Financial Reporting and Corporate Regulation in Australia

VerifiedAdded on 2023/06/07

|12

|2966

|397

Report

AI Summary

This report provides a comprehensive analysis of financial reporting practices in Australian companies, focusing on corporate regulation, the adoption of International Financial Reporting Standards (IFRS) within the Australian Accounting Standards Board (AASB) framework, and the significance of owner's equity. The discussion covers the importance of financial reporting regulations for various stakeholders, the role of the AASB in setting accounting standards, and the impact of IFRS adoption. The report examines owner’s equity components for selected companies, including Woolworths, Wesfarmers, JB Hi-Fi, and Metcash, and conducts a comparative analysis of their debt-to-equity ratios over a four-year period. The analysis aims to provide insights into the financial performance and regulatory environment of these companies, offering a detailed overview of their financial reporting practices and the implications of accounting standards.

Running head: COMPANY AND FINANCIAL REPORTING

Company and financial reporting

Name of the Student:

Name of the University:

Company and financial reporting

Name of the Student:

Name of the University:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPANY AND FINANCIAL REPORTING

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

The Corporate regulation and mangement..................................................................................3

Accounting standard setting of AASB and IFRS........................................................................4

Owner’s equity.............................................................................................................................6

Comparative analysis of debt and equity of the chosen companies:..............................................8

Conclusion:......................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

The Corporate regulation and mangement..................................................................................3

Accounting standard setting of AASB and IFRS........................................................................4

Owner’s equity.............................................................................................................................6

Comparative analysis of debt and equity of the chosen companies:..............................................8

Conclusion:......................................................................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

2COMPANY AND FINANCIAL REPORTING

Executive Summary

The following topic has three sections that consist of the need corporate regulation by business

management in the process of accounting, the evaluation of the adaptation of IFRS by the AASB

framework and analysis and importance of the owner’s equity in the four ASX listed company.

In addition to that the report would also analyze the change in the debt equity ratio for the last

four years. The primary motive of the discussion is to know the nature and purpose of the

financial reporting of the Australian companies under the guidance of the AASB framework.

Introduction

The primary objective is to provide a base for the analysis of the implications of in the

financial reporting for the organizations. With the help of the regulators the profession of

accountancy is powerful in the achievement a major rise in the comparability of financial

statements. It provides a usual boundary for what is to be accounted for in the financial reports,

along with the rules about how transactions and items must be accounted for. Moreover the

discussion deals with the adaptation of IFRS in the AASB framework (Acharya and Ryan 2016).

The participation of Australian accounting standard board in the setting process of global

accounting standard outlines the power and function of the contribution and working to the

worldwide process standard setting.

Executive Summary

The following topic has three sections that consist of the need corporate regulation by business

management in the process of accounting, the evaluation of the adaptation of IFRS by the AASB

framework and analysis and importance of the owner’s equity in the four ASX listed company.

In addition to that the report would also analyze the change in the debt equity ratio for the last

four years. The primary motive of the discussion is to know the nature and purpose of the

financial reporting of the Australian companies under the guidance of the AASB framework.

Introduction

The primary objective is to provide a base for the analysis of the implications of in the

financial reporting for the organizations. With the help of the regulators the profession of

accountancy is powerful in the achievement a major rise in the comparability of financial

statements. It provides a usual boundary for what is to be accounted for in the financial reports,

along with the rules about how transactions and items must be accounted for. Moreover the

discussion deals with the adaptation of IFRS in the AASB framework (Acharya and Ryan 2016).

The participation of Australian accounting standard board in the setting process of global

accounting standard outlines the power and function of the contribution and working to the

worldwide process standard setting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPANY AND FINANCIAL REPORTING

Discussion

The Corporate regulation and management

The importance for the regulation in the financial reporting is vital for the organizations

since there are various vital user of financial reporting that includes equity investors, employee,

analyst adviser, public the government and stakeholders. The various stakeholders however,

required to able to understand and interpret the monetary information in a organized process for

make the needed monetary decisions. In case the various accounting users made the financial

reports, it shall be made in varied ways that would comply with their suitable requirements. In

the case, the varied groups will understand the various financial reports their own ways thus may

create a global differences in the practice of accounting (Capkun, Collins and Jeanjean 2016).

The Accounting practices differ from country to country as well as their frame work of

regulation. Therefore in order to maintain a balance between the various accounting frameworks

the regulations are important. This also sets a boundary for the users of accounting so that there

is a systematic interpretation of the financial data. The requirements disclosure resolves some of

the issues that are associated with of information between the user groups of accounting. It also

enables the user to compare the inducements level with the received by the other users (Leuz,

and Wysocki 2016). The regulations therefore, addresses the various issues of financial

information by requiring the setting a boundary for the of certain key items of interest to the user

groups. With the help of the regulators the profession of accountancy is more powerful in

achieving a major increase in the financial statements comparability (Hoskin, Fizzell, and Cherry

2014). It provides a general framework for what is to be accounted for in the financial reports,

along with the rules about how items and transactions should be accounted for (Christensen, Lee,

Walker and Zeng 2015).

Discussion

The Corporate regulation and management

The importance for the regulation in the financial reporting is vital for the organizations

since there are various vital user of financial reporting that includes equity investors, employee,

analyst adviser, public the government and stakeholders. The various stakeholders however,

required to able to understand and interpret the monetary information in a organized process for

make the needed monetary decisions. In case the various accounting users made the financial

reports, it shall be made in varied ways that would comply with their suitable requirements. In

the case, the varied groups will understand the various financial reports their own ways thus may

create a global differences in the practice of accounting (Capkun, Collins and Jeanjean 2016).

The Accounting practices differ from country to country as well as their frame work of

regulation. Therefore in order to maintain a balance between the various accounting frameworks

the regulations are important. This also sets a boundary for the users of accounting so that there

is a systematic interpretation of the financial data. The requirements disclosure resolves some of

the issues that are associated with of information between the user groups of accounting. It also

enables the user to compare the inducements level with the received by the other users (Leuz,

and Wysocki 2016). The regulations therefore, addresses the various issues of financial

information by requiring the setting a boundary for the of certain key items of interest to the user

groups. With the help of the regulators the profession of accountancy is more powerful in

achieving a major increase in the financial statements comparability (Hoskin, Fizzell, and Cherry

2014). It provides a general framework for what is to be accounted for in the financial reports,

along with the rules about how items and transactions should be accounted for (Christensen, Lee,

Walker and Zeng 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPANY AND FINANCIAL REPORTING

The regulations may include the mandates like the conventions like the materiality, the

revenue recognition and objectivity. There exist various objectives and criteria that are helpful at

the time of choosing the method of accounting. The choice of accounting method must always be

reliable, relevant, understandable and comparable to all involved parties for the same to be

favorable to the accounting users. Accounting regulations may however, may limit the extent to

which the accountants are able to prepare the financial statements to meet the needs of different

user groups (Coleman, Cotei and Farhatn 2016). However, this may discourage the accountants

from experimenting new techniques of accounting transaction recordings. There is no assurance

that the standard procedure will provide the required information by the different groups of

financial reports. Yet, there is the need for the reports to be regulated as it would be comparable

and it can save money and time while adjusting them into a general arrangement.

Accounting standard setting of AASB and IFRS

Every major country has their own accounting standards, however to bring

standardization and comparability, efforts has been made by organizations like IFRS to bring in

the accountability with the Australian accounting standard board (AASB). The participation of

Australian accounting standard board in the setting process of global accounting standard

outlines the power and function of the contribution and working to the worldwide process

standard setting. The international financial reporting that has been adopted by Australia is

similar to the council for strategic direction of financial reporting (Jin, Shan and Taylor 2015).

Therefore, the operational process of AASB incorporates the work program and IASB and IFRS.

However, there is difference in involvement degree which may be substantive or non non

substantive. The operational process of Global public segment standard of accounting board is

strictly supervised by the AASB.

The regulations may include the mandates like the conventions like the materiality, the

revenue recognition and objectivity. There exist various objectives and criteria that are helpful at

the time of choosing the method of accounting. The choice of accounting method must always be

reliable, relevant, understandable and comparable to all involved parties for the same to be

favorable to the accounting users. Accounting regulations may however, may limit the extent to

which the accountants are able to prepare the financial statements to meet the needs of different

user groups (Coleman, Cotei and Farhatn 2016). However, this may discourage the accountants

from experimenting new techniques of accounting transaction recordings. There is no assurance

that the standard procedure will provide the required information by the different groups of

financial reports. Yet, there is the need for the reports to be regulated as it would be comparable

and it can save money and time while adjusting them into a general arrangement.

Accounting standard setting of AASB and IFRS

Every major country has their own accounting standards, however to bring

standardization and comparability, efforts has been made by organizations like IFRS to bring in

the accountability with the Australian accounting standard board (AASB). The participation of

Australian accounting standard board in the setting process of global accounting standard

outlines the power and function of the contribution and working to the worldwide process

standard setting. The international financial reporting that has been adopted by Australia is

similar to the council for strategic direction of financial reporting (Jin, Shan and Taylor 2015).

Therefore, the operational process of AASB incorporates the work program and IASB and IFRS.

However, there is difference in involvement degree which may be substantive or non non

substantive. The operational process of Global public segment standard of accounting board is

strictly supervised by the AASB.

5COMPANY AND FINANCIAL REPORTING

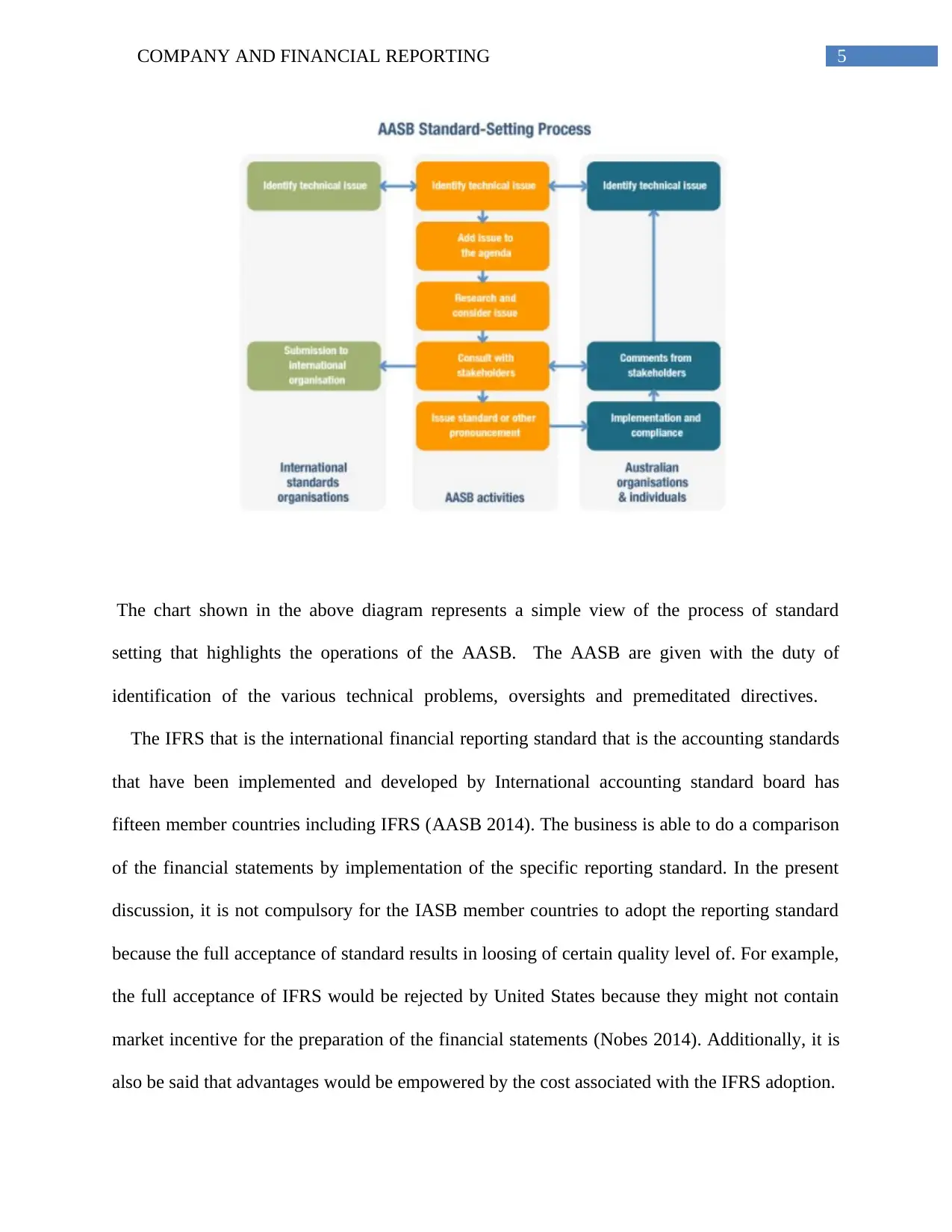

The chart shown in the above diagram represents a simple view of the process of standard

setting that highlights the operations of the AASB. The AASB are given with the duty of

identification of the various technical problems, oversights and premeditated directives.

The IFRS that is the international financial reporting standard that is the accounting standards

that have been implemented and developed by International accounting standard board has

fifteen member countries including IFRS (AASB 2014). The business is able to do a comparison

of the financial statements by implementation of the specific reporting standard. In the present

discussion, it is not compulsory for the IASB member countries to adopt the reporting standard

because the full acceptance of standard results in loosing of certain quality level of. For example,

the full acceptance of IFRS would be rejected by United States because they might not contain

market incentive for the preparation of the financial statements (Nobes 2014). Additionally, it is

also be said that advantages would be empowered by the cost associated with the IFRS adoption.

The chart shown in the above diagram represents a simple view of the process of standard

setting that highlights the operations of the AASB. The AASB are given with the duty of

identification of the various technical problems, oversights and premeditated directives.

The IFRS that is the international financial reporting standard that is the accounting standards

that have been implemented and developed by International accounting standard board has

fifteen member countries including IFRS (AASB 2014). The business is able to do a comparison

of the financial statements by implementation of the specific reporting standard. In the present

discussion, it is not compulsory for the IASB member countries to adopt the reporting standard

because the full acceptance of standard results in loosing of certain quality level of. For example,

the full acceptance of IFRS would be rejected by United States because they might not contain

market incentive for the preparation of the financial statements (Nobes 2014). Additionally, it is

also be said that advantages would be empowered by the cost associated with the IFRS adoption.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COMPANY AND FINANCIAL REPORTING

Owner’s equity

The owner's equity is one of the primary components of the balance sheet

and accounting equation. It represents the investment in the business deducting the owner's

draws or drawings from the operations adding with the net profit. It refers to the amount of assets

minus the liabilities. As the amounts need to follow the principle of cost the amount of equity

does not show the current fair market value of the organization. It is viewed as a residual

claim on the operational assets as the liabilities have a higher claim (De George, Li and

Shivakumar 2016). The owner’s equity can also be viewed as a business assets source. The

chosen Australian companies whose financial report is to be analyzed are Woolworths,

Wesfarmers, JB Hi-Fi and Met cash.

Analysis of items of equity of Woolworths:

The amount of contributed equity stood at $ (million) 6055 in year 2018 compared to $

5615, $ 5252 and 5064.9 in year 2017, 2016 and 2015 respectively. From the figures, it can be

said that the value of equity has risen since year 2015. The reserves are recorded at $ 353, $ 357

in year 2018 and 2017 compared to $ 93.9 and 95.1 in year 2016 and 2015. It can be suggested

that the reserves has increased (Johnston and Petacchi 2017). Furthermore, retained earnings are

recorded at $ 4073, $ 3554, $ 3124.5 and $ 5831.0 in year 2018, 2017, 2016 and 2015

respectively.

Analysis of each items of equity of Met cash:

For Met cash, the amount of contributed and other equity is recorded at $ 600 in year

2018 as against $ 1719.3, $ 1626, $ 2391.9 in year 2017, 2016 and 2015. As per the abnual

report the amounts of value of equity decreased in year 2018. Analyzing the amounts of the

Owner’s equity

The owner's equity is one of the primary components of the balance sheet

and accounting equation. It represents the investment in the business deducting the owner's

draws or drawings from the operations adding with the net profit. It refers to the amount of assets

minus the liabilities. As the amounts need to follow the principle of cost the amount of equity

does not show the current fair market value of the organization. It is viewed as a residual

claim on the operational assets as the liabilities have a higher claim (De George, Li and

Shivakumar 2016). The owner’s equity can also be viewed as a business assets source. The

chosen Australian companies whose financial report is to be analyzed are Woolworths,

Wesfarmers, JB Hi-Fi and Met cash.

Analysis of items of equity of Woolworths:

The amount of contributed equity stood at $ (million) 6055 in year 2018 compared to $

5615, $ 5252 and 5064.9 in year 2017, 2016 and 2015 respectively. From the figures, it can be

said that the value of equity has risen since year 2015. The reserves are recorded at $ 353, $ 357

in year 2018 and 2017 compared to $ 93.9 and 95.1 in year 2016 and 2015. It can be suggested

that the reserves has increased (Johnston and Petacchi 2017). Furthermore, retained earnings are

recorded at $ 4073, $ 3554, $ 3124.5 and $ 5831.0 in year 2018, 2017, 2016 and 2015

respectively.

Analysis of each items of equity of Met cash:

For Met cash, the amount of contributed and other equity is recorded at $ 600 in year

2018 as against $ 1719.3, $ 1626, $ 2391.9 in year 2017, 2016 and 2015. As per the abnual

report the amounts of value of equity decreased in year 2018. Analyzing the amounts of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPANY AND FINANCIAL REPORTING

retained earnings, it represents that value has increased to $ 780.6 in year 2018 as against

accumulated loss of $ 87.7 in year 2017, $ 184.7 and $ 765.9 in year 2017, 2016 and 2015

respectively (Tschopp and Huefner 2015). Amount of reserves for year 2018 stood at $ 0.7

compared to $ 3.0 in year 2017 and $ 4.1 in year 2016 and 2015.

Analysis of items of equity of Wesfarmers:

For year ending 2018 and 2017, issued capital is reported at $ 22277 million and $ 22268

million compared to $ 21937 and $ 21844 in year 2016 and 2015 respectively. There has been

constant rise in value of issued capital. Value of retained earnings is recorded at $ 176 for year

2018 compared to $ 1509, $ 874 and $ 2742 for year 2017, 2016 and 2015 respectively (Mardini,

Crawford and Power 2015). The retained earning has reduced initially and has risen and decline

further in the present year. Reserves were at 344, 190, 166 and 226 for year 2018, 2017, 2016

and 2015. The reserves declined and then increased showing that the reserves account has

increased due to rise in profits.

Analysis of each items of equity of JB Hi-Fi:

The equity stood at $ 438.7 and $ 49.3 in year 2017 and 2016 in comparison to $ 565.21

in year 2015. It is showed according the annual report that there is a fall in value of the equity.

Value of reserves is recorded at $ 33.2 and $ 27.1 in year 2017 and 2016 compared to $ 17.63 in

year 2015 respectively indicating a consistent increase in value (Sutherland 2017). Now, looking

at the figures of retained earnings, it can be seen that the amount is recorded at $ 381.6 and $

328.3 in year 2017 and 2016 respectively compared to $ 269.3 in year 2015. The figure suggests

that the value of retained earnings is rising.

retained earnings, it represents that value has increased to $ 780.6 in year 2018 as against

accumulated loss of $ 87.7 in year 2017, $ 184.7 and $ 765.9 in year 2017, 2016 and 2015

respectively (Tschopp and Huefner 2015). Amount of reserves for year 2018 stood at $ 0.7

compared to $ 3.0 in year 2017 and $ 4.1 in year 2016 and 2015.

Analysis of items of equity of Wesfarmers:

For year ending 2018 and 2017, issued capital is reported at $ 22277 million and $ 22268

million compared to $ 21937 and $ 21844 in year 2016 and 2015 respectively. There has been

constant rise in value of issued capital. Value of retained earnings is recorded at $ 176 for year

2018 compared to $ 1509, $ 874 and $ 2742 for year 2017, 2016 and 2015 respectively (Mardini,

Crawford and Power 2015). The retained earning has reduced initially and has risen and decline

further in the present year. Reserves were at 344, 190, 166 and 226 for year 2018, 2017, 2016

and 2015. The reserves declined and then increased showing that the reserves account has

increased due to rise in profits.

Analysis of each items of equity of JB Hi-Fi:

The equity stood at $ 438.7 and $ 49.3 in year 2017 and 2016 in comparison to $ 565.21

in year 2015. It is showed according the annual report that there is a fall in value of the equity.

Value of reserves is recorded at $ 33.2 and $ 27.1 in year 2017 and 2016 compared to $ 17.63 in

year 2015 respectively indicating a consistent increase in value (Sutherland 2017). Now, looking

at the figures of retained earnings, it can be seen that the amount is recorded at $ 381.6 and $

328.3 in year 2017 and 2016 respectively compared to $ 269.3 in year 2015. The figure suggests

that the value of retained earnings is rising.

8COMPANY AND FINANCIAL REPORTING

Comparative analysis of debt and equity of the chosen companies:

The debt to equity ratio, evaluated by dividing the total liabilities of company by its

equity of stockholders, is a debt ratio used to measure a financial leverage of the organization

(Leuz and Wysocki 2016). The debt to equity ratio represents the amount how much debt a

company is using to finance its assets relative to the value of equity of the shareholders.

The total amount of liabilities of Woolworths limited for year ending 2018 and 2017 is

recorded at $ 12709 and $ 13167 compared to total value of equity that is recorded at $ 10849

and $ 9876. It is suggested by the figure that value of equity is less as against total amount of

debt. The amount of total debt for Met Cash is recorded at $ 2330.4 and $ 2294.9 in year 2018

and 2017 compared to $ 2254.2 and $ 2313.3 in year 2016 and 2015 respectively. On other hand,

the value of equity is recorded at $ 1388.6 and $ 1637.4 in year 2018 and 2017 compared to $

1538.4 and $ 1275.2 in year 2016 and 2015 respectively (Perera and Chand 2015). In case of

Wesfarmers limited, the total amount of liabilities is recorded at $ 14179 in year 2018 and 16174

in year 2017 respectively indicating that total amount owed by organization to other has reduced.

Looking at the figures of equity, it can be seen that equity has reduced from $ 23941 in year

2017 to $ 22754 in year 2018 respectively (Kim, Shi and Zhou 2014). For the company of JB

Hi-Fi, the total liabilities amount or debt is recorded at $ 1598.9 and $ 587.6 in year 2017 and

2016 compared to 551.5 in year 2015 respectively. It can be observed from the figures that the

total liabilities amount has increased in year 2017. Total amount of equity on other hand stood at

$ 853.5 in year 2017 compared to $ 404.7 in year 2016 and $ 343.47 in year 2015

respectively).The amounts shows that total value of equity has risen in year 2017.

Comparative analysis of debt and equity of the chosen companies:

The debt to equity ratio, evaluated by dividing the total liabilities of company by its

equity of stockholders, is a debt ratio used to measure a financial leverage of the organization

(Leuz and Wysocki 2016). The debt to equity ratio represents the amount how much debt a

company is using to finance its assets relative to the value of equity of the shareholders.

The total amount of liabilities of Woolworths limited for year ending 2018 and 2017 is

recorded at $ 12709 and $ 13167 compared to total value of equity that is recorded at $ 10849

and $ 9876. It is suggested by the figure that value of equity is less as against total amount of

debt. The amount of total debt for Met Cash is recorded at $ 2330.4 and $ 2294.9 in year 2018

and 2017 compared to $ 2254.2 and $ 2313.3 in year 2016 and 2015 respectively. On other hand,

the value of equity is recorded at $ 1388.6 and $ 1637.4 in year 2018 and 2017 compared to $

1538.4 and $ 1275.2 in year 2016 and 2015 respectively (Perera and Chand 2015). In case of

Wesfarmers limited, the total amount of liabilities is recorded at $ 14179 in year 2018 and 16174

in year 2017 respectively indicating that total amount owed by organization to other has reduced.

Looking at the figures of equity, it can be seen that equity has reduced from $ 23941 in year

2017 to $ 22754 in year 2018 respectively (Kim, Shi and Zhou 2014). For the company of JB

Hi-Fi, the total liabilities amount or debt is recorded at $ 1598.9 and $ 587.6 in year 2017 and

2016 compared to 551.5 in year 2015 respectively. It can be observed from the figures that the

total liabilities amount has increased in year 2017. Total amount of equity on other hand stood at

$ 853.5 in year 2017 compared to $ 404.7 in year 2016 and $ 343.47 in year 2015

respectively).The amounts shows that total value of equity has risen in year 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPANY AND FINANCIAL REPORTING

Conclusion

The primary purpose of the study is to understand the nature and purpose of the financial

reporting of the Australian companies under the guidance of the AASB framework. The chosen

Australian companies whose financial report is to be analyzed are Woolworths, Wesfarmers, JB

Hi-Fi and Met cash. From the figures of all the four companies, it can be observed that JB Hi-Fi

has less amount of total debt followed by Woolworths compared to Wesfarmers and Met Cash.

For the figures of equities, it can be seen that the value of equity of Wesfarmers is more than all

other firms.

Conclusion

The primary purpose of the study is to understand the nature and purpose of the financial

reporting of the Australian companies under the guidance of the AASB framework. The chosen

Australian companies whose financial report is to be analyzed are Woolworths, Wesfarmers, JB

Hi-Fi and Met cash. From the figures of all the four companies, it can be observed that JB Hi-Fi

has less amount of total debt followed by Woolworths compared to Wesfarmers and Met Cash.

For the figures of equities, it can be seen that the value of equity of Wesfarmers is more than all

other firms.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPANY AND FINANCIAL REPORTING

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research, 54(2), pp.277-340.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Coleman, S., Cotei, C. and Farhat, J., 2016. The debt-equity financing decisions of US startup

firms. Journal of Economics and Finance, 40(1), pp.105-126.

De George, E.T., Li, X. and Shivakumar, L., 2016. A review of the IFRS adoption

literature. Review of Accounting Studies, 21(3), pp.898-1004.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

References

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Acharya, V.V. and Ryan, S.G., 2016. Banks’ financial reporting and financial system

stability. Journal of Accounting Research, 54(2), pp.277-340.

Capkun, V., Collins, D. and Jeanjean, T., 2016. The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting and

Public Policy, 35(4), pp.352-394.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

Coleman, S., Cotei, C. and Farhat, J., 2016. The debt-equity financing decisions of US startup

firms. Journal of Economics and Finance, 40(1), pp.105-126.

De George, E.T., Li, X. and Shivakumar, L., 2016. A review of the IFRS adoption

literature. Review of Accounting Studies, 21(3), pp.898-1004.

Hoskin, R.E., Fizzell, M.R. and Cherry, D.C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Jin, K., Shan, Y. and Taylor, S., 2015. Matching between revenues and expenses and the

adoption of International Financial Reporting Standards. Pacific-Basin Finance Journal, 35,

pp.90-107.

11COMPANY AND FINANCIAL REPORTING

Johnston, R. and Petacchi, R., 2017. Regulatory oversight of financial reporting: Securities and

Exchange Commission comment letters. Contemporary Accounting Research, 34(2), pp.1128-

1155.

Kim, J.B., Shi, H. and Zhou, J., 2014. International Financial Reporting Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of Quantitative

Finance and Accounting, 42(3), pp.469-507.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

Mardini, G.H., Crawford, L. and Power, D.M., 2015. Perceptions of external auditors, preparers

and users of financial statements about the adoption of IFRS 8: Evidence from Jordan. Journal of

Applied Accounting Research, 16(1), pp.2-27.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

accounting, 31(1), pp.165-178.

Sutherland, D.W., 2017. Independent audit report. Newsmonth, 37(3), p.19.

Tschopp, D. and Huefner, R.J., 2015. Comparing the Evolution of CSR Reporting to that of

Financial Reporting. Journal of Business Ethics, 127(3), pp.565-577.

Johnston, R. and Petacchi, R., 2017. Regulatory oversight of financial reporting: Securities and

Exchange Commission comment letters. Contemporary Accounting Research, 34(2), pp.1128-

1155.

Kim, J.B., Shi, H. and Zhou, J., 2014. International Financial Reporting Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of Quantitative

Finance and Accounting, 42(3), pp.469-507.

Leuz, C. and Wysocki, P.D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research, 54(2),

pp.525-622.

Mardini, G.H., Crawford, L. and Power, D.M., 2015. Perceptions of external auditors, preparers

and users of financial statements about the adoption of IFRS 8: Evidence from Jordan. Journal of

Applied Accounting Research, 16(1), pp.2-27.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

accounting, 31(1), pp.165-178.

Sutherland, D.W., 2017. Independent audit report. Newsmonth, 37(3), p.19.

Tschopp, D. and Huefner, R.J., 2015. Comparing the Evolution of CSR Reporting to that of

Financial Reporting. Journal of Business Ethics, 127(3), pp.565-577.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.