Business Case: Addressing Cybercrime Impact on CommBank's Performance

VerifiedAdded on 2022/10/18

|22

|4172

|180

Report

AI Summary

This business case report analyzes the impact of cybercrime on CommBank's financial performance, stemming from data breaches and outsourcing issues. The report highlights the problem, including the loss of sensitive customer data and its effect on customer confidence and profitability. It proposes benefits such as improved customer value, government support for open banking, and increased profit through enhanced security. The strategic response focuses on creating a sense of urgency and defending the core business by prioritizing data security. The recommended strategic option involves hiring professionals on a permanent basis instead of outsourcing, along with staff awareness programs. The report includes a detailed project options analysis, financial analysis, and risk comparison, concluding with an integrated analysis and options ranking. The deliverability section provides details of the recommended solution, including commercial, financial, management, and delivery aspects, supported by appendices detailing a benefit management plan, sign-off checklist, and project management strategy.

COMMBANK

i

STRATEGIC ASSESSMENT

i

STRATEGIC ASSESSMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive summary 1

Part 1 Problem...................................................................................................................2

1.1 Background....................................................................................................2

1.2 Definition of the problem...............................................................................2

1.3 Evidence of the problem...............................................................................2

1.4 Timing considerations...................................................................................4

1.5 Consideration of the broader context............................................................4

2. Part 2 Benefits...............................................................................................4

2.1 Benefits to be delivered................................................................................4

2.2 Importance of the benefits to Government...................................................4

2.3 Evidence of the benefit delivery...................................................................4

2.4 Interdependencies.........................................................................................4

3. Part 3 Strategic response...............................................................................5

3.1 Method and criteria.......................................................................................5

3.2 Strategic option analysis...............................................................................5

3.3 Recommended strategic option.....................................................................5

4 Part 4 Project options analysis......................................................................6

4.1 Project options considered............................................................................6

4.2 Stakeholder identification and consultation..................................................6

4.3 Social impacts...............................................................................................6

4.4 Environmental impacts.................................................................................7

4.5 Economic impacts.........................................................................................7

4.6 Overall evaluation of socio-economic and environmental impacts..............7

4.7 Financial analysis..........................................................................................7

4.8 Risk comparison...........................................................................................8

4.9 Integrated analysis and options ranking........................................................8

5 Part 5: Deliverability of recommended solution...........................................8

5.1 Details of recommended solution.................................................................9

5.2 Commercial and financial.............................................................................9

5.2.4 Funding sources..............................................................................12

5.3 Management................................................................................................12

5.4 Delivery......................................................................................................13

Appendix 1: Benefit management Plan 14

Appendix B: Sign-off checklist 15

References..........................................................................................................16

Appendix D: Project management strategy........................................................18

ii

Executive summary 1

Part 1 Problem...................................................................................................................2

1.1 Background....................................................................................................2

1.2 Definition of the problem...............................................................................2

1.3 Evidence of the problem...............................................................................2

1.4 Timing considerations...................................................................................4

1.5 Consideration of the broader context............................................................4

2. Part 2 Benefits...............................................................................................4

2.1 Benefits to be delivered................................................................................4

2.2 Importance of the benefits to Government...................................................4

2.3 Evidence of the benefit delivery...................................................................4

2.4 Interdependencies.........................................................................................4

3. Part 3 Strategic response...............................................................................5

3.1 Method and criteria.......................................................................................5

3.2 Strategic option analysis...............................................................................5

3.3 Recommended strategic option.....................................................................5

4 Part 4 Project options analysis......................................................................6

4.1 Project options considered............................................................................6

4.2 Stakeholder identification and consultation..................................................6

4.3 Social impacts...............................................................................................6

4.4 Environmental impacts.................................................................................7

4.5 Economic impacts.........................................................................................7

4.6 Overall evaluation of socio-economic and environmental impacts..............7

4.7 Financial analysis..........................................................................................7

4.8 Risk comparison...........................................................................................8

4.9 Integrated analysis and options ranking........................................................8

5 Part 5: Deliverability of recommended solution...........................................8

5.1 Details of recommended solution.................................................................9

5.2 Commercial and financial.............................................................................9

5.2.4 Funding sources..............................................................................12

5.3 Management................................................................................................12

5.4 Delivery......................................................................................................13

Appendix 1: Benefit management Plan 14

Appendix B: Sign-off checklist 15

References..........................................................................................................16

Appendix D: Project management strategy........................................................18

ii

Executive summary

This business case is purposed to get formal approval for investing $50 million in 2019 to

2021. Decision makers are requested to consider the low profit that CommBank has registered

since the data scandal that came from outsourcing some operations dealing with delicate

customer data. The proposal is in agreement with the government policy of addressing

cybercrime and minimising losses incurred by banks from the same. The different options that

are available for the project are hiring professionals on permanent basis and creation of staff

awareness on the dangers of cybercrime. This project can be successfully completed within

three years with minimal cost. The cost that will be incurred will be realized as increased

profit in the first one year into implementation.

1

This business case is purposed to get formal approval for investing $50 million in 2019 to

2021. Decision makers are requested to consider the low profit that CommBank has registered

since the data scandal that came from outsourcing some operations dealing with delicate

customer data. The proposal is in agreement with the government policy of addressing

cybercrime and minimising losses incurred by banks from the same. The different options that

are available for the project are hiring professionals on permanent basis and creation of staff

awareness on the dangers of cybercrime. This project can be successfully completed within

three years with minimal cost. The cost that will be incurred will be realized as increased

profit in the first one year into implementation.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1 Problem

The world has witnessed many cases of cybercrime. These crimes have the potential

to collapse the banking industry and see businesses run bankrupt. Cybercrime is an

ongoing problem that financial institutions must learn to prevent. Sensitive customer

data and finances are at risk and vulnerable if any bank does not take adequate

proactive measures. Over-reliance on third parties to provide services in CommBank

has cost the bank billions of dollars. Fuji-Xerox was contracted to destroy some

magnetic tapes that contained sensitive customer information and that was the cause

of the problem. It is very critical to be careful when contracting third parties to handle

customer related data since their interests may not rhyme with the interests of the

institution. CommBank has not stopped hiring third parties to perform some of the

tasks required to be performed in the bank. Due to the benefits of outsourcing

(Varajão, Cruz-Cunha, & Da Glória Fraga, 2017), the bank finds it cheaper to

outsource services instead of hiring the professionals who perform some of the

sensitive tasks. This poses threats t the customers and more customers will be

refraining from banking in banks they are not confident of the security of their data.

The Australian banking industry has not been spared and specifically, CommBank.

1.1 Background

There has been an escalation in the rate of data breaches and data crime (Burlakov,

2019; Malik and Islam, 2019). Financial institutions are bearing the brunt of the

attacks in terms of millions of dollars’ loss per year. The advent of technology has

birthed many of the problems the world is battling today. Although not all technology

is disruptive (Christensen, 1997), there is an urgent need to address the issue before it

ruins the future of financial institutions.

1.2 Definition of the problem

CommBank has been providing financial services for a long time. Due to the

experience that the bank has, it would be expected that the bank can easily address the

challenges that threaten it. However, this is a fast-paced industry where things change

at a high speed. Data breaches and data crime are a continual threat to CommBank.

For instance, last year (2018) saw a high quantity of data that span 15 years lost form

the bank. This backup data was on customer accounts where over 20 million accounts

were affected. The data loss was attributed to cybercrime. As a result of the data loss,

customers and potential customers were bound to have a negative perception of the

bank and this saw a decline in income in the first quarter of 2019. The bank posted a

profit of $4.7 billion, much less than what was expected (Freeman, 2019).

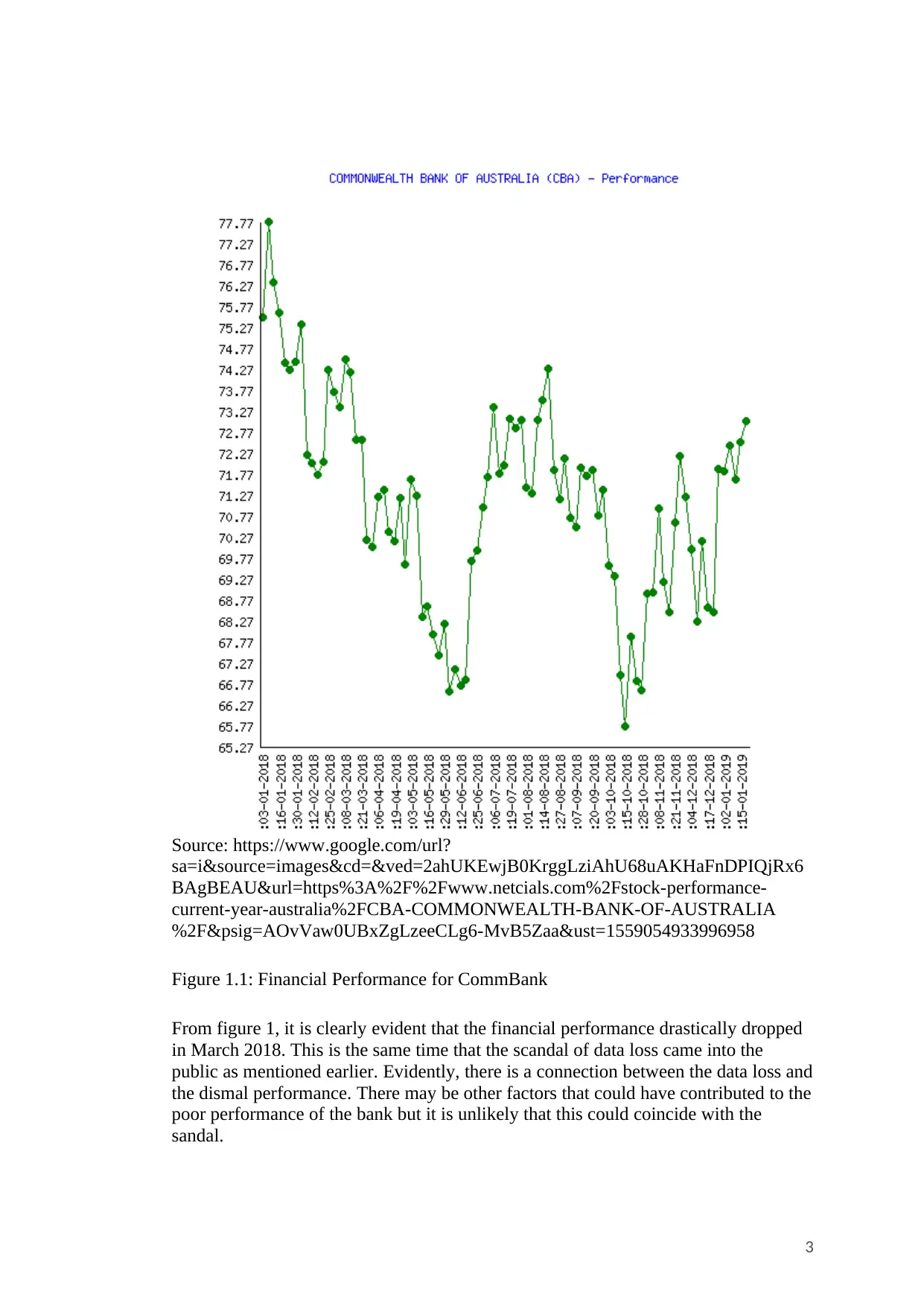

1.3 Evidence of the problem

Customers are getting more concerned with their privacy due to the level of

cybercrimes in the world. This has seen some significant decline in the overall

financial performance for the bank over the last couple of months. Figure 1 shows the

financial performance for the period spanning from January 2018 to January 2019.

2

The world has witnessed many cases of cybercrime. These crimes have the potential

to collapse the banking industry and see businesses run bankrupt. Cybercrime is an

ongoing problem that financial institutions must learn to prevent. Sensitive customer

data and finances are at risk and vulnerable if any bank does not take adequate

proactive measures. Over-reliance on third parties to provide services in CommBank

has cost the bank billions of dollars. Fuji-Xerox was contracted to destroy some

magnetic tapes that contained sensitive customer information and that was the cause

of the problem. It is very critical to be careful when contracting third parties to handle

customer related data since their interests may not rhyme with the interests of the

institution. CommBank has not stopped hiring third parties to perform some of the

tasks required to be performed in the bank. Due to the benefits of outsourcing

(Varajão, Cruz-Cunha, & Da Glória Fraga, 2017), the bank finds it cheaper to

outsource services instead of hiring the professionals who perform some of the

sensitive tasks. This poses threats t the customers and more customers will be

refraining from banking in banks they are not confident of the security of their data.

The Australian banking industry has not been spared and specifically, CommBank.

1.1 Background

There has been an escalation in the rate of data breaches and data crime (Burlakov,

2019; Malik and Islam, 2019). Financial institutions are bearing the brunt of the

attacks in terms of millions of dollars’ loss per year. The advent of technology has

birthed many of the problems the world is battling today. Although not all technology

is disruptive (Christensen, 1997), there is an urgent need to address the issue before it

ruins the future of financial institutions.

1.2 Definition of the problem

CommBank has been providing financial services for a long time. Due to the

experience that the bank has, it would be expected that the bank can easily address the

challenges that threaten it. However, this is a fast-paced industry where things change

at a high speed. Data breaches and data crime are a continual threat to CommBank.

For instance, last year (2018) saw a high quantity of data that span 15 years lost form

the bank. This backup data was on customer accounts where over 20 million accounts

were affected. The data loss was attributed to cybercrime. As a result of the data loss,

customers and potential customers were bound to have a negative perception of the

bank and this saw a decline in income in the first quarter of 2019. The bank posted a

profit of $4.7 billion, much less than what was expected (Freeman, 2019).

1.3 Evidence of the problem

Customers are getting more concerned with their privacy due to the level of

cybercrimes in the world. This has seen some significant decline in the overall

financial performance for the bank over the last couple of months. Figure 1 shows the

financial performance for the period spanning from January 2018 to January 2019.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Source: https://www.google.com/url?

sa=i&source=images&cd=&ved=2ahUKEwjB0KrggLziAhU68uAKHaFnDPIQjRx6

BAgBEAU&url=https%3A%2F%2Fwww.netcials.com%2Fstock-performance-

current-year-australia%2FCBA-COMMONWEALTH-BANK-OF-AUSTRALIA

%2F&psig=AOvVaw0UBxZgLzeeCLg6-MvB5Zaa&ust=1559054933996958

Figure 1.1: Financial Performance for CommBank

From figure 1, it is clearly evident that the financial performance drastically dropped

in March 2018. This is the same time that the scandal of data loss came into the

public as mentioned earlier. Evidently, there is a connection between the data loss and

the dismal performance. There may be other factors that could have contributed to the

poor performance of the bank but it is unlikely that this could coincide with the

sandal.

3

sa=i&source=images&cd=&ved=2ahUKEwjB0KrggLziAhU68uAKHaFnDPIQjRx6

BAgBEAU&url=https%3A%2F%2Fwww.netcials.com%2Fstock-performance-

current-year-australia%2FCBA-COMMONWEALTH-BANK-OF-AUSTRALIA

%2F&psig=AOvVaw0UBxZgLzeeCLg6-MvB5Zaa&ust=1559054933996958

Figure 1.1: Financial Performance for CommBank

From figure 1, it is clearly evident that the financial performance drastically dropped

in March 2018. This is the same time that the scandal of data loss came into the

public as mentioned earlier. Evidently, there is a connection between the data loss and

the dismal performance. There may be other factors that could have contributed to the

poor performance of the bank but it is unlikely that this could coincide with the

sandal.

3

1.4 Timing considerations

Reduced customer confidence will see CommBank continue performing dismally. If

the problem is not solved urgently, there may be more incidences of cybercrime that

are waiting. An increase in such incidences will ultimately discourage customers and

erode any confidence in the bank. This may finally lead to the collapse of the bank.

1.5 Consideration of the broader context

Cybercrime is expected to cause ripples in the banking sector. All banking institutions

are expected to suffer some form of loss in connection to cybercrime. The problems

are not limited to CommBank alone and addressing the problem in a comprehensive

manner would be beneficial to the entire industry. There is a need for all stakeholders

to marshal their strength together and address the issue before it brings the sector to

its knees.

2. Part 2 Benefits

2.1 Benefits to be delivered

This project is aimed at improving value for CommBank customers. There has been

in an increased rate of cybercrime in CommBank, making customer data to be

vulnerable to attacks by fraudsters. When customers put their money in CommBank,

they want safety and interest on their savings. When this is addressed, customers will

not need to worry about losing their money when they have already accumulated it

and saved it for future use or investment.

2.2 Importance of the benefits to Government

Once cybercrime is addressed and eliminated in CommBank, there are several

stakeholders who will benefit. First, the government will be able to realize part of its

goals of trimming cybercrime so as to encourage investment in open banking. On the

other hand, CommBank will be one of the greatest beneficiaries since they stand to

make more profit by increased savings and transactions when customers have

confidence in the bank’s cyber security. On the other hand, the customers will also

benefit and in turn help in nation-building.

2.3 Evidence of the benefit delivery

The key performance indicators showing the status of the benefits will be the financial

performance of CommBank in the next three years. There needs to be an improved

financial performance that will be measured by the bank’s balance sheet. From the

balance sheet, it will be clear the amount of profit that was made over the year. Matt

Comyn, the Chief Executive Officer will be the person who is expected to facilitate

the realization of these benefits. As expected from the closure of many offline

branches as the bank focuses on online transactions, more transactions at a lower cost

are expected (Vercoe, 2019).

2.4 Interdependencies

Although cybercrime is an issue, it is not the only concern when forecasting the future

performance of CommBank. Introductions made by the new leader, Matt, like laying

off laborers to cut expenditure is a key thing. There is also a key role played by the

4

Reduced customer confidence will see CommBank continue performing dismally. If

the problem is not solved urgently, there may be more incidences of cybercrime that

are waiting. An increase in such incidences will ultimately discourage customers and

erode any confidence in the bank. This may finally lead to the collapse of the bank.

1.5 Consideration of the broader context

Cybercrime is expected to cause ripples in the banking sector. All banking institutions

are expected to suffer some form of loss in connection to cybercrime. The problems

are not limited to CommBank alone and addressing the problem in a comprehensive

manner would be beneficial to the entire industry. There is a need for all stakeholders

to marshal their strength together and address the issue before it brings the sector to

its knees.

2. Part 2 Benefits

2.1 Benefits to be delivered

This project is aimed at improving value for CommBank customers. There has been

in an increased rate of cybercrime in CommBank, making customer data to be

vulnerable to attacks by fraudsters. When customers put their money in CommBank,

they want safety and interest on their savings. When this is addressed, customers will

not need to worry about losing their money when they have already accumulated it

and saved it for future use or investment.

2.2 Importance of the benefits to Government

Once cybercrime is addressed and eliminated in CommBank, there are several

stakeholders who will benefit. First, the government will be able to realize part of its

goals of trimming cybercrime so as to encourage investment in open banking. On the

other hand, CommBank will be one of the greatest beneficiaries since they stand to

make more profit by increased savings and transactions when customers have

confidence in the bank’s cyber security. On the other hand, the customers will also

benefit and in turn help in nation-building.

2.3 Evidence of the benefit delivery

The key performance indicators showing the status of the benefits will be the financial

performance of CommBank in the next three years. There needs to be an improved

financial performance that will be measured by the bank’s balance sheet. From the

balance sheet, it will be clear the amount of profit that was made over the year. Matt

Comyn, the Chief Executive Officer will be the person who is expected to facilitate

the realization of these benefits. As expected from the closure of many offline

branches as the bank focuses on online transactions, more transactions at a lower cost

are expected (Vercoe, 2019).

2.4 Interdependencies

Although cybercrime is an issue, it is not the only concern when forecasting the future

performance of CommBank. Introductions made by the new leader, Matt, like laying

off laborers to cut expenditure is a key thing. There is also a key role played by the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

macro-economy. People’s acceptance of open banking is another variable that

intertwines with cybercrime. There will definitely be a need for flexibility while

executing the proposal.

3. Part 3 Strategic response

To be effective in responding to disruption in a business, there is a need to be

competitive. An organization will need to consider being clear, creating a sense of

urgency, considering the disruption as an opportunity and threat, defending the core

business, and disrupting the disruptor.

3.1 Method and criteria

CommBank will need to respond by creating a sense of urgency and by defending the

core business. When a sense of urgency is created and the issued considered, it will

present a timely intervention before the reputation of the bank suffers immensely,

hindering future customers. Defending the core business will entail making sure that

the existing customers and their data are intact. Deliberate moves to ensure that the

data is not made accessible to third parties will be of utmost importance.

3.2 Strategic option analysis

3.2.1 Strategic interventions

First, it will be needful to accept that there is a threat to the bank. This is an important

thing that will create the need for intervention. If the bank does not perceive that there

is any threat to the operations and functions of the bank, then it will be impossible to

come up with an intervention. After this, the bank will need to defend the core

business. This will be impactful since the activities of the bank must be protected

from any further threat of cybercrime to restore customer confidence. The other

intervention will be addressing the issue of cyber-security immediately. This will be

impactful since the issue can be easily arrested before it gets out of hand and more

staff are involved.

3.2.2 Strategic options

Due to disruptive threats, CommBank has been ready to put its strategic options into

use. When Matt took over as the new CEO in 2018, he came with a plan to cut the

labor costs by closing up branches and laying off employees as the bank looks into

open banking. The main aim of the bank is to improve financial performance in the

next few years by cutting on cost. This would address cybercrime and defend the core

business.

3.2.2 Strategic fit

Unmatched customer data security to all.

3.3 Recommended strategic option

This report makes a recommendation that CommBank employs professionals it

requires on a permanent basis instead of outsourcing services. This is because service

providers who are outsourced may not have the heart of the permanent employees in

guarding the company. Tayauova (2012) argues that despite outsourcing being a good

and effective way to cut down on labor costs, it is quite disadvantageous in leaking

organizations’ data to outsiders. It was through outsourcing that CommBank got into

trouble with customer data management.

5

intertwines with cybercrime. There will definitely be a need for flexibility while

executing the proposal.

3. Part 3 Strategic response

To be effective in responding to disruption in a business, there is a need to be

competitive. An organization will need to consider being clear, creating a sense of

urgency, considering the disruption as an opportunity and threat, defending the core

business, and disrupting the disruptor.

3.1 Method and criteria

CommBank will need to respond by creating a sense of urgency and by defending the

core business. When a sense of urgency is created and the issued considered, it will

present a timely intervention before the reputation of the bank suffers immensely,

hindering future customers. Defending the core business will entail making sure that

the existing customers and their data are intact. Deliberate moves to ensure that the

data is not made accessible to third parties will be of utmost importance.

3.2 Strategic option analysis

3.2.1 Strategic interventions

First, it will be needful to accept that there is a threat to the bank. This is an important

thing that will create the need for intervention. If the bank does not perceive that there

is any threat to the operations and functions of the bank, then it will be impossible to

come up with an intervention. After this, the bank will need to defend the core

business. This will be impactful since the activities of the bank must be protected

from any further threat of cybercrime to restore customer confidence. The other

intervention will be addressing the issue of cyber-security immediately. This will be

impactful since the issue can be easily arrested before it gets out of hand and more

staff are involved.

3.2.2 Strategic options

Due to disruptive threats, CommBank has been ready to put its strategic options into

use. When Matt took over as the new CEO in 2018, he came with a plan to cut the

labor costs by closing up branches and laying off employees as the bank looks into

open banking. The main aim of the bank is to improve financial performance in the

next few years by cutting on cost. This would address cybercrime and defend the core

business.

3.2.2 Strategic fit

Unmatched customer data security to all.

3.3 Recommended strategic option

This report makes a recommendation that CommBank employs professionals it

requires on a permanent basis instead of outsourcing services. This is because service

providers who are outsourced may not have the heart of the permanent employees in

guarding the company. Tayauova (2012) argues that despite outsourcing being a good

and effective way to cut down on labor costs, it is quite disadvantageous in leaking

organizations’ data to outsiders. It was through outsourcing that CommBank got into

trouble with customer data management.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 Part 4 Project options analysis

When all required professionals are hired on a permanent basis, it may seem like a

move against the intention of the bank to cut on cost. However, this move perfectly

rhymes with this since it will ensure that there are no costs emanating from litigation

due to data security-related cases. These are cases that can cost the bank immensely.

Consequently, this move continues CommBank’s existing strategy and also ensures

that there is adequate data security, an issue that will see more customers gain

confidence with the bank and see the bank make more profit.

It is proposed that CommBank creates awareness on all its staff on modern threats to

delicate bank data. The employees will be able to provide needed support to the

professionals who are hired in the IT department for enhanced customer data security.

Again, the bank can offer top-notch service to its customers and ensure that their

privacy is guaranteed.

4.1 Project options considered

CommBank will need to be clear. There will be a singleness of purpose so that the

vision is achievable in an easy manner. All ambiguity will be eradicated. The entire

areas that the bank’s services are available will be addressed and covered in this. Due

to this, the market will be receptive to the banks services since they will be focussed.

It will be assumed that all the branches of the bank will cooperate with what the CEO

wants.

There will also be the creation of a sense of urgency. There will be a need to treat this

as urgent wherever CommBank is. This will be meant to ensure that the solution is

achieved within a short time. It will be assumed that all the staff will be like-minded

and will refrain from being involved in dubious transactions. This is congruent with

the government since the government wants cybercrime to be eliminated by all

means.

Again, the threat will be considered as a distraction and a threat to the bank. This will

be in the whole of Australia.

4.2 Stakeholder identification and consultation

The investors and customers of the bank will be impacted on by the options. When

the financial performance of the bank is improved, the investors will have more trust

with the management of the bank and the entire bank fraternity. In addition to that,

the customers will feel safer to transact with the bank and will be in a position to refer

their friends and family to the bank’s services. All this will see the bank on the road

to recovery from the tainted image and making more profit in the long- run.

4.3 Social impacts

When there is a singleness of purpose, the entire staff of ComBank will be bound

together in unity and there will be a better performance. On the other hand, when a

sense of urgency is created, all the stakeholders will appreciate the way the matter is

addressed and trust with the bank will be restored before long. Additionally, the threat

once treated as a distraction in the bank, the stakeholders will have a positive attitude

with the bank’s management and trust will be restored.

6

When all required professionals are hired on a permanent basis, it may seem like a

move against the intention of the bank to cut on cost. However, this move perfectly

rhymes with this since it will ensure that there are no costs emanating from litigation

due to data security-related cases. These are cases that can cost the bank immensely.

Consequently, this move continues CommBank’s existing strategy and also ensures

that there is adequate data security, an issue that will see more customers gain

confidence with the bank and see the bank make more profit.

It is proposed that CommBank creates awareness on all its staff on modern threats to

delicate bank data. The employees will be able to provide needed support to the

professionals who are hired in the IT department for enhanced customer data security.

Again, the bank can offer top-notch service to its customers and ensure that their

privacy is guaranteed.

4.1 Project options considered

CommBank will need to be clear. There will be a singleness of purpose so that the

vision is achievable in an easy manner. All ambiguity will be eradicated. The entire

areas that the bank’s services are available will be addressed and covered in this. Due

to this, the market will be receptive to the banks services since they will be focussed.

It will be assumed that all the branches of the bank will cooperate with what the CEO

wants.

There will also be the creation of a sense of urgency. There will be a need to treat this

as urgent wherever CommBank is. This will be meant to ensure that the solution is

achieved within a short time. It will be assumed that all the staff will be like-minded

and will refrain from being involved in dubious transactions. This is congruent with

the government since the government wants cybercrime to be eliminated by all

means.

Again, the threat will be considered as a distraction and a threat to the bank. This will

be in the whole of Australia.

4.2 Stakeholder identification and consultation

The investors and customers of the bank will be impacted on by the options. When

the financial performance of the bank is improved, the investors will have more trust

with the management of the bank and the entire bank fraternity. In addition to that,

the customers will feel safer to transact with the bank and will be in a position to refer

their friends and family to the bank’s services. All this will see the bank on the road

to recovery from the tainted image and making more profit in the long- run.

4.3 Social impacts

When there is a singleness of purpose, the entire staff of ComBank will be bound

together in unity and there will be a better performance. On the other hand, when a

sense of urgency is created, all the stakeholders will appreciate the way the matter is

addressed and trust with the bank will be restored before long. Additionally, the threat

once treated as a distraction in the bank, the stakeholders will have a positive attitude

with the bank’s management and trust will be restored.

6

4.4 Environmental impacts

A better financial performance by the bank will have an impact on the environment.

As the bank moves from outsourcing to handling all the operations, it will be

important for the bank to consider waste disposal. Waste paper and other things like

used print cartridges will need to be properly disposed of in a safe manner. There will

be adherence to the guidelines set by the local government on waste disposal.

Additionally, safety standards will be maintained in the banks.

4.5 Economic impacts

Data security is key in the banking industry and banks have a responsibility to protect

the information of their clients (Pacelli, 2016). When the customer data in

CommBank is secured, the bank will report improved financial performance. This

will mean that the dividends shared by the shareholders will be more. Consequently,

the living standards of the shareholders will be improved and this will have a

spiraling impact on the local economy. This is because the buying and spending

patterns of the shareholders will be altered. An improvement in the local economy

will have an impact on the overall GDP of the country. Improved performance will

mean a higher chance for the workforce to be paid well. These are people who also

engage other services like cleaning services in their homes and the overall economy

in the locality will be improved.

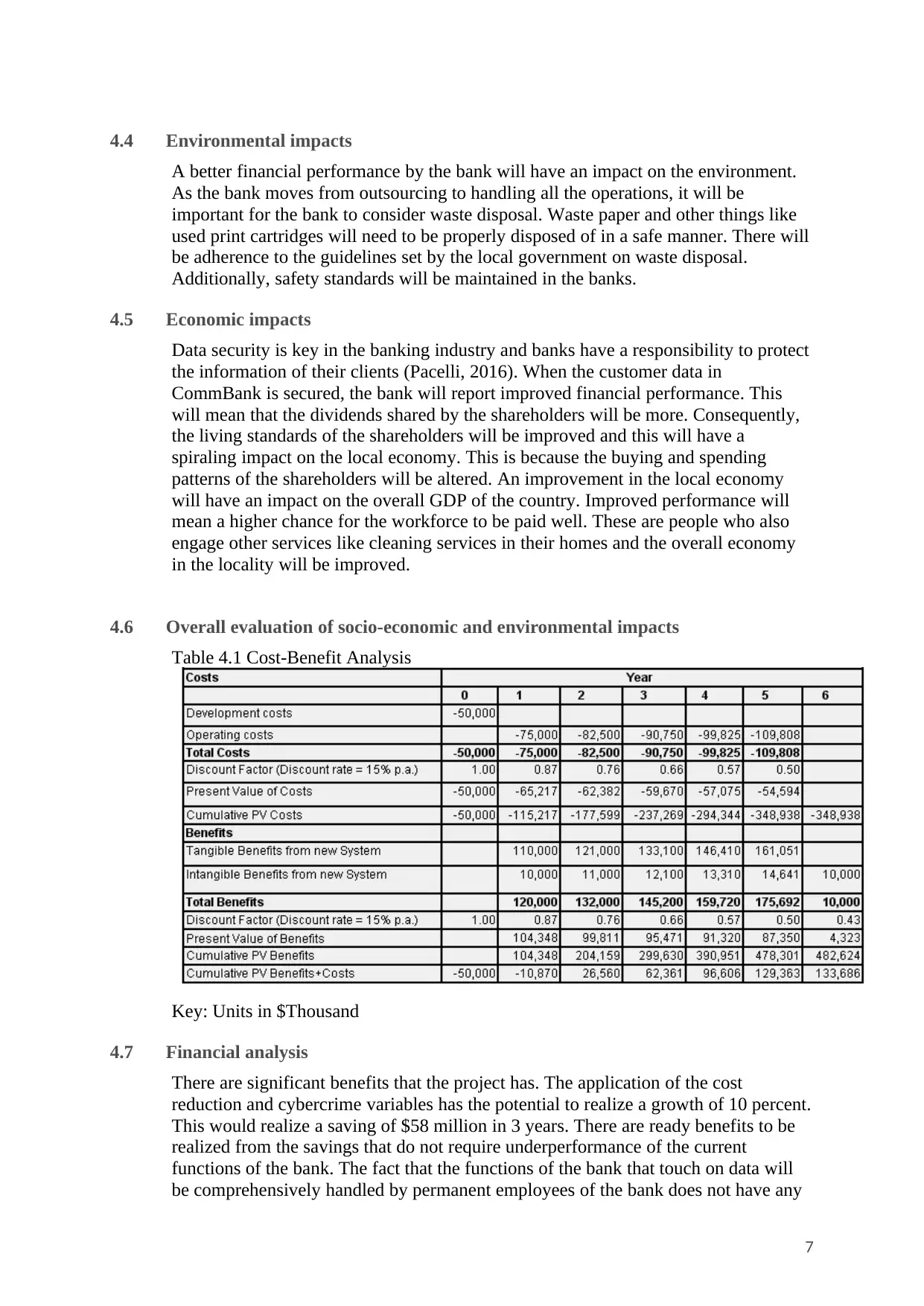

4.6 Overall evaluation of socio-economic and environmental impacts

Table 4.1 Cost-Benefit Analysis

Key: Units in $Thousand

4.7 Financial analysis

There are significant benefits that the project has. The application of the cost

reduction and cybercrime variables has the potential to realize a growth of 10 percent.

This would realize a saving of $58 million in 3 years. There are ready benefits to be

realized from the savings that do not require underperformance of the current

functions of the bank. The fact that the functions of the bank that touch on data will

be comprehensively handled by permanent employees of the bank does not have any

7

A better financial performance by the bank will have an impact on the environment.

As the bank moves from outsourcing to handling all the operations, it will be

important for the bank to consider waste disposal. Waste paper and other things like

used print cartridges will need to be properly disposed of in a safe manner. There will

be adherence to the guidelines set by the local government on waste disposal.

Additionally, safety standards will be maintained in the banks.

4.5 Economic impacts

Data security is key in the banking industry and banks have a responsibility to protect

the information of their clients (Pacelli, 2016). When the customer data in

CommBank is secured, the bank will report improved financial performance. This

will mean that the dividends shared by the shareholders will be more. Consequently,

the living standards of the shareholders will be improved and this will have a

spiraling impact on the local economy. This is because the buying and spending

patterns of the shareholders will be altered. An improvement in the local economy

will have an impact on the overall GDP of the country. Improved performance will

mean a higher chance for the workforce to be paid well. These are people who also

engage other services like cleaning services in their homes and the overall economy

in the locality will be improved.

4.6 Overall evaluation of socio-economic and environmental impacts

Table 4.1 Cost-Benefit Analysis

Key: Units in $Thousand

4.7 Financial analysis

There are significant benefits that the project has. The application of the cost

reduction and cybercrime variables has the potential to realize a growth of 10 percent.

This would realize a saving of $58 million in 3 years. There are ready benefits to be

realized from the savings that do not require underperformance of the current

functions of the bank. The fact that the functions of the bank that touch on data will

be comprehensively handled by permanent employees of the bank does not have any

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

additional cost implication since the overall expenditure is lower than when

outsourcing the services and getting involved in litigation emanating from misuse of

private customer information.

4.8 Risk comparison

In sound risk management, balance is quite essential. The interests of the CommBank

customers should be weighed against the better financial performance of CommBank.

Increased cybercrime will negatively impact on the financial performance of

CommBank. It is essential to address cybercrime in CommBank. Leakage of

customer data will negatively impact on the financial performance of the bank.

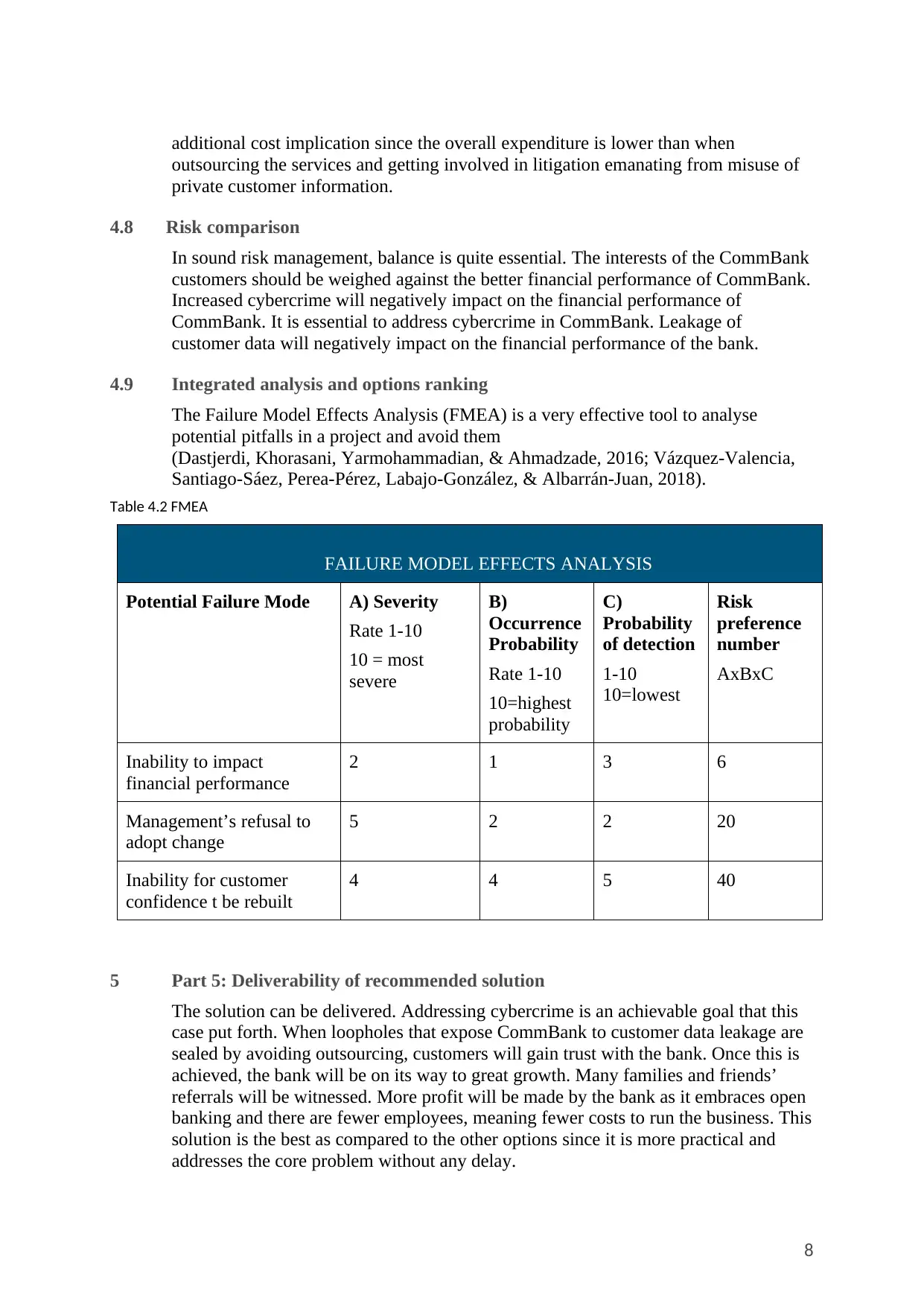

4.9 Integrated analysis and options ranking

The Failure Model Effects Analysis (FMEA) is a very effective tool to analyse

potential pitfalls in a project and avoid them

(Dastjerdi, Khorasani, Yarmohammadian, & Ahmadzade, 2016; Vázquez-Valencia,

Santiago-Sáez, Perea-Pérez, Labajo-González, & Albarrán-Juan, 2018).

Table 4.2 FMEA

FAILURE MODEL EFFECTS ANALYSIS

Potential Failure Mode A) Severity

Rate 1-10

10 = most

severe

B)

Occurrence

Probability

Rate 1-10

10=highest

probability

C)

Probability

of detection

1-10

10=lowest

Risk

preference

number

AxBxC

Inability to impact

financial performance

2 1 3 6

Management’s refusal to

adopt change

5 2 2 20

Inability for customer

confidence t be rebuilt

4 4 5 40

5 Part 5: Deliverability of recommended solution

The solution can be delivered. Addressing cybercrime is an achievable goal that this

case put forth. When loopholes that expose CommBank to customer data leakage are

sealed by avoiding outsourcing, customers will gain trust with the bank. Once this is

achieved, the bank will be on its way to great growth. Many families and friends’

referrals will be witnessed. More profit will be made by the bank as it embraces open

banking and there are fewer employees, meaning fewer costs to run the business. This

solution is the best as compared to the other options since it is more practical and

addresses the core problem without any delay.

8

outsourcing the services and getting involved in litigation emanating from misuse of

private customer information.

4.8 Risk comparison

In sound risk management, balance is quite essential. The interests of the CommBank

customers should be weighed against the better financial performance of CommBank.

Increased cybercrime will negatively impact on the financial performance of

CommBank. It is essential to address cybercrime in CommBank. Leakage of

customer data will negatively impact on the financial performance of the bank.

4.9 Integrated analysis and options ranking

The Failure Model Effects Analysis (FMEA) is a very effective tool to analyse

potential pitfalls in a project and avoid them

(Dastjerdi, Khorasani, Yarmohammadian, & Ahmadzade, 2016; Vázquez-Valencia,

Santiago-Sáez, Perea-Pérez, Labajo-González, & Albarrán-Juan, 2018).

Table 4.2 FMEA

FAILURE MODEL EFFECTS ANALYSIS

Potential Failure Mode A) Severity

Rate 1-10

10 = most

severe

B)

Occurrence

Probability

Rate 1-10

10=highest

probability

C)

Probability

of detection

1-10

10=lowest

Risk

preference

number

AxBxC

Inability to impact

financial performance

2 1 3 6

Management’s refusal to

adopt change

5 2 2 20

Inability for customer

confidence t be rebuilt

4 4 5 40

5 Part 5: Deliverability of recommended solution

The solution can be delivered. Addressing cybercrime is an achievable goal that this

case put forth. When loopholes that expose CommBank to customer data leakage are

sealed by avoiding outsourcing, customers will gain trust with the bank. Once this is

achieved, the bank will be on its way to great growth. Many families and friends’

referrals will be witnessed. More profit will be made by the bank as it embraces open

banking and there are fewer employees, meaning fewer costs to run the business. This

solution is the best as compared to the other options since it is more practical and

addresses the core problem without any delay.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5.1 Details of recommended solution

CommBank will be ready to put its recommended options into use. Although Matt

introduced layoffs as a way of addressing the financial shortfall, the recommended

solution will be to deal with cybercrime as it is the root cause of reduced customer

confidence hence reduced profits. When customers will be presented with a data

secure CommBank, they will have their confidence restored and this will realize

better profit margins. Awareness creation through advertising will be considered

keenly since the customers and staff alike need to know the risks associated with data

security in the banking industry. All stakeholders will be considered and involved in

this endeavour.

5.2 Commercial and financial

5.2.1 Procurement

This part is not applicable since there will be nothing to be bought/procured.

5.2.2 Risk assessment and management

Table 5.1: Key success risks

Risk Management strategy

Loss of

customer

confidence

Lack of finances

Restoring customer confidence

Ensure better financial performance

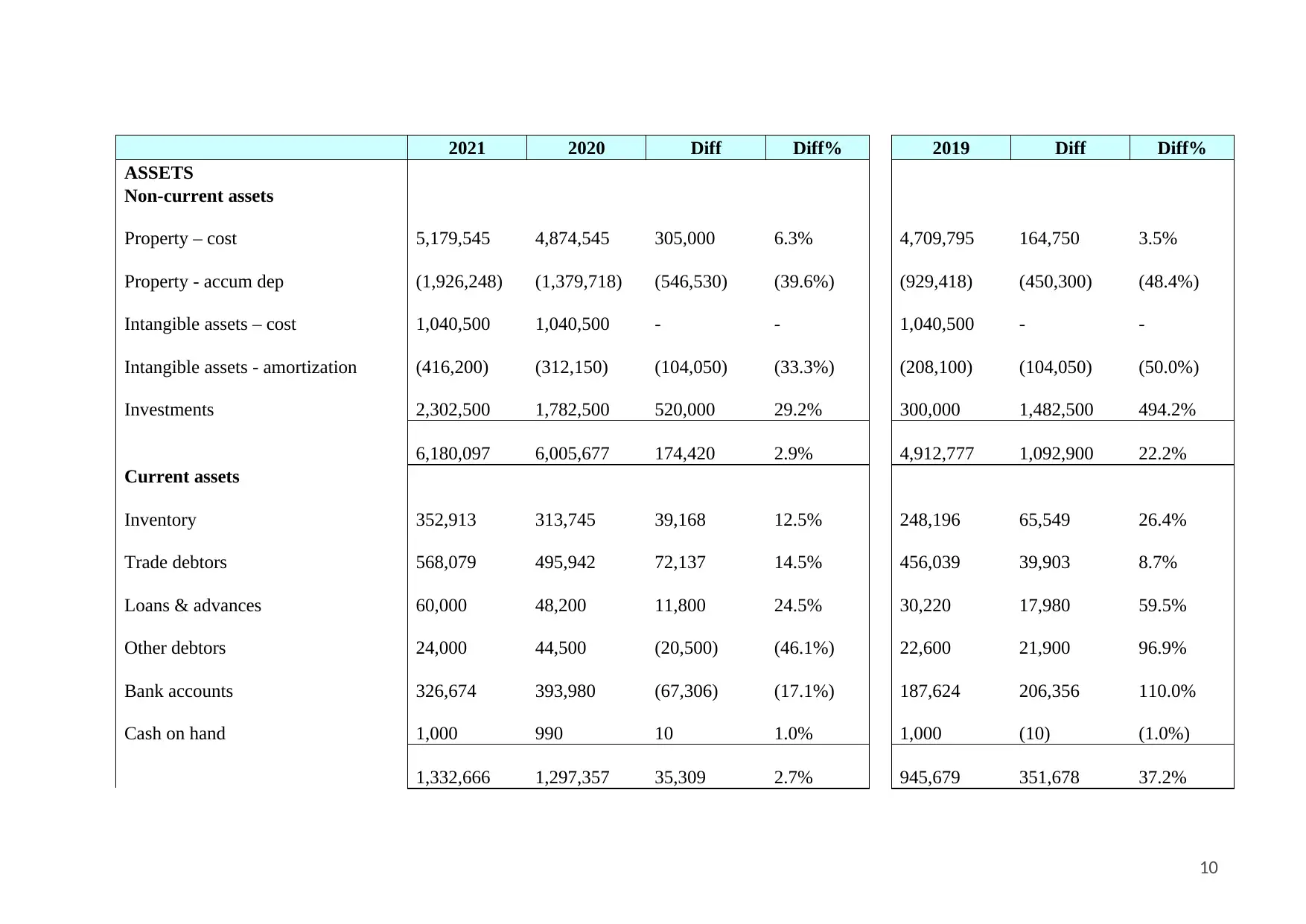

5.2.3 Detailed costing and economic evaluation

Following is the cashflow for three years from 2019 to 2021.

9

CommBank will be ready to put its recommended options into use. Although Matt

introduced layoffs as a way of addressing the financial shortfall, the recommended

solution will be to deal with cybercrime as it is the root cause of reduced customer

confidence hence reduced profits. When customers will be presented with a data

secure CommBank, they will have their confidence restored and this will realize

better profit margins. Awareness creation through advertising will be considered

keenly since the customers and staff alike need to know the risks associated with data

security in the banking industry. All stakeholders will be considered and involved in

this endeavour.

5.2 Commercial and financial

5.2.1 Procurement

This part is not applicable since there will be nothing to be bought/procured.

5.2.2 Risk assessment and management

Table 5.1: Key success risks

Risk Management strategy

Loss of

customer

confidence

Lack of finances

Restoring customer confidence

Ensure better financial performance

5.2.3 Detailed costing and economic evaluation

Following is the cashflow for three years from 2019 to 2021.

9

table©

2021 2020 Diff Diff% 2019 Diff Diff%

ASSETS

Non-current assets

Property – cost 5,179,545 4,874,545 305,000 6.3% 4,709,795 164,750 3.5%

Property - accum dep (1,926,248) (1,379,718) (546,530) (39.6%) (929,418) (450,300) (48.4%)

Intangible assets – cost 1,040,500 1,040,500 - - 1,040,500 - -

Intangible assets - amortization (416,200) (312,150) (104,050) (33.3%) (208,100) (104,050) (50.0%)

Investments 2,302,500 1,782,500 520,000 29.2% 300,000 1,482,500 494.2%

6,180,097 6,005,677 174,420 2.9% 4,912,777 1,092,900 22.2%

Current assets

Inventory 352,913 313,745 39,168 12.5% 248,196 65,549 26.4%

Trade debtors 568,079 495,942 72,137 14.5% 456,039 39,903 8.7%

Loans & advances 60,000 48,200 11,800 24.5% 30,220 17,980 59.5%

Other debtors 24,000 44,500 (20,500) (46.1%) 22,600 21,900 96.9%

Bank accounts 326,674 393,980 (67,306) (17.1%) 187,624 206,356 110.0%

Cash on hand 1,000 990 10 1.0% 1,000 (10) (1.0%)

1,332,666 1,297,357 35,309 2.7% 945,679 351,678 37.2%

10

2021 2020 Diff Diff% 2019 Diff Diff%

ASSETS

Non-current assets

Property – cost 5,179,545 4,874,545 305,000 6.3% 4,709,795 164,750 3.5%

Property - accum dep (1,926,248) (1,379,718) (546,530) (39.6%) (929,418) (450,300) (48.4%)

Intangible assets – cost 1,040,500 1,040,500 - - 1,040,500 - -

Intangible assets - amortization (416,200) (312,150) (104,050) (33.3%) (208,100) (104,050) (50.0%)

Investments 2,302,500 1,782,500 520,000 29.2% 300,000 1,482,500 494.2%

6,180,097 6,005,677 174,420 2.9% 4,912,777 1,092,900 22.2%

Current assets

Inventory 352,913 313,745 39,168 12.5% 248,196 65,549 26.4%

Trade debtors 568,079 495,942 72,137 14.5% 456,039 39,903 8.7%

Loans & advances 60,000 48,200 11,800 24.5% 30,220 17,980 59.5%

Other debtors 24,000 44,500 (20,500) (46.1%) 22,600 21,900 96.9%

Bank accounts 326,674 393,980 (67,306) (17.1%) 187,624 206,356 110.0%

Cash on hand 1,000 990 10 1.0% 1,000 (10) (1.0%)

1,332,666 1,297,357 35,309 2.7% 945,679 351,678 37.2%

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.