Company Accounting

Formatting requirements for COMPANY ACCOUNTING assignment

7 Pages1454 Words22 Views

Added on 2023-01-12

About This Document

This document provides information about company accounting, including the revaluation model and fair value measurement hierarchy. It also discusses financial reporting based on historical costs and provides examples from Medibank Private Insurance's financial reports.

Company Accounting

Formatting requirements for COMPANY ACCOUNTING assignment

Added on 2023-01-12

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Revaluations and Impairment Testing of Non-Current Assets

|11

|2737

|184

Revaluations and Impairment Testing of Non-Current Assets

|9

|2971

|64

Impairment Testing in Accounting

|11

|2457

|399

Revaluations and Impairment Testing of Non-Current Assets

|10

|2812

|67

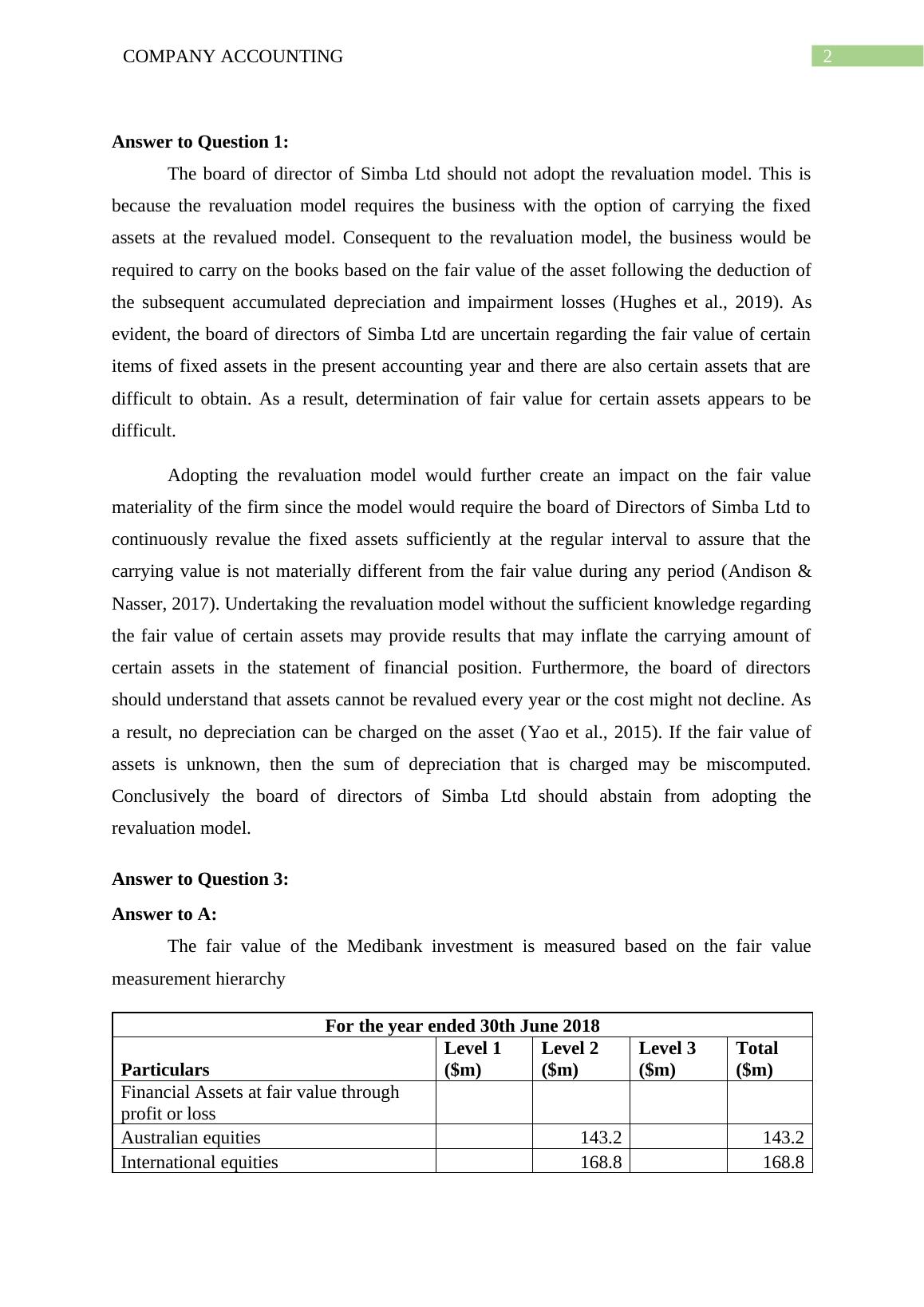

Adoption of Fair Value Method in Accounting

|10

|2533

|172

Revaluation and Impairment Testing of Non Current Assets

|10

|2379

|467