Comparative Analysis: Exploring IFRS and GAAP Accounting Standards

VerifiedAdded on 2023/06/13

|6

|1352

|263

Report

AI Summary

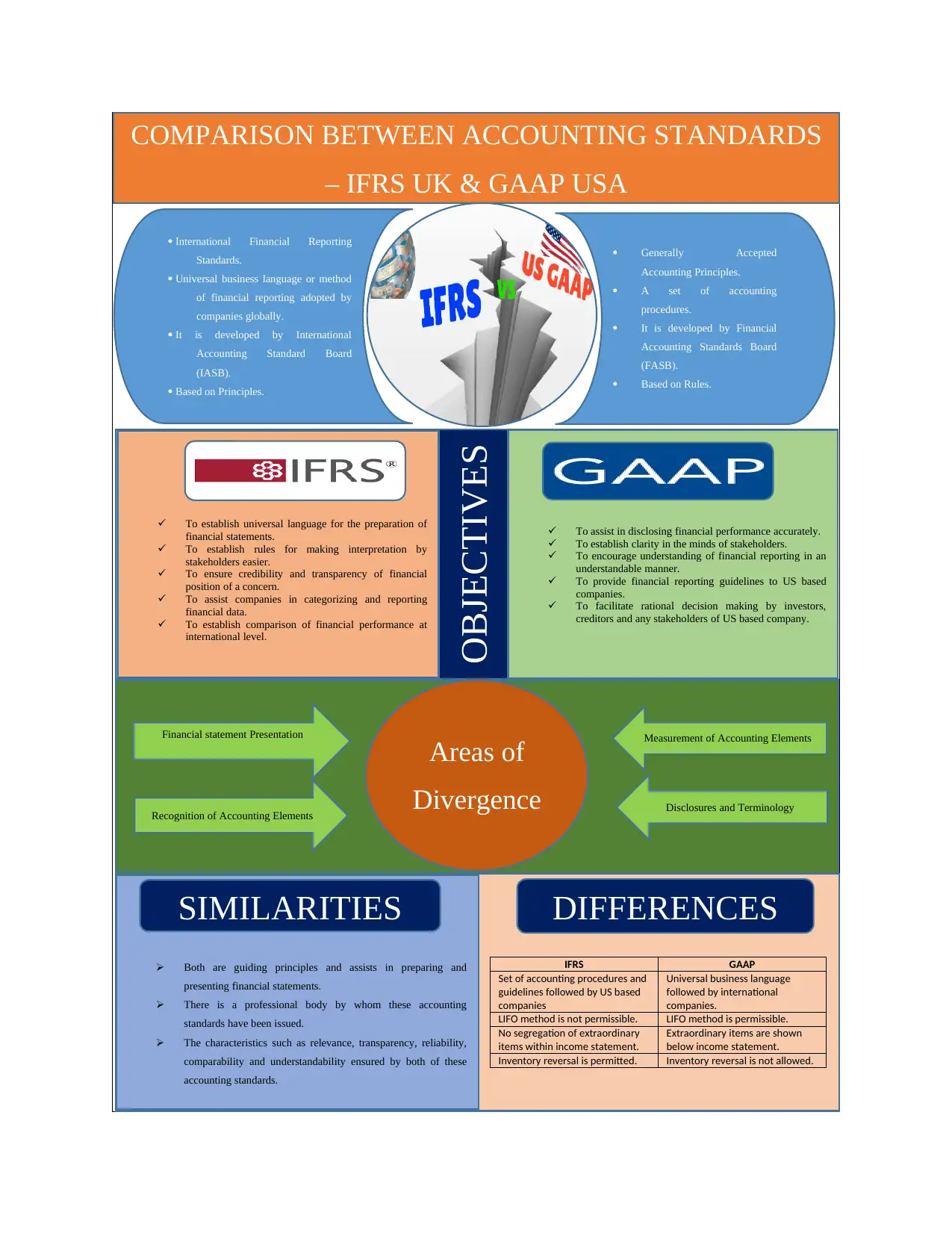

This report provides a detailed comparison between International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), focusing on their objectives, similarities, and areas of divergence. IFRS aims to establish a universal language for financial reporting, ensuring transparency and comparability across international companies, while GAAP provides specific guidelines for US-based companies. The report highlights differences in financial statement presentation, recognition of accounting elements, measurement of accounting elements (such as inventory valuation), and disclosures, including the treatment of extraordinary items. Despite these differences, both IFRS and GAAP serve as guiding principles for financial reporting, promoting reliability, transparency, and comparability. The report references several studies to support its analysis of the key distinctions and commonalities between these two major accounting standards. Desklib provides more resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.