Detailed Analysis of Job Costing System for Turramurra Furniture

VerifiedAdded on 2020/06/05

|9

|2508

|64

Report

AI Summary

This report provides a comprehensive analysis of the job costing system at Turramurra Furniture. It begins with an introduction to accounting and the suitability of job costing for the company. The report then delves into specific calculations, including determining the work-in-progress (WIP) at the end of June 2017 and calculating the cost of chairs in the finished inventory. A significant portion of the report is dedicated to computing over or under-applied overhead for the year, with detailed calculations and interpretations. The report suggests corrective measures for over-applied overhead and discusses the appropriate approach for adjusting the over or under-application of overhead. Finally, it assesses the suitability of activity-based budgeting (ABB) for Turramurra Furniture, outlining the advantages and disadvantages of adopting this technique. The report concludes with a summary of the key findings and recommendations.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

A). Describing situation where job costing system proves to be suitable..............................1

B). Determining work-in-progress of Turramurra Furniture at 30th June 2017......................2

C). Calculating cost of chairs in the finished inventory.........................................................2

D): Computing over or under applied overhead for the period of one year...........................3

E. Suggesting corrective measure for the situation of over-applied overhead.......................4

F. Stating approach that company should use to adjust the over or under application of

overhead.................................................................................................................................5

G. Suggesting Turramurra Furniture whether it should undertake activity based budgeting

technique or not......................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

A). Describing situation where job costing system proves to be suitable..............................1

B). Determining work-in-progress of Turramurra Furniture at 30th June 2017......................2

C). Calculating cost of chairs in the finished inventory.........................................................2

D): Computing over or under applied overhead for the period of one year...........................3

E. Suggesting corrective measure for the situation of over-applied overhead.......................4

F. Stating approach that company should use to adjust the over or under application of

overhead.................................................................................................................................5

G. Suggesting Turramurra Furniture whether it should undertake activity based budgeting

technique or not......................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Accounting is the tool which is used by each and every company for having systematic

records of all transactions. There is a strong need to adopt the systematic accounting reporting

standards by organisations so that they can be safeguard from prosecution. This is the only tool

by which a company could get sustainable development. The present report is based on

Turramurra Furniture which will provide deeper insight about the situations in which the system

of job costing needs to be undertaken. Besides this, it will shed light on the concept or aspects

under and over applied overhead. Further, report also depicts the manner in which activity based

costing technique helps in taking suitable decision regarding cost.

TASK

A). Describing situation where job costing system proves to be suitable

Job order costing is a normal way that been used by company producing diverse range of

products. This is one among mostly implemented system of costing in production area and is also

used in service industry. Mostly, production organisation implementes job order costing with a

motive to achieve orders for customised goods and services. These customized orders are also

known as jobs or batches. For example, A clothing company might attain an order for men shirts

with specific size, colour, and design.

When Turramurra Furniture Company accept jobs for diverse goods, the assignment of cost

to goods become a complicated task. Under these situations, cost record for every individual job

is kept as each job has a diverse good and henceforth, diverse costs is linked to it.

Per unit cost of a specific job is calculated by dividing the total cost allocated by number of

units under. Per unit cost formula is provided as below:

Per unit cost= Total cost applicable to job/ Number of units in the job

Job order costing is mostly implemented by organisations all around the globe. A job cost

sheet segregate production projects into three types of costs. These are direct material, direct

labour and manufacturing overheads. Direct material is related to the material required to

produce the project. Direct labour is the amount of the manpower cost which is implemented to

fulfil the project (Mu, Jiang and Leng, 2017). Manufacturing overheads are the third one which

is the indirect costs connected to manufacturing of goods.

1

Accounting is the tool which is used by each and every company for having systematic

records of all transactions. There is a strong need to adopt the systematic accounting reporting

standards by organisations so that they can be safeguard from prosecution. This is the only tool

by which a company could get sustainable development. The present report is based on

Turramurra Furniture which will provide deeper insight about the situations in which the system

of job costing needs to be undertaken. Besides this, it will shed light on the concept or aspects

under and over applied overhead. Further, report also depicts the manner in which activity based

costing technique helps in taking suitable decision regarding cost.

TASK

A). Describing situation where job costing system proves to be suitable

Job order costing is a normal way that been used by company producing diverse range of

products. This is one among mostly implemented system of costing in production area and is also

used in service industry. Mostly, production organisation implementes job order costing with a

motive to achieve orders for customised goods and services. These customized orders are also

known as jobs or batches. For example, A clothing company might attain an order for men shirts

with specific size, colour, and design.

When Turramurra Furniture Company accept jobs for diverse goods, the assignment of cost

to goods become a complicated task. Under these situations, cost record for every individual job

is kept as each job has a diverse good and henceforth, diverse costs is linked to it.

Per unit cost of a specific job is calculated by dividing the total cost allocated by number of

units under. Per unit cost formula is provided as below:

Per unit cost= Total cost applicable to job/ Number of units in the job

Job order costing is mostly implemented by organisations all around the globe. A job cost

sheet segregate production projects into three types of costs. These are direct material, direct

labour and manufacturing overheads. Direct material is related to the material required to

produce the project. Direct labour is the amount of the manpower cost which is implemented to

fulfil the project (Mu, Jiang and Leng, 2017). Manufacturing overheads are the third one which

is the indirect costs connected to manufacturing of goods.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

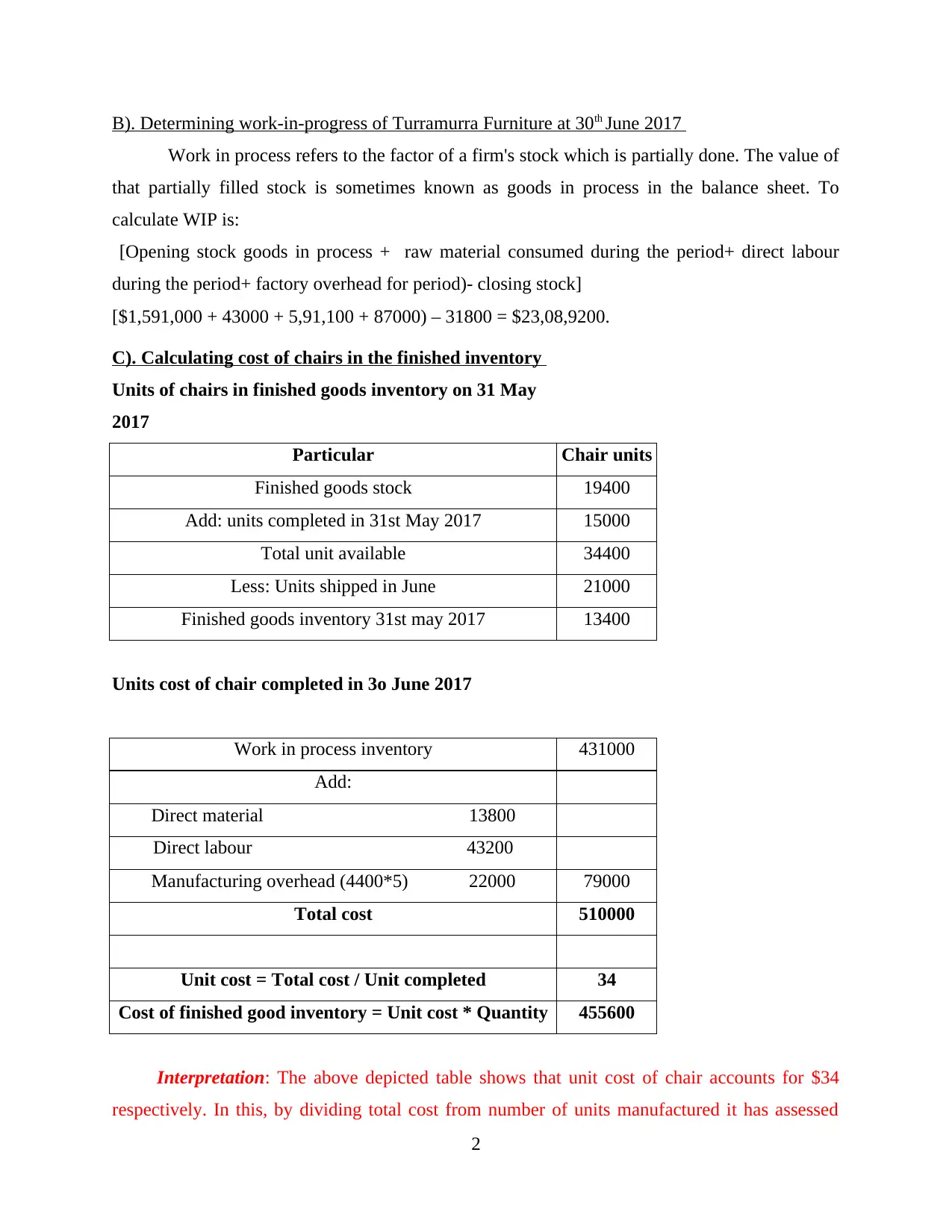

B). Determining work-in-progress of Turramurra Furniture at 30th June 2017

Work in process refers to the factor of a firm's stock which is partially done. The value of

that partially filled stock is sometimes known as goods in process in the balance sheet. To

calculate WIP is:

[Opening stock goods in process + raw material consumed during the period+ direct labour

during the period+ factory overhead for period)- closing stock]

[$1,591,000 + 43000 + 5,91,100 + 87000) – 31800 = $23,08,9200.

C). Calculating cost of chairs in the finished inventory

Units of chairs in finished goods inventory on 31 May

2017

Particular Chair units

Finished goods stock 19400

Add: units completed in 31st May 2017 15000

Total unit available 34400

Less: Units shipped in June 21000

Finished goods inventory 31st may 2017 13400

Units cost of chair completed in 3o June 2017

Work in process inventory 431000

Add:

Direct material 13800

Direct labour 43200

Manufacturing overhead (4400*5) 22000 79000

Total cost 510000

Unit cost = Total cost / Unit completed 34

Cost of finished good inventory = Unit cost * Quantity 455600

Interpretation: The above depicted table shows that unit cost of chair accounts for $34

respectively. In this, by dividing total cost from number of units manufactured it has assessed

2

Work in process refers to the factor of a firm's stock which is partially done. The value of

that partially filled stock is sometimes known as goods in process in the balance sheet. To

calculate WIP is:

[Opening stock goods in process + raw material consumed during the period+ direct labour

during the period+ factory overhead for period)- closing stock]

[$1,591,000 + 43000 + 5,91,100 + 87000) – 31800 = $23,08,9200.

C). Calculating cost of chairs in the finished inventory

Units of chairs in finished goods inventory on 31 May

2017

Particular Chair units

Finished goods stock 19400

Add: units completed in 31st May 2017 15000

Total unit available 34400

Less: Units shipped in June 21000

Finished goods inventory 31st may 2017 13400

Units cost of chair completed in 3o June 2017

Work in process inventory 431000

Add:

Direct material 13800

Direct labour 43200

Manufacturing overhead (4400*5) 22000 79000

Total cost 510000

Unit cost = Total cost / Unit completed 34

Cost of finished good inventory = Unit cost * Quantity 455600

Interpretation: The above depicted table shows that unit cost of chair accounts for $34

respectively. In this, by dividing total cost from number of units manufactured it has assessed

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

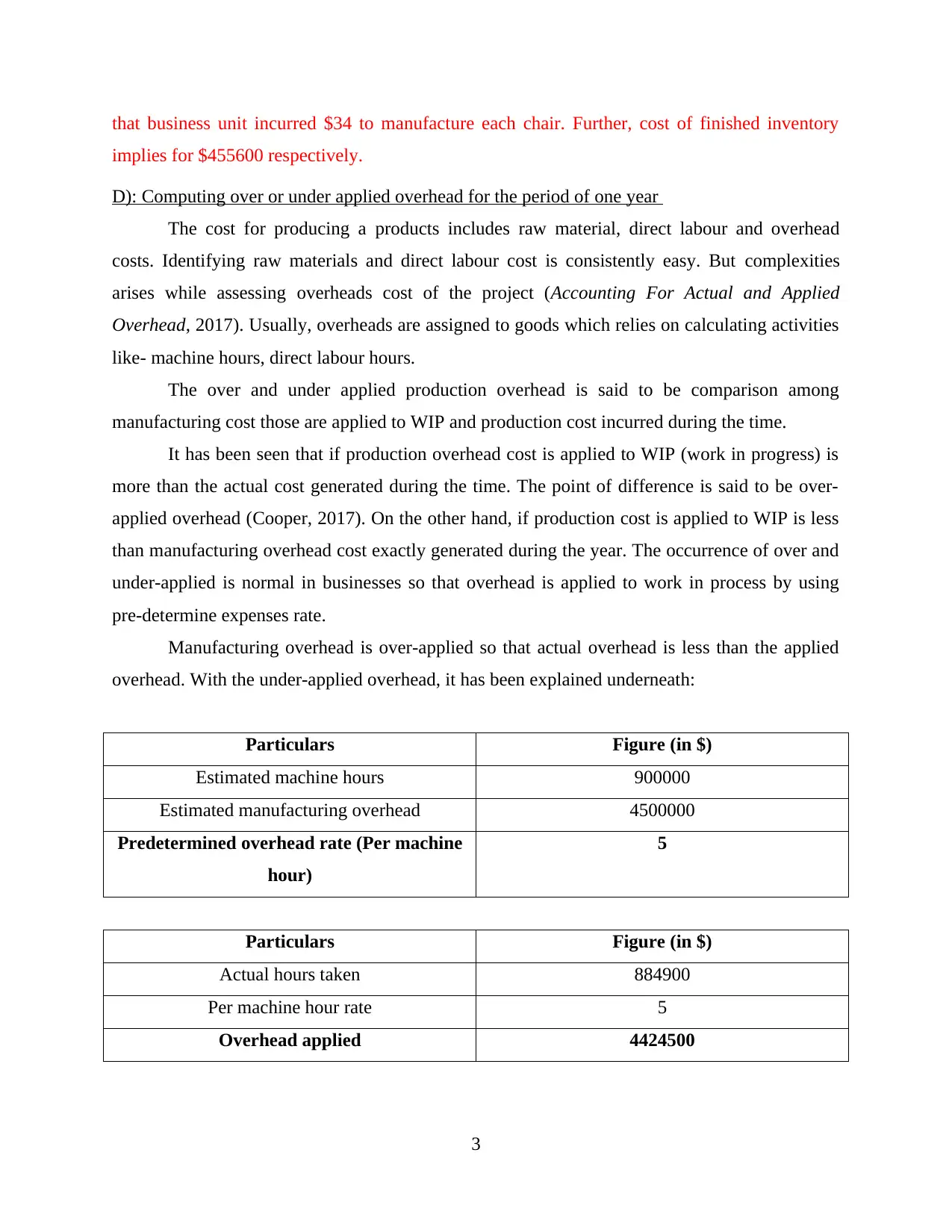

that business unit incurred $34 to manufacture each chair. Further, cost of finished inventory

implies for $455600 respectively.

D): Computing over or under applied overhead for the period of one year

The cost for producing a products includes raw material, direct labour and overhead

costs. Identifying raw materials and direct labour cost is consistently easy. But complexities

arises while assessing overheads cost of the project (Accounting For Actual and Applied

Overhead, 2017). Usually, overheads are assigned to goods which relies on calculating activities

like- machine hours, direct labour hours.

The over and under applied production overhead is said to be comparison among

manufacturing cost those are applied to WIP and production cost incurred during the time.

It has been seen that if production overhead cost is applied to WIP (work in progress) is

more than the actual cost generated during the time. The point of difference is said to be over-

applied overhead (Cooper, 2017). On the other hand, if production cost is applied to WIP is less

than manufacturing overhead cost exactly generated during the year. The occurrence of over and

under-applied is normal in businesses so that overhead is applied to work in process by using

pre-determine expenses rate.

Manufacturing overhead is over-applied so that actual overhead is less than the applied

overhead. With the under-applied overhead, it has been explained underneath:

Particulars Figure (in $)

Estimated machine hours 900000

Estimated manufacturing overhead 4500000

Predetermined overhead rate (Per machine

hour)

5

Particulars Figure (in $)

Actual hours taken 884900

Per machine hour rate 5

Overhead applied 4424500

3

implies for $455600 respectively.

D): Computing over or under applied overhead for the period of one year

The cost for producing a products includes raw material, direct labour and overhead

costs. Identifying raw materials and direct labour cost is consistently easy. But complexities

arises while assessing overheads cost of the project (Accounting For Actual and Applied

Overhead, 2017). Usually, overheads are assigned to goods which relies on calculating activities

like- machine hours, direct labour hours.

The over and under applied production overhead is said to be comparison among

manufacturing cost those are applied to WIP and production cost incurred during the time.

It has been seen that if production overhead cost is applied to WIP (work in progress) is

more than the actual cost generated during the time. The point of difference is said to be over-

applied overhead (Cooper, 2017). On the other hand, if production cost is applied to WIP is less

than manufacturing overhead cost exactly generated during the year. The occurrence of over and

under-applied is normal in businesses so that overhead is applied to work in process by using

pre-determine expenses rate.

Manufacturing overhead is over-applied so that actual overhead is less than the applied

overhead. With the under-applied overhead, it has been explained underneath:

Particulars Figure (in $)

Estimated machine hours 900000

Estimated manufacturing overhead 4500000

Predetermined overhead rate (Per machine

hour)

5

Particulars Figure (in $)

Actual hours taken 884900

Per machine hour rate 5

Overhead applied 4424500

3

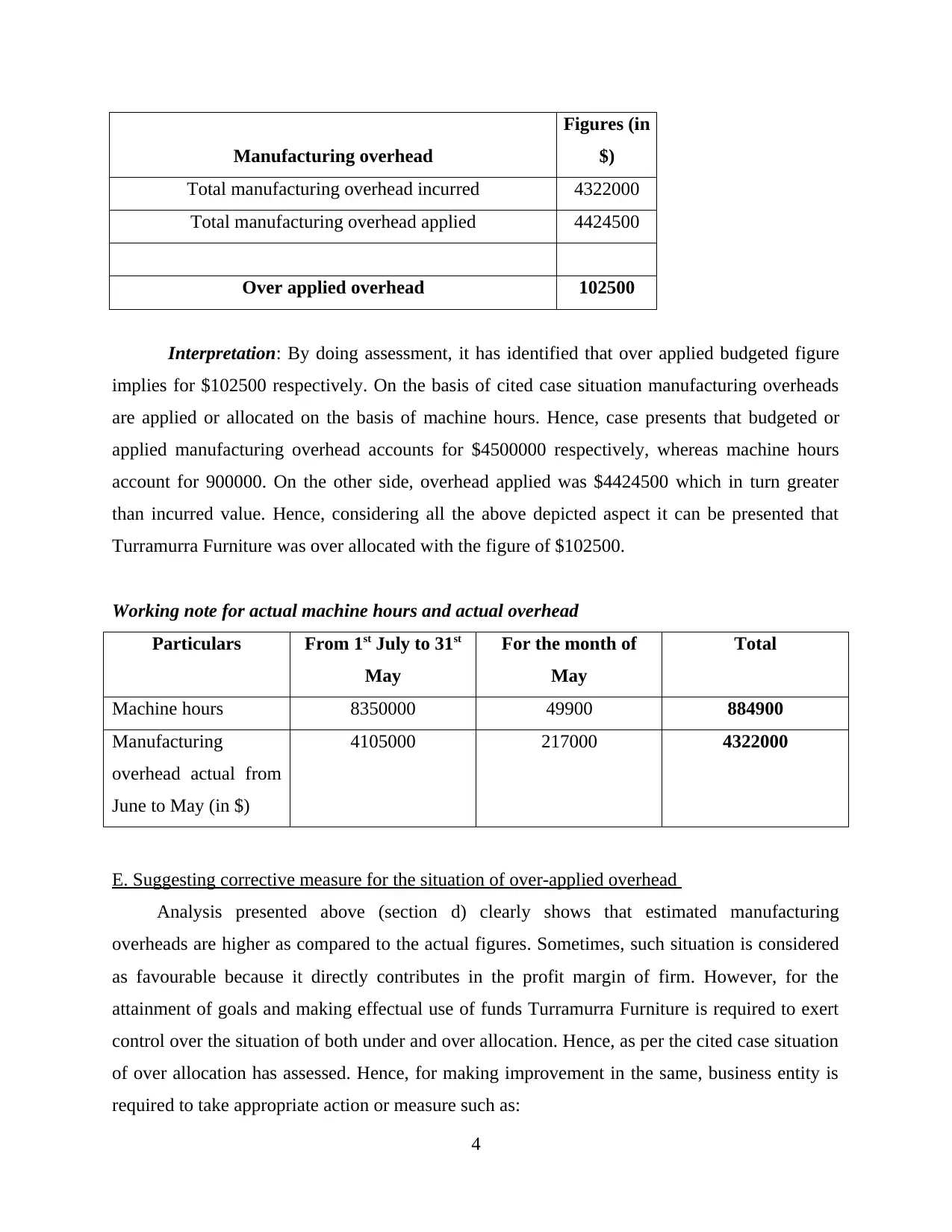

Manufacturing overhead

Figures (in

$)

Total manufacturing overhead incurred 4322000

Total manufacturing overhead applied 4424500

Over applied overhead 102500

Interpretation: By doing assessment, it has identified that over applied budgeted figure

implies for $102500 respectively. On the basis of cited case situation manufacturing overheads

are applied or allocated on the basis of machine hours. Hence, case presents that budgeted or

applied manufacturing overhead accounts for $4500000 respectively, whereas machine hours

account for 900000. On the other side, overhead applied was $4424500 which in turn greater

than incurred value. Hence, considering all the above depicted aspect it can be presented that

Turramurra Furniture was over allocated with the figure of $102500.

Working note for actual machine hours and actual overhead

Particulars From 1st July to 31st

May

For the month of

May

Total

Machine hours 8350000 49900 884900

Manufacturing

overhead actual from

June to May (in $)

4105000 217000 4322000

E. Suggesting corrective measure for the situation of over-applied overhead

Analysis presented above (section d) clearly shows that estimated manufacturing

overheads are higher as compared to the actual figures. Sometimes, such situation is considered

as favourable because it directly contributes in the profit margin of firm. However, for the

attainment of goals and making effectual use of funds Turramurra Furniture is required to exert

control over the situation of both under and over allocation. Hence, as per the cited case situation

of over allocation has assessed. Hence, for making improvement in the same, business entity is

required to take appropriate action or measure such as:

4

Figures (in

$)

Total manufacturing overhead incurred 4322000

Total manufacturing overhead applied 4424500

Over applied overhead 102500

Interpretation: By doing assessment, it has identified that over applied budgeted figure

implies for $102500 respectively. On the basis of cited case situation manufacturing overheads

are applied or allocated on the basis of machine hours. Hence, case presents that budgeted or

applied manufacturing overhead accounts for $4500000 respectively, whereas machine hours

account for 900000. On the other side, overhead applied was $4424500 which in turn greater

than incurred value. Hence, considering all the above depicted aspect it can be presented that

Turramurra Furniture was over allocated with the figure of $102500.

Working note for actual machine hours and actual overhead

Particulars From 1st July to 31st

May

For the month of

May

Total

Machine hours 8350000 49900 884900

Manufacturing

overhead actual from

June to May (in $)

4105000 217000 4322000

E. Suggesting corrective measure for the situation of over-applied overhead

Analysis presented above (section d) clearly shows that estimated manufacturing

overheads are higher as compared to the actual figures. Sometimes, such situation is considered

as favourable because it directly contributes in the profit margin of firm. However, for the

attainment of goals and making effectual use of funds Turramurra Furniture is required to exert

control over the situation of both under and over allocation. Hence, as per the cited case situation

of over allocation has assessed. Hence, for making improvement in the same, business entity is

required to take appropriate action or measure such as:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lays emphasis on the adoption of suitable and modern budgeting techniques such as Zero

base (ZBB), activity based (ABB) financial framework. This in turn facilitates optimum

allocation and usage of funds. Turramurra Furniture comes under the category of

manufacturing firms so it should follow ABB technique for the purpose of evaluation.

Along with this, business unit should consider or evaluate the reasons associated with the

aspect of over applied. By keeping such aspects in mind business unit would become able

to set suitable framework regarding cost allocation.

F. Stating approach that company should use to adjust the over or under application of overhead

Concerned case situation presents that if situation of over or under applied occurs with

the amount of $40000 then accountant needs to write off such figure to cost of goods sold.

Hence, on the basis of such approach, by apportioning the figure of under and over applied in

ending balance of COGS, WIP and finished goods inventory Turramurra Furniture can deal with

such situation. Thus, by undertaking one method out of such two alternatives available business

unit can adjust the figure of under and over applied.

G. Suggesting Turramurra Furniture whether it should undertake activity based budgeting

technique or not

Give case summary of Turramurra Furniture presents that it is highly concerned in relation

to the application of overhead and costing aspects. Further, cited case also presents that owner of

the furniture company is planning to explore its product range and concerned pertaining to

overhead application. Hence, considering the business aspect and organization concern it is

suggested to the management team to lay high level of emphasis on employing the technique of

activity based costing (Braun, 2013). Such technique highly suits to the modern era and offer

assistance to the business unit specifically the one which is involved in manufacturing aspects.

Thus, Turramurra Furniture should adopt ABB tool for assigning indirect cost or overheads.

Moreover, such method primarily focuses on recognizing relationship which takes place

between cost, activities and products. In other words, it can be stated that it is a highly logical

way which tends to focus on allocating overheads on the basis of items they actually use it. By

using such budgeting system or method Turramurra Furniture can reduce the level of targeted

overhead cost. Hence, as per such method overhead costs are allocated on the basis of cost pool

and relevant drivers. Thus, such method of budgeting is highly effective which in turn assists in

avoiding the issue of over and under allocation of overheads.

5

base (ZBB), activity based (ABB) financial framework. This in turn facilitates optimum

allocation and usage of funds. Turramurra Furniture comes under the category of

manufacturing firms so it should follow ABB technique for the purpose of evaluation.

Along with this, business unit should consider or evaluate the reasons associated with the

aspect of over applied. By keeping such aspects in mind business unit would become able

to set suitable framework regarding cost allocation.

F. Stating approach that company should use to adjust the over or under application of overhead

Concerned case situation presents that if situation of over or under applied occurs with

the amount of $40000 then accountant needs to write off such figure to cost of goods sold.

Hence, on the basis of such approach, by apportioning the figure of under and over applied in

ending balance of COGS, WIP and finished goods inventory Turramurra Furniture can deal with

such situation. Thus, by undertaking one method out of such two alternatives available business

unit can adjust the figure of under and over applied.

G. Suggesting Turramurra Furniture whether it should undertake activity based budgeting

technique or not

Give case summary of Turramurra Furniture presents that it is highly concerned in relation

to the application of overhead and costing aspects. Further, cited case also presents that owner of

the furniture company is planning to explore its product range and concerned pertaining to

overhead application. Hence, considering the business aspect and organization concern it is

suggested to the management team to lay high level of emphasis on employing the technique of

activity based costing (Braun, 2013). Such technique highly suits to the modern era and offer

assistance to the business unit specifically the one which is involved in manufacturing aspects.

Thus, Turramurra Furniture should adopt ABB tool for assigning indirect cost or overheads.

Moreover, such method primarily focuses on recognizing relationship which takes place

between cost, activities and products. In other words, it can be stated that it is a highly logical

way which tends to focus on allocating overheads on the basis of items they actually use it. By

using such budgeting system or method Turramurra Furniture can reduce the level of targeted

overhead cost. Hence, as per such method overhead costs are allocated on the basis of cost pool

and relevant drivers. Thus, such method of budgeting is highly effective which in turn assists in

avoiding the issue of over and under allocation of overheads.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Turramurra Furniture needs to keep in mind all the benefits and drawbacks which are

associated with activity based costing system before making selection of such budgeting tool or

method:

Advantages

Evaluation: ABB method helps in making evaluation or assessment of overhead on the

basis of cost driver. Hence, by following specific steps Turramurra Furniture would

become able to avoid unnecessary activities from the business.

Competitive edge: By using ABB tool Turramurra Furniture can save cost because it

helps in eliminating all undesirable activities from product line. In this, by reducing cost

firm would become able to offer products to the customers at suitable price. In this way,

ABB technique will assist firm in building and sustain competitive position over others.

Facilitates elimination of bottlenecks: ABB assists in removing all sorts of deficiencies

that prevail in the business activities and thereby streamlines overall operations.

Improves relationship: The main motives of business unit to provide customers with high

quality products at suitable price. In this regard, by using the techniques of ABB firm can

exert control on cost would become able to meet the expectation level of customers.

Drawbacks

Complex and requires high understanding: For setting budget as per such technique and

determining cost Turramurra Furniture requires highly talented personnel. Moreover,

ABB is complex in nature and requires high level of understanding for the purpose of

evaluation.

Resource consumption: In this, for conducting analysis, business entity has to employ

top officials. Along with this, it is highly consuming process and places negative impact

on other operational activities. Moreover, if manager would not become able to devote

their tine in other productive activities then it may result into loss of return.

Hence, by taking into account all the above depicted aspects, it can be stated that benefits offer

by activity based system is highly significant over its limitations. Thus, for getting the desired

level of outcome or success and avoiding all the current issues related to cost allocation

Turramurra Furniture needs to undertake ABB technique.

6

associated with activity based costing system before making selection of such budgeting tool or

method:

Advantages

Evaluation: ABB method helps in making evaluation or assessment of overhead on the

basis of cost driver. Hence, by following specific steps Turramurra Furniture would

become able to avoid unnecessary activities from the business.

Competitive edge: By using ABB tool Turramurra Furniture can save cost because it

helps in eliminating all undesirable activities from product line. In this, by reducing cost

firm would become able to offer products to the customers at suitable price. In this way,

ABB technique will assist firm in building and sustain competitive position over others.

Facilitates elimination of bottlenecks: ABB assists in removing all sorts of deficiencies

that prevail in the business activities and thereby streamlines overall operations.

Improves relationship: The main motives of business unit to provide customers with high

quality products at suitable price. In this regard, by using the techniques of ABB firm can

exert control on cost would become able to meet the expectation level of customers.

Drawbacks

Complex and requires high understanding: For setting budget as per such technique and

determining cost Turramurra Furniture requires highly talented personnel. Moreover,

ABB is complex in nature and requires high level of understanding for the purpose of

evaluation.

Resource consumption: In this, for conducting analysis, business entity has to employ

top officials. Along with this, it is highly consuming process and places negative impact

on other operational activities. Moreover, if manager would not become able to devote

their tine in other productive activities then it may result into loss of return.

Hence, by taking into account all the above depicted aspects, it can be stated that benefits offer

by activity based system is highly significant over its limitations. Thus, for getting the desired

level of outcome or success and avoiding all the current issues related to cost allocation

Turramurra Furniture needs to undertake ABB technique.

6

CONCLUSION

From the above report, it has been concluded that technique of job costing is suitable for

manufacturing companies. Such costing technique is highly significant which in turn helps

Turramurra Furniture in tracking cost of specific job. Besides this, it can be inferred that through

using the system of job costing and WIP owner of the furniture company can assess the situation

of under or over applied. It can be seen in the report that concerned business unit should lay

emphasis on undertaking activity based budgeting technique. Hence, such budgeting tool enables

firm to allocate cost on the basis of relevant driver and make effective use of financial resources.

7

From the above report, it has been concluded that technique of job costing is suitable for

manufacturing companies. Such costing technique is highly significant which in turn helps

Turramurra Furniture in tracking cost of specific job. Besides this, it can be inferred that through

using the system of job costing and WIP owner of the furniture company can assess the situation

of under or over applied. It can be seen in the report that concerned business unit should lay

emphasis on undertaking activity based budgeting technique. Hence, such budgeting tool enables

firm to allocate cost on the basis of relevant driver and make effective use of financial resources.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.