HI5020 Corporate Accounting: A Financial Report on CBA and Westpac

VerifiedAdded on 2023/06/03

|23

|4410

|498

Report

AI Summary

This report provides a comparative financial analysis of two major Australian banks, Commonwealth Bank (CBA) and Westpac, focusing on their equity structure, cash flow statements, comprehensive income, and corporate income tax. The analysis includes a detailed discussion of each equity item, a comparison of debt and equity ratios, and an examination of cash flow activities over three years. It also covers items reported in the Other Comprehensive Income (OCI) statement, the effective income tax rate, deferred tax assets and liabilities, and the calculation of cash tax using book tax. The report concludes with a summary of the key differences and similarities between the two banks' financial performances. Find more solved assignments and study resources on Desklib.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

An industry average is calculated through the average of returns of various companies working

within it. The performance of such companies together describes the performance of an industry

in the market. From an investor's point of view, it is important to know about a company in terms

of its internal management, internal control, effectiveness & efficiency of a business, etc so that

useful decisions can be made. Thus, for such reasons it's important that the financial statements

prepared are authenticated and reliable and an efficient analysis has been made based on such

information. The following discussion is a comparative analysis of two listed Australian

companies called Commonwealth bank and Westpac bank, working within the same industry.

An industry average is calculated through the average of returns of various companies working

within it. The performance of such companies together describes the performance of an industry

in the market. From an investor's point of view, it is important to know about a company in terms

of its internal management, internal control, effectiveness & efficiency of a business, etc so that

useful decisions can be made. Thus, for such reasons it's important that the financial statements

prepared are authenticated and reliable and an efficient analysis has been made based on such

information. The following discussion is a comparative analysis of two listed Australian

companies called Commonwealth bank and Westpac bank, working within the same industry.

Contents

INTRODUCTION...........................................................................................................................4

ANALYSIS OF EQUITY................................................................................................................5

DISCUSSION ABOUT EACH EQUITY ITEM.........................................................................5

DISCUSSION REGARDING DEBT & EQUITY OF BOTH THE COMPANIES...................7

ANALYSIS OF CASH FLOW STATEMENT...............................................................................9

DISCUSSION REGARDING CASH FLOW STATEMENT.....................................................9

COMPARISON OF CASH FLOW OF BOTH THE COMPANIES FOR THE PAST 3

YEARS.......................................................................................................................................10

DESCRIPTION OF ANALYSIS OF CASH FLOW OF BOTH THE COMPANIES..............12

ANALYSIS OF COMPREHENSIVE INCOME STATEMENT.................................................14

ITEMS REPORTED IN THE OTHER COMPREHENSIVE INCOME STATEMENT..........14

REASONS FOR NOT REPORTING THIS ITEM IN THE INCOME STATEMENT............14

COMPARATIVE ANALYSIS OF THE OCI STATEMENT's ITEMS...................................14

USE OF OCI IN EVALUATION OF PERFORMANCE OF MANAGERS............................15

ANALYSIS OF CORPORATE INCOME TAX...........................................................................16

EFFECTIVE INCOME TAX RATE.........................................................................................16

DEFERRED TAX ASSETS AND LIABILITIES.....................................................................16

INCREASE IN DTA AND DTL...............................................................................................17

CALCULATION OF CASH TAX USING THE BOOK TAX.................................................17

INTRODUCTION...........................................................................................................................4

ANALYSIS OF EQUITY................................................................................................................5

DISCUSSION ABOUT EACH EQUITY ITEM.........................................................................5

DISCUSSION REGARDING DEBT & EQUITY OF BOTH THE COMPANIES...................7

ANALYSIS OF CASH FLOW STATEMENT...............................................................................9

DISCUSSION REGARDING CASH FLOW STATEMENT.....................................................9

COMPARISON OF CASH FLOW OF BOTH THE COMPANIES FOR THE PAST 3

YEARS.......................................................................................................................................10

DESCRIPTION OF ANALYSIS OF CASH FLOW OF BOTH THE COMPANIES..............12

ANALYSIS OF COMPREHENSIVE INCOME STATEMENT.................................................14

ITEMS REPORTED IN THE OTHER COMPREHENSIVE INCOME STATEMENT..........14

REASONS FOR NOT REPORTING THIS ITEM IN THE INCOME STATEMENT............14

COMPARATIVE ANALYSIS OF THE OCI STATEMENT's ITEMS...................................14

USE OF OCI IN EVALUATION OF PERFORMANCE OF MANAGERS............................15

ANALYSIS OF CORPORATE INCOME TAX...........................................................................16

EFFECTIVE INCOME TAX RATE.........................................................................................16

DEFERRED TAX ASSETS AND LIABILITIES.....................................................................16

INCREASE IN DTA AND DTL...............................................................................................17

CALCULATION OF CASH TAX USING THE BOOK TAX.................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CALCULATION OF CASH TAX RATE.................................................................................19

DIFFERENCE IN CASH TAX AND BOOK TAX..................................................................19

CONCLUSION..............................................................................................................................20

Bibliography..................................................................................................................................21

DIFFERENCE IN CASH TAX AND BOOK TAX..................................................................19

CONCLUSION..............................................................................................................................20

Bibliography..................................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

There are various financial & non-financial information together are used for the preparation of

various components that forms the financial reports of an organization (Alvarez, 2013). All these

factors differ in terms of nature and characteristics. The selected two companies belong to the

banking sector and a comparative analysis has been made between them on the basis of equity,

cash flow statement, comprehensive income, corporate income tax, deferred tax assets and

deferred tax liabilities, cash tax, etc.

Commonwealth bank of Australia, being the largest bank in Southern Hemisphere, is a global

bank having its business operations at United States, United Kingdom and New Zealand. The

activities undertaken by this company includes business and retail management of funds,

superannuation facilities, insurance services, investment services, Institutional banking and such

other services such as brokerage services. This company earned the title of being largest listed

company on the Australian Securities Exchange with brands such as Commonwealth insurance

or securities, Bankwest etc.

Considered as one of the 'big four' Australian banks, Westpac Banking Corporation is a financial

services provider with its headquarters at Sydney. The words 'Western' and 'Pacific' are

combined together to form the word 'Westpac'. The company is currently acquainted with 40,000

employees and 14 million employees (Atkinson, 2012). The company has a long term objective

that not only includes its growth in profits or expansion but also to prosper in terms of customers

and communities by providing best services. As per 2017 Dow Jones Sustainability Index, it was

considered as one of the most sustainable bank which was for the fourth time in a row.

Let us discuss the comparative analysis of both the companies along with their reasons and

impact on the financial reports.

There are various financial & non-financial information together are used for the preparation of

various components that forms the financial reports of an organization (Alvarez, 2013). All these

factors differ in terms of nature and characteristics. The selected two companies belong to the

banking sector and a comparative analysis has been made between them on the basis of equity,

cash flow statement, comprehensive income, corporate income tax, deferred tax assets and

deferred tax liabilities, cash tax, etc.

Commonwealth bank of Australia, being the largest bank in Southern Hemisphere, is a global

bank having its business operations at United States, United Kingdom and New Zealand. The

activities undertaken by this company includes business and retail management of funds,

superannuation facilities, insurance services, investment services, Institutional banking and such

other services such as brokerage services. This company earned the title of being largest listed

company on the Australian Securities Exchange with brands such as Commonwealth insurance

or securities, Bankwest etc.

Considered as one of the 'big four' Australian banks, Westpac Banking Corporation is a financial

services provider with its headquarters at Sydney. The words 'Western' and 'Pacific' are

combined together to form the word 'Westpac'. The company is currently acquainted with 40,000

employees and 14 million employees (Atkinson, 2012). The company has a long term objective

that not only includes its growth in profits or expansion but also to prosper in terms of customers

and communities by providing best services. As per 2017 Dow Jones Sustainability Index, it was

considered as one of the most sustainable bank which was for the fourth time in a row.

Let us discuss the comparative analysis of both the companies along with their reasons and

impact on the financial reports.

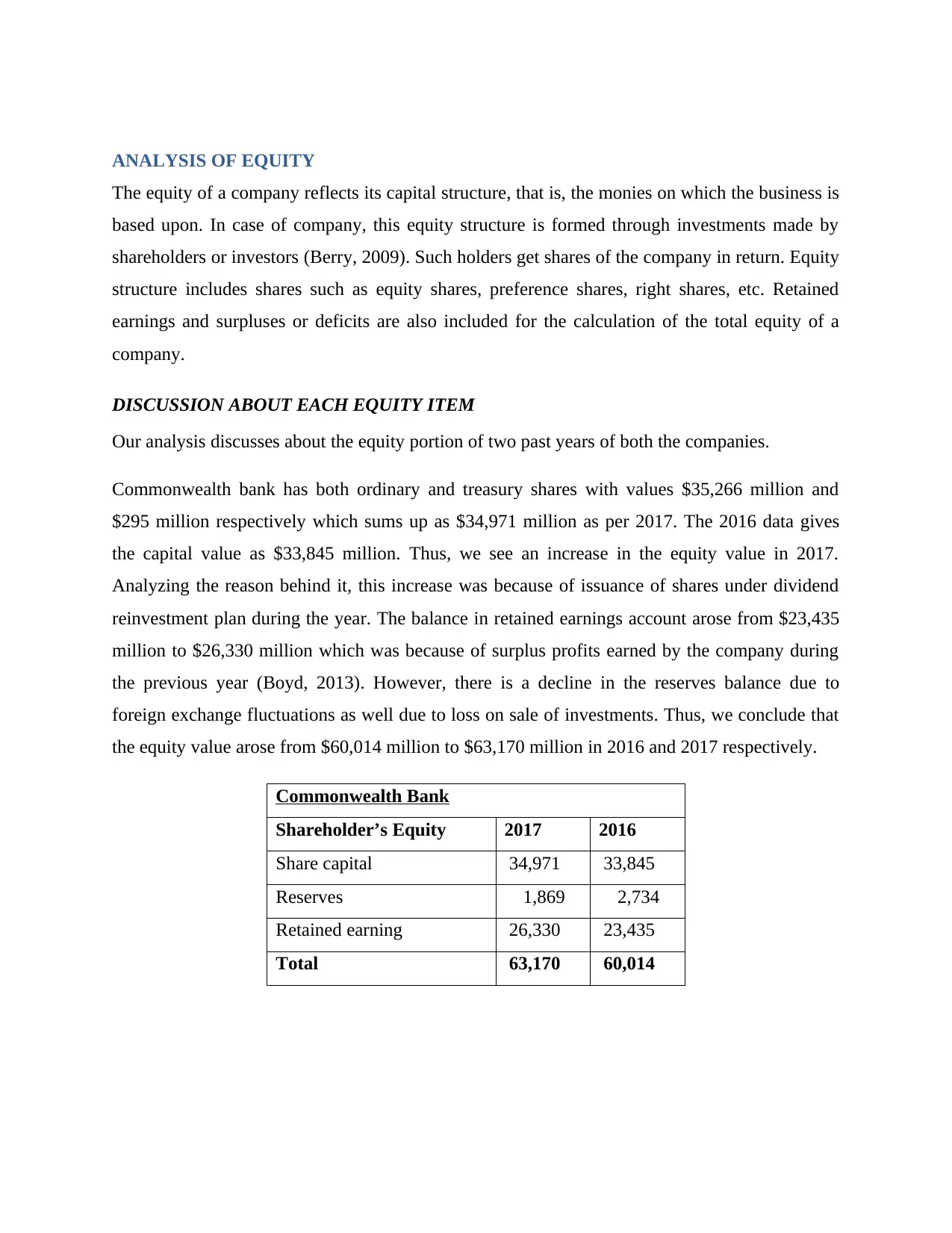

ANALYSIS OF EQUITY

The equity of a company reflects its capital structure, that is, the monies on which the business is

based upon. In case of company, this equity structure is formed through investments made by

shareholders or investors (Berry, 2009). Such holders get shares of the company in return. Equity

structure includes shares such as equity shares, preference shares, right shares, etc. Retained

earnings and surpluses or deficits are also included for the calculation of the total equity of a

company.

DISCUSSION ABOUT EACH EQUITY ITEM

Our analysis discusses about the equity portion of two past years of both the companies.

Commonwealth bank has both ordinary and treasury shares with values $35,266 million and

$295 million respectively which sums up as $34,971 million as per 2017. The 2016 data gives

the capital value as $33,845 million. Thus, we see an increase in the equity value in 2017.

Analyzing the reason behind it, this increase was because of issuance of shares under dividend

reinvestment plan during the year. The balance in retained earnings account arose from $23,435

million to $26,330 million which was because of surplus profits earned by the company during

the previous year (Boyd, 2013). However, there is a decline in the reserves balance due to

foreign exchange fluctuations as well due to loss on sale of investments. Thus, we conclude that

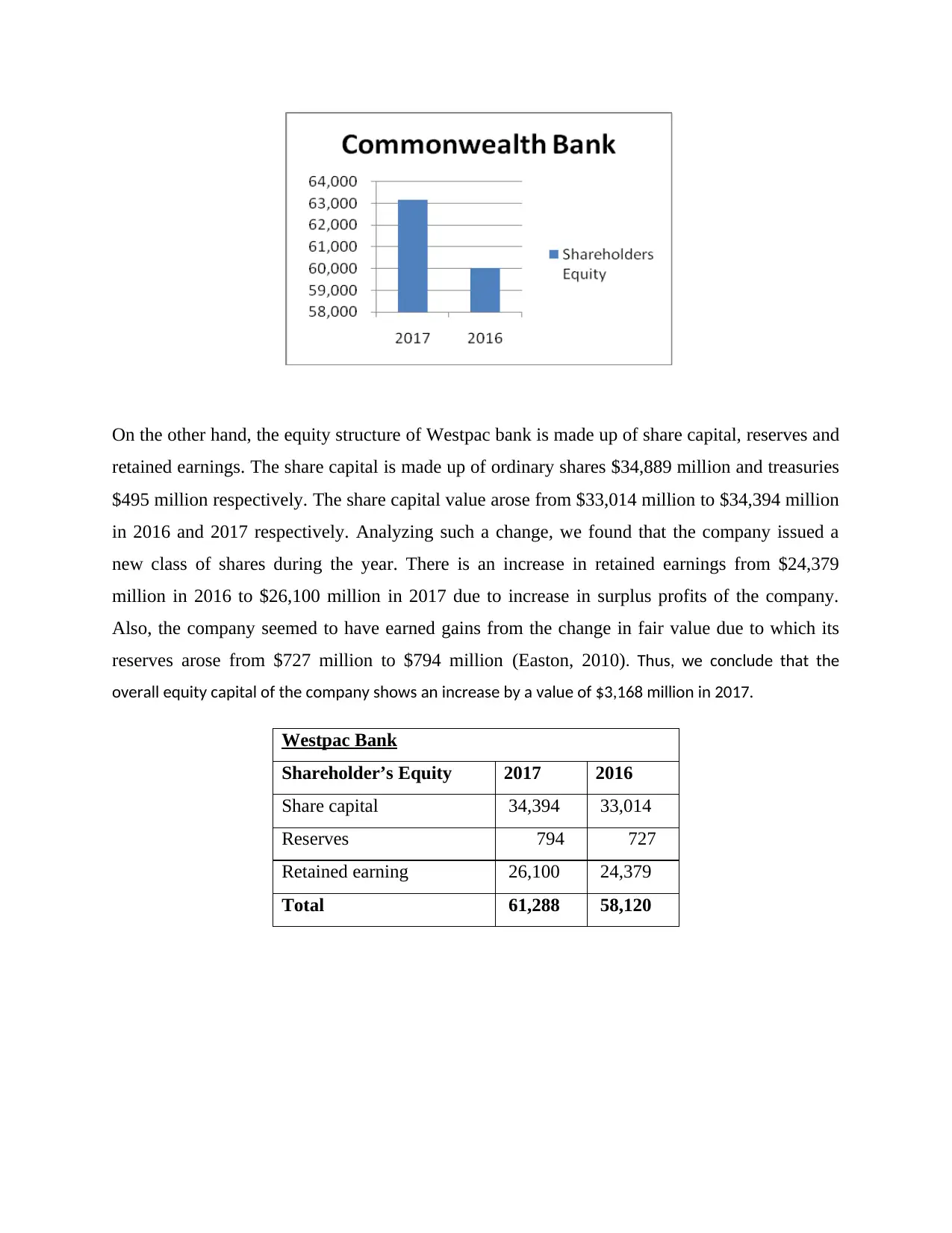

the equity value arose from $60,014 million to $63,170 million in 2016 and 2017 respectively.

Commonwealth Bank

Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves 1,869 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

The equity of a company reflects its capital structure, that is, the monies on which the business is

based upon. In case of company, this equity structure is formed through investments made by

shareholders or investors (Berry, 2009). Such holders get shares of the company in return. Equity

structure includes shares such as equity shares, preference shares, right shares, etc. Retained

earnings and surpluses or deficits are also included for the calculation of the total equity of a

company.

DISCUSSION ABOUT EACH EQUITY ITEM

Our analysis discusses about the equity portion of two past years of both the companies.

Commonwealth bank has both ordinary and treasury shares with values $35,266 million and

$295 million respectively which sums up as $34,971 million as per 2017. The 2016 data gives

the capital value as $33,845 million. Thus, we see an increase in the equity value in 2017.

Analyzing the reason behind it, this increase was because of issuance of shares under dividend

reinvestment plan during the year. The balance in retained earnings account arose from $23,435

million to $26,330 million which was because of surplus profits earned by the company during

the previous year (Boyd, 2013). However, there is a decline in the reserves balance due to

foreign exchange fluctuations as well due to loss on sale of investments. Thus, we conclude that

the equity value arose from $60,014 million to $63,170 million in 2016 and 2017 respectively.

Commonwealth Bank

Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves 1,869 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

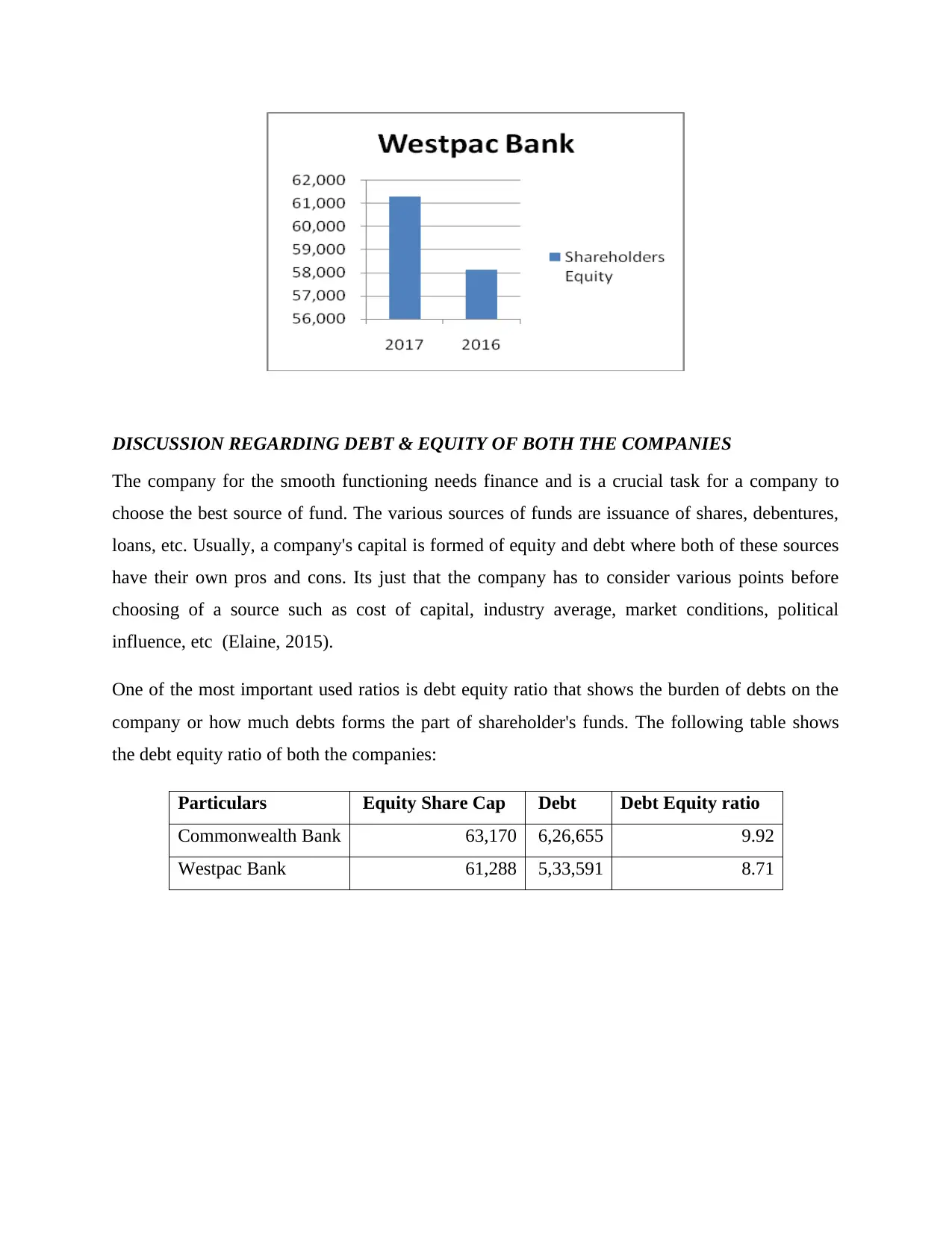

On the other hand, the equity structure of Westpac bank is made up of share capital, reserves and

retained earnings. The share capital is made up of ordinary shares $34,889 million and treasuries

$495 million respectively. The share capital value arose from $33,014 million to $34,394 million

in 2016 and 2017 respectively. Analyzing such a change, we found that the company issued a

new class of shares during the year. There is an increase in retained earnings from $24,379

million in 2016 to $26,100 million in 2017 due to increase in surplus profits of the company.

Also, the company seemed to have earned gains from the change in fair value due to which its

reserves arose from $727 million to $794 million (Easton, 2010). Thus, we conclude that the

overall equity capital of the company shows an increase by a value of $3,168 million in 2017.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves 794 727

Retained earning 26,100 24,379

Total 61,288 58,120

retained earnings. The share capital is made up of ordinary shares $34,889 million and treasuries

$495 million respectively. The share capital value arose from $33,014 million to $34,394 million

in 2016 and 2017 respectively. Analyzing such a change, we found that the company issued a

new class of shares during the year. There is an increase in retained earnings from $24,379

million in 2016 to $26,100 million in 2017 due to increase in surplus profits of the company.

Also, the company seemed to have earned gains from the change in fair value due to which its

reserves arose from $727 million to $794 million (Easton, 2010). Thus, we conclude that the

overall equity capital of the company shows an increase by a value of $3,168 million in 2017.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves 794 727

Retained earning 26,100 24,379

Total 61,288 58,120

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DISCUSSION REGARDING DEBT & EQUITY OF BOTH THE COMPANIES

The company for the smooth functioning needs finance and is a crucial task for a company to

choose the best source of fund. The various sources of funds are issuance of shares, debentures,

loans, etc. Usually, a company's capital is formed of equity and debt where both of these sources

have their own pros and cons. Its just that the company has to consider various points before

choosing of a source such as cost of capital, industry average, market conditions, political

influence, etc (Elaine, 2015).

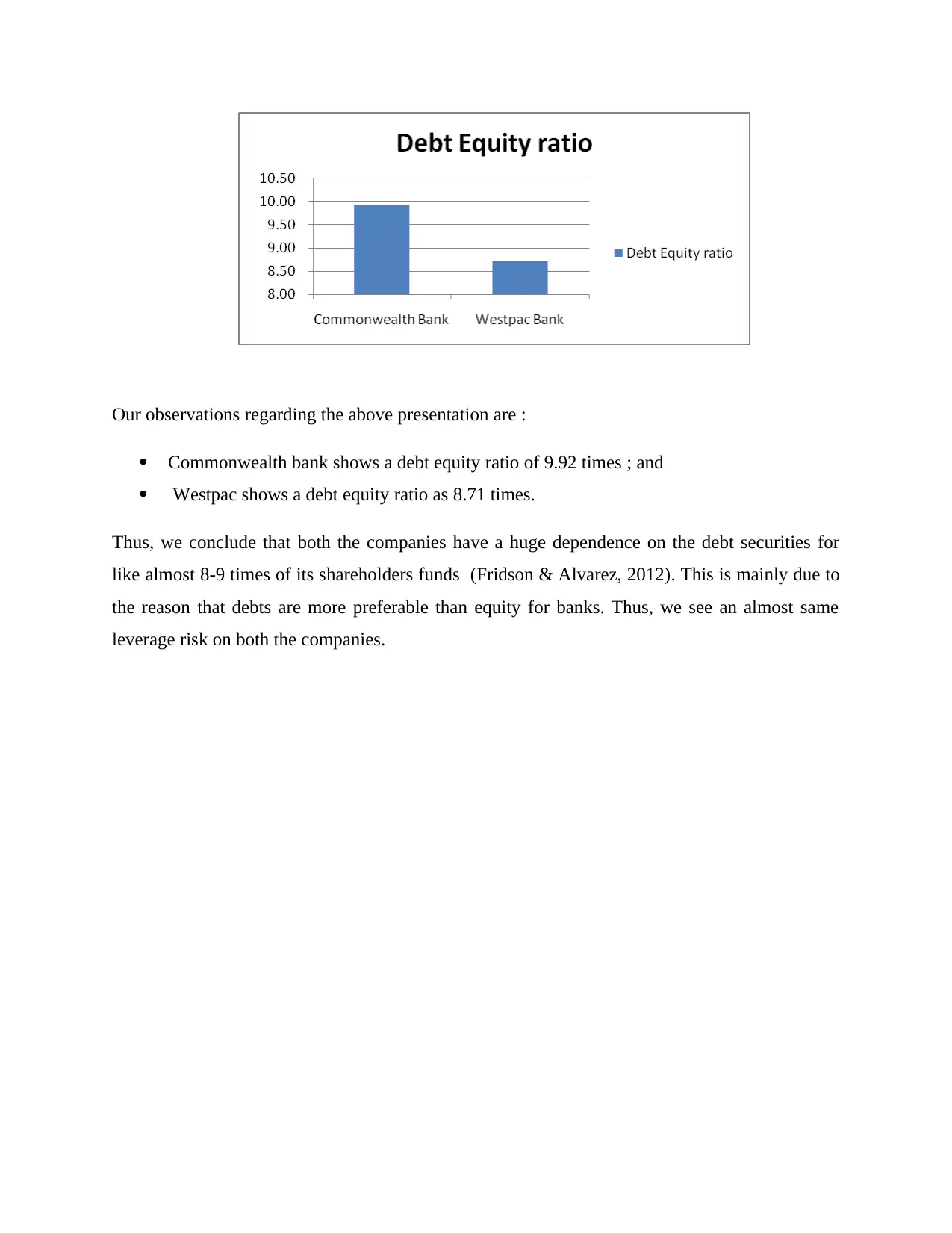

One of the most important used ratios is debt equity ratio that shows the burden of debts on the

company or how much debts forms the part of shareholder's funds. The following table shows

the debt equity ratio of both the companies:

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank 63,170 6,26,655 9.92

Westpac Bank 61,288 5,33,591 8.71

The company for the smooth functioning needs finance and is a crucial task for a company to

choose the best source of fund. The various sources of funds are issuance of shares, debentures,

loans, etc. Usually, a company's capital is formed of equity and debt where both of these sources

have their own pros and cons. Its just that the company has to consider various points before

choosing of a source such as cost of capital, industry average, market conditions, political

influence, etc (Elaine, 2015).

One of the most important used ratios is debt equity ratio that shows the burden of debts on the

company or how much debts forms the part of shareholder's funds. The following table shows

the debt equity ratio of both the companies:

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank 63,170 6,26,655 9.92

Westpac Bank 61,288 5,33,591 8.71

Our observations regarding the above presentation are :

Commonwealth bank shows a debt equity ratio of 9.92 times ; and

Westpac shows a debt equity ratio as 8.71 times.

Thus, we conclude that both the companies have a huge dependence on the debt securities for

like almost 8-9 times of its shareholders funds (Fridson & Alvarez, 2012). This is mainly due to

the reason that debts are more preferable than equity for banks. Thus, we see an almost same

leverage risk on both the companies.

Commonwealth bank shows a debt equity ratio of 9.92 times ; and

Westpac shows a debt equity ratio as 8.71 times.

Thus, we conclude that both the companies have a huge dependence on the debt securities for

like almost 8-9 times of its shareholders funds (Fridson & Alvarez, 2012). This is mainly due to

the reason that debts are more preferable than equity for banks. Thus, we see an almost same

leverage risk on both the companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ANALYSIS OF CASH FLOW STATEMENT

There are two basis for recording of accounting information, either on the accrual basis or on the

cash basis. Where the books are usually prepared on the accrual basis, cash flow statement are

prepared on the cash basis as its main purpose is to reflect the actual cash inflow or outflow. This

helps in letting the stakeholders know about the liquidity position of a company (Girard, 2014).

DISCUSSION REGARDING CASH FLOW STATEMENT

Three activities together form the cash flow statement that is, operating activities, investing

activities and financing activities. In case of Commonwealth bank:

Operating activities include incomes from investment; payment of interests, etc as

interest receipt and payment are the main activities of a banking company (Jensen &

Meckling, 1976).

Investing activities shows the outflow of cash due to acquiring of subsidiaries or

associates, investments, tangible assets and inflow of cash due to dividend income.

Financing activities are composed of receipts due to issuance of debts, issuance of equity

shares and repayments of respective funds.

Analyzing the cash flow statement of Commonwealth bank, we see an outflow of cash in

operating activities, that is, $4,561 million and $807 million in 2016 and 2017. There is decline

in the outflow due to having incomes from investments and interest receipts. In a similar way, we

see a decrease in outflow of cash in case of investing activities, that is, $677 million and $2,032

million in 2017 and 2016. Such a decrease is as a result of nonpayment of purchased entities

which are under control, decrease in purchases of plant, property and equipment including

intangible assets. However, we see an increase in financing activities which is because the

company made fewer payments during redemption of debt securities (Lyon, 2010).

Thus, we conclude that the company shows a drastic change as it had negative balance in 2016,

$4,973 million which is now $8,988 million in 2017.

In case of Westpac bank :

There are two basis for recording of accounting information, either on the accrual basis or on the

cash basis. Where the books are usually prepared on the accrual basis, cash flow statement are

prepared on the cash basis as its main purpose is to reflect the actual cash inflow or outflow. This

helps in letting the stakeholders know about the liquidity position of a company (Girard, 2014).

DISCUSSION REGARDING CASH FLOW STATEMENT

Three activities together form the cash flow statement that is, operating activities, investing

activities and financing activities. In case of Commonwealth bank:

Operating activities include incomes from investment; payment of interests, etc as

interest receipt and payment are the main activities of a banking company (Jensen &

Meckling, 1976).

Investing activities shows the outflow of cash due to acquiring of subsidiaries or

associates, investments, tangible assets and inflow of cash due to dividend income.

Financing activities are composed of receipts due to issuance of debts, issuance of equity

shares and repayments of respective funds.

Analyzing the cash flow statement of Commonwealth bank, we see an outflow of cash in

operating activities, that is, $4,561 million and $807 million in 2016 and 2017. There is decline

in the outflow due to having incomes from investments and interest receipts. In a similar way, we

see a decrease in outflow of cash in case of investing activities, that is, $677 million and $2,032

million in 2017 and 2016. Such a decrease is as a result of nonpayment of purchased entities

which are under control, decrease in purchases of plant, property and equipment including

intangible assets. However, we see an increase in financing activities which is because the

company made fewer payments during redemption of debt securities (Lyon, 2010).

Thus, we conclude that the company shows a drastic change as it had negative balance in 2016,

$4,973 million which is now $8,988 million in 2017.

In case of Westpac bank :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The income from insurances, interest receipts and income tax together forms the

operating activities.

Investing activities are composed of sales and purchases of subsidiaries or associates,

fixed assets, investments and other securities.

Repayment and revenues of and from debts and equity together forms financing

activities.

Analyzing the cash flow statement of Westpac bank, we see that the cash outflow has decreased

in the operating activities, that is, from $5,497 million to $2,820 million in 2016 and 2017

respectively. This is due to the company have losses from fair value measurement of

investments. In case of investing activities, a decline is seen in outflow of cash as it was $7,245

million in 2016 and $1,698 million in 2017. This is because the company made sales of securities

and associates during the year. In case of financing activities, we again see that there is a drastic

decrease in cash inflows in 2017 as compared to 2016 cash inflows by a value of $4,021 million.

This happened due to increase in cash outflows while redeeming loans and issuance of debt

securities in lower quantities (McLaney & Adril, 2016).

Overall, we see a decrease of $1,151 million in the net cash flow in the year 2017.

COMPARISON OF CASH FLOW OF BOTH THE COMPANIES FOR THE PAST 3 YEARS

Let us have a view on the below table and charts for a better understanding of cash flow

statement of both the companies (Parrino, 2013):

Operating Activities

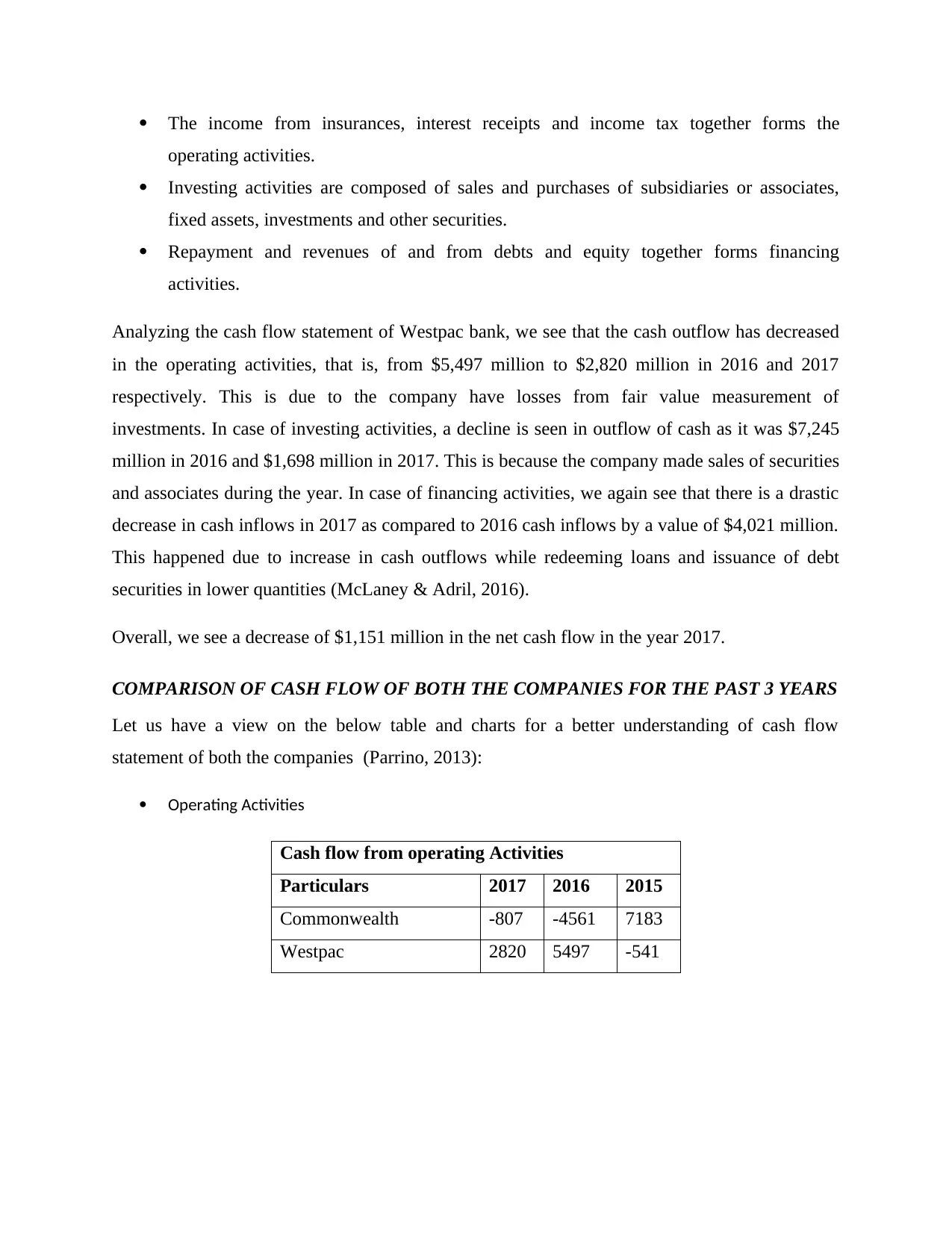

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

operating activities.

Investing activities are composed of sales and purchases of subsidiaries or associates,

fixed assets, investments and other securities.

Repayment and revenues of and from debts and equity together forms financing

activities.

Analyzing the cash flow statement of Westpac bank, we see that the cash outflow has decreased

in the operating activities, that is, from $5,497 million to $2,820 million in 2016 and 2017

respectively. This is due to the company have losses from fair value measurement of

investments. In case of investing activities, a decline is seen in outflow of cash as it was $7,245

million in 2016 and $1,698 million in 2017. This is because the company made sales of securities

and associates during the year. In case of financing activities, we again see that there is a drastic

decrease in cash inflows in 2017 as compared to 2016 cash inflows by a value of $4,021 million.

This happened due to increase in cash outflows while redeeming loans and issuance of debt

securities in lower quantities (McLaney & Adril, 2016).

Overall, we see a decrease of $1,151 million in the net cash flow in the year 2017.

COMPARISON OF CASH FLOW OF BOTH THE COMPANIES FOR THE PAST 3 YEARS

Let us have a view on the below table and charts for a better understanding of cash flow

statement of both the companies (Parrino, 2013):

Operating Activities

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

The operating activities of both the companies do not show any trend in the values.

Investing Activities

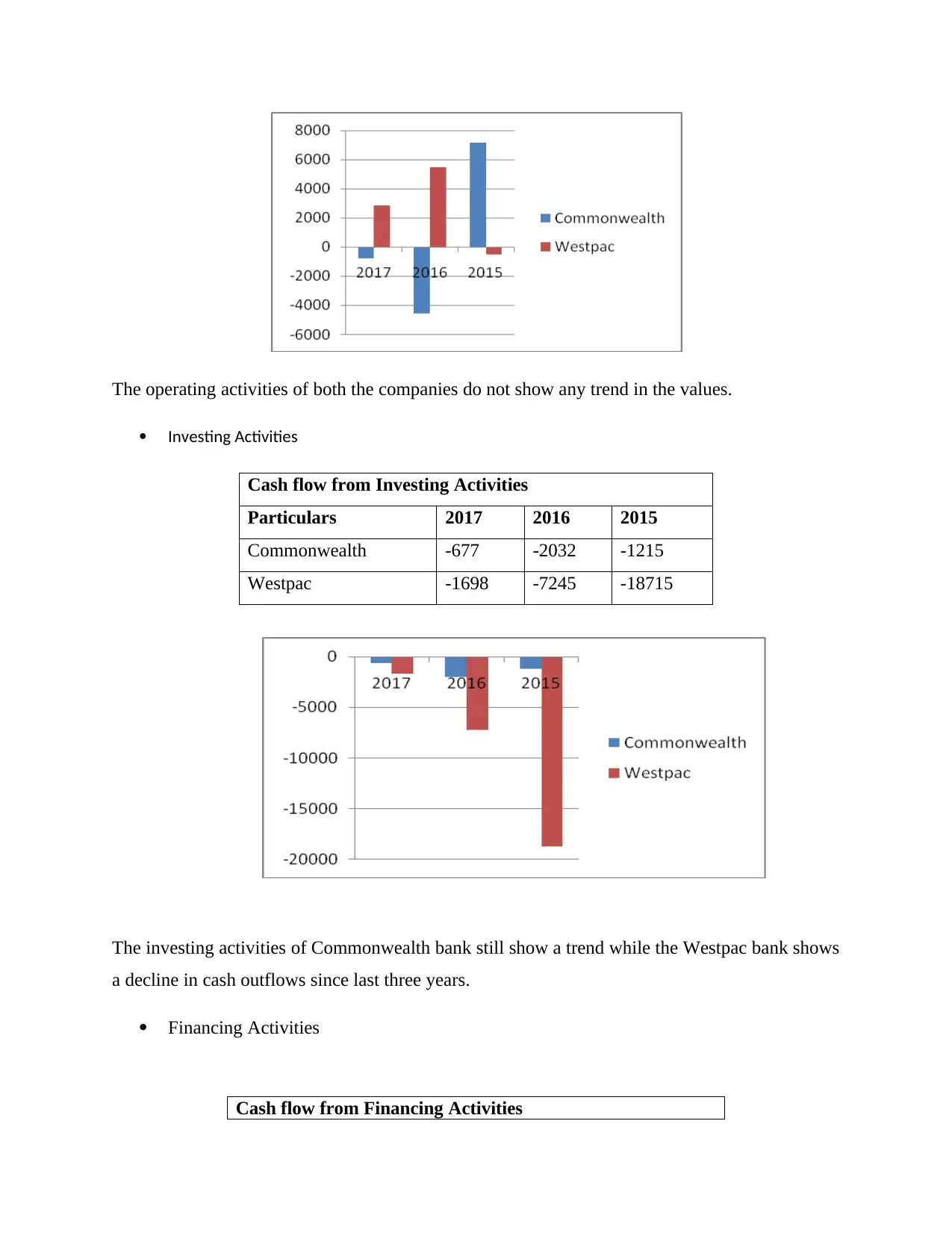

Cash flow from Investing Activities

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac -1698 -7245 -18715

The investing activities of Commonwealth bank still show a trend while the Westpac bank shows

a decline in cash outflows since last three years.

Financing Activities

Cash flow from Financing Activities

Investing Activities

Cash flow from Investing Activities

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac -1698 -7245 -18715

The investing activities of Commonwealth bank still show a trend while the Westpac bank shows

a decline in cash outflows since last three years.

Financing Activities

Cash flow from Financing Activities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.