Financial Performance Analysis of Domino's Pizza Enterprises Limited

VerifiedAdded on 2023/03/31

|14

|3656

|484

Report

AI Summary

This report presents a comprehensive financial analysis of Domino's Pizza Enterprises Limited. The analysis begins with a company description and then delves into a detailed examination of profitability ratios (gross margin, net margin, ROCE) and operating efficiency ratios (inventory turnover, receivables turnover, payables turnover, and cash conversion cycle) from 2016 to 2018. The report evaluates the company's financial health, highlighting trends and providing insights into the factors driving performance. It also includes an assessment of marketable securities, a sensitivity analysis, and a discussion of systemic and unsystemic risks. Furthermore, the report computes and evaluates the dividend payout ratio and policy. The report concludes with a letter of recommendation regarding investment feasibility, summarizing the key findings and offering strategic recommendations for future performance. The report is prepared for a Finance for Business course and aims to assess the company's financial standing and provide investment insights.

Running head: COMPANY PERFORMANCE ANALYSIS

Company Performance Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Company Performance Analysis

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPANY PERFORMANCE ANALYSIS

Abstract:

The report is prepared with the objective for performing the financial evaluation of an

entity listed in ASX in order to undertake decisions. Therefore, Dominos Pizza

Enterprises Limited is selected as the entity. Different sections are prepared for

effective presentation of the report. Dominos Pizza Enterprises Limited has sound

profitability position because of the significant rise in both gross margin and net

margin. However, the entity is needed to formulate strategies for enhancing its

ROCE in future, since it is deemed to be a vital indicator of business profitability. In

addition, Dominos Pizza Enterprises Limited is able to maintain its operating

efficiency as well as profitability that would maximise the wealth of the shareholders

as well as the investors. It could be observed that the dividend payout ratio of the

entity has increased massively in 2017 and it has fallen slightly in 2018. This implies

that Dominos Pizza Enterprises Limited is involved in following constant dividend

policy, as it distributes dividends based on the profit generated by the organisation.

Hence, the investor is recommended to invest in the shares of Dominos Pizza

Enterprises Limited.

Abstract:

The report is prepared with the objective for performing the financial evaluation of an

entity listed in ASX in order to undertake decisions. Therefore, Dominos Pizza

Enterprises Limited is selected as the entity. Different sections are prepared for

effective presentation of the report. Dominos Pizza Enterprises Limited has sound

profitability position because of the significant rise in both gross margin and net

margin. However, the entity is needed to formulate strategies for enhancing its

ROCE in future, since it is deemed to be a vital indicator of business profitability. In

addition, Dominos Pizza Enterprises Limited is able to maintain its operating

efficiency as well as profitability that would maximise the wealth of the shareholders

as well as the investors. It could be observed that the dividend payout ratio of the

entity has increased massively in 2017 and it has fallen slightly in 2018. This implies

that Dominos Pizza Enterprises Limited is involved in following constant dividend

policy, as it distributes dividends based on the profit generated by the organisation.

Hence, the investor is recommended to invest in the shares of Dominos Pizza

Enterprises Limited.

2COMPANY PERFORMANCE ANALYSIS

Table of Contents

I. Introduction:...............................................................................................................3

II. Financial analysis of Dominos Pizza Enterprises Limited:.......................................3

2.1 Company description:.........................................................................................3

2.2 Computation and assessment of performance ratios:........................................3

2.3 Detection of marketable securities:.....................................................................7

2.4 Sensitivity analysis:.............................................................................................7

2.5 Systemic and un-systemic risks:.........................................................................9

2.6 Dividend payout ratio and payout policy:..........................................................10

III. Letter of recommendation:.....................................................................................10

IV. Conclusion:............................................................................................................11

References:................................................................................................................12

Table of Contents

I. Introduction:...............................................................................................................3

II. Financial analysis of Dominos Pizza Enterprises Limited:.......................................3

2.1 Company description:.........................................................................................3

2.2 Computation and assessment of performance ratios:........................................3

2.3 Detection of marketable securities:.....................................................................7

2.4 Sensitivity analysis:.............................................................................................7

2.5 Systemic and un-systemic risks:.........................................................................9

2.6 Dividend payout ratio and payout policy:..........................................................10

III. Letter of recommendation:.....................................................................................10

IV. Conclusion:............................................................................................................11

References:................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPANY PERFORMANCE ANALYSIS

I. Introduction:

By assessing the financial health of the entities, it becomes possible to gauge

the ongoing financial performance along with gathering an idea of their future

performance (Amit and Villalonga 2014). Due to this reason, the investment

professionals conduct financial performance analysis of those entities so that

appropriate investment decision could be undertaken. For performing the evaluation,

there are different tools used such as sensitivity analysis, ratio analysis and others.

The qualitative aspects to be taken into account include risk analysis of the firms,

marketable securities as well as others (Atanasov and Black 2016). The report is

prepared with the objective for performing the financial evaluation of an entity listed

in ASX in order to undertake decisions. Therefore, Dominos Pizza Enterprises

Limited is selected as the entity. Different sections are prepared for effective

presentation of the report. Initially, a brief overview of the business operations of the

above-mentioned entity would be provided in the paper. The next section elaborates

on the financial health of the entity by performing ratio analysis related to profitability

and operating efficiency. The next section focuses on performing cash management

evaluation that is made with the help of identifying marketable securities. After this,

there has been conduction of sensitivity analysis so that the viability of the proposed

project could be analysed accordingly. The aim of the next section is to include a

discussion of systemic and un-systemic risks. In addition, dividend payout ratio is

computed for the chosen entity and accordingly, evaluation would be made of its

payout policy. Finally, the report would shed light on recommending the feasibility of

investing in the chosen entity.

II. Financial analysis of Dominos Pizza Enterprises Limited:

2.1 Company description:

Dominos Pizza Enterprises Limited is the biggest pizza chain in Australia in

terms of network sales and network store numbers and it is the biggest global

franchise for Dominos Pizza brand. In other words, it is involved in operating retail

food outlets. The organisation is involved in operating a network of nearly 2,400

stores. The first store of Dominos that opened in Australia has been in the year 1983

in Springwood, Queensland. It then offered home delivery after the concept was

used by the Pizza Oven Family Restaurant in the year 1981 in Holland Park

Brisbane. Silvio’s Dial-a-Pizza has bought the Master Franchise of Australia and

New Zealand in 1993 and in 1995, the two brands merged and they are rebranded in

the name of Domino’s Pizza. In the year 2018, Dominos Pizza Enterprises Limited

has been inducted into the “Queensland Business Leaders Hall of Fame”

(Dominos.com.au 2019).

2.2 Computation and assessment of performance ratios:

The assessment of operating efficiency and profitability could be taken into

account in the form of two significant aspects in order to determine the current

financial performance and standing of Dominos Pizza Enterprises Limited. The

below-stated discussion reveals the assessment of different ratios under operating

efficacy and profitability of the selected organisation:

Analysis of profitability:

I. Introduction:

By assessing the financial health of the entities, it becomes possible to gauge

the ongoing financial performance along with gathering an idea of their future

performance (Amit and Villalonga 2014). Due to this reason, the investment

professionals conduct financial performance analysis of those entities so that

appropriate investment decision could be undertaken. For performing the evaluation,

there are different tools used such as sensitivity analysis, ratio analysis and others.

The qualitative aspects to be taken into account include risk analysis of the firms,

marketable securities as well as others (Atanasov and Black 2016). The report is

prepared with the objective for performing the financial evaluation of an entity listed

in ASX in order to undertake decisions. Therefore, Dominos Pizza Enterprises

Limited is selected as the entity. Different sections are prepared for effective

presentation of the report. Initially, a brief overview of the business operations of the

above-mentioned entity would be provided in the paper. The next section elaborates

on the financial health of the entity by performing ratio analysis related to profitability

and operating efficiency. The next section focuses on performing cash management

evaluation that is made with the help of identifying marketable securities. After this,

there has been conduction of sensitivity analysis so that the viability of the proposed

project could be analysed accordingly. The aim of the next section is to include a

discussion of systemic and un-systemic risks. In addition, dividend payout ratio is

computed for the chosen entity and accordingly, evaluation would be made of its

payout policy. Finally, the report would shed light on recommending the feasibility of

investing in the chosen entity.

II. Financial analysis of Dominos Pizza Enterprises Limited:

2.1 Company description:

Dominos Pizza Enterprises Limited is the biggest pizza chain in Australia in

terms of network sales and network store numbers and it is the biggest global

franchise for Dominos Pizza brand. In other words, it is involved in operating retail

food outlets. The organisation is involved in operating a network of nearly 2,400

stores. The first store of Dominos that opened in Australia has been in the year 1983

in Springwood, Queensland. It then offered home delivery after the concept was

used by the Pizza Oven Family Restaurant in the year 1981 in Holland Park

Brisbane. Silvio’s Dial-a-Pizza has bought the Master Franchise of Australia and

New Zealand in 1993 and in 1995, the two brands merged and they are rebranded in

the name of Domino’s Pizza. In the year 2018, Dominos Pizza Enterprises Limited

has been inducted into the “Queensland Business Leaders Hall of Fame”

(Dominos.com.au 2019).

2.2 Computation and assessment of performance ratios:

The assessment of operating efficiency and profitability could be taken into

account in the form of two significant aspects in order to determine the current

financial performance and standing of Dominos Pizza Enterprises Limited. The

below-stated discussion reveals the assessment of different ratios under operating

efficacy and profitability of the selected organisation:

Analysis of profitability:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPANY PERFORMANCE ANALYSIS

The evaluation of profitability ratios is made with the objective of determining

the capability of the business in generating income compared to the expenses

required to be incurred fir carrying out business operations (Benson, Faff and Smith

2014). Profitability ratios are of various types and in this case, three key ratios are

considered, which are evaluated briefly as follows:

Profitability Ratios

Particulars

Detail

s

2016 (in

$'000)

2017 (in

$'000)

%

Chang

e

2018 (in

$'000)

%

Chang

e

Revenue A 705,702 790,861 794,072

Gross profit B 419,633 436,734 408,397

Operating profit C 119,358 137,605 165,223

Net profit D 86,592 105,804 121,693

Total assets E 1,125,728 1,132,793 1,302,411

Current liabilities F 260,955 230,146 201,045

Gross margin B/A 59.46% 55.22% -7.13% 51.43% -6.87%

Net margin D/A 12.27% 13.38% 9.03% 15.33% 14.55%

Return on capital employed

(ROCE)

C/(E-

F) 13.80% 15.24% 10.45% 15.00% -1.59%

Table 1: Profitability ratios of Dominos Pizza Enterprises Limited for the years

2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios of Dominos Pizza Enterprises Limited for the years

2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

Based on the above table and figure, it could be stated that the first ratio is

gross margin, which represents the proportion of profit remaining to the organisation

after all the production payments are settled by the organisation (Brown 2014). In

accordance with the 2018 annual report of Dominos Pizza Enterprises Limited, the

main expense includes food costs disclosed under expenses in the income

The evaluation of profitability ratios is made with the objective of determining

the capability of the business in generating income compared to the expenses

required to be incurred fir carrying out business operations (Benson, Faff and Smith

2014). Profitability ratios are of various types and in this case, three key ratios are

considered, which are evaluated briefly as follows:

Profitability Ratios

Particulars

Detail

s

2016 (in

$'000)

2017 (in

$'000)

%

Chang

e

2018 (in

$'000)

%

Chang

e

Revenue A 705,702 790,861 794,072

Gross profit B 419,633 436,734 408,397

Operating profit C 119,358 137,605 165,223

Net profit D 86,592 105,804 121,693

Total assets E 1,125,728 1,132,793 1,302,411

Current liabilities F 260,955 230,146 201,045

Gross margin B/A 59.46% 55.22% -7.13% 51.43% -6.87%

Net margin D/A 12.27% 13.38% 9.03% 15.33% 14.55%

Return on capital employed

(ROCE)

C/(E-

F) 13.80% 15.24% 10.45% 15.00% -1.59%

Table 1: Profitability ratios of Dominos Pizza Enterprises Limited for the years

2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratios

Gross margin

Net margin

Return on capital employed

(ROCE)

Figure 1: Profitability ratios of Dominos Pizza Enterprises Limited for the years

2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

Based on the above table and figure, it could be stated that the first ratio is

gross margin, which represents the proportion of profit remaining to the organisation

after all the production payments are settled by the organisation (Brown 2014). In

accordance with the 2018 annual report of Dominos Pizza Enterprises Limited, the

main expense includes food costs disclosed under expenses in the income

5COMPANY PERFORMANCE ANALYSIS

statement. From the above figure, it could be seen that Dominos Pizza Enterprises

Limited has experienced a falling trend in gross margin from 2016 to 2018 and rise in

food expenses has been a crucial reason behind the downfall of the ratio and this is

not a sound indicator for Dominos Pizza Enterprises Limited.

Net margin implies the ability of any firm to produce profit after it has cleared

its non-direct payment of expenses (Decisions 2015). In case of Dominos Pizza

Enterprises Limited, net margin is observed to increase over the stated period and

this is a favourable signal to the profitability of the organisation. The minimisation in

some significant expenses such rise in interest income and marketing costs could be

adjudged as the major reasons for such increase.

ROCE gauges the capacity of an entity to derive profit from the employed

capital by contrasting net operating income to total assets less current liabilities

(Easton and Sommers 2018). From the above figure, it could be seen that after

ROCE has increased from 2016 to 2017, it has fallen slightly in 2018 owing to the

considerable amount of increase in operating income. However, the decline in the

ratio could be observed in 2-18 and excess increase in current liabilities could be

adjudged as the primary reason behind the same.

It is noteworthy to state that depending on the above discussion, Dominos

Pizza Enterprises Limited has sound profitability position because of the significant

rise in both gross margin and net margin. However, the entity is needed to formulate

strategies for enhancing its ROCE in future, since it is deemed to be a vital indicator

of business profitability.

Analysis of operating efficiency:

The internal efficacy of the firms in using assets and liabilities could be

ascertained by analysing operating efficiency. This aids in determining the overall

business performance of an organisation (Gallo 2014). There are four ratios that

have been used in evaluating the operational efficacy of Dominos Pizza Enterprises

Limited, which include the following:

Operating Efficiency Ratios:-

Particulars Details

2016 (in

$m)

2017 (in

$m)

%

Change

2018 (in

$m)

%

Change

Revenue A 705,702 790,861 794,072

Cost of sales B 286,069 354,127 385,675

Opening inventories C 12,282 16,675 21,098

Closing inventories D 16,675 21,098 19,271

Average inventories E=(C+D)/2 14,479 18,887 20,185

Opening receivables F 43,883 72,143 72,615

Closing receivables G 72,143 72,615 78,181

Average receivables H=(F+G)/2 58,013 72,379 75,398

Opening payables I 108,826 150,665 136,376

Closing payables J

statement. From the above figure, it could be seen that Dominos Pizza Enterprises

Limited has experienced a falling trend in gross margin from 2016 to 2018 and rise in

food expenses has been a crucial reason behind the downfall of the ratio and this is

not a sound indicator for Dominos Pizza Enterprises Limited.

Net margin implies the ability of any firm to produce profit after it has cleared

its non-direct payment of expenses (Decisions 2015). In case of Dominos Pizza

Enterprises Limited, net margin is observed to increase over the stated period and

this is a favourable signal to the profitability of the organisation. The minimisation in

some significant expenses such rise in interest income and marketing costs could be

adjudged as the major reasons for such increase.

ROCE gauges the capacity of an entity to derive profit from the employed

capital by contrasting net operating income to total assets less current liabilities

(Easton and Sommers 2018). From the above figure, it could be seen that after

ROCE has increased from 2016 to 2017, it has fallen slightly in 2018 owing to the

considerable amount of increase in operating income. However, the decline in the

ratio could be observed in 2-18 and excess increase in current liabilities could be

adjudged as the primary reason behind the same.

It is noteworthy to state that depending on the above discussion, Dominos

Pizza Enterprises Limited has sound profitability position because of the significant

rise in both gross margin and net margin. However, the entity is needed to formulate

strategies for enhancing its ROCE in future, since it is deemed to be a vital indicator

of business profitability.

Analysis of operating efficiency:

The internal efficacy of the firms in using assets and liabilities could be

ascertained by analysing operating efficiency. This aids in determining the overall

business performance of an organisation (Gallo 2014). There are four ratios that

have been used in evaluating the operational efficacy of Dominos Pizza Enterprises

Limited, which include the following:

Operating Efficiency Ratios:-

Particulars Details

2016 (in

$m)

2017 (in

$m)

%

Change

2018 (in

$m)

%

Change

Revenue A 705,702 790,861 794,072

Cost of sales B 286,069 354,127 385,675

Opening inventories C 12,282 16,675 21,098

Closing inventories D 16,675 21,098 19,271

Average inventories E=(C+D)/2 14,479 18,887 20,185

Opening receivables F 43,883 72,143 72,615

Closing receivables G 72,143 72,615 78,181

Average receivables H=(F+G)/2 58,013 72,379 75,398

Opening payables I 108,826 150,665 136,376

Closing payables J

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COMPANY PERFORMANCE ANALYSIS

150,665 136,376 156,045

Average payables K=(I+J)/2 129,746 143,521 146,211

Days inventory

turnover L=365/(B/E) 18.47 19.47 5.38% 19.10 -1.87%

Days receivables

turnover

M=365/(A/

H) 30.01 33.40 11.33% 34.66 3.75%

Days payables

turnover

N=365/(B/

K) 192.24 140.56 -26.88% 147.68 5.06%

Cash conversion cycle L+M-N

-

143.76

-

87.69 -39.00%

-

93.92 7.10%

Table 2: Operating efficiency ratios of Dominos Pizza Enterprises Limited for

the years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-200.00

-150.00

-100.00

-50.00

-

50.00

100.00

150.00

200.00

250.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Operating efficiency ratios of Dominos Pizza Enterprises Limited for

the years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

By using inventory turnover days, it becomes possible to gauge the efficiency

of a firm to manage inventory (Gaur and Kesavan 2015). In accordance with the

above figure, it could be seen that inventory turnover days after increasing from 2016

to 2017 has fallen slightly in 2018 denoting that it is efficient in receiving its due

amounts from the customers. This implies that the company has managed to

discharge its inventory at a slightly higher rate.

Receivables turnover days imply the efficiency of an entity in settling the

amounts owed to the suppliers (Gippel, Smith and Zhu 2015). In accordance with the

above figure, it could be seen that the receivables turnover days after increasing

from 2016 to 2017 has risen again in 2018 denoting that it is not efficient in receiving

its due amounts from the customers. Thus, it has not managed to reduce the time in

collecting the receivables.

Payables turnover days signify how efficient an entity is when it comes to

settlement of its dues (Gitman, Juchau and Flanagan 2015). This ratio has fallen

significantly in 2017; however, slight increase could be observed in the year 2018.

Since the fluctuations are severe, they denote that the creditors are paid either after

150,665 136,376 156,045

Average payables K=(I+J)/2 129,746 143,521 146,211

Days inventory

turnover L=365/(B/E) 18.47 19.47 5.38% 19.10 -1.87%

Days receivables

turnover

M=365/(A/

H) 30.01 33.40 11.33% 34.66 3.75%

Days payables

turnover

N=365/(B/

K) 192.24 140.56 -26.88% 147.68 5.06%

Cash conversion cycle L+M-N

-

143.76

-

87.69 -39.00%

-

93.92 7.10%

Table 2: Operating efficiency ratios of Dominos Pizza Enterprises Limited for

the years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

Days inventory

turnover Days receivables

turnover Days payables

turnover Cash conversion

cycle

-200.00

-150.00

-100.00

-50.00

-

50.00

100.00

150.00

200.00

250.00

Operating Efficiency Ratios

2016

2017

2018

Figure 2: Operating efficiency ratios of Dominos Pizza Enterprises Limited for

the years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

By using inventory turnover days, it becomes possible to gauge the efficiency

of a firm to manage inventory (Gaur and Kesavan 2015). In accordance with the

above figure, it could be seen that inventory turnover days after increasing from 2016

to 2017 has fallen slightly in 2018 denoting that it is efficient in receiving its due

amounts from the customers. This implies that the company has managed to

discharge its inventory at a slightly higher rate.

Receivables turnover days imply the efficiency of an entity in settling the

amounts owed to the suppliers (Gippel, Smith and Zhu 2015). In accordance with the

above figure, it could be seen that the receivables turnover days after increasing

from 2016 to 2017 has risen again in 2018 denoting that it is not efficient in receiving

its due amounts from the customers. Thus, it has not managed to reduce the time in

collecting the receivables.

Payables turnover days signify how efficient an entity is when it comes to

settlement of its dues (Gitman, Juchau and Flanagan 2015). This ratio has fallen

significantly in 2017; however, slight increase could be observed in the year 2018.

Since the fluctuations are severe, they denote that the creditors are paid either after

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPANY PERFORMANCE ANALYSIS

or before the stipulated time, which might have unfavourable impact on the business

operations in future.

Cash conversion cycle implies how capable an entity is when it comes to

converting business resources into cash (Hillier et al. 2014). The cash conversion

cycle of Dominos Pizza Enterprises Limited is found to be negative in all the years

denoting that lower time is required for sale of inventory along with obtaining cash

from the customers against the time where the inventory supplier payments have to

be settled.

Based on the above discussion, it could be stated that Dominos Pizza

Enterprises Limited is able to maintain its operating efficiency as well as profitability

that would maximise the wealth of the shareholders as well as the investors.

2.3 Detection of marketable securities:

The current assets include certain marketable securities, which are deemed to

be the type of liquid assets on the statement of financial position, which is possible to

be transferred into cash (Hirshleifer 2015). Based on the 2018 annual report of

Dominos Pizza Enterprises Limited, cash at bank and in hand along with short-term

deposits could be categorised under marketable securities. Considerable increase

could be observed in cash and other short-term deposits of the entity in 2018

compared to 2017.

It is noteworthy to state that the organisations are engaged to utilise such

instruments for earning return on assets and this is applicable in case of Dominos

Pizza Enterprises Limited as well. It has been identified that the entity makes interest

on floating rates depending on daily rates of bank deposits made in its business

accounts. This denotes that the firm uses the securities as cash sources so that it

could maintain credible policies related to cash management (Iooss and Lemaître

2015). It is not possible to ignore the significance of sound cash management policy.

The rise in marketable securities in the balance sheet statement represents the

policy of Dominos Pizza Enterprises Limited for improving the cash collection in

order to boost the liquidity position, which is beneficial for cash management.

Moreover, maintaining adequate cash balance provides the firm with the chance of

combating with the economic downturns coupled with financial stability in order to

undertake investments when suitable price is present. The big investors could make

Dominos Pizza Enterprises Limited in undertaking effective acquisition target when

large balance of cash balance is used for productive measures (Khadafi, Heikal and

Ummah 2014).

2.4 Sensitivity analysis:

In this case, a situation is assumed where Dominos Pizza Enterprises Limited

is intending to develop a new product. Two different scenarios are taken into account

that comprises of the normal scenario and sensitivity analysis with identical value

drivers when there are a number of changes.

Normal situation:

or before the stipulated time, which might have unfavourable impact on the business

operations in future.

Cash conversion cycle implies how capable an entity is when it comes to

converting business resources into cash (Hillier et al. 2014). The cash conversion

cycle of Dominos Pizza Enterprises Limited is found to be negative in all the years

denoting that lower time is required for sale of inventory along with obtaining cash

from the customers against the time where the inventory supplier payments have to

be settled.

Based on the above discussion, it could be stated that Dominos Pizza

Enterprises Limited is able to maintain its operating efficiency as well as profitability

that would maximise the wealth of the shareholders as well as the investors.

2.3 Detection of marketable securities:

The current assets include certain marketable securities, which are deemed to

be the type of liquid assets on the statement of financial position, which is possible to

be transferred into cash (Hirshleifer 2015). Based on the 2018 annual report of

Dominos Pizza Enterprises Limited, cash at bank and in hand along with short-term

deposits could be categorised under marketable securities. Considerable increase

could be observed in cash and other short-term deposits of the entity in 2018

compared to 2017.

It is noteworthy to state that the organisations are engaged to utilise such

instruments for earning return on assets and this is applicable in case of Dominos

Pizza Enterprises Limited as well. It has been identified that the entity makes interest

on floating rates depending on daily rates of bank deposits made in its business

accounts. This denotes that the firm uses the securities as cash sources so that it

could maintain credible policies related to cash management (Iooss and Lemaître

2015). It is not possible to ignore the significance of sound cash management policy.

The rise in marketable securities in the balance sheet statement represents the

policy of Dominos Pizza Enterprises Limited for improving the cash collection in

order to boost the liquidity position, which is beneficial for cash management.

Moreover, maintaining adequate cash balance provides the firm with the chance of

combating with the economic downturns coupled with financial stability in order to

undertake investments when suitable price is present. The big investors could make

Dominos Pizza Enterprises Limited in undertaking effective acquisition target when

large balance of cash balance is used for productive measures (Khadafi, Heikal and

Ummah 2014).

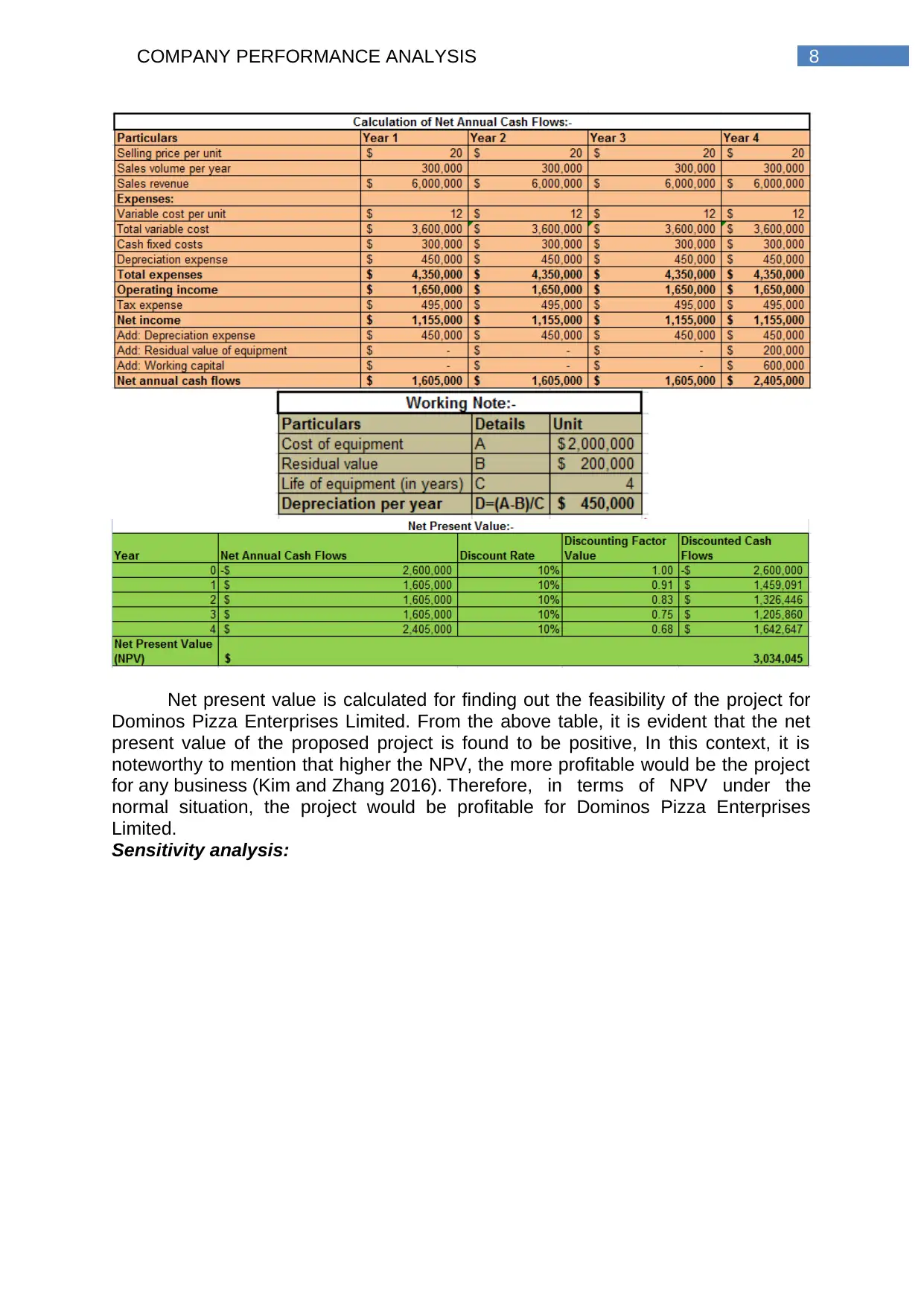

2.4 Sensitivity analysis:

In this case, a situation is assumed where Dominos Pizza Enterprises Limited

is intending to develop a new product. Two different scenarios are taken into account

that comprises of the normal scenario and sensitivity analysis with identical value

drivers when there are a number of changes.

Normal situation:

8COMPANY PERFORMANCE ANALYSIS

Net present value is calculated for finding out the feasibility of the project for

Dominos Pizza Enterprises Limited. From the above table, it is evident that the net

present value of the proposed project is found to be positive, In this context, it is

noteworthy to mention that higher the NPV, the more profitable would be the project

for any business (Kim and Zhang 2016). Therefore, in terms of NPV under the

normal situation, the project would be profitable for Dominos Pizza Enterprises

Limited.

Sensitivity analysis:

Net present value is calculated for finding out the feasibility of the project for

Dominos Pizza Enterprises Limited. From the above table, it is evident that the net

present value of the proposed project is found to be positive, In this context, it is

noteworthy to mention that higher the NPV, the more profitable would be the project

for any business (Kim and Zhang 2016). Therefore, in terms of NPV under the

normal situation, the project would be profitable for Dominos Pizza Enterprises

Limited.

Sensitivity analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPANY PERFORMANCE ANALYSIS

For conducting the sensitivity analysis of the project, selling price unit and unit

sales have been declined by 10% per annum, while variable cost per unit has

increased by 10% and cash fixed cost would rise by 10% as well. Based on the

above tables, it could be seen that there would be decrease in cash inflows and cash

outflows would rise accordingly. However, the NPV of the project is still found to be

positive implying that the project would still yield benefits to Dominos Pizza

Enterprises Limited. Hence, the firm is advised to accept the project.

2.5 Systemic and un-systemic risks:

The main reason of occurrence of systemic risk is due to the variations in

macroeconomic factors such as changes in interest rate, inflation as well as others

(Kuttner and Shim 2016). The main systemic risks of Dominos Pizza Enterprises

Limited include the following:

Equity price risk:

The entity is prone to this particular risk on listed investments, which are

categorised and measured at fair value with the help of other comprehensive

income. The entity is not engaged in hedging such risk. The management of the firm

is involved in monitoring the specific risk exposure by contrasting the quoted stock

price movements in relation to long-term investments (Lee, Sameen and Cowling

2015).

The relation of un-systemic risk could be observed with the particular industry

and such risks of Dominos Pizza Enterprise Limited are represented as follows:

Supply chain:

For conducting the sensitivity analysis of the project, selling price unit and unit

sales have been declined by 10% per annum, while variable cost per unit has

increased by 10% and cash fixed cost would rise by 10% as well. Based on the

above tables, it could be seen that there would be decrease in cash inflows and cash

outflows would rise accordingly. However, the NPV of the project is still found to be

positive implying that the project would still yield benefits to Dominos Pizza

Enterprises Limited. Hence, the firm is advised to accept the project.

2.5 Systemic and un-systemic risks:

The main reason of occurrence of systemic risk is due to the variations in

macroeconomic factors such as changes in interest rate, inflation as well as others

(Kuttner and Shim 2016). The main systemic risks of Dominos Pizza Enterprises

Limited include the following:

Equity price risk:

The entity is prone to this particular risk on listed investments, which are

categorised and measured at fair value with the help of other comprehensive

income. The entity is not engaged in hedging such risk. The management of the firm

is involved in monitoring the specific risk exposure by contrasting the quoted stock

price movements in relation to long-term investments (Lee, Sameen and Cowling

2015).

The relation of un-systemic risk could be observed with the particular industry

and such risks of Dominos Pizza Enterprise Limited are represented as follows:

Supply chain:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPANY PERFORMANCE ANALYSIS

The ability of the firm in maintaining product supply could be tarnished, if there

is adverse and material change in operation of one or additional suppliers and

minimisation in support from them.

Hike in rivalry:

Since Dominos Pizza Enterprises Limited functions in an increasingly

competitive sector, since hike in rivalry could act as barriers to the business

operations. These risks are identified to be one of the un-systemic risks in the

operations of the entity (Liu et al. 2013).

2.6 Dividend payout ratio and payout policy:

Particulars Details 2016 2017 2018

Dividend per share A $ 0.39 $ 0.93 $ 1.08

Earnings per share B $ 0.94 $ 1.16 $ 1.39

Dividend payout

ratio A/B 41.49% 80.17% 77.70%

Table 3: Dividend payout ratio of Dominos Pizza Enterprises Limited for the

years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

This is deemed to be a significant criterion for the entities as well as the

investors that gauge the proportion of net income distributed to the shareholders as

dividends during the period (Yazdanfar and Öhman 2014). More precisely, the ratio

assists in denoting the percentage of income distributed to the shareholders. The

investors have significant interest in the ratio since they want to have an

understanding of whether the firms are providing adequate profit proportion to the

investors (Žižlavský 2014).

According to the above table, it could be observed that the dividend payout

ratio of the entity has increased massively in 2017 and it has fallen slightly in 2018.

This implies that Dominos Pizza Enterprises Limited is involved in following constant

dividend policy, as it distributes dividends based on the profit generated by the

organisation.

III. Letter of recommendation:

To,

Mr. XYZ

Date: 31st May 2019

Subject: Letter of recommendation

Based on the above analysis, it could be seen that it is noteworthy to state

that depending on the above discussion, Dominos Pizza Enterprises Limited has

sound profitability position because of the significant rise in both gross margin and

net margin. However, the entity is needed to formulate strategies for enhancing its

ROCE in future, since it is deemed to be a vital indicator of business profitability. In

addition, Dominos Pizza Enterprises Limited is able to maintain its operating

efficiency as well as profitability that would maximise the wealth of the shareholders

as well as the investors. It could be observed that the dividend payout ratio of the

entity has increased massively in 2017 and it has fallen slightly in 2018. This implies

that Dominos Pizza Enterprises Limited is involved in following constant dividend

policy, as it distributes dividends based on the profit generated by the organisation.

The ability of the firm in maintaining product supply could be tarnished, if there

is adverse and material change in operation of one or additional suppliers and

minimisation in support from them.

Hike in rivalry:

Since Dominos Pizza Enterprises Limited functions in an increasingly

competitive sector, since hike in rivalry could act as barriers to the business

operations. These risks are identified to be one of the un-systemic risks in the

operations of the entity (Liu et al. 2013).

2.6 Dividend payout ratio and payout policy:

Particulars Details 2016 2017 2018

Dividend per share A $ 0.39 $ 0.93 $ 1.08

Earnings per share B $ 0.94 $ 1.16 $ 1.39

Dividend payout

ratio A/B 41.49% 80.17% 77.70%

Table 3: Dividend payout ratio of Dominos Pizza Enterprises Limited for the

years 2016-2018

(Source: Annualreport2018.dominos.com.au 2019)

This is deemed to be a significant criterion for the entities as well as the

investors that gauge the proportion of net income distributed to the shareholders as

dividends during the period (Yazdanfar and Öhman 2014). More precisely, the ratio

assists in denoting the percentage of income distributed to the shareholders. The

investors have significant interest in the ratio since they want to have an

understanding of whether the firms are providing adequate profit proportion to the

investors (Žižlavský 2014).

According to the above table, it could be observed that the dividend payout

ratio of the entity has increased massively in 2017 and it has fallen slightly in 2018.

This implies that Dominos Pizza Enterprises Limited is involved in following constant

dividend policy, as it distributes dividends based on the profit generated by the

organisation.

III. Letter of recommendation:

To,

Mr. XYZ

Date: 31st May 2019

Subject: Letter of recommendation

Based on the above analysis, it could be seen that it is noteworthy to state

that depending on the above discussion, Dominos Pizza Enterprises Limited has

sound profitability position because of the significant rise in both gross margin and

net margin. However, the entity is needed to formulate strategies for enhancing its

ROCE in future, since it is deemed to be a vital indicator of business profitability. In

addition, Dominos Pizza Enterprises Limited is able to maintain its operating

efficiency as well as profitability that would maximise the wealth of the shareholders

as well as the investors. It could be observed that the dividend payout ratio of the

entity has increased massively in 2017 and it has fallen slightly in 2018. This implies

that Dominos Pizza Enterprises Limited is involved in following constant dividend

policy, as it distributes dividends based on the profit generated by the organisation.

11COMPANY PERFORMANCE ANALYSIS

Hence, the investor is recommended to invest in the shares of Dominos Pizza

Enterprises Limited.

IV. Conclusion:

By taking into consideration all the possible aspects, it could be seen that

Dominos Pizza Enterprises Limited is the biggest pizza chain in Australia in terms of

network sales and network store numbers and it is the biggest global franchise for

Dominos Pizza brand. In other words, it is involved in operating retail food outlets.

The organisation is involved in operating a network of nearly 2,400 stores. Moreover,

the firm is advised to accept the project, as it would yield significant benefits to them.

It could be observed that the dividend payout ratio of the entity has increased

massively in 2017 and it has fallen slightly in 2018. This implies that Dominos Pizza

Enterprises Limited is involved in following constant dividend policy, as it distributes

dividends based on the profit generated by the organisation. Hence, the investor is

recommended to invest in the shares of Dominos Pizza Enterprises Limited.

Hence, the investor is recommended to invest in the shares of Dominos Pizza

Enterprises Limited.

IV. Conclusion:

By taking into consideration all the possible aspects, it could be seen that

Dominos Pizza Enterprises Limited is the biggest pizza chain in Australia in terms of

network sales and network store numbers and it is the biggest global franchise for

Dominos Pizza brand. In other words, it is involved in operating retail food outlets.

The organisation is involved in operating a network of nearly 2,400 stores. Moreover,

the firm is advised to accept the project, as it would yield significant benefits to them.

It could be observed that the dividend payout ratio of the entity has increased

massively in 2017 and it has fallen slightly in 2018. This implies that Dominos Pizza

Enterprises Limited is involved in following constant dividend policy, as it distributes

dividends based on the profit generated by the organisation. Hence, the investor is

recommended to invest in the shares of Dominos Pizza Enterprises Limited.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.