Telstra's Financial Performance Analysis

VerifiedAdded on 2020/03/23

|19

|3159

|67

AI Summary

This assignment requires a thorough analysis of Telstra Corporation Limited's 2016 Annual Report. The focus is on understanding the company's financial performance, examining its key assets like Property, Plant & Equipment, Goodwill, and Investments in Controlled Entities. The analysis should also delve into amortization details provided in Table-D and consider specific transactions like the sale of AUTOHOME detailed in Table-B.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Company and Financial Reporting

EXECUTIVE SUMMARY

‘Conceptual Framework’ is a concise presentation of a company’s financial aspects,

especially those which demonstrate its financial strengths. AASB has framed three

standards for this, namely AASB 101, AASB 136 and AASB 138.

AASB 101 is related to the financial statements which provide information about

financial position, financial performance and cash flows of the entity. This can be used

by a wide range of users for making economic decisions. In the case of Telstra, this

information assists this report in understanding Telstra’s future cash flows, in particular,

their timing and certainty.

AASB 136 Impairment of Assets deals with the issue of impairment of an asset and it

defines this as –

‘An asset is impaired when its carrying amount exceeds its recoverable amount.’

This report concludes that when estimating an asset’s recoverable amount from the

financial statement of Telstra, the management uses a great degree of judgement and

estimation.

Objective AASB 138, which deals with Intangible Assets, is to account for how these

non-monetary assets which have no physical presence, can be recognised, measured and

disclosed within financial statement of Telstra.

PART – I

ANSWER – 1 (a)

Management of Telstra has the practice of identifying all profit earning segments as

Cash Generating Units (CGUs), Telstra, (2016). With the commencement of the revised

NBN Definitive Agreements (NBN DAs), the company is going to transfer the Hybrid

Fibre Coaxial (HFC) cable network, which was functioning as a separate CGU for

EXECUTIVE SUMMARY

‘Conceptual Framework’ is a concise presentation of a company’s financial aspects,

especially those which demonstrate its financial strengths. AASB has framed three

standards for this, namely AASB 101, AASB 136 and AASB 138.

AASB 101 is related to the financial statements which provide information about

financial position, financial performance and cash flows of the entity. This can be used

by a wide range of users for making economic decisions. In the case of Telstra, this

information assists this report in understanding Telstra’s future cash flows, in particular,

their timing and certainty.

AASB 136 Impairment of Assets deals with the issue of impairment of an asset and it

defines this as –

‘An asset is impaired when its carrying amount exceeds its recoverable amount.’

This report concludes that when estimating an asset’s recoverable amount from the

financial statement of Telstra, the management uses a great degree of judgement and

estimation.

Objective AASB 138, which deals with Intangible Assets, is to account for how these

non-monetary assets which have no physical presence, can be recognised, measured and

disclosed within financial statement of Telstra.

PART – I

ANSWER – 1 (a)

Management of Telstra has the practice of identifying all profit earning segments as

Cash Generating Units (CGUs), Telstra, (2016). With the commencement of the revised

NBN Definitive Agreements (NBN DAs), the company is going to transfer the Hybrid

Fibre Coaxial (HFC) cable network, which was functioning as a separate CGU for

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

impairment assessment, to the assets of NBN Co. The transfer will include assets such

as Lead-in Conduits (LICs), HFC and certain other external infrastructure assets

associated with this CGU. The management has acknowledged that after the revised

NBN Das coming into force, it is not possible to separate the cash inflows jointly

generated by both the networks, as per Baker & Riddick, (2013). (See Extract-01 of

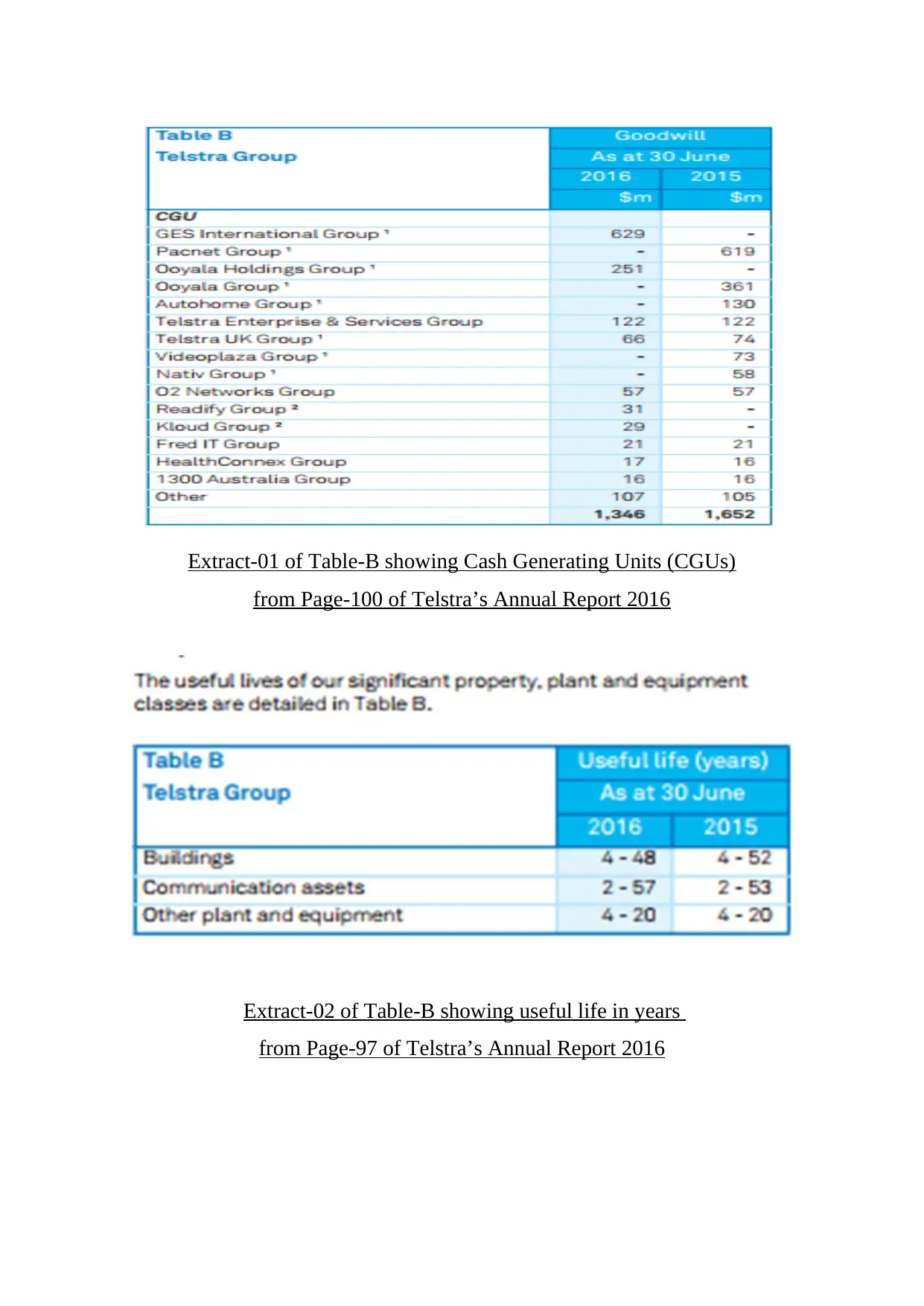

Table-B showing Cash Generating Units (CGUs) from Page-100 of Telstra’s Annual

Report 2016 in Appendix)

This is also in conformation with the Australian Conceptual Framework which

prescribes AASB 101, the standard which prescribes the following segments to be

reported cohesively.

Acquisition

Property, Plant and Equipment are to be recorded at cost price less the accumulated

depreciation and impairment. Telstra capitalises all borrowing costs, attributing them

directly to an acquisition of a qualifying asset. Telstra then recognises as expense all

other borrowing costs in its income statement, assert Greuning, Scott & Terblanche,

(2011).

Depreciation

All items of Property, Plant and Equipment are depreciated by Telstra on a straight-line

basis over their estimated useful lives, Telstra, (2016). Depreciation of assets starts after

their installation. The useful lives of the Property, Plant and Equipment assets are

shown in Table B, as per Janousek et al, (2015). (See Extract-02 of Table-B showing

Useful Life of Assets in Years from Page-97 of Telstra’s Annual Report 2016 in

Appendix)

ANSWER – 1 (b)

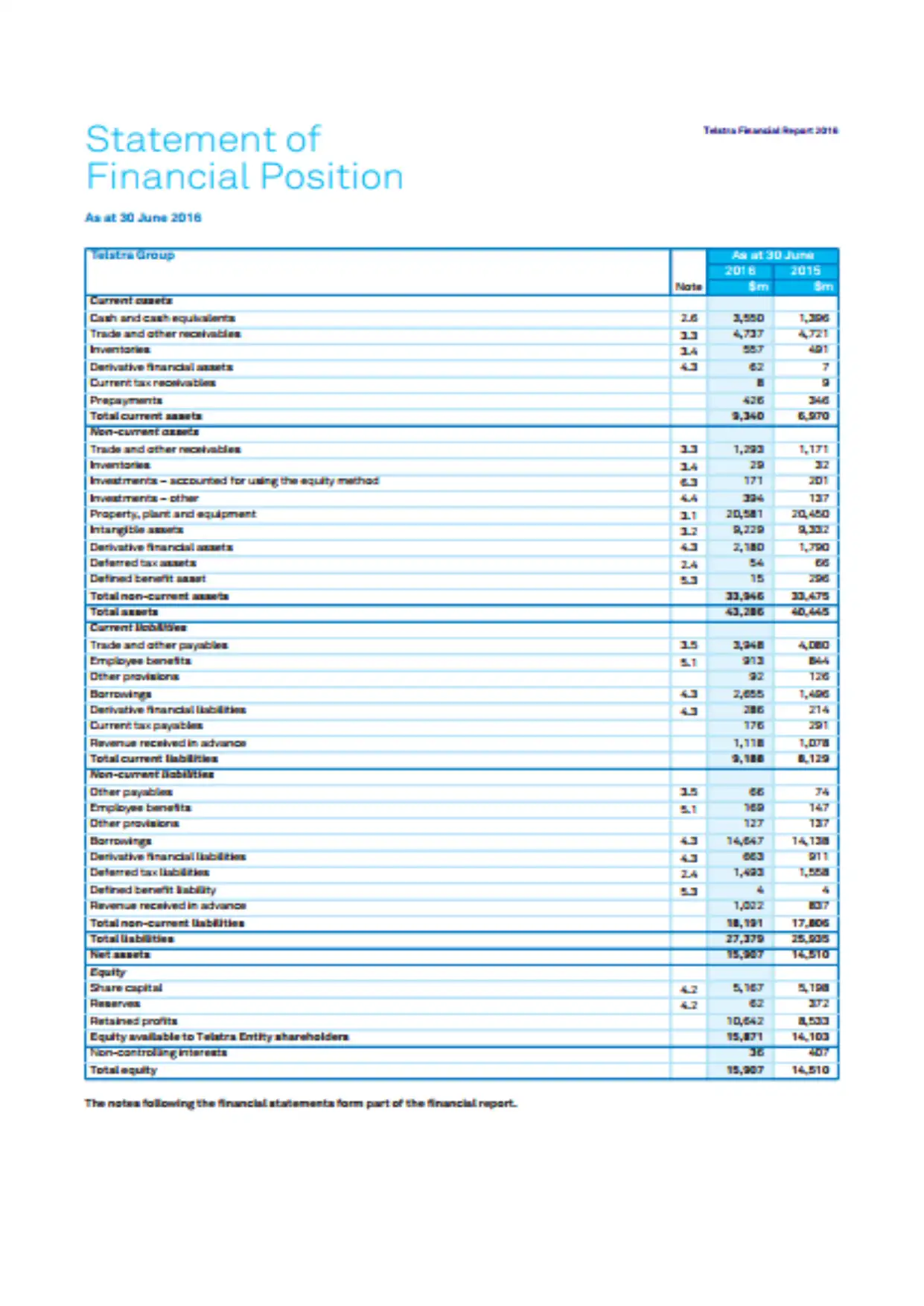

Telstra transferred its assets valued at $1,004 million, as explained above, to NBN Co.

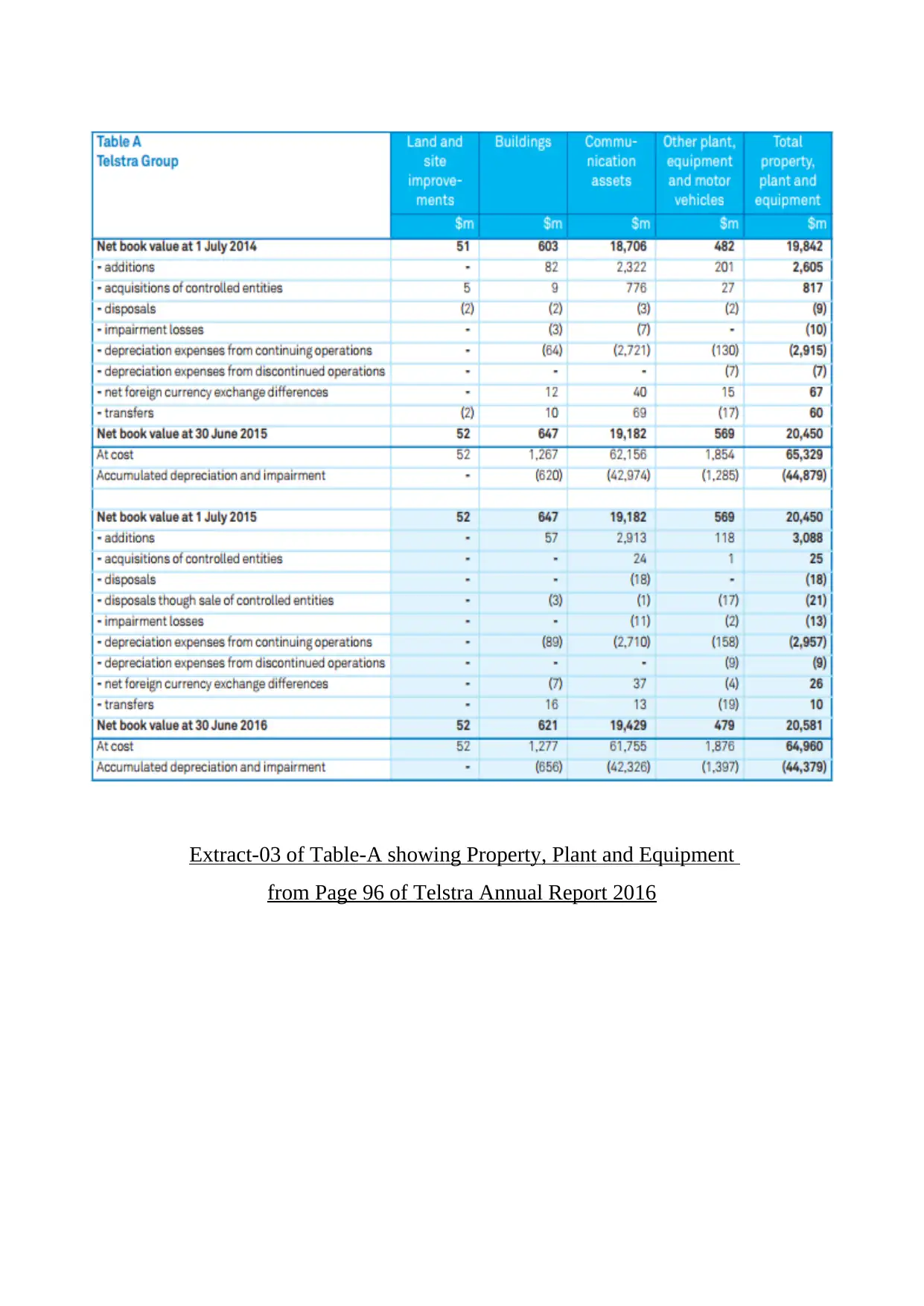

under the revised NBN DAs as at 30 June 2016. This was 4.9 per cent of Telstra’s Net

Book Value of its total Property, Plant and Equipment (See Extract-03 of Table-A

showing Details of Property, Plant and Equipment from page 96 of Telstra Annual

Report 2016 in Appendix). Management judgement was applied by Telstra in assessing

as Lead-in Conduits (LICs), HFC and certain other external infrastructure assets

associated with this CGU. The management has acknowledged that after the revised

NBN Das coming into force, it is not possible to separate the cash inflows jointly

generated by both the networks, as per Baker & Riddick, (2013). (See Extract-01 of

Table-B showing Cash Generating Units (CGUs) from Page-100 of Telstra’s Annual

Report 2016 in Appendix)

This is also in conformation with the Australian Conceptual Framework which

prescribes AASB 101, the standard which prescribes the following segments to be

reported cohesively.

Acquisition

Property, Plant and Equipment are to be recorded at cost price less the accumulated

depreciation and impairment. Telstra capitalises all borrowing costs, attributing them

directly to an acquisition of a qualifying asset. Telstra then recognises as expense all

other borrowing costs in its income statement, assert Greuning, Scott & Terblanche,

(2011).

Depreciation

All items of Property, Plant and Equipment are depreciated by Telstra on a straight-line

basis over their estimated useful lives, Telstra, (2016). Depreciation of assets starts after

their installation. The useful lives of the Property, Plant and Equipment assets are

shown in Table B, as per Janousek et al, (2015). (See Extract-02 of Table-B showing

Useful Life of Assets in Years from Page-97 of Telstra’s Annual Report 2016 in

Appendix)

ANSWER – 1 (b)

Telstra transferred its assets valued at $1,004 million, as explained above, to NBN Co.

under the revised NBN DAs as at 30 June 2016. This was 4.9 per cent of Telstra’s Net

Book Value of its total Property, Plant and Equipment (See Extract-03 of Table-A

showing Details of Property, Plant and Equipment from page 96 of Telstra Annual

Report 2016 in Appendix). Management judgement was applied by Telstra in assessing

the useful lives of these assets and was based on the anticipated NBNTM network rollout

period, Telstra, (2016). The full impact on the useful lives of these assets cannot be

assessed fully as of now and will depend on the selection of access technologies by

NBN Co. in each of the rollout region and also on the sequence in which this rollout

progresses, as per Cichosz, (2014). (See Extract-04 of Table-A Goodwill and other

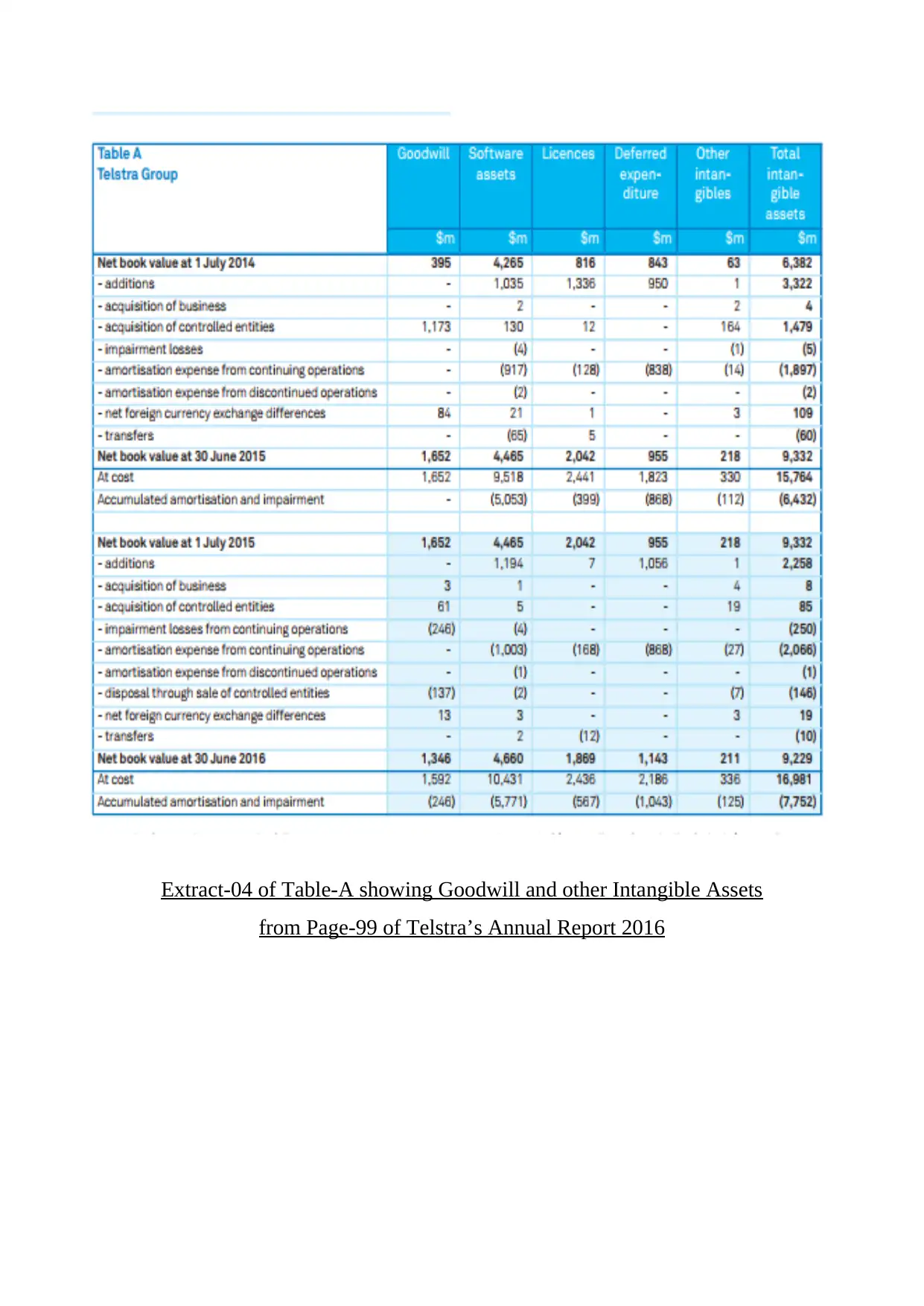

Intangible assets from Page-99 of Telstra’s Annual Report 2016 in Appendix). During

the financial year 2016, Telstra has made assessment of its telecommunications network

CGU based on the identify indicators of impairment, as has been specified by AASB

standard 136. This has been done by using both the external as well as the internal

sources of information, asserts Yona, (2011).

PART – II

ANSWER – 2 (a)

Rolling out the services of 4G voice by using the small cells technology was part of

Telstra’s long standing commitment towards expansion of its 4G coverage in the

regional Australia. This has made Telstra, the first carrier in Australia which is going to

provide 4G voice services to customers using the small cell technology. During this

financial year itself, Telstra has identified 50 small cell sites with 4G voice services and

have already become operational in rural Australia, Telstra, (2016). A further 10 more

such sites are expected to be activated by the end of June. This technology is based on

the ongoing investment commitments under the revised NBN DAs which Telstra is

making in the rural areas of Australia for its mobile network used by the rural

customers, as per Kurth, (2011).

A small cell is kind of a miniature version of the large size standard base station which

are set up by telcos, mostly in highly congested networks found in densely populated

urban areas. The purpose of the small cell is also to boost coverage and capacity of the

4G voice calls in rural areas. Being a technical hardware, the small cells are also

classified under the Property, Plant and Equipment head in the Annual Report of 2016,

Telstra, (2016). Since Telstra’s commitment is part of its support to the Federal

Government’s Mobile Black Spots program, the management is committed to funding

period, Telstra, (2016). The full impact on the useful lives of these assets cannot be

assessed fully as of now and will depend on the selection of access technologies by

NBN Co. in each of the rollout region and also on the sequence in which this rollout

progresses, as per Cichosz, (2014). (See Extract-04 of Table-A Goodwill and other

Intangible assets from Page-99 of Telstra’s Annual Report 2016 in Appendix). During

the financial year 2016, Telstra has made assessment of its telecommunications network

CGU based on the identify indicators of impairment, as has been specified by AASB

standard 136. This has been done by using both the external as well as the internal

sources of information, asserts Yona, (2011).

PART – II

ANSWER – 2 (a)

Rolling out the services of 4G voice by using the small cells technology was part of

Telstra’s long standing commitment towards expansion of its 4G coverage in the

regional Australia. This has made Telstra, the first carrier in Australia which is going to

provide 4G voice services to customers using the small cell technology. During this

financial year itself, Telstra has identified 50 small cell sites with 4G voice services and

have already become operational in rural Australia, Telstra, (2016). A further 10 more

such sites are expected to be activated by the end of June. This technology is based on

the ongoing investment commitments under the revised NBN DAs which Telstra is

making in the rural areas of Australia for its mobile network used by the rural

customers, as per Kurth, (2011).

A small cell is kind of a miniature version of the large size standard base station which

are set up by telcos, mostly in highly congested networks found in densely populated

urban areas. The purpose of the small cell is also to boost coverage and capacity of the

4G voice calls in rural areas. Being a technical hardware, the small cells are also

classified under the Property, Plant and Equipment head in the Annual Report of 2016,

Telstra, (2016). Since Telstra’s commitment is part of its support to the Federal

Government’s Mobile Black Spots program, the management is committed to funding

up to 250 small cells during its overall expansion program. In this regard, full funding is

being provided by Telstra from its internal resources, say Marchildon & McDowall,

(2013).

Deferred Expenditure

A Deferred Expenditure is not only related to the direct incremental costs associated

with the establishment of a customer contract, it also relates to the costs incurred for

installation and connection fees for providing basic access to existing and new services.

It also relates to the deferred costs which are related to the costs incurred on small cell

installations under the revised NBN DAs, Telstra, (2016). All such costs, incurred in

excess of the future revenues earned, shall be recognised in the subsequent income

statement reported in the Annual Report of 2017. The amortised deferred expenditure,

which is expected to be realised, shall be recognised in the subsequent operating

expenses of 2017, as explained by Cichosz, (2014).

ANSWER – 2 (b)

Telstra’s intangible assets mainly include the following three items –

A. All IT related development costs of designing, building and testing of new or

improvised IT systems.

B. Research costs which are expensed when incurred.

C. Capitalised development costs, which include:

(a) External direct costs related to materials and services consumed.

(b) Payroll and payroll-related costs for employees associated with a project.

(c) Borrowing costs which are directly attributed to a qualifying asset.

All internally generated intangible assets are assessed as having a finite life and hence

are amortised over their useful lives on a straight-line basis. Recognition of the

development costs are done on the basis of management judgement (Refer to

‘Capitalisation of development costs’), Telstra, (2016).

PART – III

being provided by Telstra from its internal resources, say Marchildon & McDowall,

(2013).

Deferred Expenditure

A Deferred Expenditure is not only related to the direct incremental costs associated

with the establishment of a customer contract, it also relates to the costs incurred for

installation and connection fees for providing basic access to existing and new services.

It also relates to the deferred costs which are related to the costs incurred on small cell

installations under the revised NBN DAs, Telstra, (2016). All such costs, incurred in

excess of the future revenues earned, shall be recognised in the subsequent income

statement reported in the Annual Report of 2017. The amortised deferred expenditure,

which is expected to be realised, shall be recognised in the subsequent operating

expenses of 2017, as explained by Cichosz, (2014).

ANSWER – 2 (b)

Telstra’s intangible assets mainly include the following three items –

A. All IT related development costs of designing, building and testing of new or

improvised IT systems.

B. Research costs which are expensed when incurred.

C. Capitalised development costs, which include:

(a) External direct costs related to materials and services consumed.

(b) Payroll and payroll-related costs for employees associated with a project.

(c) Borrowing costs which are directly attributed to a qualifying asset.

All internally generated intangible assets are assessed as having a finite life and hence

are amortised over their useful lives on a straight-line basis. Recognition of the

development costs are done on the basis of management judgement (Refer to

‘Capitalisation of development costs’), Telstra, (2016).

PART – III

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ANSWER – 3 (a)

Telstra accounts for its acquired joint ventures as well as the associated entities using

the equity method. The company recognises the investment under this method at

acquisition cost and this is subsequently adjusted by the share of profits or losses

received. Such receipts are duly recognised in the relevant income statement of the

company under comprehensive income, assert Greuning, Scott & Terblanche, (2011).

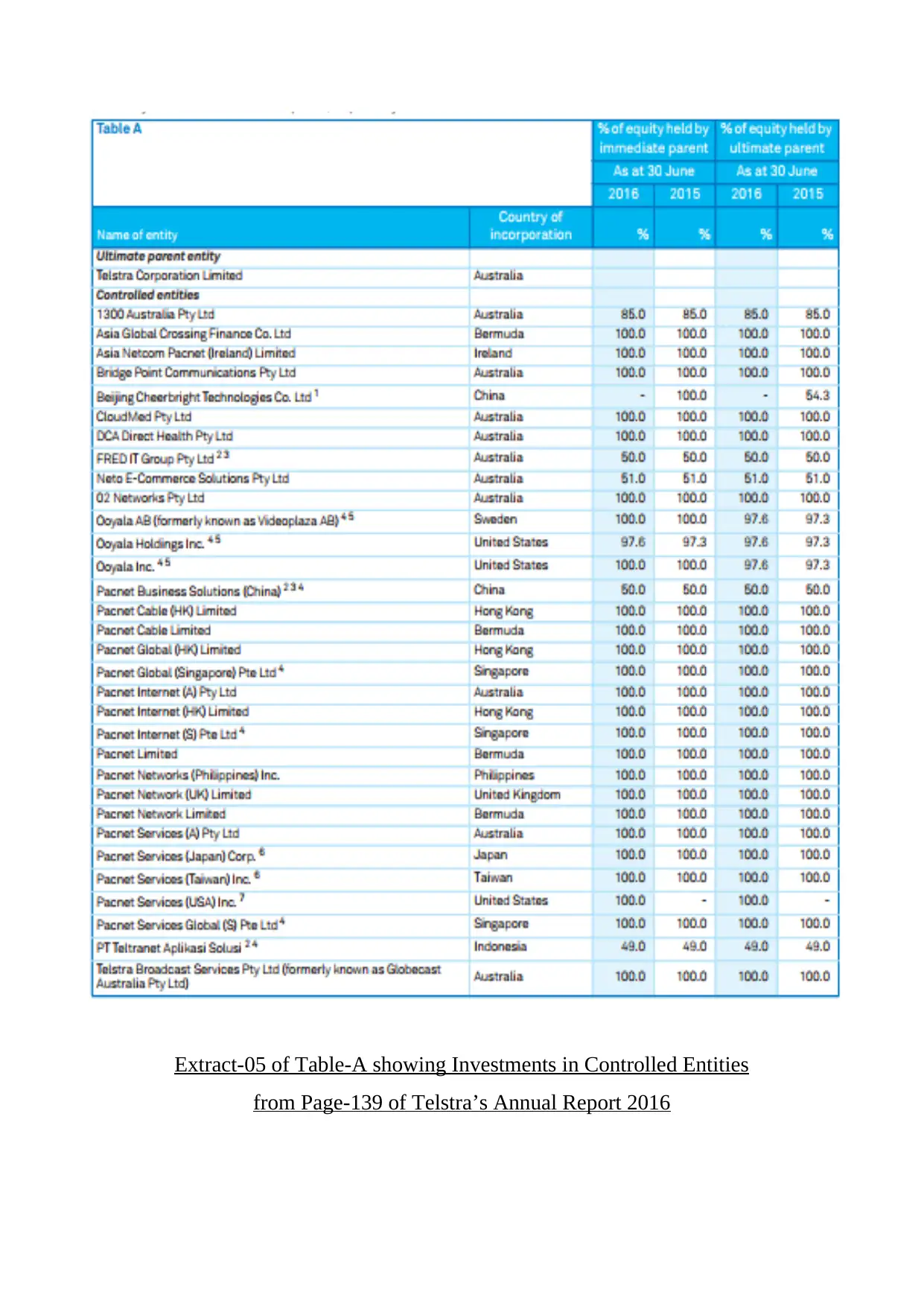

Telstra entered into venture capital investments in the year 2008, investing mainly in

controlled entities and a list of its investments in such controlled entities is detailed in

Table –A, Telstra, (2016).

This table gives details of the company’s material operating controlled entities as at 30

June 2016. This presentation is segregated on the basis of the percentage of earnings

before interest, income tax expense, depreciation and amortisation (EBITDA) of each

entity and includes the details of Ooyala too, Telstra, (2016). The company’s ownership

percentage in Ooyala represents that portion of equity which was held by Telstra in the

subsidiary as well as in its immediate parent respectively, according to Mudra, (2014).

(See Extract-05 of Table-A showing Investments in Controlled Entities from Page-139

of Telstra’s Annual Report 2016 in Appendix)

The statement confirmed that the fair value of trade and other receivables was equal to

the gross contractual amount which the company expected to collect. The goodwill

component describes the cost synergies, revenue growth opportunities, workforce talent

and the future profitability of the acquired business. No goodwill, recognised at present,

is going to be claimed as a deductible expense for income tax purposes. All acquisition

costs, incurred during acquisition, have been included under the head ‘other expenses’

in the income statement of the relevant year, assert Keown et al, (2012).

ANSWER – 3 (b)

There are two reasons why companies do this and the first reason is strategic. This

happens because the processes have been in-built over the years and hence, it is difficult

for managements to avoid or innovate them. The second reason is financial. Companies

Telstra accounts for its acquired joint ventures as well as the associated entities using

the equity method. The company recognises the investment under this method at

acquisition cost and this is subsequently adjusted by the share of profits or losses

received. Such receipts are duly recognised in the relevant income statement of the

company under comprehensive income, assert Greuning, Scott & Terblanche, (2011).

Telstra entered into venture capital investments in the year 2008, investing mainly in

controlled entities and a list of its investments in such controlled entities is detailed in

Table –A, Telstra, (2016).

This table gives details of the company’s material operating controlled entities as at 30

June 2016. This presentation is segregated on the basis of the percentage of earnings

before interest, income tax expense, depreciation and amortisation (EBITDA) of each

entity and includes the details of Ooyala too, Telstra, (2016). The company’s ownership

percentage in Ooyala represents that portion of equity which was held by Telstra in the

subsidiary as well as in its immediate parent respectively, according to Mudra, (2014).

(See Extract-05 of Table-A showing Investments in Controlled Entities from Page-139

of Telstra’s Annual Report 2016 in Appendix)

The statement confirmed that the fair value of trade and other receivables was equal to

the gross contractual amount which the company expected to collect. The goodwill

component describes the cost synergies, revenue growth opportunities, workforce talent

and the future profitability of the acquired business. No goodwill, recognised at present,

is going to be claimed as a deductible expense for income tax purposes. All acquisition

costs, incurred during acquisition, have been included under the head ‘other expenses’

in the income statement of the relevant year, assert Keown et al, (2012).

ANSWER – 3 (b)

There are two reasons why companies do this and the first reason is strategic. This

happens because the processes have been in-built over the years and hence, it is difficult

for managements to avoid or innovate them. The second reason is financial. Companies

like Telstra, who are aspiring tech companies are often found to have piled a large

amount of excess cash, Telstra, (2016). Hence, acquisitions become an easy way out to

invest this excess cash. Moreover, investments made in start-up entities provides Telstra

with fresh insight into the emerging industries, as stated by Kurth, (2011). Theoretically,

the factor most widely considered by an investing company is to create a hedge against

any new, potential competitor. Telstra accounts for the acquisition of its controlled

entities by using the Acquisition Method of accounting, Telstra, (2016). This method

involves the recognition of the acquiree entities identifiable assets, liabilities and

contingent liabilities taken at their fair values as on the acquisition date. Goodwill is

recognised as the excess amount over and above the fair value. Telstra deducts the

expenses of acquisition as incurred expenses in its income statement, assert Marchildon

& McDowall, (2013).

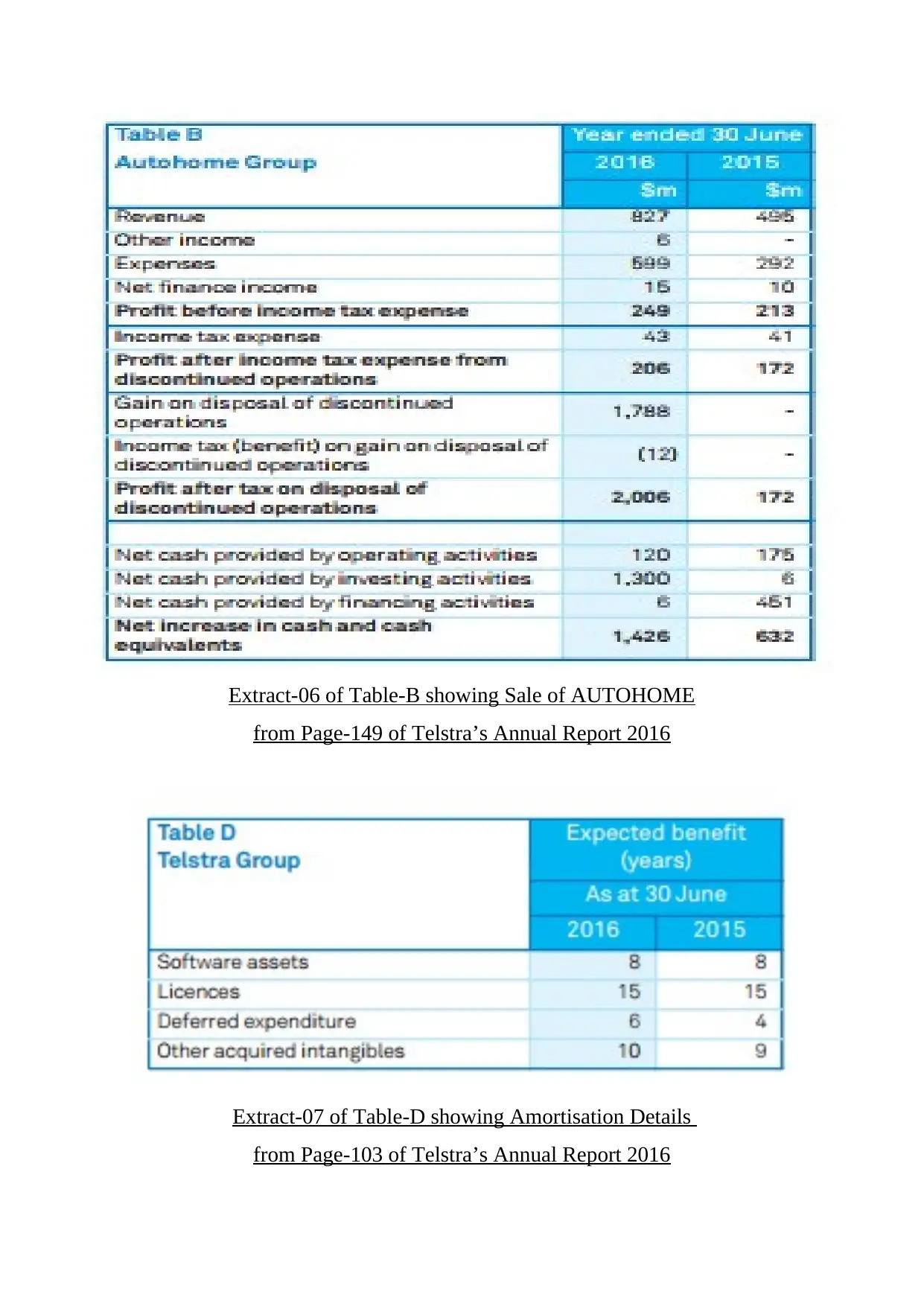

Current Year Disposals

Telstra’s receipts from sale of businesses including its share in the controlled entities,

taken at net of cash disposed, for the current financial year, are $1,340 million. Of this,

$1,323 million is from the sale of controlling rights in Autohome Inc. and its controlled

entities, on 23 June 2016. (See Extract-06 of Table-B showing Sale of Autohome Group

from Page-149 of Telstra’s Annual Report 2016 in Appendix)

Non-controlling Interests

Non-controlling interests, on the date of acquisition, are measured either at their fair

value or at non-controlling shareholders’ proportion of the assumed net fair value of the

asset. Such transactions are recorded directly under the statement of comprehensive

income, as stated by Marchildon & McDowall, (2013).

Contingent Consideration

This is recognised at the fair value of the asset at the time of acquisition, with any

changes in the recognised fair value taken in the income statement. In case a business is

acquired in stages, Telstra re-measures the previously held equity interest at the

acquisition fair value and the resulting gain or loss is shown in the income statement,

say Greuning, Scott & Terblanche, (2011).

PART – IV

ANSWER – 4 (a)

amount of excess cash, Telstra, (2016). Hence, acquisitions become an easy way out to

invest this excess cash. Moreover, investments made in start-up entities provides Telstra

with fresh insight into the emerging industries, as stated by Kurth, (2011). Theoretically,

the factor most widely considered by an investing company is to create a hedge against

any new, potential competitor. Telstra accounts for the acquisition of its controlled

entities by using the Acquisition Method of accounting, Telstra, (2016). This method

involves the recognition of the acquiree entities identifiable assets, liabilities and

contingent liabilities taken at their fair values as on the acquisition date. Goodwill is

recognised as the excess amount over and above the fair value. Telstra deducts the

expenses of acquisition as incurred expenses in its income statement, assert Marchildon

& McDowall, (2013).

Current Year Disposals

Telstra’s receipts from sale of businesses including its share in the controlled entities,

taken at net of cash disposed, for the current financial year, are $1,340 million. Of this,

$1,323 million is from the sale of controlling rights in Autohome Inc. and its controlled

entities, on 23 June 2016. (See Extract-06 of Table-B showing Sale of Autohome Group

from Page-149 of Telstra’s Annual Report 2016 in Appendix)

Non-controlling Interests

Non-controlling interests, on the date of acquisition, are measured either at their fair

value or at non-controlling shareholders’ proportion of the assumed net fair value of the

asset. Such transactions are recorded directly under the statement of comprehensive

income, as stated by Marchildon & McDowall, (2013).

Contingent Consideration

This is recognised at the fair value of the asset at the time of acquisition, with any

changes in the recognised fair value taken in the income statement. In case a business is

acquired in stages, Telstra re-measures the previously held equity interest at the

acquisition fair value and the resulting gain or loss is shown in the income statement,

say Greuning, Scott & Terblanche, (2011).

PART – IV

ANSWER – 4 (a)

Capitalisation of Development Costs

Once the rollout of NBN is completed, Telstra may have to replace all those earnings

which will be lost because of this huge outlay. A simple logic is behind this. Whenever

a company tries to convert the Development Costs into Capitalisation of Assets, it

must suffer the consequences of lost revenues, as per Cichosz, (2014). Development

costs should only be capitalised when the project has been, technically and

commercially, assessed to be feasible. This in fact depends on the following two factors

–

(a) Amortisation

The company applies a managed judgement for determining the amortisation period

which is based on the expected useful lives of each class of assets. At present, the

average amortisation periods of Telstra’s identifiable intangible assets are as shown in

Table-D. (See Extract-07 of Table-D showing Amortisation Details from Page-103 of

Telstra’s Annual Report 2016 in Appendix)

(b) Useful Lives of Intangible Assets

In addition to the above, the company also applies a managed judgement for assessing,

on an annual basis, the indefinite useful life assumption which is required to be applied

in certain acquired intangible assets. The net calculated effect of such a reassessment of

the useful lives, for the financial year 2016, was found to be $67 million as compared to

$51 million in 2015, Telstra, (2016). Telstra has already given indications that the

rollout of National Broadband Network is bound to cut $2 to $3 billion annually from

its earnings. Telstra is sure to remain the biggest telco in Australia, but the management

will need to find newer revenue streams or must reduce its debt, once the NBN is active,

if it wants to maintain its current A2 credit rating, as stated by Keown et al, (2012).

ANSWER – 4 (b)

The two factors which are going to affect Telstra’s choices, shown above, of its

amortisation of software assets are –

1. Trade and Other Receivables

Once the NBN rollout is completed and it is due by 2020, Telstra may find its earnings

margin contracting down to high 30%. Telstra will not be compensated for loss of its

Once the rollout of NBN is completed, Telstra may have to replace all those earnings

which will be lost because of this huge outlay. A simple logic is behind this. Whenever

a company tries to convert the Development Costs into Capitalisation of Assets, it

must suffer the consequences of lost revenues, as per Cichosz, (2014). Development

costs should only be capitalised when the project has been, technically and

commercially, assessed to be feasible. This in fact depends on the following two factors

–

(a) Amortisation

The company applies a managed judgement for determining the amortisation period

which is based on the expected useful lives of each class of assets. At present, the

average amortisation periods of Telstra’s identifiable intangible assets are as shown in

Table-D. (See Extract-07 of Table-D showing Amortisation Details from Page-103 of

Telstra’s Annual Report 2016 in Appendix)

(b) Useful Lives of Intangible Assets

In addition to the above, the company also applies a managed judgement for assessing,

on an annual basis, the indefinite useful life assumption which is required to be applied

in certain acquired intangible assets. The net calculated effect of such a reassessment of

the useful lives, for the financial year 2016, was found to be $67 million as compared to

$51 million in 2015, Telstra, (2016). Telstra has already given indications that the

rollout of National Broadband Network is bound to cut $2 to $3 billion annually from

its earnings. Telstra is sure to remain the biggest telco in Australia, but the management

will need to find newer revenue streams or must reduce its debt, once the NBN is active,

if it wants to maintain its current A2 credit rating, as stated by Keown et al, (2012).

ANSWER – 4 (b)

The two factors which are going to affect Telstra’s choices, shown above, of its

amortisation of software assets are –

1. Trade and Other Receivables

Once the NBN rollout is completed and it is due by 2020, Telstra may find its earnings

margin contracting down to high 30%. Telstra will not be compensated for loss of its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earnings by the wholesale business which it is expecting from the rollout, says Mudra,

(2014).

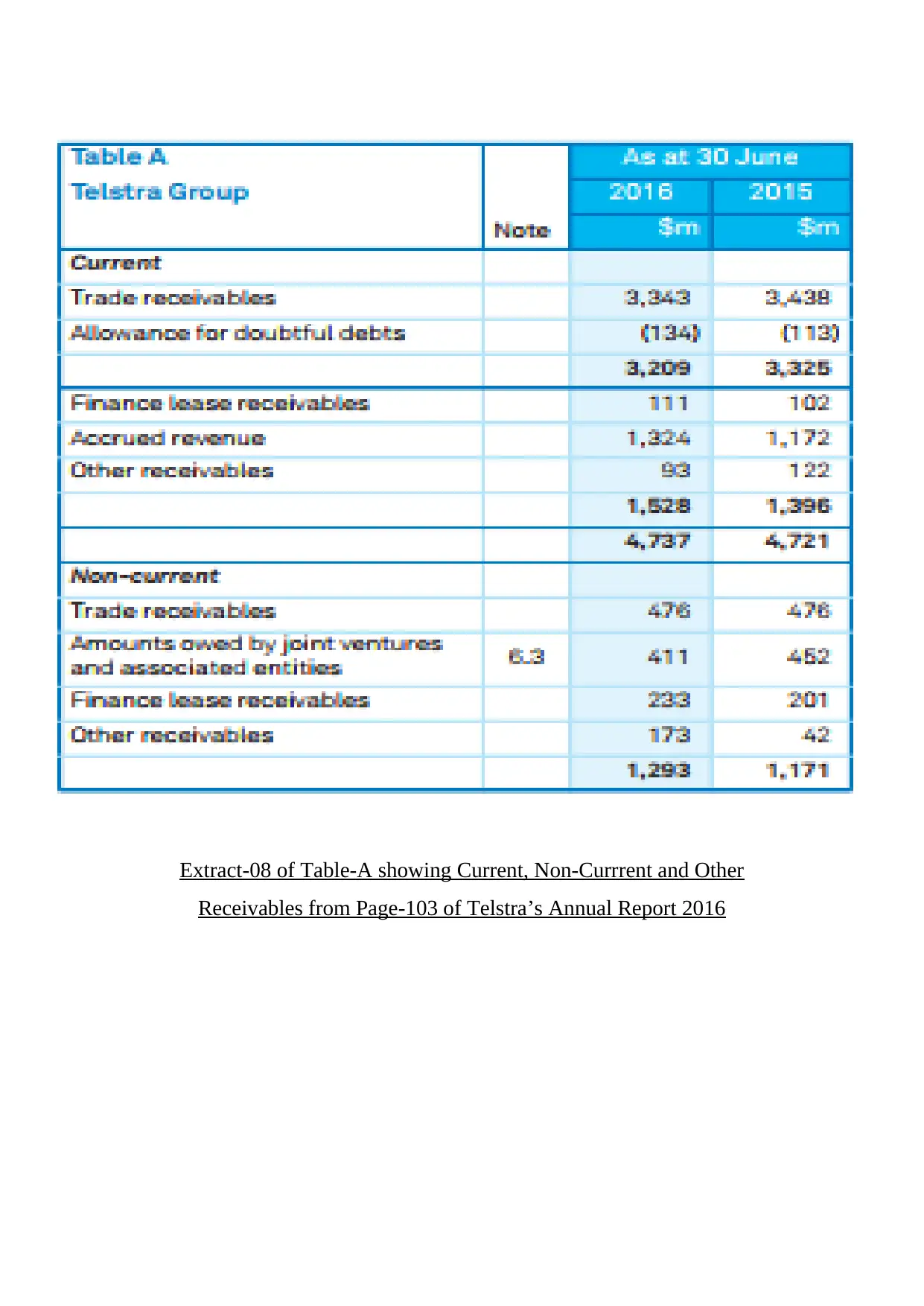

2. Current and Non-current Trade and Other Receivables

Although Telstra will remain the industry leader, it will lose a huge portion of its fixed

retail voice and broadband market share. Moreover, its mobile market share is also

going to stagnate or may fall due to competitors getting stronger. To permanently fill

this earnings gap, Telstra needs to find new revenue streams and to increase its existing

streams, Telstra, (2016). Assuming that Telstra has an earnings gap in 2020, it could

maintain its credit ratings by either reducing the dividend payments and using the extra

cash for cutting its debt or by acquiring extra cash from other sources, such as NBN

payments or sale of some of its non-core business, asserts Mudra, (2014).

(See Extract-08 of Table-A showing Current and Non-current Trade and Other

Receivables from Page-103 of Telstra’s Annual Report 2016 in Appendix)

LIST OF REFERENCES

Baker, H.K. and Riddick, L.A. 2013. International Finance: A Survey. OUP USA,

Oxford.

Cichosz, P. 2014. Data Mining Algorithms: Explained Using R. John Wiley & Sons,

West Sussex.

Greuning, H., Scott, D. and Terblanche, S. 2011. International Financial Reporting

Standards: A Practical Guide. World Bank Publications, Washington DC.

Janousek, V., Moyen, J., Martin, H., Erban, V. and Farrow, C. 2015. Geochemical

Modelling of Igneous Processes. Springer, Berlin.

Keown, A.J., Martin, J.D., Petty, J.W. and Scott, D.F. 2012. Financial Management:

Principles and Applications (10th ed). Pearson Education India, New Delhi.

Kurth, S. 2011. Discuss covered interest rate parity (CIRP) with reference to foreign

exchange market efficiency. GRIN Verlag, Norderstedt.

Marchildon, G.P. and McDowall, D. 2013. Canadian Multinationals and International

Finance. Routledge, New York.

(2014).

2. Current and Non-current Trade and Other Receivables

Although Telstra will remain the industry leader, it will lose a huge portion of its fixed

retail voice and broadband market share. Moreover, its mobile market share is also

going to stagnate or may fall due to competitors getting stronger. To permanently fill

this earnings gap, Telstra needs to find new revenue streams and to increase its existing

streams, Telstra, (2016). Assuming that Telstra has an earnings gap in 2020, it could

maintain its credit ratings by either reducing the dividend payments and using the extra

cash for cutting its debt or by acquiring extra cash from other sources, such as NBN

payments or sale of some of its non-core business, asserts Mudra, (2014).

(See Extract-08 of Table-A showing Current and Non-current Trade and Other

Receivables from Page-103 of Telstra’s Annual Report 2016 in Appendix)

LIST OF REFERENCES

Baker, H.K. and Riddick, L.A. 2013. International Finance: A Survey. OUP USA,

Oxford.

Cichosz, P. 2014. Data Mining Algorithms: Explained Using R. John Wiley & Sons,

West Sussex.

Greuning, H., Scott, D. and Terblanche, S. 2011. International Financial Reporting

Standards: A Practical Guide. World Bank Publications, Washington DC.

Janousek, V., Moyen, J., Martin, H., Erban, V. and Farrow, C. 2015. Geochemical

Modelling of Igneous Processes. Springer, Berlin.

Keown, A.J., Martin, J.D., Petty, J.W. and Scott, D.F. 2012. Financial Management:

Principles and Applications (10th ed). Pearson Education India, New Delhi.

Kurth, S. 2011. Discuss covered interest rate parity (CIRP) with reference to foreign

exchange market efficiency. GRIN Verlag, Norderstedt.

Marchildon, G.P. and McDowall, D. 2013. Canadian Multinationals and International

Finance. Routledge, New York.

Mudra, J. 2014. International Financial Management (12th ed). Cengage Learning,

Stamford, CT.

Telstra Corporation Limited. (AU) Annual Report 2016. Extracted on 1 October 2017

from https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/FY16-

Annual-Report.pdf

Yona, L. 2011. International Finance for Developing Countries. Author House,

Keynes.

APPENDIX

Stamford, CT.

Telstra Corporation Limited. (AU) Annual Report 2016. Extracted on 1 October 2017

from https://www.telstra.com.au/content/dam/tcom/about-us/investors/pdf-e/FY16-

Annual-Report.pdf

Yona, L. 2011. International Finance for Developing Countries. Author House,

Keynes.

APPENDIX

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Extract-01 of Table-B showing Cash Generating Units (CGUs)

from Page-100 of Telstra’s Annual Report 2016

Extract-02 of Table-B showing useful life in years

from Page-97 of Telstra’s Annual Report 2016

from Page-100 of Telstra’s Annual Report 2016

Extract-02 of Table-B showing useful life in years

from Page-97 of Telstra’s Annual Report 2016

Extract-03 of Table-A showing Property, Plant and Equipment

from Page 96 of Telstra Annual Report 2016

from Page 96 of Telstra Annual Report 2016

Extract-04 of Table-A showing Goodwill and other Intangible Assets

from Page-99 of Telstra’s Annual Report 2016

from Page-99 of Telstra’s Annual Report 2016

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Extract-05 of Table-A showing Investments in Controlled Entities

from Page-139 of Telstra’s Annual Report 2016

from Page-139 of Telstra’s Annual Report 2016

Extract-06 of Table-B showing Sale of AUTOHOME

from Page-149 of Telstra’s Annual Report 2016

Extract-07 of Table-D showing Amortisation Details

from Page-103 of Telstra’s Annual Report 2016

from Page-149 of Telstra’s Annual Report 2016

Extract-07 of Table-D showing Amortisation Details

from Page-103 of Telstra’s Annual Report 2016

Extract-08 of Table-A showing Current, Non-Currrent and Other

Receivables from Page-103 of Telstra’s Annual Report 2016

Receivables from Page-103 of Telstra’s Annual Report 2016

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.