Accounting Assignment: IFRS, Percentage Completion, Revaluation

VerifiedAdded on 2020/05/16

|10

|1483

|124

Homework Assignment

AI Summary

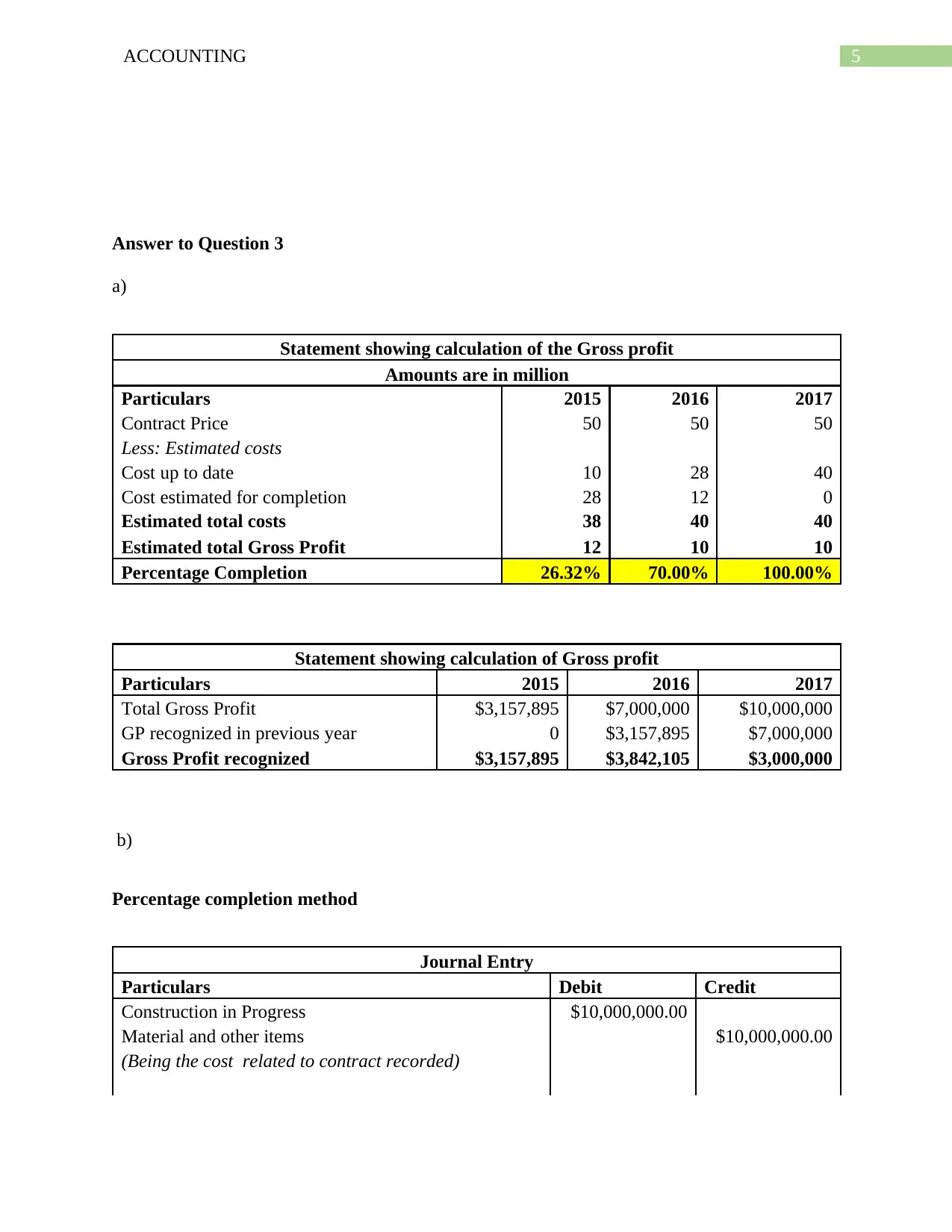

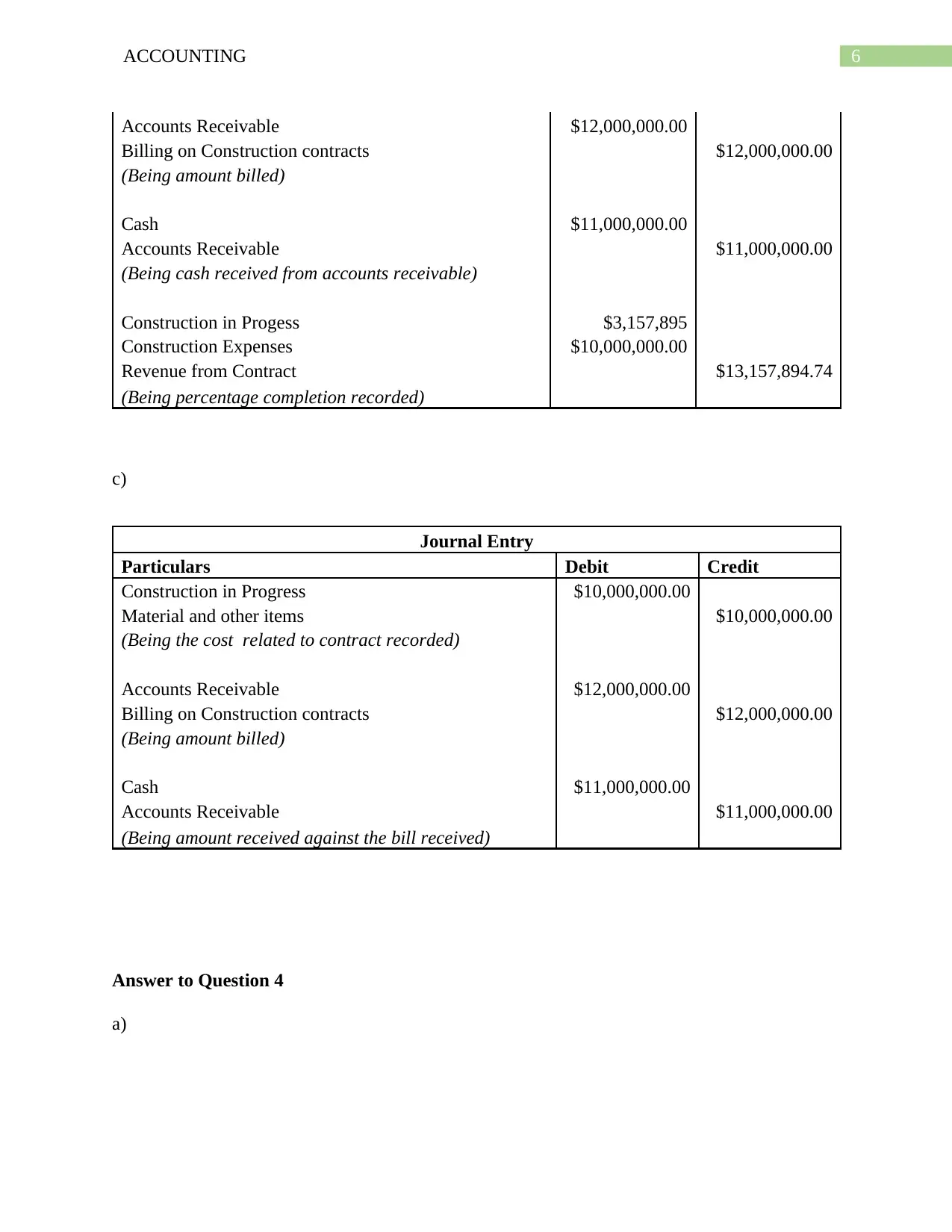

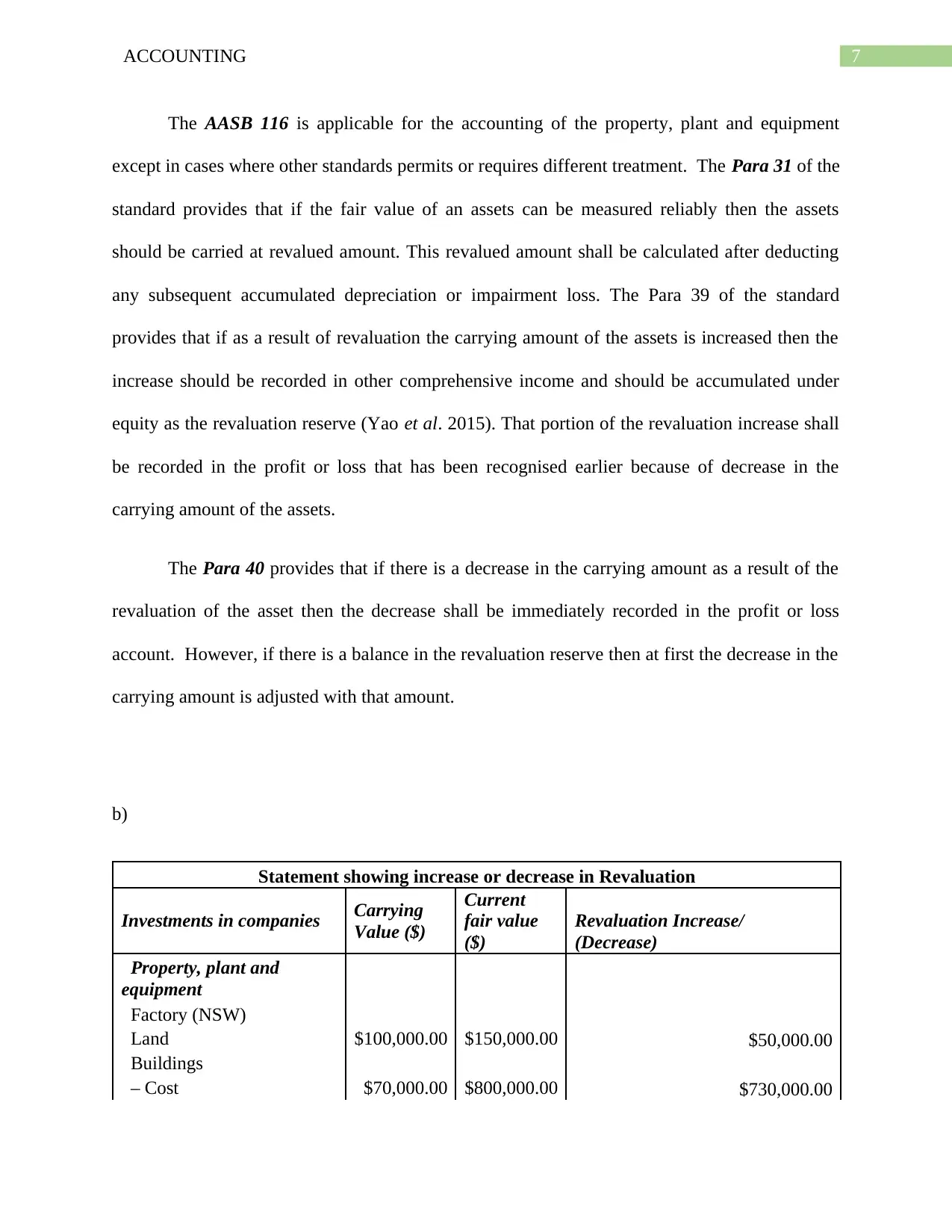

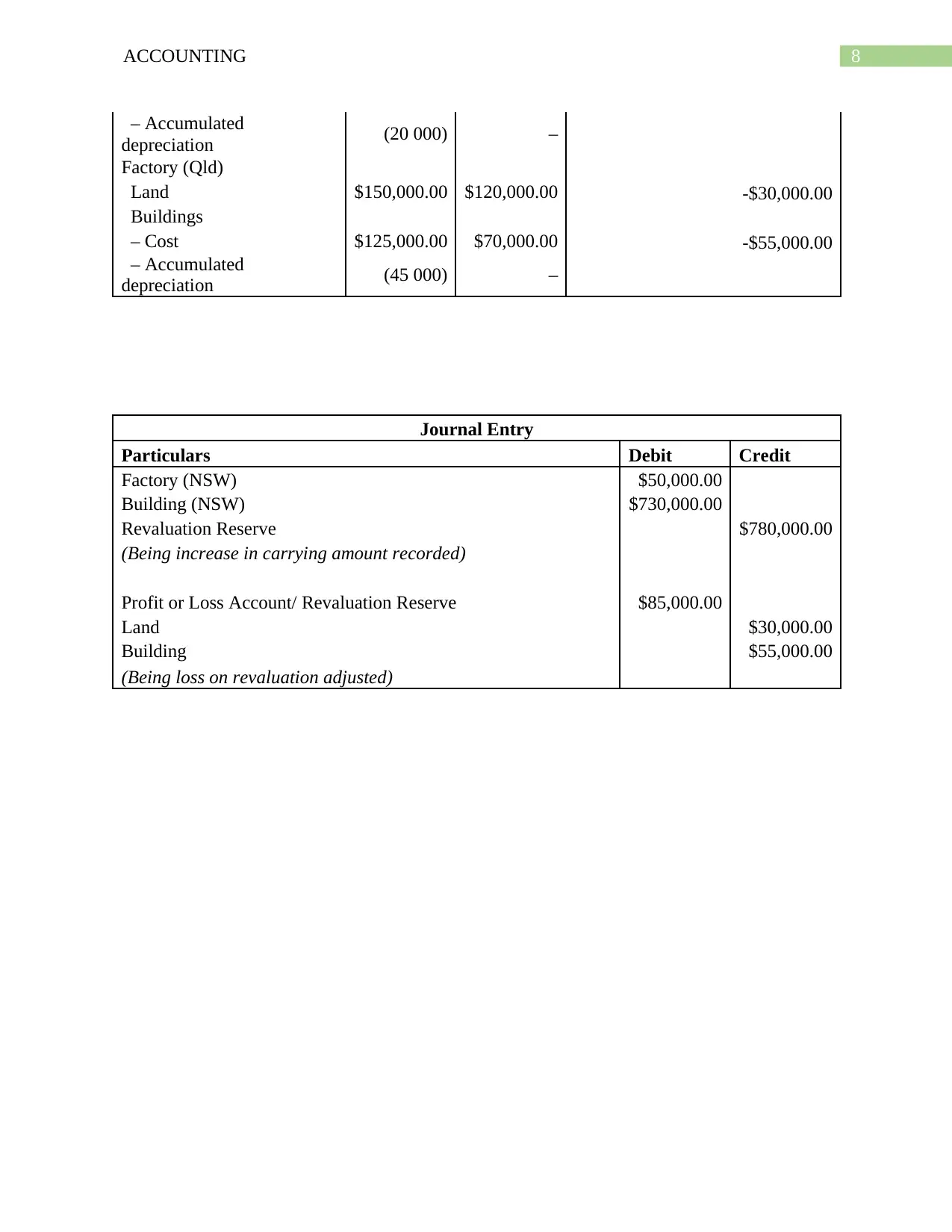

This accounting assignment provides solutions to four key questions related to financial accounting. The first question addresses the accounting treatment of goodwill, comparing the traditional amortization method with impairment testing, highlighting the relevance of IFRS 3. The second question focuses on debentures, including calculations for issue price based on semi-annual coupon rates and market interest rates, accompanied by journal entries for debenture issuance and interest recognition. The third question examines the percentage completion method in construction accounting, presenting calculations for gross profit recognition and illustrating journal entries for cost recording, billing, and revenue recognition. Finally, the fourth question covers property, plant, and equipment, specifically addressing revaluation under AASB 116, including journal entries for increases and decreases in asset carrying amounts. The assignment demonstrates the application of accounting standards and principles.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.