Journal Entries for Financing Company Operations, Property Plant and Equipment, Lease, and Intangible Assets

VerifiedAdded on 2023/01/19

|13

|1975

|26

AI Summary

This document provides journal entries for various scenarios including financing company operations, property plant and equipment, lease, and intangible assets. It includes detailed explanations and examples.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

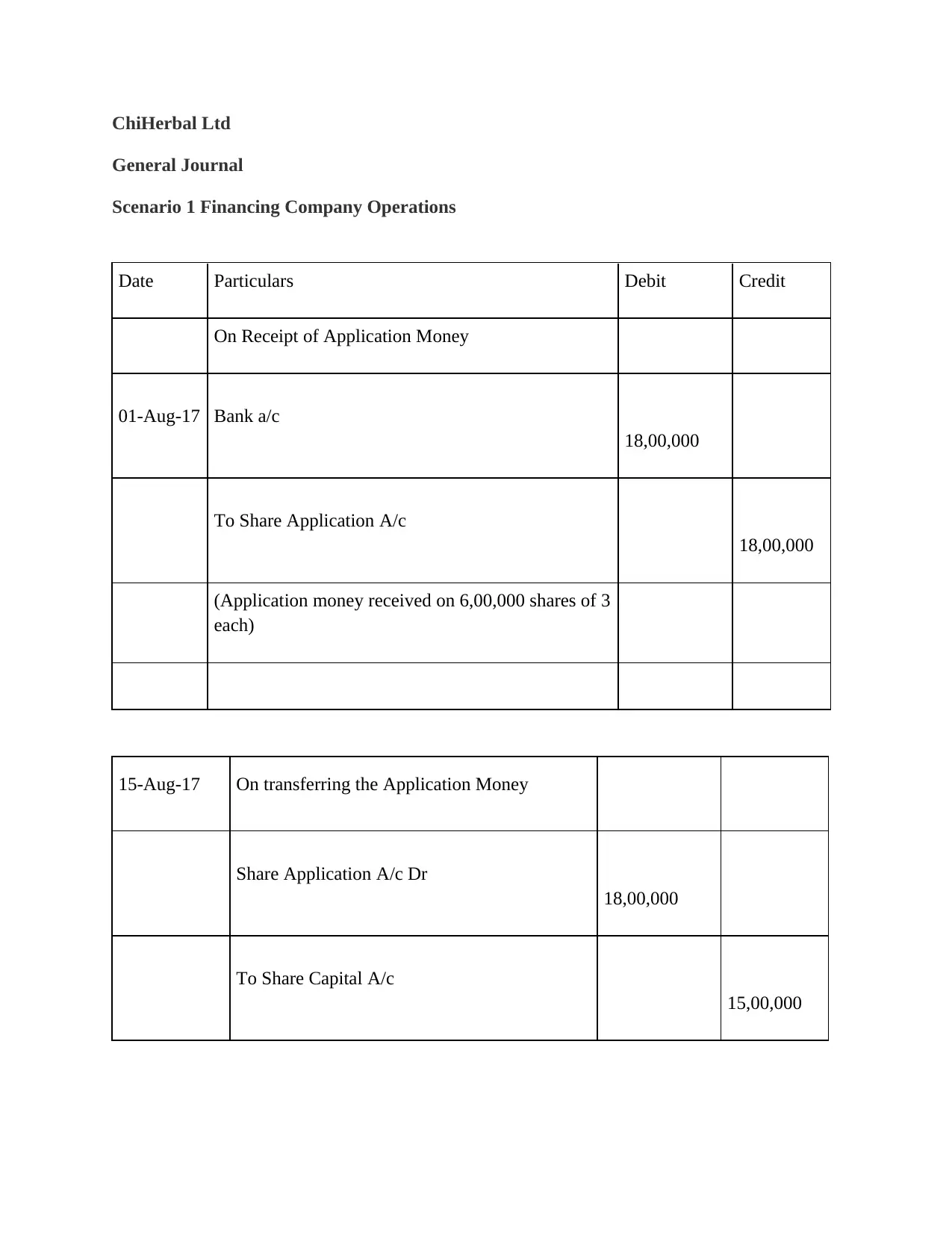

ChiHerbal Ltd

General Journal

Scenario 1 Financing Company Operations

Date Particulars Debit Credit

On Receipt of Application Money

01-Aug-17 Bank a/c

18,00,000

To Share Application A/c

18,00,000

(Application money received on 6,00,000 shares of 3

each)

15-Aug-17 On transferring the Application Money

Share Application A/c Dr

18,00,000

To Share Capital A/c

15,00,000

General Journal

Scenario 1 Financing Company Operations

Date Particulars Debit Credit

On Receipt of Application Money

01-Aug-17 Bank a/c

18,00,000

To Share Application A/c

18,00,000

(Application money received on 6,00,000 shares of 3

each)

15-Aug-17 On transferring the Application Money

Share Application A/c Dr

18,00,000

To Share Capital A/c

15,00,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

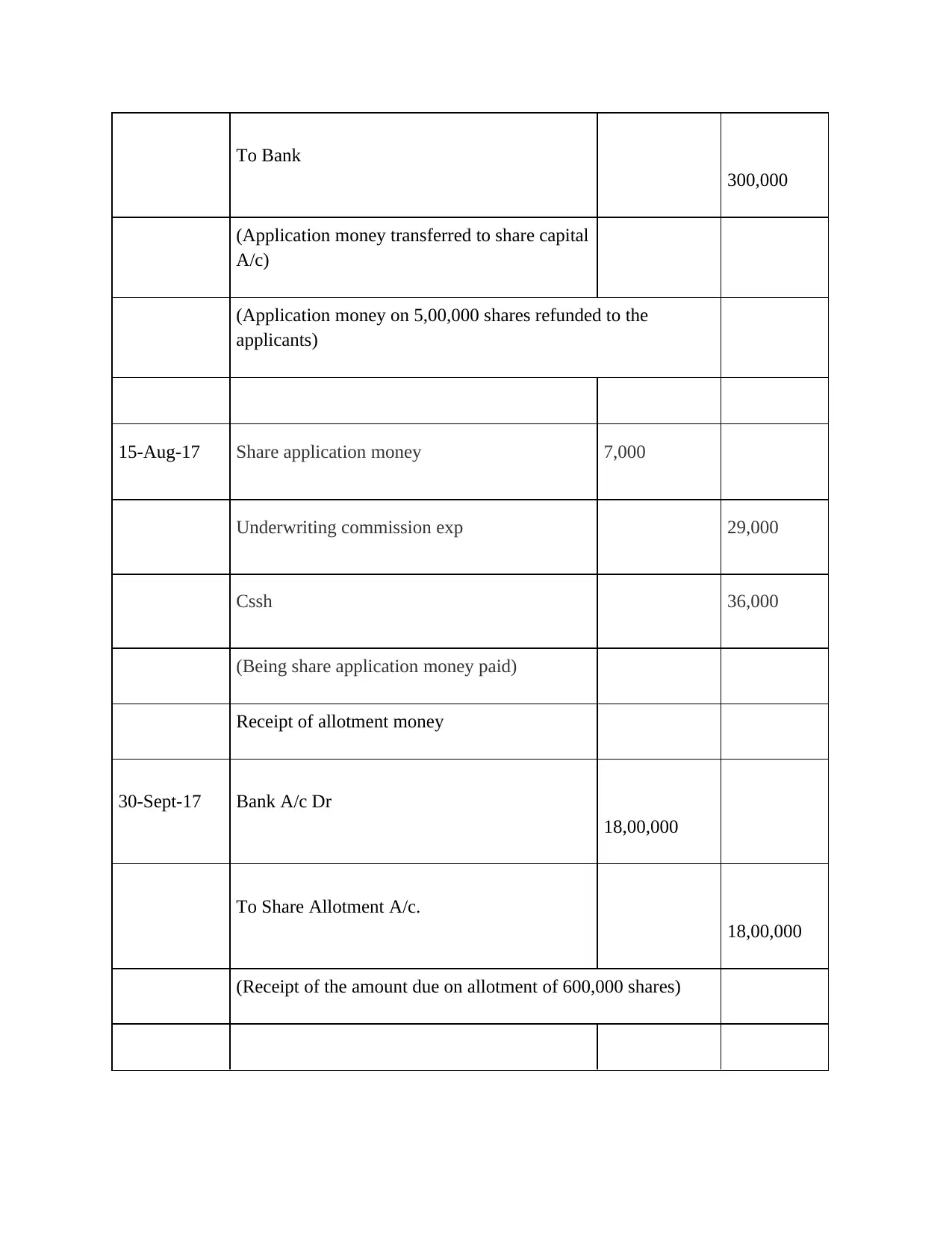

To Bank

300,000

(Application money transferred to share capital

A/c)

(Application money on 5,00,000 shares refunded to the

applicants)

15-Aug-17 Share application money 7,000

Underwriting commission exp 29,000

Cssh 36,000

(Being share application money paid)

Receipt of allotment money

30-Sept-17 Bank A/c Dr

18,00,000

To Share Allotment A/c.

18,00,000

(Receipt of the amount due on allotment of 600,000 shares)

300,000

(Application money transferred to share capital

A/c)

(Application money on 5,00,000 shares refunded to the

applicants)

15-Aug-17 Share application money 7,000

Underwriting commission exp 29,000

Cssh 36,000

(Being share application money paid)

Receipt of allotment money

30-Sept-17 Bank A/c Dr

18,00,000

To Share Allotment A/c.

18,00,000

(Receipt of the amount due on allotment of 600,000 shares)

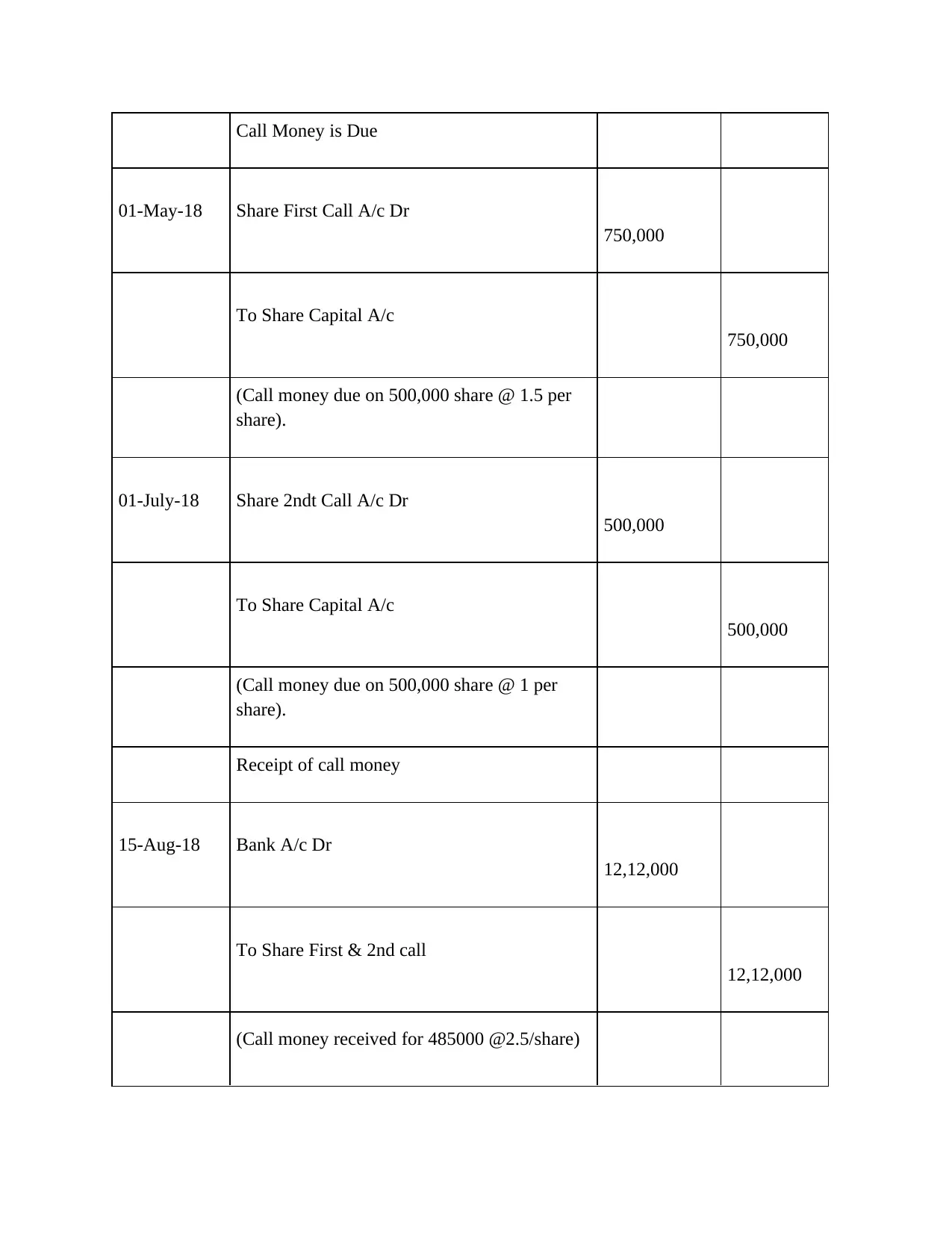

Call Money is Due

01-May-18 Share First Call A/c Dr

750,000

To Share Capital A/c

750,000

(Call money due on 500,000 share @ 1.5 per

share).

01-July-18 Share 2ndt Call A/c Dr

500,000

To Share Capital A/c

500,000

(Call money due on 500,000 share @ 1 per

share).

Receipt of call money

15-Aug-18 Bank A/c Dr

12,12,000

To Share First & 2nd call

12,12,000

(Call money received for 485000 @2.5/share)

01-May-18 Share First Call A/c Dr

750,000

To Share Capital A/c

750,000

(Call money due on 500,000 share @ 1.5 per

share).

01-July-18 Share 2ndt Call A/c Dr

500,000

To Share Capital A/c

500,000

(Call money due on 500,000 share @ 1 per

share).

Receipt of call money

15-Aug-18 Bank A/c Dr

12,12,000

To Share First & 2nd call

12,12,000

(Call money received for 485000 @2.5/share)

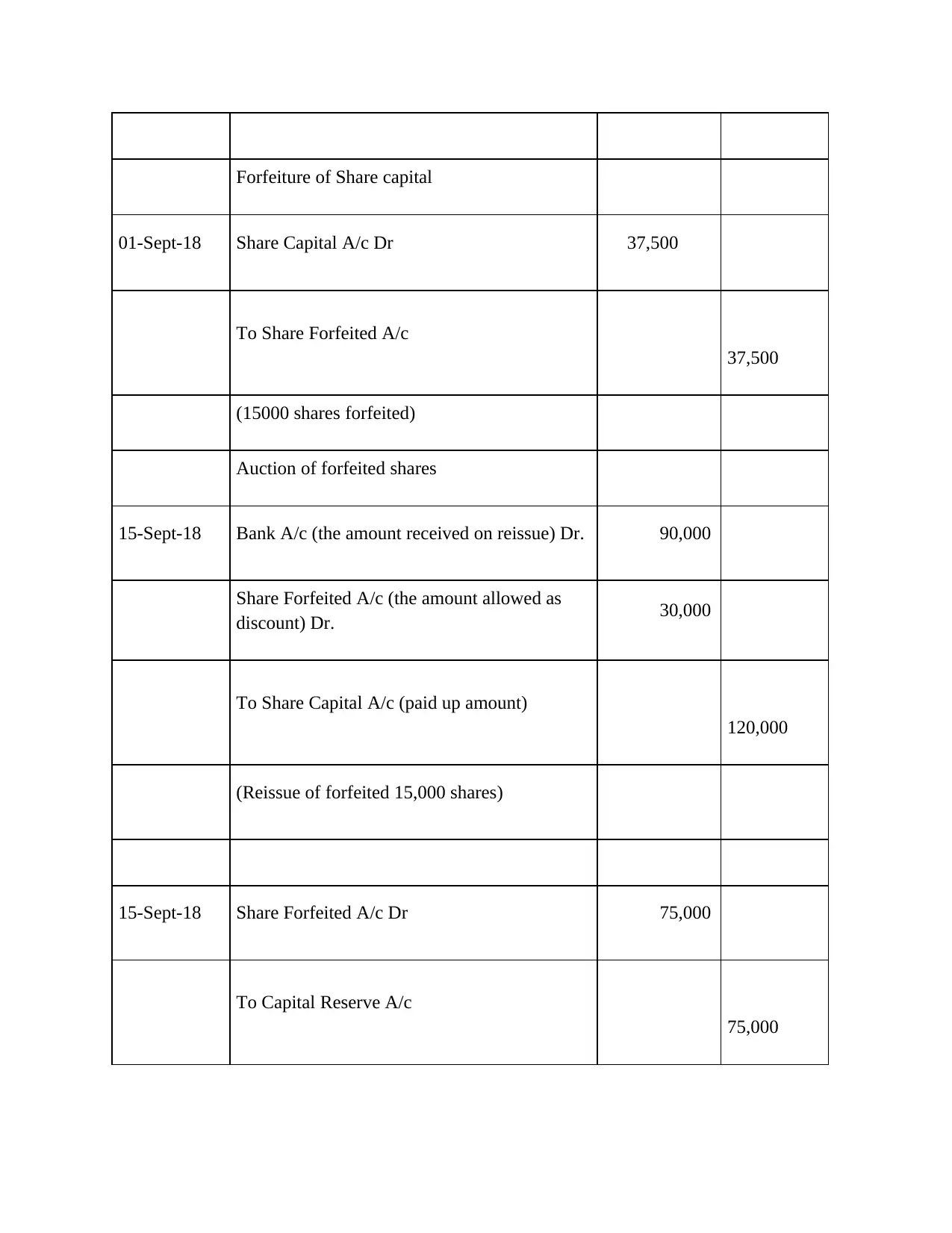

Forfeiture of Share capital

01-Sept-18 Share Capital A/c Dr 37,500

To Share Forfeited A/c

37,500

(15000 shares forfeited)

Auction of forfeited shares

15-Sept-18 Bank A/c (the amount received on reissue) Dr. 90,000

Share Forfeited A/c (the amount allowed as

discount) Dr. 30,000

To Share Capital A/c (paid up amount)

120,000

(Reissue of forfeited 15,000 shares)

15-Sept-18 Share Forfeited A/c Dr 75,000

To Capital Reserve A/c

75,000

01-Sept-18 Share Capital A/c Dr 37,500

To Share Forfeited A/c

37,500

(15000 shares forfeited)

Auction of forfeited shares

15-Sept-18 Bank A/c (the amount received on reissue) Dr. 90,000

Share Forfeited A/c (the amount allowed as

discount) Dr. 30,000

To Share Capital A/c (paid up amount)

120,000

(Reissue of forfeited 15,000 shares)

15-Sept-18 Share Forfeited A/c Dr 75,000

To Capital Reserve A/c

75,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

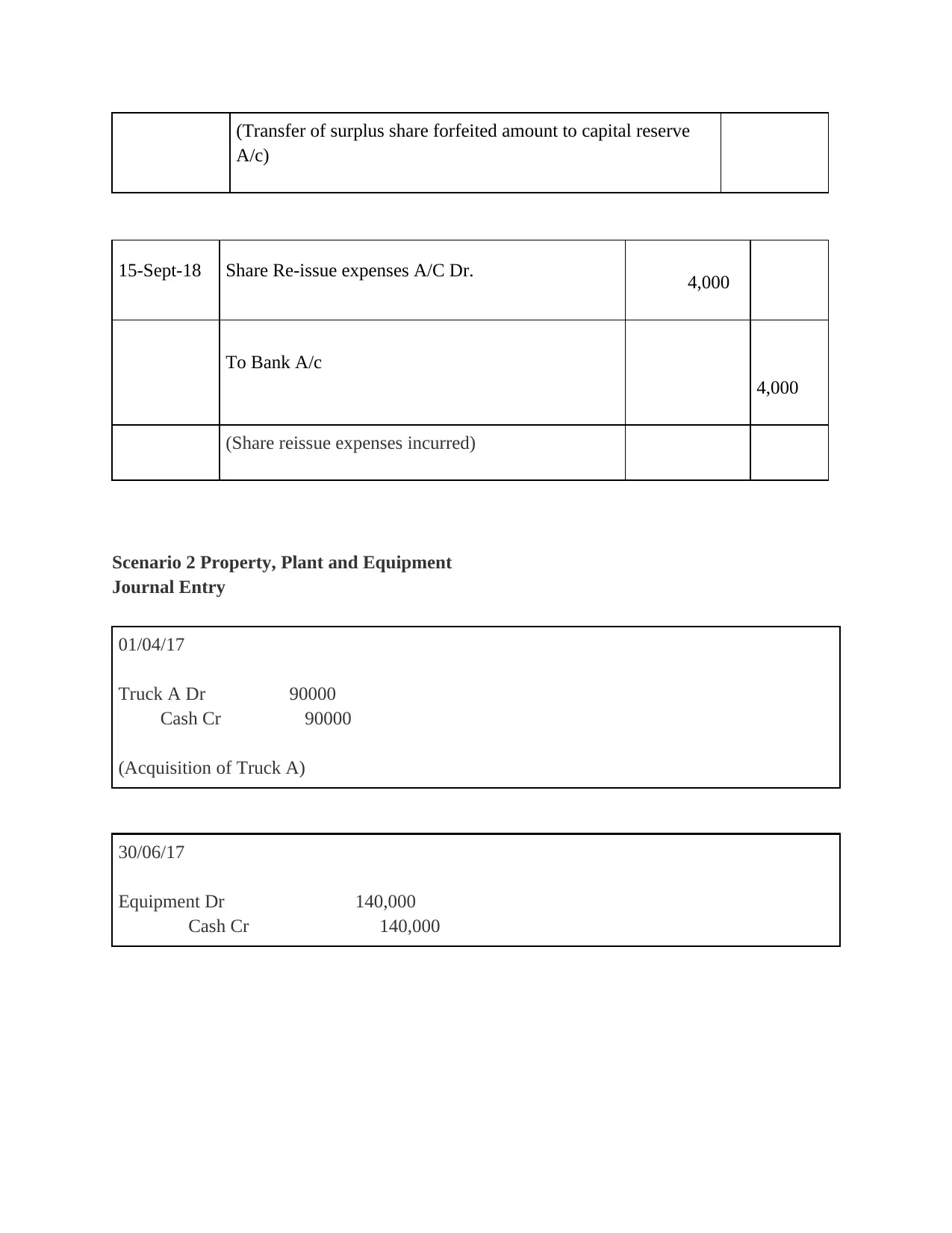

(Transfer of surplus share forfeited amount to capital reserve

A/c)

15-Sept-18 Share Re-issue expenses A/C Dr. 4,000

To Bank A/c

4,000

(Share reissue expenses incurred)

Scenario 2 Property, Plant and Equipment

Journal Entry

01/04/17

Truck A Dr 90000

Cash Cr 90000

(Acquisition of Truck A)

30/06/17

Equipment Dr 140,000

Cash Cr 140,000

A/c)

15-Sept-18 Share Re-issue expenses A/C Dr. 4,000

To Bank A/c

4,000

(Share reissue expenses incurred)

Scenario 2 Property, Plant and Equipment

Journal Entry

01/04/17

Truck A Dr 90000

Cash Cr 90000

(Acquisition of Truck A)

30/06/17

Equipment Dr 140,000

Cash Cr 140,000

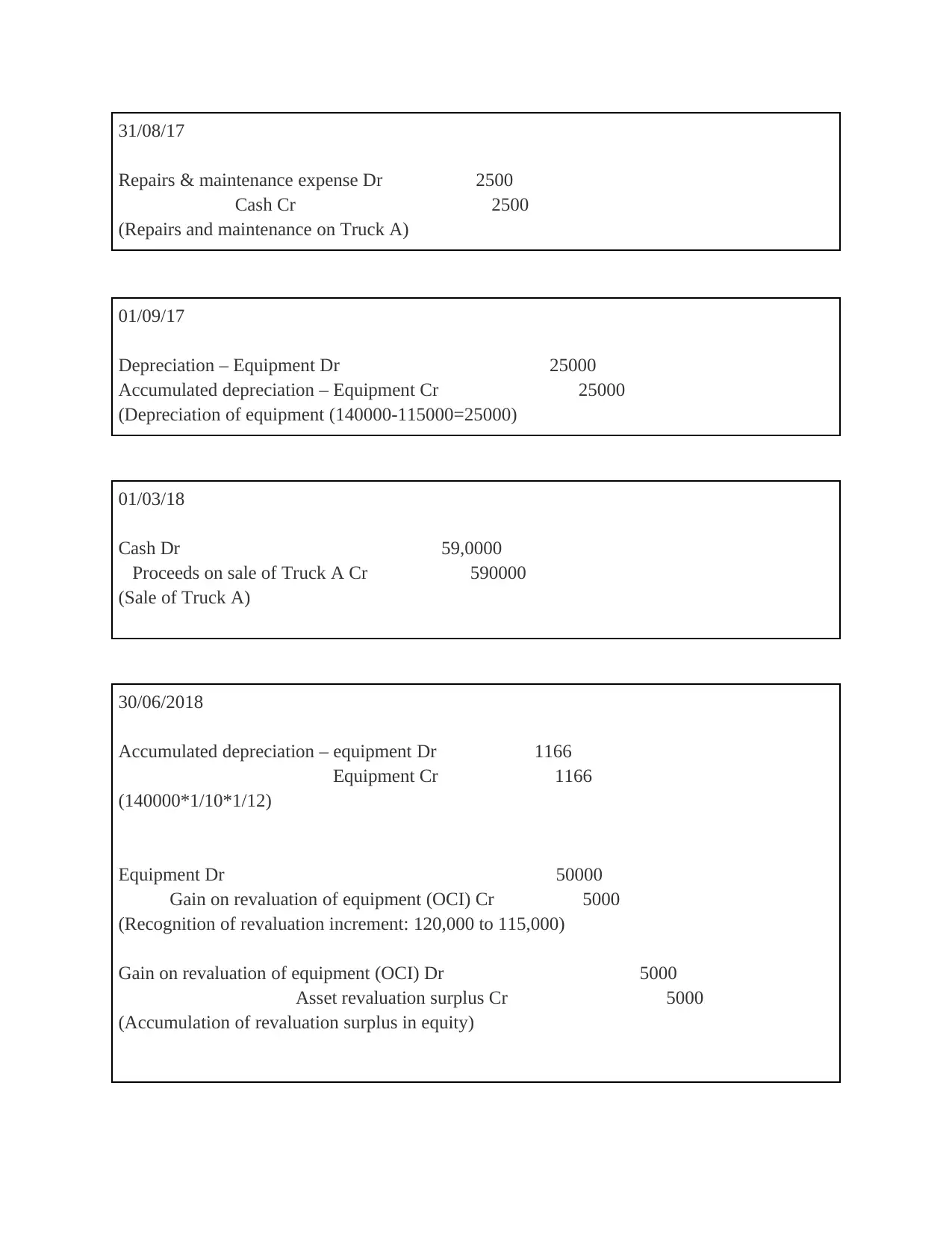

31/08/17

Repairs & maintenance expense Dr 2500

Cash Cr 2500

(Repairs and maintenance on Truck A)

01/09/17

Depreciation – Equipment Dr 25000

Accumulated depreciation – Equipment Cr 25000

(Depreciation of equipment (140000-115000=25000)

01/03/18

Cash Dr 59,0000

Proceeds on sale of Truck A Cr 590000

(Sale of Truck A)

30/06/2018

Accumulated depreciation – equipment Dr 1166

Equipment Cr 1166

(140000*1/10*1/12)

Equipment Dr 50000

Gain on revaluation of equipment (OCI) Cr 5000

(Recognition of revaluation increment: 120,000 to 115,000)

Gain on revaluation of equipment (OCI) Dr 5000

Asset revaluation surplus Cr 5000

(Accumulation of revaluation surplus in equity)

Repairs & maintenance expense Dr 2500

Cash Cr 2500

(Repairs and maintenance on Truck A)

01/09/17

Depreciation – Equipment Dr 25000

Accumulated depreciation – Equipment Cr 25000

(Depreciation of equipment (140000-115000=25000)

01/03/18

Cash Dr 59,0000

Proceeds on sale of Truck A Cr 590000

(Sale of Truck A)

30/06/2018

Accumulated depreciation – equipment Dr 1166

Equipment Cr 1166

(140000*1/10*1/12)

Equipment Dr 50000

Gain on revaluation of equipment (OCI) Cr 5000

(Recognition of revaluation increment: 120,000 to 115,000)

Gain on revaluation of equipment (OCI) Dr 5000

Asset revaluation surplus Cr 5000

(Accumulation of revaluation surplus in equity)

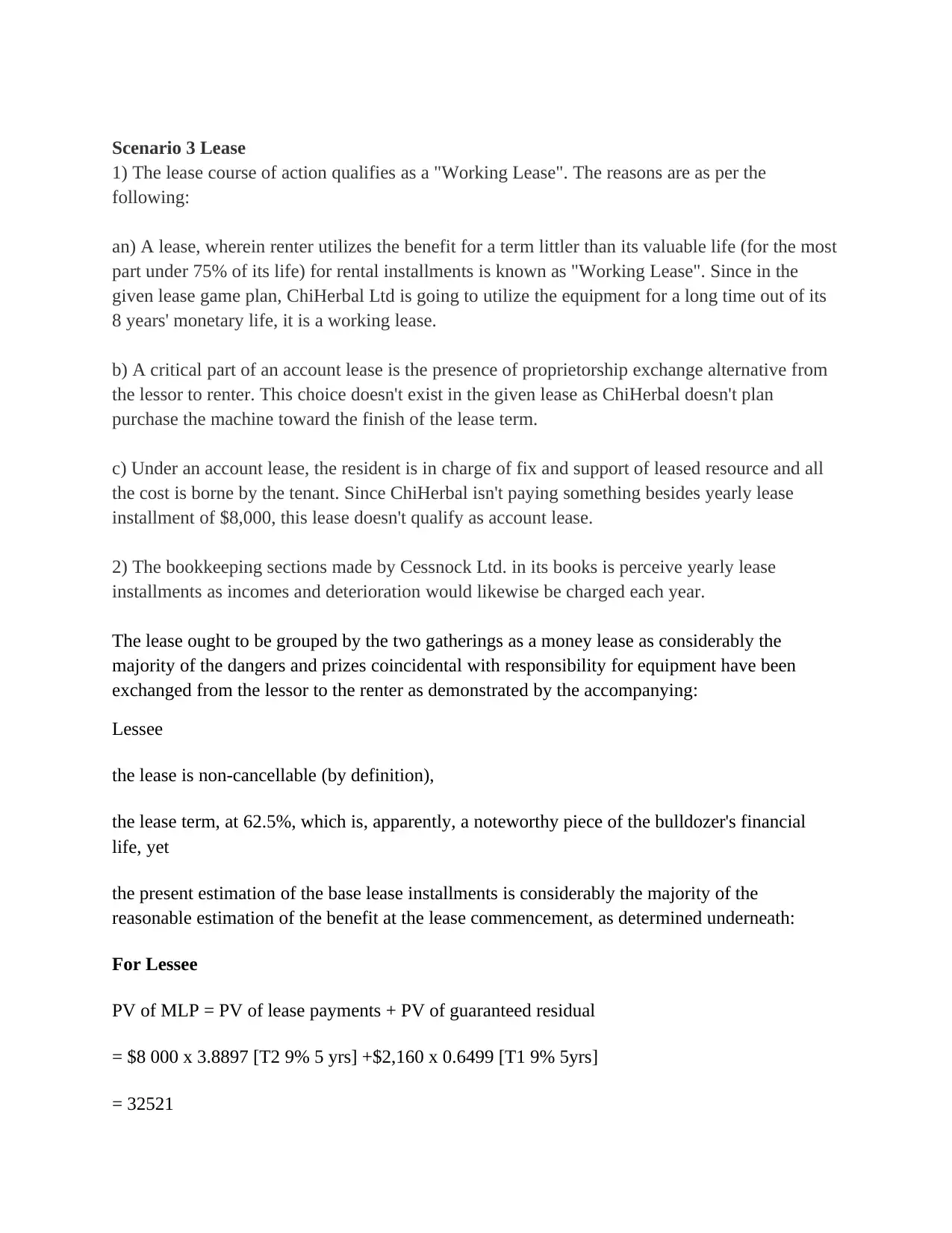

Scenario 3 Lease

1) The lease course of action qualifies as a "Working Lease". The reasons are as per the

following:

an) A lease, wherein renter utilizes the benefit for a term littler than its valuable life (for the most

part under 75% of its life) for rental installments is known as "Working Lease". Since in the

given lease game plan, ChiHerbal Ltd is going to utilize the equipment for a long time out of its

8 years' monetary life, it is a working lease.

b) A critical part of an account lease is the presence of proprietorship exchange alternative from

the lessor to renter. This choice doesn't exist in the given lease as ChiHerbal doesn't plan

purchase the machine toward the finish of the lease term.

c) Under an account lease, the resident is in charge of fix and support of leased resource and all

the cost is borne by the tenant. Since ChiHerbal isn't paying something besides yearly lease

installment of $8,000, this lease doesn't qualify as account lease.

2) The bookkeeping sections made by Cessnock Ltd. in its books is perceive yearly lease

installments as incomes and deterioration would likewise be charged each year.

The lease ought to be grouped by the two gatherings as a money lease as considerably the

majority of the dangers and prizes coincidental with responsibility for equipment have been

exchanged from the lessor to the renter as demonstrated by the accompanying:

Lessee

the lease is non-cancellable (by definition),

the lease term, at 62.5%, which is, apparently, a noteworthy piece of the bulldozer's financial

life, yet

the present estimation of the base lease installments is considerably the majority of the

reasonable estimation of the benefit at the lease commencement, as determined underneath:

For Lessee

PV of MLP = PV of lease payments + PV of guaranteed residual

= $8 000 x 3.8897 [T2 9% 5 yrs] +$2,160 x 0.6499 [T1 9% 5yrs]

= 32521

1) The lease course of action qualifies as a "Working Lease". The reasons are as per the

following:

an) A lease, wherein renter utilizes the benefit for a term littler than its valuable life (for the most

part under 75% of its life) for rental installments is known as "Working Lease". Since in the

given lease game plan, ChiHerbal Ltd is going to utilize the equipment for a long time out of its

8 years' monetary life, it is a working lease.

b) A critical part of an account lease is the presence of proprietorship exchange alternative from

the lessor to renter. This choice doesn't exist in the given lease as ChiHerbal doesn't plan

purchase the machine toward the finish of the lease term.

c) Under an account lease, the resident is in charge of fix and support of leased resource and all

the cost is borne by the tenant. Since ChiHerbal isn't paying something besides yearly lease

installment of $8,000, this lease doesn't qualify as account lease.

2) The bookkeeping sections made by Cessnock Ltd. in its books is perceive yearly lease

installments as incomes and deterioration would likewise be charged each year.

The lease ought to be grouped by the two gatherings as a money lease as considerably the

majority of the dangers and prizes coincidental with responsibility for equipment have been

exchanged from the lessor to the renter as demonstrated by the accompanying:

Lessee

the lease is non-cancellable (by definition),

the lease term, at 62.5%, which is, apparently, a noteworthy piece of the bulldozer's financial

life, yet

the present estimation of the base lease installments is considerably the majority of the

reasonable estimation of the benefit at the lease commencement, as determined underneath:

For Lessee

PV of MLP = PV of lease payments + PV of guaranteed residual

= $8 000 x 3.8897 [T2 9% 5 yrs] +$2,160 x 0.6499 [T1 9% 5yrs]

= 32521

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

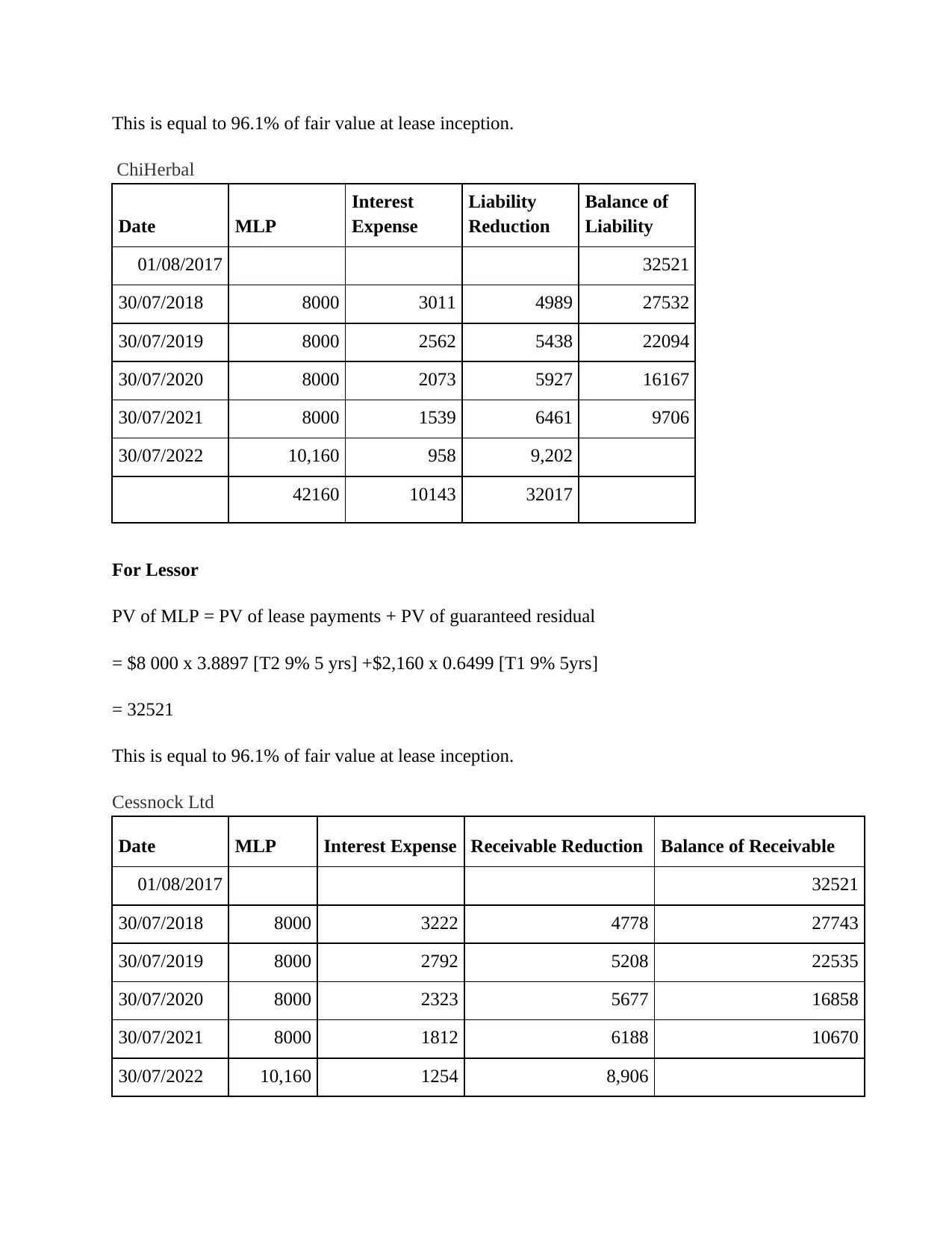

This is equal to 96.1% of fair value at lease inception.

ChiHerbal

Date MLP

Interest

Expense

Liability

Reduction

Balance of

Liability

01/08/2017 32521

30/07/2018 8000 3011 4989 27532

30/07/2019 8000 2562 5438 22094

30/07/2020 8000 2073 5927 16167

30/07/2021 8000 1539 6461 9706

30/07/2022 10,160 958 9,202

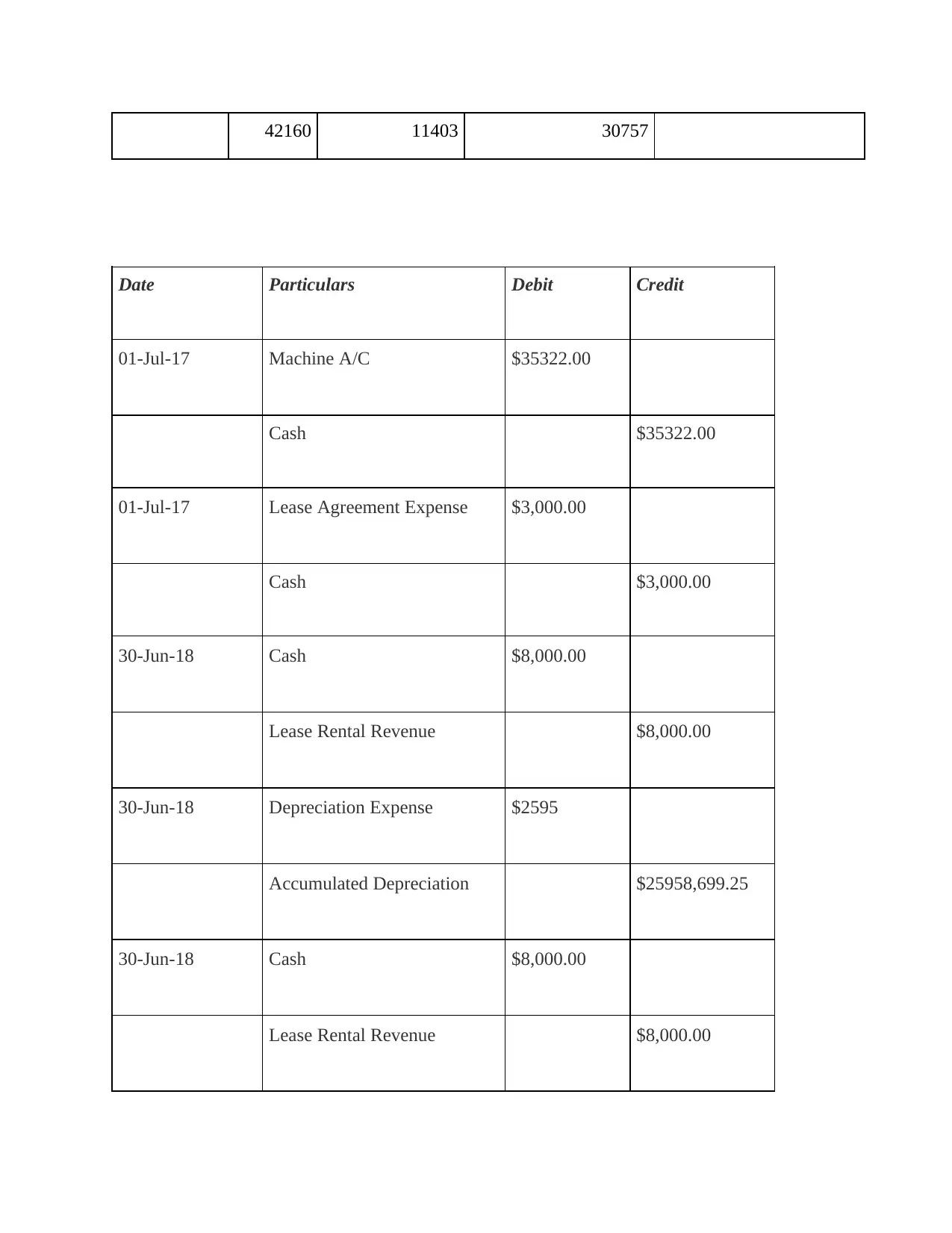

42160 10143 32017

For Lessor

PV of MLP = PV of lease payments + PV of guaranteed residual

= $8 000 x 3.8897 [T2 9% 5 yrs] +$2,160 x 0.6499 [T1 9% 5yrs]

= 32521

This is equal to 96.1% of fair value at lease inception.

Cessnock Ltd

Date MLP Interest Expense Receivable Reduction Balance of Receivable

01/08/2017 32521

30/07/2018 8000 3222 4778 27743

30/07/2019 8000 2792 5208 22535

30/07/2020 8000 2323 5677 16858

30/07/2021 8000 1812 6188 10670

30/07/2022 10,160 1254 8,906

ChiHerbal

Date MLP

Interest

Expense

Liability

Reduction

Balance of

Liability

01/08/2017 32521

30/07/2018 8000 3011 4989 27532

30/07/2019 8000 2562 5438 22094

30/07/2020 8000 2073 5927 16167

30/07/2021 8000 1539 6461 9706

30/07/2022 10,160 958 9,202

42160 10143 32017

For Lessor

PV of MLP = PV of lease payments + PV of guaranteed residual

= $8 000 x 3.8897 [T2 9% 5 yrs] +$2,160 x 0.6499 [T1 9% 5yrs]

= 32521

This is equal to 96.1% of fair value at lease inception.

Cessnock Ltd

Date MLP Interest Expense Receivable Reduction Balance of Receivable

01/08/2017 32521

30/07/2018 8000 3222 4778 27743

30/07/2019 8000 2792 5208 22535

30/07/2020 8000 2323 5677 16858

30/07/2021 8000 1812 6188 10670

30/07/2022 10,160 1254 8,906

42160 11403 30757

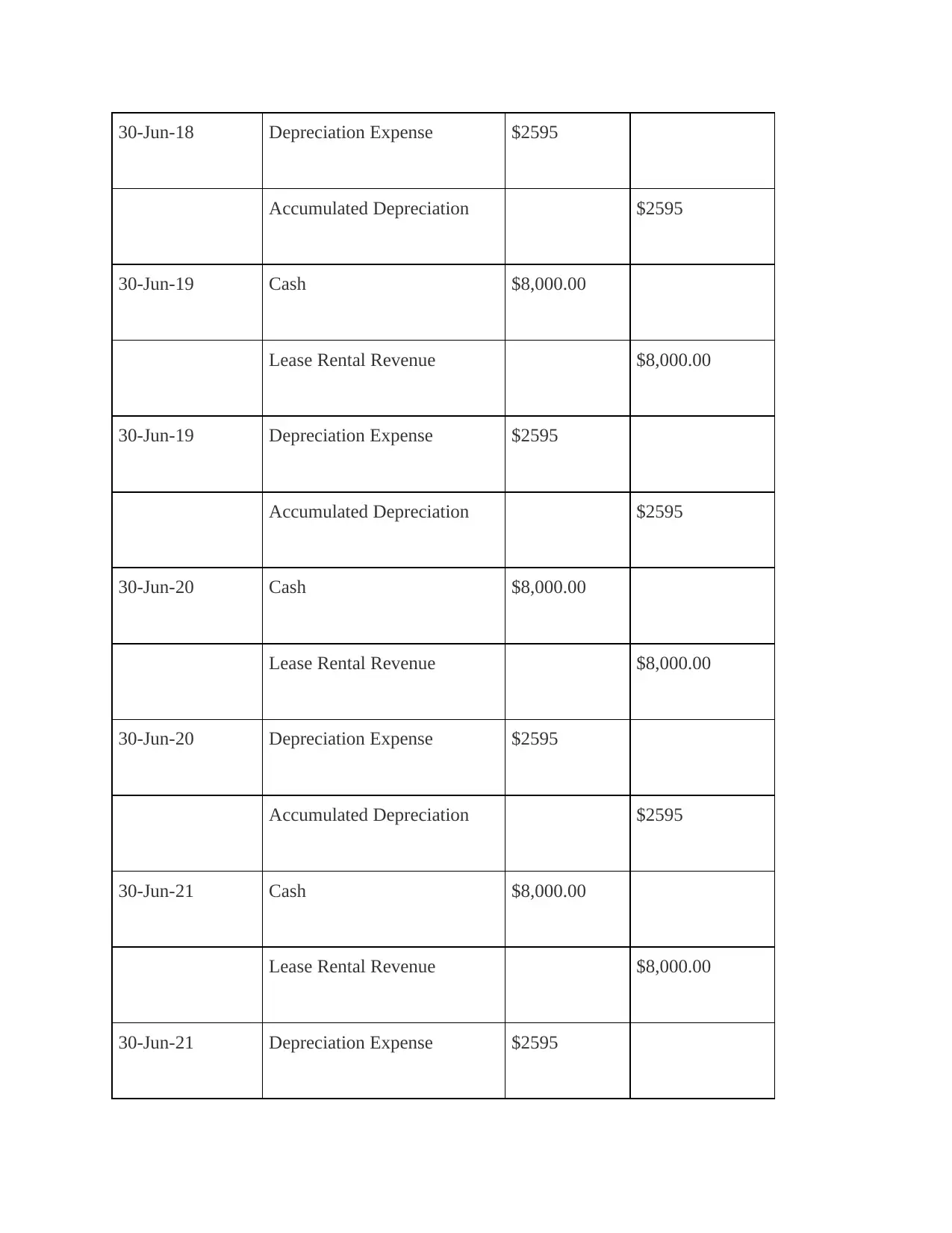

Date Particulars Debit Credit

01-Jul-17 Machine A/C $35322.00

Cash $35322.00

01-Jul-17 Lease Agreement Expense $3,000.00

Cash $3,000.00

30-Jun-18 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-18 Depreciation Expense $2595

Accumulated Depreciation $25958,699.25

30-Jun-18 Cash $8,000.00

Lease Rental Revenue $8,000.00

Date Particulars Debit Credit

01-Jul-17 Machine A/C $35322.00

Cash $35322.00

01-Jul-17 Lease Agreement Expense $3,000.00

Cash $3,000.00

30-Jun-18 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-18 Depreciation Expense $2595

Accumulated Depreciation $25958,699.25

30-Jun-18 Cash $8,000.00

Lease Rental Revenue $8,000.00

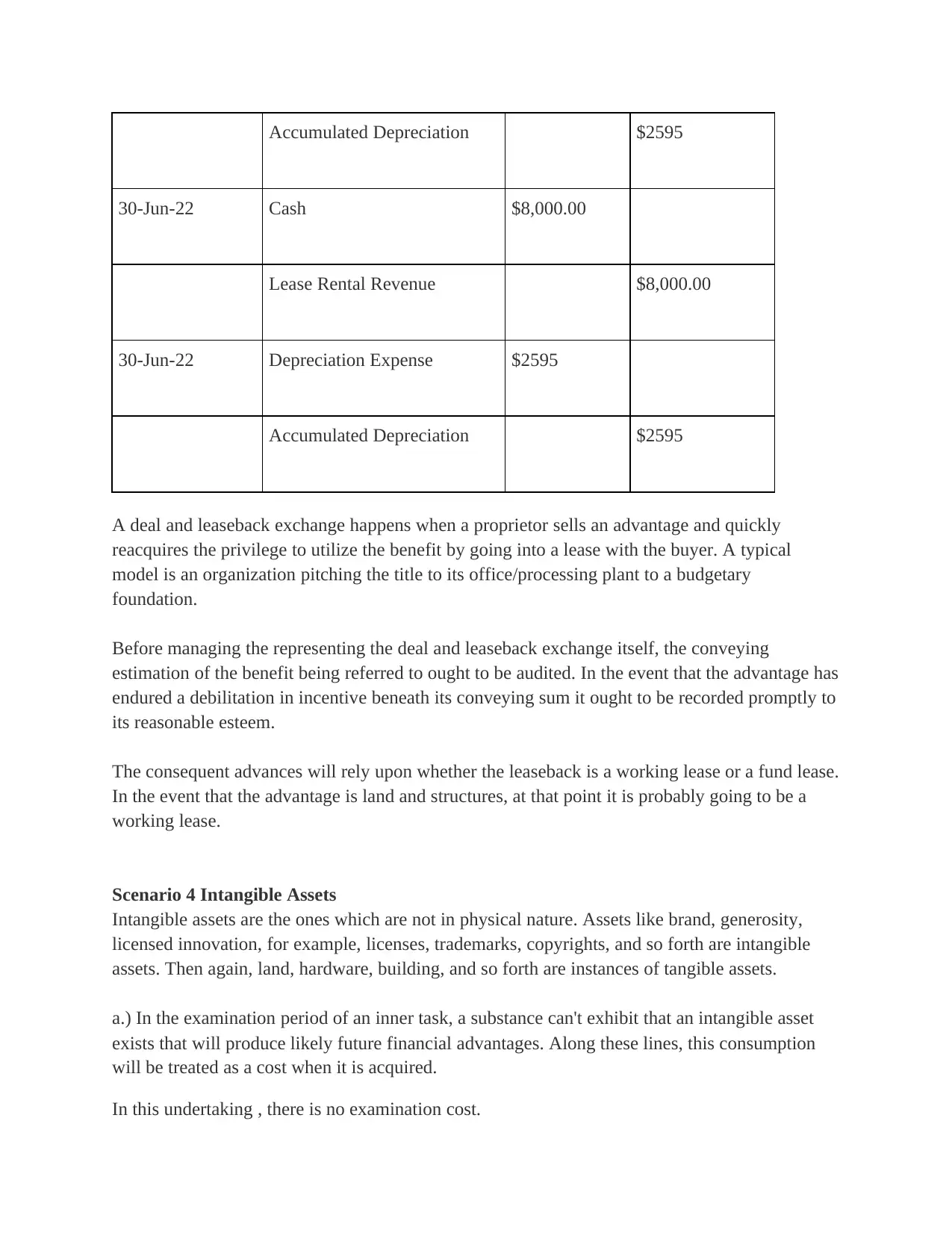

30-Jun-18 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-19 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-19 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-20 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-20 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-21 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-21 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-19 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-19 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-20 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-20 Depreciation Expense $2595

Accumulated Depreciation $2595

30-Jun-21 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-21 Depreciation Expense $2595

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Accumulated Depreciation $2595

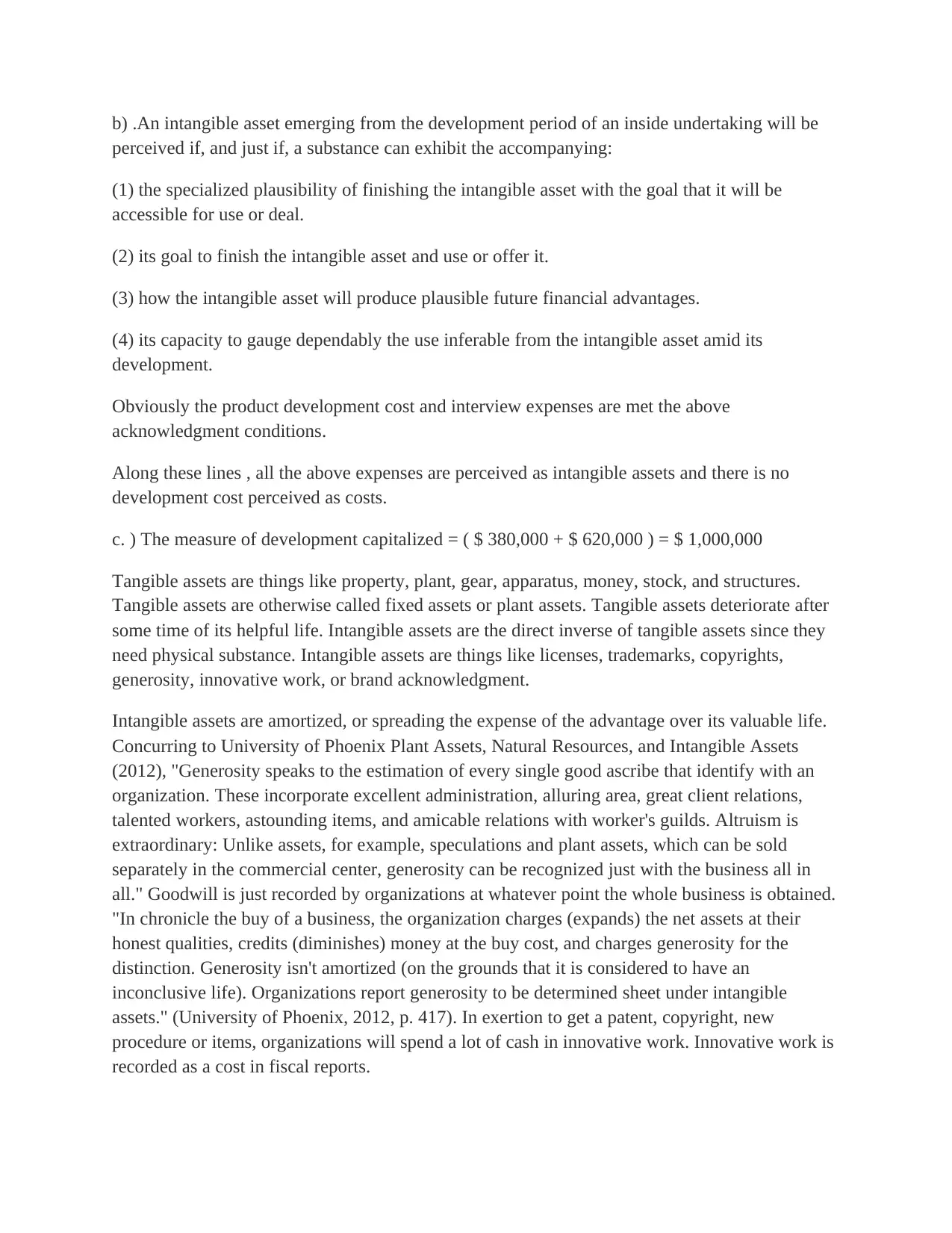

30-Jun-22 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-22 Depreciation Expense $2595

Accumulated Depreciation $2595

A deal and leaseback exchange happens when a proprietor sells an advantage and quickly

reacquires the privilege to utilize the benefit by going into a lease with the buyer. A typical

model is an organization pitching the title to its office/processing plant to a budgetary

foundation.

Before managing the representing the deal and leaseback exchange itself, the conveying

estimation of the benefit being referred to ought to be audited. In the event that the advantage has

endured a debilitation in incentive beneath its conveying sum it ought to be recorded promptly to

its reasonable esteem.

The consequent advances will rely upon whether the leaseback is a working lease or a fund lease.

In the event that the advantage is land and structures, at that point it is probably going to be a

working lease.

Scenario 4 Intangible Assets

Intangible assets are the ones which are not in physical nature. Assets like brand, generosity,

licensed innovation, for example, licenses, trademarks, copyrights, and so forth are intangible

assets. Then again, land, hardware, building, and so forth are instances of tangible assets.

a.) In the examination period of an inner task, a substance can't exhibit that an intangible asset

exists that will produce likely future financial advantages. Along these lines, this consumption

will be treated as a cost when it is acquired.

In this undertaking , there is no examination cost.

30-Jun-22 Cash $8,000.00

Lease Rental Revenue $8,000.00

30-Jun-22 Depreciation Expense $2595

Accumulated Depreciation $2595

A deal and leaseback exchange happens when a proprietor sells an advantage and quickly

reacquires the privilege to utilize the benefit by going into a lease with the buyer. A typical

model is an organization pitching the title to its office/processing plant to a budgetary

foundation.

Before managing the representing the deal and leaseback exchange itself, the conveying

estimation of the benefit being referred to ought to be audited. In the event that the advantage has

endured a debilitation in incentive beneath its conveying sum it ought to be recorded promptly to

its reasonable esteem.

The consequent advances will rely upon whether the leaseback is a working lease or a fund lease.

In the event that the advantage is land and structures, at that point it is probably going to be a

working lease.

Scenario 4 Intangible Assets

Intangible assets are the ones which are not in physical nature. Assets like brand, generosity,

licensed innovation, for example, licenses, trademarks, copyrights, and so forth are intangible

assets. Then again, land, hardware, building, and so forth are instances of tangible assets.

a.) In the examination period of an inner task, a substance can't exhibit that an intangible asset

exists that will produce likely future financial advantages. Along these lines, this consumption

will be treated as a cost when it is acquired.

In this undertaking , there is no examination cost.

b) .An intangible asset emerging from the development period of an inside undertaking will be

perceived if, and just if, a substance can exhibit the accompanying:

(1) the specialized plausibility of finishing the intangible asset with the goal that it will be

accessible for use or deal.

(2) its goal to finish the intangible asset and use or offer it.

(3) how the intangible asset will produce plausible future financial advantages.

(4) its capacity to gauge dependably the use inferable from the intangible asset amid its

development.

Obviously the product development cost and interview expenses are met the above

acknowledgment conditions.

Along these lines , all the above expenses are perceived as intangible assets and there is no

development cost perceived as costs.

c. ) The measure of development capitalized = ( $ 380,000 + $ 620,000 ) = $ 1,000,000

Tangible assets are things like property, plant, gear, apparatus, money, stock, and structures.

Tangible assets are otherwise called fixed assets or plant assets. Tangible assets deteriorate after

some time of its helpful life. Intangible assets are the direct inverse of tangible assets since they

need physical substance. Intangible assets are things like licenses, trademarks, copyrights,

generosity, innovative work, or brand acknowledgment.

Intangible assets are amortized, or spreading the expense of the advantage over its valuable life.

Concurring to University of Phoenix Plant Assets, Natural Resources, and Intangible Assets

(2012), "Generosity speaks to the estimation of every single good ascribe that identify with an

organization. These incorporate excellent administration, alluring area, great client relations,

talented workers, astounding items, and amicable relations with worker's guilds. Altruism is

extraordinary: Unlike assets, for example, speculations and plant assets, which can be sold

separately in the commercial center, generosity can be recognized just with the business all in

all." Goodwill is just recorded by organizations at whatever point the whole business is obtained.

"In chronicle the buy of a business, the organization charges (expands) the net assets at their

honest qualities, credits (diminishes) money at the buy cost, and charges generosity for the

distinction. Generosity isn't amortized (on the grounds that it is considered to have an

inconclusive life). Organizations report generosity to be determined sheet under intangible

assets." (University of Phoenix, 2012, p. 417). In exertion to get a patent, copyright, new

procedure or items, organizations will spend a lot of cash in innovative work. Innovative work is

recorded as a cost in fiscal reports.

perceived if, and just if, a substance can exhibit the accompanying:

(1) the specialized plausibility of finishing the intangible asset with the goal that it will be

accessible for use or deal.

(2) its goal to finish the intangible asset and use or offer it.

(3) how the intangible asset will produce plausible future financial advantages.

(4) its capacity to gauge dependably the use inferable from the intangible asset amid its

development.

Obviously the product development cost and interview expenses are met the above

acknowledgment conditions.

Along these lines , all the above expenses are perceived as intangible assets and there is no

development cost perceived as costs.

c. ) The measure of development capitalized = ( $ 380,000 + $ 620,000 ) = $ 1,000,000

Tangible assets are things like property, plant, gear, apparatus, money, stock, and structures.

Tangible assets are otherwise called fixed assets or plant assets. Tangible assets deteriorate after

some time of its helpful life. Intangible assets are the direct inverse of tangible assets since they

need physical substance. Intangible assets are things like licenses, trademarks, copyrights,

generosity, innovative work, or brand acknowledgment.

Intangible assets are amortized, or spreading the expense of the advantage over its valuable life.

Concurring to University of Phoenix Plant Assets, Natural Resources, and Intangible Assets

(2012), "Generosity speaks to the estimation of every single good ascribe that identify with an

organization. These incorporate excellent administration, alluring area, great client relations,

talented workers, astounding items, and amicable relations with worker's guilds. Altruism is

extraordinary: Unlike assets, for example, speculations and plant assets, which can be sold

separately in the commercial center, generosity can be recognized just with the business all in

all." Goodwill is just recorded by organizations at whatever point the whole business is obtained.

"In chronicle the buy of a business, the organization charges (expands) the net assets at their

honest qualities, credits (diminishes) money at the buy cost, and charges generosity for the

distinction. Generosity isn't amortized (on the grounds that it is considered to have an

inconclusive life). Organizations report generosity to be determined sheet under intangible

assets." (University of Phoenix, 2012, p. 417). In exertion to get a patent, copyright, new

procedure or items, organizations will spend a lot of cash in innovative work. Innovative work is

recorded as a cost in fiscal reports.

Reference

Ampofo, A., & Sellani, R. (2005). Examining the differences between United States

Generally Accepted Accounting Principles (U.S. GAAP) and International Accounting

Standards (IAS): implications for the harmonization of accounting standards. Accounting Forum,

29(2), 219-231. doi: 10.1016/j.accfor.2004.11.002

Accounting Tools. (2016). What is Capital Expenditure? Retrieved from

http://www.accountingtools.com/questions-and-answers/what-is-a-capital-

expenditure.html

University of Phoenix. (2012). Plant Assets, Natural Resources, and Intangible Assets.

Retrieved from University of Phoenix, XACC/291 Principles of Accounting 11

website.

Blake, J., & Lunt, H. (2018). Accounting standards. Harlow, Essex, England: Pearson

Education.

Ampofo, A., & Sellani, R. (2005). Examining the differences between United States

Generally Accepted Accounting Principles (U.S. GAAP) and International Accounting

Standards (IAS): implications for the harmonization of accounting standards. Accounting Forum,

29(2), 219-231. doi: 10.1016/j.accfor.2004.11.002

Accounting Tools. (2016). What is Capital Expenditure? Retrieved from

http://www.accountingtools.com/questions-and-answers/what-is-a-capital-

expenditure.html

University of Phoenix. (2012). Plant Assets, Natural Resources, and Intangible Assets.

Retrieved from University of Phoenix, XACC/291 Principles of Accounting 11

website.

Blake, J., & Lunt, H. (2018). Accounting standards. Harlow, Essex, England: Pearson

Education.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.