MSc Financial Management: NPV vs IRR Analysis of Project Appraisal

VerifiedAdded on 2023/04/22

|13

|1756

|427

Report

AI Summary

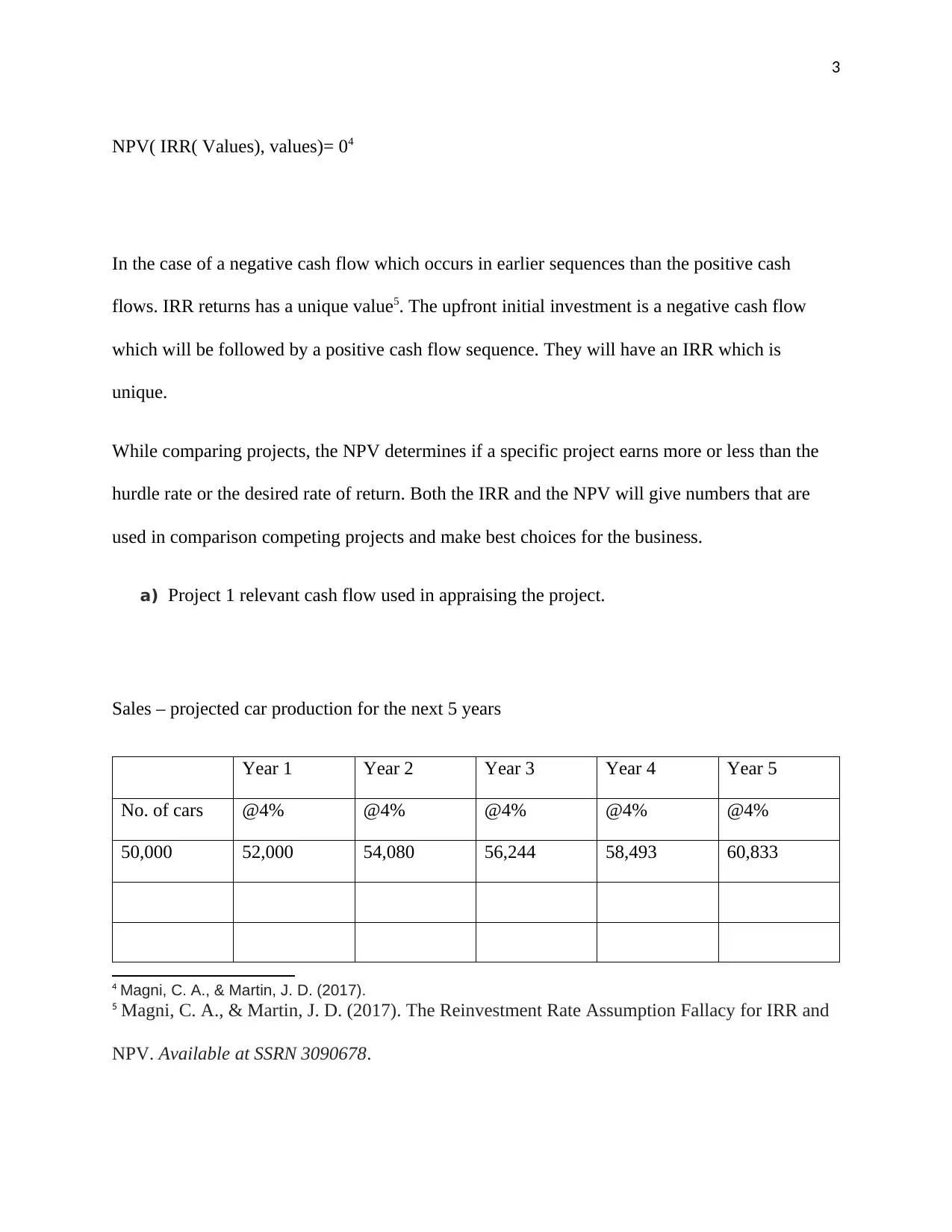

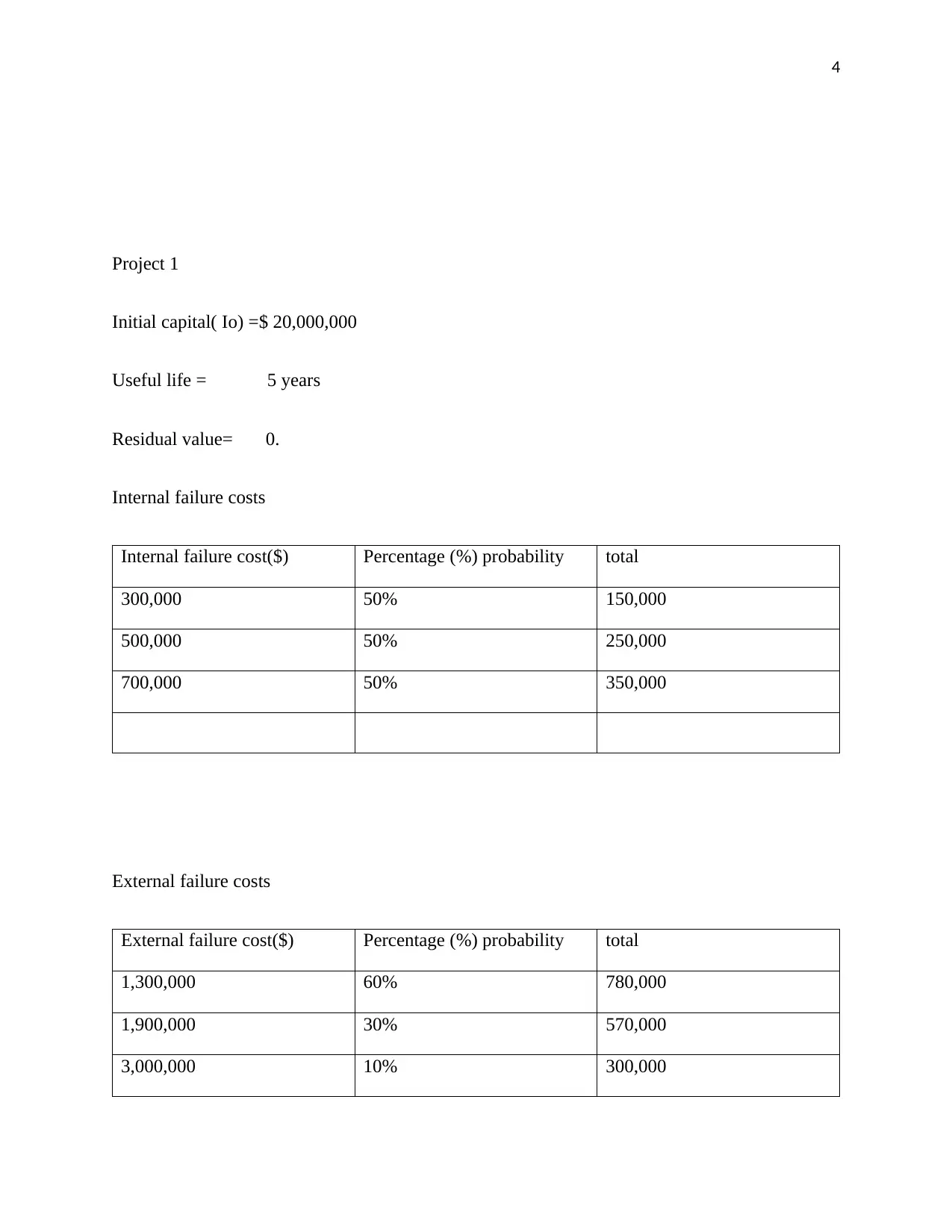

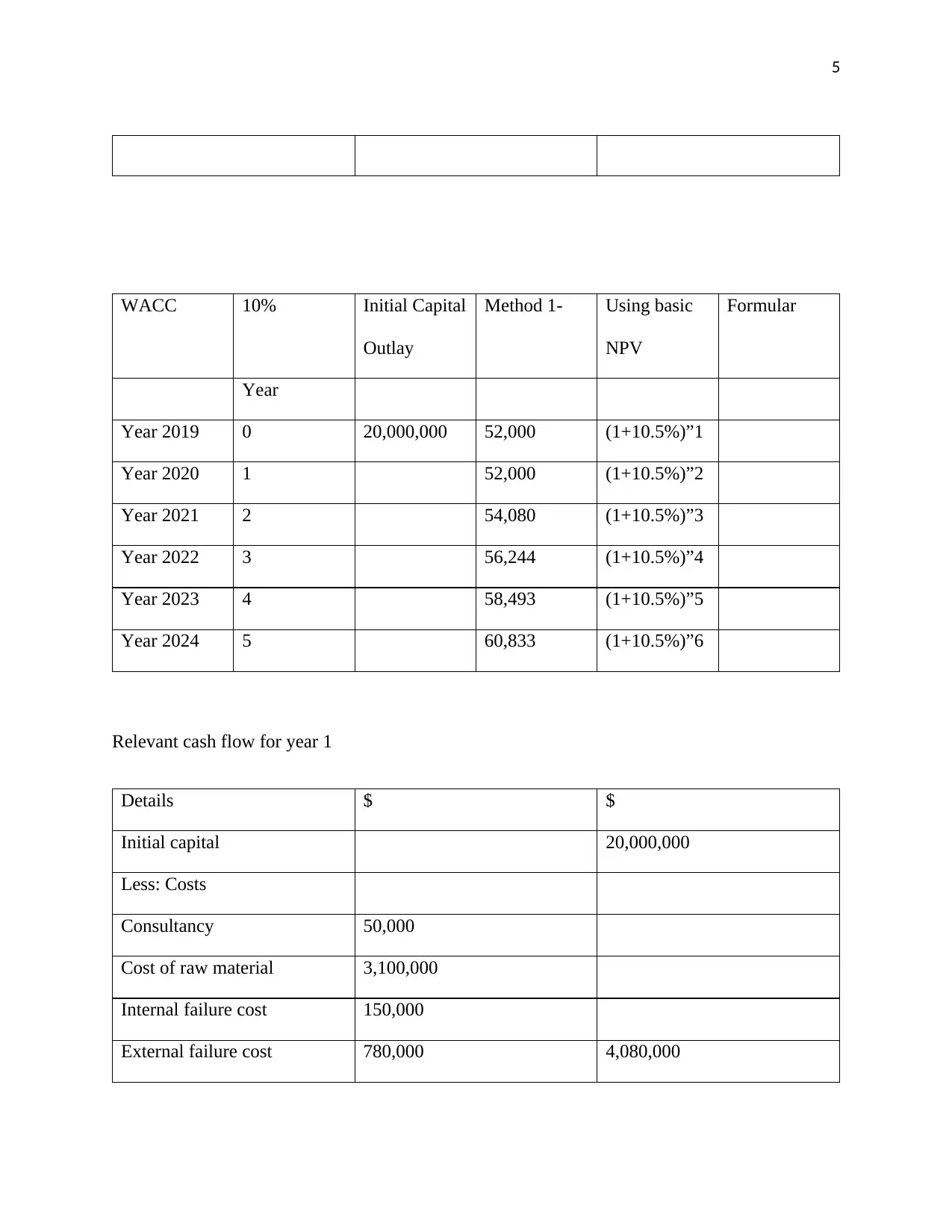

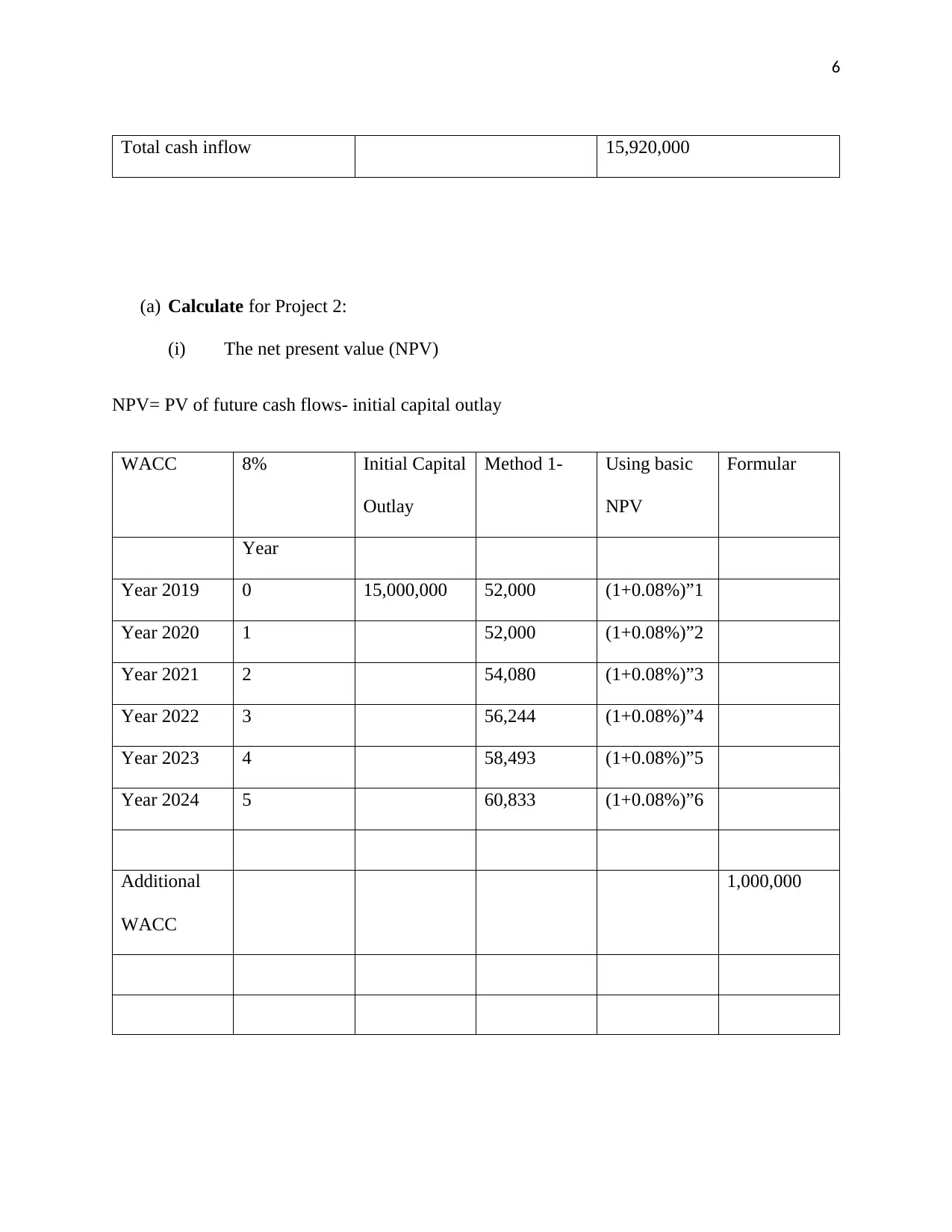

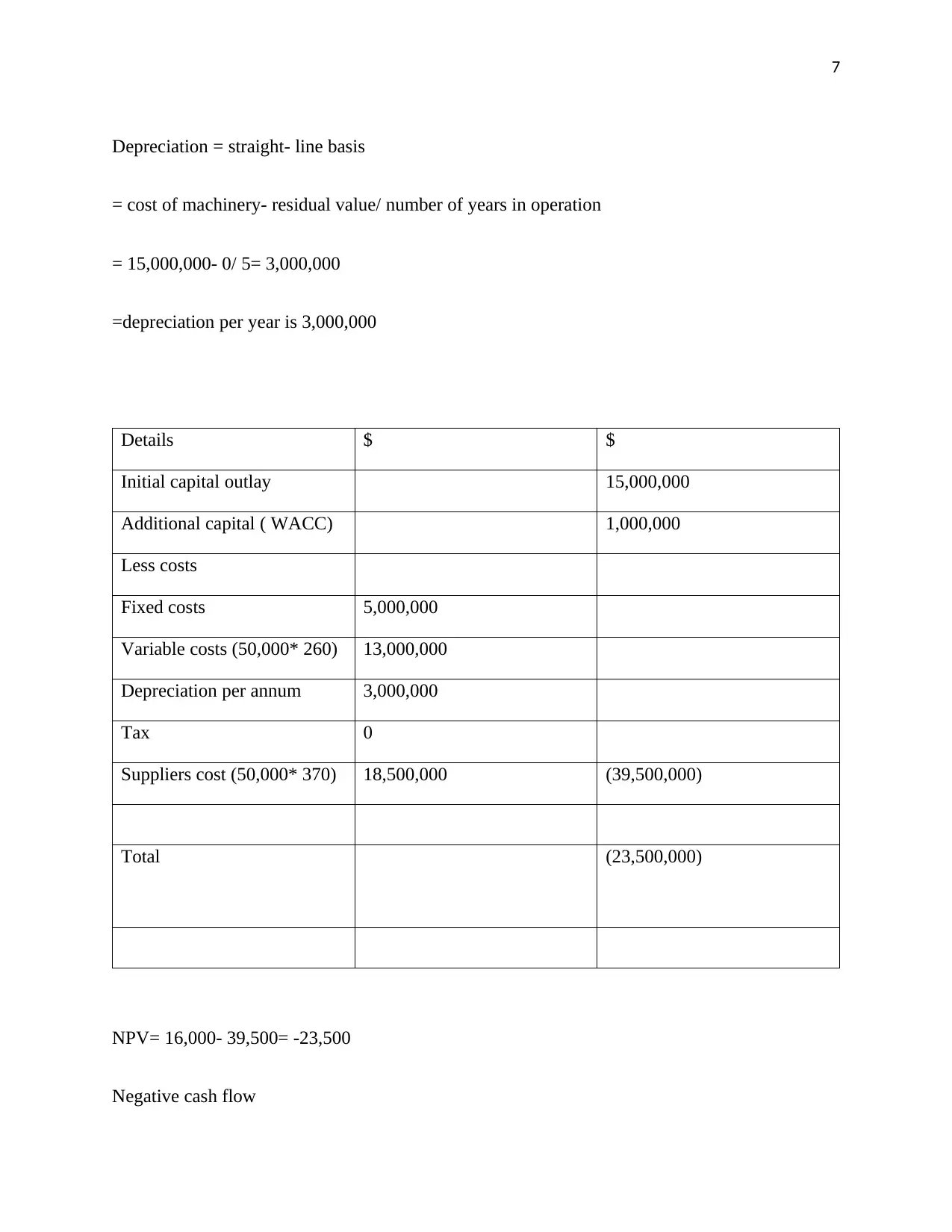

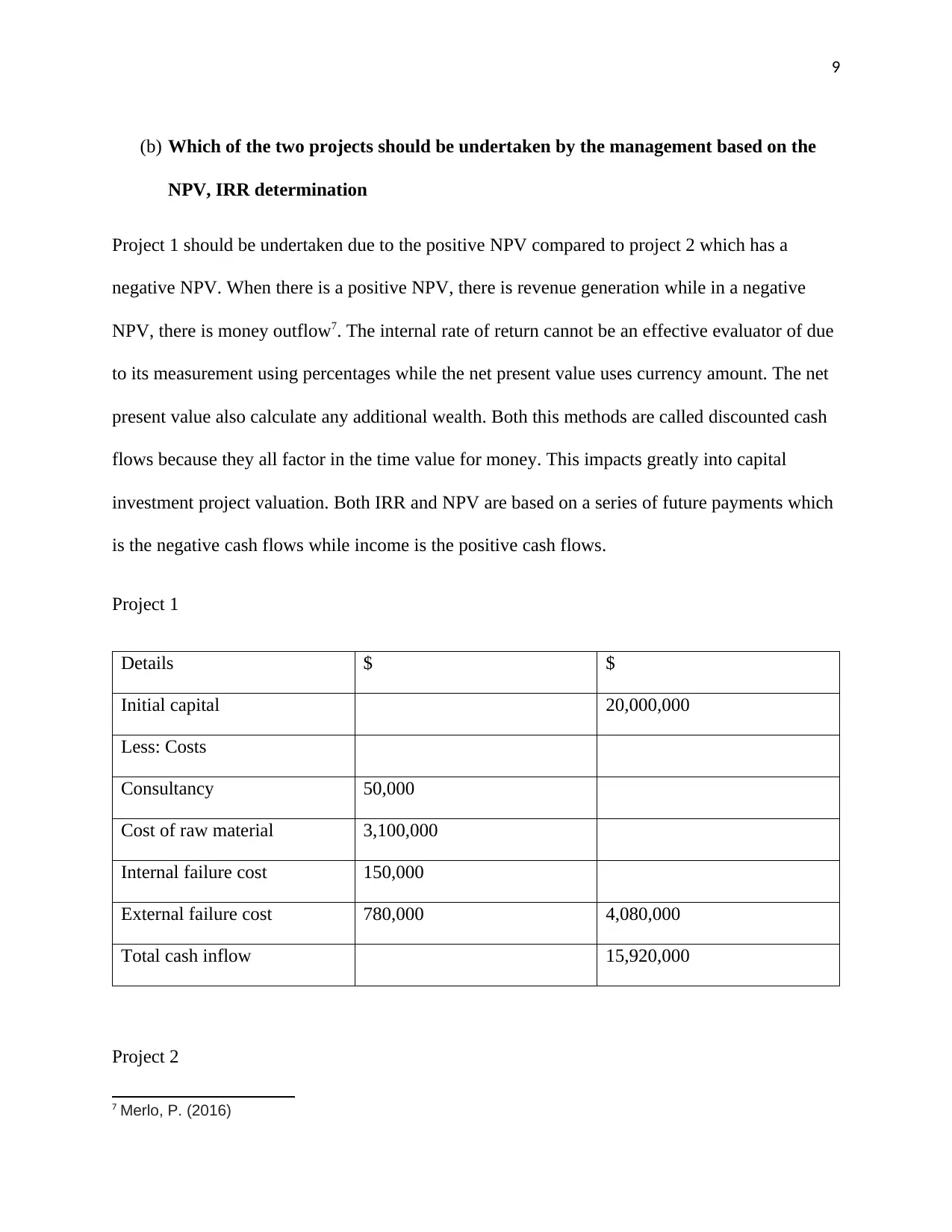

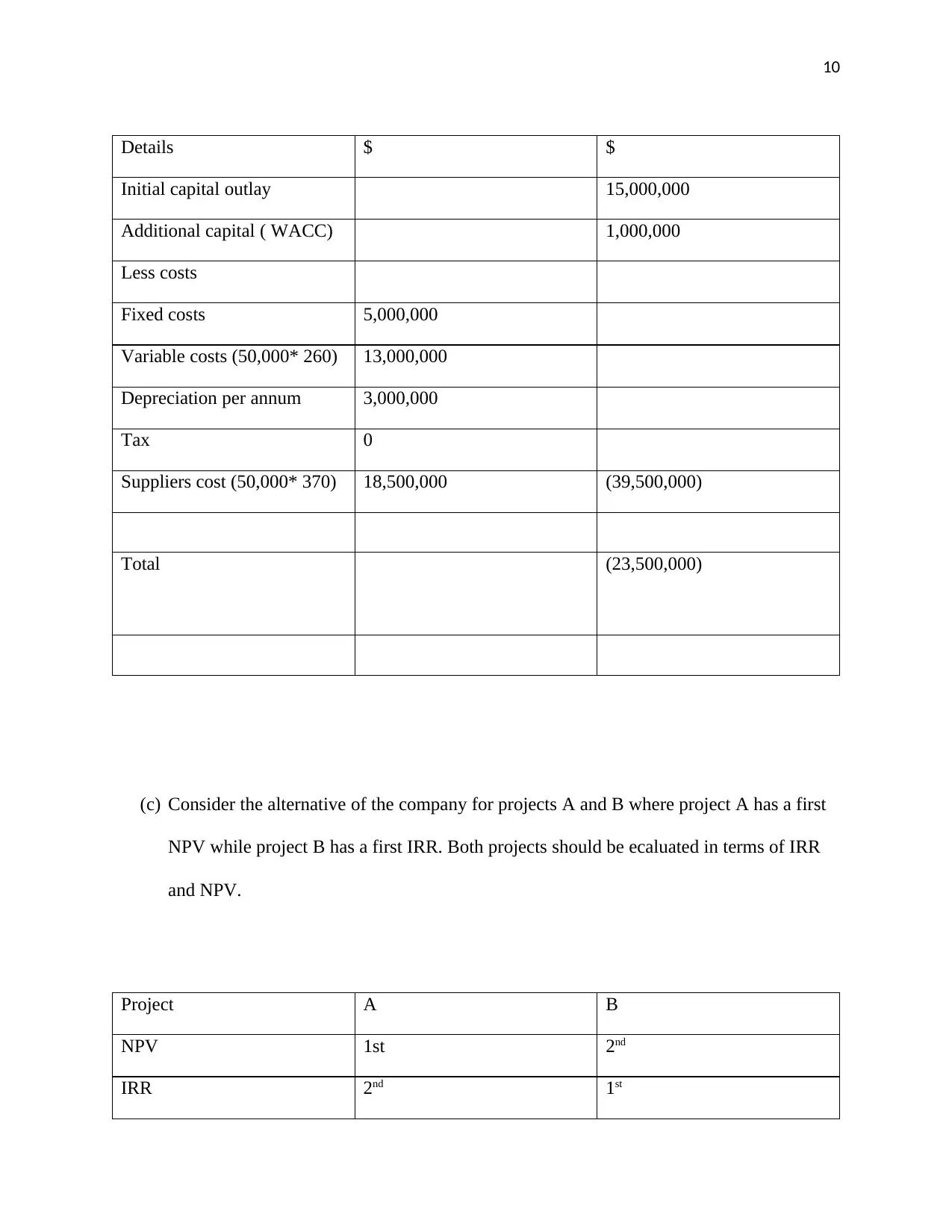

This report evaluates the superiority of Net Present Value (NPV) over Internal Rate of Return (IRR) in investment appraisal, particularly within the context of financial management. It highlights that NPV, measured in currency, offers a more straightforward understanding compared to IRR, which is expressed as a percentage. The report analyzes two potential investment projects for a car manufacturer facing financial challenges, calculating the NPV and IRR for each project. Project 1, involving a new quality control process, is recommended due to its positive NPV, unlike Project 2, which exhibits a negative NPV. Furthermore, the report explores potential variations between IRR and NPV rankings for projects A and B, attributing these differences to factors like cash inflow patterns and differing costs of capital. The analysis emphasizes the importance of considering both NPV and IRR when making investment decisions, while also acknowledging the limitations of IRR in certain scenarios. Desklib provides solved assignments and past papers for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.