The Impact of Computerised Accounting Systems on Financial Reporting in Maldives SMEs

VerifiedAdded on 2023/06/15

|80

|18849

|104

AI Summary

This paper analyses the impact of computerised accounting systems on financial reporting in Maldives SMEs. It explores the quality of financial reports and the effect of computerised accounting systems on it. The study concludes that computerised accounting systems have a positive effect on financial reporting in Maldives SMEs.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN

THE FINANCIAL REPORTING AMONG SMES IN MALDIVES

The impact of using computerised accounting systems (CAS) in financial reporting among SMEs

in Maldives

Name of the Student:

Name of the University:

Author’s Note:

THE FINANCIAL REPORTING AMONG SMES IN MALDIVES

The impact of using computerised accounting systems (CAS) in financial reporting among SMEs

in Maldives

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Abstract

This paper is related to having an understanding of the impact of “Computerised Accounting

Systems” in the financial documentation among the SMEs in Maldives. Computerised

Accounting Systems are a new tool and technology that are available to the organizations with

the help of which companies are able operate their business in a much better way create financial

statements that are ideal for the companies in order to keep track of all their records and

transactions and assist in the process decision making for the business. The objective of the paper

has been fundamental in understanding the aspects with regards to which the results will be

attained. In the same manner, data has been collected and thereafter data analysis process has

been undertaken with the help of which effective level of results are obtained for this paper. The

results that have been obtained expresses that “Computerised Accounting System” has a positive

effect on the financial reporting of the SMEs in Maldives and effective supervision and

maintenance can enhance the activities of the process in the SMEs as well as in the other

industries in Maldives in the future.

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Abstract

This paper is related to having an understanding of the impact of “Computerised Accounting

Systems” in the financial documentation among the SMEs in Maldives. Computerised

Accounting Systems are a new tool and technology that are available to the organizations with

the help of which companies are able operate their business in a much better way create financial

statements that are ideal for the companies in order to keep track of all their records and

transactions and assist in the process decision making for the business. The objective of the paper

has been fundamental in understanding the aspects with regards to which the results will be

attained. In the same manner, data has been collected and thereafter data analysis process has

been undertaken with the help of which effective level of results are obtained for this paper. The

results that have been obtained expresses that “Computerised Accounting System” has a positive

effect on the financial reporting of the SMEs in Maldives and effective supervision and

maintenance can enhance the activities of the process in the SMEs as well as in the other

industries in Maldives in the future.

2

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Table of Contents

Chapter 1: Introduction....................................................................................................................6

1.1 Background of the Study.......................................................................................................6

1.1.1 Computerised Accounting System.................................................................................8

1.1.2 Quality of the Financial Reports.....................................................................................9

1.1.3 Effect of Computerised Accounting System on the Financial Report Quality.............10

1.2 Statement of the Problem.....................................................................................................11

1.3 Research Objectives.............................................................................................................12

1.4 Research Question...............................................................................................................12

1.5 Significance of the Study.....................................................................................................13

1.6 Scope and Limitations of the Study.....................................................................................13

Chapter 2: Literature Review.........................................................................................................14

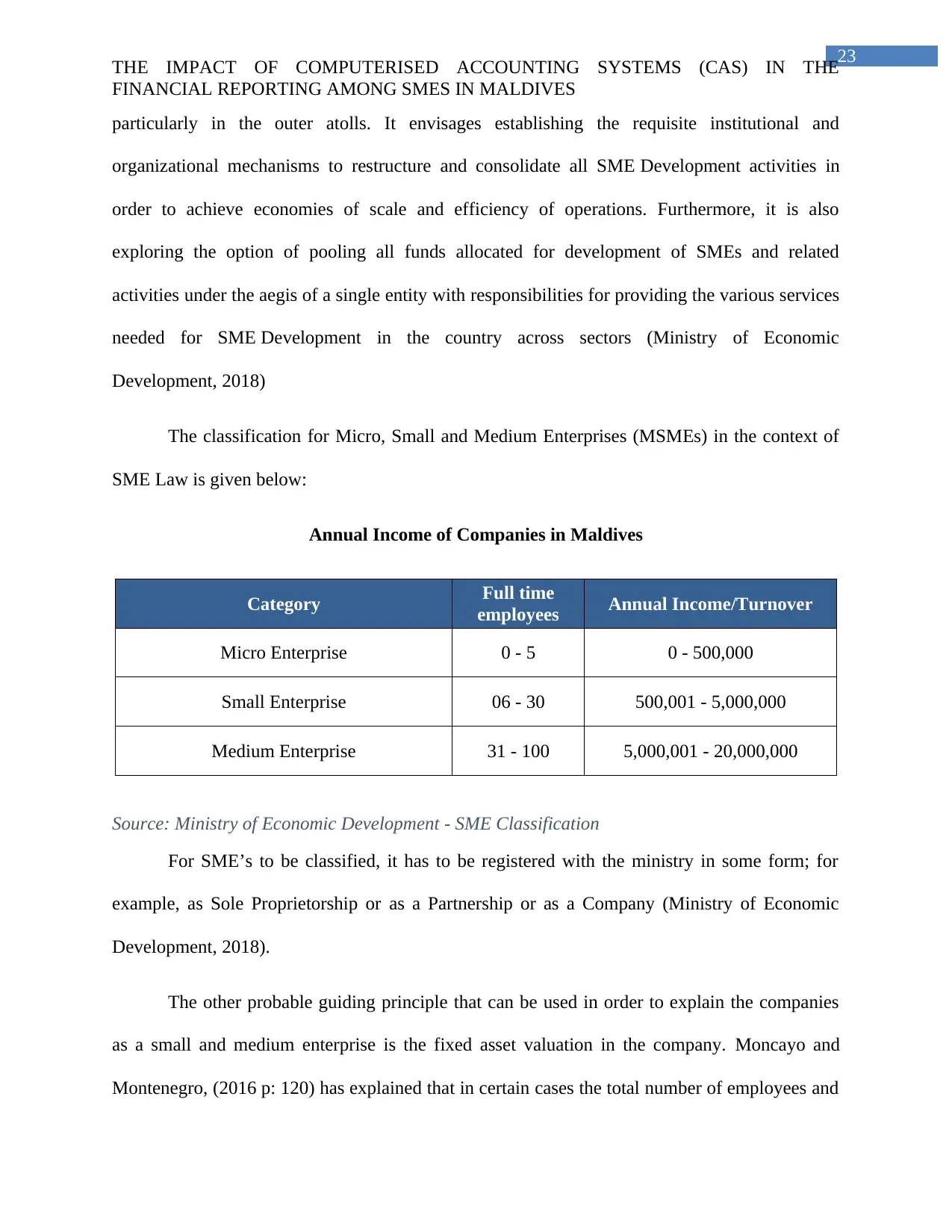

2.1 Related Studies....................................................................................................................20

2.2Small and medium enterprises in Maldives..........................................................................22

2.3Factors that influence computerised accounting system......................................................25

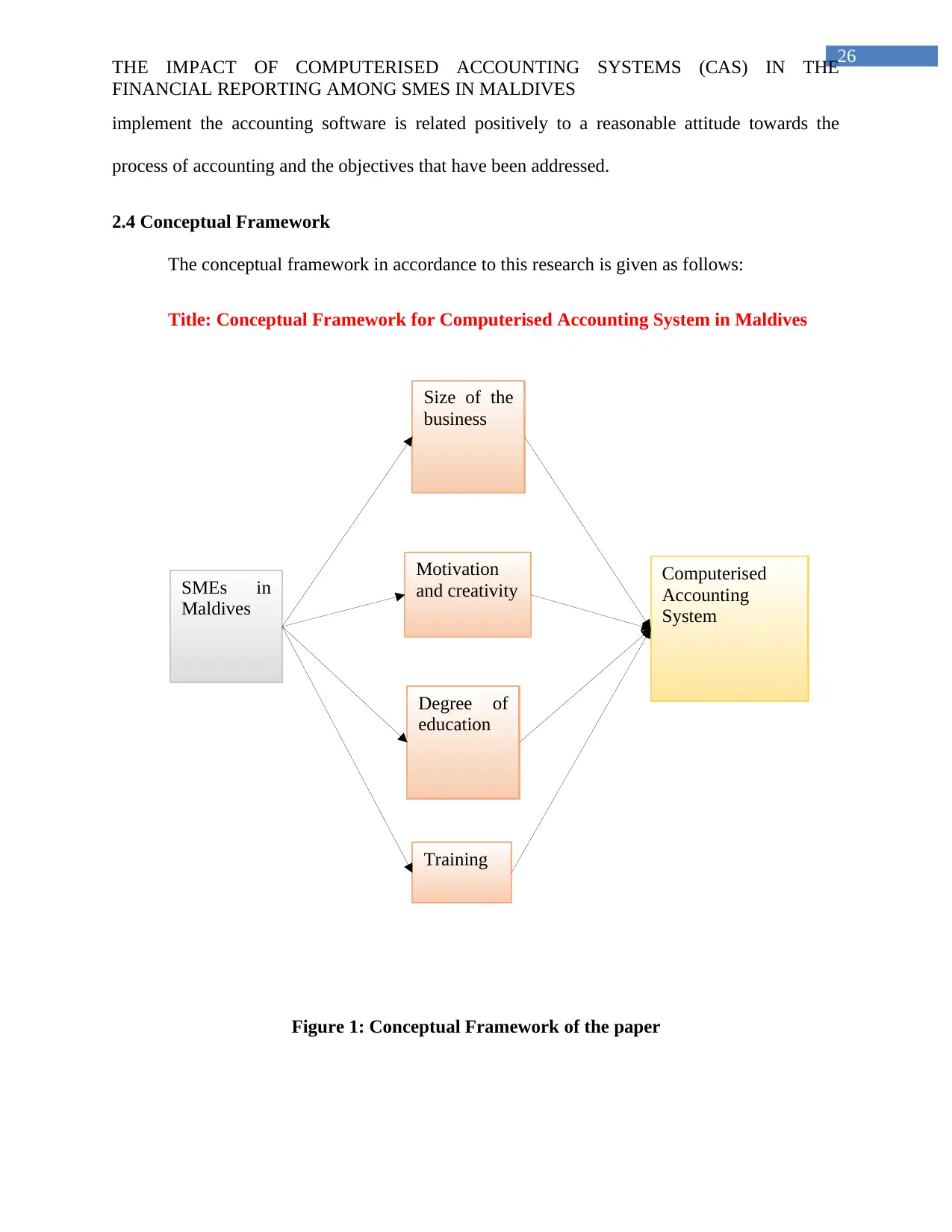

2.4 Conceptual Framework........................................................................................................26

2.5 Summary of the Literature...................................................................................................27

Chapter 3: Research Methodology................................................................................................28

3.1 Introduction..........................................................................................................................28

3.2 Research Philosophy............................................................................................................28

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Table of Contents

Chapter 1: Introduction....................................................................................................................6

1.1 Background of the Study.......................................................................................................6

1.1.1 Computerised Accounting System.................................................................................8

1.1.2 Quality of the Financial Reports.....................................................................................9

1.1.3 Effect of Computerised Accounting System on the Financial Report Quality.............10

1.2 Statement of the Problem.....................................................................................................11

1.3 Research Objectives.............................................................................................................12

1.4 Research Question...............................................................................................................12

1.5 Significance of the Study.....................................................................................................13

1.6 Scope and Limitations of the Study.....................................................................................13

Chapter 2: Literature Review.........................................................................................................14

2.1 Related Studies....................................................................................................................20

2.2Small and medium enterprises in Maldives..........................................................................22

2.3Factors that influence computerised accounting system......................................................25

2.4 Conceptual Framework........................................................................................................26

2.5 Summary of the Literature...................................................................................................27

Chapter 3: Research Methodology................................................................................................28

3.1 Introduction..........................................................................................................................28

3.2 Research Philosophy............................................................................................................28

3

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

3.3 Research Approach..............................................................................................................29

3.4 Research Design..................................................................................................................31

3.5 Quantitative Data.................................................................................................................32

3.6 Primary Data........................................................................................................................32

3.7 Sample Size.........................................................................................................................33

3.8 Access to the respondents....................................................................................................33

3.9 Data Analysis.......................................................................................................................34

3.10 Ethical Considerations.......................................................................................................34

Chapter 4: Data Analysis and Discussion......................................................................................35

4.1 Introduction..........................................................................................................................35

4.2 Frequency Analysis.............................................................................................................35

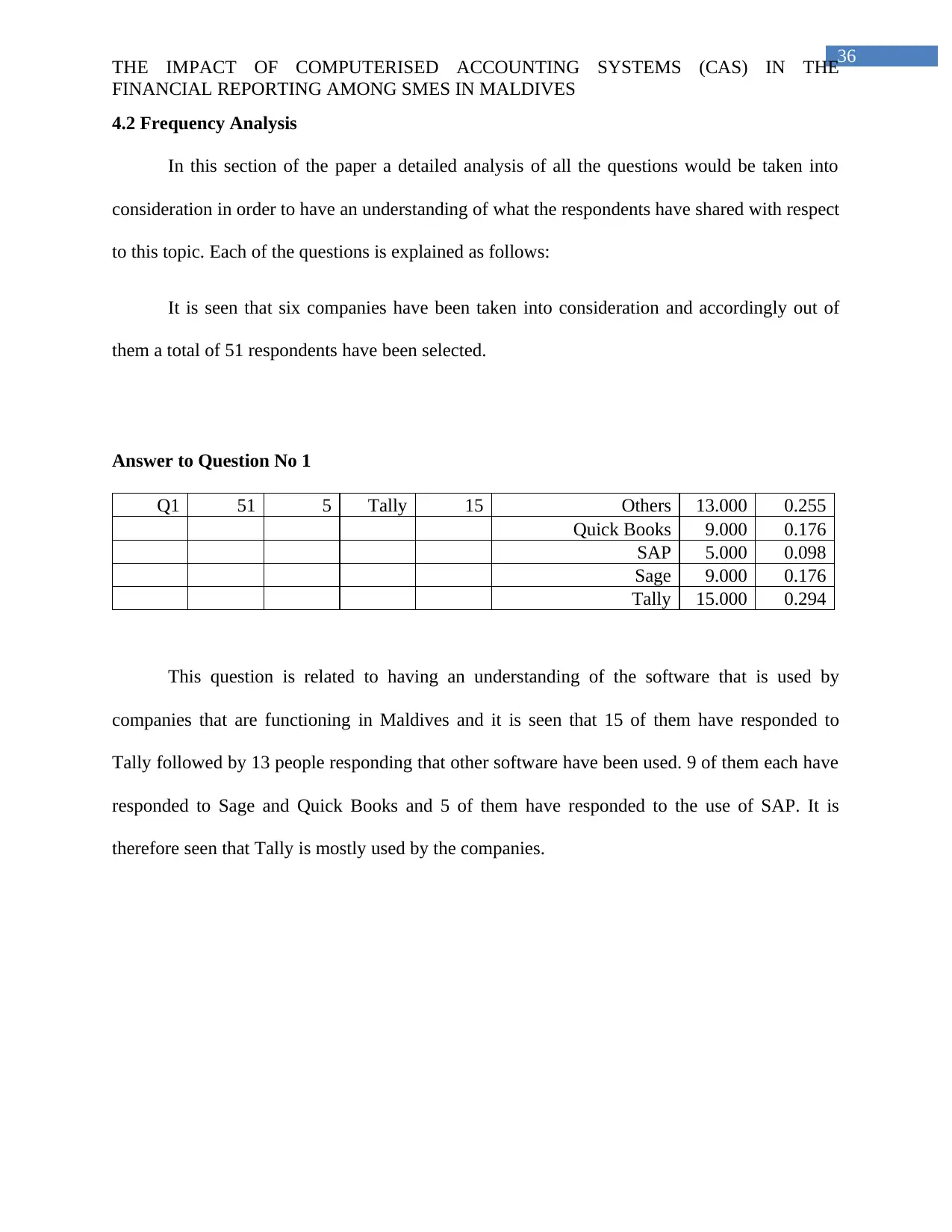

Answer to Question No 1......................................................................................................36

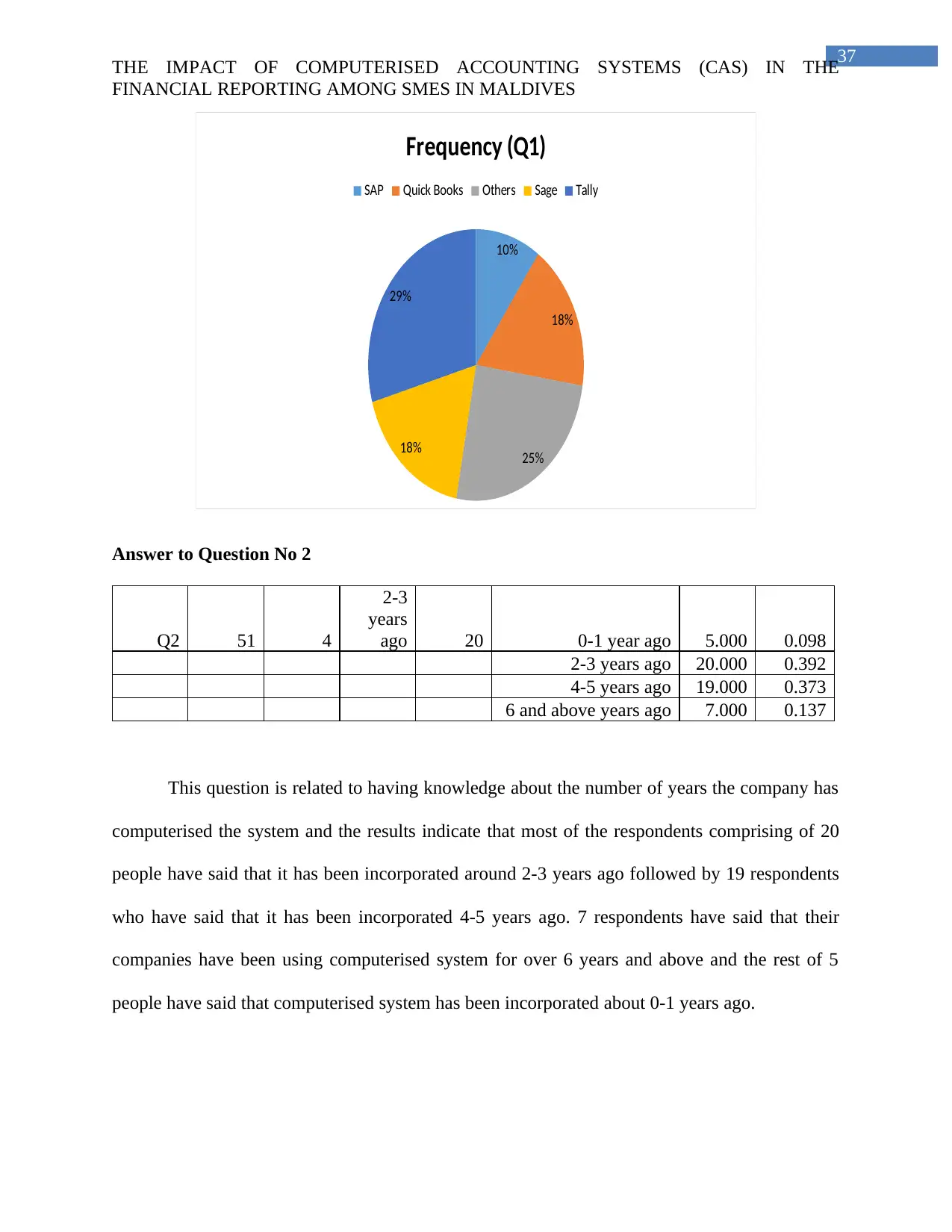

Answer to Question No 2......................................................................................................36

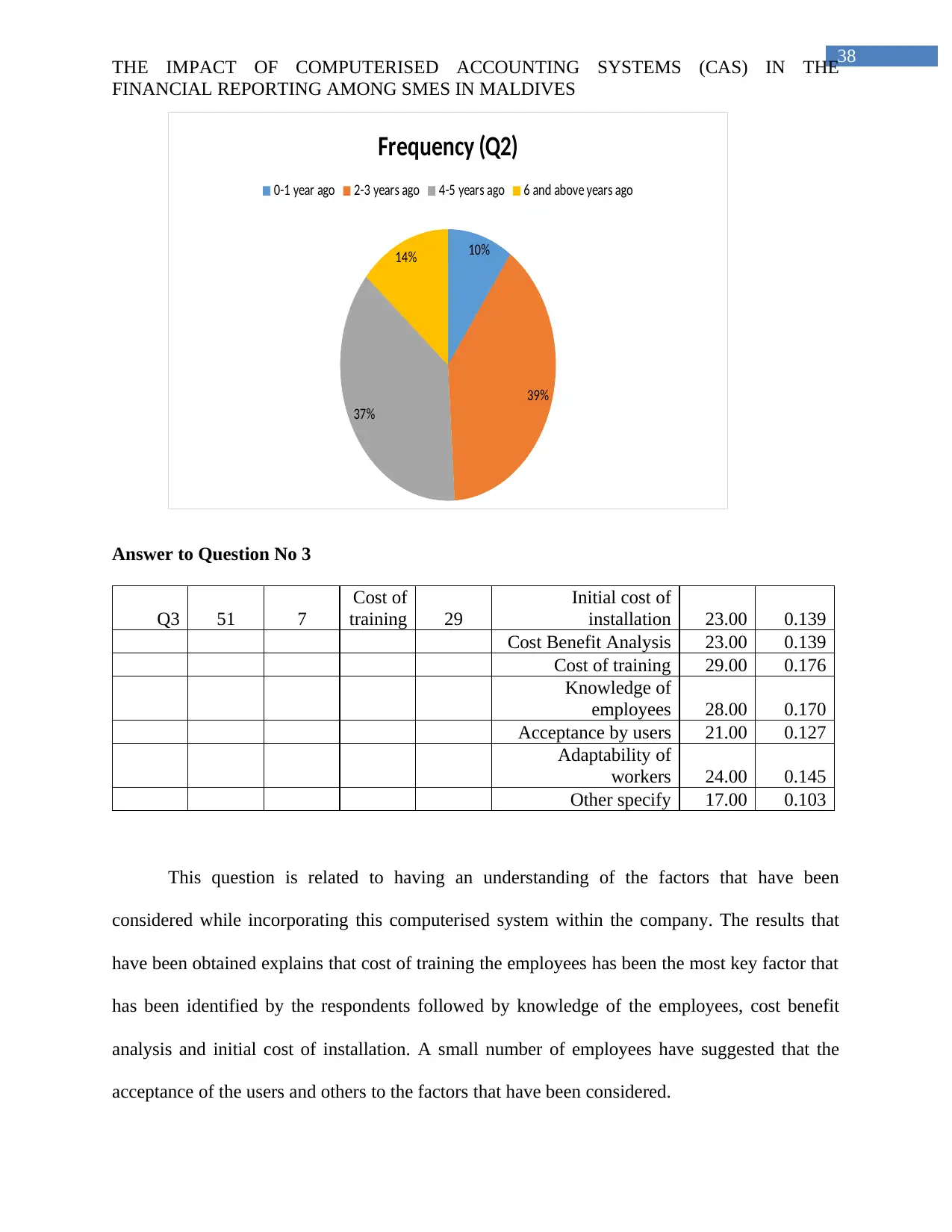

Answer to Question No 3......................................................................................................37

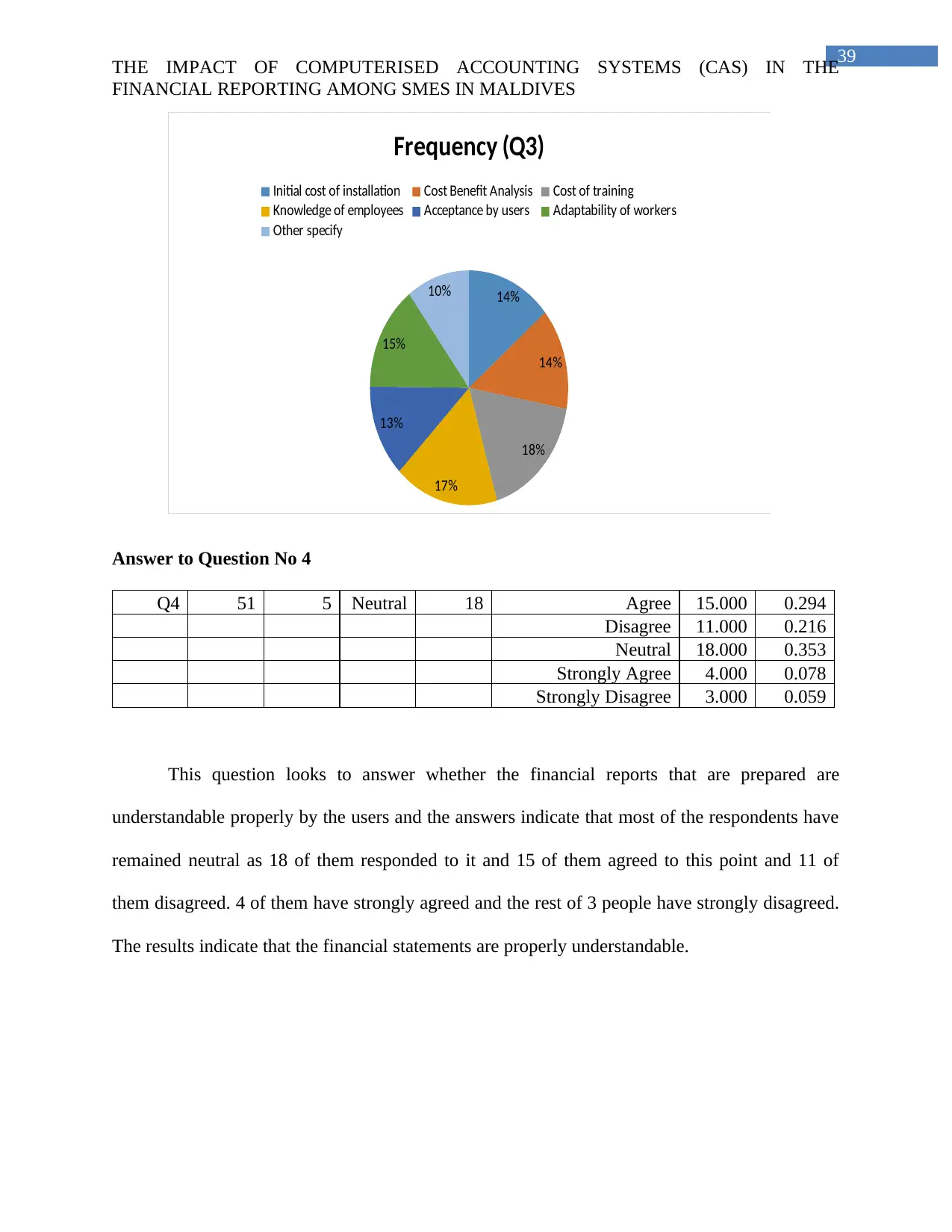

Answer to Question No 4......................................................................................................38

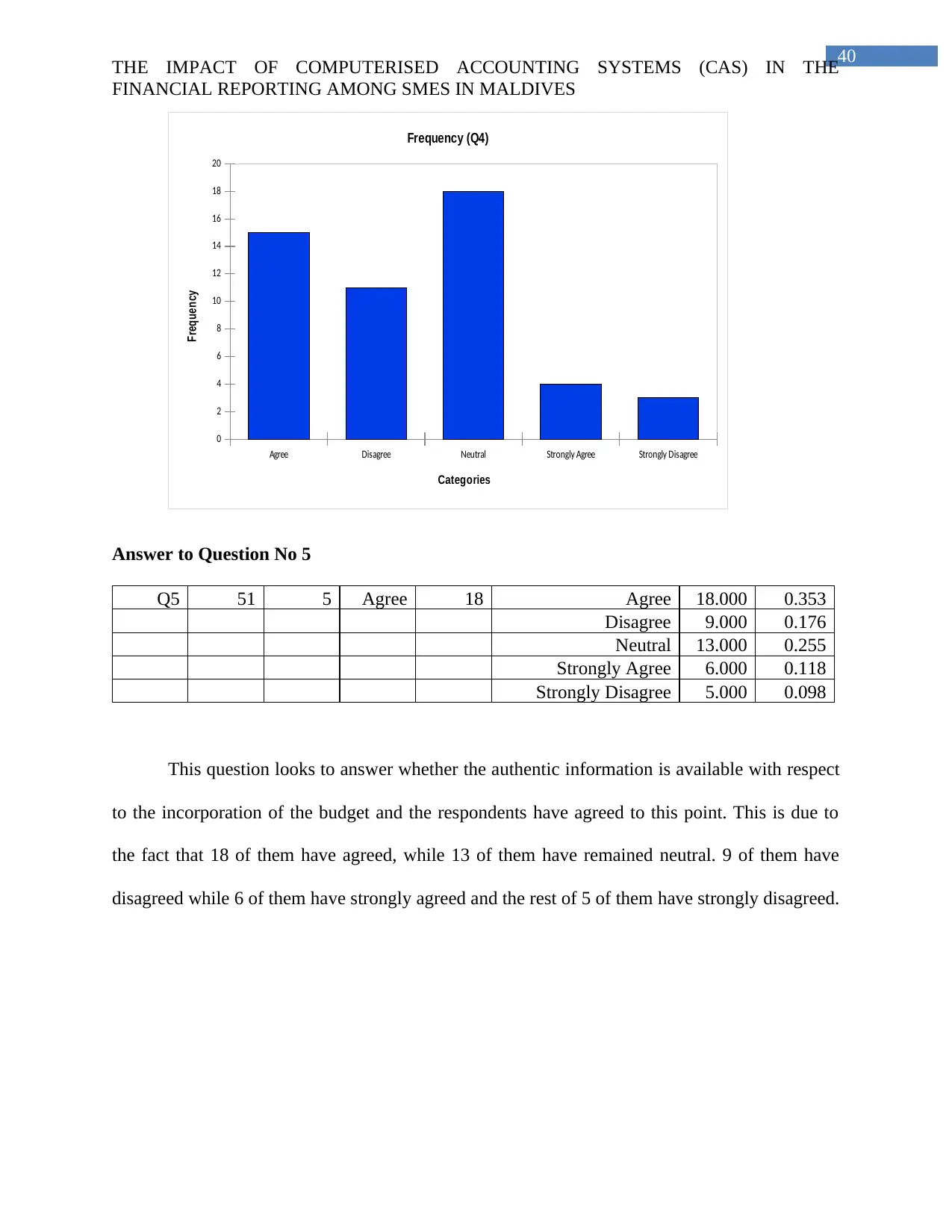

Answer to Question No 5......................................................................................................39

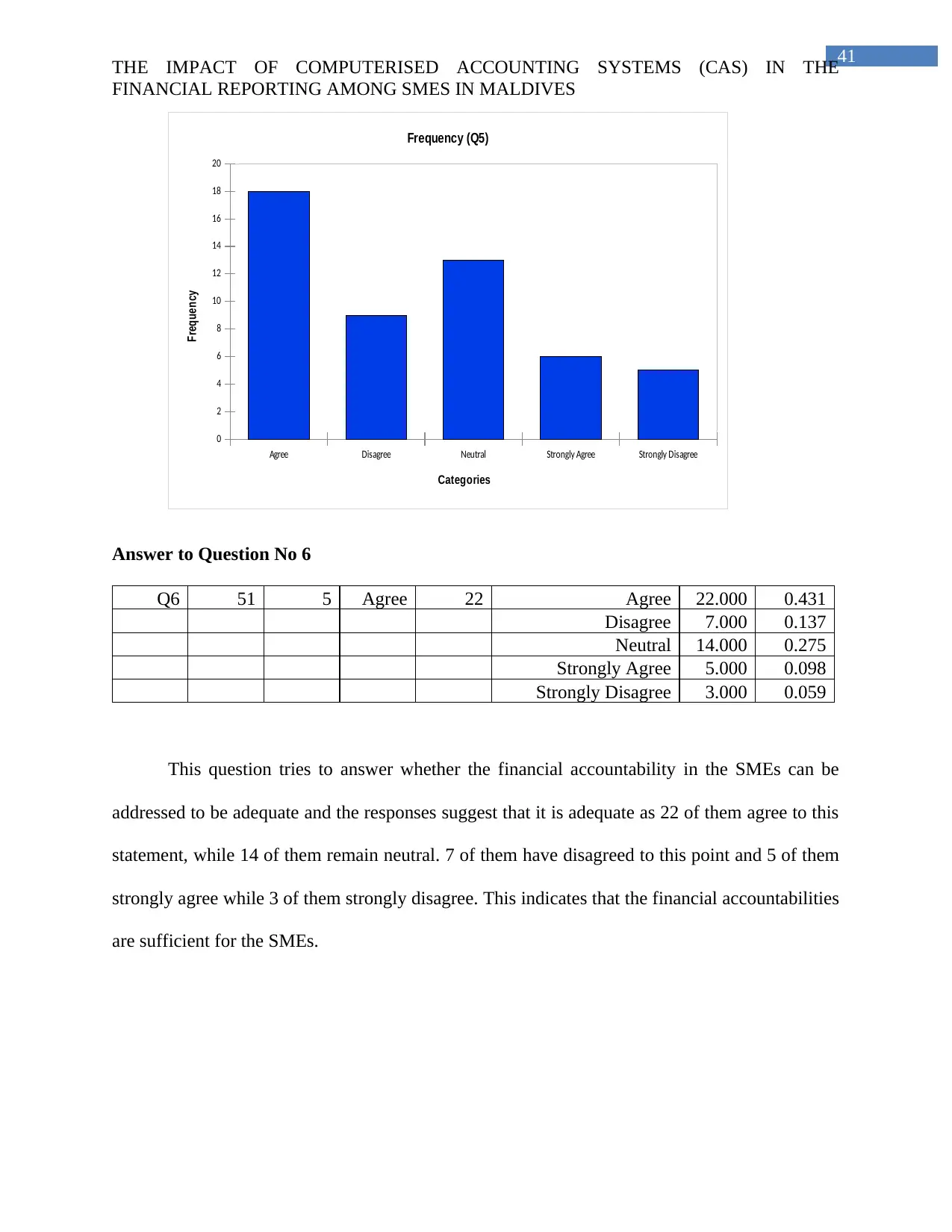

Answer to Question No 6......................................................................................................40

Answer to Question No 7......................................................................................................41

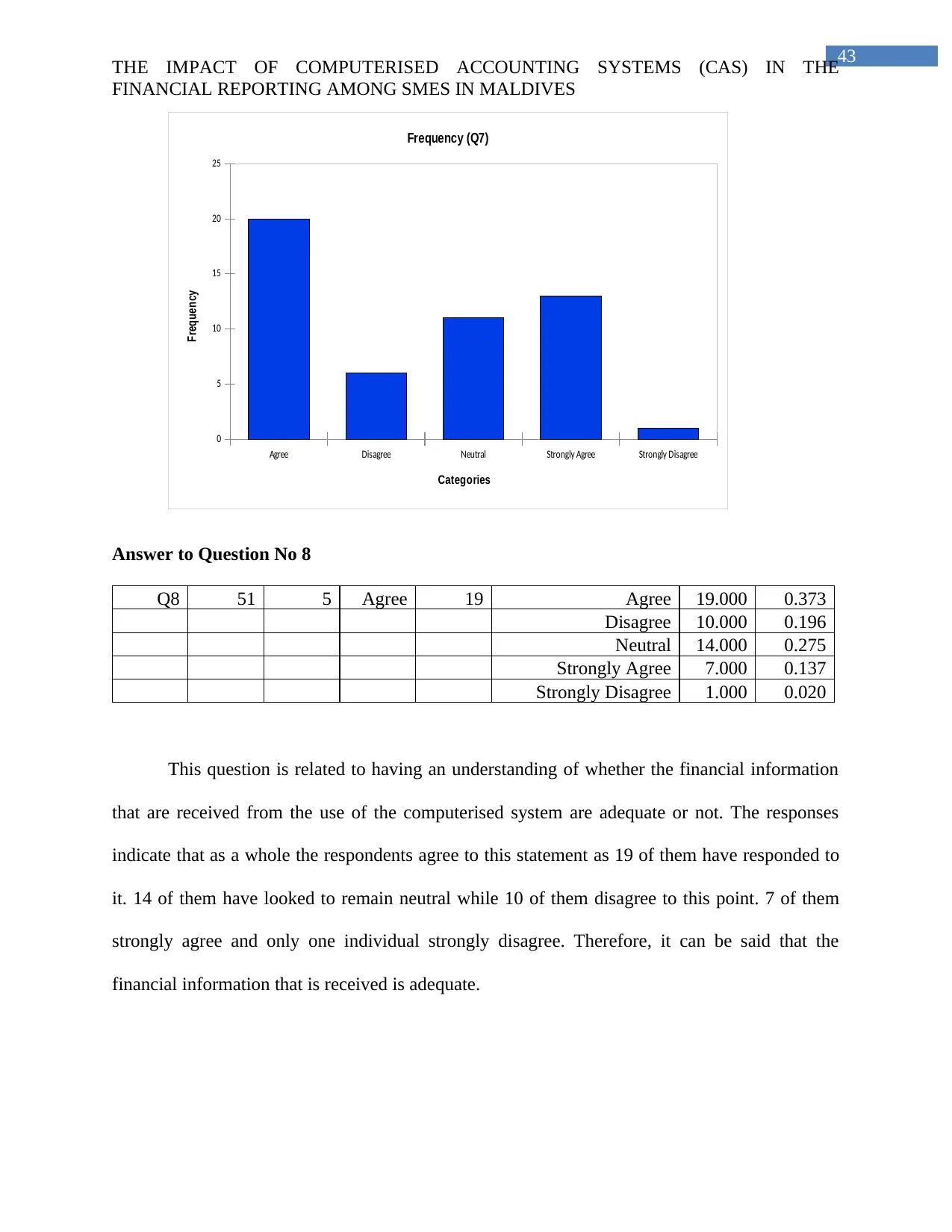

Answer to Question No 8......................................................................................................42

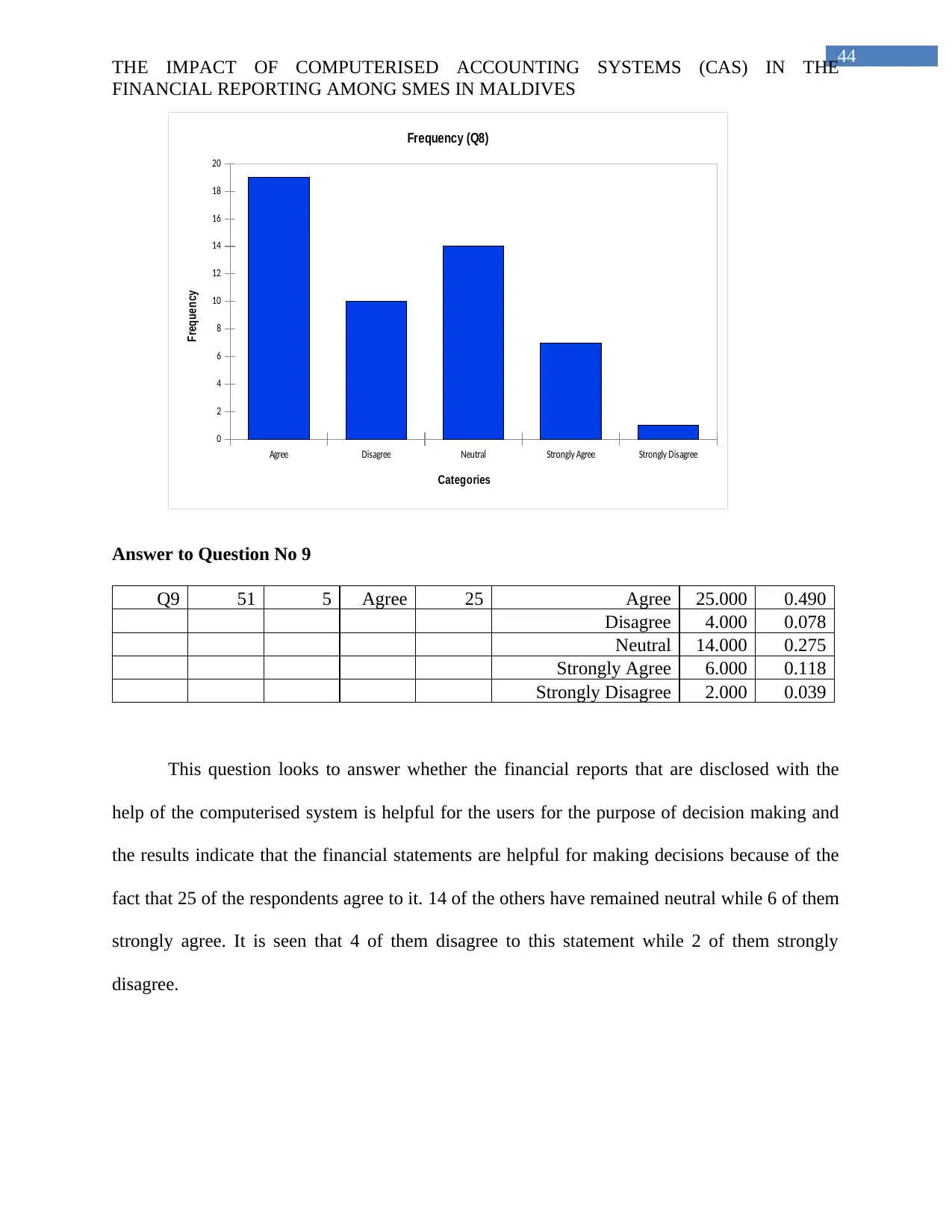

Answer to Question No 9......................................................................................................43

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

3.3 Research Approach..............................................................................................................29

3.4 Research Design..................................................................................................................31

3.5 Quantitative Data.................................................................................................................32

3.6 Primary Data........................................................................................................................32

3.7 Sample Size.........................................................................................................................33

3.8 Access to the respondents....................................................................................................33

3.9 Data Analysis.......................................................................................................................34

3.10 Ethical Considerations.......................................................................................................34

Chapter 4: Data Analysis and Discussion......................................................................................35

4.1 Introduction..........................................................................................................................35

4.2 Frequency Analysis.............................................................................................................35

Answer to Question No 1......................................................................................................36

Answer to Question No 2......................................................................................................36

Answer to Question No 3......................................................................................................37

Answer to Question No 4......................................................................................................38

Answer to Question No 5......................................................................................................39

Answer to Question No 6......................................................................................................40

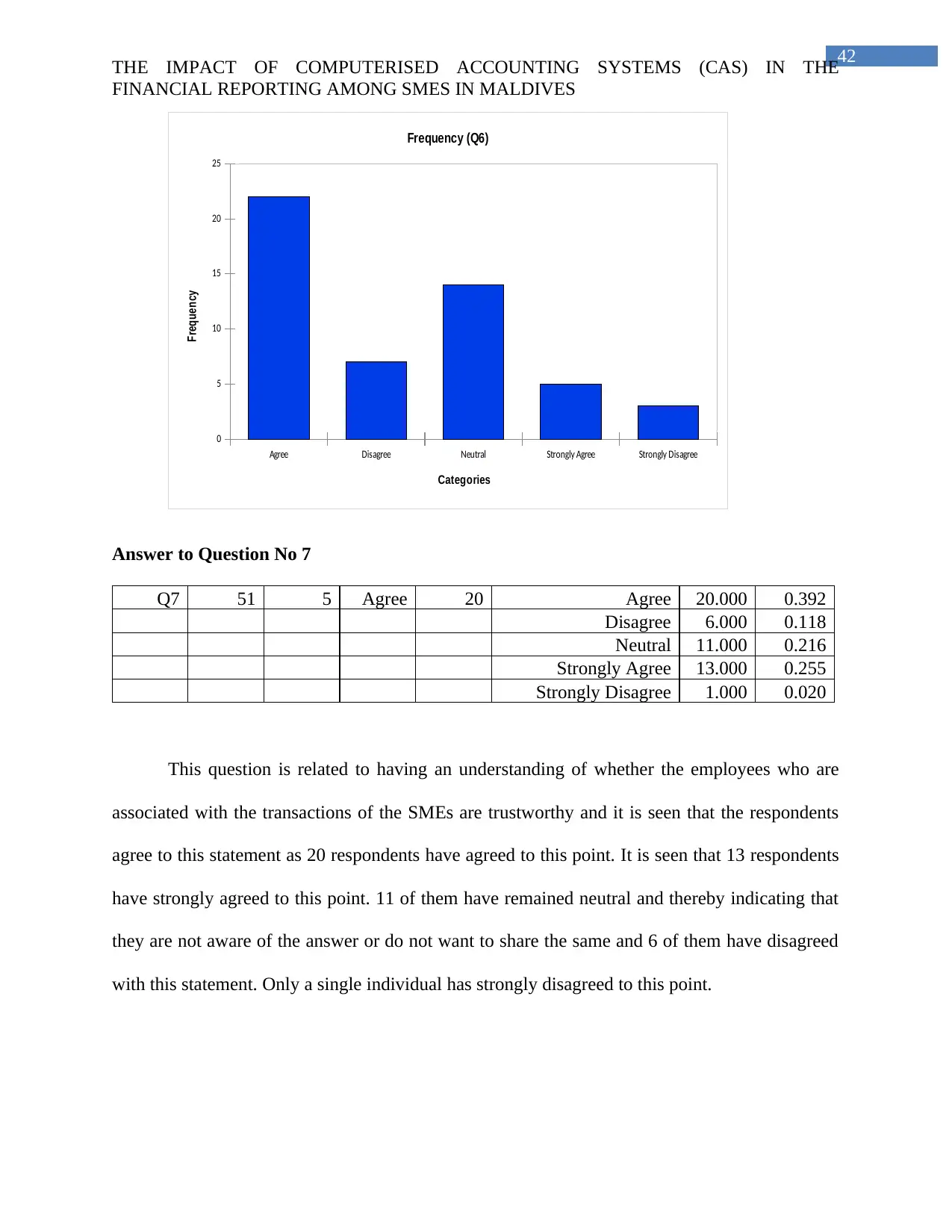

Answer to Question No 7......................................................................................................41

Answer to Question No 8......................................................................................................42

Answer to Question No 9......................................................................................................43

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

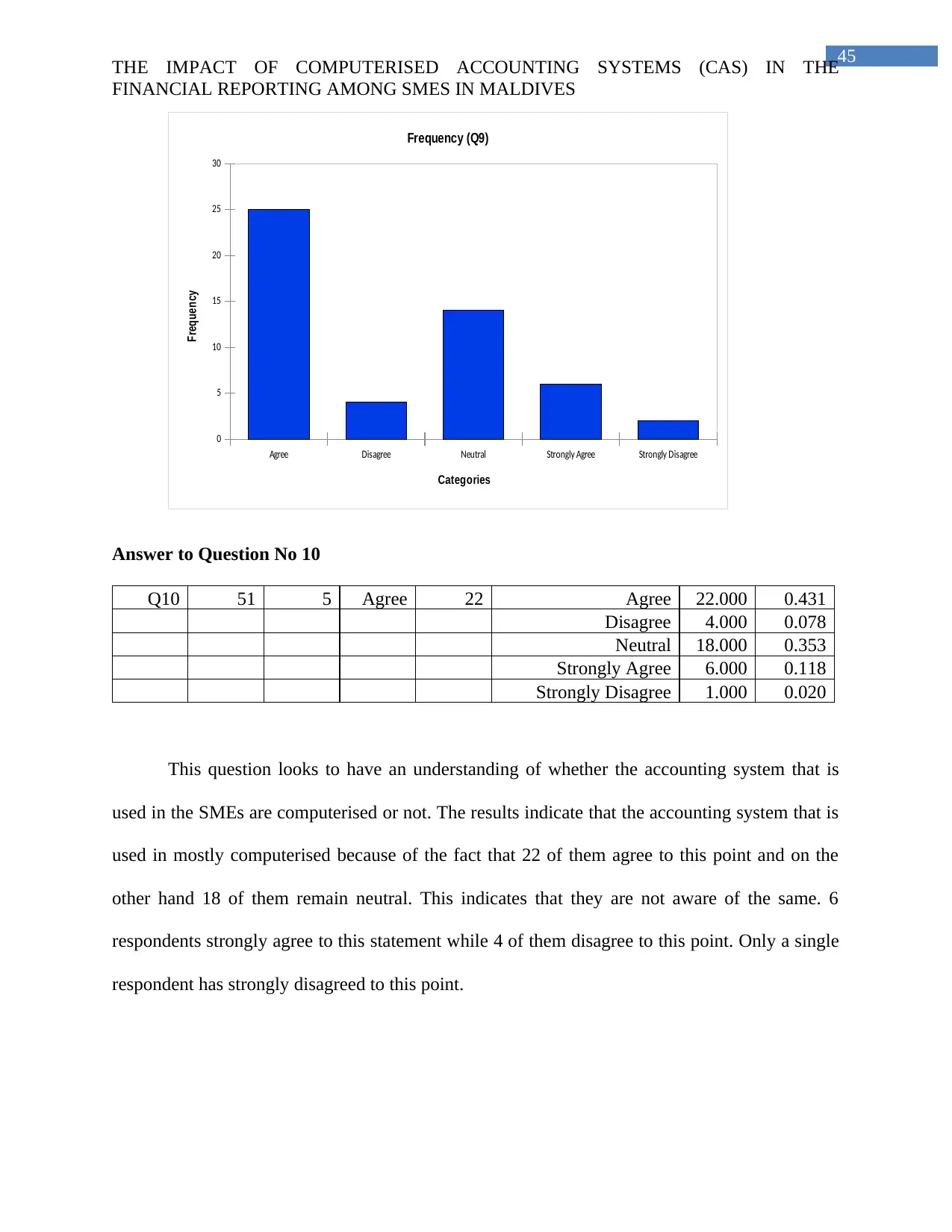

Answer to Question No 10....................................................................................................44

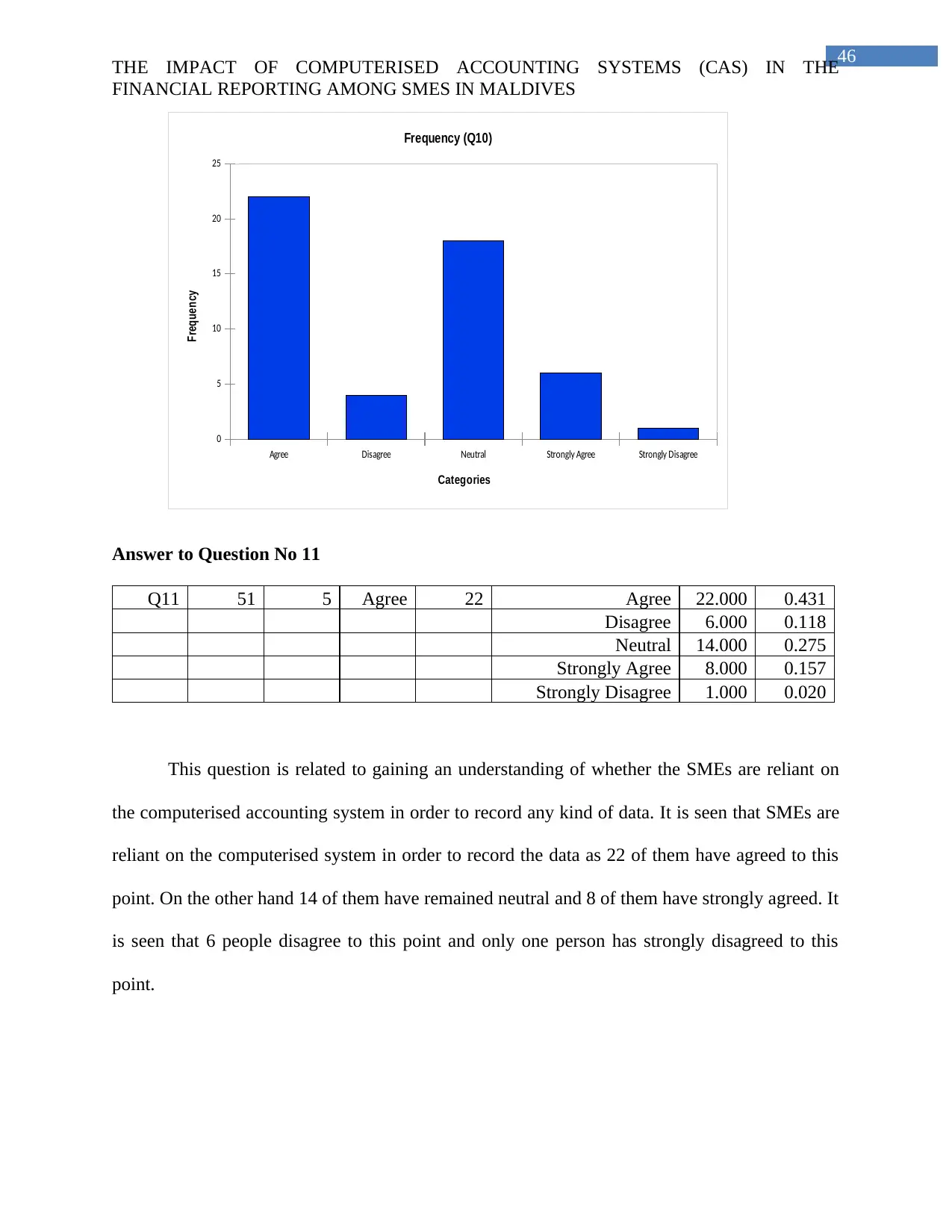

Answer to Question No 11....................................................................................................45

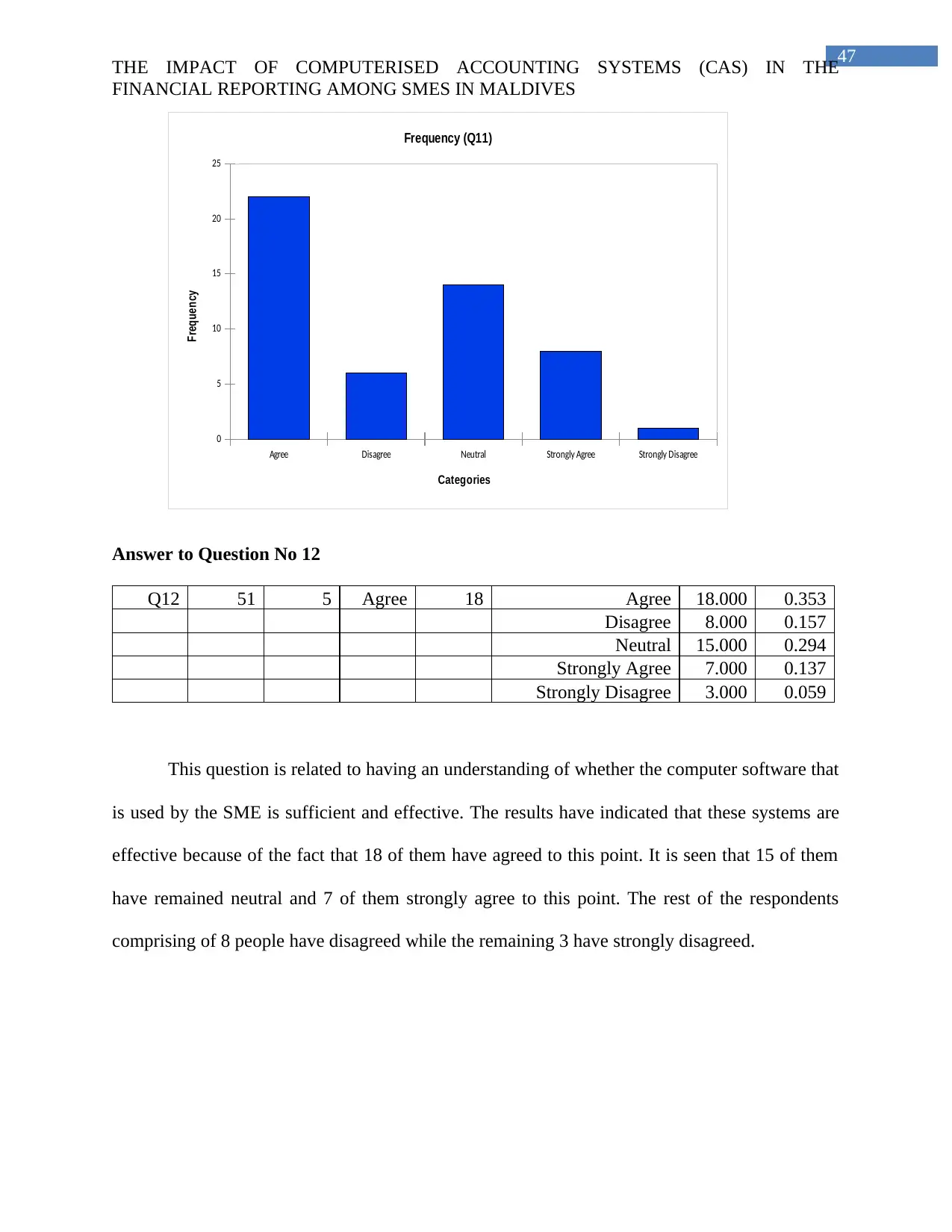

Answer to Question No 12....................................................................................................46

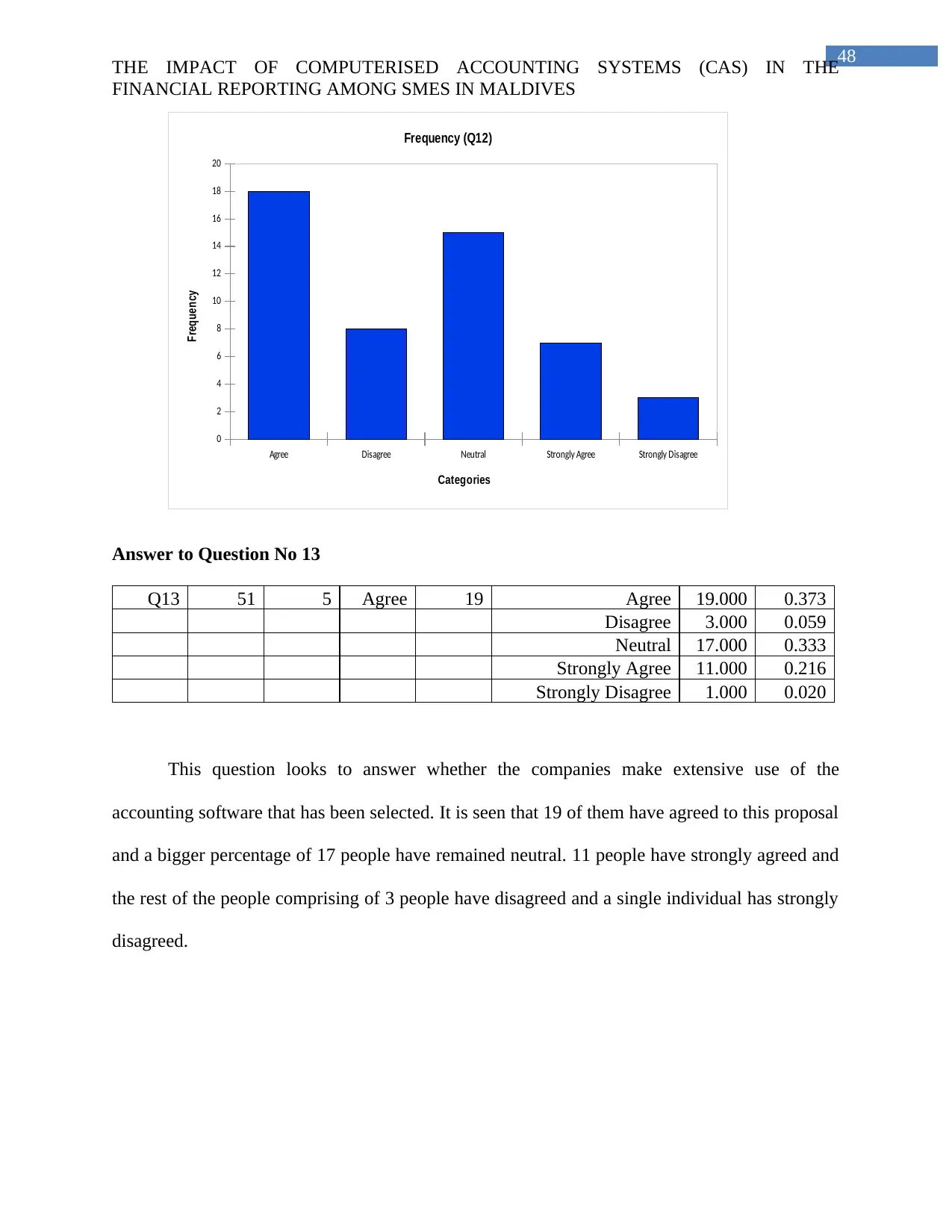

Answer to Question No 13....................................................................................................47

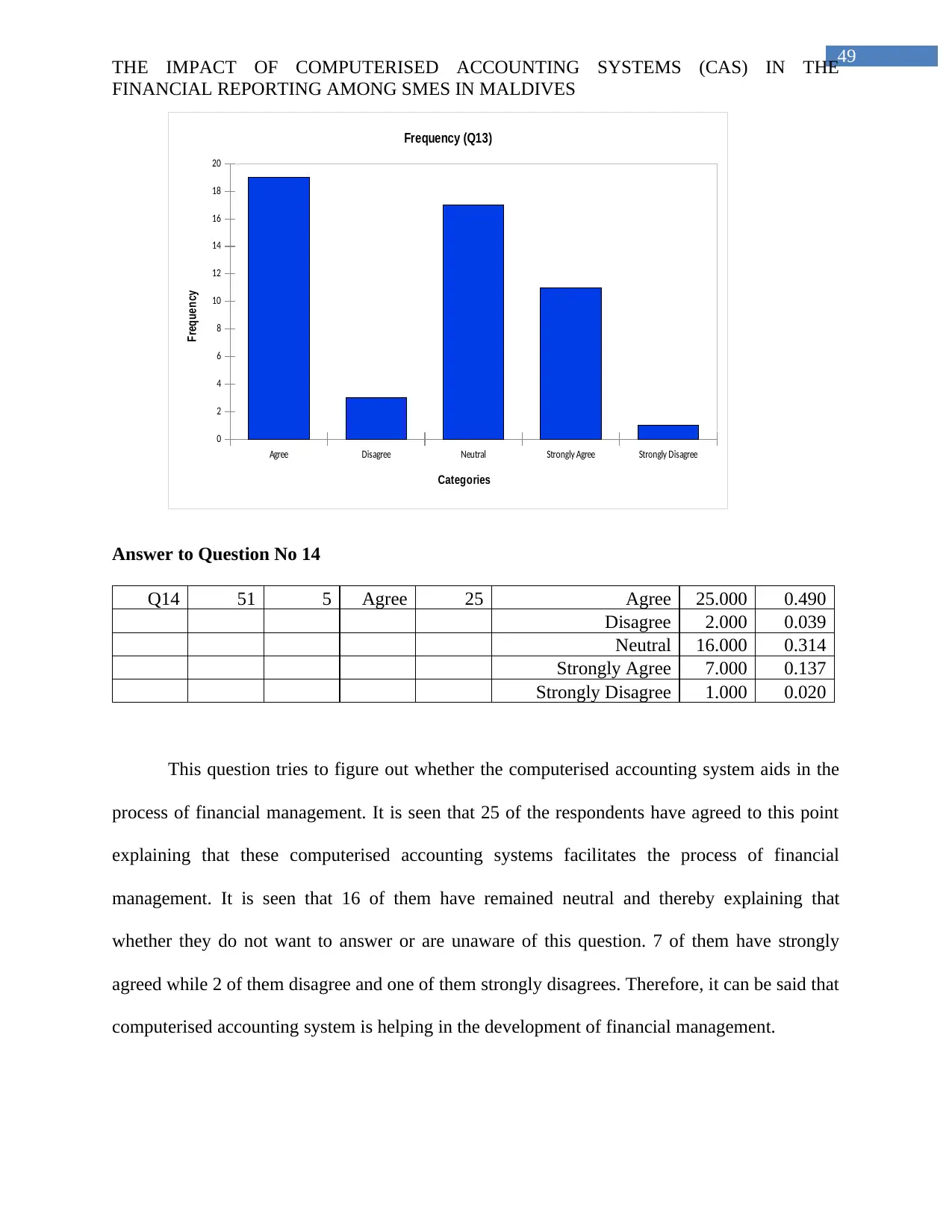

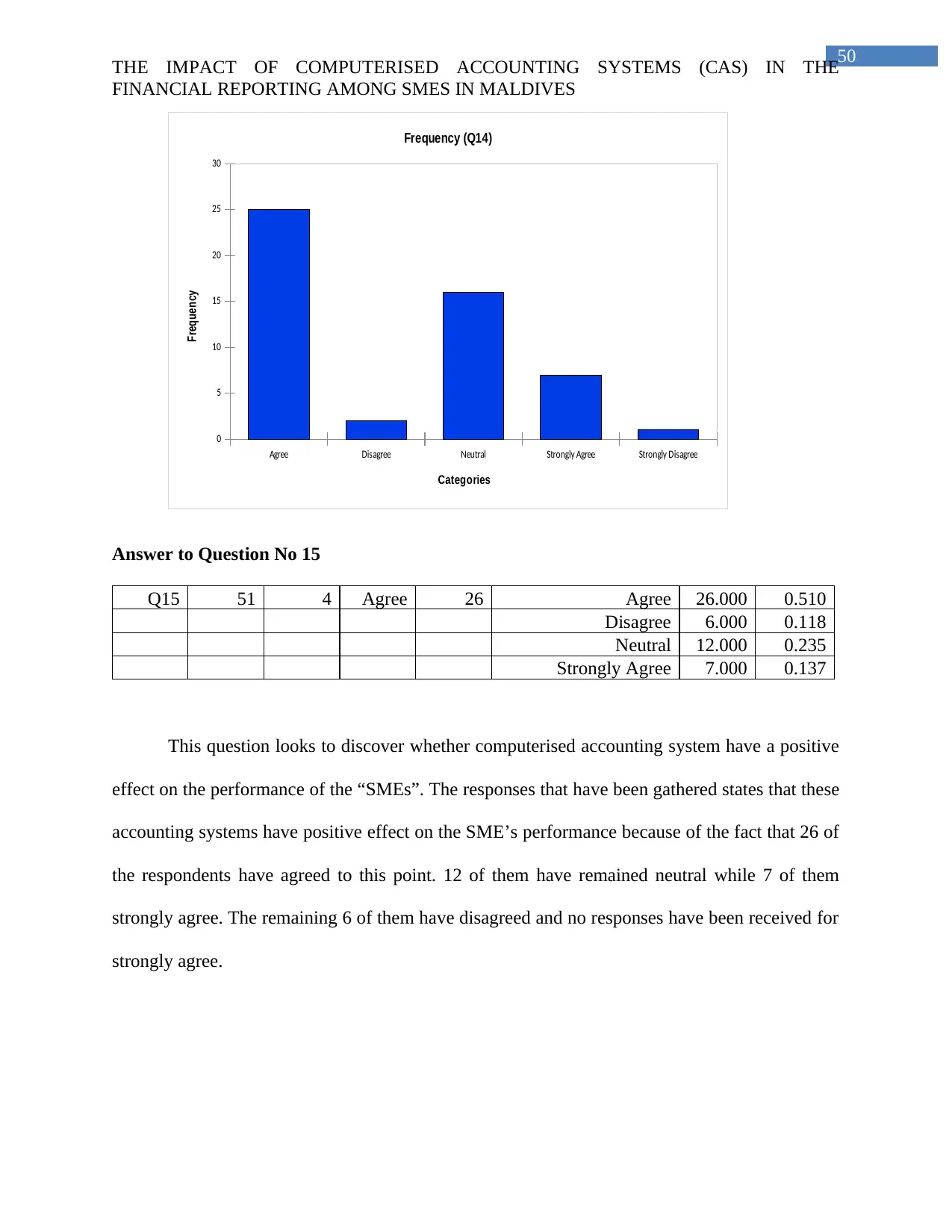

Answer to Question No 14....................................................................................................48

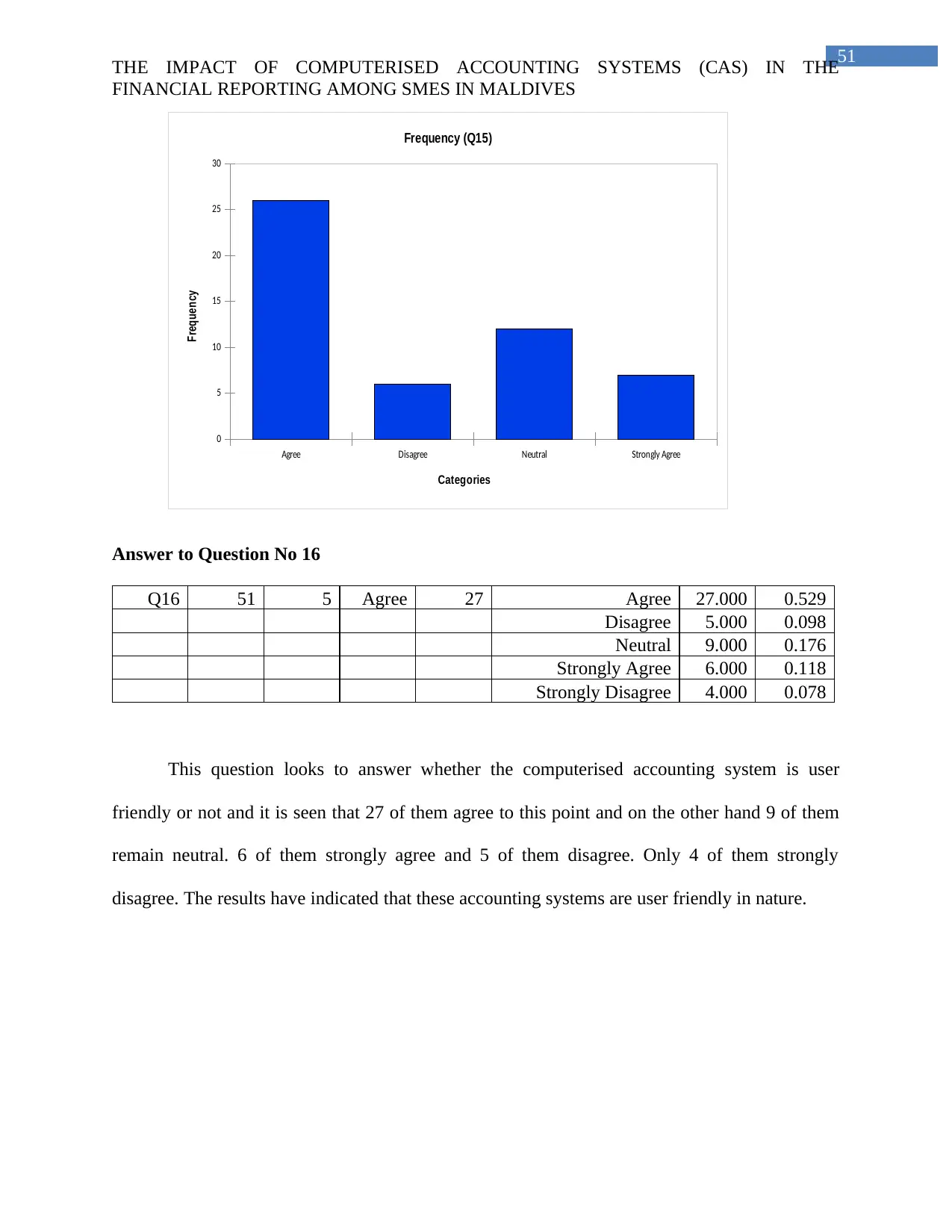

Answer to Question No 15....................................................................................................49

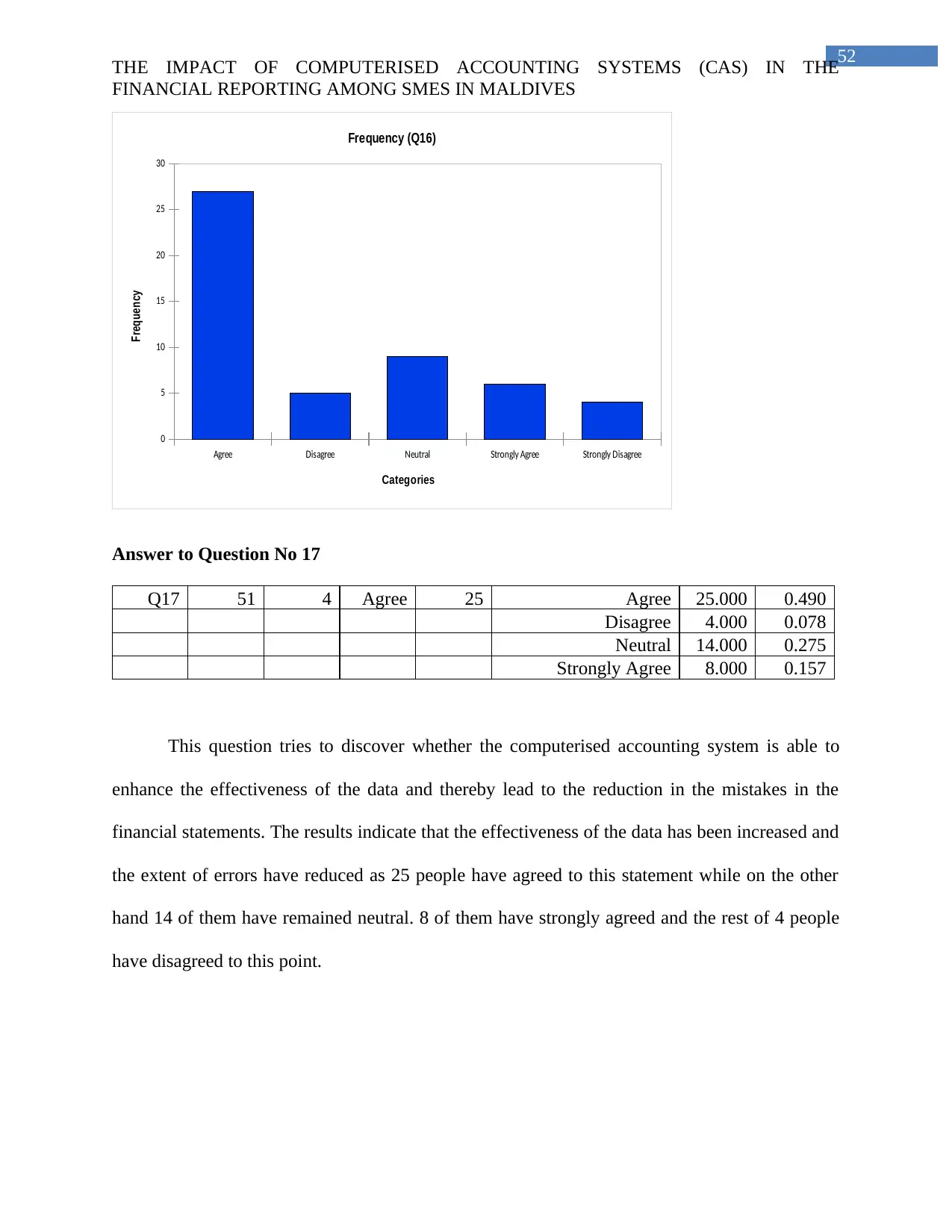

Answer to Question No 16....................................................................................................50

Answer to Question No 17....................................................................................................51

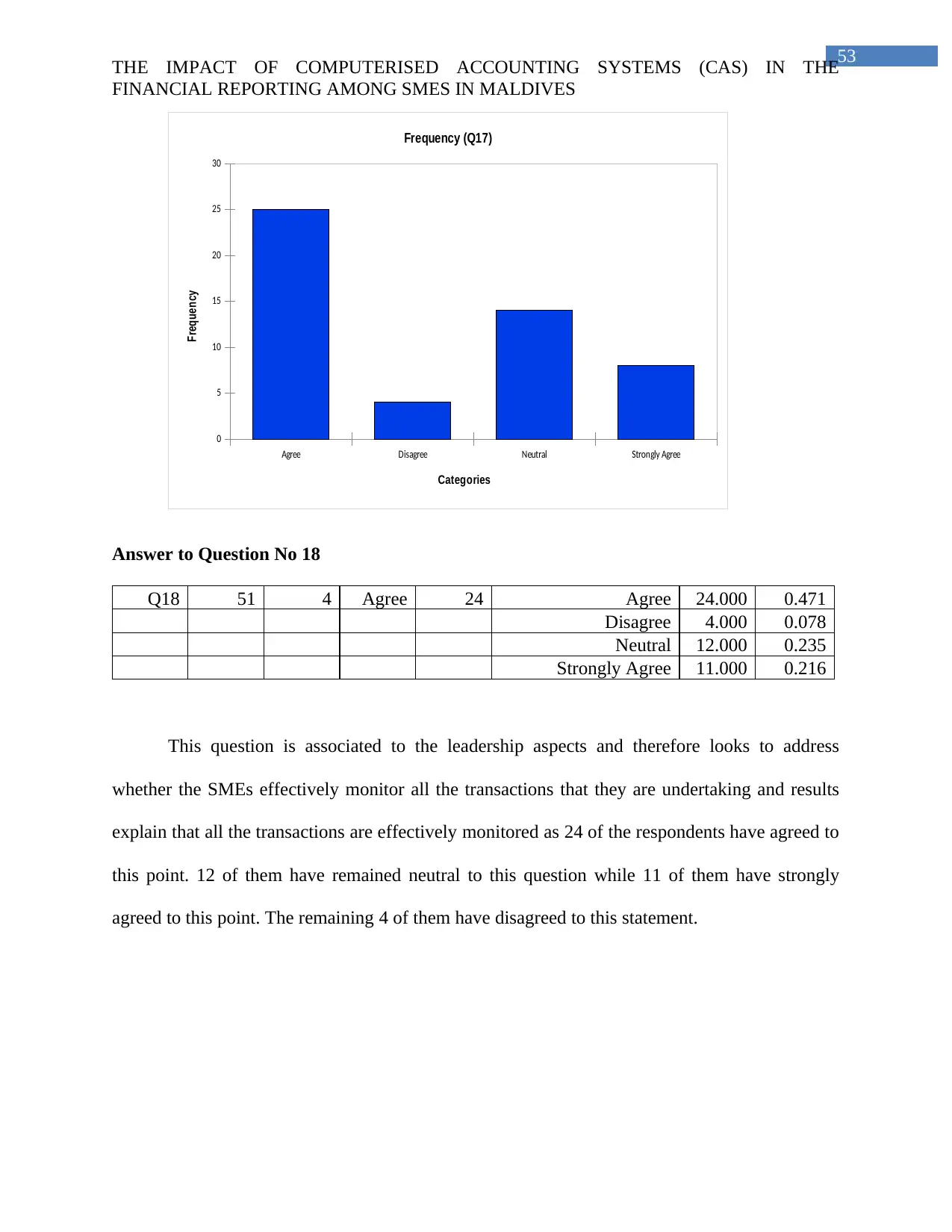

Answer to Question No 18....................................................................................................52

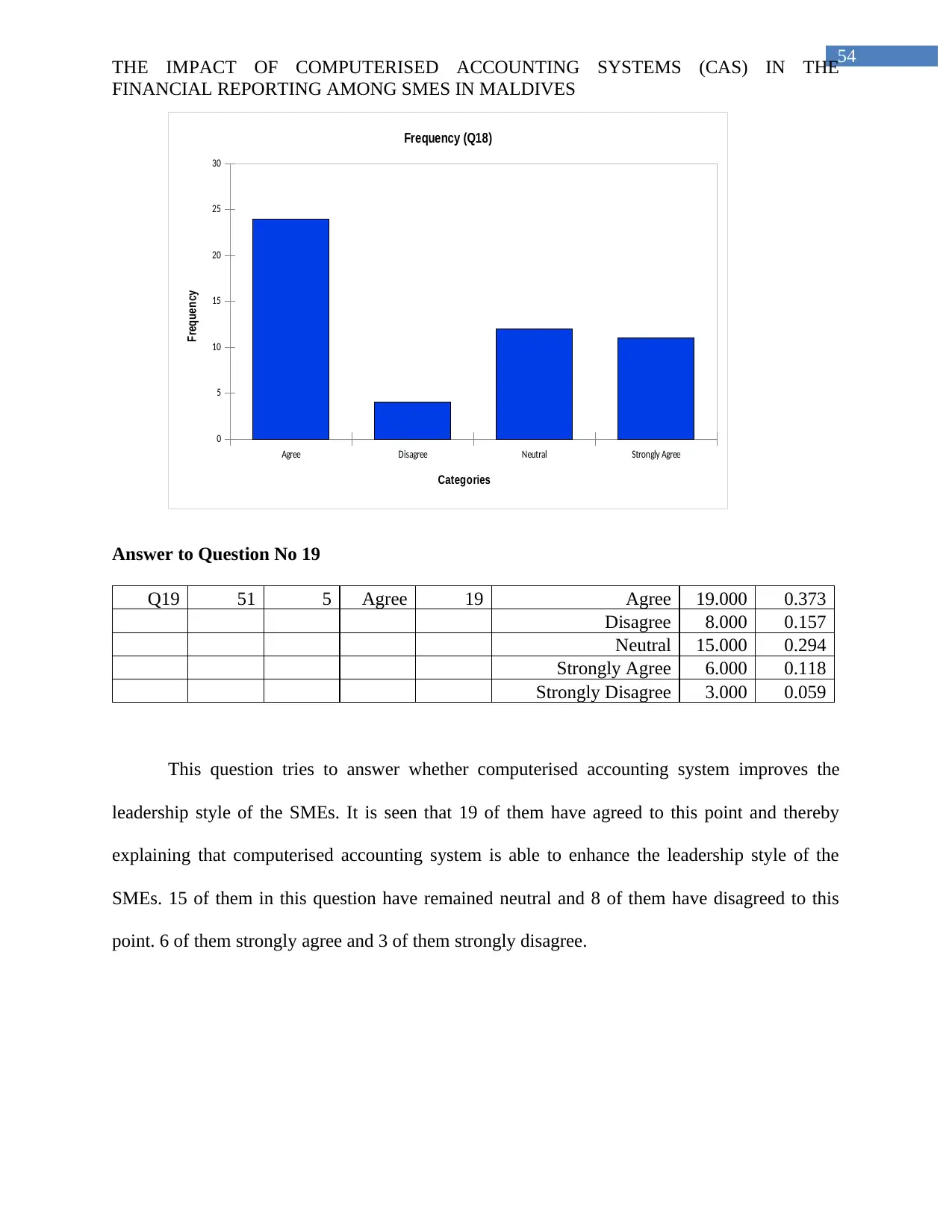

Answer to Question No 19....................................................................................................53

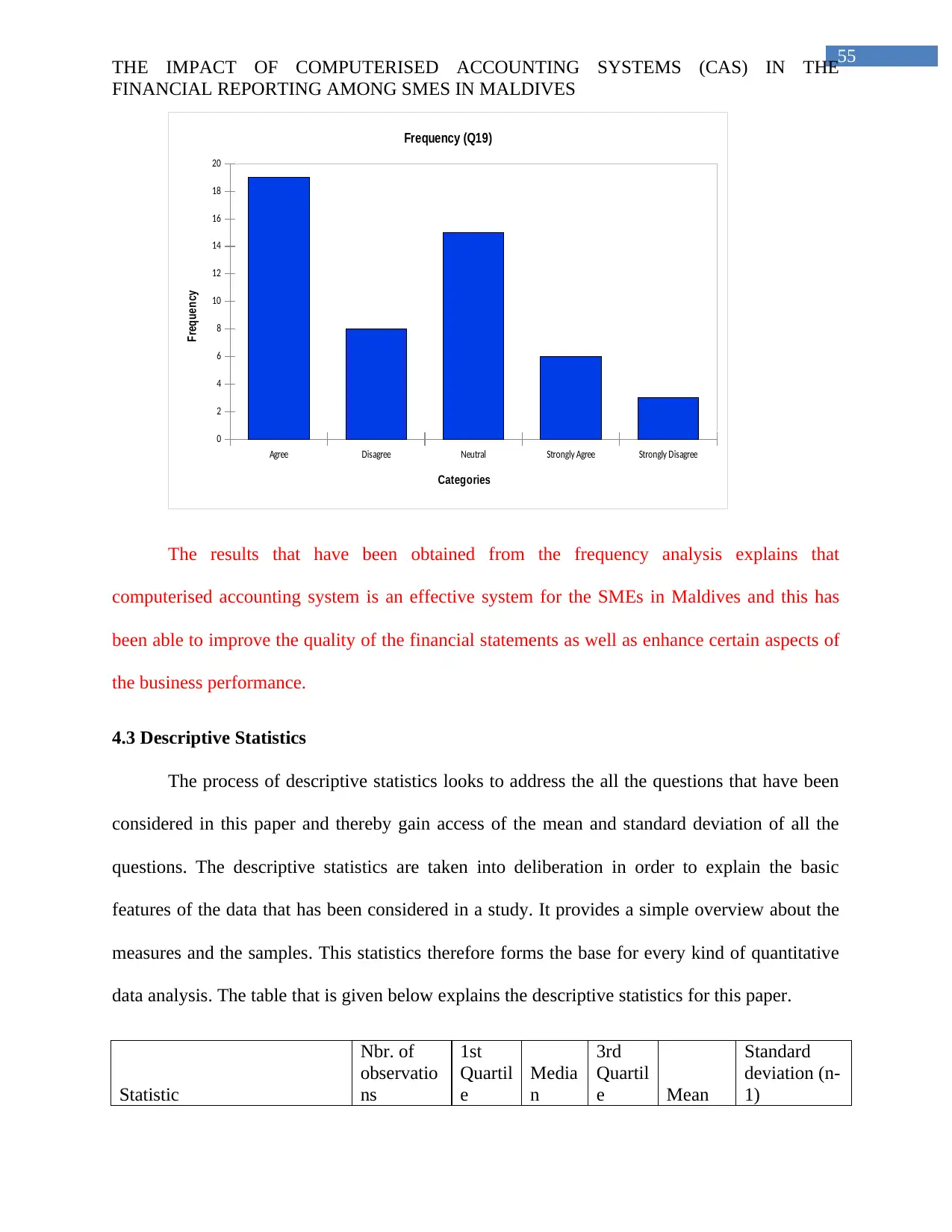

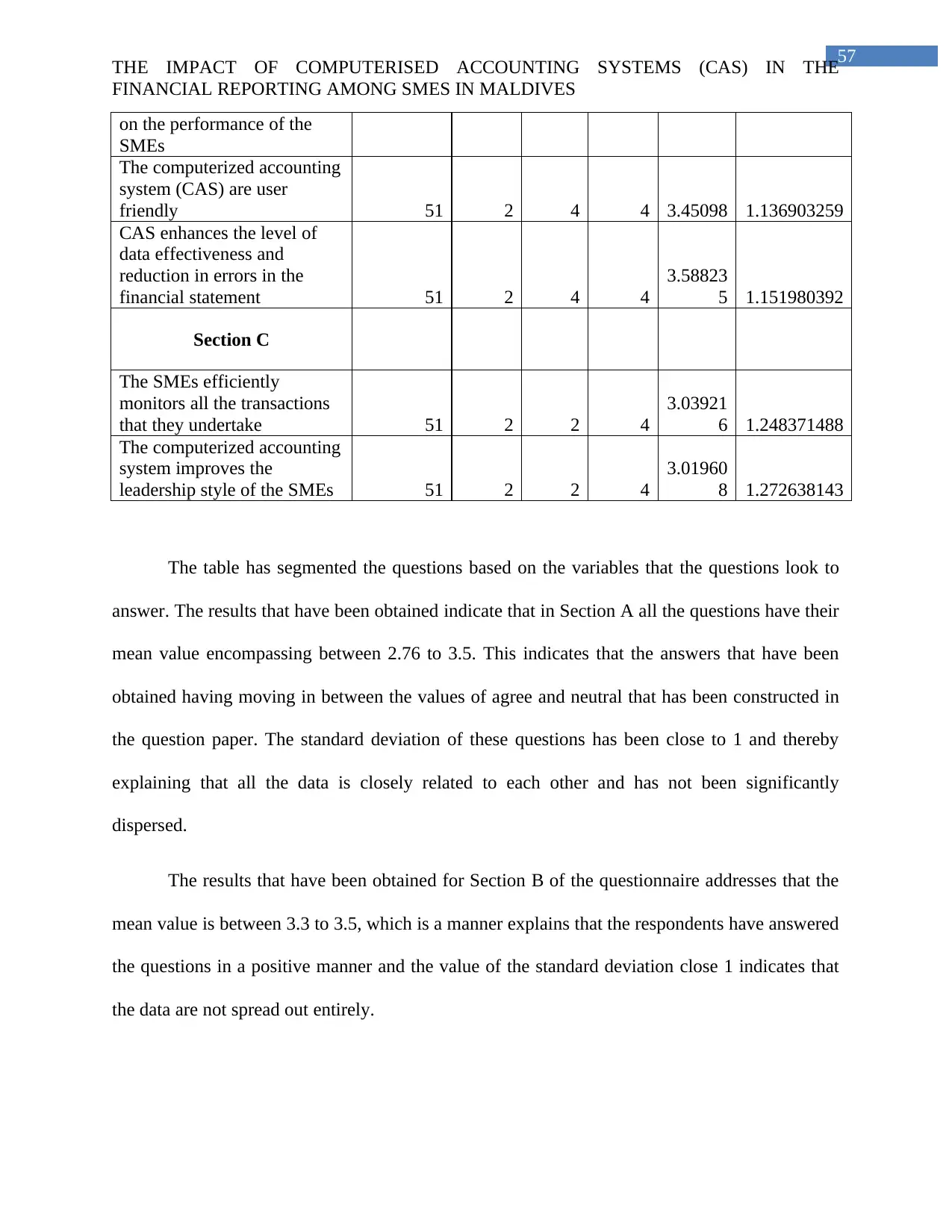

4.3 Descriptive Statistics...........................................................................................................54

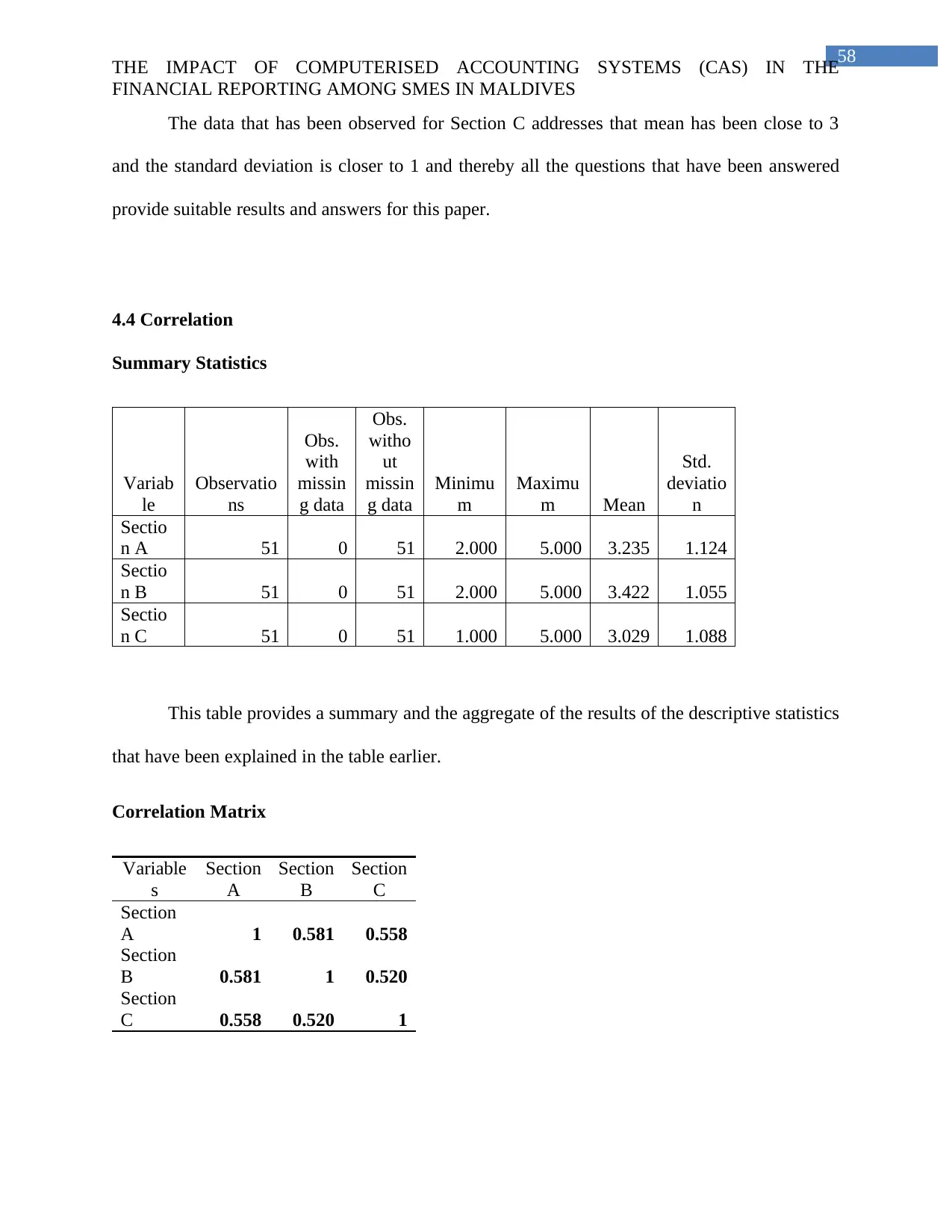

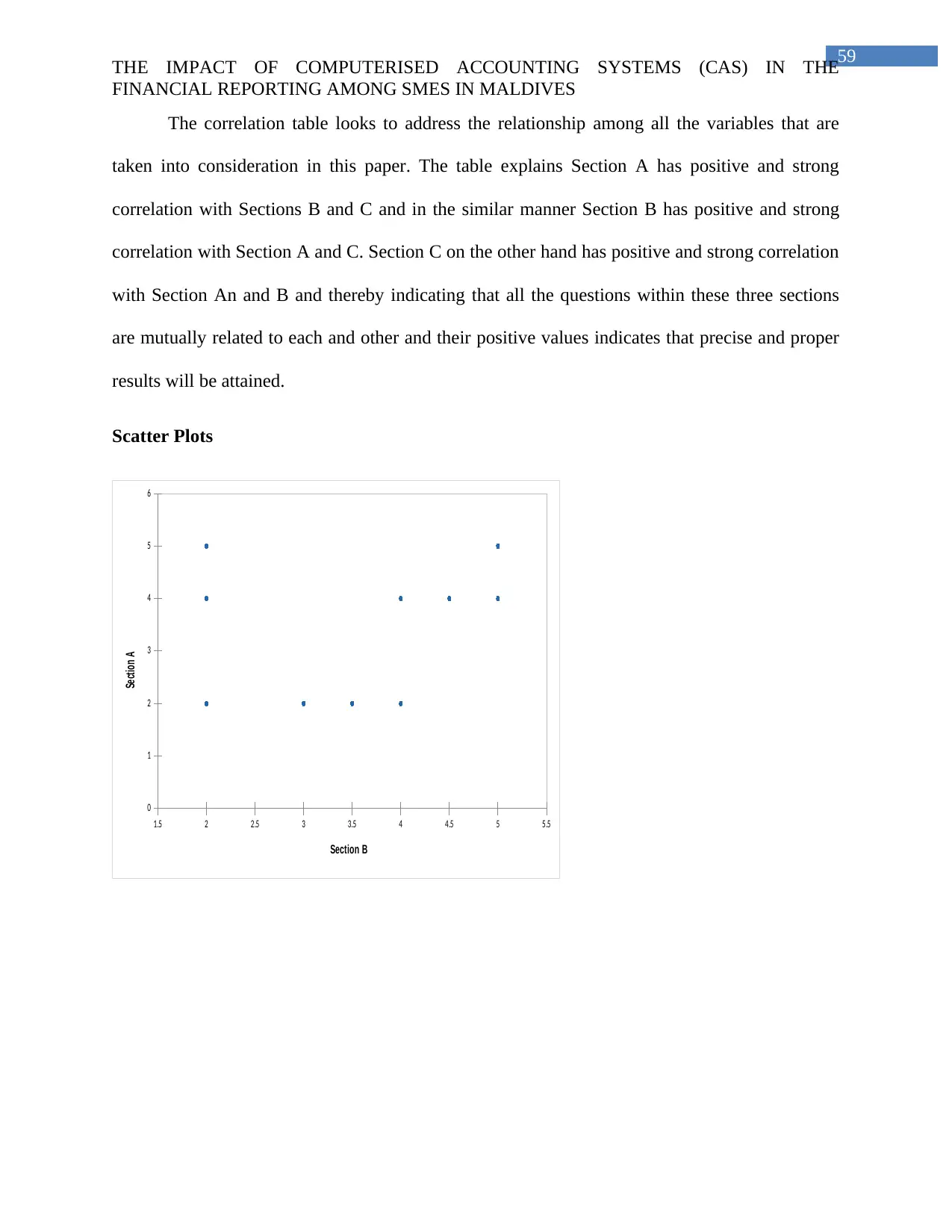

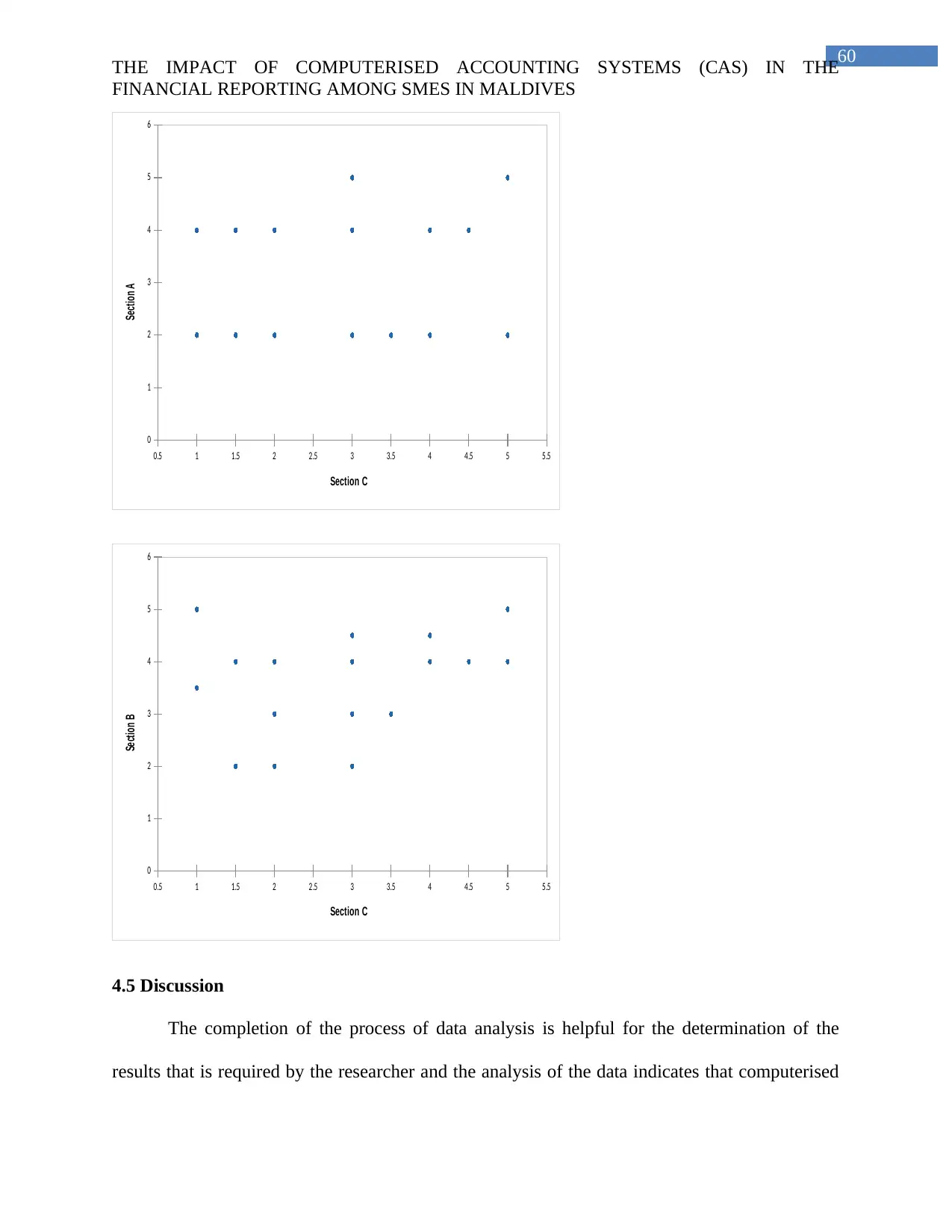

4.4 Correlation...........................................................................................................................57

4.5 Discussion............................................................................................................................59

Chapter 5: Conclusion, Recommendation and Future Work.........................................................61

5.1 Conclusion...........................................................................................................................61

5.2 Addressing the Objective.....................................................................................................62

5.3 Recommendation.................................................................................................................63

5.4 Future Work.........................................................................................................................63

Reference List................................................................................................................................64

Questionnaire.................................................................................................................................73

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Answer to Question No 10....................................................................................................44

Answer to Question No 11....................................................................................................45

Answer to Question No 12....................................................................................................46

Answer to Question No 13....................................................................................................47

Answer to Question No 14....................................................................................................48

Answer to Question No 15....................................................................................................49

Answer to Question No 16....................................................................................................50

Answer to Question No 17....................................................................................................51

Answer to Question No 18....................................................................................................52

Answer to Question No 19....................................................................................................53

4.3 Descriptive Statistics...........................................................................................................54

4.4 Correlation...........................................................................................................................57

4.5 Discussion............................................................................................................................59

Chapter 5: Conclusion, Recommendation and Future Work.........................................................61

5.1 Conclusion...........................................................................................................................61

5.2 Addressing the Objective.....................................................................................................62

5.3 Recommendation.................................................................................................................63

5.4 Future Work.........................................................................................................................63

Reference List................................................................................................................................64

Questionnaire.................................................................................................................................73

5

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Section A...................................................................................................................................74

Section B....................................................................................................................................75

Section C....................................................................................................................................78

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Section A...................................................................................................................................74

Section B....................................................................................................................................75

Section C....................................................................................................................................78

6

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Chapter 1: Introduction

The changes that are taking place in the global economy have steered to the development

of innovative technologies, which are helpful in the development functional activities of a

company. There are numerous computerised accounting systems that have been helpful in

ascertaining the financial transactions. The maintenance of the financial transactions can be

helpful in creating the financial statements that can be used in the future course of time and

thereby understand the financial scenario of an organization. The incorporation of the

computerised accounting system is a process with the help of which financial reporting can be

done in a precise manner and even reduces the chances of any miscalculations if done manually

(Ismail and King, 2014). This research thesis is therefore constructed in order to have an

understanding of the effect of the “computerised accounting system” in the financial

documenting of the small and medium enterprises in Maldives. There are several small and

medium companies available in the economy of Maldives and therefore impact on the financial

reporting of these companies by making use of the computerised accounting system can be

understood. A total of five small and medium enterprises of Maldives have been taken into

consideration who have incorporated computerised accounting system in order to have

knowledge of the effect of financial reporting in these organizations.

1.1 Background of the Study

Accounting has been looked upon as a key part of any business that is useful for small

and large profit making organizations. There are several organizations that undertake their

process of accounting manually and even feel satisfied. The other companies may be looking for

computerised accounting process as the software related to accounting are reasonable and

affordable (Diatmika, Irianto and Baridwan, 2016). The computerised and manual system of

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Chapter 1: Introduction

The changes that are taking place in the global economy have steered to the development

of innovative technologies, which are helpful in the development functional activities of a

company. There are numerous computerised accounting systems that have been helpful in

ascertaining the financial transactions. The maintenance of the financial transactions can be

helpful in creating the financial statements that can be used in the future course of time and

thereby understand the financial scenario of an organization. The incorporation of the

computerised accounting system is a process with the help of which financial reporting can be

done in a precise manner and even reduces the chances of any miscalculations if done manually

(Ismail and King, 2014). This research thesis is therefore constructed in order to have an

understanding of the effect of the “computerised accounting system” in the financial

documenting of the small and medium enterprises in Maldives. There are several small and

medium companies available in the economy of Maldives and therefore impact on the financial

reporting of these companies by making use of the computerised accounting system can be

understood. A total of five small and medium enterprises of Maldives have been taken into

consideration who have incorporated computerised accounting system in order to have

knowledge of the effect of financial reporting in these organizations.

1.1 Background of the Study

Accounting has been looked upon as a key part of any business that is useful for small

and large profit making organizations. There are several organizations that undertake their

process of accounting manually and even feel satisfied. The other companies may be looking for

computerised accounting process as the software related to accounting are reasonable and

affordable (Diatmika, Irianto and Baridwan, 2016). The computerised and manual system of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

accounting basically performs similar mechanisms, the accounting concepts and principles are

even similar with the difference being in the process technicalities (Smith and BintiPuasa, 2016).

It is seen that the computerised accounting system is a bit expensive in accordance to manual

accounting process bit their advantage is reliant on the speed and thereby being able to record

and gather information.

“Small and Medium Enterprises” (SMEs) are accounted for by deciding the number of

employees and the amount of revenue generated by a company. In order to define a small and

medium enterprise, these two factors must come under a specific standard that is held by the

respective nation. The small and medium enterprises do not have adequate amount of resources

unlike the large organizations, the essence being entrepreneurial and hence they are significant to

the development and innovation of the economy of the country (Seethamraju, 2015). This is due

to the fact that the SMEs have less capital in accordance to the companies that are functional at a

beiger stage and therefore have the ability to incorporate changes and develop their business

accordingly.

Over the previous decade, there has been remarkable development of SMEs in the

developing countries. There are several researchers who have looked at SMEs as an effective

substitute to the governmental agencies in receiving the assistance and the services to the ones

who are in need of it especially in the nations that are pressured by the political corruption and

favouritism (Azmi et al., 2016). These activities have been fundamental in the development of

the SMEs and the influence of the SMEs to incorporate new and innovative computerised

accounting services.

In accordance to Azmi et al., (2016 p: 13). Accountability explains the scenario within

which the function holder provides account to the other so that decisions may be undertaken

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

accounting basically performs similar mechanisms, the accounting concepts and principles are

even similar with the difference being in the process technicalities (Smith and BintiPuasa, 2016).

It is seen that the computerised accounting system is a bit expensive in accordance to manual

accounting process bit their advantage is reliant on the speed and thereby being able to record

and gather information.

“Small and Medium Enterprises” (SMEs) are accounted for by deciding the number of

employees and the amount of revenue generated by a company. In order to define a small and

medium enterprise, these two factors must come under a specific standard that is held by the

respective nation. The small and medium enterprises do not have adequate amount of resources

unlike the large organizations, the essence being entrepreneurial and hence they are significant to

the development and innovation of the economy of the country (Seethamraju, 2015). This is due

to the fact that the SMEs have less capital in accordance to the companies that are functional at a

beiger stage and therefore have the ability to incorporate changes and develop their business

accordingly.

Over the previous decade, there has been remarkable development of SMEs in the

developing countries. There are several researchers who have looked at SMEs as an effective

substitute to the governmental agencies in receiving the assistance and the services to the ones

who are in need of it especially in the nations that are pressured by the political corruption and

favouritism (Azmi et al., 2016). These activities have been fundamental in the development of

the SMEs and the influence of the SMEs to incorporate new and innovative computerised

accounting services.

In accordance to Azmi et al., (2016 p: 13). Accountability explains the scenario within

which the function holder provides account to the other so that decisions may be undertaken

8

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

about the performance adequacy. Amin and Mohamed,(2016p:132) cite accountability not only

for the purpose of reporting but even the explanation of the performance, they even sustain to

explain the accountability as the explicit and implicit expectations that any one of them will be

asked upon in order to clarify the feelings, belief and actions of a person towards other. The

process of computerization safeguards time in accordance to the level of transaction thereby

leading to financial reporting quality for example accurate, timely and dependable data that can

be created. This is the necessity for undertaking the study.

1.1.1 Computerised Accounting System

The process of computerised accounting is the implication of the computer dependent

software utilised to process, “input” and “store” and “output” of the accounting information. This

software is in assistance of the developing technology which aids the companies to make use of

the “computer programs” in order to conduct the jobs that were manually done in the earlier time

period. A computerised accounting process hence associates with the accounting information

system which is generated in order to assist the process of decision making (Cleary and Quinn,

2016). These are related with various numbers of benefits like the tenacity of undertaking the

routine transactions, quick assessment, timeliness, reporting and accuracy.

According to Germann and Manasseh,(2017p: 51) an accounting system comprises of the

business records, statements, reports and the procedures that are utilised by a company in order

to record the transactions and examining the impacts. Albu et al.,(2016 p: 178) addresses the fact

that an accounting process is a technique of maintaining a manual record of all the transactions.

The earnings are provided for all the received money by a company and the earnings are asked at

any time when expenses are undertaken with the money. Accountability for the SMEs is both an

ethical and legal accountability for the company that utilise the resources that is received to

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

about the performance adequacy. Amin and Mohamed,(2016p:132) cite accountability not only

for the purpose of reporting but even the explanation of the performance, they even sustain to

explain the accountability as the explicit and implicit expectations that any one of them will be

asked upon in order to clarify the feelings, belief and actions of a person towards other. The

process of computerization safeguards time in accordance to the level of transaction thereby

leading to financial reporting quality for example accurate, timely and dependable data that can

be created. This is the necessity for undertaking the study.

1.1.1 Computerised Accounting System

The process of computerised accounting is the implication of the computer dependent

software utilised to process, “input” and “store” and “output” of the accounting information. This

software is in assistance of the developing technology which aids the companies to make use of

the “computer programs” in order to conduct the jobs that were manually done in the earlier time

period. A computerised accounting process hence associates with the accounting information

system which is generated in order to assist the process of decision making (Cleary and Quinn,

2016). These are related with various numbers of benefits like the tenacity of undertaking the

routine transactions, quick assessment, timeliness, reporting and accuracy.

According to Germann and Manasseh,(2017p: 51) an accounting system comprises of the

business records, statements, reports and the procedures that are utilised by a company in order

to record the transactions and examining the impacts. Albu et al.,(2016 p: 178) addresses the fact

that an accounting process is a technique of maintaining a manual record of all the transactions.

The earnings are provided for all the received money by a company and the earnings are asked at

any time when expenses are undertaken with the money. Accountability for the SMEs is both an

ethical and legal accountability for the company that utilise the resources that is received to

9

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

expand their level of investment and accountability covers an entire report of the operations

along with the justification for the process with the help of which the resources are monitored.

1.1.2 Quality of the Financial Reports

Financial statement is a process of portraying the financial accountabilities for the

purpose of the reviewing the financial operations of an organization of the previous years and

construct plans for the coming future in order to publish and prepare the yearly accounts or the

financial statements. Ruivo, Oliveira and Neto,(2014 p: 184) explained financial reporting as the

mechanism of providing the financial data which is complete, accurate and dependable to the

stakeholders in order to undertake decisions related to economics. Bahri, St-Pierre and Sakka,

(2017 p: 36) have cited that financial statements are the yields of an accounting process and they

are constructed at the completion of the accounting year which is even known as the final

accounts. According to Kiliç, Uyar and Ataman,(2016 p: 178), the financial statements are

inclusive of a narrative explanation of the organizational activities and the financial reports that

are audited. Kiliç, Uyar and Ataman, (2016p: 178) have even debated that these aids the

stakeholders to observe the performance of a company and the overall financial scenario of the

company. Albu et al.,(2015:p: 178) explains that the accountants and the managers are generally

required to safeguard the outcomes that have been explained in the financial statements as a

section of the process of accountability.

According to Abrokwah et al., (2015 p: 269), timelines is a key feature of the quality of

the financial data. In order to assist the users, the financial data needs to be presented at the

correct time or else it would lose its relevancy. Relevance is even a feature of the quality of the

financial statements. Seyal and Rahman, (2015 p: 22) have focused on the fact that users must

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

expand their level of investment and accountability covers an entire report of the operations

along with the justification for the process with the help of which the resources are monitored.

1.1.2 Quality of the Financial Reports

Financial statement is a process of portraying the financial accountabilities for the

purpose of the reviewing the financial operations of an organization of the previous years and

construct plans for the coming future in order to publish and prepare the yearly accounts or the

financial statements. Ruivo, Oliveira and Neto,(2014 p: 184) explained financial reporting as the

mechanism of providing the financial data which is complete, accurate and dependable to the

stakeholders in order to undertake decisions related to economics. Bahri, St-Pierre and Sakka,

(2017 p: 36) have cited that financial statements are the yields of an accounting process and they

are constructed at the completion of the accounting year which is even known as the final

accounts. According to Kiliç, Uyar and Ataman,(2016 p: 178), the financial statements are

inclusive of a narrative explanation of the organizational activities and the financial reports that

are audited. Kiliç, Uyar and Ataman, (2016p: 178) have even debated that these aids the

stakeholders to observe the performance of a company and the overall financial scenario of the

company. Albu et al.,(2015:p: 178) explains that the accountants and the managers are generally

required to safeguard the outcomes that have been explained in the financial statements as a

section of the process of accountability.

According to Abrokwah et al., (2015 p: 269), timelines is a key feature of the quality of

the financial data. In order to assist the users, the financial data needs to be presented at the

correct time or else it would lose its relevancy. Relevance is even a feature of the quality of the

financial statements. Seyal and Rahman, (2015 p: 22) have focused on the fact that users must

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

have the ability to compare the financial statements of the organization in accordance to time in

order to have knowledge about the patterns in the financial performance and position.

1.1.3 Effect of Computerised Accounting System on the Financial Report Quality

It is expressed theoretically that a computerised accounting process would lead to quality

and effective financial statements. The researches undertaken by Uyar, Gungormus and Kuzey,

(2017 p: 9) explain that it is easy to undertake the functions of accounting by making use of the

computerised accounting mechanisms. Kvaal, (2017 p: 157) explained that the management

cannot satisfy easily the statutory requirements of reporting like the profit or loss account,

customised reporting and the balance sheet without exploiting the computerised accounting

process. By the assistance of incorporating the system, these activities can be done very quickly

with minimum effort (Azmi et al., 2016). The computerised accounting system simplifies the

process of auditing and has enhanced accessibility to the information that is demanded payments

and other kinds of transactions which are helpful in lowering the time required to give out this

kind of data and assist in the process of documentation during the time of auditing.

The basic principles of computerised accounting system is inclusive of the all the primary

requirements of any data-base related application in the computers. It assists in simplifying,

streamlining and integrating all the organizational processes in a cost effective way and thereby

assists in revealing the actual picture of all the undertakings of the business to the financial

statement users.

Due to the fast transformations in the technology, several small businesses look to track

the financial transactions with the help of computerised software than keeping track of all the

financial operations manually with the assistance of physical ledger (Corsi, Mancini and

Piscitelli, 2017). The developments in the computerised innovations have gradually steered to the

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

have the ability to compare the financial statements of the organization in accordance to time in

order to have knowledge about the patterns in the financial performance and position.

1.1.3 Effect of Computerised Accounting System on the Financial Report Quality

It is expressed theoretically that a computerised accounting process would lead to quality

and effective financial statements. The researches undertaken by Uyar, Gungormus and Kuzey,

(2017 p: 9) explain that it is easy to undertake the functions of accounting by making use of the

computerised accounting mechanisms. Kvaal, (2017 p: 157) explained that the management

cannot satisfy easily the statutory requirements of reporting like the profit or loss account,

customised reporting and the balance sheet without exploiting the computerised accounting

process. By the assistance of incorporating the system, these activities can be done very quickly

with minimum effort (Azmi et al., 2016). The computerised accounting system simplifies the

process of auditing and has enhanced accessibility to the information that is demanded payments

and other kinds of transactions which are helpful in lowering the time required to give out this

kind of data and assist in the process of documentation during the time of auditing.

The basic principles of computerised accounting system is inclusive of the all the primary

requirements of any data-base related application in the computers. It assists in simplifying,

streamlining and integrating all the organizational processes in a cost effective way and thereby

assists in revealing the actual picture of all the undertakings of the business to the financial

statement users.

Due to the fast transformations in the technology, several small businesses look to track

the financial transactions with the help of computerised software than keeping track of all the

financial operations manually with the assistance of physical ledger (Corsi, Mancini and

Piscitelli, 2017). The developments in the computerised innovations have gradually steered to the

11

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

incorporation of the “computerised accounting system” in order to assist manufacture the precise

and the trustworthy presentation of the financial statements for the management as well as for the

external users for the determination of undertaking the decision making method.

The process of computerised accounting looks to bring in dedicated accounting software

and the “digital spreadsheets” maintain a trajectory of the business and the financial transactions

of the customers. It is an effective utilisation of the present technological developments

(Ware,2015). It has not only revolutionised the conventional papers for the process of

accounting, but has even generated new kinds of applications of accounting for the business. The

organizations now generate the overall accounting information systems that assimilate all the

operations of the business that is inclusive of the external vendors and suppliers.

The process of computerised accounting system mechanise the process of accounting

enhancing the effectiveness and lowering the level of expenses and looks to be more precise,

easy to use and less subjective to any mistakes than their manual counterparts (Malagueño,

Lopez-Valeiras and Gomez-Conde, 2017). In the current interconnected, computerised global

business atmosphere, the computerised accounting system has become the lifeline for

development in the business firms. Hence, it involves the computerisation of the accounting data

systems which is created in order to assist in the process of decision making. These are related

with several advantages and benefits like the swiftness of undertaking the routine transactions,

swift assessment, reporting, accuracy and timeliness.

1.2 Statement of the Problem

As the information tools and technologies have been developing increasingly, the

physical accounting system has slowly become insufficient for the requirement of making

decisions. Maldives is a country that has the potential of developing in terms of the global

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

incorporation of the “computerised accounting system” in order to assist manufacture the precise

and the trustworthy presentation of the financial statements for the management as well as for the

external users for the determination of undertaking the decision making method.

The process of computerised accounting looks to bring in dedicated accounting software

and the “digital spreadsheets” maintain a trajectory of the business and the financial transactions

of the customers. It is an effective utilisation of the present technological developments

(Ware,2015). It has not only revolutionised the conventional papers for the process of

accounting, but has even generated new kinds of applications of accounting for the business. The

organizations now generate the overall accounting information systems that assimilate all the

operations of the business that is inclusive of the external vendors and suppliers.

The process of computerised accounting system mechanise the process of accounting

enhancing the effectiveness and lowering the level of expenses and looks to be more precise,

easy to use and less subjective to any mistakes than their manual counterparts (Malagueño,

Lopez-Valeiras and Gomez-Conde, 2017). In the current interconnected, computerised global

business atmosphere, the computerised accounting system has become the lifeline for

development in the business firms. Hence, it involves the computerisation of the accounting data

systems which is created in order to assist in the process of decision making. These are related

with several advantages and benefits like the swiftness of undertaking the routine transactions,

swift assessment, reporting, accuracy and timeliness.

1.2 Statement of the Problem

As the information tools and technologies have been developing increasingly, the

physical accounting system has slowly become insufficient for the requirement of making

decisions. Maldives is a country that has the potential of developing in terms of the global

12

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

economy and therefore understanding the impact of computerised accounting system is essential

with the help of which the advantages in accordance to the manual accounting system can be

understood with the help of which the SMEs can incorporate the computerised accounting

system and thereby improve the financial statements and the maintenance of the financial

records. SMEs are looked upon as one of the key industries that looks to manufacture products

and services with their limited capital. Therefore, incorporation of the computerised accounting

system in the SMEs is very low and therefore it is essential to have knowledge about the impact

of computerised accounting process on the SMEs and how it can be incorporated in the same.

This is the key factor and the statement of the problem according to which the paper is being

constructed.

1.3 Research Objectives

The research objectives are to discover the effect of Computerised Accounting Systems

that have led to transformations in various aspects of the accounting practices of the SME

businesses in Maldives.

1.4 Research Question

The “research question” that have been created in accordance to this research are

explained below:

Q1. What are the key advantages and the issues related with the utilisation of “Computerised

Accounting Systems” in the financial reporting in the “Small and Medium Enterprises” in

Maldives?

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

economy and therefore understanding the impact of computerised accounting system is essential

with the help of which the advantages in accordance to the manual accounting system can be

understood with the help of which the SMEs can incorporate the computerised accounting

system and thereby improve the financial statements and the maintenance of the financial

records. SMEs are looked upon as one of the key industries that looks to manufacture products

and services with their limited capital. Therefore, incorporation of the computerised accounting

system in the SMEs is very low and therefore it is essential to have knowledge about the impact

of computerised accounting process on the SMEs and how it can be incorporated in the same.

This is the key factor and the statement of the problem according to which the paper is being

constructed.

1.3 Research Objectives

The research objectives are to discover the effect of Computerised Accounting Systems

that have led to transformations in various aspects of the accounting practices of the SME

businesses in Maldives.

1.4 Research Question

The “research question” that have been created in accordance to this research are

explained below:

Q1. What are the key advantages and the issues related with the utilisation of “Computerised

Accounting Systems” in the financial reporting in the “Small and Medium Enterprises” in

Maldives?

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

1.5 Significance of the Study

The importance of the research thesis is to give out essential data about the effect of

making use of the “Computerised Accounting Systems” (CAS) in the process of financial

documenting in the “Small and Medium Enterprises” in Maldives. This thesis will address the

massive effect and the impact “CAS” can have in the process of constructing the financial

reports. The transformation of the entire world has observed modernization as a segment of the

wider technology and thereby brings in greater benefits to the world of business in the current

time period.

1.6 Scope and Limitations of the Study

This research concentrates on evaluating the effect of the usage of “Computerised

Accounting Systems” in the process of financial reporting in the “Small and Medium

Enterprises” in Maldives. This will ascertain the probable effect of computerised accounting

process in the construction of the financial statements and how it can have an impact in the

method of decision making of an organization.

The participants who will be selected for this thesis are restricted only to the small and

medium enterprises in Maldives. The theoretical limitation has been attaining better data and

information with the help of which effective results can be attained. The conceptual limitation

refers to the discovery of the framework and the model that is ideal for this paper with the help

of which effective results can be obtained for the completion of the paper.

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

1.5 Significance of the Study

The importance of the research thesis is to give out essential data about the effect of

making use of the “Computerised Accounting Systems” (CAS) in the process of financial

documenting in the “Small and Medium Enterprises” in Maldives. This thesis will address the

massive effect and the impact “CAS” can have in the process of constructing the financial

reports. The transformation of the entire world has observed modernization as a segment of the

wider technology and thereby brings in greater benefits to the world of business in the current

time period.

1.6 Scope and Limitations of the Study

This research concentrates on evaluating the effect of the usage of “Computerised

Accounting Systems” in the process of financial reporting in the “Small and Medium

Enterprises” in Maldives. This will ascertain the probable effect of computerised accounting

process in the construction of the financial statements and how it can have an impact in the

method of decision making of an organization.

The participants who will be selected for this thesis are restricted only to the small and

medium enterprises in Maldives. The theoretical limitation has been attaining better data and

information with the help of which effective results can be attained. The conceptual limitation

refers to the discovery of the framework and the model that is ideal for this paper with the help

of which effective results can be obtained for the completion of the paper.

14

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Chapter 2: Literature Review

This part of the research has looked to evaluate the related studies and literature which

are associated closely to the topic of the current research thesis that is available from the local

and the foreign sources. This information has been useful to the researchers in providing certain

information and background in ascertaining the kind of approach to be utilised for this study.

The literature review that has been constructed below would be acting as supportive

information about the effect of Computerised Accounting System in the process of financial

reporting.

Da Silva Laureano, Cardoso Vieira Machado and Da Silva Laureano, (2016 p: 156)

explained that accounting is one of the oldest but are even reliable management disciplines. In

spite of its continuity and stability, accounting process has observed key transformations in the

previous decade. It is very astonishing if a decade from the current period, accounting has been

similar to today. Every organization implements the process of accounting as it is accepted

generally that the companies have to disclose definite management and financial data to the users

and due to the fact that accounting is a requisite mechanism in the process of making business

decisions. Accounting is a key segment of each organization and therefore organizations are

required to maintain effective books of accounts. Financial accounting is the art of systematic

identification, measurement, classifying, summarising and recording in a key way and with

respect to the money, events and transactions which are in a way financial in nature and

assessing, communicating and interpreting the outcomes thereafter.

Orobia, Padachi and Munene, (2016 p: 110) stated that computerised accounting system

is a process that makes use of computers to the inputs, stores, processes and outputs the

accounting data in form of financial statements. Orobia, Padachi and Munene, (2016 p: 110)

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Chapter 2: Literature Review

This part of the research has looked to evaluate the related studies and literature which

are associated closely to the topic of the current research thesis that is available from the local

and the foreign sources. This information has been useful to the researchers in providing certain

information and background in ascertaining the kind of approach to be utilised for this study.

The literature review that has been constructed below would be acting as supportive

information about the effect of Computerised Accounting System in the process of financial

reporting.

Da Silva Laureano, Cardoso Vieira Machado and Da Silva Laureano, (2016 p: 156)

explained that accounting is one of the oldest but are even reliable management disciplines. In

spite of its continuity and stability, accounting process has observed key transformations in the

previous decade. It is very astonishing if a decade from the current period, accounting has been

similar to today. Every organization implements the process of accounting as it is accepted

generally that the companies have to disclose definite management and financial data to the users

and due to the fact that accounting is a requisite mechanism in the process of making business

decisions. Accounting is a key segment of each organization and therefore organizations are

required to maintain effective books of accounts. Financial accounting is the art of systematic

identification, measurement, classifying, summarising and recording in a key way and with

respect to the money, events and transactions which are in a way financial in nature and

assessing, communicating and interpreting the outcomes thereafter.

Orobia, Padachi and Munene, (2016 p: 110) stated that computerised accounting system

is a process that makes use of computers to the inputs, stores, processes and outputs the

accounting data in form of financial statements. Orobia, Padachi and Munene, (2016 p: 110)

15

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

further adds that accounting system records all the relevant transactions that frequently deal with

the circumstances that have an effect on the financial scenario and the organizational

performance.

Prasad and Green, (2015 p: 139) explained a computerised accounting system as a

process or structure with the help of which the financial data related to the transactions of a

business are organised, recorded, assessed, summarised, communicated and interpreted to the

participants by making use of computers and processes related to computers like the accounting

packages. Prasad and Green,(2015 p: 139) even stressed on the fact that it is a mechanised

method of assisting the inflow of the financial data as well as the mechanisation of the

accounting jobs like the recording of the database and construction of the reports. Prasad and

Green,(2015 p: 139) states that maintaining precise records of accounting is a key part for any

company.

However, computerised accounting system associates with the utilisation of computers in

order to monitor large quantity of data with efficiency, speed and accuracy that aims at

overcoming necessary challenges which do not transform the principles.

Hussain and Raghavan, (2017 p: 137) stated that computerised packages can rapidly

create all sorts of documents required by the management like for example budget assessment

and variance evaluations. The data analysis and processing are more precise and faster which is

able to satisfy the demands of the managers and the management for timely and authentic

information for the purpose of decision making.

Lutfi, Idris and Mohamad, (2016 p: 6) agreed with the time and the speed with the help of

which accounting is undertaken and furthermore explained that a computerised accounting

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

further adds that accounting system records all the relevant transactions that frequently deal with

the circumstances that have an effect on the financial scenario and the organizational

performance.

Prasad and Green, (2015 p: 139) explained a computerised accounting system as a

process or structure with the help of which the financial data related to the transactions of a

business are organised, recorded, assessed, summarised, communicated and interpreted to the

participants by making use of computers and processes related to computers like the accounting

packages. Prasad and Green,(2015 p: 139) even stressed on the fact that it is a mechanised

method of assisting the inflow of the financial data as well as the mechanisation of the

accounting jobs like the recording of the database and construction of the reports. Prasad and

Green,(2015 p: 139) states that maintaining precise records of accounting is a key part for any

company.

However, computerised accounting system associates with the utilisation of computers in

order to monitor large quantity of data with efficiency, speed and accuracy that aims at

overcoming necessary challenges which do not transform the principles.

Hussain and Raghavan, (2017 p: 137) stated that computerised packages can rapidly

create all sorts of documents required by the management like for example budget assessment

and variance evaluations. The data analysis and processing are more precise and faster which is

able to satisfy the demands of the managers and the management for timely and authentic

information for the purpose of decision making.

Lutfi, Idris and Mohamad, (2016 p: 6) agreed with the time and the speed with the help of

which accounting is undertaken and furthermore explained that a computerised accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

system can construct statement of income, balance sheet and other kinds of accounting

statements at any point of time. He even agreed that “computerised accounting system” permits

the management and the managers to recognise easily and solve issues instantly.

Rikhardsson and Dull, (2016 p: 37) cited that development in the performance of a

business is an outcome of the computerised accounting system as it is a highly cohesive

mechanism that changes the process of a business with the features of performance development

which is inclusive of inventory control, statutory and reporting methods. Rikhardsson and Dull,

(2016 p: 37) even states that this aids an organization in accessing the information quicker and

undertake precise and faster decisions as it even helps in improving the level of communication.

According to López‐pérez, Melero and Javier Sese, (2017 p: 999), it is easy to undertake

the functions of accounting by utilising the computerised accounting systems. The posting of the

transactions to the ledger, the double entry principle can be mechanised by making use of the

computerized accounting process.

Falkner and Hiebl, (2015 p: 144) addressed that managers cannot easily fulfil the donor

and the statutory statement requirements like the balance sheet, profit or loss account and

personalised statements without making use of the “computerised accounting systems”. With the

incorporation of “computerised accounting system”, the process can be done in a quick manner

with minimum level of effort. Computerised accounting system simplifies auditing and have

effective access to the required data like the payments, cheque numbers and various other

transactions, which would be helpful in mitigating the time needed in order to give out this sort

of data and documentation during the auditing time.

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

system can construct statement of income, balance sheet and other kinds of accounting

statements at any point of time. He even agreed that “computerised accounting system” permits

the management and the managers to recognise easily and solve issues instantly.

Rikhardsson and Dull, (2016 p: 37) cited that development in the performance of a

business is an outcome of the computerised accounting system as it is a highly cohesive

mechanism that changes the process of a business with the features of performance development

which is inclusive of inventory control, statutory and reporting methods. Rikhardsson and Dull,

(2016 p: 37) even states that this aids an organization in accessing the information quicker and

undertake precise and faster decisions as it even helps in improving the level of communication.

According to López‐pérez, Melero and Javier Sese, (2017 p: 999), it is easy to undertake

the functions of accounting by utilising the computerised accounting systems. The posting of the

transactions to the ledger, the double entry principle can be mechanised by making use of the

computerized accounting process.

Falkner and Hiebl, (2015 p: 144) addressed that managers cannot easily fulfil the donor

and the statutory statement requirements like the balance sheet, profit or loss account and

personalised statements without making use of the “computerised accounting systems”. With the

incorporation of “computerised accounting system”, the process can be done in a quick manner

with minimum level of effort. Computerised accounting system simplifies auditing and have

effective access to the required data like the payments, cheque numbers and various other

transactions, which would be helpful in mitigating the time needed in order to give out this sort

of data and documentation during the auditing time.

17

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Klovienė and Gimzauskiene, (2015 p: 1712) addresses that there exists a challenge of

ineffective human involvement with the “computer files and computer programs”. The staffs in

the companies may fiddle with the records that are in the computers and computer programs for

the idea of intentionally altering the accounting data. This leads to the misrepresentation of the

data that would be vital for the purpose of decision making.

According to Limburg, Knowles McCulloch and Spira, (2017 p: 188), one of the

limitations and threats of computerised accounting system is the availability of computer virus. It

is known that computer virus is kind of a computer code or a program that is constructed

essentially to cause harm and damage to the computer and computer software that leads to

unbalanced behaviour in the various programs within the computer. The critical impact is that it

may create damage to the software and the hardware and thereby leading to loss of priceless

information like the data related to the customer account, past financial statements, data related

to the loans that have been allowed to others that are already recorded in the computer.

Aduamoah et al.,(2017 p: 5) explained that financial statements is the mechanism of

disclosing the financial data or the information about the financial scenario of an organization,

operating activities and their flow of funds for an accounting time period.

According to Grabinskia, Kedziora and Krasodomska, (2014 p: 281), financial statement

is associated with revealing helpful data to the users so that effective decisions can be

constructed and implemented within an organization. Kemppainen et al.,(2017 p: 21) implied

that financial documentation is the process with the help of which financial data can be used for

the purpose of assessing the transactional figures, timing and the cash flow hesitations. It is even

seen that financial reporting needs to deliver the data about the economic resources of the

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Klovienė and Gimzauskiene, (2015 p: 1712) addresses that there exists a challenge of

ineffective human involvement with the “computer files and computer programs”. The staffs in

the companies may fiddle with the records that are in the computers and computer programs for

the idea of intentionally altering the accounting data. This leads to the misrepresentation of the

data that would be vital for the purpose of decision making.

According to Limburg, Knowles McCulloch and Spira, (2017 p: 188), one of the

limitations and threats of computerised accounting system is the availability of computer virus. It

is known that computer virus is kind of a computer code or a program that is constructed

essentially to cause harm and damage to the computer and computer software that leads to

unbalanced behaviour in the various programs within the computer. The critical impact is that it

may create damage to the software and the hardware and thereby leading to loss of priceless

information like the data related to the customer account, past financial statements, data related

to the loans that have been allowed to others that are already recorded in the computer.

Aduamoah et al.,(2017 p: 5) explained that financial statements is the mechanism of

disclosing the financial data or the information about the financial scenario of an organization,

operating activities and their flow of funds for an accounting time period.

According to Grabinskia, Kedziora and Krasodomska, (2014 p: 281), financial statement

is associated with revealing helpful data to the users so that effective decisions can be

constructed and implemented within an organization. Kemppainen et al.,(2017 p: 21) implied

that financial documentation is the process with the help of which financial data can be used for

the purpose of assessing the transactional figures, timing and the cash flow hesitations. It is even

seen that financial reporting needs to deliver the data about the economic resources of the

18

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

companies, the entitlements against these resources, equity of the owners and the transformations

in the claims and the resources.

Parnell, Long and Lester, (2015 p: 431) stressed that financial statements should provide

facts about the financial performance during the time when the management discharges their

accountabilities to the management and the owners. It would therefore be helpful to the

managers and the management so that they can undertake decisions on behalf of the

entrepreneurs.

In accordance to Patra and Nath, (2016 p: 41), the quality of the financial statement is

dependent on the user who is using the data and therefore should be assess in accordance to the

requirement and demand of the users. Federations of Accounting Standards Board (FASB)

explained quality to be a hierarchy of the qualities of accounting with reliability and preciseness

which is regarded as the key features while representing the verifiability, comparability,

neutrality, faithfulness, understandability and consistency which are looked upon as the

secondary features (Klimczak and Krasodomska, 2017) .

Adeyemi, Obah and Udofiaa, (2015 p: 546) explained that the data is looked upon to be

reliable and dependable if it is independent from material faults and bias and explains effectively

that it looks to disclose. In this manner effective results can be attained.

Rikhardsson and Dull, (2016 p: 37) even explains that the user needs to be able to

compare and assess the financial reports of an organization over a specific time period in order to

recognise the patterns in their financial performance and scenario. This is able to provide better

understanding and knowledge to the companies.

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

companies, the entitlements against these resources, equity of the owners and the transformations

in the claims and the resources.

Parnell, Long and Lester, (2015 p: 431) stressed that financial statements should provide

facts about the financial performance during the time when the management discharges their

accountabilities to the management and the owners. It would therefore be helpful to the

managers and the management so that they can undertake decisions on behalf of the

entrepreneurs.

In accordance to Patra and Nath, (2016 p: 41), the quality of the financial statement is

dependent on the user who is using the data and therefore should be assess in accordance to the

requirement and demand of the users. Federations of Accounting Standards Board (FASB)

explained quality to be a hierarchy of the qualities of accounting with reliability and preciseness

which is regarded as the key features while representing the verifiability, comparability,

neutrality, faithfulness, understandability and consistency which are looked upon as the

secondary features (Klimczak and Krasodomska, 2017) .

Adeyemi, Obah and Udofiaa, (2015 p: 546) explained that the data is looked upon to be

reliable and dependable if it is independent from material faults and bias and explains effectively

that it looks to disclose. In this manner effective results can be attained.

Rikhardsson and Dull, (2016 p: 37) even explains that the user needs to be able to

compare and assess the financial reports of an organization over a specific time period in order to

recognise the patterns in their financial performance and scenario. This is able to provide better

understanding and knowledge to the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Troshani, Parker and Lymer,(2015 p: 228) stresses on the fact that timeliness is another

key feature of the quality of the financial data. This ascends as an outcome of accounting data

perishability. In order to assist the users, the financial data must be disclosed at the precise time

or else the data would lose their relevance.

Yanto et al., (2016 p: 63), stated that understandability is a feature of financial

documenting that assists the users to understand the vitality of the financial data. He even

debates that the users are expected to have significant amount of knowledge about the business

and the willingness to examine and have proper understanding of the information. The

International Accounting Standards Boards further brings in that data should not be omitted on

the factor that it may be complex for few of the users to gain an understanding.

The effect of “computerised accounting system” on the construction of the financial

statements has been connected to the advantages of incorporating the computer process while

constructing the financial reports.

In accordance to Ng et al.,(2017 p: 349), the disclosure of the scheduled documents can

be simplified and triggered and constructed at systematic interval with ease. With the

implementation of computerization, construction of the financial statements would be easier as

the data can be created easily and on a frequent basis can be updated.

With the considerable rise in the frequency of transactions and rise in the demand for

actual time data, the management of the accounting information on an actual time basis has

become significant. This is attainable by utilising the computerised processes and thereby

stimulating the quality of the financial statements. Giner,hellman, Jorissen-Quagli and Taleb,

THE IMPACT OF COMPUTERISED ACCOUNTING SYSTEMS (CAS) IN THE

FINANCIAL REPORTING AMONG SMES IN MALDIVES

Troshani, Parker and Lymer,(2015 p: 228) stresses on the fact that timeliness is another

key feature of the quality of the financial data. This ascends as an outcome of accounting data

perishability. In order to assist the users, the financial data must be disclosed at the precise time

or else the data would lose their relevance.

Yanto et al., (2016 p: 63), stated that understandability is a feature of financial

documenting that assists the users to understand the vitality of the financial data. He even