Taxation Theory, Practice & Law Assignment: Client Scenario Analysis

VerifiedAdded on 2023/06/04

|13

|3057

|418

Homework Assignment

AI Summary

This assignment solution addresses a taxation scenario involving a client who is an investor and antique collector. The solution analyzes the capital gains tax (CGT) implications of asset sales, including land, an antique bed, shares, and a violin, considering pre-CGT assets, cost base, and the discount method. It also examines the fringe benefit tax (FBT) liabilities for the client's company, Rapid Heat, focusing on car fringe benefits and loan fringe benefits provided to an employee, Jasmine. The analysis includes detailed calculations of taxable values and incorporates relevant tax legislation and rulings, such as TR 94/29, and relevant sections of the ITAA 1997 to determine the tax consequences of each transaction and benefit provided.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

The scenario that has been presented provides detail of a client who is primarily an investor

along with being a collector. In 2017/2018, a series of transactions have been entered into by the

client, which involved sale of selected assets. Two scenarios can emerge based on the given

information. Under one scenario, the client may have a business whereby these assets are

regularly bought and sold and thereby treated as trading stock. The resultant income would be

assessable income as per s. 6-5 ITAA 1997 in this scenario. However, this is not feasible as the

provided information makes it apparent that this scenario is not true considering that it is given

that the client does not conduct business dealing with these assets. In such situation, only one

possible explanation remains whereby these are investment assets and have been liquidated to

yield capital proceeds. While these proceeds are immune from any taxation, any difference from

the capital base would lead to capital gains/loss implications which need to be dealt with under

the aegis of Capital Gains Tax (CGT).

Some key aspects which are pivotal with regards to computation of CGT consequences are

indicated below.

Aspect 1: Pre-CGT Asset

Before moving ahead, for every asset the first criterion to be applied is whether the given asset is

a pre-CGT asset is not. This is imperative to apply as s. 149-10 ITAA 1997 exempts such assets

from any CGT being levied on capital gains or losses (Austlii, 2018 a). The rule to determine if

a given asset belongs to this class or not is to consider the date of purchase which must be before

20th September 1985 in order to asset be classified as pre-CGT asset (Hodgson,Mortimer and

Butler, 2016).

Aspect 2: Defining a CGT Event

The computation of capital gains/ losses is started with the taking place of a CGT event

(Barkoczy, 2017). Subsection 104-5 ITAA 1997 lists down the summary of various possible

CGT events along with the precise approach to determine the gains and losses (Krever, 2017).

With regards to the given scenario, only one event has special relevance as all the transactions

tend to fall within the ambit of the same event which is A1 event. The precise manner of capital

1

The scenario that has been presented provides detail of a client who is primarily an investor

along with being a collector. In 2017/2018, a series of transactions have been entered into by the

client, which involved sale of selected assets. Two scenarios can emerge based on the given

information. Under one scenario, the client may have a business whereby these assets are

regularly bought and sold and thereby treated as trading stock. The resultant income would be

assessable income as per s. 6-5 ITAA 1997 in this scenario. However, this is not feasible as the

provided information makes it apparent that this scenario is not true considering that it is given

that the client does not conduct business dealing with these assets. In such situation, only one

possible explanation remains whereby these are investment assets and have been liquidated to

yield capital proceeds. While these proceeds are immune from any taxation, any difference from

the capital base would lead to capital gains/loss implications which need to be dealt with under

the aegis of Capital Gains Tax (CGT).

Some key aspects which are pivotal with regards to computation of CGT consequences are

indicated below.

Aspect 1: Pre-CGT Asset

Before moving ahead, for every asset the first criterion to be applied is whether the given asset is

a pre-CGT asset is not. This is imperative to apply as s. 149-10 ITAA 1997 exempts such assets

from any CGT being levied on capital gains or losses (Austlii, 2018 a). The rule to determine if

a given asset belongs to this class or not is to consider the date of purchase which must be before

20th September 1985 in order to asset be classified as pre-CGT asset (Hodgson,Mortimer and

Butler, 2016).

Aspect 2: Defining a CGT Event

The computation of capital gains/ losses is started with the taking place of a CGT event

(Barkoczy, 2017). Subsection 104-5 ITAA 1997 lists down the summary of various possible

CGT events along with the precise approach to determine the gains and losses (Krever, 2017).

With regards to the given scenario, only one event has special relevance as all the transactions

tend to fall within the ambit of the same event which is A1 event. The precise manner of capital

1

gains/losses computation is contingent on two factors namely the proceeds that the sale generates

and the asset cost base associated with respective asset.

Aspect 3: Cost base

The above section clearly underlines the need to define the cost base for which the relevant

section is 110-25 (Barkoczy, 2017). While the most obvious element to be included in the cost

base is the price at which the asset purchase is done but there are other elements also as indicated

follows (Hodgson, Mortimer and Butler, 2016).

Aspect 4: Concession on Capital Gains

The capital gains derived from the methodology highlighted in A1 CGT event are not subject to

CGT. Instead, these are applied certain concessions and only the remainder capital gains after

concession would be levied CGT. There are two key approaches namely the indexation method

and discount method (Nethercott, Richardson and Devos, 2016). However, discussion would be

limited to the second method as it is the one more relevant for the given transactions where the

capital gains are significant. The discount method has been explained in s. 115-25 which opines

that a flat discount to the tune of 50% would be levied provided the underlying capital gains

from asset sale are long term (Austlii, 2018 b). The necessary condition for this to happen is that

the underlying asset needs to be held in excess of one year (Sadiq, et.al., 2015).

Aspect 5: Accommodation of capital losses

As per s. 102-5, any capital losses that are generated need to be adjusted against the capital gains

that would have been generated in the same year (Deutsch, et.al., 2015). However, if this is not

possible due to absence of capital gains, then the capital losses are taken into next year for

combining with capital gains. The shifting of capital losses would continue till the time capital

2

and the asset cost base associated with respective asset.

Aspect 3: Cost base

The above section clearly underlines the need to define the cost base for which the relevant

section is 110-25 (Barkoczy, 2017). While the most obvious element to be included in the cost

base is the price at which the asset purchase is done but there are other elements also as indicated

follows (Hodgson, Mortimer and Butler, 2016).

Aspect 4: Concession on Capital Gains

The capital gains derived from the methodology highlighted in A1 CGT event are not subject to

CGT. Instead, these are applied certain concessions and only the remainder capital gains after

concession would be levied CGT. There are two key approaches namely the indexation method

and discount method (Nethercott, Richardson and Devos, 2016). However, discussion would be

limited to the second method as it is the one more relevant for the given transactions where the

capital gains are significant. The discount method has been explained in s. 115-25 which opines

that a flat discount to the tune of 50% would be levied provided the underlying capital gains

from asset sale are long term (Austlii, 2018 b). The necessary condition for this to happen is that

the underlying asset needs to be held in excess of one year (Sadiq, et.al., 2015).

Aspect 5: Accommodation of capital losses

As per s. 102-5, any capital losses that are generated need to be adjusted against the capital gains

that would have been generated in the same year (Deutsch, et.al., 2015). However, if this is not

possible due to absence of capital gains, then the capital losses are taken into next year for

combining with capital gains. The shifting of capital losses would continue till the time capital

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gains are encountered. Under no circumstance can these be levelled against the taxable income to

reduce tax liability (Krever, 2017).

Using the concepts outlined above, the transactions enacted need to be analysed so as to

highlight the taxable capital gains.

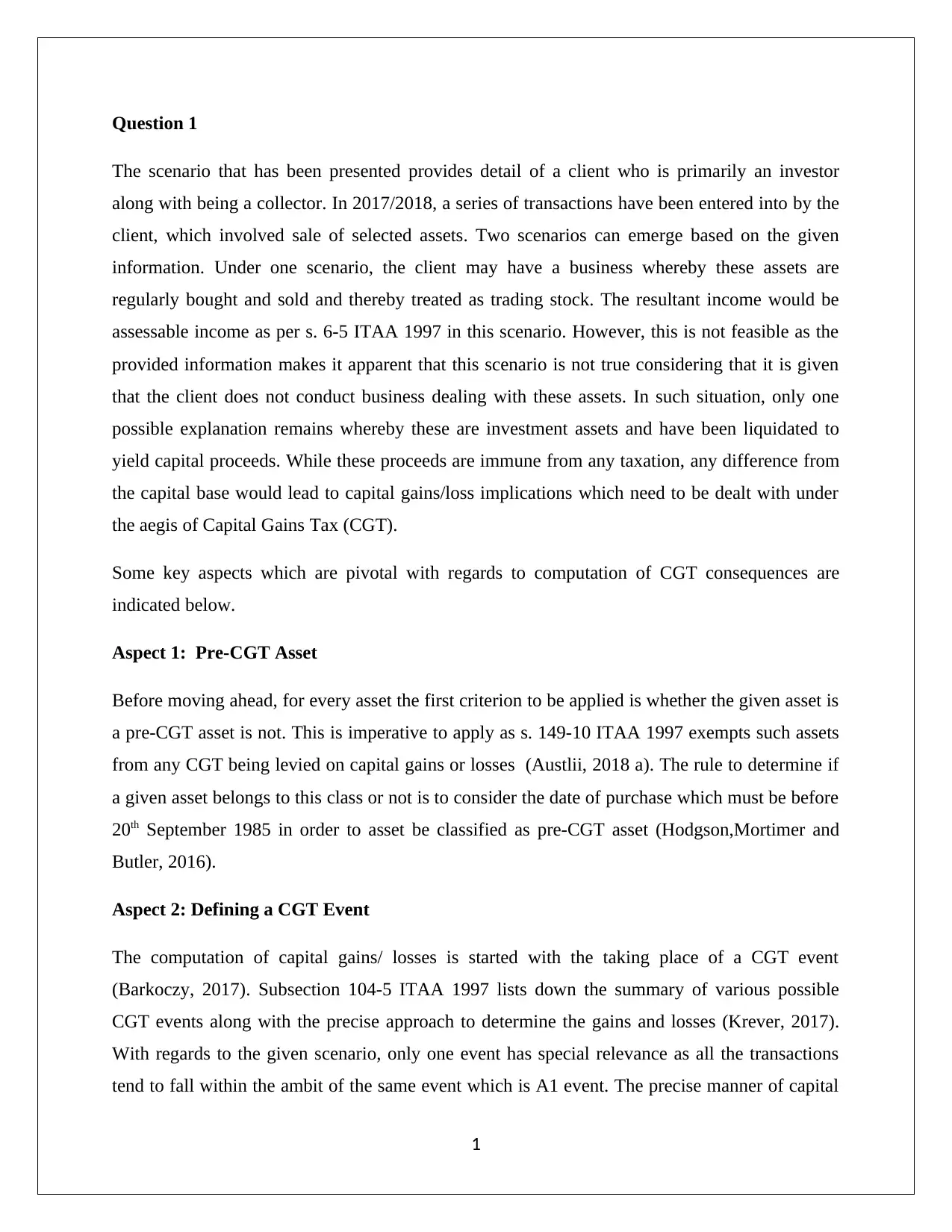

1. LAND

The purchase date for the land asset can be traced to 2001 implying that it cannot be placed in

the category of pre-CGT asset. Thus, CGT exemption cannot be availed for this asset. Further,

the sale of land has triggered CGT event A1 and hence it is imperative to compute the underlying

gains or losses. The first step in this direction is the determination of the cost base of land asset

in accordance with the discussion carried out above. This has been carried out below.

Also, an interesting aspect in the transaction is that the contract for sale in case of land has

already been enacted but the sales proceeds will not be collected till the next tax year. In this

situation, it becomes pivotal to determine as to whether the CGT would be applicable on the

capital gains in 2017/2018 or 2018/2019. Appropriate solution to this issue has been indicated in

TR 94/29 which clearly endorses the computation of capital gains in the year when execution of

sale contract takes place (ATO, 1994). Thereby, the CGT consequences for the capital gains

realised would be levied in the current year only. Further consideration would be given to the

longer than one year holding period of land by client which entitles to 50% rebate in line with the

discount method highlighted in s. 115-25.

3

reduce tax liability (Krever, 2017).

Using the concepts outlined above, the transactions enacted need to be analysed so as to

highlight the taxable capital gains.

1. LAND

The purchase date for the land asset can be traced to 2001 implying that it cannot be placed in

the category of pre-CGT asset. Thus, CGT exemption cannot be availed for this asset. Further,

the sale of land has triggered CGT event A1 and hence it is imperative to compute the underlying

gains or losses. The first step in this direction is the determination of the cost base of land asset

in accordance with the discussion carried out above. This has been carried out below.

Also, an interesting aspect in the transaction is that the contract for sale in case of land has

already been enacted but the sales proceeds will not be collected till the next tax year. In this

situation, it becomes pivotal to determine as to whether the CGT would be applicable on the

capital gains in 2017/2018 or 2018/2019. Appropriate solution to this issue has been indicated in

TR 94/29 which clearly endorses the computation of capital gains in the year when execution of

sale contract takes place (ATO, 1994). Thereby, the CGT consequences for the capital gains

realised would be levied in the current year only. Further consideration would be given to the

longer than one year holding period of land by client which entitles to 50% rebate in line with the

discount method highlighted in s. 115-25.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

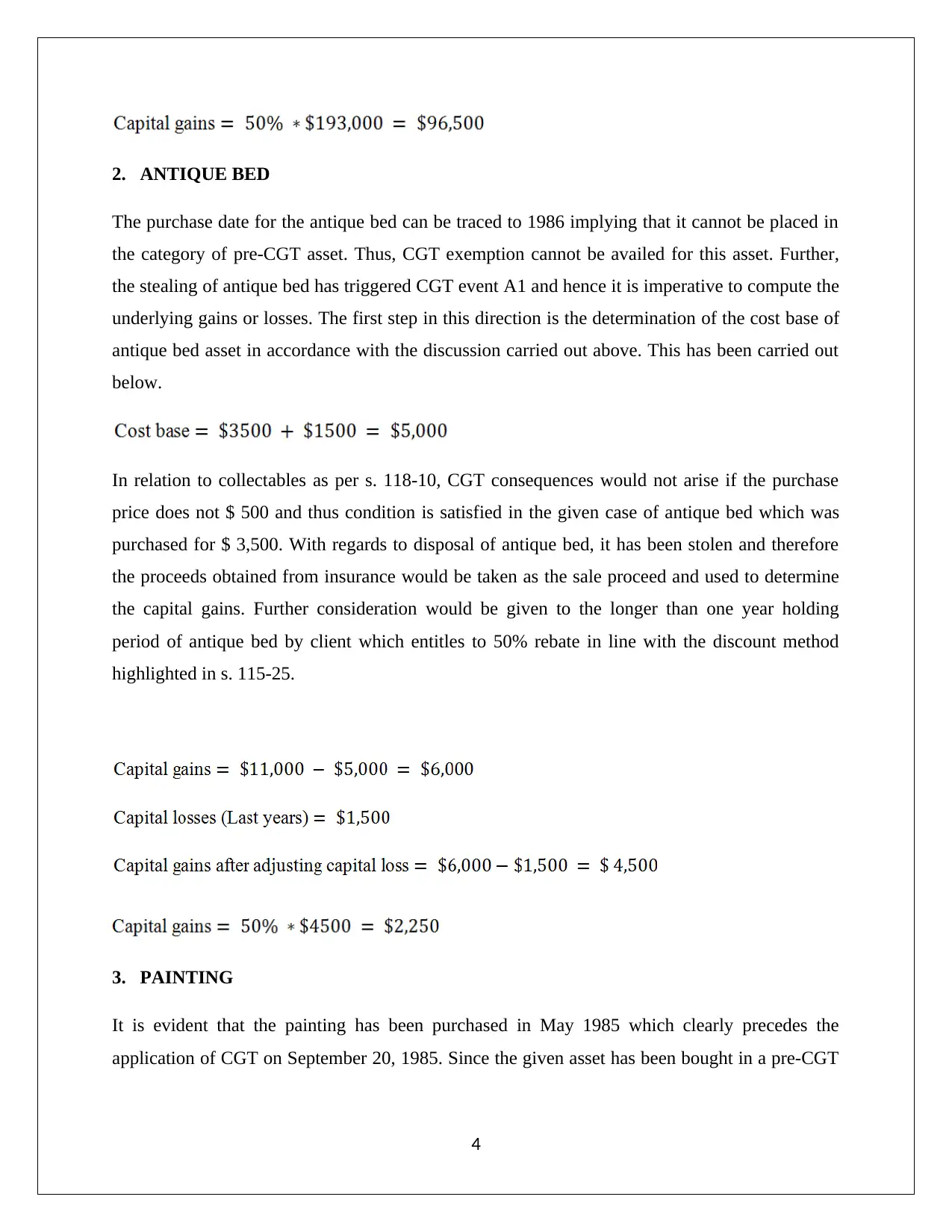

2. ANTIQUE BED

The purchase date for the antique bed can be traced to 1986 implying that it cannot be placed in

the category of pre-CGT asset. Thus, CGT exemption cannot be availed for this asset. Further,

the stealing of antique bed has triggered CGT event A1 and hence it is imperative to compute the

underlying gains or losses. The first step in this direction is the determination of the cost base of

antique bed asset in accordance with the discussion carried out above. This has been carried out

below.

In relation to collectables as per s. 118-10, CGT consequences would not arise if the purchase

price does not $ 500 and thus condition is satisfied in the given case of antique bed which was

purchased for $ 3,500. With regards to disposal of antique bed, it has been stolen and therefore

the proceeds obtained from insurance would be taken as the sale proceed and used to determine

the capital gains. Further consideration would be given to the longer than one year holding

period of antique bed by client which entitles to 50% rebate in line with the discount method

highlighted in s. 115-25.

3. PAINTING

It is evident that the painting has been purchased in May 1985 which clearly precedes the

application of CGT on September 20, 1985. Since the given asset has been bought in a pre-CGT

4

The purchase date for the antique bed can be traced to 1986 implying that it cannot be placed in

the category of pre-CGT asset. Thus, CGT exemption cannot be availed for this asset. Further,

the stealing of antique bed has triggered CGT event A1 and hence it is imperative to compute the

underlying gains or losses. The first step in this direction is the determination of the cost base of

antique bed asset in accordance with the discussion carried out above. This has been carried out

below.

In relation to collectables as per s. 118-10, CGT consequences would not arise if the purchase

price does not $ 500 and thus condition is satisfied in the given case of antique bed which was

purchased for $ 3,500. With regards to disposal of antique bed, it has been stolen and therefore

the proceeds obtained from insurance would be taken as the sale proceed and used to determine

the capital gains. Further consideration would be given to the longer than one year holding

period of antique bed by client which entitles to 50% rebate in line with the discount method

highlighted in s. 115-25.

3. PAINTING

It is evident that the painting has been purchased in May 1985 which clearly precedes the

application of CGT on September 20, 1985. Since the given asset has been bought in a pre-CGT

4

era, hence it fall within the ambit of a pre-CGT era. Thereby, s. 149-10 would apply and hence

full exemption from CGT would apply for this asset (Nethercott, Richardson and Devos, 2016).

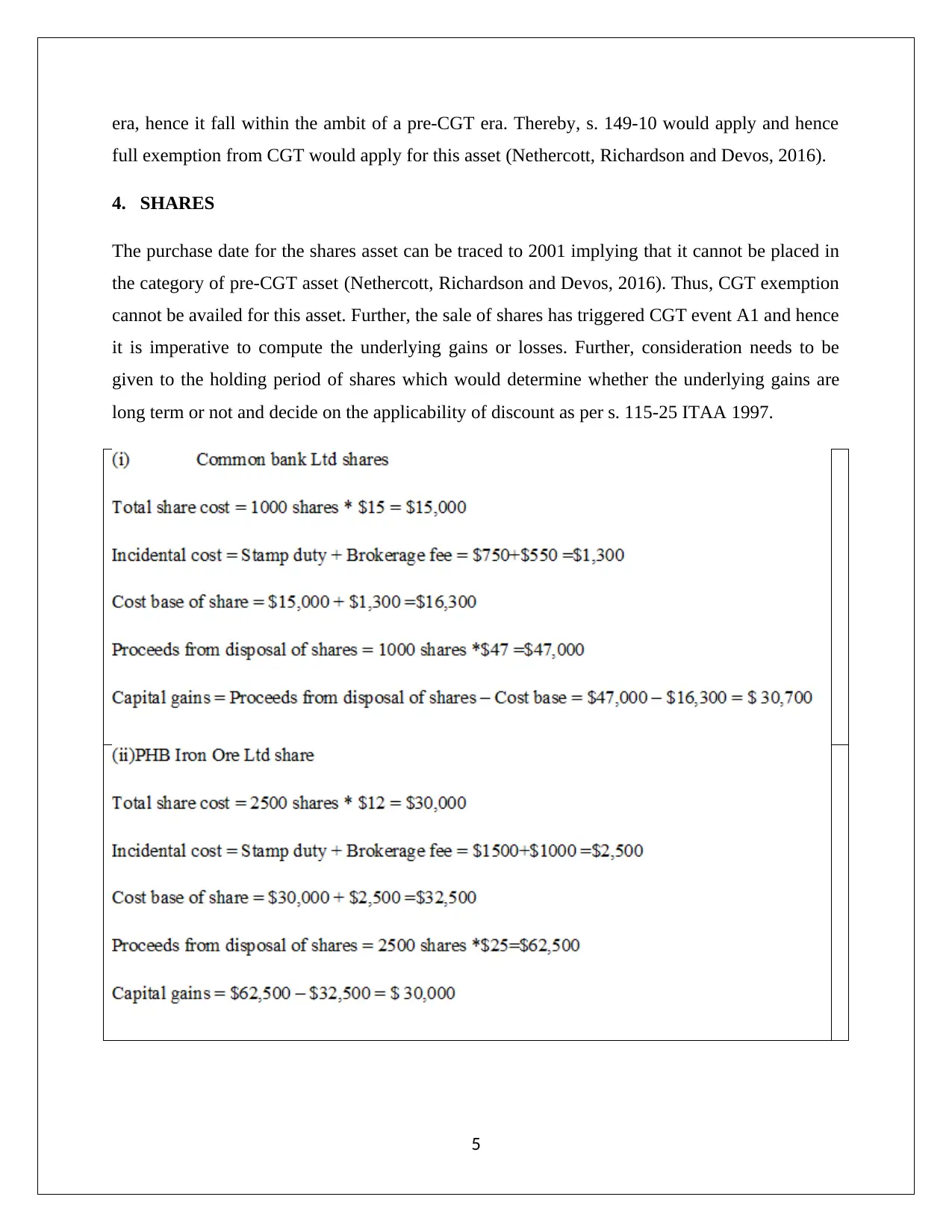

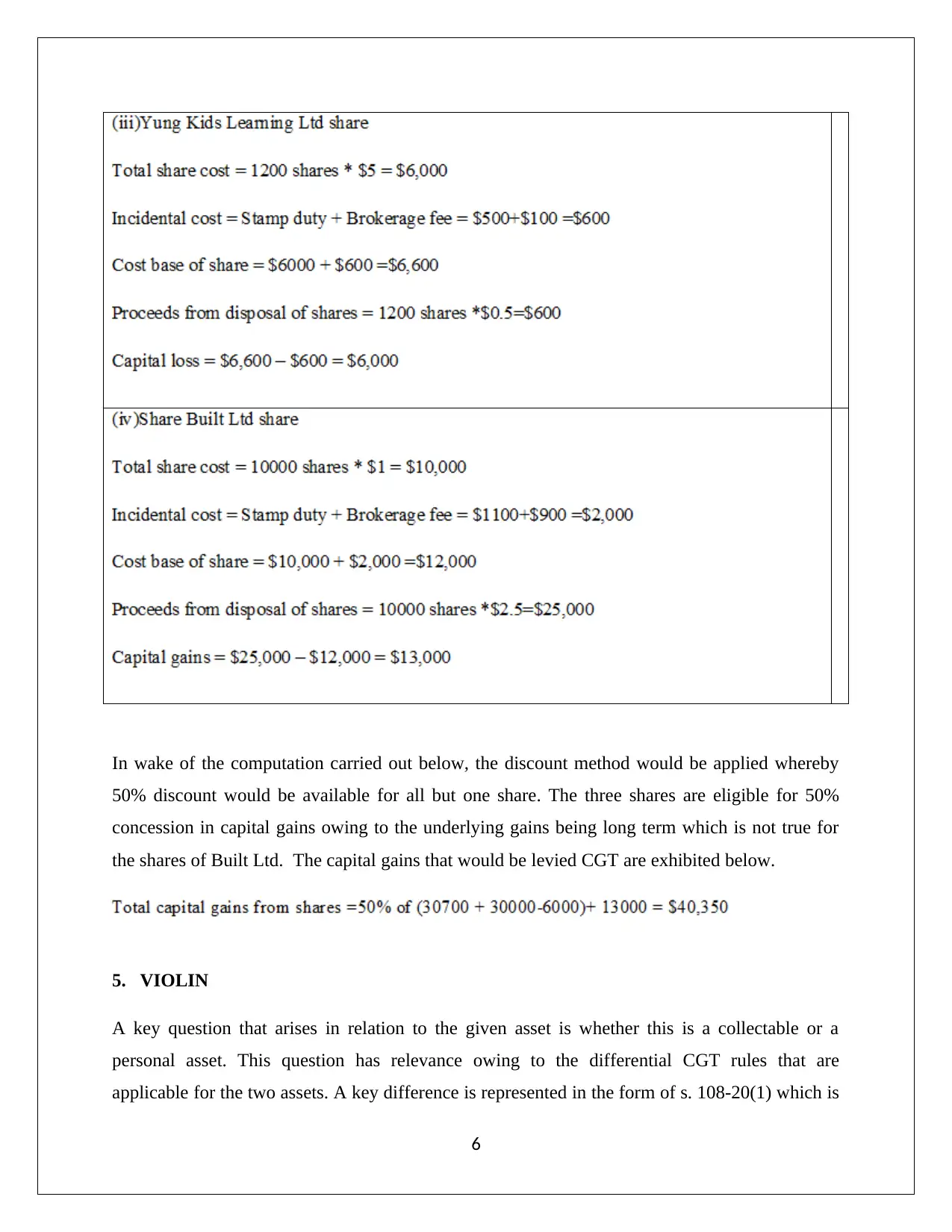

4. SHARES

The purchase date for the shares asset can be traced to 2001 implying that it cannot be placed in

the category of pre-CGT asset (Nethercott, Richardson and Devos, 2016). Thus, CGT exemption

cannot be availed for this asset. Further, the sale of shares has triggered CGT event A1 and hence

it is imperative to compute the underlying gains or losses. Further, consideration needs to be

given to the holding period of shares which would determine whether the underlying gains are

long term or not and decide on the applicability of discount as per s. 115-25 ITAA 1997.

5

full exemption from CGT would apply for this asset (Nethercott, Richardson and Devos, 2016).

4. SHARES

The purchase date for the shares asset can be traced to 2001 implying that it cannot be placed in

the category of pre-CGT asset (Nethercott, Richardson and Devos, 2016). Thus, CGT exemption

cannot be availed for this asset. Further, the sale of shares has triggered CGT event A1 and hence

it is imperative to compute the underlying gains or losses. Further, consideration needs to be

given to the holding period of shares which would determine whether the underlying gains are

long term or not and decide on the applicability of discount as per s. 115-25 ITAA 1997.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In wake of the computation carried out below, the discount method would be applied whereby

50% discount would be available for all but one share. The three shares are eligible for 50%

concession in capital gains owing to the underlying gains being long term which is not true for

the shares of Built Ltd. The capital gains that would be levied CGT are exhibited below.

5. VIOLIN

A key question that arises in relation to the given asset is whether this is a collectable or a

personal asset. This question has relevance owing to the differential CGT rules that are

applicable for the two assets. A key difference is represented in the form of s. 108-20(1) which is

6

50% discount would be available for all but one share. The three shares are eligible for 50%

concession in capital gains owing to the underlying gains being long term which is not true for

the shares of Built Ltd. The capital gains that would be levied CGT are exhibited below.

5. VIOLIN

A key question that arises in relation to the given asset is whether this is a collectable or a

personal asset. This question has relevance owing to the differential CGT rules that are

applicable for the two assets. A key difference is represented in the form of s. 108-20(1) which is

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

applicable only for personal use assets and demands that CGT must be levied only on those

assets which have a purchase price exceeding $ 10,000 (Deutsch, et.al., 2015). The

corresponding limit for collectables is $ 500 as exhibited by s. 118-10.

The asset in question would be a personal use asset considering the regular use by the client for

personal entertainment. Thus, it is not a collectable item but rather an asset which is of regular

use by the client. Further, the purchase price of the violin in question does not exceed $ 10,000

as it is only $ 6,500. Owing to this, the violin sale would not produce any CGT liability on the

client.

The cumulative taxable capital gains for the client are summarised below for the year 2017/2018.

Question 2

The key issue in the situation presented is to highlight the liability on account of Fringe Benefit

Tax (FBT) that would be payable by Rapid Heat due to the benefits that have been availed by

Jasmine (the employee)..

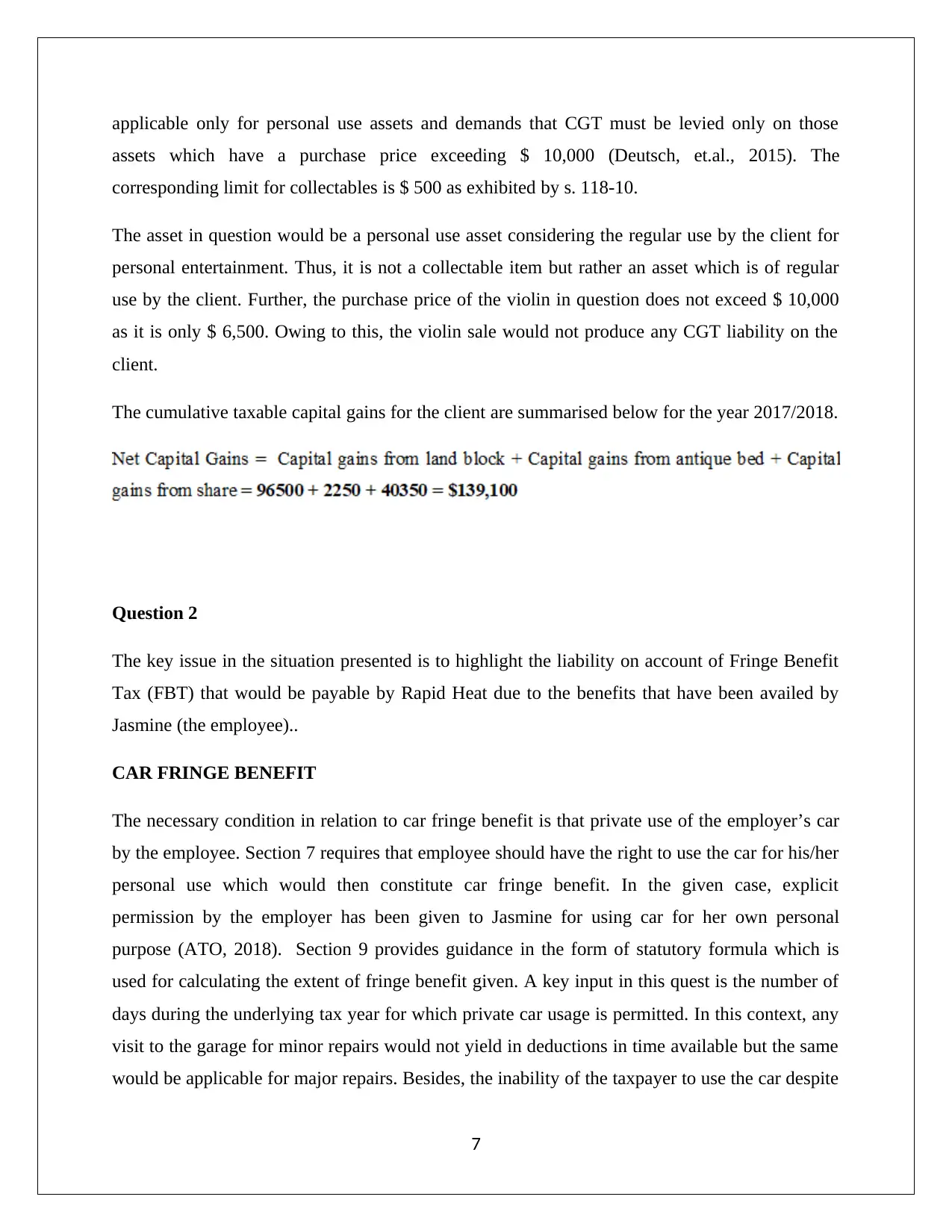

CAR FRINGE BENEFIT

The necessary condition in relation to car fringe benefit is that private use of the employer’s car

by the employee. Section 7 requires that employee should have the right to use the car for his/her

personal use which would then constitute car fringe benefit. In the given case, explicit

permission by the employer has been given to Jasmine for using car for her own personal

purpose (ATO, 2018). Section 9 provides guidance in the form of statutory formula which is

used for calculating the extent of fringe benefit given. A key input in this quest is the number of

days during the underlying tax year for which private car usage is permitted. In this context, any

visit to the garage for minor repairs would not yield in deductions in time available but the same

would be applicable for major repairs. Besides, the inability of the taxpayer to use the car despite

7

assets which have a purchase price exceeding $ 10,000 (Deutsch, et.al., 2015). The

corresponding limit for collectables is $ 500 as exhibited by s. 118-10.

The asset in question would be a personal use asset considering the regular use by the client for

personal entertainment. Thus, it is not a collectable item but rather an asset which is of regular

use by the client. Further, the purchase price of the violin in question does not exceed $ 10,000

as it is only $ 6,500. Owing to this, the violin sale would not produce any CGT liability on the

client.

The cumulative taxable capital gains for the client are summarised below for the year 2017/2018.

Question 2

The key issue in the situation presented is to highlight the liability on account of Fringe Benefit

Tax (FBT) that would be payable by Rapid Heat due to the benefits that have been availed by

Jasmine (the employee)..

CAR FRINGE BENEFIT

The necessary condition in relation to car fringe benefit is that private use of the employer’s car

by the employee. Section 7 requires that employee should have the right to use the car for his/her

personal use which would then constitute car fringe benefit. In the given case, explicit

permission by the employer has been given to Jasmine for using car for her own personal

purpose (ATO, 2018). Section 9 provides guidance in the form of statutory formula which is

used for calculating the extent of fringe benefit given. A key input in this quest is the number of

days during the underlying tax year for which private car usage is permitted. In this context, any

visit to the garage for minor repairs would not yield in deductions in time available but the same

would be applicable for major repairs. Besides, the inability of the taxpayer to use the car despite

7

being available would not result in any time deduction (Barkoczy, 2017). Hence, in the given

case, no deduction would be considered for the time spent in garage since minor repairs and also

the days at car parking since the car availability was intact and only Jasmine was not available to

use the car.

For ascertaining the car fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 1 Good) = 2.0802

FBT rate (2017/2018) = 47%

Days of allowed private usage in 2017/2018 = 335

LOAN FRINGE BENEFIT

For the doling out of loan fringe benefit to employee, a key condition is that the interest rate

charged must be lower than the benchmark interest rate for the given year under consideration.

The benchmark interest rate is revised on an annual basis by the RBA (Reserve Bank of

Australia) (ATO, 2018). Providing of loan lesser than this rate implies that the employee would

have lower interest expense and hence would be benefitted.

The case details highlight extension of loan to Jasmine at an interest cost of 4.25% p.a. This is

clearly 100 basis points lower than the applicable benchmark rate of 5.25% p.a. for the year

under consideration. Hence, there is extension of loan fringe benefits which would result in FBT

liability to apply on Rapid Heat (the employer).

For ascertaining the loan fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 2 Good) = 1.8868

FBT rate (2017/2018) = 47% (ATO, 2017)

Days of loan usage in 2017/2018 (September 1, 2017 to March 31, 2018) = 212

8

case, no deduction would be considered for the time spent in garage since minor repairs and also

the days at car parking since the car availability was intact and only Jasmine was not available to

use the car.

For ascertaining the car fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 1 Good) = 2.0802

FBT rate (2017/2018) = 47%

Days of allowed private usage in 2017/2018 = 335

LOAN FRINGE BENEFIT

For the doling out of loan fringe benefit to employee, a key condition is that the interest rate

charged must be lower than the benchmark interest rate for the given year under consideration.

The benchmark interest rate is revised on an annual basis by the RBA (Reserve Bank of

Australia) (ATO, 2018). Providing of loan lesser than this rate implies that the employee would

have lower interest expense and hence would be benefitted.

The case details highlight extension of loan to Jasmine at an interest cost of 4.25% p.a. This is

clearly 100 basis points lower than the applicable benchmark rate of 5.25% p.a. for the year

under consideration. Hence, there is extension of loan fringe benefits which would result in FBT

liability to apply on Rapid Heat (the employer).

For ascertaining the loan fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 2 Good) = 1.8868

FBT rate (2017/2018) = 47% (ATO, 2017)

Days of loan usage in 2017/2018 (September 1, 2017 to March 31, 2018) = 212

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Also, deduction is also permitted for the employer as per s. 18, FBTAA. However, a necessary

condition is that the loan must be used for generation of income by the employee. Further,

deduction is not available if the loan money is used by any associate of employee irrespective of

income being produced. In the given case, 90% of the loan amount i.e. $450,000 is used by

Jasmine while the remainder 10% is being used by her husband. A holiday home has been

purchased by Jasmine which is quite likely to produce income as rent since it would not be used

as a main residence. As a result, possible deductions may be claimed by employer based on

income generation by the holiday home.

EXPENSES FRINGE BENEFIT

The expenses of personal nature must be borne by the employees themselves. However, some

employers help the employees in meeting these expenses by paying for these and such acts result

in expense fringe benefit as outlined in s. 20, FBTAA 1986 (Barkoczy, 2017). For the given

circumstance, Rapid Heat is a manufacturer of electric heaters. Jasmine wants to purchase an

electric heater manufactured by Rapid Heat for her personal use. The price at which these heaters

are sold in the market by Rapid Heat is $ 2,600 per piece. Hence, the same amount should be

paid by jasmine. However, the employer shoulders this personal expense burden and hence pays

half of the amount, thus leaving Jasmine to pay the balance amount of $ 1,300.

For ascertaining the expense fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 1 Good) = 2.0802

FBT rate (2017/2018) = 47%

Personal savings realised = $1,300

9

condition is that the loan must be used for generation of income by the employee. Further,

deduction is not available if the loan money is used by any associate of employee irrespective of

income being produced. In the given case, 90% of the loan amount i.e. $450,000 is used by

Jasmine while the remainder 10% is being used by her husband. A holiday home has been

purchased by Jasmine which is quite likely to produce income as rent since it would not be used

as a main residence. As a result, possible deductions may be claimed by employer based on

income generation by the holiday home.

EXPENSES FRINGE BENEFIT

The expenses of personal nature must be borne by the employees themselves. However, some

employers help the employees in meeting these expenses by paying for these and such acts result

in expense fringe benefit as outlined in s. 20, FBTAA 1986 (Barkoczy, 2017). For the given

circumstance, Rapid Heat is a manufacturer of electric heaters. Jasmine wants to purchase an

electric heater manufactured by Rapid Heat for her personal use. The price at which these heaters

are sold in the market by Rapid Heat is $ 2,600 per piece. Hence, the same amount should be

paid by jasmine. However, the employer shoulders this personal expense burden and hence pays

half of the amount, thus leaving Jasmine to pay the balance amount of $ 1,300.

For ascertaining the expense fringe benefit taxable value, the key inputs are as follows.

Gross up factor (2017/2018 Type 1 Good) = 2.0802

FBT rate (2017/2018) = 47%

Personal savings realised = $1,300

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) It is known that Jasmine now utilises the complete amount of $ 500,000. The addition is of $

50,000 which she is investing in Telstra shares in a manner similar to her husband before.

Clearly, dividend income would be generated which is assessable income in accordance with s.

6(5) ITAA 1997. As a result, s. 20 FBTAA would apply and additional deduction to the extent of

$ 500 would be available on the FBT liability imposed on the employer as explained below.

10

50,000 which she is investing in Telstra shares in a manner similar to her husband before.

Clearly, dividend income would be generated which is assessable income in accordance with s.

6(5) ITAA 1997. As a result, s. 20 FBTAA would apply and additional deduction to the extent of

$ 500 would be available on the FBT liability imposed on the employer as explained below.

10

References

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 28 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 28 September 2018)

ATO, (2018) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 28

September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 28

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 115.25 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.25.html (Accessed: 28

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

11

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 28 September 2018)

ATO, (2017) Taxation Determination –TD 2017/3 [Online].

http://law.ato.gov.au/atolaw/view.htm?docid=%22TXD%2FTD20173%2FNAT%2FATO

%2F00001%22 (Accessed: 28 September 2018)

ATO, (2018) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 28

September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 149.10 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s149.10.html (Accessed: 28

September 2018)

Austlii, (2018 b) Income Tax Assessment Act 1997- SECT 115.25 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.25.html (Accessed: 28

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.