Comprehensive Financial Accounting Assignment Solution, Analysis

VerifiedAdded on 2023/06/07

|17

|2898

|275

Homework Assignment

AI Summary

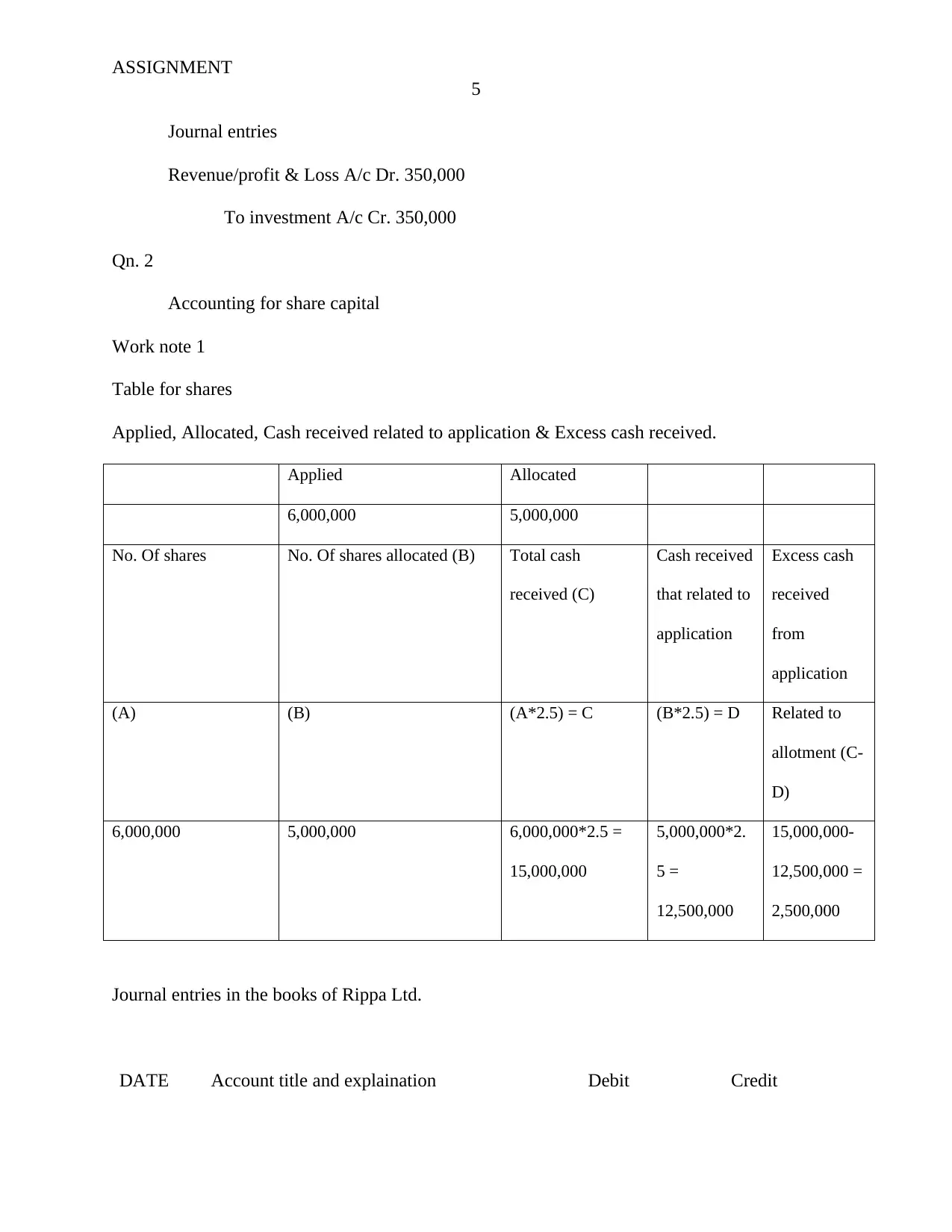

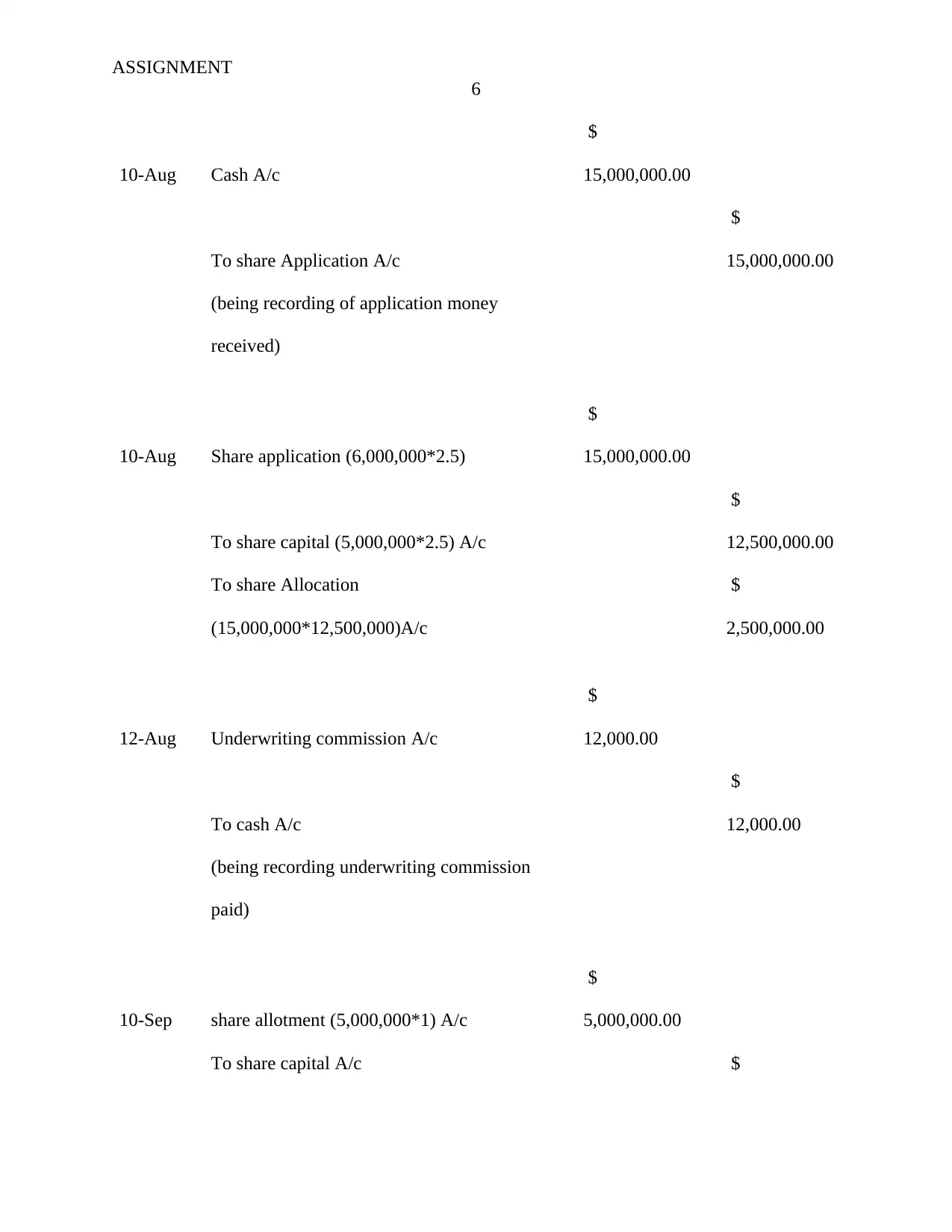

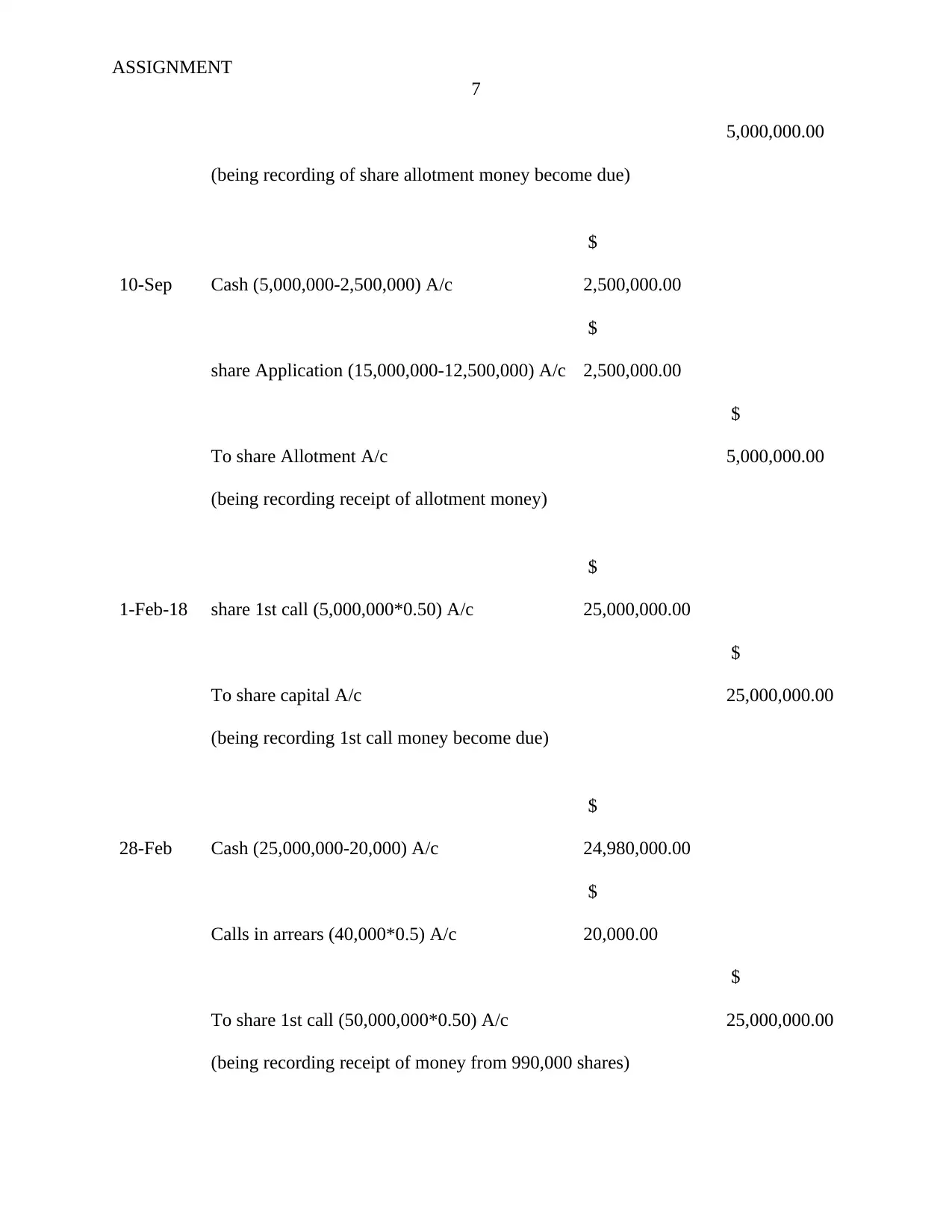

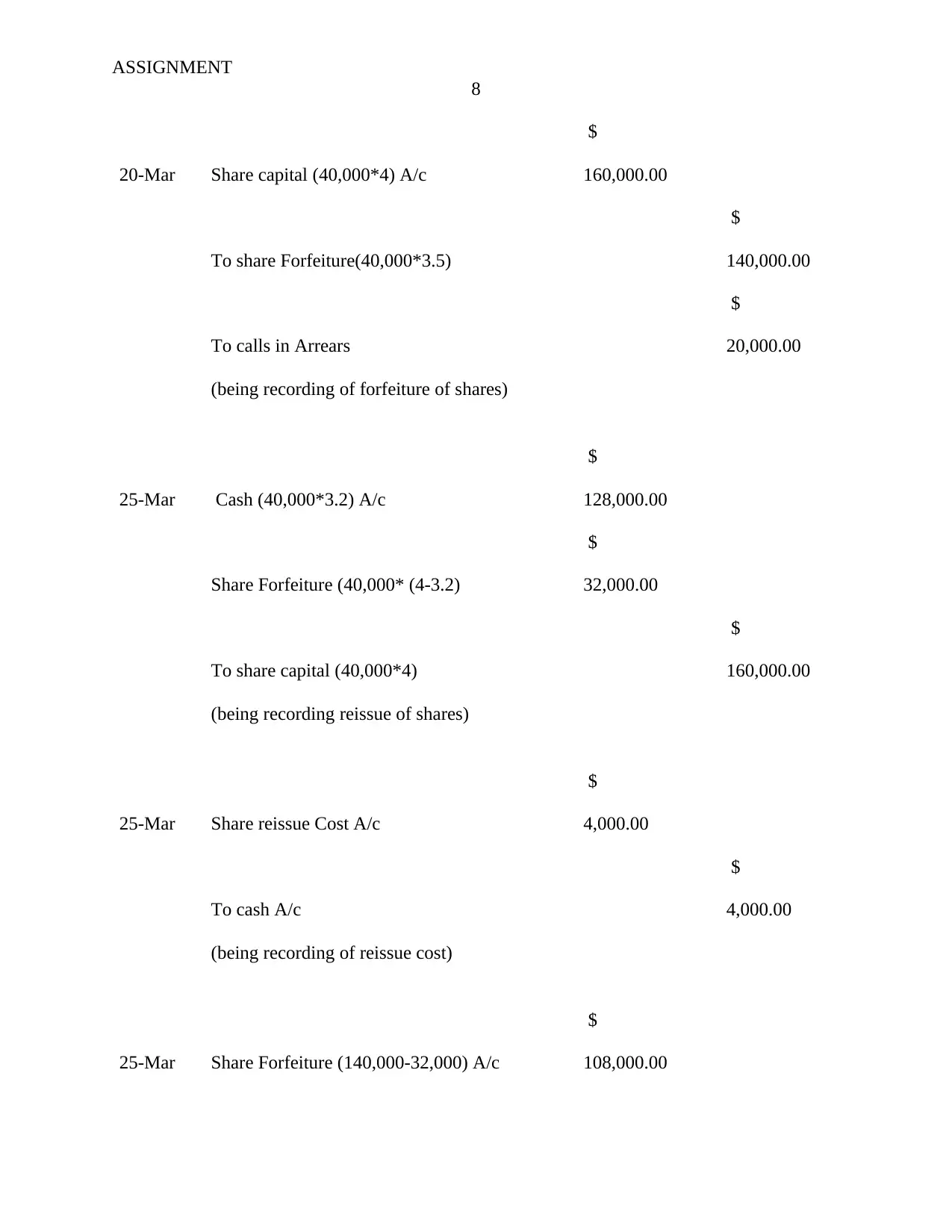

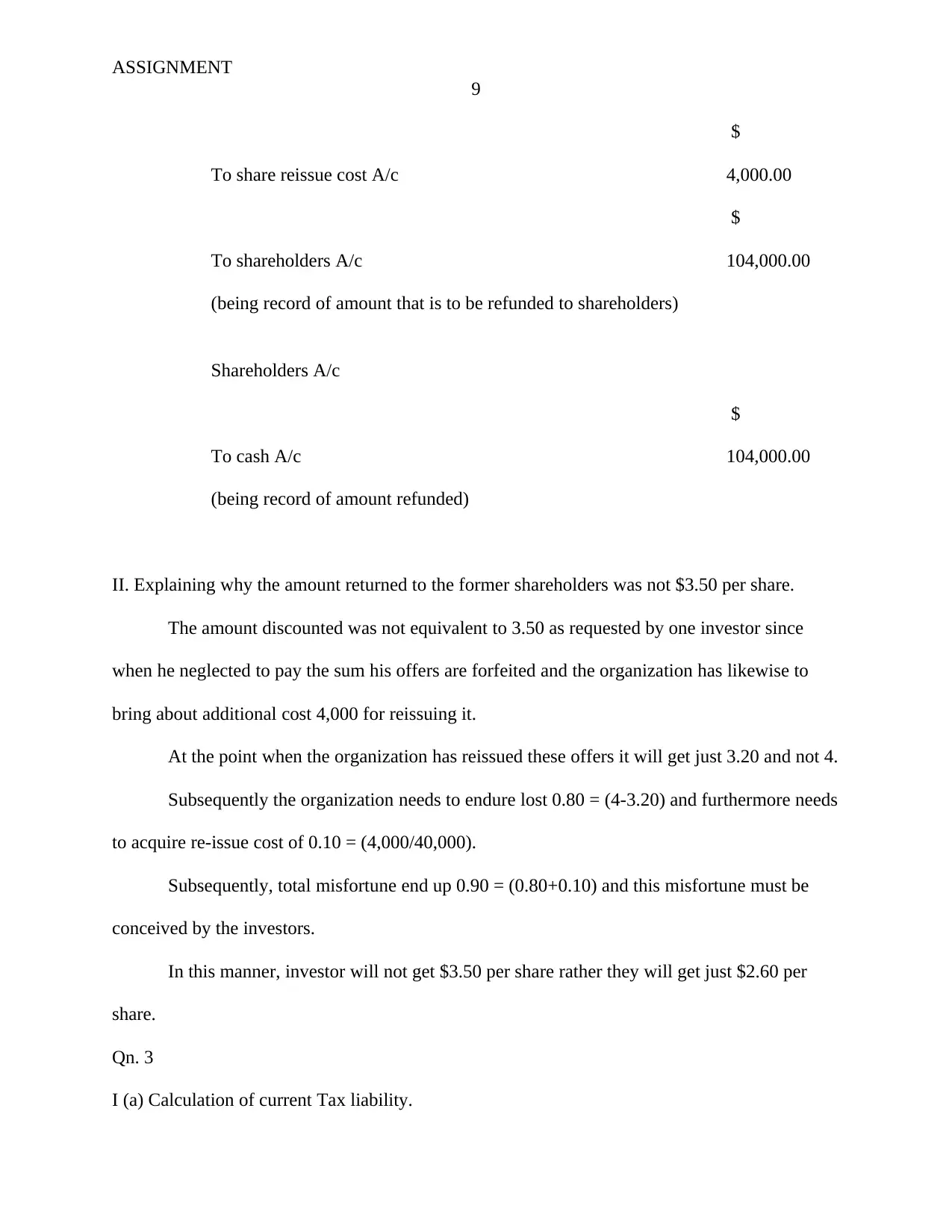

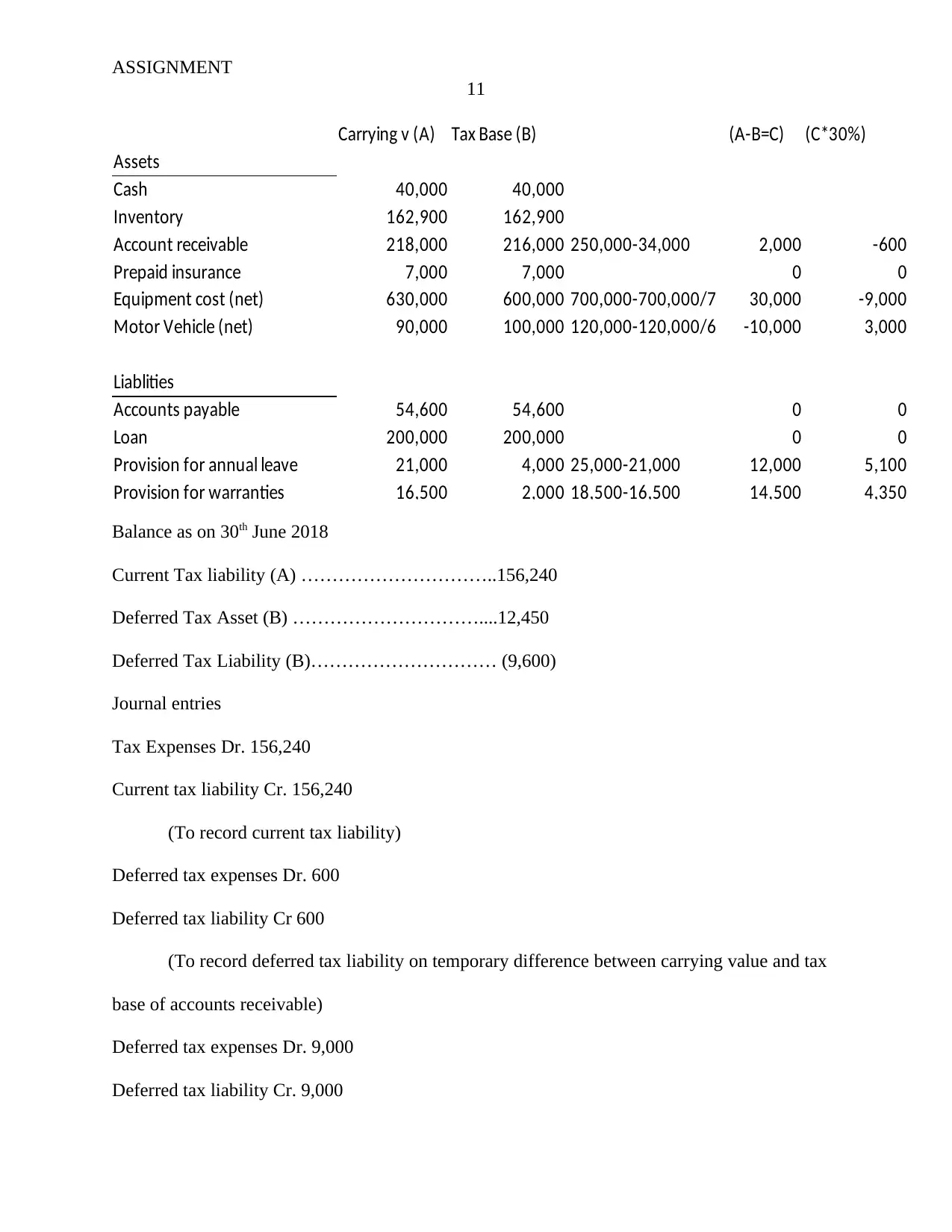

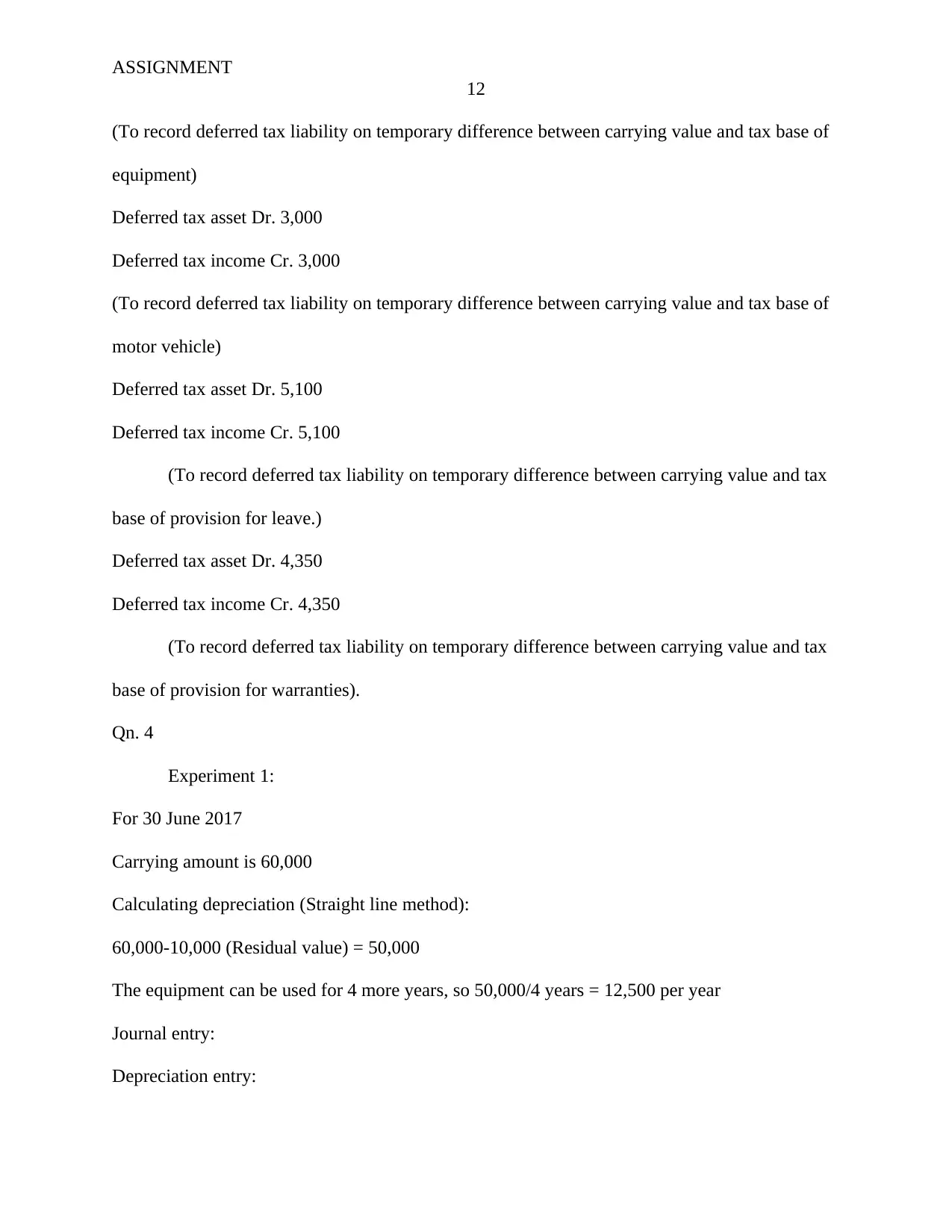

This document provides a comprehensive solution to a financial accounting assignment, addressing key areas such as changes in accounting standards by the IASB (International Accounting Standards Board) including measurement, presentation, disclosure, and definitions of assets and liabilities. The solution includes detailed calculations for depreciation, adjustments, and share capital accounting, with corresponding journal entries. It also covers current and deferred tax liability calculations, along with journal entries, and provides examples of asset revaluation with associated journal entries. The assignment assesses the student's ability to apply accounting principles to various scenarios, including share capital, depreciation, and tax-related computations, and to prepare appropriate journal entries to reflect the accounting treatment of different transactions and events.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.