Comprehensive Financial Performance Analysis of A2 Milk Company

VerifiedAdded on 2023/02/01

|15

|4502

|48

Report

AI Summary

This report offers a comprehensive financial analysis of the A2 Milk Company for investment purposes. It evaluates the company's performance using profitability and efficiency ratios, revealing a strong financial position. The report also examines cash management, identifies marketable securities, and performs a sensitivity analysis to assess project feasibility. It identifies both systemic and unsystemic risks and notes the company's dividend policy. The analysis covers gross margin, net margin, ROCE, days inventory turnover, and cash conversion cycle. The conclusion recommends project acceptance based on the positive findings. The report also highlights the importance of effective cash management and the potential impact of a large cash balance on the company's strategic options. The report concludes with a recommendation letter and a conclusion summarizing the key findings.

Running head: COMPANY PERFORMANCE ANALYSIS

Company Performance Analysis

Name of the Student

Name of the University

Author’s Note

Company Performance Analysis

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2COMPANY PERFORMANCE ANALYSIS

Abstract

This report aims at the analysis of the financial performance of the A2 Milk Company for

the investment purpose. The findings of the report show the strong profitability and

efficiency position of the company. The cash management position of the company is

also good and effective. The findings of the sensitivity analysis states that the proposed

project should be accepted since it will be profitable. There are both systemic and un-

systemic risks in A2 Milk Company. Due to not paying dividend, the dividend payout

ratio of the company for the last three years is nil.

Abstract

This report aims at the analysis of the financial performance of the A2 Milk Company for

the investment purpose. The findings of the report show the strong profitability and

efficiency position of the company. The cash management position of the company is

also good and effective. The findings of the sensitivity analysis states that the proposed

project should be accepted since it will be profitable. There are both systemic and un-

systemic risks in A2 Milk Company. Due to not paying dividend, the dividend payout

ratio of the company for the last three years is nil.

3COMPANY PERFORMANCE ANALYSIS

Table of Contents

I. Introduction..............................................................................................................................................4

II. Financial Analysis of A2 Milk....................................................................................................................4

2.1 Company Description........................................................................................................................4

2.2 Calculation and Analysis of Performance Ratios................................................................................4

2.3 Identification of Marketable Securities..............................................................................................8

2.4 Sensitivity Analysis.............................................................................................................................8

2.5 Systemic and Un-systemic Risks......................................................................................................11

2.6 Dividend Payout Ratio and Dividend Policy.....................................................................................12

III. Recommendation Letter.......................................................................................................................12

IV. Conclusion............................................................................................................................................13

References.................................................................................................................................................14

Table of Contents

I. Introduction..............................................................................................................................................4

II. Financial Analysis of A2 Milk....................................................................................................................4

2.1 Company Description........................................................................................................................4

2.2 Calculation and Analysis of Performance Ratios................................................................................4

2.3 Identification of Marketable Securities..............................................................................................8

2.4 Sensitivity Analysis.............................................................................................................................8

2.5 Systemic and Un-systemic Risks......................................................................................................11

2.6 Dividend Payout Ratio and Dividend Policy.....................................................................................12

III. Recommendation Letter.......................................................................................................................12

IV. Conclusion............................................................................................................................................13

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4COMPANY PERFORMANCE ANALYSIS

I. Introduction

Analysis of the financial performance of the companies is considered as a crucial

tool to measure the current financial performance and to get an idea about the

company’s future performance as well (Delen, Kuzey and Uyar 2013). For the same

reason, investment analysts consider analyzing financial performance of the firms as a

crucial part of the investment decision-making process. The use of certain tools and

techniques can be seen for this purpose such as ratio analysis of the selected company,

sensitivity analysis and others. Certain other aspects need to be considered are the

analysis of the risks of the companies, marketable securities and many others (Amit and

Villalonga 2014). The aim of this report is the analysis of the financial performance of an

ASX listed company for the purpose of investment decision-making. The considered

ASX listed company is A2 Milk Company. The whole report is divided into certain

sections. The first section involves the description of the selected company. The second

part involves in calculating as well as analyzing certain profitability as well as efficiency

ratios of A2 Milk for explaining the trend of these financial ratios. The next part

undertakes cash management analysis through the identification of marketable

securities. The next part involves in performing a sensitivity analysis for the

determination of the project. Identification of the systemic and unsystematic risk is the

aim of the next section. The next part identifies the dividend payout ratio along with the

dividend policy. The report ends with a recommendation letter and a conclusion.

II. Financial Analysis of A2 Milk

2.1 Company Description

A2 Milk is a public listed Australian company involves in the commercialization of

intellectual property relating to A1 protein-free milk that the company sells under A2 and

A2 milk brands along with other mil related products. The company was established in

the year 2000 and it is headquartered at Sydney, Australia. A2 Milk Company operates

in the Australian dairy industry which is considered as a strong and well-established

market for the companies under this industry (thea2milkcompany.com 2019). A2 Milk

Company is regarded as the successor of the A2 Corporation Limited. A2 Corporation

sold its interest to A2 Australia which is considered as the inception of the A2 Milk

Company. Since A2 Milk Company operates in the milk and dairy industry in Australia,

the company has to face major competition in some of its key competitors such as

Bellamy’s Australia, Bega Cheese, Freedom Foods Group and Inghams Group

(thea2milkcompany.com 2019).

2.2 Calculation and Analysis of Performance Ratios

Analysis of profitability and operating efficiency can be considered as two crucial

aspects for ascertaining the current financial standing and performance of A2 Milk

Company. The following discussion shows the analysis of certain ratios under

profitability and operating efficiency of A2 Milk Company.

Analysis of Profitability

The analysis of the profitability ratio is done with the aim to ascertain the ability of

the company to generate income against all the expenses that need to incur to conduct

I. Introduction

Analysis of the financial performance of the companies is considered as a crucial

tool to measure the current financial performance and to get an idea about the

company’s future performance as well (Delen, Kuzey and Uyar 2013). For the same

reason, investment analysts consider analyzing financial performance of the firms as a

crucial part of the investment decision-making process. The use of certain tools and

techniques can be seen for this purpose such as ratio analysis of the selected company,

sensitivity analysis and others. Certain other aspects need to be considered are the

analysis of the risks of the companies, marketable securities and many others (Amit and

Villalonga 2014). The aim of this report is the analysis of the financial performance of an

ASX listed company for the purpose of investment decision-making. The considered

ASX listed company is A2 Milk Company. The whole report is divided into certain

sections. The first section involves the description of the selected company. The second

part involves in calculating as well as analyzing certain profitability as well as efficiency

ratios of A2 Milk for explaining the trend of these financial ratios. The next part

undertakes cash management analysis through the identification of marketable

securities. The next part involves in performing a sensitivity analysis for the

determination of the project. Identification of the systemic and unsystematic risk is the

aim of the next section. The next part identifies the dividend payout ratio along with the

dividend policy. The report ends with a recommendation letter and a conclusion.

II. Financial Analysis of A2 Milk

2.1 Company Description

A2 Milk is a public listed Australian company involves in the commercialization of

intellectual property relating to A1 protein-free milk that the company sells under A2 and

A2 milk brands along with other mil related products. The company was established in

the year 2000 and it is headquartered at Sydney, Australia. A2 Milk Company operates

in the Australian dairy industry which is considered as a strong and well-established

market for the companies under this industry (thea2milkcompany.com 2019). A2 Milk

Company is regarded as the successor of the A2 Corporation Limited. A2 Corporation

sold its interest to A2 Australia which is considered as the inception of the A2 Milk

Company. Since A2 Milk Company operates in the milk and dairy industry in Australia,

the company has to face major competition in some of its key competitors such as

Bellamy’s Australia, Bega Cheese, Freedom Foods Group and Inghams Group

(thea2milkcompany.com 2019).

2.2 Calculation and Analysis of Performance Ratios

Analysis of profitability and operating efficiency can be considered as two crucial

aspects for ascertaining the current financial standing and performance of A2 Milk

Company. The following discussion shows the analysis of certain ratios under

profitability and operating efficiency of A2 Milk Company.

Analysis of Profitability

The analysis of the profitability ratio is done with the aim to ascertain the ability of

the company to generate income against all the expenses that need to incur to conduct

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5COMPANY PERFORMANCE ANALYSIS

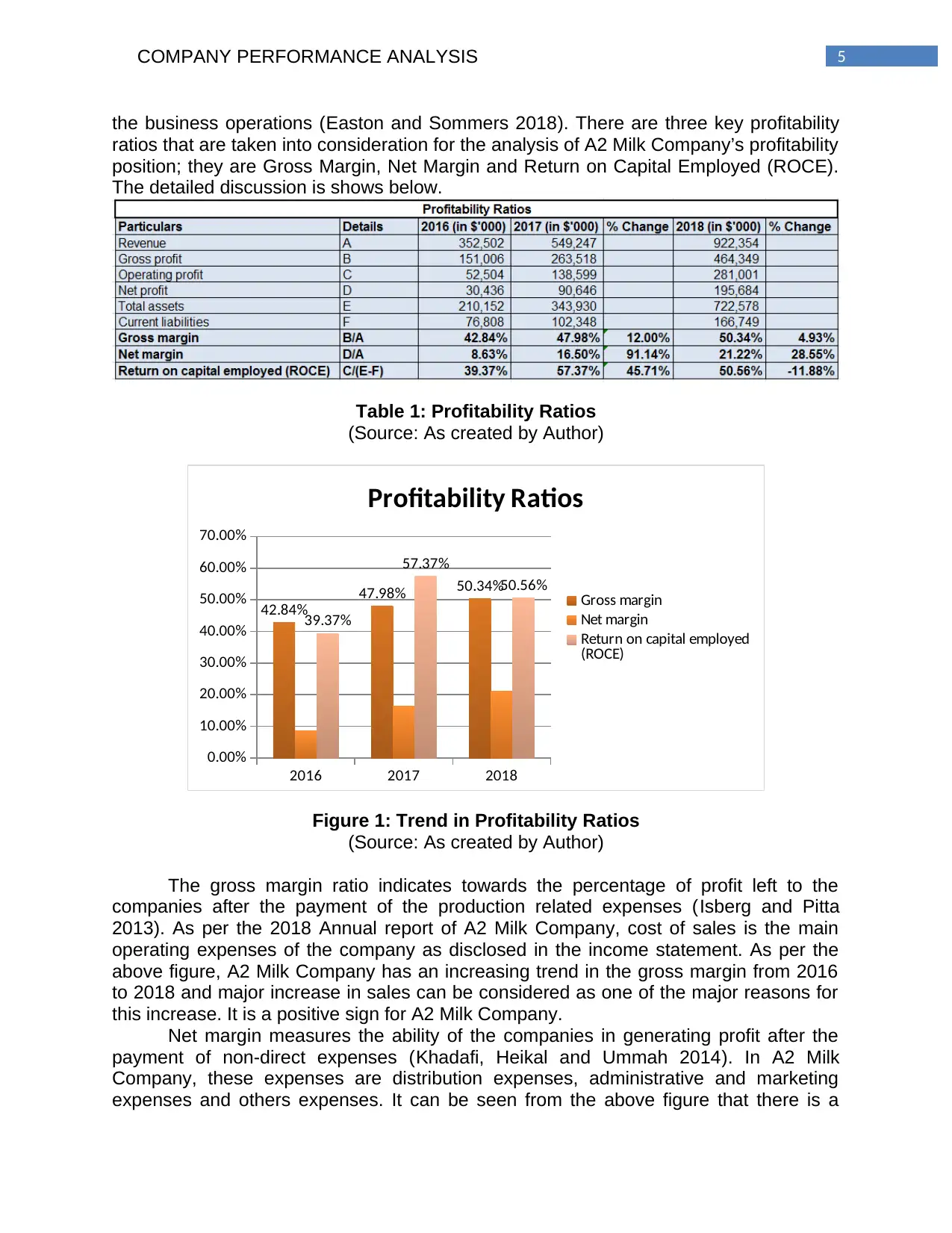

the business operations (Easton and Sommers 2018). There are three key profitability

ratios that are taken into consideration for the analysis of A2 Milk Company’s profitability

position; they are Gross Margin, Net Margin and Return on Capital Employed (ROCE).

The detailed discussion is shows below.

Table 1: Profitability Ratios

(Source: As created by Author)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

42.84%

47.98% 50.34%

39.37%

57.37%

50.56%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Trend in Profitability Ratios

(Source: As created by Author)

The gross margin ratio indicates towards the percentage of profit left to the

companies after the payment of the production related expenses (Isberg and Pitta

2013). As per the 2018 Annual report of A2 Milk Company, cost of sales is the main

operating expenses of the company as disclosed in the income statement. As per the

above figure, A2 Milk Company has an increasing trend in the gross margin from 2016

to 2018 and major increase in sales can be considered as one of the major reasons for

this increase. It is a positive sign for A2 Milk Company.

Net margin measures the ability of the companies in generating profit after the

payment of non-direct expenses (Khadafi, Heikal and Ummah 2014). In A2 Milk

Company, these expenses are distribution expenses, administrative and marketing

expenses and others expenses. It can be seen from the above figure that there is a

the business operations (Easton and Sommers 2018). There are three key profitability

ratios that are taken into consideration for the analysis of A2 Milk Company’s profitability

position; they are Gross Margin, Net Margin and Return on Capital Employed (ROCE).

The detailed discussion is shows below.

Table 1: Profitability Ratios

(Source: As created by Author)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

42.84%

47.98% 50.34%

39.37%

57.37%

50.56%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Trend in Profitability Ratios

(Source: As created by Author)

The gross margin ratio indicates towards the percentage of profit left to the

companies after the payment of the production related expenses (Isberg and Pitta

2013). As per the 2018 Annual report of A2 Milk Company, cost of sales is the main

operating expenses of the company as disclosed in the income statement. As per the

above figure, A2 Milk Company has an increasing trend in the gross margin from 2016

to 2018 and major increase in sales can be considered as one of the major reasons for

this increase. It is a positive sign for A2 Milk Company.

Net margin measures the ability of the companies in generating profit after the

payment of non-direct expenses (Khadafi, Heikal and Ummah 2014). In A2 Milk

Company, these expenses are distribution expenses, administrative and marketing

expenses and others expenses. It can be seen from the above figure that there is a

6COMPANY PERFORMANCE ANALYSIS

healthy increase in the net margin of A2 Milk Company from 2016 to 2018 which can be

considered as a positive indicator of the company’s profitability. Reduction in some of

the major expenses like marketing expenses and increase in interest income can be

considered as the key reasons for this increase.

ROCE measures the ability of the companies in generating profit from the capital

employed through the comparison of net operating profit to the capital employed ( San

and Heng 2013). As per the above figure, there is a healthy increase in ROCE in 2017

from 2016 due to the massive increase in operating profit. However, decease in this

ratio can be seen in 2018 from 2017 and excess increase in current liabilities can be

considered as the prime reason for this.

It needs to be mentioned based on the above discussion that A2 Milk Company

has an effective profitability position owing to the massive increase in both the gross

margin and net profit. However, the companies is needed to develop strategies for

improvising heir ROCE in the coming years since it is considered as a crucial indicator

of company’s profitability.

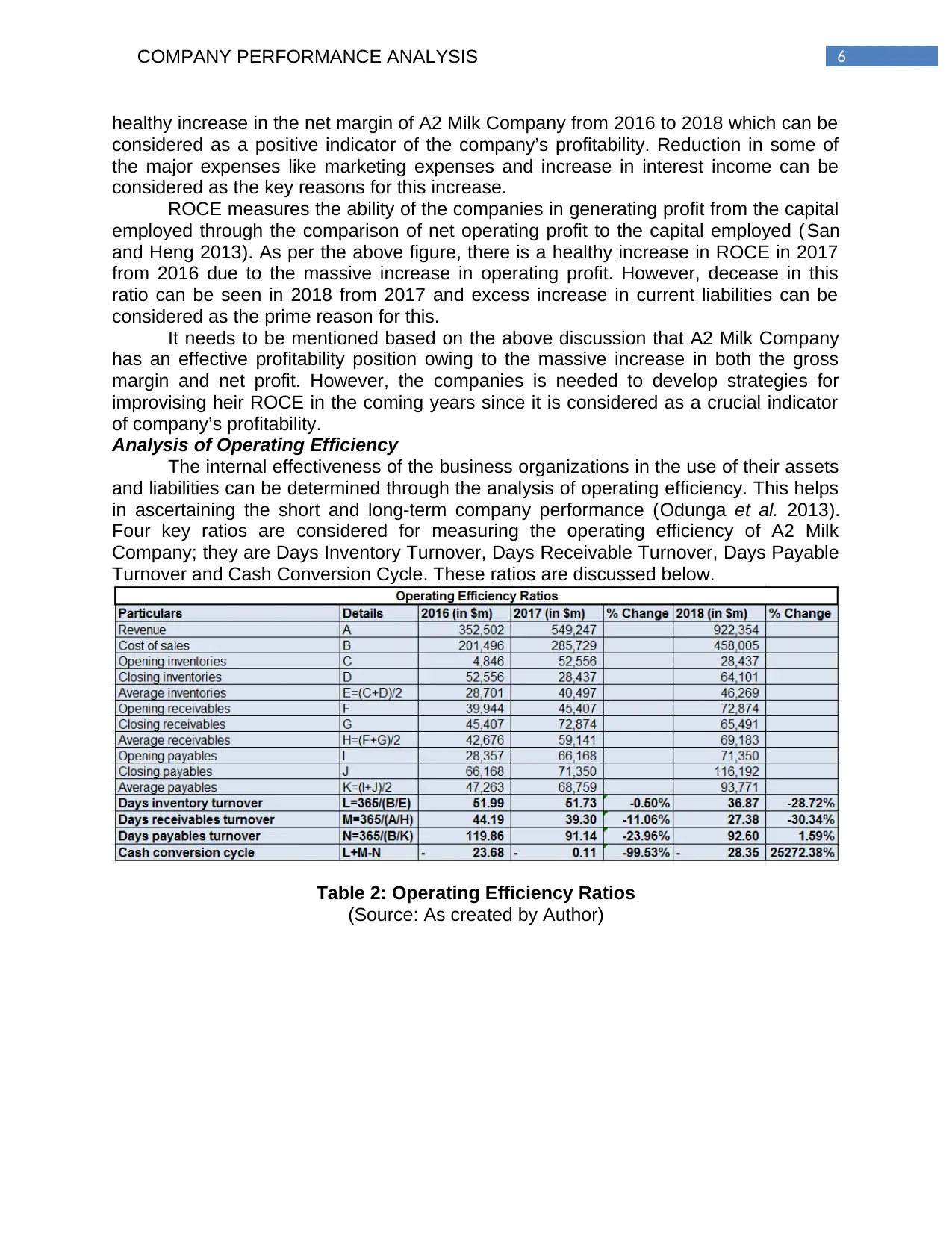

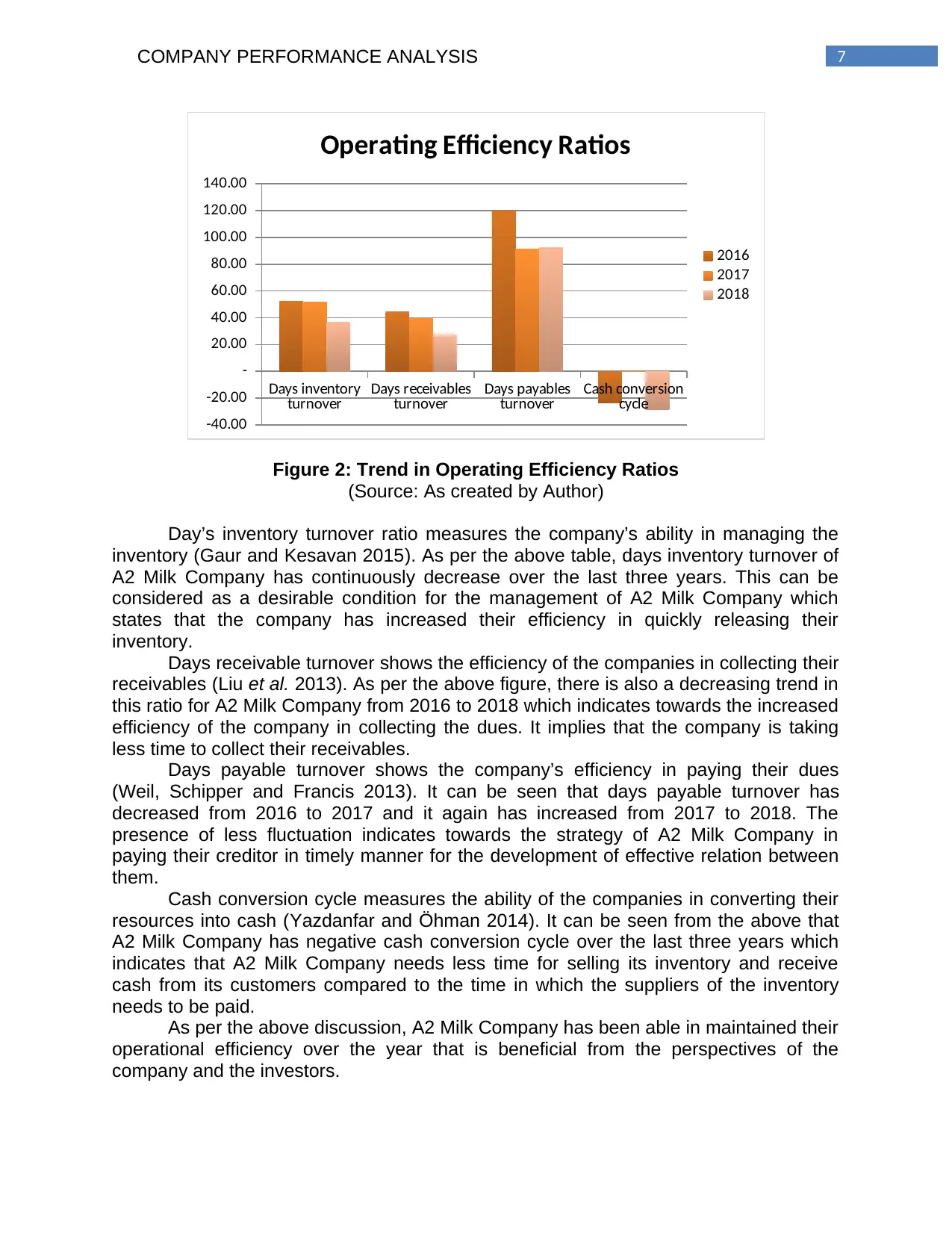

Analysis of Operating Efficiency

The internal effectiveness of the business organizations in the use of their assets

and liabilities can be determined through the analysis of operating efficiency. This helps

in ascertaining the short and long-term company performance (Odunga et al. 2013).

Four key ratios are considered for measuring the operating efficiency of A2 Milk

Company; they are Days Inventory Turnover, Days Receivable Turnover, Days Payable

Turnover and Cash Conversion Cycle. These ratios are discussed below.

Table 2: Operating Efficiency Ratios

(Source: As created by Author)

healthy increase in the net margin of A2 Milk Company from 2016 to 2018 which can be

considered as a positive indicator of the company’s profitability. Reduction in some of

the major expenses like marketing expenses and increase in interest income can be

considered as the key reasons for this increase.

ROCE measures the ability of the companies in generating profit from the capital

employed through the comparison of net operating profit to the capital employed ( San

and Heng 2013). As per the above figure, there is a healthy increase in ROCE in 2017

from 2016 due to the massive increase in operating profit. However, decease in this

ratio can be seen in 2018 from 2017 and excess increase in current liabilities can be

considered as the prime reason for this.

It needs to be mentioned based on the above discussion that A2 Milk Company

has an effective profitability position owing to the massive increase in both the gross

margin and net profit. However, the companies is needed to develop strategies for

improvising heir ROCE in the coming years since it is considered as a crucial indicator

of company’s profitability.

Analysis of Operating Efficiency

The internal effectiveness of the business organizations in the use of their assets

and liabilities can be determined through the analysis of operating efficiency. This helps

in ascertaining the short and long-term company performance (Odunga et al. 2013).

Four key ratios are considered for measuring the operating efficiency of A2 Milk

Company; they are Days Inventory Turnover, Days Receivable Turnover, Days Payable

Turnover and Cash Conversion Cycle. These ratios are discussed below.

Table 2: Operating Efficiency Ratios

(Source: As created by Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7COMPANY PERFORMANCE ANALYSIS

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-40.00

-20.00

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Trend in Operating Efficiency Ratios

(Source: As created by Author)

Day’s inventory turnover ratio measures the company’s ability in managing the

inventory (Gaur and Kesavan 2015). As per the above table, days inventory turnover of

A2 Milk Company has continuously decrease over the last three years. This can be

considered as a desirable condition for the management of A2 Milk Company which

states that the company has increased their efficiency in quickly releasing their

inventory.

Days receivable turnover shows the efficiency of the companies in collecting their

receivables (Liu et al. 2013). As per the above figure, there is also a decreasing trend in

this ratio for A2 Milk Company from 2016 to 2018 which indicates towards the increased

efficiency of the company in collecting the dues. It implies that the company is taking

less time to collect their receivables.

Days payable turnover shows the company’s efficiency in paying their dues

(Weil, Schipper and Francis 2013). It can be seen that days payable turnover has

decreased from 2016 to 2017 and it again has increased from 2017 to 2018. The

presence of less fluctuation indicates towards the strategy of A2 Milk Company in

paying their creditor in timely manner for the development of effective relation between

them.

Cash conversion cycle measures the ability of the companies in converting their

resources into cash (Yazdanfar and Öhman 2014). It can be seen from the above that

A2 Milk Company has negative cash conversion cycle over the last three years which

indicates that A2 Milk Company needs less time for selling its inventory and receive

cash from its customers compared to the time in which the suppliers of the inventory

needs to be paid.

As per the above discussion, A2 Milk Company has been able in maintained their

operational efficiency over the year that is beneficial from the perspectives of the

company and the investors.

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-40.00

-20.00

-

20.00

40.00

60.00

80.00

100.00

120.00

140.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Trend in Operating Efficiency Ratios

(Source: As created by Author)

Day’s inventory turnover ratio measures the company’s ability in managing the

inventory (Gaur and Kesavan 2015). As per the above table, days inventory turnover of

A2 Milk Company has continuously decrease over the last three years. This can be

considered as a desirable condition for the management of A2 Milk Company which

states that the company has increased their efficiency in quickly releasing their

inventory.

Days receivable turnover shows the efficiency of the companies in collecting their

receivables (Liu et al. 2013). As per the above figure, there is also a decreasing trend in

this ratio for A2 Milk Company from 2016 to 2018 which indicates towards the increased

efficiency of the company in collecting the dues. It implies that the company is taking

less time to collect their receivables.

Days payable turnover shows the company’s efficiency in paying their dues

(Weil, Schipper and Francis 2013). It can be seen that days payable turnover has

decreased from 2016 to 2017 and it again has increased from 2017 to 2018. The

presence of less fluctuation indicates towards the strategy of A2 Milk Company in

paying their creditor in timely manner for the development of effective relation between

them.

Cash conversion cycle measures the ability of the companies in converting their

resources into cash (Yazdanfar and Öhman 2014). It can be seen from the above that

A2 Milk Company has negative cash conversion cycle over the last three years which

indicates that A2 Milk Company needs less time for selling its inventory and receive

cash from its customers compared to the time in which the suppliers of the inventory

needs to be paid.

As per the above discussion, A2 Milk Company has been able in maintained their

operational efficiency over the year that is beneficial from the perspectives of the

company and the investors.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8COMPANY PERFORMANCE ANALYSIS

2.3 Identification of Marketable Securities

Marketable securities in the current assets are considered as the type of liquid

assets on the balance sheet that can be easily converted into cash (Brown 2014).

According to the 2018 Annual Report of A2 Milk Company, cash in hand and cash in

bank and short term deposits can be considered as the marketable deposit of the

company which values $340,455,000 in 2018 and $121,020,000 in 2017

(thea2milkcompany.com 2019). It can be seen that there is significant increase in cash

and other short-term deposits of A2 Milk Company in 2018 as compared to 2017.

It needs to be mentioned that the companies use these instruments in order to

earn return on case and the same aspect can be seen in A2 Milk Company. As per Note

D3 of the Financial Statements of A2 Milk Company, the company earns interest on

floating rates on the basis of daily bank deposit rates. It implies that these securities

works as source of cash for the company which is needed for sound cash management

(Brown 2014). The importance of effective cash management mechanism cannot be

ignored for the companies. Increase in the amount of these marketable securities in the

balance sheet reflects the strategy of A2 Milk Company to enhance the cash collection

for strengthens their liquidity position and it is a crucial aspect for cash management. In

addition, the maintenance of this suffificnet cash balance provides A2 Milk Company the

scope to fight economic downturns along with the financial stability to make investments

in the presence of suitable price. Large corporate investors can make A2 Milk Company

suitable takeover target in the presence of this large cash balance which can be used in

different productive manners (Kuttner and Shim 2016).

2.4 Sensitivity Analysis

This section considers a situation where a project is considered by A2 Milk

Company for a new product. Two different scenarios have taken into account for this;

that are the normal scenario and sensitivity analysis with the same value drivers in the

presence of certain changes.

Normal Scenario

2.3 Identification of Marketable Securities

Marketable securities in the current assets are considered as the type of liquid

assets on the balance sheet that can be easily converted into cash (Brown 2014).

According to the 2018 Annual Report of A2 Milk Company, cash in hand and cash in

bank and short term deposits can be considered as the marketable deposit of the

company which values $340,455,000 in 2018 and $121,020,000 in 2017

(thea2milkcompany.com 2019). It can be seen that there is significant increase in cash

and other short-term deposits of A2 Milk Company in 2018 as compared to 2017.

It needs to be mentioned that the companies use these instruments in order to

earn return on case and the same aspect can be seen in A2 Milk Company. As per Note

D3 of the Financial Statements of A2 Milk Company, the company earns interest on

floating rates on the basis of daily bank deposit rates. It implies that these securities

works as source of cash for the company which is needed for sound cash management

(Brown 2014). The importance of effective cash management mechanism cannot be

ignored for the companies. Increase in the amount of these marketable securities in the

balance sheet reflects the strategy of A2 Milk Company to enhance the cash collection

for strengthens their liquidity position and it is a crucial aspect for cash management. In

addition, the maintenance of this suffificnet cash balance provides A2 Milk Company the

scope to fight economic downturns along with the financial stability to make investments

in the presence of suitable price. Large corporate investors can make A2 Milk Company

suitable takeover target in the presence of this large cash balance which can be used in

different productive manners (Kuttner and Shim 2016).

2.4 Sensitivity Analysis

This section considers a situation where a project is considered by A2 Milk

Company for a new product. Two different scenarios have taken into account for this;

that are the normal scenario and sensitivity analysis with the same value drivers in the

presence of certain changes.

Normal Scenario

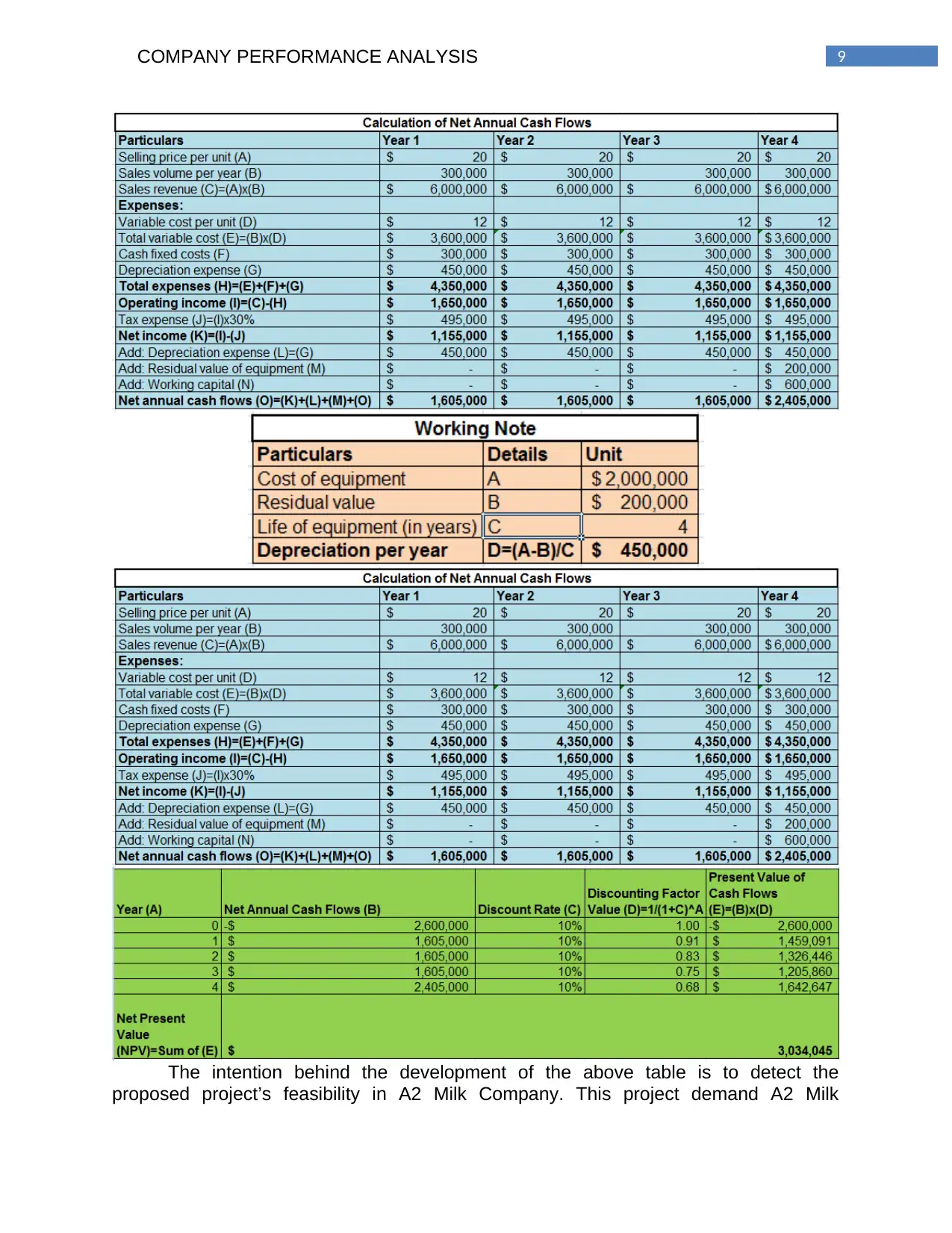

9COMPANY PERFORMANCE ANALYSIS

The intention behind the development of the above table is to detect the

proposed project’s feasibility in A2 Milk Company. This project demand A2 Milk

The intention behind the development of the above table is to detect the

proposed project’s feasibility in A2 Milk Company. This project demand A2 Milk

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10COMPANY PERFORMANCE ANALYSIS

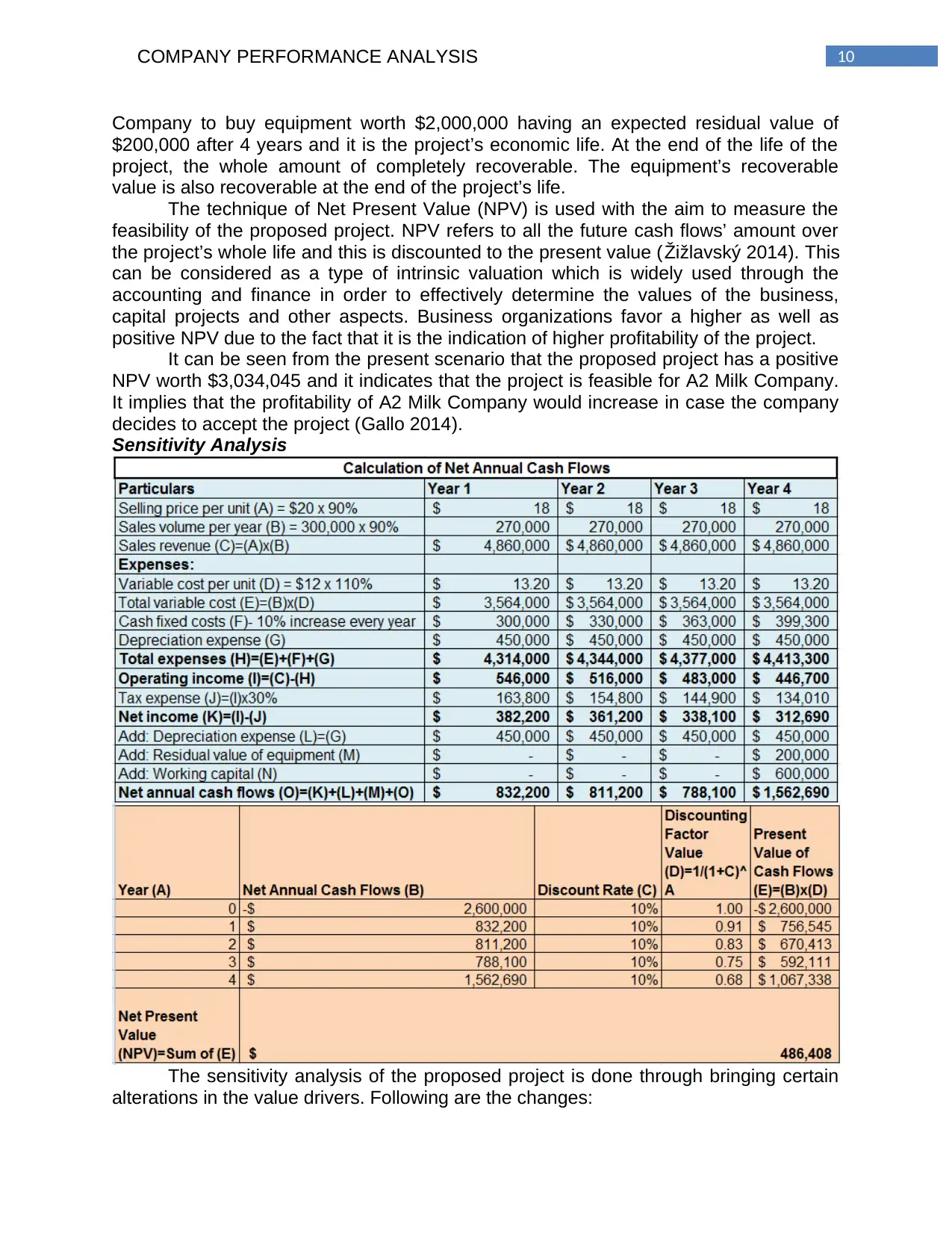

Company to buy equipment worth $2,000,000 having an expected residual value of

$200,000 after 4 years and it is the project’s economic life. At the end of the life of the

project, the whole amount of completely recoverable. The equipment’s recoverable

value is also recoverable at the end of the project’s life.

The technique of Net Present Value (NPV) is used with the aim to measure the

feasibility of the proposed project. NPV refers to all the future cash flows’ amount over

the project’s whole life and this is discounted to the present value (Žižlavský 2014). This

can be considered as a type of intrinsic valuation which is widely used through the

accounting and finance in order to effectively determine the values of the business,

capital projects and other aspects. Business organizations favor a higher as well as

positive NPV due to the fact that it is the indication of higher profitability of the project.

It can be seen from the present scenario that the proposed project has a positive

NPV worth $3,034,045 and it indicates that the project is feasible for A2 Milk Company.

It implies that the profitability of A2 Milk Company would increase in case the company

decides to accept the project (Gallo 2014).

Sensitivity Analysis

The sensitivity analysis of the proposed project is done through bringing certain

alterations in the value drivers. Following are the changes:

Company to buy equipment worth $2,000,000 having an expected residual value of

$200,000 after 4 years and it is the project’s economic life. At the end of the life of the

project, the whole amount of completely recoverable. The equipment’s recoverable

value is also recoverable at the end of the project’s life.

The technique of Net Present Value (NPV) is used with the aim to measure the

feasibility of the proposed project. NPV refers to all the future cash flows’ amount over

the project’s whole life and this is discounted to the present value (Žižlavský 2014). This

can be considered as a type of intrinsic valuation which is widely used through the

accounting and finance in order to effectively determine the values of the business,

capital projects and other aspects. Business organizations favor a higher as well as

positive NPV due to the fact that it is the indication of higher profitability of the project.

It can be seen from the present scenario that the proposed project has a positive

NPV worth $3,034,045 and it indicates that the project is feasible for A2 Milk Company.

It implies that the profitability of A2 Milk Company would increase in case the company

decides to accept the project (Gallo 2014).

Sensitivity Analysis

The sensitivity analysis of the proposed project is done through bringing certain

alterations in the value drivers. Following are the changes:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11COMPANY PERFORMANCE ANALYSIS

o 10% decrease in the unit sales

o 10% decrease in per unit

o 10% increase in the variable cost per unit

o 10% increase in the cash fixed cost per year

This revised situation also involved the application of the technique of NPV. It can be

observed that the proposed project’s NPV as per the computation is $486,408 and this

value is lower than the actual situation. The main reasons behind this decrease are the

decline in sales volume and sales price per unit along with the increase in the fixed as

well as variable expenses (French 2014). However, the NPV of the project still can be

seen as positive in spite of the fall in the sales performance. This aspect indicates

towards the crucial fact that the proposed project is still profitable for A2 Milk Company

in the presence of positive NPV in spite of the decrease in revenue and increase in

costs. To infer, it can be concluded that the project still has the feasibility for A2 Milk

Company for maximizing the overall return on investment (Iooss and Lemaître 2015).

2.5 Systemic and Un-systemic Risks

Systemic risk arises due to the changes in macroeconomic factors like inflation,

interest rate changes and others (Brunnermeier and Oehmke 2013). Below are the

systemic risks in A2 Milk Company:

Foreign Currency Risk – The operations of A2 Milk Company are exposed to the

foreign currency risk that arises due to the movements in the currencies of the countries

like the US, the UK and Chine against the currencies of Australia and New Zealand. A2

Milk Company does not adopt any hedging strategy, but they may transfer the cash

balances on timely basis between currencies for the reduction of exposure

(thea2milkcompany.com 2019).

Equity Price Risk – A2 Milk Company is exposed to this particular risk on the listed

investments that are classified as well as measured at fair value through other

comprehensive income. The company does not hedge this risk. The management of A2

Milk Company monitors this particular risk exposure through the comparison of the

movement in the quoted share price of the long-term investments (Acemoglu, Ozdaglar

and Tahbaz-Salehi 2015).

The association of un-systemic risk can be only being seen with the specific

industry and these risks of A2 Milk Company are shown below:

Product Quality – A2 Milk Company is exposed to this risk as their products may

become polluted, tampered with, adulterated or unsafe consumption. These aspects

could lead to the harm or injury to the customers (thea2milkcompany.com 2019).

Supply Chain – The ability of the company to maintain the supply of their products can

be hampered in case there is material and adverse change in the operation of one or

more suppliers and reduction in the support from one of more suppliers.

Increase in Competition – Since A2 Milk Company operates in a highly competitive

industry, increase in competition can hamper the operation of the company, specifically

is sales and other revenue bases. These are the major un-systemic risk in the

operations of A2 Milk Company (Decisions 2015).

o 10% decrease in the unit sales

o 10% decrease in per unit

o 10% increase in the variable cost per unit

o 10% increase in the cash fixed cost per year

This revised situation also involved the application of the technique of NPV. It can be

observed that the proposed project’s NPV as per the computation is $486,408 and this

value is lower than the actual situation. The main reasons behind this decrease are the

decline in sales volume and sales price per unit along with the increase in the fixed as

well as variable expenses (French 2014). However, the NPV of the project still can be

seen as positive in spite of the fall in the sales performance. This aspect indicates

towards the crucial fact that the proposed project is still profitable for A2 Milk Company

in the presence of positive NPV in spite of the decrease in revenue and increase in

costs. To infer, it can be concluded that the project still has the feasibility for A2 Milk

Company for maximizing the overall return on investment (Iooss and Lemaître 2015).

2.5 Systemic and Un-systemic Risks

Systemic risk arises due to the changes in macroeconomic factors like inflation,

interest rate changes and others (Brunnermeier and Oehmke 2013). Below are the

systemic risks in A2 Milk Company:

Foreign Currency Risk – The operations of A2 Milk Company are exposed to the

foreign currency risk that arises due to the movements in the currencies of the countries

like the US, the UK and Chine against the currencies of Australia and New Zealand. A2

Milk Company does not adopt any hedging strategy, but they may transfer the cash

balances on timely basis between currencies for the reduction of exposure

(thea2milkcompany.com 2019).

Equity Price Risk – A2 Milk Company is exposed to this particular risk on the listed

investments that are classified as well as measured at fair value through other

comprehensive income. The company does not hedge this risk. The management of A2

Milk Company monitors this particular risk exposure through the comparison of the

movement in the quoted share price of the long-term investments (Acemoglu, Ozdaglar

and Tahbaz-Salehi 2015).

The association of un-systemic risk can be only being seen with the specific

industry and these risks of A2 Milk Company are shown below:

Product Quality – A2 Milk Company is exposed to this risk as their products may

become polluted, tampered with, adulterated or unsafe consumption. These aspects

could lead to the harm or injury to the customers (thea2milkcompany.com 2019).

Supply Chain – The ability of the company to maintain the supply of their products can

be hampered in case there is material and adverse change in the operation of one or

more suppliers and reduction in the support from one of more suppliers.

Increase in Competition – Since A2 Milk Company operates in a highly competitive

industry, increase in competition can hamper the operation of the company, specifically

is sales and other revenue bases. These are the major un-systemic risk in the

operations of A2 Milk Company (Decisions 2015).

12COMPANY PERFORMANCE ANALYSIS

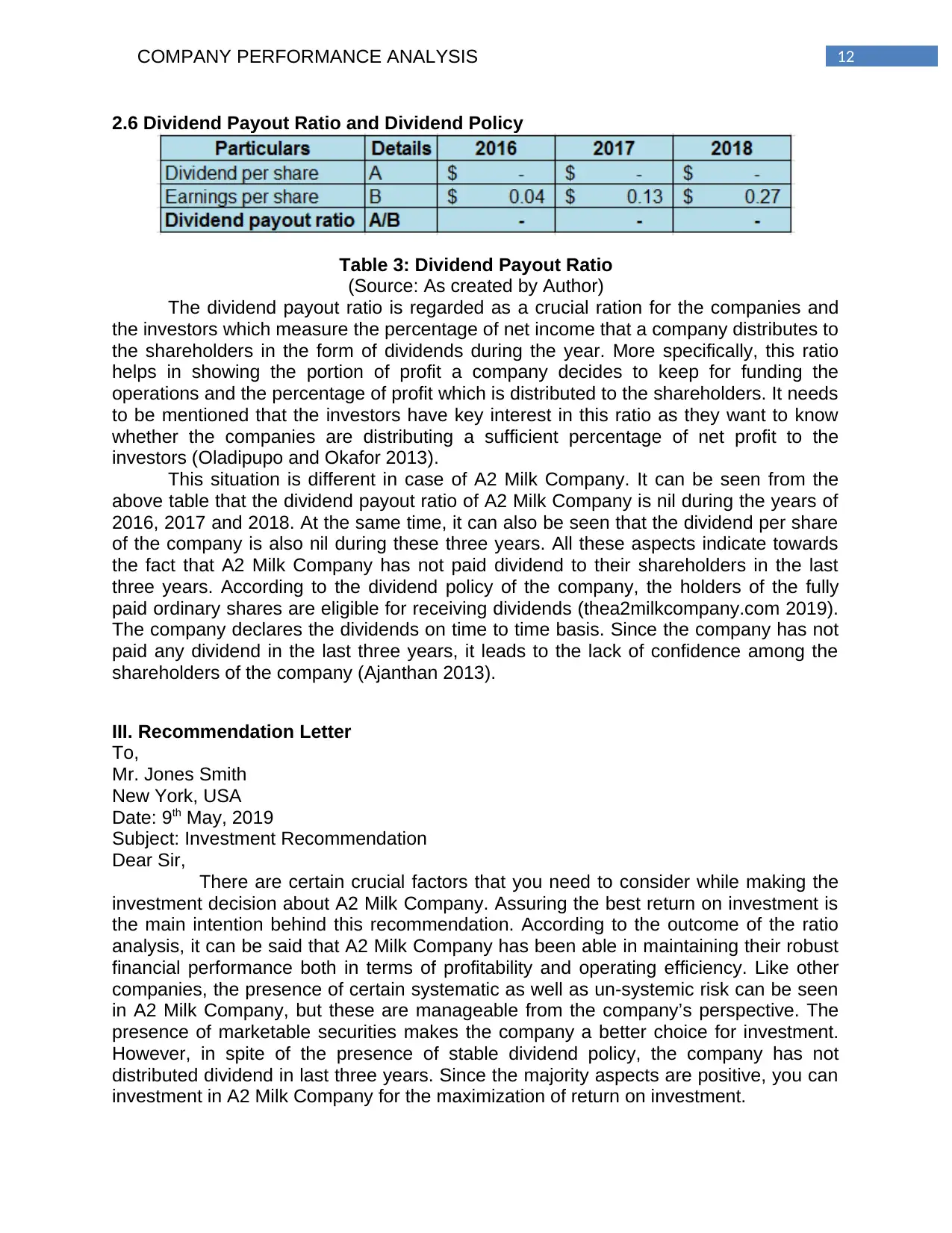

2.6 Dividend Payout Ratio and Dividend Policy

Table 3: Dividend Payout Ratio

(Source: As created by Author)

The dividend payout ratio is regarded as a crucial ration for the companies and

the investors which measure the percentage of net income that a company distributes to

the shareholders in the form of dividends during the year. More specifically, this ratio

helps in showing the portion of profit a company decides to keep for funding the

operations and the percentage of profit which is distributed to the shareholders. It needs

to be mentioned that the investors have key interest in this ratio as they want to know

whether the companies are distributing a sufficient percentage of net profit to the

investors (Oladipupo and Okafor 2013).

This situation is different in case of A2 Milk Company. It can be seen from the

above table that the dividend payout ratio of A2 Milk Company is nil during the years of

2016, 2017 and 2018. At the same time, it can also be seen that the dividend per share

of the company is also nil during these three years. All these aspects indicate towards

the fact that A2 Milk Company has not paid dividend to their shareholders in the last

three years. According to the dividend policy of the company, the holders of the fully

paid ordinary shares are eligible for receiving dividends (thea2milkcompany.com 2019).

The company declares the dividends on time to time basis. Since the company has not

paid any dividend in the last three years, it leads to the lack of confidence among the

shareholders of the company (Ajanthan 2013).

III. Recommendation Letter

To,

Mr. Jones Smith

New York, USA

Date: 9th May, 2019

Subject: Investment Recommendation

Dear Sir,

There are certain crucial factors that you need to consider while making the

investment decision about A2 Milk Company. Assuring the best return on investment is

the main intention behind this recommendation. According to the outcome of the ratio

analysis, it can be said that A2 Milk Company has been able in maintaining their robust

financial performance both in terms of profitability and operating efficiency. Like other

companies, the presence of certain systematic as well as un-systemic risk can be seen

in A2 Milk Company, but these are manageable from the company’s perspective. The

presence of marketable securities makes the company a better choice for investment.

However, in spite of the presence of stable dividend policy, the company has not

distributed dividend in last three years. Since the majority aspects are positive, you can

investment in A2 Milk Company for the maximization of return on investment.

2.6 Dividend Payout Ratio and Dividend Policy

Table 3: Dividend Payout Ratio

(Source: As created by Author)

The dividend payout ratio is regarded as a crucial ration for the companies and

the investors which measure the percentage of net income that a company distributes to

the shareholders in the form of dividends during the year. More specifically, this ratio

helps in showing the portion of profit a company decides to keep for funding the

operations and the percentage of profit which is distributed to the shareholders. It needs

to be mentioned that the investors have key interest in this ratio as they want to know

whether the companies are distributing a sufficient percentage of net profit to the

investors (Oladipupo and Okafor 2013).

This situation is different in case of A2 Milk Company. It can be seen from the

above table that the dividend payout ratio of A2 Milk Company is nil during the years of

2016, 2017 and 2018. At the same time, it can also be seen that the dividend per share

of the company is also nil during these three years. All these aspects indicate towards

the fact that A2 Milk Company has not paid dividend to their shareholders in the last

three years. According to the dividend policy of the company, the holders of the fully

paid ordinary shares are eligible for receiving dividends (thea2milkcompany.com 2019).

The company declares the dividends on time to time basis. Since the company has not

paid any dividend in the last three years, it leads to the lack of confidence among the

shareholders of the company (Ajanthan 2013).

III. Recommendation Letter

To,

Mr. Jones Smith

New York, USA

Date: 9th May, 2019

Subject: Investment Recommendation

Dear Sir,

There are certain crucial factors that you need to consider while making the

investment decision about A2 Milk Company. Assuring the best return on investment is

the main intention behind this recommendation. According to the outcome of the ratio

analysis, it can be said that A2 Milk Company has been able in maintaining their robust

financial performance both in terms of profitability and operating efficiency. Like other

companies, the presence of certain systematic as well as un-systemic risk can be seen

in A2 Milk Company, but these are manageable from the company’s perspective. The

presence of marketable securities makes the company a better choice for investment.

However, in spite of the presence of stable dividend policy, the company has not

distributed dividend in last three years. Since the majority aspects are positive, you can

investment in A2 Milk Company for the maximization of return on investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.