Report on Accounting and Finance: APN Outdoor Group Analysis

VerifiedAdded on 2020/03/28

|9

|1396

|78

Report

AI Summary

This report provides a comprehensive analysis of APN Outdoor's capital structure, focusing on its debt and equity composition. It computes the company's Weighted Average Cost of Capital (WACC) and evaluates key financial ratios, including earnings per share, price-earnings ratio, and liquidity ratios such as cash, quick, and current ratios. The report compares APN Outdoor's capital structure to that of its competitor, Ooh Media, highlighting similarities and differences in their financing approaches. It also examines the impact of capital structure changes on the company's cost of capital and overall financial performance, concluding with an assessment of APN Outdoor's dividend payouts and shareholder returns. The report utilizes various financial metrics and ratios to assess APN Outdoor's financial health and investment potential.

Running head: ACCOUNTING AND FINANCE

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING AND FINANCE

Table of Contents

Answer to Part A........................................................................................................................2

Requirement 1:.......................................................................................................................2

Requirement 2:.......................................................................................................................4

Requirement 3........................................................................................................................4

Answer to Part B........................................................................................................................5

Introduction............................................................................................................................5

Evaluation of APN’s Capital Structure..................................................................................5

Computation of After-Tax WACC.........................................................................................6

Evaluation of the financial ratios of APN..............................................................................6

APN Outdoor and the performance of its competitors...........................................................6

Capital Structure of APN Outdoor group...............................................................................7

Conclusion..............................................................................................................................7

Reference List and Bibliography...............................................................................................8

ACCOUNTING AND FINANCE

Table of Contents

Answer to Part A........................................................................................................................2

Requirement 1:.......................................................................................................................2

Requirement 2:.......................................................................................................................4

Requirement 3........................................................................................................................4

Answer to Part B........................................................................................................................5

Introduction............................................................................................................................5

Evaluation of APN’s Capital Structure..................................................................................5

Computation of After-Tax WACC.........................................................................................6

Evaluation of the financial ratios of APN..............................................................................6

APN Outdoor and the performance of its competitors...........................................................6

Capital Structure of APN Outdoor group...............................................................................7

Conclusion..............................................................................................................................7

Reference List and Bibliography...............................................................................................8

2

ACCOUNTING AND FINANCE

Answer to Part A

Requirement 1:

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

ACCOUNTING AND FINANCE

Answer to Part A

Requirement 1:

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,589,500 $1,748,450 $1,923,295 $2,115,625 $2,327,187 $2,559,906 $2,815,896

Staff Cost ($900,000) ($954,000) ($1,011,240) ($1,071,914) ($1,136,229) ($1,204,403) ($1,276,667) ($1,353,267)

Material Costs ($210,000) ($222,600) ($235,956) ($250,113) ($265,120) ($281,027) ($297,889) ($315,762)

Marketing Costs ($46,000) ($48,760) ($51,686) ($54,787) ($58,074) ($61,558) ($65,252) ($69,167)

Other Costs ($25,000) ($26,500) ($28,090) ($29,775) ($31,562) ($33,456) ($35,463) ($37,591)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $131,390 $215,228 $310,455 $418,389 $540,493 $678,385 $833,859

Less: Tax on Profit ($17,325) ($39,417) ($64,569) ($93,137) ($125,517) ($162,148) ($203,515) ($250,158)

Net Profit after Tax $40,425 $91,973 $150,660 $217,319 $292,872 $378,345 $474,869 $583,701

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $789,951

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $298,223 $356,910 $423,569 $499,122 $584,595 $681,119 $889,951

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,105,102) ($748,192) ($324,624) $174,499 $759,094 $1,440,213 $2,330,164

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $221,628 $228,657 $233,933 $237,639 $239,942 $241,000 $271,458

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,215,721) ($987,064) ($753,131) ($515,492) ($275,550) ($34,549) $236,908

Discounted Payback period

Net Present Value

Profitability Index

4.65

7.13

$236,908

114.36%

Period

Capital Budgeting for Base-Case:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,531,700 $1,623,602 $1,721,018 $1,824,279 $1,933,736 $2,049,760 $2,172,746

Staff Cost ($900,000) ($990,000) ($1,089,000) ($1,197,900) ($1,317,690) ($1,449,459) ($1,594,405) ($1,753,845)

Material Costs ($210,000) ($231,000) ($254,100) ($279,510) ($307,461) ($338,207) ($372,028) ($409,231)

Marketing Costs ($46,000) ($50,600) ($55,660) ($61,226) ($67,349) ($74,083) ($81,492) ($89,641)

Other Costs ($25,000) ($27,500) ($30,250) ($33,275) ($36,603) ($40,263) ($44,289) ($48,718)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $26,350 ($11,658) ($57,143) ($111,073) ($174,526) ($248,703) ($334,939)

Less: Tax on Profit ($17,325) ($7,905) $3,497 $17,143 $33,322 $52,358 $74,611 $100,482

Net Profit after Tax $40,425 $18,445 ($8,161) ($40,000) ($77,751) ($122,168) ($174,092) ($234,457)

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 ($28,207)

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $224,695 $198,089 $166,250 $128,499 $84,082 $32,158 $71,793

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,178,630) ($980,541) ($814,291) ($685,792) ($601,710) ($569,552) ($497,760)

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $166,985 $126,907 $91,818 $61,180 $34,511 $11,378 $21,899

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,270,364) ($1,143,457) ($1,051,638) ($990,458) ($955,948) ($944,569) ($922,671)

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Worst-Case:

Period

10.34

50.13

($922,671)

44.08%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

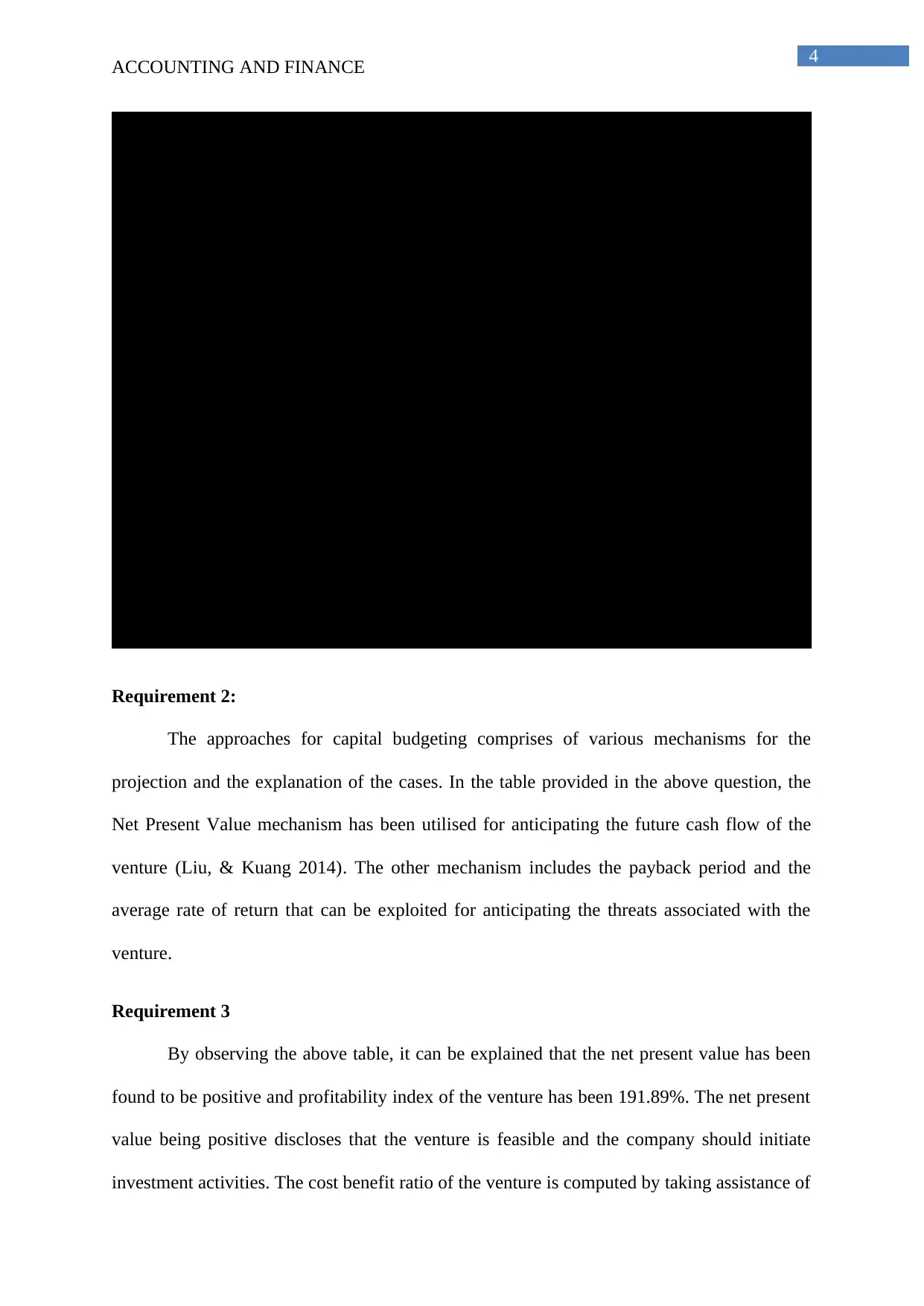

Requirement 2:

The approaches for capital budgeting comprises of various mechanisms for the

projection and the explanation of the cases. In the table provided in the above question, the

Net Present Value mechanism has been utilised for anticipating the future cash flow of the

venture (Liu, & Kuang 2014). The other mechanism includes the payback period and the

average rate of return that can be exploited for anticipating the threats associated with the

venture.

Requirement 3

By observing the above table, it can be explained that the net present value has been

found to be positive and profitability index of the venture has been 191.89%. The net present

value being positive discloses that the venture is feasible and the company should initiate

investment activities. The cost benefit ratio of the venture is computed by taking assistance of

ACCOUNTING AND FINANCE

Particulars 0 1 2 3 4 5 6 7 8

Initial Investment ($1,650,000)

Annual Cash Flow:

Incremental Revene $1,445,000 $1,661,750 $1,911,013 $2,197,664 $2,527,314 $2,906,411 $3,342,373 $3,843,729

Staff Cost ($900,000) ($927,000) ($954,810) ($983,454) ($1,012,958) ($1,043,347) ($1,074,647) ($1,106,886)

Material Costs ($210,000) ($216,300) ($222,789) ($229,473) ($236,357) ($243,448) ($250,751) ($258,274)

Marketing Costs ($46,000) ($47,380) ($48,801) ($50,265) ($51,773) ($53,327) ($54,926) ($56,574)

Other Costs ($25,000) ($25,750) ($26,523) ($27,318) ($28,138) ($28,982) ($29,851) ($30,747)

Depreciation of Lab ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250) ($206,250)

Net Profit before Tax $57,750 $239,070 $451,840 $700,904 $991,838 $1,331,058 $1,725,947 $2,184,998

Less: Tax on Profit ($17,325) ($71,721) ($135,552) ($210,271) ($297,551) ($399,318) ($517,784) ($655,499)

Net Profit after Tax $40,425 $167,349 $316,288 $490,633 $694,287 $931,741 $1,208,163 $1,529,498

Add: Depreciation $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250 $206,250

Annual After-Tax Cash Flow $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,735,748

Salvage Value $100,000

Net Annual Cash Flow ($1,650,000) $246,675 $373,599 $522,538 $696,883 $900,537 $1,137,991 $1,414,413 $1,835,748

Cumulative Cash Flow ($1,650,000) ($1,403,325) ($1,029,726) ($507,188) $189,694 $1,090,231 $2,228,222 $3,642,635 $5,478,383

Payback Period

Required Rate of Return 16% 16% 16% 16% 16% 16% 16% 16% 16%

Discounted Cash Flow ($1,650,000) $212,651 $277,645 $334,768 $384,882 $428,757 $467,080 $500,461 $559,950

Cumulative Discounted Cash Flow ($1,650,000) ($1,437,349) ($1,159,704) ($824,936) ($440,054) ($11,297) $455,782 $956,244 $1,516,194

Discounted Payback period

Net Present Value

Profitability Index

Capital Budgeting for Best-Case:

Period

3.79

5.29

$1,516,194

191.89%

Requirement 2:

The approaches for capital budgeting comprises of various mechanisms for the

projection and the explanation of the cases. In the table provided in the above question, the

Net Present Value mechanism has been utilised for anticipating the future cash flow of the

venture (Liu, & Kuang 2014). The other mechanism includes the payback period and the

average rate of return that can be exploited for anticipating the threats associated with the

venture.

Requirement 3

By observing the above table, it can be explained that the net present value has been

found to be positive and profitability index of the venture has been 191.89%. The net present

value being positive discloses that the venture is feasible and the company should initiate

investment activities. The cost benefit ratio of the venture is computed by taking assistance of

5

ACCOUNTING AND FINANCE

the profitability index and in this case the value is 191.89% thereby indicating that the present

value of the future cash flow is higher than the initial investment amount undertaken by the

firm. The other information with respect to the rejection and the acceptance of the venture

can be undertaken with the help of the implementation of other mechanisms of capital

budgeting like the average rate of return and the payback period.

Answer to Part B

Introduction

The financial report has been constructed in order gain knowledge about the capital

structure of APN Outdoor Group which is an ASX listed organization. the report has

explained that the computation of the weighted average cost of capital and the assessment of

the vital financial ratios of the firm.

Evaluation of APN’s Capital Structure

APN’s WACC has been computed as 8.32%. An extra amount of $181.8 of equity

was developed by APN in the year 2016 for the construction of the new capital structures.

The company looks to lower the cost of capital with the help of the maintenance of the most

favourable capital structure. With the assistance of the evaluation of the annual report, it can

be suggested that during the 2016 accounting years, the debt proportion in the capital

structure has decreased. The cost of capital of APN can be decreased further by raising the

value of the debt proportion in their capital structure (Chiarini, & Vagnoni 2015). The cause

has been due to the fact that the equity capital that has been issued has raised and interest

bearing liabilities has decreased in the current year. In order to conclude, it can be said that

the equity value remained at 38.1 in the present accounting year and the overall debt to

capital has summed up to 27.61.

ACCOUNTING AND FINANCE

the profitability index and in this case the value is 191.89% thereby indicating that the present

value of the future cash flow is higher than the initial investment amount undertaken by the

firm. The other information with respect to the rejection and the acceptance of the venture

can be undertaken with the help of the implementation of other mechanisms of capital

budgeting like the average rate of return and the payback period.

Answer to Part B

Introduction

The financial report has been constructed in order gain knowledge about the capital

structure of APN Outdoor Group which is an ASX listed organization. the report has

explained that the computation of the weighted average cost of capital and the assessment of

the vital financial ratios of the firm.

Evaluation of APN’s Capital Structure

APN’s WACC has been computed as 8.32%. An extra amount of $181.8 of equity

was developed by APN in the year 2016 for the construction of the new capital structures.

The company looks to lower the cost of capital with the help of the maintenance of the most

favourable capital structure. With the assistance of the evaluation of the annual report, it can

be suggested that during the 2016 accounting years, the debt proportion in the capital

structure has decreased. The cost of capital of APN can be decreased further by raising the

value of the debt proportion in their capital structure (Chiarini, & Vagnoni 2015). The cause

has been due to the fact that the equity capital that has been issued has raised and interest

bearing liabilities has decreased in the current year. In order to conclude, it can be said that

the equity value remained at 38.1 in the present accounting year and the overall debt to

capital has summed up to 27.61.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING AND FINANCE

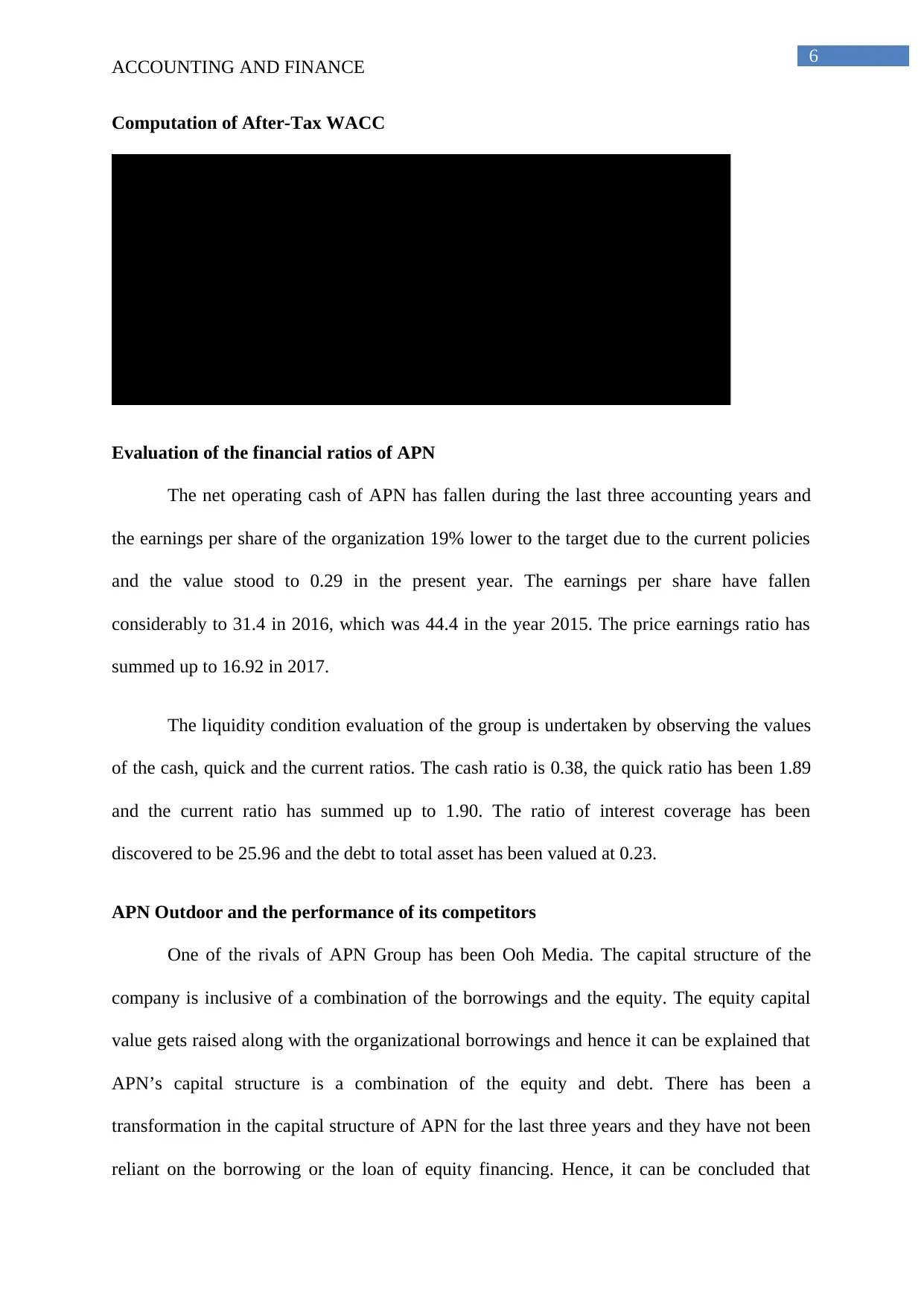

Computation of After-Tax WACC

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Evaluation of the financial ratios of APN

The net operating cash of APN has fallen during the last three accounting years and

the earnings per share of the organization 19% lower to the target due to the current policies

and the value stood to 0.29 in the present year. The earnings per share have fallen

considerably to 31.4 in 2016, which was 44.4 in the year 2015. The price earnings ratio has

summed up to 16.92 in 2017.

The liquidity condition evaluation of the group is undertaken by observing the values

of the cash, quick and the current ratios. The cash ratio is 0.38, the quick ratio has been 1.89

and the current ratio has summed up to 1.90. The ratio of interest coverage has been

discovered to be 25.96 and the debt to total asset has been valued at 0.23.

APN Outdoor and the performance of its competitors

One of the rivals of APN Group has been Ooh Media. The capital structure of the

company is inclusive of a combination of the borrowings and the equity. The equity capital

value gets raised along with the organizational borrowings and hence it can be explained that

APN’s capital structure is a combination of the equity and debt. There has been a

transformation in the capital structure of APN for the last three years and they have not been

reliant on the borrowing or the loan of equity financing. Hence, it can be concluded that

ACCOUNTING AND FINANCE

Computation of After-Tax WACC

Particulars Amount Weightage Return Rate

Weighted

Return

Total Equity Capital $836,465 83.83% 8.38% 7.03%

Total Debt Capital $161,309 16.17% 11.42% 1.85%

Tax Rate 30%

After-Tax Weighted Average Cost

of Capital 8.32%

Computation of After-Tax Weighted Avergae Cost of Capital:

Evaluation of the financial ratios of APN

The net operating cash of APN has fallen during the last three accounting years and

the earnings per share of the organization 19% lower to the target due to the current policies

and the value stood to 0.29 in the present year. The earnings per share have fallen

considerably to 31.4 in 2016, which was 44.4 in the year 2015. The price earnings ratio has

summed up to 16.92 in 2017.

The liquidity condition evaluation of the group is undertaken by observing the values

of the cash, quick and the current ratios. The cash ratio is 0.38, the quick ratio has been 1.89

and the current ratio has summed up to 1.90. The ratio of interest coverage has been

discovered to be 25.96 and the debt to total asset has been valued at 0.23.

APN Outdoor and the performance of its competitors

One of the rivals of APN Group has been Ooh Media. The capital structure of the

company is inclusive of a combination of the borrowings and the equity. The equity capital

value gets raised along with the organizational borrowings and hence it can be explained that

APN’s capital structure is a combination of the equity and debt. There has been a

transformation in the capital structure of APN for the last three years and they have not been

reliant on the borrowing or the loan of equity financing. Hence, it can be concluded that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING AND FINANCE

capital structure of both the firms is a combination of funding their assets. The company APN

Outdoor has gained a healthy cash flow that assists in financing the investments and creates

appropriate returns for the shareholders (Grabinskia et al., 2014).

Capital Structure of APN Outdoor group

The capital structure of a company is a combination of the debt and equity with the

intention of financing the asset. Cost of capital is the return rate that is anticipated by the firm

on the earning over the capital as an substitute value of investment along with the presence of

risk (Kowalczyk, 2016). The transformations in the capital structure have a direct impact on

the weighted average cost of capital. Hence, in order to raise the market value, it is crucial for

the organization to lower their cost of capital. The cost of capital of a firm can be lowered

with the help of reorganising their capital structure and it is to be monitored that the cost of

capital does not surpass the expected rate of return. The cost of capital being lower would

make financing in the new ventures economical (Klychova et al., 2014).

Conclusion

By looking at the assessment given above, it can be explained that capital structure of

APN consists of debentures and equity. They have been giving out acceptable returns to the

stakeholders and therefore have been giving out higher dividends to their shareholders. The

profits and the earnings before taxes and interest of the company have felt an upward pattern

that has assisted in creating acceptable income to the shareholders.

ACCOUNTING AND FINANCE

capital structure of both the firms is a combination of funding their assets. The company APN

Outdoor has gained a healthy cash flow that assists in financing the investments and creates

appropriate returns for the shareholders (Grabinskia et al., 2014).

Capital Structure of APN Outdoor group

The capital structure of a company is a combination of the debt and equity with the

intention of financing the asset. Cost of capital is the return rate that is anticipated by the firm

on the earning over the capital as an substitute value of investment along with the presence of

risk (Kowalczyk, 2016). The transformations in the capital structure have a direct impact on

the weighted average cost of capital. Hence, in order to raise the market value, it is crucial for

the organization to lower their cost of capital. The cost of capital of a firm can be lowered

with the help of reorganising their capital structure and it is to be monitored that the cost of

capital does not surpass the expected rate of return. The cost of capital being lower would

make financing in the new ventures economical (Klychova et al., 2014).

Conclusion

By looking at the assessment given above, it can be explained that capital structure of

APN consists of debentures and equity. They have been giving out acceptable returns to the

stakeholders and therefore have been giving out higher dividends to their shareholders. The

profits and the earnings before taxes and interest of the company have felt an upward pattern

that has assisted in creating acceptable income to the shareholders.

8

ACCOUNTING AND FINANCE

Reference List and Bibliography

Chiarini, A., & Vagnoni, E. (2015). World-class manufacturing by Fiat. Comparison with

Toyota production system from a strategic management, management accounting,

operations management and performance measurement dimension. International

Journal of Production Research, 53(2), 590-606.

Crawford, M. J., Lee, J., Jankowski, J. E., & Moris, F. A. (2014). Measuring R&D in the

national economic accounting system. Survey of current business, 94(11), 1-15.

Grabinskia, K., Kedziora, M., & Krasodomska, J. (2014). The Polish accounting system and

IFRS implementation process in the view of empirical research. Accounting and

Management Information Systems, 13(2), 281.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Kowalczyk, M. (2016). Accounting System on Polish Local Government in the Context of

New Public Management.

Liu, Y., & Kuang, Y. (2014). The Establishment of Management Accounting System in

Administrative Institutions. Journal of Accounting and Economics, 2, 003.

Seeger, J. J., & Young, J. C. (2017). U.S. Patent No. 9,697,571. Washington, DC: U.S. Patent

and Trademark Office.

ACCOUNTING AND FINANCE

Reference List and Bibliography

Chiarini, A., & Vagnoni, E. (2015). World-class manufacturing by Fiat. Comparison with

Toyota production system from a strategic management, management accounting,

operations management and performance measurement dimension. International

Journal of Production Research, 53(2), 590-606.

Crawford, M. J., Lee, J., Jankowski, J. E., & Moris, F. A. (2014). Measuring R&D in the

national economic accounting system. Survey of current business, 94(11), 1-15.

Grabinskia, K., Kedziora, M., & Krasodomska, J. (2014). The Polish accounting system and

IFRS implementation process in the view of empirical research. Accounting and

Management Information Systems, 13(2), 281.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Kowalczyk, M. (2016). Accounting System on Polish Local Government in the Context of

New Public Management.

Liu, Y., & Kuang, Y. (2014). The Establishment of Management Accounting System in

Administrative Institutions. Journal of Accounting and Economics, 2, 003.

Seeger, J. J., & Young, J. C. (2017). U.S. Patent No. 9,697,571. Washington, DC: U.S. Patent

and Trademark Office.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.