Classification of Different Types of Cost

Added on 2019-12-28

24 Pages6441 Words193 Views

MANAGEMENT ACCOUNTING 1

Table of ContentsINTRODUCTION ..........................................................................................................................3TASK 1............................................................................................................................................3P1.1 Classification of different types of cost ............................................................................3P 1.2 Computation of unit cost by using unit costing method....................................................4P 1.3 Cost of exquisite using absorption cost..............................................................................5P 1.4 Cost data of exquisite using appropriate techniques..........................................................6TASK 2............................................................................................................................................7P 2.1 Preparation and analysis of cost report for the month of September and variance analysis.....................................................................................................................................................7P 2.2 Various areas of potential improvements using performance indicators ..........................8P 2.3 Ways to reduce cost and enhancing value and quality ......................................................9TASK 3............................................................................................................................................9P3.1 Purpose and nature of the budgeting process to the budget holders of Jeffery and Son’sLtd...............................................................................................................................................9P 3.2 Use of appropriate budgeting technique..........................................................................11P 3.3 Preparation of production and material budgets .............................................................11P 3.4 Preparation of cash Budget .............................................................................................12TASK 4..........................................................................................................................................14P 4.1 Calculation of variances, identify possible causes and recommend corrective actions...14P 4.2 Operating statements includes both budgeted and actual results.....................................16P4.3 Responsibility centers.......................................................................................................17CONCLUSION ............................................................................................................................17REFERENCES .............................................................................................................................18Appendix ......................................................................................................................................20Working notes for task 1.3........................................................................................................20Working notes for task 3.1........................................................................................................232

INTRODUCTION Management accounting, in general words, is referred to as the provision of financialdata which is further used to make decision, on behalf of an organization and its businessdevelopment. Accounting information is used by the managers for deciding the financial mattersof company as well as to manage and control business functions (Drury, 2008). From a long run,this tool is considered to be the important for solving the financial matters of a business entity.The present report is going to explain about the different types of cost classification as well ascalculations of unit cost. This report is focused towards the case of Jeffrey and Son’smanufacturing company. Furthermore, calculation of cost is done exquisitely while usingabsorption costing technique. The other sections show the cost report which is prepared withrespect of manufacturing unit. Along with this, a specific consideration is given to performanceindicators for recommending the ways to improve financial positions. This unit also aims to findthe areas of improvements within the accounting systems. However, the major purpose ofbudgeting as well as its process is explained in context to Jeffery and Son’s Ltd. At last, thecauses of negative variance are identified while recommending the ways to improve thebudgetary position of company.TASK 1P1.1 Classification of different types of cost There are various kinds of expenses that are incurred by manufacturing unit whenproducing goods and services. These all operating cost is generally refereed as “Cost”. It isfurther classified into range of categories that are based upon functions, behaviors, nature ofexpenses etc (Backer, 2004. ). This section is going to describe the nature of expenses as well asthe classification of various kinds of cost:Different elements of cost: There are three major elements of cost i.e. material, laborand expenses. Use of material is essential for the purpose of manufacturing finished goods. Onthe other hand, labor cost is associated with the expense made on human resource which isinvolved in production process. However, all other expenses incurred during the production ofgoods and services are known as elements of cost. All such expenses are further divided into twocategories such as direct and indirect variety i.e. direct labor and indirect material, etc 3

Nature of Expense: Material, labor and expenses are the three major categories of costwhich are involved in a production process. Manufacturing companies are witnessed withpaying remuneration to workforce. For successful completion of manufacturing process, thecompany is required to have skilled human resources or labors. Thus, salaries and wages that arepaid to such workforce are known as “Labor cost”. The specific cost which is paid against thepurchasing of raw material is considered to be “Material cost”. The other category ofexpenditure is further known as expenses for a production unit (Griffith, Stephenson andWatson, 2014). Functions/Activities: Within manufacturing organizations, one can find differentdepartments which pay consideration to certain functions. Hence, all the departments incur theirindividual cost. It is incurred by different departments as per their functions that are generallyknown as expenses to respective departments (Drury, 2008). As per the functions of variousdepartments, the cost is classified into Manufacturing cost, Selling cost, Administration andDistribution cost, Marketing cost and Research and development cost. Behavior of Cost: The behavior of cost is to be decided as per the volume ofproduction. In other words, the cost which is based on the volume/units of production isgenerally known as behavioral cost. The production volume of company depends upon themarket demand as well as other factors. There are three major types of cost that are classified asper behavior i.e. Fixed cost, Variable cost and Semi variable cost. The cost which does notchange at any level of production is called as fixed cost (Mistry, Sharma and Low,2014. ).However, the cost remains same at every level of production, else whatever the production is atany point. The fixed cost includes: rent, transportation. Variable cost, on the other hand, includesexpenses that changes as per the production level. The single alteration is production units thatlead to change in cost of production. Semi-variable cost is the combination of both kinds of costsincluding fixed as well as variable (Backer, 2004). In other words, it is the cost which remainssame at a specific level of production. However, it changes after certain limit and hence is calledas semi variable cost. P 1.2 Computation of unit cost by using unit costing methodJob costing method is the most famous method of calculating cost for a job that is ofunique nature. This method is applied to the business manufactures specific types of goods and4

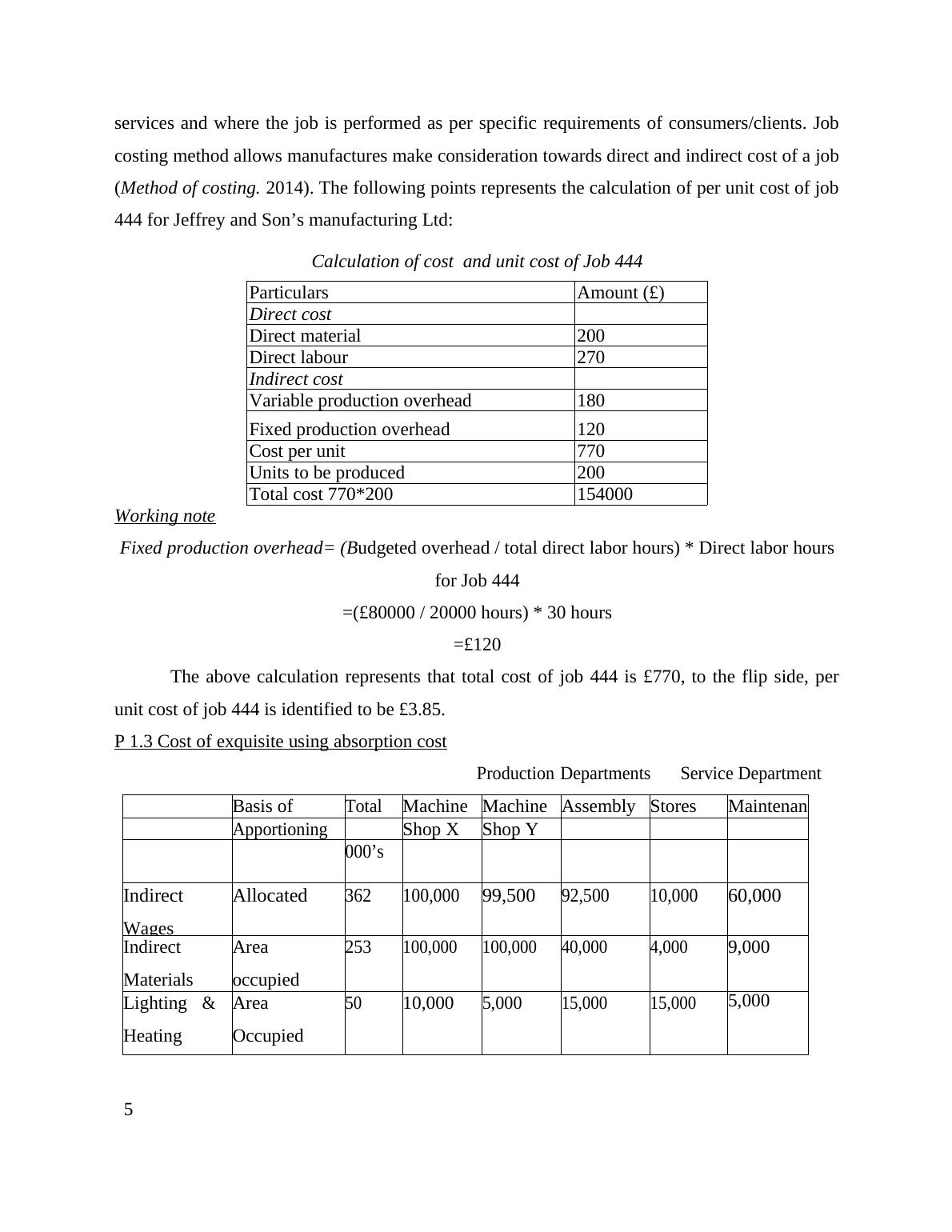

services and where the job is performed as per specific requirements of consumers/clients. Jobcosting method allows manufactures make consideration towards direct and indirect cost of a job(Method of costing. 2014). The following points represents the calculation of per unit cost of job444 for Jeffrey and Son’s manufacturing Ltd: Calculation of cost and unit cost of Job 444ParticularsAmount (£)Direct cost Direct material200Direct labour270Indirect cost Variable production overhead180Fixed production overhead120Cost per unit770Units to be produced200Total cost 770*200154000Working noteFixed production overhead= (Budgeted overhead / total direct labor hours) * Direct labor hoursfor Job 444=(£80000 / 20000 hours) * 30 hours=£120The above calculation represents that total cost of job 444 is £770, to the flip side, perunit cost of job 444 is identified to be £3.85. P 1.3 Cost of exquisite using absorption costProductionDepartmentsServiceDepartmentBasisofTotalMachineMachineAssemblyStoresMaintenanceApportioningShopXShopY000’sIndirectWagesAllocated362100,00099,50092,50010,00060,000IndirectMaterialsAreaoccupied253100,000100,00040,0004,0009,000LightingHeating&AreaOccupied5010,0005,00015,00015,0005,0005

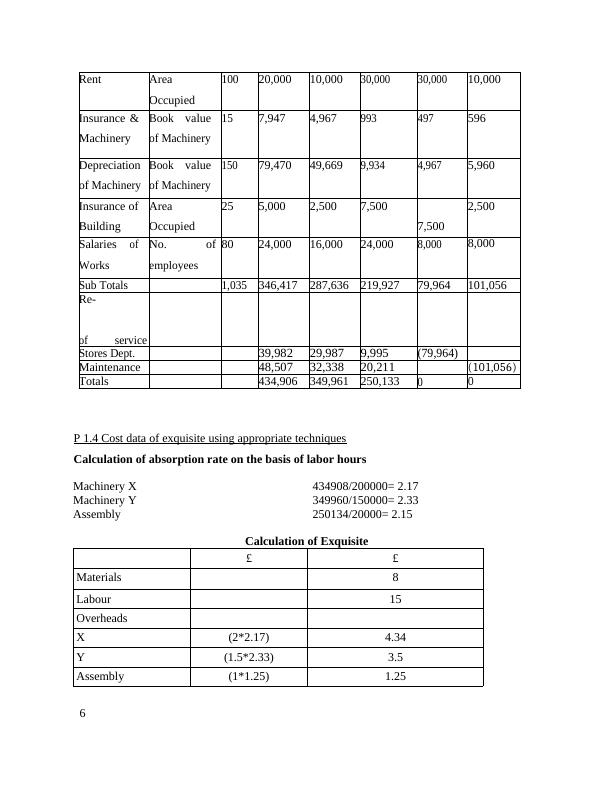

RentAreaOccupied10020,00010,00030,00030,00010,000Insurance&MachineryBookvalueofMachinery157,9474,967993497596DepreciationofMachineryBookvalueofMachinery15079,47049,6699,9344,9675,960InsuranceofBuildingAreaOccupied255,0002,5007,5007,5002,500SalariesWorksofNo.employeesof8024,00016,00024,0008,0008,000SubTotals1,035346,417287,636219,92779,964101,056Re-ofserviceStoresDept.39,98229,9879,995(79,964)Maintenance48,50732,33820,211(101,056)Totals434,906349,961250,13300P 1.4 Cost data of exquisite using appropriate techniquesCalculation of absorption rate on the basis of labor hours Machinery X434908/200000= 2.17Machinery Y349960/150000= 2.33Assembly250134/20000= 2.15Calculation of Exquisite££Materials8Labour15OverheadsX(2*2.17)4.34Y (1.5*2.33)3.5Assembly(1*1.25)1.256

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Management Accounting | Case Study On Jeffrey & Son'slg...

|24

|6619

|45

Preparation and Analysis of Cost Report for Septemberlg...

|19

|5665

|471

Management Accounting: Cost Classification, Job Costing, Absorption Costing, and Cost Analysislg...

|21

|5124

|225

TASK 11 1.1 Cost Analysis of Exquisitelg...

|25

|6901

|101

5964 management accountinglg...

|20

|5393

|438

Unit 9 Management Accounting- Jeffery and Son'slg...

|19

|5388

|35