Certificate IV in Finance and Mortgage Broking Assignment

VerifiedAdded on 2023/04/25

|69

|18731

|128

AI Summary

This document is an assignment for Certificate IV in Finance and Mortgage Broking (CIVMB_AS_v3A3). It includes instructions for completing and submitting the assignment, case studies, proposed loan details, and other relevant information. The case study 1 is about Clinton and Jennifer Andrews who want to purchase an investment property. The document also includes their financial and employment details, assets, liabilities, income, expenditure, and solicitor's details.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Assignment

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v3A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

CIVMB_AS_v3A3

Certificate IV in Finance and Mortgage Broking

(CIVMB_AS_v3A3)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

CIVMB_AS_v3A3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Result summary (assessor to complete)

First submission Resubmission (if required)

Section 1: Case study 1 —

Clinton and Jennifer Andrews

Task 1 — Initial disclosures Not yet demonstrated Not yet demonstrated

Task 2 — Gathering and documenting client information Not yet demonstrated Not yet demonstrated

Task 3 — Assessing the clients’ situation Not yet demonstrated Not yet demonstrated

Task 4 — Using equity Not yet demonstrated Not yet demonstrated

Task 5 — Reasonable enquiries Not yet demonstrated Not yet demonstrated

Task 6 — Recommendations Not yet demonstrated Not yet demonstrated

Task 7 — Clinton and Jennifer’s professional network Not yet demonstrated Not yet demonstrated

Task 8 — Interest rates Not yet demonstrated Not yet demonstrated

Task 9 — Settlement Not yet demonstrated Not yet demonstrated

Section 2: Case study 2 —

Tony and Lorraine Denton

Task 10 — Establishing level of financial knowledge Not yet demonstrated Not yet demonstrated

Task 11 — Responsible lending obligations Not yet demonstrated Not yet demonstrated

Task 12 — Self Employed special considerations Not yet demonstrated Not yet demonstrated

Task 13 — Advising on strategies Not yet demonstrated Not yet demonstrated

Task 14 — Impact of credit history Not yet demonstrated Not yet demonstrated

Task 15 — External dispute resolution Not yet demonstrated Not yet demonstrated

Task 16 — Effective access to files Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 69

First submission Resubmission (if required)

Section 1: Case study 1 —

Clinton and Jennifer Andrews

Task 1 — Initial disclosures Not yet demonstrated Not yet demonstrated

Task 2 — Gathering and documenting client information Not yet demonstrated Not yet demonstrated

Task 3 — Assessing the clients’ situation Not yet demonstrated Not yet demonstrated

Task 4 — Using equity Not yet demonstrated Not yet demonstrated

Task 5 — Reasonable enquiries Not yet demonstrated Not yet demonstrated

Task 6 — Recommendations Not yet demonstrated Not yet demonstrated

Task 7 — Clinton and Jennifer’s professional network Not yet demonstrated Not yet demonstrated

Task 8 — Interest rates Not yet demonstrated Not yet demonstrated

Task 9 — Settlement Not yet demonstrated Not yet demonstrated

Section 2: Case study 2 —

Tony and Lorraine Denton

Task 10 — Establishing level of financial knowledge Not yet demonstrated Not yet demonstrated

Task 11 — Responsible lending obligations Not yet demonstrated Not yet demonstrated

Task 12 — Self Employed special considerations Not yet demonstrated Not yet demonstrated

Task 13 — Advising on strategies Not yet demonstrated Not yet demonstrated

Task 14 — Impact of credit history Not yet demonstrated Not yet demonstrated

Task 15 — External dispute resolution Not yet demonstrated Not yet demonstrated

Task 16 — Effective access to files Not yet demonstrated Not yet demonstrated

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 69

Before you begin

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v3A3).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Section 1: Case study 1 — Clinton and Jennifer Andrews

– Task 1 — Initial disclosures

– Task 2 — Gathering and documenting client information

– Task 3 — Assessing the clients’ situation

– Task 4 — Using equity

– Task 5 — Reasonable enquiries

– Task 6 — Recommendations

– Task 7 — Clinton and Jennifer’s professional network

– Task 8 — Interest rates

– Task 9 — Settlement

• Section 2: Case study 2 — Tony and Lorraine Denton

– Task 10 — Establishing level of financial knowledge

– Task 11 — Responsible lending obligations

– Task 12 — Self Employed special considerations

– Task 13 — Advising on strategies

– Task 14 — Impact of credit history

– Task 15 — External dispute resolution

– Task 16 — Effective access to files

• Appendix 1: Client information collection tool/Fact Finder.

• Appendix 2: Serviceability calculator.

How to use the study plan

We recommend that you use the study plan for this subject; it will help you manage your time

effectively and complete the assignment within your enrolment period. Your study plan is in the

KapLearn Certificate IV in Finance and Mortgage Broking (CIVMBv3) subject room.

Page 3 of 69

Read everything in this document before you start your assignment for Certificate IV in Finance and

Mortgage Broking (CIVMB_AS_v3A3).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Section 1: Case study 1 — Clinton and Jennifer Andrews

– Task 1 — Initial disclosures

– Task 2 — Gathering and documenting client information

– Task 3 — Assessing the clients’ situation

– Task 4 — Using equity

– Task 5 — Reasonable enquiries

– Task 6 — Recommendations

– Task 7 — Clinton and Jennifer’s professional network

– Task 8 — Interest rates

– Task 9 — Settlement

• Section 2: Case study 2 — Tony and Lorraine Denton

– Task 10 — Establishing level of financial knowledge

– Task 11 — Responsible lending obligations

– Task 12 — Self Employed special considerations

– Task 13 — Advising on strategies

– Task 14 — Impact of credit history

– Task 15 — External dispute resolution

– Task 16 — Effective access to files

• Appendix 1: Client information collection tool/Fact Finder.

• Appendix 2: Serviceability calculator.

How to use the study plan

We recommend that you use the study plan for this subject; it will help you manage your time

effectively and complete the assignment within your enrolment period. Your study plan is in the

KapLearn Certificate IV in Finance and Mortgage Broking (CIVMBv3) subject room.

Page 3 of 69

Part 1: Instructions for completing and submitting

this assignment

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_CIVMBv3A3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete

all 16 tasks.

The information and data needed to complete Sections 1 and 2 is presented in case studies at the

beginning of those sections.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted,

although they must not be in conflict with the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements or to calculate any service fees that

may be applicable.

Page 4 of 69

this assignment

Completing the assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_CIVMBv3A3_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

The assignment

This assignment is split into 16 Tasks, over 3 Sections. To finish this assignment, you must complete

all 16 tasks.

The information and data needed to complete Sections 1 and 2 is presented in case studies at the

beginning of those sections.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the Client Information Collection Tool in Appendix 1, assumptions are permitted,

although they must not be in conflict with the information provided in the Case Study.

You may also be required to source additional information from other organisations in the finance industry

to find the right products or services to meet your client’s requirements or to calculate any service fees that

may be applicable.

Page 4 of 69

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Submitting the assignment

You must submit the completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be given an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv3) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assessing your responses to each question (and sub-parts if applicable) then determining whether you

have demonstrated competence in each question.

• Determining if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 69

You must submit the completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not delete/remove any sections of the document template.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete assignments will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be given an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv3) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed assignment.

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assessing your responses to each question (and sub-parts if applicable) then determining whether you

have demonstrated competence in each question.

• Determining if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

Page 5 of 69

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

When making changes to your original submission, use a different text colour for your resubmission.

This way, your assessor will be in a better position to gauge the quality and nature of your changes.

Ensure you leave your first assessor’s comments in your assignment, so your second assessor can see the

instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room.

Before you submit your assignment

If you have any queries about the assignment questions, please use the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer from your Tutor within 24 hours of posting your question.

Remember, your online tutor cannot preview or check your assignment answers, or provide specific answer

guidance. Please ensure that your questions are about clarification of the intent of an assignment question.

After your assignment has been assessed

If you have questions about your assessor’s feedback, please email: <studentadviser@kaplan.edu.au>

and include a copy of your assessed assignment. Never post your assignment answers or assessor

comments in the ‘Ask Your Tutor’ forum.

Page 6 of 69

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need to amend those

sections where the assessor has determined you are ‘not yet competent’.

When making changes to your original submission, use a different text colour for your resubmission.

This way, your assessor will be in a better position to gauge the quality and nature of your changes.

Ensure you leave your first assessor’s comments in your assignment, so your second assessor can see the

instructions that were originally provided for you. Do not change any comments made by a

Kaplan assessor.

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room.

Before you submit your assignment

If you have any queries about the assignment questions, please use the ‘Ask your Tutor’ forum in your

subject room. You can expect an answer from your Tutor within 24 hours of posting your question.

Remember, your online tutor cannot preview or check your assignment answers, or provide specific answer

guidance. Please ensure that your questions are about clarification of the intent of an assignment question.

After your assignment has been assessed

If you have questions about your assessor’s feedback, please email: <studentadviser@kaplan.edu.au>

and include a copy of your assessed assignment. Never post your assignment answers or assessor

comments in the ‘Ask Your Tutor’ forum.

Page 6 of 69

Section 1: Case study 1 — Clinton and Jennifer Andrews

Background

Clinton and Jennifer Andrews live in Sydney with their two school-age children. They bought their home

15 years ago. With the rise in its value over time they have generated substantial equity and have decided

to purchase an investment property. Recently they went to a real estate seminar where the presenter

explained that it is possible with correct leverage to purchase more than one investment property.

Consequently, they have decided to borrow 90% LVR on the investment property plus the LMI. The deposit,

stamp duties and other costs will come from their ‘offset account’ attached to their home loan. They have

requested not to use their current lender.

After conducting research over the last six months they have decided to purchase a new four-bedroom

home in outer Brisbane for $450,000 with a rental income of $450.00 per week.

The real estate agent has recommended they contact you to arrange their finance. Their accountant has

been providing some advice in relation to negative gearing benefits.

The following tables are a summary of the details obtained from the couple during the fact find interview.

The details provided include a description of the property they wish to purchase, their financial and

employment details and the loan features that they require.

The investment property

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Purchase price: $450,000

Description: 4-bedroom brick veneer home

Rent: $450.00 per week

Agent details: Rain and Hall

Phone: 07 9322 1113

Mobile: 0412 880 088

The borrower’s home address

Current address: 17 Moss Ave, East Hills, NSW 2213

Description: 5-bedroom full brick home

Value: $850,000

Mortgage: $190,000

Monthly repayment: $1,020.00 per month

Home phone: 02 6051 2121

Clients’ view of funding requirements

Purchase price: $450,000

Estimated costs: $20,000

Total required: $470,000

Loan: $405,000 + LMI

Own contribution: $65,000

Page 7 of 69

Background

Clinton and Jennifer Andrews live in Sydney with their two school-age children. They bought their home

15 years ago. With the rise in its value over time they have generated substantial equity and have decided

to purchase an investment property. Recently they went to a real estate seminar where the presenter

explained that it is possible with correct leverage to purchase more than one investment property.

Consequently, they have decided to borrow 90% LVR on the investment property plus the LMI. The deposit,

stamp duties and other costs will come from their ‘offset account’ attached to their home loan. They have

requested not to use their current lender.

After conducting research over the last six months they have decided to purchase a new four-bedroom

home in outer Brisbane for $450,000 with a rental income of $450.00 per week.

The real estate agent has recommended they contact you to arrange their finance. Their accountant has

been providing some advice in relation to negative gearing benefits.

The following tables are a summary of the details obtained from the couple during the fact find interview.

The details provided include a description of the property they wish to purchase, their financial and

employment details and the loan features that they require.

The investment property

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Purchase price: $450,000

Description: 4-bedroom brick veneer home

Rent: $450.00 per week

Agent details: Rain and Hall

Phone: 07 9322 1113

Mobile: 0412 880 088

The borrower’s home address

Current address: 17 Moss Ave, East Hills, NSW 2213

Description: 5-bedroom full brick home

Value: $850,000

Mortgage: $190,000

Monthly repayment: $1,020.00 per month

Home phone: 02 6051 2121

Clients’ view of funding requirements

Purchase price: $450,000

Estimated costs: $20,000

Total required: $470,000

Loan: $405,000 + LMI

Own contribution: $65,000

Page 7 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

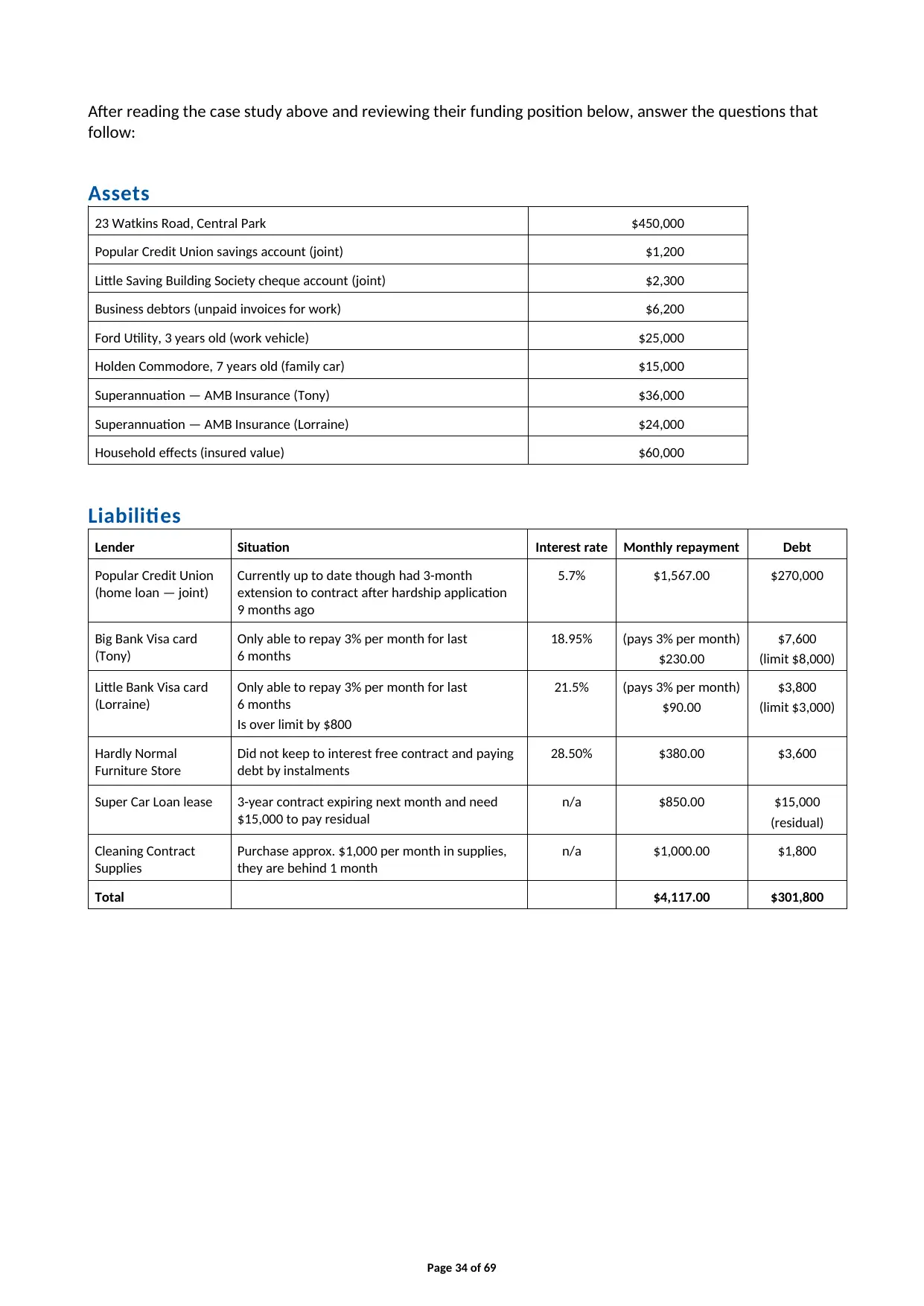

Assets

Big Bank offset savings account (joint) $180,000

Little Bank fixed term account (joint) $10,000

Ford Falcon G6, 8 years old (Clinton) $15,000

Holden Barina, 10 years old (Jennifer) $5,000

Superannuation — MPA Insurance (Clinton) $82,000

Superannuation — CLM Insurance (Jennifer) $54,000

Household effects (insured value) $80,000

Liabilities

Big Bank standard home loan (Joint)

(P&I repayment, variable, no fees)

5.0% $190,000 (repayments $1,020 p.m.)

Big Bank Visa card (Clinton) 18.5% $800 (limit $5,000) (clears monthly)

Little Bank Visa card (Jennifer) 12.9% $1,200 (limit $3,000) (pays $500 per month)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment for servicing purposes should be calculated at 3% of the credit limit.

Income/employment

Clinton (date of birth 24/5/84)

Position: Project Manager (full time)

Employer: ACM Construction

10 Wide Rd, Ryde, NSW

Phone: 02 7061 2111

Income (gross): $85,000 p.a., gross monthly income of $7,083, net monthly income of $5,476

Employer contact: Kelly Williams, HR Manager

Length of service: 16 years

Driver’s licence: 8869KL

Email: clinta@acm.com.au

Jennifer (date of birth 8/10/87)

Position: Accounts Assistant (full time)

Employer: Pretty Clothing Pty Ltd

80 High Street, Penrith, NSW

Phone: 02 9940 3677

Income (gross): $74,000 p.a., gross monthly income of $6,166, net monthly income of $4,837

Employer contact: Joan Collins, HR Manager

Length of service: 7 years

Driver’s licence: 2897HT

Email: Jennya@pc.com.au

Page 8 of 69

Big Bank offset savings account (joint) $180,000

Little Bank fixed term account (joint) $10,000

Ford Falcon G6, 8 years old (Clinton) $15,000

Holden Barina, 10 years old (Jennifer) $5,000

Superannuation — MPA Insurance (Clinton) $82,000

Superannuation — CLM Insurance (Jennifer) $54,000

Household effects (insured value) $80,000

Liabilities

Big Bank standard home loan (Joint)

(P&I repayment, variable, no fees)

5.0% $190,000 (repayments $1,020 p.m.)

Big Bank Visa card (Clinton) 18.5% $800 (limit $5,000) (clears monthly)

Little Bank Visa card (Jennifer) 12.9% $1,200 (limit $3,000) (pays $500 per month)

All debts have been repaid according to arrangements. In relation to the credit card debt, the minimum

monthly commitment for servicing purposes should be calculated at 3% of the credit limit.

Income/employment

Clinton (date of birth 24/5/84)

Position: Project Manager (full time)

Employer: ACM Construction

10 Wide Rd, Ryde, NSW

Phone: 02 7061 2111

Income (gross): $85,000 p.a., gross monthly income of $7,083, net monthly income of $5,476

Employer contact: Kelly Williams, HR Manager

Length of service: 16 years

Driver’s licence: 8869KL

Email: clinta@acm.com.au

Jennifer (date of birth 8/10/87)

Position: Accounts Assistant (full time)

Employer: Pretty Clothing Pty Ltd

80 High Street, Penrith, NSW

Phone: 02 9940 3677

Income (gross): $74,000 p.a., gross monthly income of $6,166, net monthly income of $4,837

Employer contact: Joan Collins, HR Manager

Length of service: 7 years

Driver’s licence: 2897HT

Email: Jennya@pc.com.au

Page 8 of 69

Interest income

Approximately $30 per month from the $10,000 term deposit, interest of 3.5% p.a.

Expenditure

Monthly expenditure for living expenses — $3,200.

Solicitor’s details

Jackson & Williams

28 West Street, Yagoona, NSW

Phone: 02 9283 1365

Fax: 02 9283 1802

Note: The solicitor has quoted $1,500 to cover estimates costs.

Proposed loan details

• application fee — $600.00 (includes valuation)

• 30-year term

• principal and interest

• residential investment loan

• standard variable interest rate of 5.68% (comparison 5.82%), special offer rate of 4.78%

(5.16% comparison) (Note: Clinton & Jennifer will qualify for this special loan offer.)

• proposed settlement date — 6 weeks’ time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• internet banking.

Page 9 of 69

Approximately $30 per month from the $10,000 term deposit, interest of 3.5% p.a.

Expenditure

Monthly expenditure for living expenses — $3,200.

Solicitor’s details

Jackson & Williams

28 West Street, Yagoona, NSW

Phone: 02 9283 1365

Fax: 02 9283 1802

Note: The solicitor has quoted $1,500 to cover estimates costs.

Proposed loan details

• application fee — $600.00 (includes valuation)

• 30-year term

• principal and interest

• residential investment loan

• standard variable interest rate of 5.68% (comparison 5.82%), special offer rate of 4.78%

(5.16% comparison) (Note: Clinton & Jennifer will qualify for this special loan offer.)

• proposed settlement date — 6 weeks’ time

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• internet banking.

Page 9 of 69

Assignment tasks (student to complete)

Task 1 — Initial disclosures

Following a personal introduction and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker.

These disclosures include the way you are remunerated and the range and limitation of your services.

1. There are four (4) documents listed in ASIC Information sheet INFO 146 ‘Responsible lending disclosure

obligations – Overview for credit licensees and representatives’ that must be provided to customers.

Refer to this Information sheet and the information contained in your topic notes to answer part (a) and

(b) below.

(a) Identify which of these four (4) documents you must provide your client before you commence

providing credit assistance and explain the main disclosures relevant to that document.

(40 words)

Student response to Task 1: Question 1(a)

Before you initiate giving credit guide you should give a Credit Guide to a customer. Credit guide gives

initial informaiton about you to a client. The time at which you need to give a credit guide will rely upon

what sort of entity you are and what credit exercises you take part in, yet will by and large be before you

take part in acknowledge exercises for the buyer

Credit Guide generally must include:

• your name, contact details and Australian credit permit number or credit agent number, and

information about your procedure for settling debate with a buyer, including contact details to get to:

• your inside debate goals (IDR) procedure, and

• the EDR plan of which you are a part.

There are also additional obligations, depending on the type of entity as listed in Aisc Information sheet

INFO 146

Page 10 of 69

Task 1 — Initial disclosures

Following a personal introduction and before you begin gathering information about the clients’ existing

financial situation or needs, there are certain disclosures you are required to make as a finance broker.

These disclosures include the way you are remunerated and the range and limitation of your services.

1. There are four (4) documents listed in ASIC Information sheet INFO 146 ‘Responsible lending disclosure

obligations – Overview for credit licensees and representatives’ that must be provided to customers.

Refer to this Information sheet and the information contained in your topic notes to answer part (a) and

(b) below.

(a) Identify which of these four (4) documents you must provide your client before you commence

providing credit assistance and explain the main disclosures relevant to that document.

(40 words)

Student response to Task 1: Question 1(a)

Before you initiate giving credit guide you should give a Credit Guide to a customer. Credit guide gives

initial informaiton about you to a client. The time at which you need to give a credit guide will rely upon

what sort of entity you are and what credit exercises you take part in, yet will by and large be before you

take part in acknowledge exercises for the buyer

Credit Guide generally must include:

• your name, contact details and Australian credit permit number or credit agent number, and

information about your procedure for settling debate with a buyer, including contact details to get to:

• your inside debate goals (IDR) procedure, and

• the EDR plan of which you are a part.

There are also additional obligations, depending on the type of entity as listed in Aisc Information sheet

INFO 146

Page 10 of 69

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(b) Identify which of these four documents you will provide the client should you intend to charge a

broker fee and explain what is required for it to be valid. (40 words)

Student response to Task 1: Question 1(b)

Expect to charge a broker fee, at that point it must be clearly referenced and clarified in the statement that

you will give to a client. The statement should mention the following.

- For which service the fee will be charged.

- Express plainly the amount of the fee will be charged.

- Mention when fee is payable.

It is require to marked by the client upon acknowledgment and give duplicate.

Assessor feedback: Resubmission required?

No

Task 2 — Gathering and documenting client information

Complete the Client Information Collection Tool (located at the end of the assignment in Appendix 1)

using the information provided in Case Study 1.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback: Resubmission required?

No

Task 3 — Assessing the clients’ situation

1. Using the Excel or Online version of the Genworth Serviceability Calculator, calculate the Genworth NDI

for the borrowers. This will require you to enter all the data, including their future rental income.

<http://www.genworth.com.au/online-tools-forms-and-reports/lmi-tools/serviceability-calculator>.

Once you have completed the calculations, copy the data into the Serviceability Calculator

(located at the end of this assignment in Appendix 2).

Do not upload the Excel spreadsheet as a separate file.

Assessor feedback: Resubmission required?

No

Page 11 of 69

broker fee and explain what is required for it to be valid. (40 words)

Student response to Task 1: Question 1(b)

Expect to charge a broker fee, at that point it must be clearly referenced and clarified in the statement that

you will give to a client. The statement should mention the following.

- For which service the fee will be charged.

- Express plainly the amount of the fee will be charged.

- Mention when fee is payable.

It is require to marked by the client upon acknowledgment and give duplicate.

Assessor feedback: Resubmission required?

No

Task 2 — Gathering and documenting client information

Complete the Client Information Collection Tool (located at the end of the assignment in Appendix 1)

using the information provided in Case Study 1.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback: Resubmission required?

No

Task 3 — Assessing the clients’ situation

1. Using the Excel or Online version of the Genworth Serviceability Calculator, calculate the Genworth NDI

for the borrowers. This will require you to enter all the data, including their future rental income.

<http://www.genworth.com.au/online-tools-forms-and-reports/lmi-tools/serviceability-calculator>.

Once you have completed the calculations, copy the data into the Serviceability Calculator

(located at the end of this assignment in Appendix 2).

Do not upload the Excel spreadsheet as a separate file.

Assessor feedback: Resubmission required?

No

Page 11 of 69

2. Based on the information provided in the case study and using the tools available to you

(e.g. loan calculators, including those available on lenders’ websites), provide an assessment

of the clients’ borrowing ability. Consider and comment on the following issues:

(a) the maximum loan using the Genworth calculator

(b) deposit requirements for the loan required

(c) combined net monthly income, less cost of living expense as specified by the borrower

(d) do they require Lenders Mortgage Insurance (LMI) and if so, how much will it cost?

Refer to Genworth LMI estimator for this figure

(e) any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions.

(No word count requirement for questions (a) to (d)).

Question (e) (100 words)

Student response to Task 3: Question 2(a)

$798666.00

Student response to Task 3: Question 2(b)

$45000.00

Student response to Task 3: Question 2(c)

Joined net month to month Income $5476 + $4837 = $10313 (*12) =$123756.00

Less month to month costs of living $3,200 (*12)=$38,400

Joined net month to month salary after removing everyday costs $7113 (*12)=$85356.00

Student response to Task 3: Question 2(d)

LMI is require. It will cost $8627.00 plus stamp duty or $43.00 every month if premium promoted

Student response to Task 3: Question 2(e)

Following are mentioned points could be the reasons that may impact on clients ability to meet their

obligations

1. Clinton and/or accomplice may loose their job.

2. Construction industry is directly relative to monetary conditions in Australia. With back off in

development industry, Clinton's business has great shot of getting influenced and income may

reduce.

3. Clothing industry is chiefly retail. It is likewise focused industry. Most assembling is being sent

to abroad to diminish the expense. Expecting that Pretty Clothing as of now fabricates the item

in Australia, in vain Jennifer's activity could be affected with conceivable rebuilding. In any case,

the odds are less.

4. Property remain empty for long time without inhabitant. This would reduce their income and

their capacity to pay the home loan reimbursement.

5. In that case lease should be diminished to pull in occupant.

Page 12 of 69

(e.g. loan calculators, including those available on lenders’ websites), provide an assessment

of the clients’ borrowing ability. Consider and comment on the following issues:

(a) the maximum loan using the Genworth calculator

(b) deposit requirements for the loan required

(c) combined net monthly income, less cost of living expense as specified by the borrower

(d) do they require Lenders Mortgage Insurance (LMI) and if so, how much will it cost?

Refer to Genworth LMI estimator for this figure

(e) any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions.

(No word count requirement for questions (a) to (d)).

Question (e) (100 words)

Student response to Task 3: Question 2(a)

$798666.00

Student response to Task 3: Question 2(b)

$45000.00

Student response to Task 3: Question 2(c)

Joined net month to month Income $5476 + $4837 = $10313 (*12) =$123756.00

Less month to month costs of living $3,200 (*12)=$38,400

Joined net month to month salary after removing everyday costs $7113 (*12)=$85356.00

Student response to Task 3: Question 2(d)

LMI is require. It will cost $8627.00 plus stamp duty or $43.00 every month if premium promoted

Student response to Task 3: Question 2(e)

Following are mentioned points could be the reasons that may impact on clients ability to meet their

obligations

1. Clinton and/or accomplice may loose their job.

2. Construction industry is directly relative to monetary conditions in Australia. With back off in

development industry, Clinton's business has great shot of getting influenced and income may

reduce.

3. Clothing industry is chiefly retail. It is likewise focused industry. Most assembling is being sent

to abroad to diminish the expense. Expecting that Pretty Clothing as of now fabricates the item

in Australia, in vain Jennifer's activity could be affected with conceivable rebuilding. In any case,

the odds are less.

4. Property remain empty for long time without inhabitant. This would reduce their income and

their capacity to pay the home loan reimbursement.

5. In that case lease should be diminished to pull in occupant.

Page 12 of 69

6. Possibilities of sudden family costs which were not arranged for example sickness.

7. Possibilities of sudden episode that can confine the capacity of Clinton or Jennifer to have the

capacity to work fulltime.

8. Interest rates can ascend higher than considered for diminishing their functionality of home

loan.

9. Family circumstance can change for instance another child conceived, separation , supporting

old parents and so forth.

10. Unexpected property fixes or cost of settling any damages caused by tenant, with scenario

landlord insurance is not in place.

Assessor feedback: Resubmission required?

No

Page 13 of 69

7. Possibilities of sudden episode that can confine the capacity of Clinton or Jennifer to have the

capacity to work fulltime.

8. Interest rates can ascend higher than considered for diminishing their functionality of home

loan.

9. Family circumstance can change for instance another child conceived, separation , supporting

old parents and so forth.

10. Unexpected property fixes or cost of settling any damages caused by tenant, with scenario

landlord insurance is not in place.

Assessor feedback: Resubmission required?

No

Page 13 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 4 — Using equity

1. Although Clinton and Jennifer have chosen to borrow 90% LVR on the investment property plus the

LMI costs, what other option could you present that would avoid the cost of LMI? (100 words)

Student response to Task 4: Question 1

Assets from balance record can be utilized to lessen LVR to 80% consequently sparing LMI, as they have

adequate finances accessible in counterbalanced record.

To keep LVR to 80%, they can obtain $360000.00 and pay staying 20% ($90,000) on top different expenses

from their counterbalance account. Hense, spare them LMI premium of $8627.00

Assessor feedback: Resubmission required?

No

2. Explain how it could be possible for Clinton and Jennifer to borrow 100% of the purchase price

($450,000) and obtain a tax benefit for the interest charged. (100 words)

Student response to Task 4: Question 2

A)

Estimation of their house is $850,000

Home loan balance is $190,000

Equity is $660,000 in their home.

Clinton and Jennifer can setup a Line of Credit of $90,000 to pay for the 20% of the advance and obtain

80%. The interest paid on credit extension can be deducted as expense and will decrease the assessment

on pay.

They are equipped for administration this Line of Credit, as they have the usefulness as to serviceability

calculation done before.

B)

They can utilize the equity from their home to get 100% on the venture advance.

Asset Value $850,000+$450,000 = $1,300,000

Loan $190,000+$450,000 = $640,000 (100%borrowing for investment property)

LVR = 49.23%

They have the usefulness according to the functionality estimation.

B is the better choice for them as the financing cost on LoC is higher than home loan.

Assessor feedback: Resubmission required?

No

Page 14 of 69

1. Although Clinton and Jennifer have chosen to borrow 90% LVR on the investment property plus the

LMI costs, what other option could you present that would avoid the cost of LMI? (100 words)

Student response to Task 4: Question 1

Assets from balance record can be utilized to lessen LVR to 80% consequently sparing LMI, as they have

adequate finances accessible in counterbalanced record.

To keep LVR to 80%, they can obtain $360000.00 and pay staying 20% ($90,000) on top different expenses

from their counterbalance account. Hense, spare them LMI premium of $8627.00

Assessor feedback: Resubmission required?

No

2. Explain how it could be possible for Clinton and Jennifer to borrow 100% of the purchase price

($450,000) and obtain a tax benefit for the interest charged. (100 words)

Student response to Task 4: Question 2

A)

Estimation of their house is $850,000

Home loan balance is $190,000

Equity is $660,000 in their home.

Clinton and Jennifer can setup a Line of Credit of $90,000 to pay for the 20% of the advance and obtain

80%. The interest paid on credit extension can be deducted as expense and will decrease the assessment

on pay.

They are equipped for administration this Line of Credit, as they have the usefulness as to serviceability

calculation done before.

B)

They can utilize the equity from their home to get 100% on the venture advance.

Asset Value $850,000+$450,000 = $1,300,000

Loan $190,000+$450,000 = $640,000 (100%borrowing for investment property)

LVR = 49.23%

They have the usefulness according to the functionality estimation.

B is the better choice for them as the financing cost on LoC is higher than home loan.

Assessor feedback: Resubmission required?

No

Page 14 of 69

Page 15 of 69

Task 5 — Reasonable enquiries

In the course of gathering information about the couple, you are required under the National Consumer

Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s objectives,

requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study and

explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 5

Following are the reasonable enquiries which determine Clinton and Jennifer’s objectives, requirement and

financial situation:-

PAYG – Clinton and Jennifer both are working.ThereforePAYGevidence to gather. It incorporates 2

most recent pay slips, duplicates of assessment forms for most recent two years. Additionally

affirmation of work status by calling the employer.

Assess record from credit organization. This will demonstrate their capacity and promise to keep up

a decent record as a consumer by paying bills and different installments on time.

Sparing history and use structures. Need to ask for copies of bank enunciations, for instance,

venture reserves, charge card and home advance records. Regardless of the way that they have

made sense of how to save resources in offset account, see that their expenses are planning with

their projections. Also check for any costs that are not articulated or missed by them.

Current residential situation to study for number of wards or any plans that can influence their

ability to profit the development in future.

Income delivering action, age and dialect aptitudes. To show signs of improvement comprehension

of their activity circumstance, industry situation and their capacity to continue in the activity or in

the event that they have plan to change employment or industry.

Their data of fund market and the sum they comprehend the features of an explicit credit item and

hazard related with it, for their conditions.

Additional affirmation may be required where the information outfitted is clashing with the

information recently gave, or outside the extent of satisfactory benchmarks.

These enquiries are crucial for NCCP consistence as NCCP act powers careful pending duty that

requires credit provider to ensure that a credit office is ' not inadmissible' for the borrower. It is the

credit provider's commitment to make an authentic and sensible evaluation that results in a

decision that they can ensure.

A credit supplier must

Make sensible enquiries about the customer's cash related situation, necessities and goals.

Take sensible steps to affirm the customer's present cash related situation

Decide whether the credit get the customer is requesting is 'not unacceptable' for that customer.

Credit help gives e.g. Home loan Brokers, must make a starter examination and Credit provider must make

a last assessment of the credit contract before credit is promoted.

Page 16 of 69

In the course of gathering information about the couple, you are required under the National Consumer

Credit Protection Act 2009 to make all ‘reasonable’ enquiries to determine a borrower’s objectives,

requirements and financial situation.

Identify at least six (6) ‘reasonable’ enquiries that you would make with the clients in the case study and

explain why these enquiries are important in terms of NCCP compliance. (200 words)

Student response to Task 5

Following are the reasonable enquiries which determine Clinton and Jennifer’s objectives, requirement and

financial situation:-

PAYG – Clinton and Jennifer both are working.ThereforePAYGevidence to gather. It incorporates 2

most recent pay slips, duplicates of assessment forms for most recent two years. Additionally

affirmation of work status by calling the employer.

Assess record from credit organization. This will demonstrate their capacity and promise to keep up

a decent record as a consumer by paying bills and different installments on time.

Sparing history and use structures. Need to ask for copies of bank enunciations, for instance,

venture reserves, charge card and home advance records. Regardless of the way that they have

made sense of how to save resources in offset account, see that their expenses are planning with

their projections. Also check for any costs that are not articulated or missed by them.

Current residential situation to study for number of wards or any plans that can influence their

ability to profit the development in future.

Income delivering action, age and dialect aptitudes. To show signs of improvement comprehension

of their activity circumstance, industry situation and their capacity to continue in the activity or in

the event that they have plan to change employment or industry.

Their data of fund market and the sum they comprehend the features of an explicit credit item and

hazard related with it, for their conditions.

Additional affirmation may be required where the information outfitted is clashing with the

information recently gave, or outside the extent of satisfactory benchmarks.

These enquiries are crucial for NCCP consistence as NCCP act powers careful pending duty that

requires credit provider to ensure that a credit office is ' not inadmissible' for the borrower. It is the

credit provider's commitment to make an authentic and sensible evaluation that results in a

decision that they can ensure.

A credit supplier must

Make sensible enquiries about the customer's cash related situation, necessities and goals.

Take sensible steps to affirm the customer's present cash related situation

Decide whether the credit get the customer is requesting is 'not unacceptable' for that customer.

Credit help gives e.g. Home loan Brokers, must make a starter examination and Credit provider must make

a last assessment of the credit contract before credit is promoted.

Page 16 of 69

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Assessor feedback: Resubmission required?

No

Page 17 of 69

No

Page 17 of 69

Task 6 — Recommendations

Note: Incorrect or uninformed advice can lead to significant financial detriment for your client and lead to

possible complaints against you for misleading or deceptive and misleading conduct. Therefore, all three (3)

questions of this task are ‘critical’ and you must demonstrate the required knowledge in each to be deemed

competent.

1. Based on the information presented in the case study, prepare a written proposal (letter or email)

outlining your proposal to clients. (750 words)

The style and language used in the proposal should be appropriate to the case study client’s level of

understanding. It should be clear and concise and written in language that is easy to understand,

while still remaining professional in its presentation.

You may base your response to this part of the assignment either on your knowledge of the products

currently offered by your own organisation or on the products offered by a lender you have researched.

In your proposal, you should include:

• a summary of your understanding of the clients’ needs (this could be an outline summary of their

proposed loan structure)

• a summary of their current financial position (use information from the ‘funds to complete’ template

completed in Appendix 1)

• the product options you have considered that meet their needs (research two lenders and detail

their loan features; you can use the internet or if working in industry, internal software)

• the option you recommend and the reasons for the recommendation — explain how the

recommended product meets the clients’ needs (refer to the case study and explain why you are

recommending this lender)

• disclosures applicable to the situation (a summary of likely applicable disclosures is adequate).

Include disclosures in the Credit Guide and any conflicts of interest.

Note: List any assumptions you have made about the clients and their situation in order to complete this

part of the assignment. There are no rules regarding the format. Please use the format that best suits

you. Should you require it, an example of a written proposal format has been provided in topic 3.3.

Note that the credit guide in your resources is not a ‘written proposal’.

Student response to Task 6: Question 1

By Email

Subject: Loan Proposal for Clinton and Jennifer Andrews

Dear Clinton and Jennifer,

I am writing this email to state thank you for the opportunity.

It has been a joy working with you to comprehend your prerequisites and intent for an suitable loan for

your investment property. In light of your prerequisites and destinations I am satisfied to present a

proposition with two alternatives that are suitable. If you don't mind review the two choices cautiously

before choosing which one you need to continue with.

To continue with, You have to give your acknowledgment by marking a duplicate of the proposition and

returning back to me by email.

Page 18 of 69

Note: Incorrect or uninformed advice can lead to significant financial detriment for your client and lead to

possible complaints against you for misleading or deceptive and misleading conduct. Therefore, all three (3)

questions of this task are ‘critical’ and you must demonstrate the required knowledge in each to be deemed

competent.

1. Based on the information presented in the case study, prepare a written proposal (letter or email)

outlining your proposal to clients. (750 words)

The style and language used in the proposal should be appropriate to the case study client’s level of

understanding. It should be clear and concise and written in language that is easy to understand,

while still remaining professional in its presentation.

You may base your response to this part of the assignment either on your knowledge of the products

currently offered by your own organisation or on the products offered by a lender you have researched.

In your proposal, you should include:

• a summary of your understanding of the clients’ needs (this could be an outline summary of their

proposed loan structure)

• a summary of their current financial position (use information from the ‘funds to complete’ template

completed in Appendix 1)

• the product options you have considered that meet their needs (research two lenders and detail

their loan features; you can use the internet or if working in industry, internal software)

• the option you recommend and the reasons for the recommendation — explain how the

recommended product meets the clients’ needs (refer to the case study and explain why you are

recommending this lender)

• disclosures applicable to the situation (a summary of likely applicable disclosures is adequate).

Include disclosures in the Credit Guide and any conflicts of interest.

Note: List any assumptions you have made about the clients and their situation in order to complete this

part of the assignment. There are no rules regarding the format. Please use the format that best suits

you. Should you require it, an example of a written proposal format has been provided in topic 3.3.

Note that the credit guide in your resources is not a ‘written proposal’.

Student response to Task 6: Question 1

By Email

Subject: Loan Proposal for Clinton and Jennifer Andrews

Dear Clinton and Jennifer,

I am writing this email to state thank you for the opportunity.

It has been a joy working with you to comprehend your prerequisites and intent for an suitable loan for

your investment property. In light of your prerequisites and destinations I am satisfied to present a

proposition with two alternatives that are suitable. If you don't mind review the two choices cautiously

before choosing which one you need to continue with.

To continue with, You have to give your acknowledgment by marking a duplicate of the proposition and

returning back to me by email.

Page 18 of 69

If it's not too much trouble don't hesitate to get in touch with me should you have any inquiries.

Loan Proposal for Clinton and Jennifer Andrews

Requirements and Objectives:

Clinton and Jennifer are trying to buy another investment property. The property is another four-bedroom

home in external Brisbane situated at 29 Pacific Drive, Ipswich, Queensland 4305.

Property purchase price: $450000.00

Proposed settlement: 6 weeks time from date of sale.

Looking to borrow: 90% of the purchase price with LMI.

Remaining 10% and other purchasing cost will be supported from customer's counterbalanced record.

Offset account balance: $180,000.

They are looking at a resident investment loan, P&I for 30 year term with ability to make additional

payments from timt t time without any penalty redraw facility, internet banking and fortnightly repayment

options.

Applicant Details

Applicant One Applicant Two

First Name Clinton Jennifer

Surname Andrews Andrews

Date of Birth XX/XX/XXXX XX/XX/XXXX

Number & Age of Dependants 2 (12, 10) 2 (12, 10)

Relationship to other Applicant Husband Wife

Mobile/Phone 02 6051 2121 02 6051 2121

Email clinta@acm.com.au jennya@pc.com.au

Current Address 17 Moss Ave, East Hills, NSW 2213 17 Moss Ave, East Hills, NSW

2213

Employment Status Full Time Full Time

Occupation Project Manager at ACM

Construction

Accounts Assistant at Pretty

Clothing Pty Ltd

Basis Salary (Gross) $85000.00 pa $74000.00 pa

Proposed Property:

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Type of property: Four bed room house

Purchase price: $450000.00

How much do you wish to borrow: $405000.00 +$8627.00 (LMI)

First Home buyer: No

Deposit Available: $45000.00/-

Estimated Settlement date: 6 weeks time

What is your proposed purpose for the loan proceeds? Buying an investment property

Branch access available Yes

Internet banking available Yes

Phone banking available Yes

Lenders not to be considered Big Bank

Type of loan sought P&I Investment loan

Interest rate 4.78%

Page 19 of 69

Loan Proposal for Clinton and Jennifer Andrews

Requirements and Objectives:

Clinton and Jennifer are trying to buy another investment property. The property is another four-bedroom

home in external Brisbane situated at 29 Pacific Drive, Ipswich, Queensland 4305.

Property purchase price: $450000.00

Proposed settlement: 6 weeks time from date of sale.

Looking to borrow: 90% of the purchase price with LMI.

Remaining 10% and other purchasing cost will be supported from customer's counterbalanced record.

Offset account balance: $180,000.

They are looking at a resident investment loan, P&I for 30 year term with ability to make additional

payments from timt t time without any penalty redraw facility, internet banking and fortnightly repayment

options.

Applicant Details

Applicant One Applicant Two

First Name Clinton Jennifer

Surname Andrews Andrews

Date of Birth XX/XX/XXXX XX/XX/XXXX

Number & Age of Dependants 2 (12, 10) 2 (12, 10)

Relationship to other Applicant Husband Wife

Mobile/Phone 02 6051 2121 02 6051 2121

Email clinta@acm.com.au jennya@pc.com.au

Current Address 17 Moss Ave, East Hills, NSW 2213 17 Moss Ave, East Hills, NSW

2213

Employment Status Full Time Full Time

Occupation Project Manager at ACM

Construction

Accounts Assistant at Pretty

Clothing Pty Ltd

Basis Salary (Gross) $85000.00 pa $74000.00 pa

Proposed Property:

Address: 29 Pacific Drive, Ipswich, Queensland 4305

Type of property: Four bed room house

Purchase price: $450000.00

How much do you wish to borrow: $405000.00 +$8627.00 (LMI)

First Home buyer: No

Deposit Available: $45000.00/-

Estimated Settlement date: 6 weeks time

What is your proposed purpose for the loan proceeds? Buying an investment property

Branch access available Yes

Internet banking available Yes

Phone banking available Yes

Lenders not to be considered Big Bank

Type of loan sought P&I Investment loan

Interest rate 4.78%

Page 19 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payment frequency Monthly with option for Fortnightly

Redraw Yes

Offset No

Salary crediting No

Low fees and charges Yes

Financial Position:

Assets:

Item Details Value(in $) Owner

Property 17 Moss Ave, East Hills,

NSW 2213

850000.00 Clinton & Jennifer

Motor Vehicle Ford Falcon G6, 8 years

old

15000.00 Clinton

Motor Vehicle Holden Barina, 10 years

old

5000.00 Jennifer

Cash at Bank Big Bank offset savings

account

180000.00 Clinton & Jennifer

Investment Little Bank Fixed Deposit 10000.00 Clinton & Jennifer

Superannuation MPA Insurance 82000.00 Clinton

Superannuation CLM Insurance 54000.00 Jennifer

Household effects Insured value 80000.00 Clinton & Jennifer

TOTAL ASSETS $1276000.00

Liabilities:

Item Details Monthly

Payments

Balance Owning Borrower

Home Loan Big Bank,

Variable P&I, no

fees

1020.00 190000.00 Clinton & Jennifer

Credit Card

(Limit $5,000)

Big Bank Visa

Card

150.00 800.00 Clinton

Credit Card

(Limit $3,000)

Little Bank Visa

Card

90(3% monthly

– thought she

pays $500.00

p.m.)

1200.00 Jennifer

TOTAL LIABILITIES 1260.00 192000.00

Household Expenditures:

Item Monthly Quarterly Annually

Insurance, Car, House etc 250.00 750.00 3000.00

Car- Registration, Fuel, Maintenance 400.00 1200.00 4800.00

Groceries 1500.00 4500.00 18000.00

Utilities 350.00 1050.00 4200.00

Entertainment 100.00 300.00 1200.00

Dependent Support(Childcare etc) 300.00 900.00 3600.00

Education 300.00 900.00 3600.00

TOTAL 3200.00 9600.00 38400.00

Property Purchase details:

Page 20 of 69

Redraw Yes

Offset No

Salary crediting No

Low fees and charges Yes

Financial Position:

Assets:

Item Details Value(in $) Owner

Property 17 Moss Ave, East Hills,

NSW 2213

850000.00 Clinton & Jennifer

Motor Vehicle Ford Falcon G6, 8 years

old

15000.00 Clinton

Motor Vehicle Holden Barina, 10 years

old

5000.00 Jennifer

Cash at Bank Big Bank offset savings

account

180000.00 Clinton & Jennifer

Investment Little Bank Fixed Deposit 10000.00 Clinton & Jennifer

Superannuation MPA Insurance 82000.00 Clinton

Superannuation CLM Insurance 54000.00 Jennifer

Household effects Insured value 80000.00 Clinton & Jennifer

TOTAL ASSETS $1276000.00

Liabilities:

Item Details Monthly

Payments

Balance Owning Borrower

Home Loan Big Bank,

Variable P&I, no

fees

1020.00 190000.00 Clinton & Jennifer

Credit Card

(Limit $5,000)

Big Bank Visa

Card

150.00 800.00 Clinton

Credit Card

(Limit $3,000)

Little Bank Visa

Card

90(3% monthly

– thought she

pays $500.00

p.m.)

1200.00 Jennifer

TOTAL LIABILITIES 1260.00 192000.00

Household Expenditures:

Item Monthly Quarterly Annually

Insurance, Car, House etc 250.00 750.00 3000.00

Car- Registration, Fuel, Maintenance 400.00 1200.00 4800.00

Groceries 1500.00 4500.00 18000.00

Utilities 350.00 1050.00 4200.00

Entertainment 100.00 300.00 1200.00

Dependent Support(Childcare etc) 300.00 900.00 3600.00

Education 300.00 900.00 3600.00

TOTAL 3200.00 9600.00 38400.00

Property Purchase details:

Page 20 of 69

Purchase Price 450000.00

Stamp Duty 16023.00

Solicitor/Conveyancer 1500.00

Rates & Taxes 1000.00

Pest Inspection 250.00

TOTAL COST 468205.00

Finance Required:

Loan Amount 405000.00

LMI 8627.00

TOTAL LOAN 413627.00

Total required 468205.00

Loan (before LMI) 405000.00

Shortfall/Surplus 63205.00

Estimated Repayments:

Loan Type P & I Monthly

Premium option variable home loan with offset

facility

$2120.00

Rate of Interest 4.78% pa

Term of Loan 30 years

Significant changes in the Future:

Applicant 1 (yes/no) Applicant 2 (yes/no)

Temporary change in Income No No

Permanent change in Income No No

Anticipated large Expenditure No No

Is there anything else that may reasonably be expected to have a bearing on your application for credit,

knowing that if you leave such information out it may create problems in the future?

Please specify:

NO

Are you comfortable with your ability to make repayments under the proposed loan without difficulty?

Please specify:

YES

Is there anything else that we should be aware of?

Security:

The loan will be secured by the property at 29Pcific Drive, Ipswich, Queensland 4305.

This will be subject to the valuation of the property by the bank’s authorised valuers.

Product Options:

Clinton and Jennifer are looking for Premium option home loan with the ability to make additional

payment from time to time without penalty and having redrawn facility. They also want to opt the

fortnightly repayment facility.

ASSESSMENT

This assessment is valid for 90 days from the date below. Having regard to the information above, I make

Page 21 of 69

Stamp Duty 16023.00

Solicitor/Conveyancer 1500.00

Rates & Taxes 1000.00

Pest Inspection 250.00

TOTAL COST 468205.00

Finance Required:

Loan Amount 405000.00

LMI 8627.00

TOTAL LOAN 413627.00

Total required 468205.00

Loan (before LMI) 405000.00

Shortfall/Surplus 63205.00

Estimated Repayments:

Loan Type P & I Monthly

Premium option variable home loan with offset

facility

$2120.00

Rate of Interest 4.78% pa

Term of Loan 30 years

Significant changes in the Future:

Applicant 1 (yes/no) Applicant 2 (yes/no)

Temporary change in Income No No

Permanent change in Income No No

Anticipated large Expenditure No No

Is there anything else that may reasonably be expected to have a bearing on your application for credit,

knowing that if you leave such information out it may create problems in the future?

Please specify:

NO

Are you comfortable with your ability to make repayments under the proposed loan without difficulty?

Please specify:

YES

Is there anything else that we should be aware of?

Security:

The loan will be secured by the property at 29Pcific Drive, Ipswich, Queensland 4305.

This will be subject to the valuation of the property by the bank’s authorised valuers.

Product Options:

Clinton and Jennifer are looking for Premium option home loan with the ability to make additional

payment from time to time without penalty and having redrawn facility. They also want to opt the

fortnightly repayment facility.

ASSESSMENT

This assessment is valid for 90 days from the date below. Having regard to the information above, I make

Page 21 of 69

an assessment that the following product is suitable and is appropriate finance for Clinton & Jennifer

Andrews:

Option A Option B

Lender: National Australia Bank Lender: XYZ Bank

Product: NAB Tailored Home Loan Variable Rate –

Choice Package – Residential Investment

Product: XYZ Simplicity Plus Home Loan

Interest Rate: 4.95% Interest Rate: 4.78%

Comparison Rate: 5.59% Comparison Rate: 5.16%

Recommendation:

Option B - XYZ Simplicity Plus Home Loan

Current Interest Rate: Special offer rate of 4.78%

Option B is recommended due to special offer on interest rate and features that match the

requirements. This product also offers the flexibility to make extra payments without penalty and the

redraw option. Fortnightly payment option is also available.

Extra funds can be deposited in the account and available to redraw at a later date when the need arise.

The current Interest rate applicable on the variable home loan is 4.78% which is a special offer for you.

When the interest rates change your discount level will continue to be the same off current variable

rates.

Disclosures:

Broker’s details XXX Pty Ltd XXX XXXXXX

Licensee’s name and address: Amit Patel

4/144, Oakleigh road, Carnegie, Vic 3163

Credit Licence Number 123456

External Dispute Resolution Scheme COSL (Credit Ombudsman Services Limited)

Credit representative’s name and address: Amit Patel

4/144, Oakleigh road, Carnegie, Vic 3163

Credit representatives Phone Number 0430231232

External Dispute Resolution Scheme If you have any complaints about our services, contact us.

If we are unable to resolve your problem, you may contact

our external dispute resolution scheme. External dispute

resolution is a free service established to provide you with

an independent mechanism to resolve specific complaints.

Our external dispute resolution provider is COSL (Credit

Ombudsmen Services Limited) phone 1800 138 422,

www.cosl.com.au.

Nature and range of services We will help you choose a loan which is suitable or

appropriate for your specific requirements. We will provide

you with information on a range of lenders and loans. Once

you have chosen a loan that is suitable for you, we will help

you obtain an approval.

If you have already chosen a lender and a loan, and we will

assist you in obtaining an approval (where possible)

We distribute a range of loans marketed by Vow Financial,

and only offer you a limited choice of lenders.

List of panel lenders We source loans from a panel of lenders. Our current panel

comprises the lenders listed in the Schedule. Subject to

meeting the lenders credit criteria, we are able to obtain

credit for you from these lenders. These lenders do not

necessarily represent all the lenders who offer credit of the

nature you seek.

Page 22 of 69

Andrews:

Option A Option B

Lender: National Australia Bank Lender: XYZ Bank

Product: NAB Tailored Home Loan Variable Rate –

Choice Package – Residential Investment

Product: XYZ Simplicity Plus Home Loan

Interest Rate: 4.95% Interest Rate: 4.78%

Comparison Rate: 5.59% Comparison Rate: 5.16%

Recommendation:

Option B - XYZ Simplicity Plus Home Loan

Current Interest Rate: Special offer rate of 4.78%

Option B is recommended due to special offer on interest rate and features that match the

requirements. This product also offers the flexibility to make extra payments without penalty and the

redraw option. Fortnightly payment option is also available.

Extra funds can be deposited in the account and available to redraw at a later date when the need arise.

The current Interest rate applicable on the variable home loan is 4.78% which is a special offer for you.

When the interest rates change your discount level will continue to be the same off current variable

rates.

Disclosures:

Broker’s details XXX Pty Ltd XXX XXXXXX

Licensee’s name and address: Amit Patel

4/144, Oakleigh road, Carnegie, Vic 3163

Credit Licence Number 123456

External Dispute Resolution Scheme COSL (Credit Ombudsman Services Limited)

Credit representative’s name and address: Amit Patel

4/144, Oakleigh road, Carnegie, Vic 3163

Credit representatives Phone Number 0430231232

External Dispute Resolution Scheme If you have any complaints about our services, contact us.

If we are unable to resolve your problem, you may contact

our external dispute resolution scheme. External dispute

resolution is a free service established to provide you with

an independent mechanism to resolve specific complaints.

Our external dispute resolution provider is COSL (Credit

Ombudsmen Services Limited) phone 1800 138 422,

www.cosl.com.au.

Nature and range of services We will help you choose a loan which is suitable or

appropriate for your specific requirements. We will provide

you with information on a range of lenders and loans. Once

you have chosen a loan that is suitable for you, we will help

you obtain an approval.

If you have already chosen a lender and a loan, and we will

assist you in obtaining an approval (where possible)

We distribute a range of loans marketed by Vow Financial,

and only offer you a limited choice of lenders.

List of panel lenders We source loans from a panel of lenders. Our current panel

comprises the lenders listed in the Schedule. Subject to

meeting the lenders credit criteria, we are able to obtain

credit for you from these lenders. These lenders do not

necessarily represent all the lenders who offer credit of the

nature you seek.

Page 22 of 69

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Fees payable by you We do not charge you for our services as we are paid

commission by the lender. However, you may need to pay

the lender's application fee, valuation fees, or other fees

depending on how your loan is structured.

How are we paid? Lenders/funders pay commissions for arranging loans. The

range of commissions is:

Upfront (payable one month after the settlement): Up to

1% of the loan amount

Trail (i.e. payable throughout the term of the loan): Up to

0.50% per annum (paid monthly) of the loan balance.

The exact amount paid by each lender is included in the

lender schedule provided

Commissions payable for the loan you

have selected (this information may be

completed later)

When paid:

Shortly after the loan is made *

Up to $ 150

Monthly **

Up to $ 600

* This is a percentage of the principal sum advanced on

Settlement. This is a percentage of the amount outstanding

each month

External parties sharing in remuneration We have paid or will pay a referral fee of $100 to for

referring you to us.

Please note the following:

• Before you accept your loan offer, make sure you read the credit contract/loan agreement carefully to

find full details of the loan.