Happy Land E-commerce Company: Clothes Production Line Appraisal

VerifiedAdded on 2023/06/11

|12

|3380

|108

Report

AI Summary

This report evaluates the feasibility of a clothes production line for Happy Land, an e-commerce company. It uses project appraisal techniques such as discounted payback period, internal rate of return (IRR), profitability index, and net present value (NPV) to assess the project's viability. The analysis incorporates risk through sensitivity analysis, examining the impact of price and quantity changes on NPV. The report also includes capital budgeting models, recommendations for the company, and an implementation plan. Ultimately, the evaluation determines whether the clothes product segment contributes positively to the overall value of the business, aiding management in making informed investment decisions. Desklib provides similar solved assignments and past papers for students.

HAPPY LAND ECOMMERCE COMPANY

CLOTHES PRODUCTION LINE EVALUATION

A Business Research Report on the project Appraisal techniques.

May, 2018

CLOTHES PRODUCTION LINE EVALUATION

A Business Research Report on the project Appraisal techniques.

May, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.2 INTRODUCTION.....................................................................................................................3

1.3 Problem Statement.....................................................................................................................4

1.4 Research methodology...............................................................................................................4

1.5 Analytical Findings....................................................................................................................5

1.5.1 Clothes production segment Appraisal techniques.............................................................5

1.5.2 Discounted pay-back period...............................................................................................5

1.5.3 Internal Rate of Return (IRR).............................................................................................6

1.5.4 Profitability index...............................................................................................................6

1.5.5 Net-present value (NPV)....................................................................................................6

1.6 Incorporating Risk in Project Evaluation..................................................................................7

1.6.1 Sensitivity analysis- Pricing...............................................................................................7

1.6.2 Sensitivity analysis- Quantity.............................................................................................8

1.7 Capital Budgeting Models.....................................................................................................8

1.8 Recommendations to the company............................................................................................9

1.9 Implementation plan..............................................................................................................9

2.0 Conclusions..............................................................................................................................10

REFERENCES..............................................................................................................................11

2

1.2 INTRODUCTION.....................................................................................................................3

1.3 Problem Statement.....................................................................................................................4

1.4 Research methodology...............................................................................................................4

1.5 Analytical Findings....................................................................................................................5

1.5.1 Clothes production segment Appraisal techniques.............................................................5

1.5.2 Discounted pay-back period...............................................................................................5

1.5.3 Internal Rate of Return (IRR).............................................................................................6

1.5.4 Profitability index...............................................................................................................6

1.5.5 Net-present value (NPV)....................................................................................................6

1.6 Incorporating Risk in Project Evaluation..................................................................................7

1.6.1 Sensitivity analysis- Pricing...............................................................................................7

1.6.2 Sensitivity analysis- Quantity.............................................................................................8

1.7 Capital Budgeting Models.....................................................................................................8

1.8 Recommendations to the company............................................................................................9

1.9 Implementation plan..............................................................................................................9

2.0 Conclusions..............................................................................................................................10

REFERENCES..............................................................................................................................11

2

1.1 Executive summary

Happy land is a market leader ecommerce company with range of product segments. The

company has thrived well in its operations for the past 5 years enjoying a market niche due to its

quality and fairly priced products. The management team of happy land has satisfied the board of

directors and all the shareholders in the operational running of the company. The main product

segments produced by this firm include; Latest gadgets, books, toys, household items and

clothes. The business operations of happy land have expanded resulting in new markets. The

market share across the different geographical regions is currently 25% and it is expected to hit a

target of 40% in the next 2 years. The different products segments commands various geographic

regions such as urban, suburban, small town, and rural due to their preference by the customers.

The management of this company has proven records of excellence in corporate governance. The

stakeholder’s welfare has always been a priority in the company. Investors are paid timely their

dividends every financial year when profits are announced. This has improved the shareholders

morale which in turn advance the valuation of shares by ploughing back their profits to the

business in form retained earnings and share repurchases. Happy lands attract a huge pool of

applicant to work in the firm. Recruited employees get to improve productivity through training

and motivational intrinsic rewards by the management.

Business targets have been accomplished every period they are set. The vision of the firm being

to become a market leader in the ecommerce sector is the driving force towards its set goals. The

management applies a balance score card as a management tool to gauge the productivity of each

employee. However, being a market leader in ecommerce, there are many challenges inhibiting

its fast growth. These factors beyond the organizational discretion such as economic problems,

sociological factors, political factors and legal factors affects the business negatively. For

example, Economic Conditions leads to fluctuations in prices, changing currency values, low

consumer spending, inflation and changing interest rates. Cultural differences as a result of

traditions, religion, and family relations can create uncertainty when doing business in different

regions (Bensley, 2011). While these situations are not directly influenced by government,

Political risk is also affected by changes in governments because of elections or military action.

Companies often grow by offering more and different products . New flavors, different package

sizes, and varied brands can create business expansion (Bensley, 2011). Happy land enjoys a

3

Happy land is a market leader ecommerce company with range of product segments. The

company has thrived well in its operations for the past 5 years enjoying a market niche due to its

quality and fairly priced products. The management team of happy land has satisfied the board of

directors and all the shareholders in the operational running of the company. The main product

segments produced by this firm include; Latest gadgets, books, toys, household items and

clothes. The business operations of happy land have expanded resulting in new markets. The

market share across the different geographical regions is currently 25% and it is expected to hit a

target of 40% in the next 2 years. The different products segments commands various geographic

regions such as urban, suburban, small town, and rural due to their preference by the customers.

The management of this company has proven records of excellence in corporate governance. The

stakeholder’s welfare has always been a priority in the company. Investors are paid timely their

dividends every financial year when profits are announced. This has improved the shareholders

morale which in turn advance the valuation of shares by ploughing back their profits to the

business in form retained earnings and share repurchases. Happy lands attract a huge pool of

applicant to work in the firm. Recruited employees get to improve productivity through training

and motivational intrinsic rewards by the management.

Business targets have been accomplished every period they are set. The vision of the firm being

to become a market leader in the ecommerce sector is the driving force towards its set goals. The

management applies a balance score card as a management tool to gauge the productivity of each

employee. However, being a market leader in ecommerce, there are many challenges inhibiting

its fast growth. These factors beyond the organizational discretion such as economic problems,

sociological factors, political factors and legal factors affects the business negatively. For

example, Economic Conditions leads to fluctuations in prices, changing currency values, low

consumer spending, inflation and changing interest rates. Cultural differences as a result of

traditions, religion, and family relations can create uncertainty when doing business in different

regions (Bensley, 2011). While these situations are not directly influenced by government,

Political risk is also affected by changes in governments because of elections or military action.

Companies often grow by offering more and different products . New flavors, different package

sizes, and varied brands can create business expansion (Bensley, 2011). Happy land enjoys a

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

product line consisting of latest gadgets, books, toys, household items and clothes. Dependency

on one or two products can be risky, though a firm has to ascertain the profitability of each cost

unit Centre. If demand for a company’s main product declines, profits may disappear. Producing

and selling a variety of items can reduce risk. (Bensley, 2011)

1.2 INTRODUCTION

Businesses faces many Uncertainties in their operating environments which present challenges to

the management. These risks may be viewed from geographic, economic, social, and political

perspectives (Mayo, 2017). Competition being a threat to existing business, firm endeavor to be

innovative, efficient, responsible and forward thinking to increase their market shares.

Management of firms Organizations therefore, are faced with continual challenge to seek out and

evaluate capital decisions that will provide current profits and long-term growth. Managers make

decisions that they hope will improve the company’s future success.

Dataset clothes production line

Calculation of free cash flow

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Estimated sales (units) 92000 142000 108000 71000 62000

Selling price 687 700.74 714.75 729.05 743.63

Sales revenue 63,204,000.00$ 99,505,080.00$ 77,193,518.40$ 51,762,542.62$ 46,105,115.42$

Less: Variable cost per unit 325 331.50 338.13 344.89 351.79

Total variable cost 29,900,000.00$ 47,073,000.00$ 36,518,040.00$ 24,487,374.60$ 21,811,008.02$

Contribution 33,304,000.00$ 52,432,080.00$ 40,675,478.40$ 27,275,168.02$ 24,294,107.40$

Less: Fixed cost 7,200,000.00$ 7,200,000.00$ 7,200,000.00$ 7,200,000.00$ 7,200,000.00$

Depreciation 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$

Total fixed cost 13,414,285.71$ 13,414,285.71$ 13,414,285.71$ 13,414,285.71$ 13,414,285.71$

Net profit before tax 19,889,714.29$ 39,017,794.29$ 27,261,192.69$ 13,860,882.30$ 10,879,821.68$

Less: Tax 5,569,120.00$ 10,924,982.40$ 7,633,133.95$ 3,881,047.04$ 3,046,350.07$

Net profit after tax 14,320,594.29$ 28,092,811.89$ 19,628,058.73$ 9,979,835.26$ 7,833,471.61$

Add: Depreciation 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$

Free cash flow 20,534,880.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 14,047,757.33$

Initial investment expenses

Development of prototype SSHA (1,175,000.00)$

Marketing study expenses (650,000.00)$

Manufacturing equipment (45,200,000.00)$

Salvage value of equipment 9,500,000.00$

Working capital (11,376,720.00)$

Net cash flows (47,025,000.00)$ 9,158,160.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 23,547,757.33$

Discounting factor at 12% 1 0.8929 0.7972 0.7118 0.6355 0.5674

Present value of cash flows (47,025,000.00)$ 8,177,321.06$ 27,349,618.21$ 18,394,580.78$ 10,291,363.88$ 13,360,997.51$

Total net present value 30,548,881.43$

4

on one or two products can be risky, though a firm has to ascertain the profitability of each cost

unit Centre. If demand for a company’s main product declines, profits may disappear. Producing

and selling a variety of items can reduce risk. (Bensley, 2011)

1.2 INTRODUCTION

Businesses faces many Uncertainties in their operating environments which present challenges to

the management. These risks may be viewed from geographic, economic, social, and political

perspectives (Mayo, 2017). Competition being a threat to existing business, firm endeavor to be

innovative, efficient, responsible and forward thinking to increase their market shares.

Management of firms Organizations therefore, are faced with continual challenge to seek out and

evaluate capital decisions that will provide current profits and long-term growth. Managers make

decisions that they hope will improve the company’s future success.

Dataset clothes production line

Calculation of free cash flow

Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Year 5

Estimated sales (units) 92000 142000 108000 71000 62000

Selling price 687 700.74 714.75 729.05 743.63

Sales revenue 63,204,000.00$ 99,505,080.00$ 77,193,518.40$ 51,762,542.62$ 46,105,115.42$

Less: Variable cost per unit 325 331.50 338.13 344.89 351.79

Total variable cost 29,900,000.00$ 47,073,000.00$ 36,518,040.00$ 24,487,374.60$ 21,811,008.02$

Contribution 33,304,000.00$ 52,432,080.00$ 40,675,478.40$ 27,275,168.02$ 24,294,107.40$

Less: Fixed cost 7,200,000.00$ 7,200,000.00$ 7,200,000.00$ 7,200,000.00$ 7,200,000.00$

Depreciation 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$

Total fixed cost 13,414,285.71$ 13,414,285.71$ 13,414,285.71$ 13,414,285.71$ 13,414,285.71$

Net profit before tax 19,889,714.29$ 39,017,794.29$ 27,261,192.69$ 13,860,882.30$ 10,879,821.68$

Less: Tax 5,569,120.00$ 10,924,982.40$ 7,633,133.95$ 3,881,047.04$ 3,046,350.07$

Net profit after tax 14,320,594.29$ 28,092,811.89$ 19,628,058.73$ 9,979,835.26$ 7,833,471.61$

Add: Depreciation 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$ 6,214,285.71$

Free cash flow 20,534,880.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 14,047,757.33$

Initial investment expenses

Development of prototype SSHA (1,175,000.00)$

Marketing study expenses (650,000.00)$

Manufacturing equipment (45,200,000.00)$

Salvage value of equipment 9,500,000.00$

Working capital (11,376,720.00)$

Net cash flows (47,025,000.00)$ 9,158,160.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 23,547,757.33$

Discounting factor at 12% 1 0.8929 0.7972 0.7118 0.6355 0.5674

Present value of cash flows (47,025,000.00)$ 8,177,321.06$ 27,349,618.21$ 18,394,580.78$ 10,291,363.88$ 13,360,997.51$

Total net present value 30,548,881.43$

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Problem Statement

The product line selected by a company should be influenced by organizational goals. The major

aim of a firm is to expand in sales, reduce costs of productions and increasing profits

maximizations. Financial theory emphasizes that the goal of a business should be to maximize

the shareholders wealth through improvement of the value of the firm. To achieve this,

increasing it requires the firm to consider analyzing its operational activities both in the short-

term and long-term to determines its profits. Every capital decision should increase the

company’s attractiveness

among current investors and potential future investors. (Bensley, 2011)

Happy land is operating in a competitive business environment. The management decided to

evaluate one of the product line’ clothes’ to determine if the project is feasible to the business

survival. Every investment in a corporate business must be worthwhile to generate repetitive

cashflows in the foreseeable future. The initial investment in the clothes production department

includes, Market study expenses, Development of prototype and manufacturing equipment.

Capital projects requires high initial capital investments that firm sometimes find it hard to

source out these finances. Therefore, Financing the capital project is a duty for the management

to consider. There are many uncertainties and risk associated acquisition of new financing

strategies for the business. These, uncertainties can range from inflation and lower consumer

spending to new government regulations and natural disasters. Therefore, this necessitates

analysis a valid analysis for the cash inflows and outflows for the clothes product line at happy

land company to assess its viability. Therefore, it is necessary to evaluate the clothes product

segment for happy land company to assess it contributions to the entire value of the business.

1.4 Research methodology

This study will adopt a descriptive survey design. A descriptive study is concerned with determining

the frequency with which something occurs or the relationship between variables. The total target

population is all the projected cashflows of clothes product line.

A census will be used to collect the data. This is appropriate because the target population is

small and every member of the population can be selected. The study will collect secondary data.

The data will be extracted from the financial statement. The data secondary data will be edited,

analyzed using Microsoft Excel for data analysis.

5

The product line selected by a company should be influenced by organizational goals. The major

aim of a firm is to expand in sales, reduce costs of productions and increasing profits

maximizations. Financial theory emphasizes that the goal of a business should be to maximize

the shareholders wealth through improvement of the value of the firm. To achieve this,

increasing it requires the firm to consider analyzing its operational activities both in the short-

term and long-term to determines its profits. Every capital decision should increase the

company’s attractiveness

among current investors and potential future investors. (Bensley, 2011)

Happy land is operating in a competitive business environment. The management decided to

evaluate one of the product line’ clothes’ to determine if the project is feasible to the business

survival. Every investment in a corporate business must be worthwhile to generate repetitive

cashflows in the foreseeable future. The initial investment in the clothes production department

includes, Market study expenses, Development of prototype and manufacturing equipment.

Capital projects requires high initial capital investments that firm sometimes find it hard to

source out these finances. Therefore, Financing the capital project is a duty for the management

to consider. There are many uncertainties and risk associated acquisition of new financing

strategies for the business. These, uncertainties can range from inflation and lower consumer

spending to new government regulations and natural disasters. Therefore, this necessitates

analysis a valid analysis for the cash inflows and outflows for the clothes product line at happy

land company to assess its viability. Therefore, it is necessary to evaluate the clothes product

segment for happy land company to assess it contributions to the entire value of the business.

1.4 Research methodology

This study will adopt a descriptive survey design. A descriptive study is concerned with determining

the frequency with which something occurs or the relationship between variables. The total target

population is all the projected cashflows of clothes product line.

A census will be used to collect the data. This is appropriate because the target population is

small and every member of the population can be selected. The study will collect secondary data.

The data will be extracted from the financial statement. The data secondary data will be edited,

analyzed using Microsoft Excel for data analysis.

5

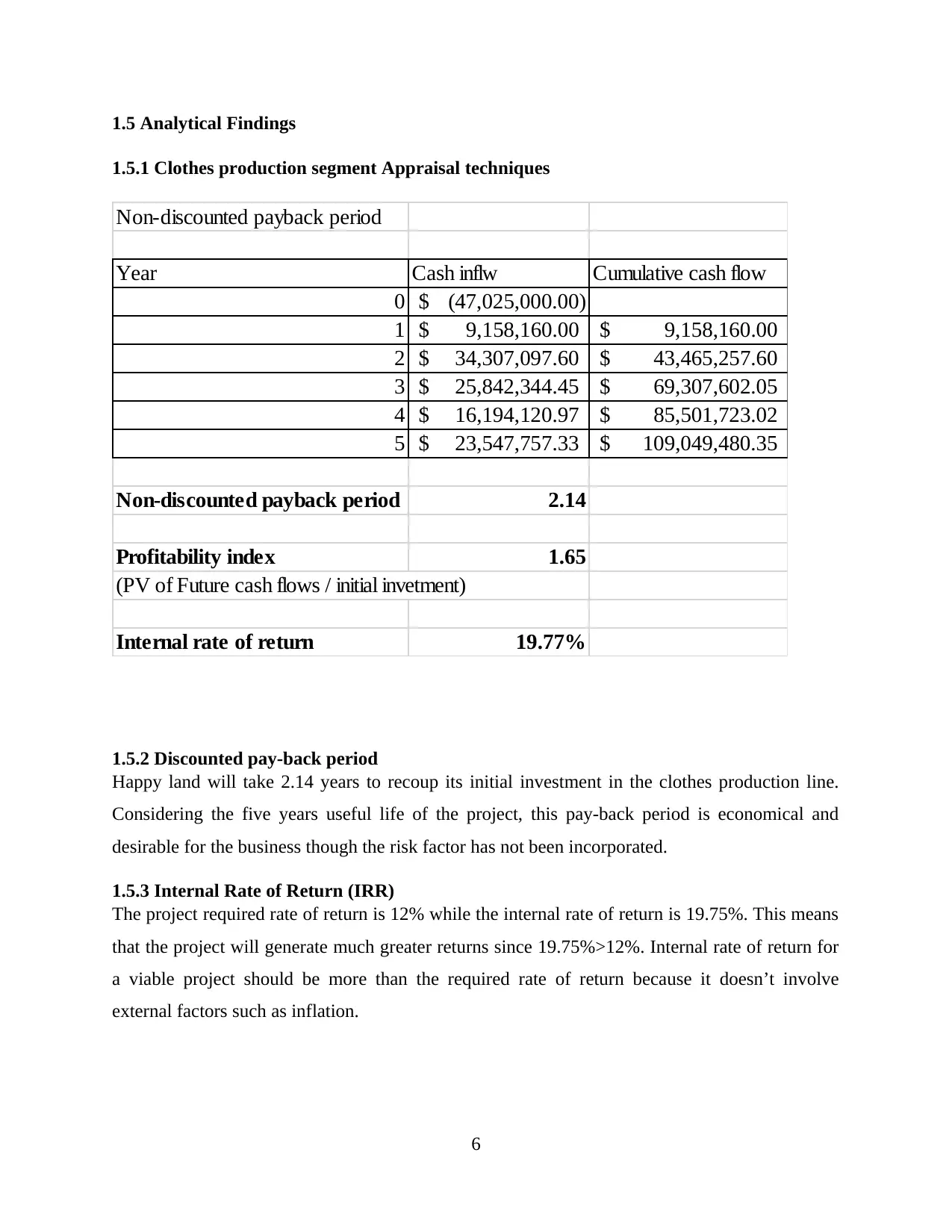

1.5 Analytical Findings

1.5.1 Clothes production segment Appraisal techniques

Non-discounted payback period

Year Cash inflw Cumulative cash flow

0 (47,025,000.00)$

1 9,158,160.00$ 9,158,160.00$

2 34,307,097.60$ 43,465,257.60$

3 25,842,344.45$ 69,307,602.05$

4 16,194,120.97$ 85,501,723.02$

5 23,547,757.33$ 109,049,480.35$

Non-discounted payback period 2.14

Profitability index 1.65

(PV of Future cash flows / initial invetment)

Internal rate of return 19.77%

1.5.2 Discounted pay-back period

Happy land will take 2.14 years to recoup its initial investment in the clothes production line.

Considering the five years useful life of the project, this pay-back period is economical and

desirable for the business though the risk factor has not been incorporated.

1.5.3 Internal Rate of Return (IRR)

The project required rate of return is 12% while the internal rate of return is 19.75%. This means

that the project will generate much greater returns since 19.75%>12%. Internal rate of return for

a viable project should be more than the required rate of return because it doesn’t involve

external factors such as inflation.

6

1.5.1 Clothes production segment Appraisal techniques

Non-discounted payback period

Year Cash inflw Cumulative cash flow

0 (47,025,000.00)$

1 9,158,160.00$ 9,158,160.00$

2 34,307,097.60$ 43,465,257.60$

3 25,842,344.45$ 69,307,602.05$

4 16,194,120.97$ 85,501,723.02$

5 23,547,757.33$ 109,049,480.35$

Non-discounted payback period 2.14

Profitability index 1.65

(PV of Future cash flows / initial invetment)

Internal rate of return 19.77%

1.5.2 Discounted pay-back period

Happy land will take 2.14 years to recoup its initial investment in the clothes production line.

Considering the five years useful life of the project, this pay-back period is economical and

desirable for the business though the risk factor has not been incorporated.

1.5.3 Internal Rate of Return (IRR)

The project required rate of return is 12% while the internal rate of return is 19.75%. This means

that the project will generate much greater returns since 19.75%>12%. Internal rate of return for

a viable project should be more than the required rate of return because it doesn’t involve

external factors such as inflation.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

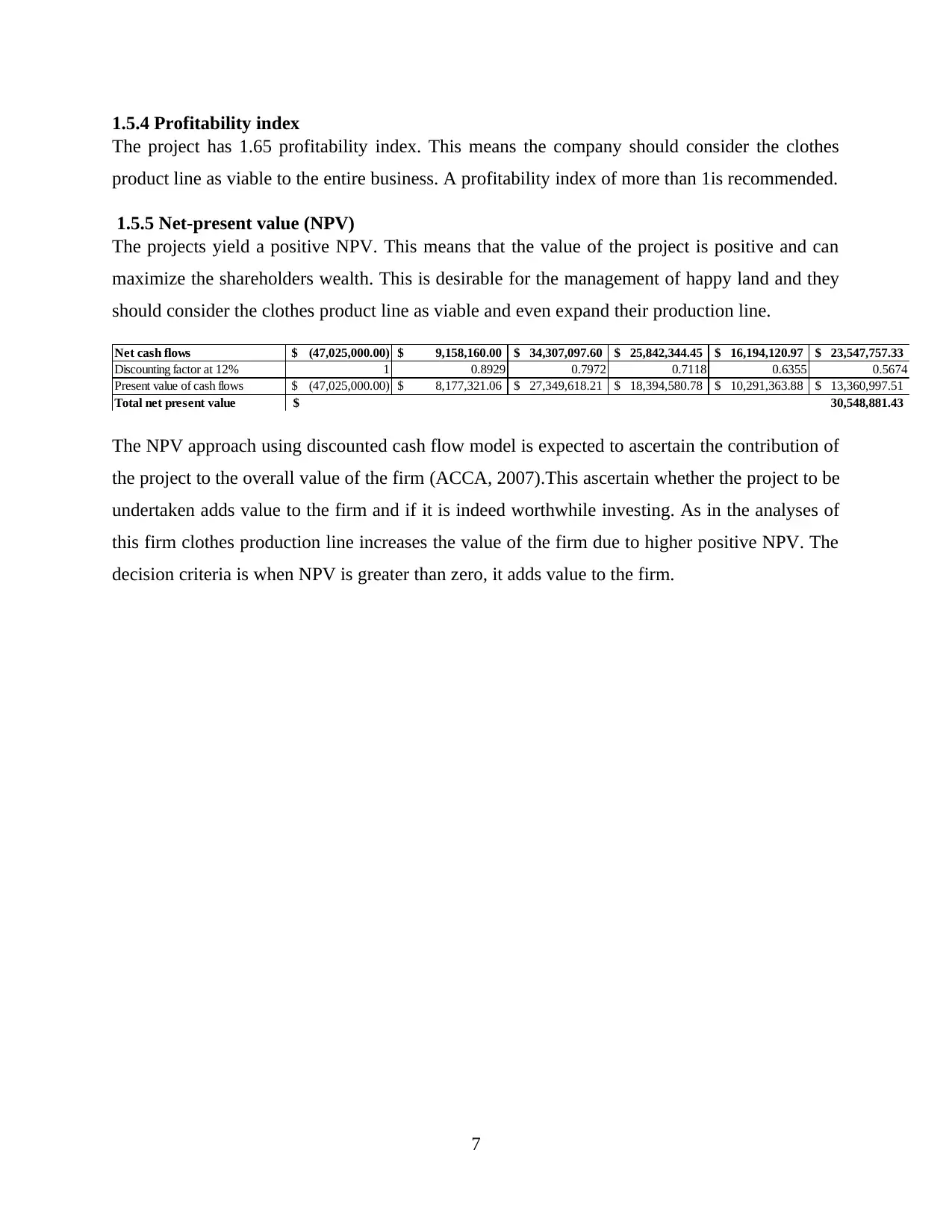

1.5.4 Profitability index

The project has 1.65 profitability index. This means the company should consider the clothes

product line as viable to the entire business. A profitability index of more than 1is recommended.

1.5.5 Net-present value (NPV)

The projects yield a positive NPV. This means that the value of the project is positive and can

maximize the shareholders wealth. This is desirable for the management of happy land and they

should consider the clothes product line as viable and even expand their production line.

Net cash flows (47,025,000.00)$ 9,158,160.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 23,547,757.33$

Discounting factor at 12% 1 0.8929 0.7972 0.7118 0.6355 0.5674

Present value of cash flows (47,025,000.00)$ 8,177,321.06$ 27,349,618.21$ 18,394,580.78$ 10,291,363.88$ 13,360,997.51$

Total net present value 30,548,881.43$

The NPV approach using discounted cash flow model is expected to ascertain the contribution of

the project to the overall value of the firm (ACCA, 2007).This ascertain whether the project to be

undertaken adds value to the firm and if it is indeed worthwhile investing. As in the analyses of

this firm clothes production line increases the value of the firm due to higher positive NPV. The

decision criteria is when NPV is greater than zero, it adds value to the firm.

7

The project has 1.65 profitability index. This means the company should consider the clothes

product line as viable to the entire business. A profitability index of more than 1is recommended.

1.5.5 Net-present value (NPV)

The projects yield a positive NPV. This means that the value of the project is positive and can

maximize the shareholders wealth. This is desirable for the management of happy land and they

should consider the clothes product line as viable and even expand their production line.

Net cash flows (47,025,000.00)$ 9,158,160.00$ 34,307,097.60$ 25,842,344.45$ 16,194,120.97$ 23,547,757.33$

Discounting factor at 12% 1 0.8929 0.7972 0.7118 0.6355 0.5674

Present value of cash flows (47,025,000.00)$ 8,177,321.06$ 27,349,618.21$ 18,394,580.78$ 10,291,363.88$ 13,360,997.51$

Total net present value 30,548,881.43$

The NPV approach using discounted cash flow model is expected to ascertain the contribution of

the project to the overall value of the firm (ACCA, 2007).This ascertain whether the project to be

undertaken adds value to the firm and if it is indeed worthwhile investing. As in the analyses of

this firm clothes production line increases the value of the firm due to higher positive NPV. The

decision criteria is when NPV is greater than zero, it adds value to the firm.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

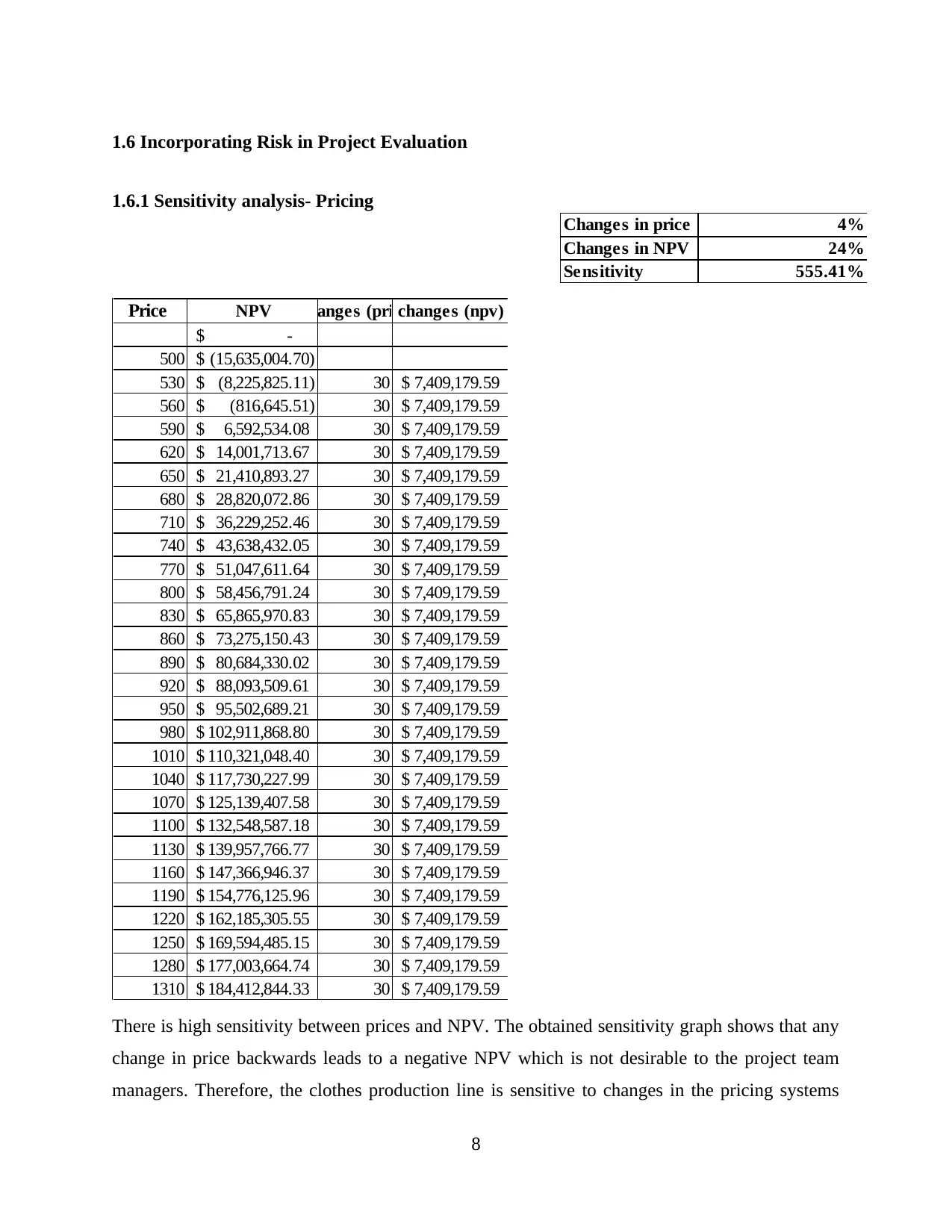

1.6 Incorporating Risk in Project Evaluation

1.6.1 Sensitivity analysis- Pricing

Changes in price 4%

Changes in NPV 24%

Sensitivity 555.41%

Price NPV Changes (price)changes (npv)

-$

500 (15,635,004.70)$

530 (8,225,825.11)$ 30 7,409,179.59$

560 (816,645.51)$ 30 7,409,179.59$

590 6,592,534.08$ 30 7,409,179.59$

620 14,001,713.67$ 30 7,409,179.59$

650 21,410,893.27$ 30 7,409,179.59$

680 28,820,072.86$ 30 7,409,179.59$

710 36,229,252.46$ 30 7,409,179.59$

740 43,638,432.05$ 30 7,409,179.59$

770 51,047,611.64$ 30 7,409,179.59$

800 58,456,791.24$ 30 7,409,179.59$

830 65,865,970.83$ 30 7,409,179.59$

860 73,275,150.43$ 30 7,409,179.59$

890 80,684,330.02$ 30 7,409,179.59$

920 88,093,509.61$ 30 7,409,179.59$

950 95,502,689.21$ 30 7,409,179.59$

980 102,911,868.80$ 30 7,409,179.59$

1010 110,321,048.40$ 30 7,409,179.59$

1040 117,730,227.99$ 30 7,409,179.59$

1070 125,139,407.58$ 30 7,409,179.59$

1100 132,548,587.18$ 30 7,409,179.59$

1130 139,957,766.77$ 30 7,409,179.59$

1160 147,366,946.37$ 30 7,409,179.59$

1190 154,776,125.96$ 30 7,409,179.59$

1220 162,185,305.55$ 30 7,409,179.59$

1250 169,594,485.15$ 30 7,409,179.59$

1280 177,003,664.74$ 30 7,409,179.59$

1310 184,412,844.33$ 30 7,409,179.59$

There is high sensitivity between prices and NPV. The obtained sensitivity graph shows that any

change in price backwards leads to a negative NPV which is not desirable to the project team

managers. Therefore, the clothes production line is sensitive to changes in the pricing systems

8

1.6.1 Sensitivity analysis- Pricing

Changes in price 4%

Changes in NPV 24%

Sensitivity 555.41%

Price NPV Changes (price)changes (npv)

-$

500 (15,635,004.70)$

530 (8,225,825.11)$ 30 7,409,179.59$

560 (816,645.51)$ 30 7,409,179.59$

590 6,592,534.08$ 30 7,409,179.59$

620 14,001,713.67$ 30 7,409,179.59$

650 21,410,893.27$ 30 7,409,179.59$

680 28,820,072.86$ 30 7,409,179.59$

710 36,229,252.46$ 30 7,409,179.59$

740 43,638,432.05$ 30 7,409,179.59$

770 51,047,611.64$ 30 7,409,179.59$

800 58,456,791.24$ 30 7,409,179.59$

830 65,865,970.83$ 30 7,409,179.59$

860 73,275,150.43$ 30 7,409,179.59$

890 80,684,330.02$ 30 7,409,179.59$

920 88,093,509.61$ 30 7,409,179.59$

950 95,502,689.21$ 30 7,409,179.59$

980 102,911,868.80$ 30 7,409,179.59$

1010 110,321,048.40$ 30 7,409,179.59$

1040 117,730,227.99$ 30 7,409,179.59$

1070 125,139,407.58$ 30 7,409,179.59$

1100 132,548,587.18$ 30 7,409,179.59$

1130 139,957,766.77$ 30 7,409,179.59$

1160 147,366,946.37$ 30 7,409,179.59$

1190 154,776,125.96$ 30 7,409,179.59$

1220 162,185,305.55$ 30 7,409,179.59$

1250 169,594,485.15$ 30 7,409,179.59$

1280 177,003,664.74$ 30 7,409,179.59$

1310 184,412,844.33$ 30 7,409,179.59$

There is high sensitivity between prices and NPV. The obtained sensitivity graph shows that any

change in price backwards leads to a negative NPV which is not desirable to the project team

managers. Therefore, the clothes production line is sensitive to changes in the pricing systems

8

may be due to competition from other firms or customers preference. (M. Kannadhasan, 2010).

Increases in prices leads to a positive NPV but we can’t ascertain if the firm is maximizing on

profits. Therefore, we recommend a set price for clothes or switch to other product with less

volatility of pricing changes to NPV.

1.6.2 Sensitivity analysis- Quantity

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

Sales volume NPV Changes (Quantity)Changes (NPV)

-$

25000 22,354,148.82$

50000 25,411,884.87$ 25000 3,057,736.05

75000 28,469,620.92$ 25000 3,057,736.05

100000 31,527,356.97$ 25000 3,057,736.05

125000 34,585,093.02$ 25000 3,057,736.05

150000 37,642,829.07$ 25000 3,057,736.05

175000 40,700,565.12$ 25000 3,057,736.05

200000 43,758,301.17$ 25000 3,057,736.05

225000 46,816,037.22$ 25000 3,057,736.05

250000 49,873,773.27$ 25000 3,057,736.05

275000 52,931,509.32$ 25000 3,057,736.05

300000 55,989,245.37$ 25000 3,057,736.05

325000 59,046,981.42$ 25000 3,057,736.05

350000 62,104,717.47$ 25000 3,057,736.05

The quantity change of clothes sold is less sensitive to NPV. Therefore, based on quantity the

firm can either increase or reduce the production at a certain limit but does not affect the overall

returns of the company. (J, 2008). The higher the quantity sold the More positive NPV meaning

that the firm can capitalize on economies of scale.

1.7 Capital Budgeting Models

Analyzing the various results from the different capital budgeting techniques, the firm should

invest in the project. With the NPV approach, a present value is given to the expected costs of

the project and the expected benefits. This ascertain whether the project to be undertaken adds

value to the firm. As in the analyses of this firm clothes production line increases the value of the

firm due to higher positive NPV. The decision criteria is when NPV is greater than zero, it adds

value to the firm. (P.K. Jain, 2013)

9

Increases in prices leads to a positive NPV but we can’t ascertain if the firm is maximizing on

profits. Therefore, we recommend a set price for clothes or switch to other product with less

volatility of pricing changes to NPV.

1.6.2 Sensitivity analysis- Quantity

Changes in quantity 27%

Changes in NPV 10%

Sensitivity 36.83%

Sales volume NPV Changes (Quantity)Changes (NPV)

-$

25000 22,354,148.82$

50000 25,411,884.87$ 25000 3,057,736.05

75000 28,469,620.92$ 25000 3,057,736.05

100000 31,527,356.97$ 25000 3,057,736.05

125000 34,585,093.02$ 25000 3,057,736.05

150000 37,642,829.07$ 25000 3,057,736.05

175000 40,700,565.12$ 25000 3,057,736.05

200000 43,758,301.17$ 25000 3,057,736.05

225000 46,816,037.22$ 25000 3,057,736.05

250000 49,873,773.27$ 25000 3,057,736.05

275000 52,931,509.32$ 25000 3,057,736.05

300000 55,989,245.37$ 25000 3,057,736.05

325000 59,046,981.42$ 25000 3,057,736.05

350000 62,104,717.47$ 25000 3,057,736.05

The quantity change of clothes sold is less sensitive to NPV. Therefore, based on quantity the

firm can either increase or reduce the production at a certain limit but does not affect the overall

returns of the company. (J, 2008). The higher the quantity sold the More positive NPV meaning

that the firm can capitalize on economies of scale.

1.7 Capital Budgeting Models

Analyzing the various results from the different capital budgeting techniques, the firm should

invest in the project. With the NPV approach, a present value is given to the expected costs of

the project and the expected benefits. This ascertain whether the project to be undertaken adds

value to the firm. As in the analyses of this firm clothes production line increases the value of the

firm due to higher positive NPV. The decision criteria is when NPV is greater than zero, it adds

value to the firm. (P.K. Jain, 2013)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Internal rate of return (IRR) approach reveals a higher rate of return as compared to the cost of

capital rate, that is, the required rate of return. (Brigham, 2012). The Clothes production line has

a higher rate of return as compared to the firms cost of capital, therefore, it should be undertaken.

It has met the risk incorporated discounting of cashflows and non-discounting techniques.

Therefore, the firm may seek to expand its operations, purchase other plants and machinery.

1.8 Recommendations to the company

The findings of the evaluations of the project is found to be feasible in all the methods of capital

budgeting. This report therefore recommends the following; 1. Improve on customer service and

delivery 2. Reduce the cost of production by applying modern technological methods 3. Pricing

of clothes be standardized 4. Carry out SWOT analysis and implement the changes 5. Seek for

mergers, partnership and alliances to improve production.

1.9 Implementation plan

Happy land management and the board of directors to form a committee to oversee the suggested

solutions to the current crisis. Furthermore, the management should assign each the operational

manager, finance managers and the human resource manager to oversee the implementations of

the recommended solutions.

The firm to Implement projects which satisfy the company’s criteria for deciding whether the

project will earn a satisfactory return on investment. Monitoring the performance of investment

projects to ensure that they perform in line with expectations. Having considered clothes

production line, there is a need to evaluate the other projects (products lines) in order to

determine the best project that meets the expected returns.

A sound financial system must be installed by the financial department that monitors the cash

flows from the cost centers and the respective revenue centers. (M. Kannadhasan, 2010). This

will enable a periodically sensitivity analysis program, that is, if the project is undertaken,

sensitive items of cash flow should be closely monitored and action taken if they vary from plan.

If a project NPV is particularly sensitive to an item of cost or revenue, management might decide

to reject the project because of the investment risk involved.

10

capital rate, that is, the required rate of return. (Brigham, 2012). The Clothes production line has

a higher rate of return as compared to the firms cost of capital, therefore, it should be undertaken.

It has met the risk incorporated discounting of cashflows and non-discounting techniques.

Therefore, the firm may seek to expand its operations, purchase other plants and machinery.

1.8 Recommendations to the company

The findings of the evaluations of the project is found to be feasible in all the methods of capital

budgeting. This report therefore recommends the following; 1. Improve on customer service and

delivery 2. Reduce the cost of production by applying modern technological methods 3. Pricing

of clothes be standardized 4. Carry out SWOT analysis and implement the changes 5. Seek for

mergers, partnership and alliances to improve production.

1.9 Implementation plan

Happy land management and the board of directors to form a committee to oversee the suggested

solutions to the current crisis. Furthermore, the management should assign each the operational

manager, finance managers and the human resource manager to oversee the implementations of

the recommended solutions.

The firm to Implement projects which satisfy the company’s criteria for deciding whether the

project will earn a satisfactory return on investment. Monitoring the performance of investment

projects to ensure that they perform in line with expectations. Having considered clothes

production line, there is a need to evaluate the other projects (products lines) in order to

determine the best project that meets the expected returns.

A sound financial system must be installed by the financial department that monitors the cash

flows from the cost centers and the respective revenue centers. (M. Kannadhasan, 2010). This

will enable a periodically sensitivity analysis program, that is, if the project is undertaken,

sensitive items of cash flow should be closely monitored and action taken if they vary from plan.

If a project NPV is particularly sensitive to an item of cost or revenue, management might decide

to reject the project because of the investment risk involved.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.0 Conclusions

The biggest challenge in today’s investment is to allocate the scarce resources (finances) to

competing projects. The management decisions therefore is vital in business investment by use

of capital budgeting techniques. Capital projects requires a high initial investment capital which

may be costly to the firm, therefore, a to ensure cash flows in the future, there is a need to ensure

an accurate capital budgeting technique. This analysis employed several capital techniques and

highlighted the following:

Sensitivity analysis is useful because it directs management attention to the critical variables in

the project. These are the variables where a variation in the cash flows by a fairly small amount

and certainly by an amount that might reasonably be expected, given uncertainty about the cash

flows would make the NPV negative and the project not financially viable.

The purpose of sensitivity analysis is to assess how the NPV of the project might be affected if

cash flow estimates are worse than expected. The management of this firm must endeavor to pay

closer attention to this prediction model of the future performance of the product line. This is

more important since the business operates in uncertain environment which affects the running

of the business. Sensitivity analysis can be used to calculate the percentage amount by which

benefits must fall below estimate or costs rise above estimate

before the project NPV becomes negative. This is a guidance to the firm since fluctuations in

sales volume, fluctuations in quantity sold affects the returns from the business.

11

The biggest challenge in today’s investment is to allocate the scarce resources (finances) to

competing projects. The management decisions therefore is vital in business investment by use

of capital budgeting techniques. Capital projects requires a high initial investment capital which

may be costly to the firm, therefore, a to ensure cash flows in the future, there is a need to ensure

an accurate capital budgeting technique. This analysis employed several capital techniques and

highlighted the following:

Sensitivity analysis is useful because it directs management attention to the critical variables in

the project. These are the variables where a variation in the cash flows by a fairly small amount

and certainly by an amount that might reasonably be expected, given uncertainty about the cash

flows would make the NPV negative and the project not financially viable.

The purpose of sensitivity analysis is to assess how the NPV of the project might be affected if

cash flow estimates are worse than expected. The management of this firm must endeavor to pay

closer attention to this prediction model of the future performance of the product line. This is

more important since the business operates in uncertain environment which affects the running

of the business. Sensitivity analysis can be used to calculate the percentage amount by which

benefits must fall below estimate or costs rise above estimate

before the project NPV becomes negative. This is a guidance to the firm since fluctuations in

sales volume, fluctuations in quantity sold affects the returns from the business.

11

REFERENCES

ACCA, 2007. Financial Management F9 Text. London: Emile Woolf International Publishing.

Bensley, b., 2011. CFIN. Australia: south-western, Cengage learning.

Brigham Eugene F, J. F., 2009. Fundamentals of financial Management. 12th ed. Canada:

Cengage Learning.

Brigham, H., 2012. Financial management. 2nd ed. Australia: Cengage learning.

Irala, L. R., 2007. Financial Management Practices in India. SSRN.

J, M., 2008. Financial Management: An introduction. s.l.:Routledge.

M. Kannadhasan, N., 2010. Capital Budgeting in Corporate sector. Journal of finance, 130(2),

pp. 12-16.

Mayo, H. B., 2017. Basic Finance: An Introduction to Financial Institutions, Investments, and

Management. 12th Edition ed. Houston: Chicago press.

P.K. Jain, S. S. S. S. Y., 2013. Financial Management Practices: An Empirical Study of Indian

Corporates. India: Springer.

Timothy R. Mayes, T. M. S., 2016. Financial Analysis with Microsoft® Excel®. 8th Edition ed.

s.l.:Cengage learning.

12

ACCA, 2007. Financial Management F9 Text. London: Emile Woolf International Publishing.

Bensley, b., 2011. CFIN. Australia: south-western, Cengage learning.

Brigham Eugene F, J. F., 2009. Fundamentals of financial Management. 12th ed. Canada:

Cengage Learning.

Brigham, H., 2012. Financial management. 2nd ed. Australia: Cengage learning.

Irala, L. R., 2007. Financial Management Practices in India. SSRN.

J, M., 2008. Financial Management: An introduction. s.l.:Routledge.

M. Kannadhasan, N., 2010. Capital Budgeting in Corporate sector. Journal of finance, 130(2),

pp. 12-16.

Mayo, H. B., 2017. Basic Finance: An Introduction to Financial Institutions, Investments, and

Management. 12th Edition ed. Houston: Chicago press.

P.K. Jain, S. S. S. S. Y., 2013. Financial Management Practices: An Empirical Study of Indian

Corporates. India: Springer.

Timothy R. Mayes, T. M. S., 2016. Financial Analysis with Microsoft® Excel®. 8th Edition ed.

s.l.:Cengage learning.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.