ACC801: Analysis of Wesfarmers and Fuji Xerox Sustainability Reports

VerifiedAdded on 2019/09/22

|14

|4103

|207

Report

AI Summary

This report analyzes and compares the sustainability reports of Wesfarmers and Fuji Xerox, focusing on their economic, environmental, and social performance as per the Global Reporting Initiative (GRI) G4 guidelines. The analysis of Wesfarmers covers economic value generated and distrib...

CHOSEN

SUSTAINABILITY PERFORMANCE

ACC801 ASSIGNMENT 2

NAME of the student

10-17-2016

SUSTAINABILITY PERFORMANCE

ACC801 ASSIGNMENT 2

NAME of the student

10-17-2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part A: Wesfarmers Comparison........................................................................................2

Economic........................................................................................................................ 2

Environmental................................................................................................................ 3

Social – Labour practices and decent work.....................................................................4

Social – Human rights..................................................................................................... 5

Social – Society............................................................................................................... 5

Social – Product responsibility........................................................................................5

Part B: Fuji Xerox Comparison............................................................................................ 7

Conclusions and Recommendations.................................................................................12

Wesfarmers.................................................................................................................. 12

Fuji Xerox..................................................................................................................... 12

Part D: Reflective Journal of personal development.........................................................13

References....................................................................................................................... 14

1

Part A: Wesfarmers Comparison........................................................................................2

Economic........................................................................................................................ 2

Environmental................................................................................................................ 3

Social – Labour practices and decent work.....................................................................4

Social – Human rights..................................................................................................... 5

Social – Society............................................................................................................... 5

Social – Product responsibility........................................................................................5

Part B: Fuji Xerox Comparison............................................................................................ 7

Conclusions and Recommendations.................................................................................12

Wesfarmers.................................................................................................................. 12

Fuji Xerox..................................................................................................................... 12

Part D: Reflective Journal of personal development.........................................................13

References....................................................................................................................... 14

1

Part A: Wesfarmers Comparison

Wesfarmers is a leading metallurgical coal producer and supplier of thermal coal for

power generation in Australia. Wesfarmers has been publishing its Sustainability report

with focus ranging from financial performance to sustainable business practices in

carbon and energy, community support, environment, governance and economic

contribution. Wesfarmers has further refined its report in 2014 to include such areas

material to the stakeholders as communicated by them during stakeholder engagement

conducted on a regular basis in a manner consistent with the principles of the Global

Reporting Initiative (GRI). GRI requires businesses to report on areas which are material

to both the organisation and its stakeholders. (Wesfarmers, 2014 Sustainability Report).

The sustainable performance for Wesfarmers for 2014 and 2015 has been analysed

under the categories of:

a. Economic

b. Environmental

c. Social

The category social is further analysed into aspects of:

a. Labour practices and decent work

b. Human rights

c. Society

d. Product Responsibility

The analysis is as below:

Economic

The G4-EC1 guideline requires the business to report and disclose the economic value

generated and distributed. These needs to be in details as per the basis components

of the statement of profit or loss at the global and significant regional level. G4 –EC5

requires the business to report analytical ratios of standard wages by gender in

relation to local minimum wage at significant locations of operations. Wesfarmers

have provided the details in respect of G4-EC1. The company has highlighted that its

operations has resulted in net outflow of monies to the suppliers amounting to $43

million, to 205,000 employees amounting to $7.8 million, to government amounting

to $1.6 million in the form taxes and to the shareholders amounting to $2.2 million in

the form of dividends. This has been a steady performance as compared to 2014

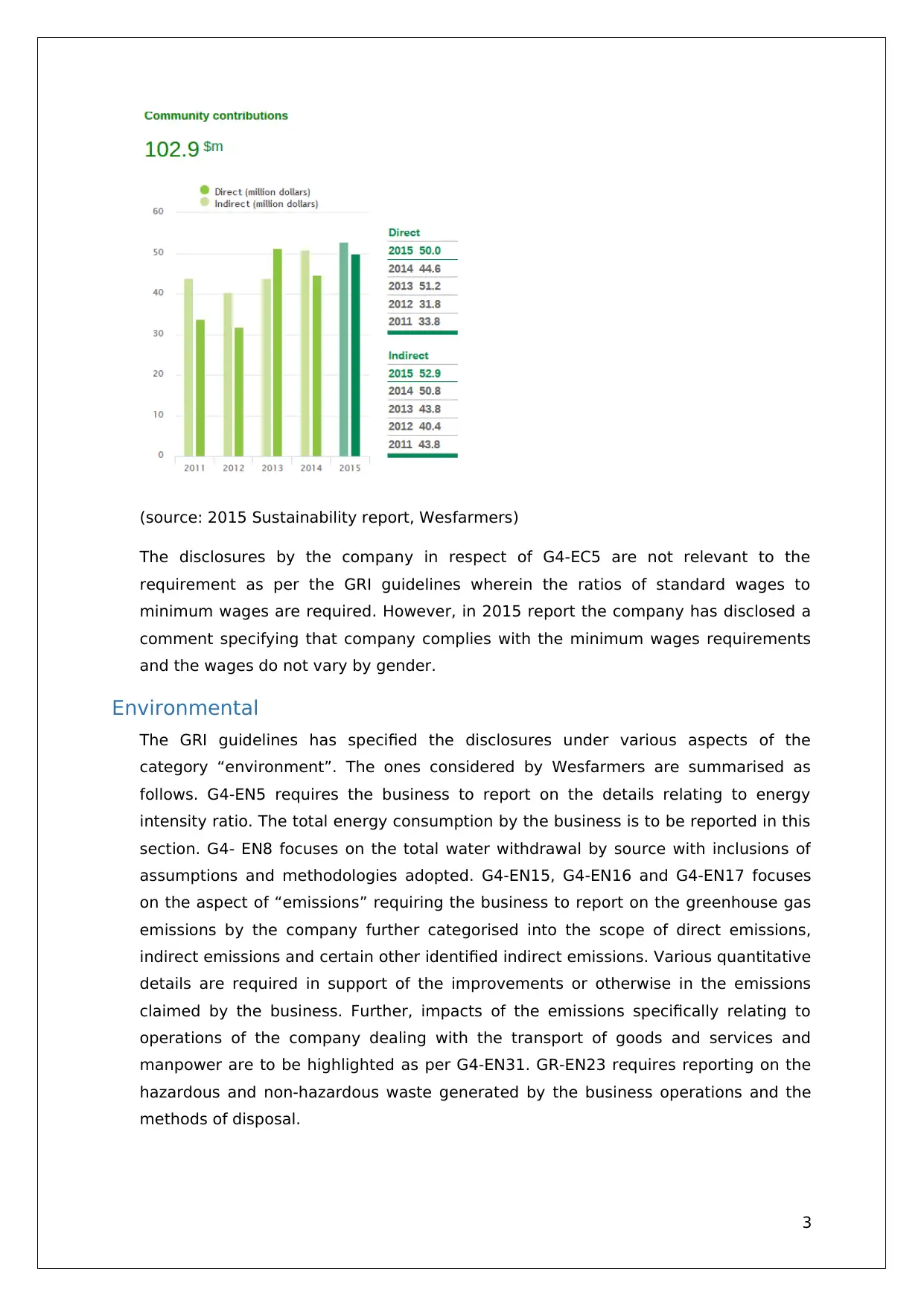

levels. No data for payments to suppliers were available for 2014. Further the direct

and indirect community contributions have increased from 2014 levels as per table

below:

2

Wesfarmers is a leading metallurgical coal producer and supplier of thermal coal for

power generation in Australia. Wesfarmers has been publishing its Sustainability report

with focus ranging from financial performance to sustainable business practices in

carbon and energy, community support, environment, governance and economic

contribution. Wesfarmers has further refined its report in 2014 to include such areas

material to the stakeholders as communicated by them during stakeholder engagement

conducted on a regular basis in a manner consistent with the principles of the Global

Reporting Initiative (GRI). GRI requires businesses to report on areas which are material

to both the organisation and its stakeholders. (Wesfarmers, 2014 Sustainability Report).

The sustainable performance for Wesfarmers for 2014 and 2015 has been analysed

under the categories of:

a. Economic

b. Environmental

c. Social

The category social is further analysed into aspects of:

a. Labour practices and decent work

b. Human rights

c. Society

d. Product Responsibility

The analysis is as below:

Economic

The G4-EC1 guideline requires the business to report and disclose the economic value

generated and distributed. These needs to be in details as per the basis components

of the statement of profit or loss at the global and significant regional level. G4 –EC5

requires the business to report analytical ratios of standard wages by gender in

relation to local minimum wage at significant locations of operations. Wesfarmers

have provided the details in respect of G4-EC1. The company has highlighted that its

operations has resulted in net outflow of monies to the suppliers amounting to $43

million, to 205,000 employees amounting to $7.8 million, to government amounting

to $1.6 million in the form taxes and to the shareholders amounting to $2.2 million in

the form of dividends. This has been a steady performance as compared to 2014

levels. No data for payments to suppliers were available for 2014. Further the direct

and indirect community contributions have increased from 2014 levels as per table

below:

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(source: 2015 Sustainability report, Wesfarmers)

The disclosures by the company in respect of G4-EC5 are not relevant to the

requirement as per the GRI guidelines wherein the ratios of standard wages to

minimum wages are required. However, in 2015 report the company has disclosed a

comment specifying that company complies with the minimum wages requirements

and the wages do not vary by gender.

Environmental

The GRI guidelines has specified the disclosures under various aspects of the

category “environment”. The ones considered by Wesfarmers are summarised as

follows. G4-EN5 requires the business to report on the details relating to energy

intensity ratio. The total energy consumption by the business is to be reported in this

section. G4- EN8 focuses on the total water withdrawal by source with inclusions of

assumptions and methodologies adopted. G4-EN15, G4-EN16 and G4-EN17 focuses

on the aspect of “emissions” requiring the business to report on the greenhouse gas

emissions by the company further categorised into the scope of direct emissions,

indirect emissions and certain other identified indirect emissions. Various quantitative

details are required in support of the improvements or otherwise in the emissions

claimed by the business. Further, impacts of the emissions specifically relating to

operations of the company dealing with the transport of goods and services and

manpower are to be highlighted as per G4-EN31. GR-EN23 requires reporting on the

hazardous and non-hazardous waste generated by the business operations and the

methods of disposal.

3

The disclosures by the company in respect of G4-EC5 are not relevant to the

requirement as per the GRI guidelines wherein the ratios of standard wages to

minimum wages are required. However, in 2015 report the company has disclosed a

comment specifying that company complies with the minimum wages requirements

and the wages do not vary by gender.

Environmental

The GRI guidelines has specified the disclosures under various aspects of the

category “environment”. The ones considered by Wesfarmers are summarised as

follows. G4-EN5 requires the business to report on the details relating to energy

intensity ratio. The total energy consumption by the business is to be reported in this

section. G4- EN8 focuses on the total water withdrawal by source with inclusions of

assumptions and methodologies adopted. G4-EN15, G4-EN16 and G4-EN17 focuses

on the aspect of “emissions” requiring the business to report on the greenhouse gas

emissions by the company further categorised into the scope of direct emissions,

indirect emissions and certain other identified indirect emissions. Various quantitative

details are required in support of the improvements or otherwise in the emissions

claimed by the business. Further, impacts of the emissions specifically relating to

operations of the company dealing with the transport of goods and services and

manpower are to be highlighted as per G4-EN31. GR-EN23 requires reporting on the

hazardous and non-hazardous waste generated by the business operations and the

methods of disposal.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

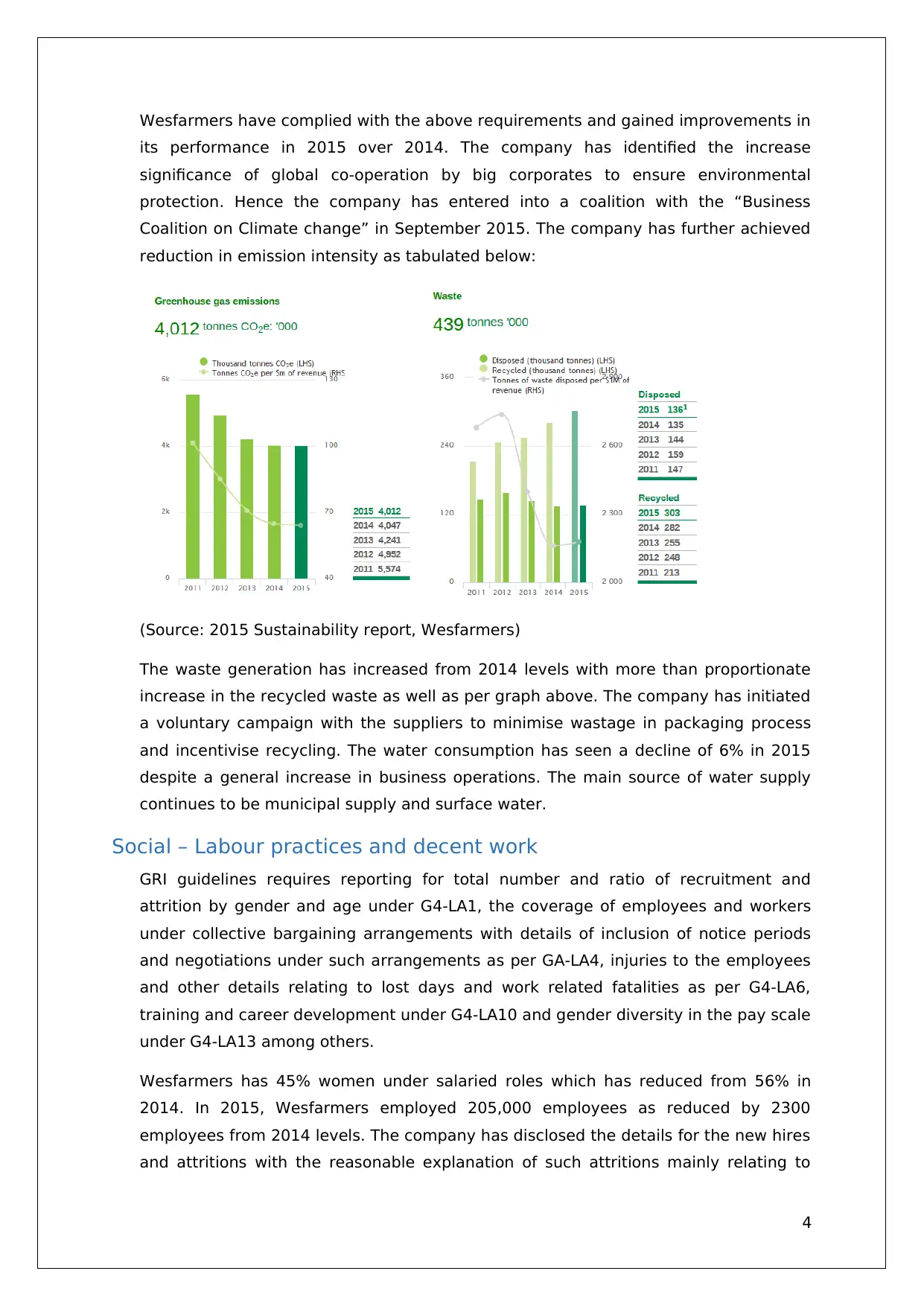

Wesfarmers have complied with the above requirements and gained improvements in

its performance in 2015 over 2014. The company has identified the increase

significance of global co-operation by big corporates to ensure environmental

protection. Hence the company has entered into a coalition with the “Business

Coalition on Climate change” in September 2015. The company has further achieved

reduction in emission intensity as tabulated below:

(Source: 2015 Sustainability report, Wesfarmers)

The waste generation has increased from 2014 levels with more than proportionate

increase in the recycled waste as well as per graph above. The company has initiated

a voluntary campaign with the suppliers to minimise wastage in packaging process

and incentivise recycling. The water consumption has seen a decline of 6% in 2015

despite a general increase in business operations. The main source of water supply

continues to be municipal supply and surface water.

Social – Labour practices and decent work

GRI guidelines requires reporting for total number and ratio of recruitment and

attrition by gender and age under G4-LA1, the coverage of employees and workers

under collective bargaining arrangements with details of inclusion of notice periods

and negotiations under such arrangements as per GA-LA4, injuries to the employees

and other details relating to lost days and work related fatalities as per G4-LA6,

training and career development under G4-LA10 and gender diversity in the pay scale

under G4-LA13 among others.

Wesfarmers has 45% women under salaried roles which has reduced from 56% in

2014. In 2015, Wesfarmers employed 205,000 employees as reduced by 2300

employees from 2014 levels. The company has disclosed the details for the new hires

and attritions with the reasonable explanation of such attritions mainly relating to

4

its performance in 2015 over 2014. The company has identified the increase

significance of global co-operation by big corporates to ensure environmental

protection. Hence the company has entered into a coalition with the “Business

Coalition on Climate change” in September 2015. The company has further achieved

reduction in emission intensity as tabulated below:

(Source: 2015 Sustainability report, Wesfarmers)

The waste generation has increased from 2014 levels with more than proportionate

increase in the recycled waste as well as per graph above. The company has initiated

a voluntary campaign with the suppliers to minimise wastage in packaging process

and incentivise recycling. The water consumption has seen a decline of 6% in 2015

despite a general increase in business operations. The main source of water supply

continues to be municipal supply and surface water.

Social – Labour practices and decent work

GRI guidelines requires reporting for total number and ratio of recruitment and

attrition by gender and age under G4-LA1, the coverage of employees and workers

under collective bargaining arrangements with details of inclusion of notice periods

and negotiations under such arrangements as per GA-LA4, injuries to the employees

and other details relating to lost days and work related fatalities as per G4-LA6,

training and career development under G4-LA10 and gender diversity in the pay scale

under G4-LA13 among others.

Wesfarmers has 45% women under salaried roles which has reduced from 56% in

2014. In 2015, Wesfarmers employed 205,000 employees as reduced by 2300

employees from 2014 levels. The company has disclosed the details for the new hires

and attritions with the reasonable explanation of such attritions mainly relating to

4

sale of Insurance division. The safety performance has improved in 2015 with 39.5

total recordable injury rate as against 42.7 in 2014. The lost time has reduced by

5.2% in 2015. The training and development initiative by the company has remained

consistent across the two periods. Wesfarmers aim for gender pay equity.

Social – Human rights

G4-HR2 requires reporting of total hours spent by the employees on the human rights

awareness. G4-HR5 requires reporting of identified risks of child labour employment

for business operations and measures to nullify such risk.

Wesfarmers has spent 2300 man hours in training for human rights in 2015 as

against 1020 hours in 2014. The factories and other places of operations are subject

to independent audits to ensure compliance. The breaches identified were acted upon

through correction or termination of the dealings with such factories.

Social – Society

GR-SO6 requires the business to report on the various political contributions made by

the company with the details of the beneficiary and the country. In case of in-kind

contributions, the valuation of such in-kind contribution in addition to the valuation

methodology adopted should be reported. GR-SO7 require the business to report on

the status of legal actions on the company in relation to malpractices alleged on it for

anti-competitive behaviour. Further, monetary and non-monetary sanctions on the

company are required to be disclosed under G4-SO8 for legal non-compliance.

Wesfarmers claims that it has suitable code of conduct and anti-bribery policies in

place to ensure that the ethical business practices are maintained. Further, there has

been no specific disclosure for such political contributions by Wesfarmers in 2014 and

2015. Wesfarmers has highlighted the cases pending in its 2015 and 2014

sustainability reports. The cases are settled as per the arbitration proceedings. The

company has disclose its settlement of fines owing to non-compliance amounting to

$2.5 million in bread litigation case and $ 10 million for supplier misconduct. There

were no major litigations concluded leading to any fines imposed on Wesfarmers in

2014.

Social – Product responsibility

G4-PR1 requires the company to report the products and services categories which

are identified as to having negative health and safety impacts. This section is not

applicable to Wesfarmers as health concerns are identified at division level and not at

product category level. There are no disclosures for this in both 2014 and 2015.

G4-PR2 requires product category wise reporting of incidents of non-compliance with

regulation in relation got health and safety of the products. The company has not

5

total recordable injury rate as against 42.7 in 2014. The lost time has reduced by

5.2% in 2015. The training and development initiative by the company has remained

consistent across the two periods. Wesfarmers aim for gender pay equity.

Social – Human rights

G4-HR2 requires reporting of total hours spent by the employees on the human rights

awareness. G4-HR5 requires reporting of identified risks of child labour employment

for business operations and measures to nullify such risk.

Wesfarmers has spent 2300 man hours in training for human rights in 2015 as

against 1020 hours in 2014. The factories and other places of operations are subject

to independent audits to ensure compliance. The breaches identified were acted upon

through correction or termination of the dealings with such factories.

Social – Society

GR-SO6 requires the business to report on the various political contributions made by

the company with the details of the beneficiary and the country. In case of in-kind

contributions, the valuation of such in-kind contribution in addition to the valuation

methodology adopted should be reported. GR-SO7 require the business to report on

the status of legal actions on the company in relation to malpractices alleged on it for

anti-competitive behaviour. Further, monetary and non-monetary sanctions on the

company are required to be disclosed under G4-SO8 for legal non-compliance.

Wesfarmers claims that it has suitable code of conduct and anti-bribery policies in

place to ensure that the ethical business practices are maintained. Further, there has

been no specific disclosure for such political contributions by Wesfarmers in 2014 and

2015. Wesfarmers has highlighted the cases pending in its 2015 and 2014

sustainability reports. The cases are settled as per the arbitration proceedings. The

company has disclose its settlement of fines owing to non-compliance amounting to

$2.5 million in bread litigation case and $ 10 million for supplier misconduct. There

were no major litigations concluded leading to any fines imposed on Wesfarmers in

2014.

Social – Product responsibility

G4-PR1 requires the company to report the products and services categories which

are identified as to having negative health and safety impacts. This section is not

applicable to Wesfarmers as health concerns are identified at division level and not at

product category level. There are no disclosures for this in both 2014 and 2015.

G4-PR2 requires product category wise reporting of incidents of non-compliance with

regulation in relation got health and safety of the products. The company has not

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

maintained product wise details of such non-compliance. The company has ensure

appropriate labelling of its products to ensure its compliance in respect of products

containing coin and button cell batteries in 2015. There were no such reported cases

in 2014.

G4-PR6 requires to report of the company is engaged in production and sale of any

products that are banned or under scrutiny for being banned. Wesfarmers has

disclosed in 2015 that they have stopped selling the controversial product “GTA5”

owing to complaints that the product depicts violence against women. However, in

2014 there were no such disclosures made by Wesfarmers in its sustainability report

of 2014.

Overall Wesfarmers have adhered to the material requirements under the G4 guidelines.

These sustainability reports has been verified by an independent accounting firm EY. The

assurance report is under limited scope to ensure the reporting is as per the criteria

specified under G4 guidelines and AA1000 Accountability Principles. Thus the

independent auditor has ensured that no information or evidence exists to negate the

information provided.

Wesfarmers has declared that they meet the reporting requirement “In Accordance” with

the G4-Guidelines Core option in 2015. IN 2014 the application level was B+ as per the

Global Reporting Initiative.

The referencing was inadequate in 2014 with the entire section linked to the various

data. The 2015 reporting is much more structured. The individual aspects and the

guidelines have been identified and commented upon, Evidences of the required

reporting has been presented with suitable links.

The overall presentation of the report is easy to understand with the reporting available

online. However, as a user of sustainability reports, I would have preferred the entire

structured report to be located at one place and be available in a pdf format. This

expectation is similar to that of the annual report. The streamlined report in a pdf format

will enhance the understanding and thus improve the utility of the sustainable reporting.

The report helps in overall assessment of the G4 guidelines compliance as the

Compliance index is available at one place in both the years.

6

appropriate labelling of its products to ensure its compliance in respect of products

containing coin and button cell batteries in 2015. There were no such reported cases

in 2014.

G4-PR6 requires to report of the company is engaged in production and sale of any

products that are banned or under scrutiny for being banned. Wesfarmers has

disclosed in 2015 that they have stopped selling the controversial product “GTA5”

owing to complaints that the product depicts violence against women. However, in

2014 there were no such disclosures made by Wesfarmers in its sustainability report

of 2014.

Overall Wesfarmers have adhered to the material requirements under the G4 guidelines.

These sustainability reports has been verified by an independent accounting firm EY. The

assurance report is under limited scope to ensure the reporting is as per the criteria

specified under G4 guidelines and AA1000 Accountability Principles. Thus the

independent auditor has ensured that no information or evidence exists to negate the

information provided.

Wesfarmers has declared that they meet the reporting requirement “In Accordance” with

the G4-Guidelines Core option in 2015. IN 2014 the application level was B+ as per the

Global Reporting Initiative.

The referencing was inadequate in 2014 with the entire section linked to the various

data. The 2015 reporting is much more structured. The individual aspects and the

guidelines have been identified and commented upon, Evidences of the required

reporting has been presented with suitable links.

The overall presentation of the report is easy to understand with the reporting available

online. However, as a user of sustainability reports, I would have preferred the entire

structured report to be located at one place and be available in a pdf format. This

expectation is similar to that of the annual report. The streamlined report in a pdf format

will enhance the understanding and thus improve the utility of the sustainable reporting.

The report helps in overall assessment of the G4 guidelines compliance as the

Compliance index is available at one place in both the years.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part B: Fuji Xerox Comparison

I have analyzed the sustainability reports of Fuji Xerox Australia for 2014 and 2015. While

retrieving the report for 2015, I have noted that the report published was included I the

head quarter level sustainable report generated in Japan under Fuji Xerox. There were no

separate sustainability report published for the Australian operations as was the case for

2014.

On detailed study of the two level of reports available, I observed that the 2014 reports

were based on the guidelines as promulgated by the Global Reporting Initiative G4. The

2015 reports were based on these similar guidelines with an addition of additional

directives as issued by the Japanese Ministry of the Environment’s Environmental

Reporting Guidelines. My initial understanding is that though the overall guidelines were

same for the reports published in both the years, the 2015 report was tweaked to ensure

compliance with the local regulation governing such reporting and the overall global

reporting guidelines under Global Reporting Initiative G4 guidelines.

F4 Guidelines under the Global Reporting Initiative is designed to provide a

comprehensive reporting framework enabling the entities to report specific performance

against specific defined codes and norms. This ensures comparability and enhanced

understanding of the reports. The boundary within which the individual reporting of 2014

and 2015 operates affects the manner of sustainability reports for the respective years.

2014 report by Fuji Xerox Australia focuses on the Australian region whereas the

sustainability report for 2015 is much broader in scale encompassing the chain of

affiliates across the globe including Australia.

The detailed analysis of 2014 and 2015 reporting in relation to the G4 guidelines are tabulated as

below:

Particulars G4 Guidelines summary Evaluation

CEO

Statement

G4.1 = Statement from the top

authority preferably the CEO

confirming the significance of

sustainability for the business and

manner in which the company will

addresses the issue

Fuji Xerox has included a CEO

message on the sustainability

issues and the manner in which

the issues are being addressed by

the company in 2014 and 2015.

Crucial

Impact

G4.2 = Summary of key impact,

risks and opportunities for the

business

The 2014 report has been silent

on the key impact, risks and

opportunities of the business. The

2015 report has provided for the

relevant details for the entire

group under “Risk Management”

7

I have analyzed the sustainability reports of Fuji Xerox Australia for 2014 and 2015. While

retrieving the report for 2015, I have noted that the report published was included I the

head quarter level sustainable report generated in Japan under Fuji Xerox. There were no

separate sustainability report published for the Australian operations as was the case for

2014.

On detailed study of the two level of reports available, I observed that the 2014 reports

were based on the guidelines as promulgated by the Global Reporting Initiative G4. The

2015 reports were based on these similar guidelines with an addition of additional

directives as issued by the Japanese Ministry of the Environment’s Environmental

Reporting Guidelines. My initial understanding is that though the overall guidelines were

same for the reports published in both the years, the 2015 report was tweaked to ensure

compliance with the local regulation governing such reporting and the overall global

reporting guidelines under Global Reporting Initiative G4 guidelines.

F4 Guidelines under the Global Reporting Initiative is designed to provide a

comprehensive reporting framework enabling the entities to report specific performance

against specific defined codes and norms. This ensures comparability and enhanced

understanding of the reports. The boundary within which the individual reporting of 2014

and 2015 operates affects the manner of sustainability reports for the respective years.

2014 report by Fuji Xerox Australia focuses on the Australian region whereas the

sustainability report for 2015 is much broader in scale encompassing the chain of

affiliates across the globe including Australia.

The detailed analysis of 2014 and 2015 reporting in relation to the G4 guidelines are tabulated as

below:

Particulars G4 Guidelines summary Evaluation

CEO

Statement

G4.1 = Statement from the top

authority preferably the CEO

confirming the significance of

sustainability for the business and

manner in which the company will

addresses the issue

Fuji Xerox has included a CEO

message on the sustainability

issues and the manner in which

the issues are being addressed by

the company in 2014 and 2015.

Crucial

Impact

G4.2 = Summary of key impact,

risks and opportunities for the

business

The 2014 report has been silent

on the key impact, risks and

opportunities of the business. The

2015 report has provided for the

relevant details for the entire

group under “Risk Management”

7

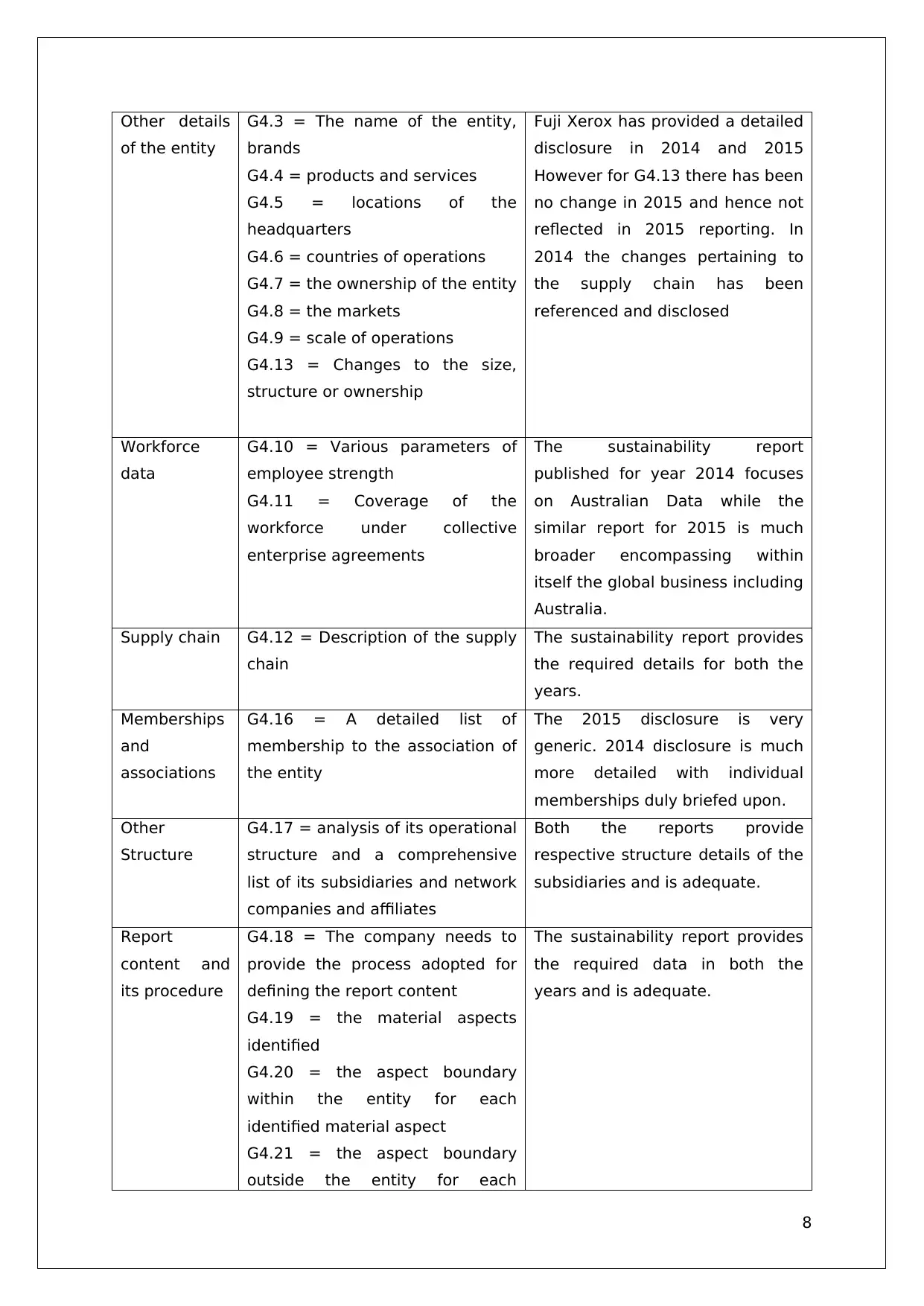

Other details

of the entity

G4.3 = The name of the entity,

brands

G4.4 = products and services

G4.5 = locations of the

headquarters

G4.6 = countries of operations

G4.7 = the ownership of the entity

G4.8 = the markets

G4.9 = scale of operations

G4.13 = Changes to the size,

structure or ownership

Fuji Xerox has provided a detailed

disclosure in 2014 and 2015

However for G4.13 there has been

no change in 2015 and hence not

reflected in 2015 reporting. In

2014 the changes pertaining to

the supply chain has been

referenced and disclosed

Workforce

data

G4.10 = Various parameters of

employee strength

G4.11 = Coverage of the

workforce under collective

enterprise agreements

The sustainability report

published for year 2014 focuses

on Australian Data while the

similar report for 2015 is much

broader encompassing within

itself the global business including

Australia.

Supply chain G4.12 = Description of the supply

chain

The sustainability report provides

the required details for both the

years.

Memberships

and

associations

G4.16 = A detailed list of

membership to the association of

the entity

The 2015 disclosure is very

generic. 2014 disclosure is much

more detailed with individual

memberships duly briefed upon.

Other

Structure

G4.17 = analysis of its operational

structure and a comprehensive

list of its subsidiaries and network

companies and affiliates

Both the reports provide

respective structure details of the

subsidiaries and is adequate.

Report

content and

its procedure

G4.18 = The company needs to

provide the process adopted for

defining the report content

G4.19 = the material aspects

identified

G4.20 = the aspect boundary

within the entity for each

identified material aspect

G4.21 = the aspect boundary

outside the entity for each

The sustainability report provides

the required data in both the

years and is adequate.

8

of the entity

G4.3 = The name of the entity,

brands

G4.4 = products and services

G4.5 = locations of the

headquarters

G4.6 = countries of operations

G4.7 = the ownership of the entity

G4.8 = the markets

G4.9 = scale of operations

G4.13 = Changes to the size,

structure or ownership

Fuji Xerox has provided a detailed

disclosure in 2014 and 2015

However for G4.13 there has been

no change in 2015 and hence not

reflected in 2015 reporting. In

2014 the changes pertaining to

the supply chain has been

referenced and disclosed

Workforce

data

G4.10 = Various parameters of

employee strength

G4.11 = Coverage of the

workforce under collective

enterprise agreements

The sustainability report

published for year 2014 focuses

on Australian Data while the

similar report for 2015 is much

broader encompassing within

itself the global business including

Australia.

Supply chain G4.12 = Description of the supply

chain

The sustainability report provides

the required details for both the

years.

Memberships

and

associations

G4.16 = A detailed list of

membership to the association of

the entity

The 2015 disclosure is very

generic. 2014 disclosure is much

more detailed with individual

memberships duly briefed upon.

Other

Structure

G4.17 = analysis of its operational

structure and a comprehensive

list of its subsidiaries and network

companies and affiliates

Both the reports provide

respective structure details of the

subsidiaries and is adequate.

Report

content and

its procedure

G4.18 = The company needs to

provide the process adopted for

defining the report content

G4.19 = the material aspects

identified

G4.20 = the aspect boundary

within the entity for each

identified material aspect

G4.21 = the aspect boundary

outside the entity for each

The sustainability report provides

the required data in both the

years and is adequate.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identified material aspect

Reporting

period details

G4.28 = Reporting period of the

company

G4.29 = previous report details

G4.30 = reporting cycle

G4.31 = point of contact for

addressing issues

The sustainability report provides

the required data in both the

years and is adequate.

Changes to

the entity

G4.22 = Summary of the changes

to the organization

G4.23 = Changes over the

previous period needs to be

summarized

There has been no change in

2015 and hence the G4.23

disclosure has not been made for

that year. In 2014, both the

disclosures have been provided.

Stakeholders’

engagement.

G4.24 = Details of the

stakeholders engaged into with

G4.25 = Basis of determining the

selected stakeholders to be

considered for further action

under this guideline

G4.26 = the approach identified

and selected by the entity

towards such engagement

G4.27 = summary of concerns

raised by stakeholders during

such engagement along with the

resolution details by the entity

The company has provided the

required details under the

Sustainability report published by

it. Thus the sustainability report

provides the required data in both

the years and is adequate.

Governance

structure

G4.34 = Review of the

governance structure on a regular

intervals

G4.35 = process of delegation of

authority and its effectiveness

G4.36 = Adoption of a committee

in charge of economic,

environmental and social impact

for reporting to such governance

G4.37 = Procedure of consultation

between stakeholders and such

governance body

G4.38 = Composition of the

governance body

G4.39 - whether CEO chairs such

The company has made the

required disclosures as covered

by the sustainability reporting

requirement. However, the

reporting is scattered across the

corporate website and the annual

report. The detailed sustainability

report, however, provides a

holistic view of the approach of

the company.

9

Reporting

period details

G4.28 = Reporting period of the

company

G4.29 = previous report details

G4.30 = reporting cycle

G4.31 = point of contact for

addressing issues

The sustainability report provides

the required data in both the

years and is adequate.

Changes to

the entity

G4.22 = Summary of the changes

to the organization

G4.23 = Changes over the

previous period needs to be

summarized

There has been no change in

2015 and hence the G4.23

disclosure has not been made for

that year. In 2014, both the

disclosures have been provided.

Stakeholders’

engagement.

G4.24 = Details of the

stakeholders engaged into with

G4.25 = Basis of determining the

selected stakeholders to be

considered for further action

under this guideline

G4.26 = the approach identified

and selected by the entity

towards such engagement

G4.27 = summary of concerns

raised by stakeholders during

such engagement along with the

resolution details by the entity

The company has provided the

required details under the

Sustainability report published by

it. Thus the sustainability report

provides the required data in both

the years and is adequate.

Governance

structure

G4.34 = Review of the

governance structure on a regular

intervals

G4.35 = process of delegation of

authority and its effectiveness

G4.36 = Adoption of a committee

in charge of economic,

environmental and social impact

for reporting to such governance

G4.37 = Procedure of consultation

between stakeholders and such

governance body

G4.38 = Composition of the

governance body

G4.39 - whether CEO chairs such

The company has made the

required disclosures as covered

by the sustainability reporting

requirement. However, the

reporting is scattered across the

corporate website and the annual

report. The detailed sustainability

report, however, provides a

holistic view of the approach of

the company.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

governance body

G4.40 = procedure to be elected

as a member of such governing

body

G4.41 = conflict resolution

mechanism

G4.42 = role of such body toward

vision, mission and strategy of the

company

G4.43 = checks to confirm that

optimum composition in terms of

knowledge and experience is

always maintained

G4.44 = performance evaluation

of such body as a whole and

individual members

G4.45 = role of such body in

identification and mitigation of

environmental, social and

economic risks

G4.46 = role in evaluation of

effectiveness of risk mitigation

procedures

G4.49 = Process of flagging off

concerns

G4.50 = Summary of such issues

Frequency of

review of risk

and

opportunities

G4.47

frequency of review of the

governance body’s role of the

economic, social and

environmental impacts,

opportunities and risk

No such specific disclosure has

been made in 2014 report.

However, the 2015 Sustainability

Report provides the details of

such frequency under the Risk

Management Section.

Review of the

report G4.48

Highest position responsible for

the formal review and approval of

the sustainable report before it is

published

No such specific disclosure has

been made in 2014 report.

However, inference can be made

from other disclosures that the

CEO would be responsible.

However, the 2015 Sustainability

Report provides the details of

such frequency under the Our

10

G4.40 = procedure to be elected

as a member of such governing

body

G4.41 = conflict resolution

mechanism

G4.42 = role of such body toward

vision, mission and strategy of the

company

G4.43 = checks to confirm that

optimum composition in terms of

knowledge and experience is

always maintained

G4.44 = performance evaluation

of such body as a whole and

individual members

G4.45 = role of such body in

identification and mitigation of

environmental, social and

economic risks

G4.46 = role in evaluation of

effectiveness of risk mitigation

procedures

G4.49 = Process of flagging off

concerns

G4.50 = Summary of such issues

Frequency of

review of risk

and

opportunities

G4.47

frequency of review of the

governance body’s role of the

economic, social and

environmental impacts,

opportunities and risk

No such specific disclosure has

been made in 2014 report.

However, the 2015 Sustainability

Report provides the details of

such frequency under the Risk

Management Section.

Review of the

report G4.48

Highest position responsible for

the formal review and approval of

the sustainable report before it is

published

No such specific disclosure has

been made in 2014 report.

However, inference can be made

from other disclosures that the

CEO would be responsible.

However, the 2015 Sustainability

Report provides the details of

such frequency under the Our

10

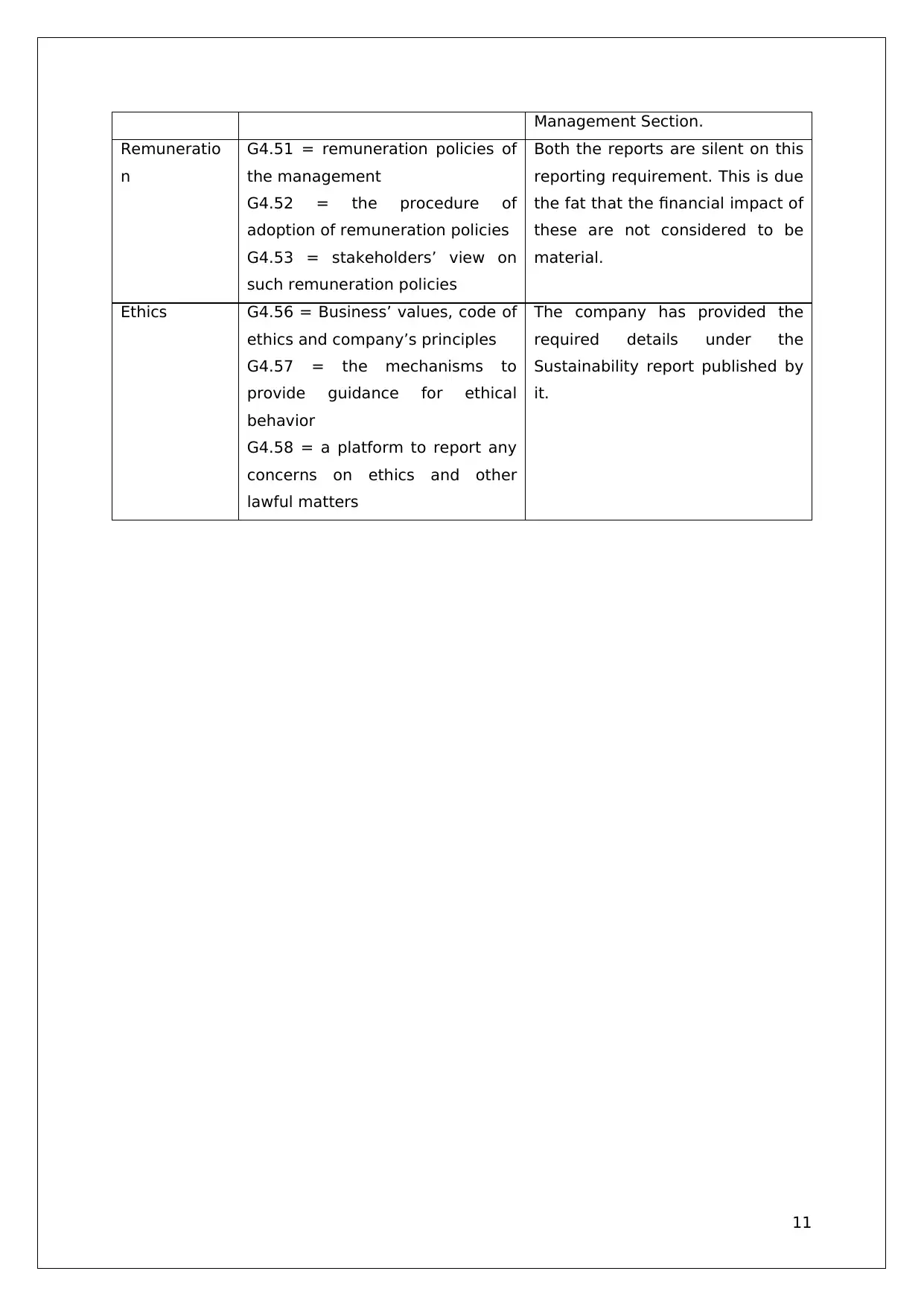

Management Section.

Remuneratio

n

G4.51 = remuneration policies of

the management

G4.52 = the procedure of

adoption of remuneration policies

G4.53 = stakeholders’ view on

such remuneration policies

Both the reports are silent on this

reporting requirement. This is due

the fat that the financial impact of

these are not considered to be

material.

Ethics G4.56 = Business’ values, code of

ethics and company’s principles

G4.57 = the mechanisms to

provide guidance for ethical

behavior

G4.58 = a platform to report any

concerns on ethics and other

lawful matters

The company has provided the

required details under the

Sustainability report published by

it.

11

Remuneratio

n

G4.51 = remuneration policies of

the management

G4.52 = the procedure of

adoption of remuneration policies

G4.53 = stakeholders’ view on

such remuneration policies

Both the reports are silent on this

reporting requirement. This is due

the fat that the financial impact of

these are not considered to be

material.

Ethics G4.56 = Business’ values, code of

ethics and company’s principles

G4.57 = the mechanisms to

provide guidance for ethical

behavior

G4.58 = a platform to report any

concerns on ethics and other

lawful matters

The company has provided the

required details under the

Sustainability report published by

it.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusions and Recommendations

Wesfarmers

The sustainability reporting for Wesfarmers have seen an improvement in 2015 over

2014. I have noted that the compliance index is much more descriptive and in line with

the specific guidelines of G4. The reports are available online in a scattered manner and

hence loose the important quality of ensuring understanding and keeping it simple. I

believe that the report should be also published in the form and manner of an annual

report of the Company. The pdf format of sustainable reports will enhance the user value

of such reports for my use. The company has not provided details on the percentage of

product categories for various reporting as it analyses and stores data on a division

basis. In such cases, Wesfarmers has specified a disclaimer that the required provisions

are not applicable. In these cases I recommend that the company should disclose the

details in the form and manner and in such detail available by the company. The

company should ensure going forward that the details are available at the level required

under G4 guidelines. Without the availability of such data, I believe that it would not be

prudent to conclude that the output would not be meaningful. Thus Wesfarmers should

strive to ensure that the data is available to the details required under G4.

Fuji Xerox

The sustainability report of Fuji Xerox for both the years has implied difference of the

scope. The 2014 report is much more decentralized and focuses on the Australian Entity

and its operations within Australia. 2015 report, on the other hand, is much broader in

scope and covers global operations under the umbrella of the Headquarters based in

Japan. The 2015 Sustainability Report considers the local environmental regulations and

reporting requirements of Japan in its scope. Thus the analysis and details provided for in

2015 report is much more comprehensive reflecting the underlying complex base of

operations in multiple countries.

The Sustainability Reports for both the years is streamlined under the umbrella principles

as provided by the Global Reporting Initiative G-4 Guidelines. The overall output may be

similar but the report for 2015 is much more complex.

12

Wesfarmers

The sustainability reporting for Wesfarmers have seen an improvement in 2015 over

2014. I have noted that the compliance index is much more descriptive and in line with

the specific guidelines of G4. The reports are available online in a scattered manner and

hence loose the important quality of ensuring understanding and keeping it simple. I

believe that the report should be also published in the form and manner of an annual

report of the Company. The pdf format of sustainable reports will enhance the user value

of such reports for my use. The company has not provided details on the percentage of

product categories for various reporting as it analyses and stores data on a division

basis. In such cases, Wesfarmers has specified a disclaimer that the required provisions

are not applicable. In these cases I recommend that the company should disclose the

details in the form and manner and in such detail available by the company. The

company should ensure going forward that the details are available at the level required

under G4 guidelines. Without the availability of such data, I believe that it would not be

prudent to conclude that the output would not be meaningful. Thus Wesfarmers should

strive to ensure that the data is available to the details required under G4.

Fuji Xerox

The sustainability report of Fuji Xerox for both the years has implied difference of the

scope. The 2014 report is much more decentralized and focuses on the Australian Entity

and its operations within Australia. 2015 report, on the other hand, is much broader in

scope and covers global operations under the umbrella of the Headquarters based in

Japan. The 2015 Sustainability Report considers the local environmental regulations and

reporting requirements of Japan in its scope. Thus the analysis and details provided for in

2015 report is much more comprehensive reflecting the underlying complex base of

operations in multiple countries.

The Sustainability Reports for both the years is streamlined under the umbrella principles

as provided by the Global Reporting Initiative G-4 Guidelines. The overall output may be

similar but the report for 2015 is much more complex.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part D: Reflective Journal of personal development

I have analysed the sustainability reports of Wesfarmers and Fuji Xerox for 2014 and

2015 period. This has been a crucial investment in time and effort to hone my

professional future. I have noted though the analysis that there has been a change in the

reporting requirement. The traditional form of reporting has evolved from mere financial

to annual reports to sustainable reports currently. I have always referred to the annual

report of the company to decide on the economic performance of the company. I have

realised that a company’s performance cannot be evaluated without realising its positive

and negative impacts. Analysis and understanding of the sustainability report has

helped me to understand that the true financial performance of the company

encompasses more than the profitability understanding. It is important that the impact of

the business on the society, people, community and environment are also evaluated. I

had an opportunity to go through the global reporting guidelines to understand the

overall requirements of a sustainable report. The comparison of these guidelines with the

real case scenarios in the form of actual published sustainability reports have helped me

to correctly understand the interpretations and actual implementation of the guidelines.

This understanding will help me in my future endeavours where my role might require

crucial inputs for preparation of sustainable reports.

The content and structure of the sustainability reports are governed by the G4-Guidelines

under the Global Reporting Initiative. The guidelines lists the comprehensive reporting

requirements with the flexibility for the reporting entity to pick and choose the required

disclosure on the basis of materiality. I have understood that all the requirement are not

mandatory. The principles of materiality guides the implementation of the guidelines. I

have noted that the sustainability reports needs to be supported by an assurance

statement by an independent specialist or the auditor. I believe this is necessary to lend

credibility to the non-financial information and related analysis disclosed by the

respective companies. The skills of data interpretation and comparison of the actual

disclosures with the underlying guidelines would be transferable to my workplace. These

skill sets gained will help me in performing any compliance related analysis and tasks in

my future workplace.

13

I have analysed the sustainability reports of Wesfarmers and Fuji Xerox for 2014 and

2015 period. This has been a crucial investment in time and effort to hone my

professional future. I have noted though the analysis that there has been a change in the

reporting requirement. The traditional form of reporting has evolved from mere financial

to annual reports to sustainable reports currently. I have always referred to the annual

report of the company to decide on the economic performance of the company. I have

realised that a company’s performance cannot be evaluated without realising its positive

and negative impacts. Analysis and understanding of the sustainability report has

helped me to understand that the true financial performance of the company

encompasses more than the profitability understanding. It is important that the impact of

the business on the society, people, community and environment are also evaluated. I

had an opportunity to go through the global reporting guidelines to understand the

overall requirements of a sustainable report. The comparison of these guidelines with the

real case scenarios in the form of actual published sustainability reports have helped me

to correctly understand the interpretations and actual implementation of the guidelines.

This understanding will help me in my future endeavours where my role might require

crucial inputs for preparation of sustainable reports.

The content and structure of the sustainability reports are governed by the G4-Guidelines

under the Global Reporting Initiative. The guidelines lists the comprehensive reporting

requirements with the flexibility for the reporting entity to pick and choose the required

disclosure on the basis of materiality. I have understood that all the requirement are not

mandatory. The principles of materiality guides the implementation of the guidelines. I

have noted that the sustainability reports needs to be supported by an assurance

statement by an independent specialist or the auditor. I believe this is necessary to lend

credibility to the non-financial information and related analysis disclosed by the

respective companies. The skills of data interpretation and comparison of the actual

disclosures with the underlying guidelines would be transferable to my workplace. These

skill sets gained will help me in performing any compliance related analysis and tasks in

my future workplace.

13

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.