ACCT20073 Company Accounting: Analysis of Accounting Issues

VerifiedAdded on 2023/06/10

|7

|975

|244

Report

AI Summary

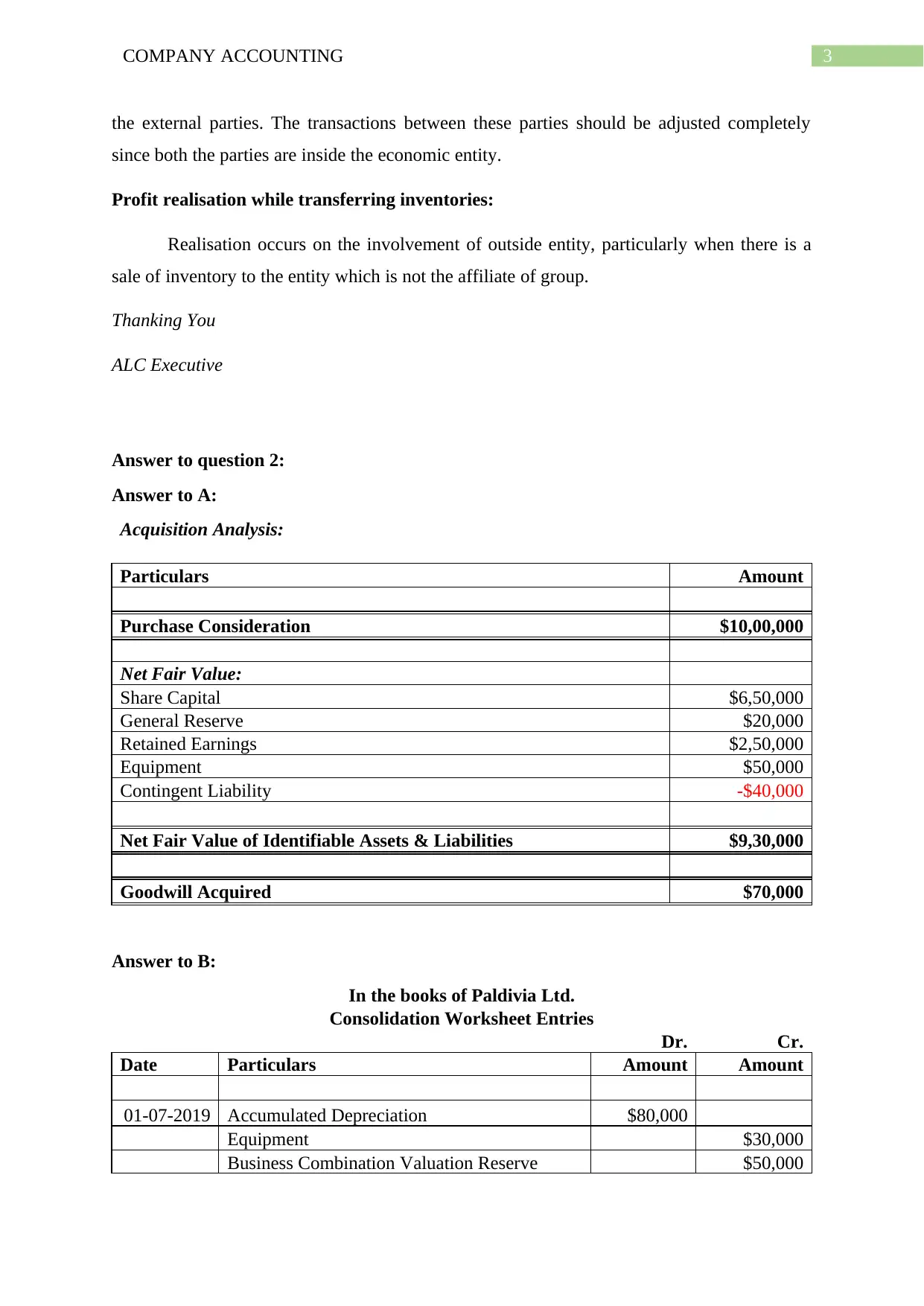

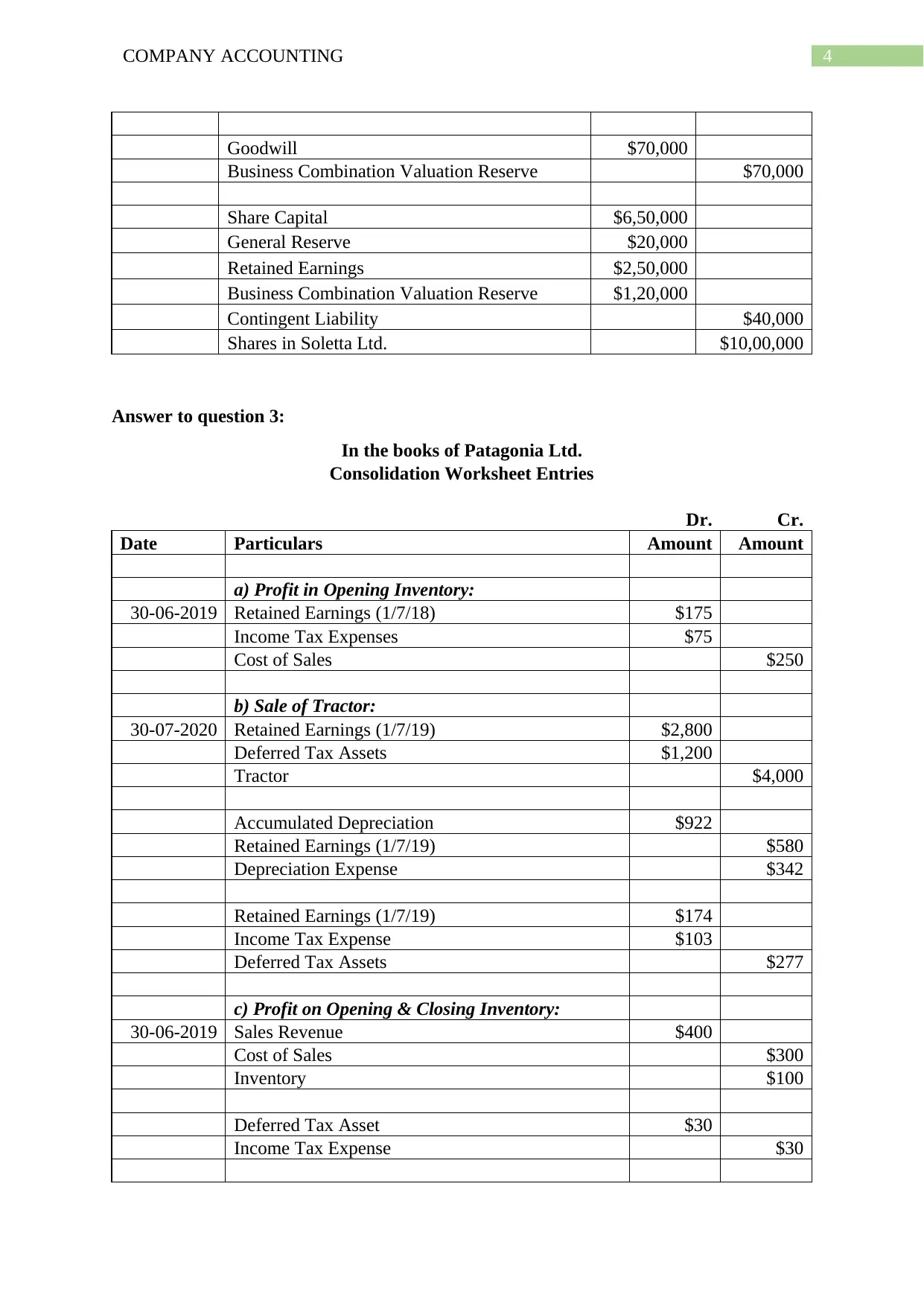

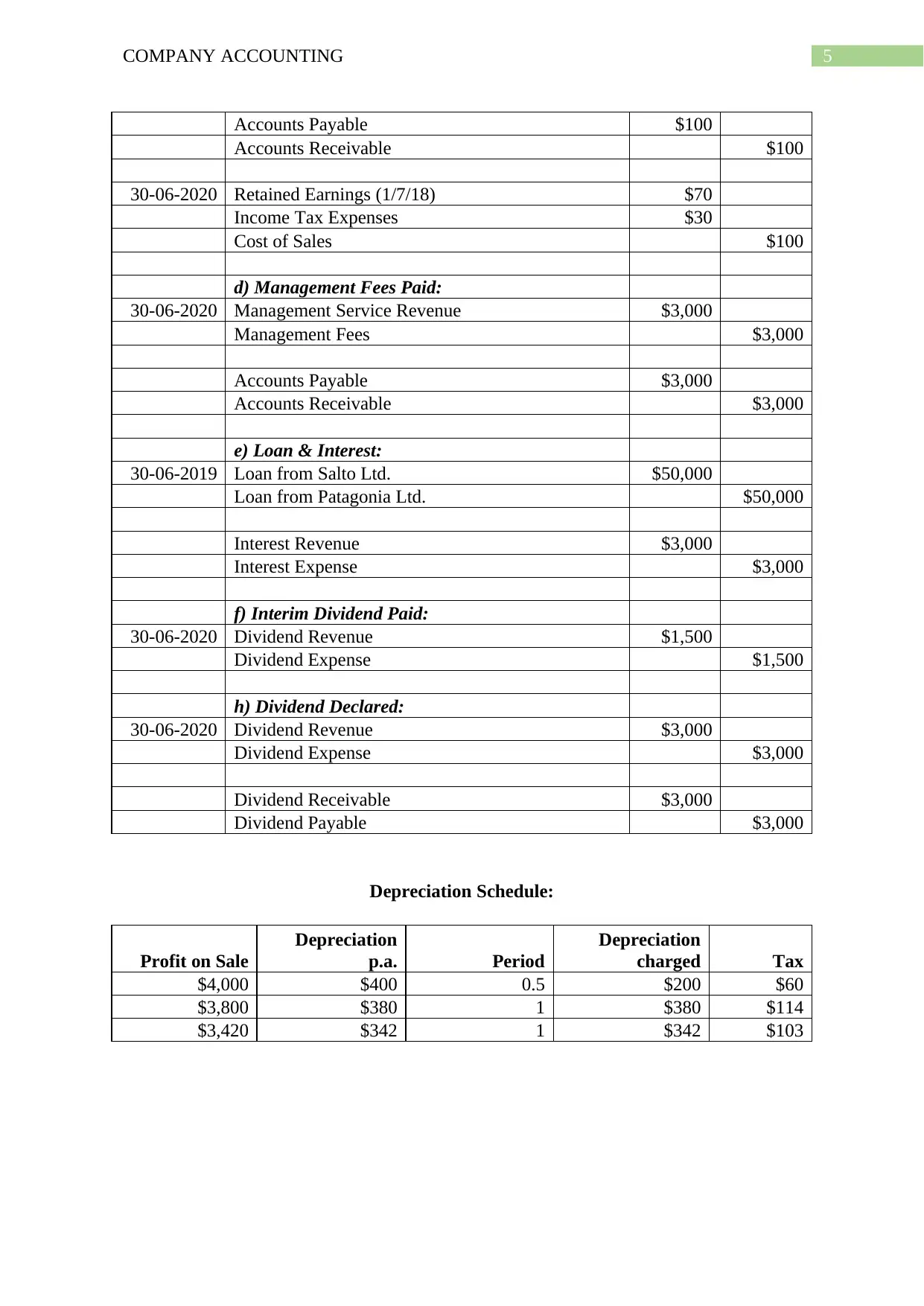

This document is a company accounting report that includes a memorandum discussing the purpose of preparing consolidated financial statements, definitions of group, parent, and subsidiary companies, and necessary adjustments to intragroup transactions. It also provides solutions to accounting problems, including acquisition analysis and consolidation worksheet entries for Paldivia Ltd. and Patagonia Ltd., addressing issues like profit in opening inventory, sale of tractor, management fees, loans, interest, and dividend payments. The report concludes with a depreciation schedule and references.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.