliver

quality services, known as the retirement tool. The Parent Entity Guarantees and Undertakings

included a guarantee which supports the corporate banking facilities. Some of the Financial

commitments say, hedging arrangements were also supported. A Third Party Guarantees, say

bank guarantee could be issued by the third party financial institutions representing the group

along with its subsidiaries (Challenger.com, 2018). This comes under the contingency of the

company, named as Contingent Future Commitments. The guarantee of its subsidiaries has been

taken by the CLC and the third parties has assured of their extraordinary performance. Assets

pledged as collateral, the company planned to provide collateral in order to secure liabilities.

This has been done in favor of the counterparties.

2. Discussing the criteria and Measurements for the Provisions and Contingencies

The contingencies should always be separated from the critical contingencies to the non critical

ones. Under the critical contingency, there shouldn’t exist any false alarm, on the basis of the

magnitude of the contingency measure. An occurrence of any misclassification in the critical

contingency and has no thermal or voltage limit violations carries a small measure and then the

contingency is not considered to be critical (Challenger.com, 2018). The contingencies of a

company should be framed in such a manner that anyone connected to the company receives a

benefit out of it. Therefore, this has been done by the Challenger Limited group.

3. Providing an debatary argument on Contingency

The inclusion of Parent Entity Guarantees and Undertakings in the financial report of the

company can be quite argumentative. As the mentioned the contingency provides letters of

support to its subsidiaries, in the day to day business (Hussey, et al. 2018, p.67). The intention of

supporting the subsidiaries is clearly stated in the letter and this would help them to continue in

4

The contingencies and the provisions provided by the Challenger group have been always

employee and company friendly. The Retirement Income Plan was one of the contingencies of

the company which would help to increase the standard of the Australian Retirees. A broader and

wider aspect of retirement income solutions was planned in FY2017 of the company, which was

for the oldies of the country. This contingency disclosure has increased the efficiency along with

market leading cost to income ratio. A retirement illustrator was launched in order to deliver

quality services, known as the retirement tool. The Parent Entity Guarantees and Undertakings

included a guarantee which supports the corporate banking facilities. Some of the Financial

commitments say, hedging arrangements were also supported. A Third Party Guarantees, say

bank guarantee could be issued by the third party financial institutions representing the group

along with its subsidiaries (Challenger.com, 2018). This comes under the contingency of the

company, named as Contingent Future Commitments. The guarantee of its subsidiaries has been

taken by the CLC and the third parties has assured of their extraordinary performance. Assets

pledged as collateral, the company planned to provide collateral in order to secure liabilities.

This has been done in favor of the counterparties.

2. Discussing the criteria and Measurements for the Provisions and Contingencies

The contingencies should always be separated from the critical contingencies to the non critical

ones. Under the critical contingency, there shouldn’t exist any false alarm, on the basis of the

magnitude of the contingency measure. An occurrence of any misclassification in the critical

contingency and has no thermal or voltage limit violations carries a small measure and then the

contingency is not considered to be critical (Challenger.com, 2018). The contingencies of a

company should be framed in such a manner that anyone connected to the company receives a

benefit out of it. Therefore, this has been done by the Challenger Limited group.

3. Providing an debatary argument on Contingency

The inclusion of Parent Entity Guarantees and Undertakings in the financial report of the

company can be quite argumentative. As the mentioned the contingency provides letters of

support to its subsidiaries, in the day to day business (Hussey, et al. 2018, p.67). The intention of

supporting the subsidiaries is clearly stated in the letter and this would help them to continue in

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

meeting their obligations. This shows the supporting nature of Challenger Limited and the belief

the company has on its subsidiaries. This may give the company a better and fruitful result at the

end. As everything has other side to it, the contingency carries some drawbacks along with its

positivity (Chen, et al. 2015, p.566). If for any reason the subsidiary company fails to deliver the

desired results, the parent company’s image and goodwill will deteriorate as it has acted as a

guarantor of the subsidiary company. The loss would be huge and the parent company would

have to spend years on rebuilding the trust of its customers and employees on failure of the

subsidiary company.

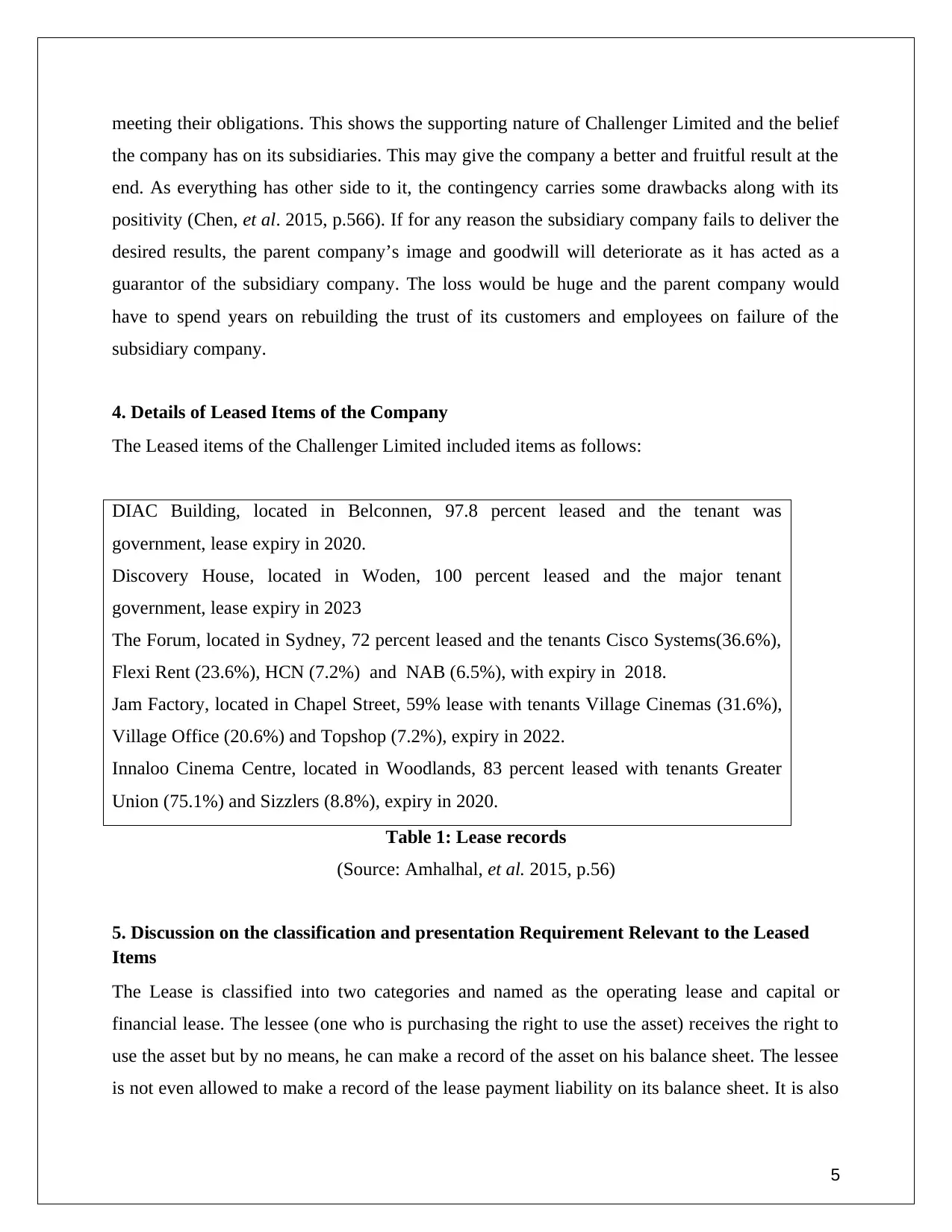

4. Details of Leased Items of the Company

The Leased items of the Challenger Limited included items as follows:

DIAC Building, located in Belconnen, 97.8 percent leased and the tenant was

government, lease expiry in 2020.

Discovery House, located in Woden, 100 percent leased and the major tenant

government, lease expiry in 2023

The Forum, located in Sydney, 72 percent leased and the tenants Cisco Systems(36.6%),

Flexi Rent (23.6%), HCN (7.2%) and NAB (6.5%), with expiry in 2018.

Jam Factory, located in Chapel Street, 59% lease with tenants Village Cinemas (31.6%),

Village Office (20.6%) and Topshop (7.2%), expiry in 2022.

Innaloo Cinema Centre, located in Woodlands, 83 percent leased with tenants Greater

Union (75.1%) and Sizzlers (8.8%), expiry in 2020.

Table 1: Lease records

(Source: Amhalhal, et al. 2015, p.56)

5. Discussion on the classification and presentation Requirement Relevant to the Leased

Items

The Lease is classified into two categories and named as the operating lease and capital or

financial lease. The lessee (one who is purchasing the right to use the asset) receives the right to

use the asset but by no means, he can make a record of the asset on his balance sheet. The lessee

is not even allowed to make a record of the lease payment liability on its balance sheet. It is also

5

the company has on its subsidiaries. This may give the company a better and fruitful result at the

end. As everything has other side to it, the contingency carries some drawbacks along with its

positivity (Chen, et al. 2015, p.566). If for any reason the subsidiary company fails to deliver the

desired results, the parent company’s image and goodwill will deteriorate as it has acted as a

guarantor of the subsidiary company. The loss would be huge and the parent company would

have to spend years on rebuilding the trust of its customers and employees on failure of the

subsidiary company.

4. Details of Leased Items of the Company

The Leased items of the Challenger Limited included items as follows:

DIAC Building, located in Belconnen, 97.8 percent leased and the tenant was

government, lease expiry in 2020.

Discovery House, located in Woden, 100 percent leased and the major tenant

government, lease expiry in 2023

The Forum, located in Sydney, 72 percent leased and the tenants Cisco Systems(36.6%),

Flexi Rent (23.6%), HCN (7.2%) and NAB (6.5%), with expiry in 2018.

Jam Factory, located in Chapel Street, 59% lease with tenants Village Cinemas (31.6%),

Village Office (20.6%) and Topshop (7.2%), expiry in 2022.

Innaloo Cinema Centre, located in Woodlands, 83 percent leased with tenants Greater

Union (75.1%) and Sizzlers (8.8%), expiry in 2020.

Table 1: Lease records

(Source: Amhalhal, et al. 2015, p.56)

5. Discussion on the classification and presentation Requirement Relevant to the Leased

Items

The Lease is classified into two categories and named as the operating lease and capital or

financial lease. The lessee (one who is purchasing the right to use the asset) receives the right to

use the asset but by no means, he can make a record of the asset on his balance sheet. The lessee

is not even allowed to make a record of the lease payment liability on its balance sheet. It is also

5

known as "off-balance sheet financing" (Lin, et al. 2017, p.127). Only in the Income statement,

the lessee is allowed to make a record of the lease payment as a rental expense. It can either be

placed under a cost of goods sold or under SG&A. The other classification is capital or finance

lease where the lessee enjoys all the rights to use the asset and explore its risks along with its

benefits of owning the asset. In this case, the lessee records the leased asset on the company

balance sheet. Challenger Limited uses the capital or finance lease and thus enjoys all the

benefits of the system. The company gets benefits of earning goodwill in the market through the

use of capital or finance lease.

6. Explanation and identification of the hypothetical Situation for further reclassification of

the leased asset

A situation may arise up in a company that a need for the reclassification of the lease occurs . It

may so happen that for some of the properties which have been previously classified as finance

leases, the land may be reclassified as the operating lease and the building elements may be

reclassified as finance lease (Hussey, et al. 20167, p.23). This is done when the land has an

indefinite economic life then it is classified as an operating lease. It has been observed that the

land is on a normal basis classified as an operating lease on a condition that the title is expected

to pass to the lessee on the termination of the lease.

7. Selection of the nation Current Asset Of the Company and Valuation Method used for it

Property, Plants and Equipment have been identified as the non-current assets of the company.

The valuation method used for this asset valuation is the Discounted Cash Flow Method. Under

this method, an assumption about the cash flow is done which the company is expected to

generate in the future. The origination of these cash flows in the operational results, even from

the mutations in working capital, fixed assets and provisions are seen. The projection of the cash

flows is done on the basis of "weighted average cost of capital" (Joubert, et al. 2017, p.1). The

weakness or drawback of the discounted cash flow method is that it includes the “cost of

capital”.

6

the lessee is allowed to make a record of the lease payment as a rental expense. It can either be

placed under a cost of goods sold or under SG&A. The other classification is capital or finance

lease where the lessee enjoys all the rights to use the asset and explore its risks along with its

benefits of owning the asset. In this case, the lessee records the leased asset on the company

balance sheet. Challenger Limited uses the capital or finance lease and thus enjoys all the

benefits of the system. The company gets benefits of earning goodwill in the market through the

use of capital or finance lease.

6. Explanation and identification of the hypothetical Situation for further reclassification of

the leased asset

A situation may arise up in a company that a need for the reclassification of the lease occurs . It

may so happen that for some of the properties which have been previously classified as finance

leases, the land may be reclassified as the operating lease and the building elements may be

reclassified as finance lease (Hussey, et al. 20167, p.23). This is done when the land has an

indefinite economic life then it is classified as an operating lease. It has been observed that the

land is on a normal basis classified as an operating lease on a condition that the title is expected

to pass to the lessee on the termination of the lease.

7. Selection of the nation Current Asset Of the Company and Valuation Method used for it

Property, Plants and Equipment have been identified as the non-current assets of the company.

The valuation method used for this asset valuation is the Discounted Cash Flow Method. Under

this method, an assumption about the cash flow is done which the company is expected to

generate in the future. The origination of these cash flows in the operational results, even from

the mutations in working capital, fixed assets and provisions are seen. The projection of the cash

flows is done on the basis of "weighted average cost of capital" (Joubert, et al. 2017, p.1). The

weakness or drawback of the discounted cash flow method is that it includes the “cost of

capital”.

6

8. Alternative Valuation Method

Appraisal Method is known for calculating the fair market price of the asset. Generally, an

appraiser gets hired to determine the value of each item worth company's balance sheet. The in-

house assets are assessed through its current condition and a consideration of the wear and tear of

the asset is done and the degree of obsolescence is also considered. Then a comparison is made

with the other assets and its current value in the market is determined. This method is more

reliable than the discounted cash flow method, which the Challenger Limited has used because

the former method provides the actual current value of the assets. In the discounted cash flow the

inclusion of the “cost of capital”, makes the picture or the value of the asset a bit clumsy and

difficult to understand (He, et al. 2016, p.330). The clarity of the financial statements helps the

investors to understand the company laws and current market status well, which builds up trust

and goodwill of the company.

7

Appraisal Method is known for calculating the fair market price of the asset. Generally, an

appraiser gets hired to determine the value of each item worth company's balance sheet. The in-

house assets are assessed through its current condition and a consideration of the wear and tear of

the asset is done and the degree of obsolescence is also considered. Then a comparison is made

with the other assets and its current value in the market is determined. This method is more

reliable than the discounted cash flow method, which the Challenger Limited has used because

the former method provides the actual current value of the assets. In the discounted cash flow the

inclusion of the “cost of capital”, makes the picture or the value of the asset a bit clumsy and

difficult to understand (He, et al. 2016, p.330). The clarity of the financial statements helps the

investors to understand the company laws and current market status well, which builds up trust

and goodwill of the company.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

The Australian Accounting Standard Board (AASB), functions as per the regulations provided

by the Australian Securities and Investments Commission Act, 2001. Challenger Limited has

overall worked in favor of its investors and customers. The mere analysis of its accounting part

and the descriptions given in the annual report creates a clear picture and standard of the

company. Providing an alternative method for valuation and an argument for the contingencies

has actually made the assignment quite interesting and effective.

8

The Australian Accounting Standard Board (AASB), functions as per the regulations provided

by the Australian Securities and Investments Commission Act, 2001. Challenger Limited has

overall worked in favor of its investors and customers. The mere analysis of its accounting part

and the descriptions given in the annual report creates a clear picture and standard of the

company. Providing an alternative method for valuation and an argument for the contingencies

has actually made the assignment quite interesting and effective.

8

References:

Amalia, A.M.A., Anchor, J.R. and Dastgir, S., (2015). The effectiveness of the use of multiple

performance measures: the influence of organisational contingencies.

Challenger.com (2018) Annual report Available at:

https://www.challenger.com.au/group/CompanyAnnouncements/Challenger_welcomes_new_fra

mework_for_retirement_income.pdf [Accessed on May 20th, 2018]

Challenger.com (2018) News Available at:

https://www.challenger.com.au/group/Interim_Financial_Report_2018.pdf [Accessed on May

20th, 2018]

Chen, S.C. and Teng, J.T., (2015). Inventory and credit decisions for time-varying deteriorating

items with up-stream and down-stream trade credit financing by discounted cash flow analysis.

European Journal of Operational Research, 243(2), pp.566-575.

He, L., Evans, E. and He, R., (2016). The Impact of AASB 8 Operating Segments on Analysts’

Earnings Forecasts: Australian Evidence. Australian Accounting Review, 26(4), pp.330-340.

Hussey, R., (2017), May. Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Hussey, R., (2018). Accounting for Leases and the Failure of Convergence, pp.23.

Joubert, M., Garvie, L. and Parle, G., (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Lin, K.C. and Graham, R.C., (2017). How Will the New Lease Accounting Standard Affect the

Relevance of Lease Asset Accounting?,pp.127.

9

Amalia, A.M.A., Anchor, J.R. and Dastgir, S., (2015). The effectiveness of the use of multiple

performance measures: the influence of organisational contingencies.

Challenger.com (2018) Annual report Available at:

https://www.challenger.com.au/group/CompanyAnnouncements/Challenger_welcomes_new_fra

mework_for_retirement_income.pdf [Accessed on May 20th, 2018]

Challenger.com (2018) News Available at:

https://www.challenger.com.au/group/Interim_Financial_Report_2018.pdf [Accessed on May

20th, 2018]

Chen, S.C. and Teng, J.T., (2015). Inventory and credit decisions for time-varying deteriorating

items with up-stream and down-stream trade credit financing by discounted cash flow analysis.

European Journal of Operational Research, 243(2), pp.566-575.

He, L., Evans, E. and He, R., (2016). The Impact of AASB 8 Operating Segments on Analysts’

Earnings Forecasts: Australian Evidence. Australian Accounting Review, 26(4), pp.330-340.

Hussey, R., (2017), May. Leasing of Assets: A Content Analysis of Comment. In GAI

International Academic Conferences Proceedings (p. 23).

Hussey, R., (2018). Accounting for Leases and the Failure of Convergence, pp.23.

Joubert, M., Garvie, L. and Parle, G., (2017). Implications of the New Accounting Standard for

Leases AASB 16 (IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. The

Journal of New Business Ideas & Trends, 15(2), pp.1-11.

Lin, K.C. and Graham, R.C., (2017). How Will the New Lease Accounting Standard Affect the

Relevance of Lease Asset Accounting?,pp.127.

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.