Concepts and the Process of Cost Accounting

VerifiedAdded on 2021/06/18

|15

|2831

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Cost Accounting

1

Project Report: Cost accounting

1

Project Report: Cost accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost Accounting

2

Job costing:

Normal Solution:

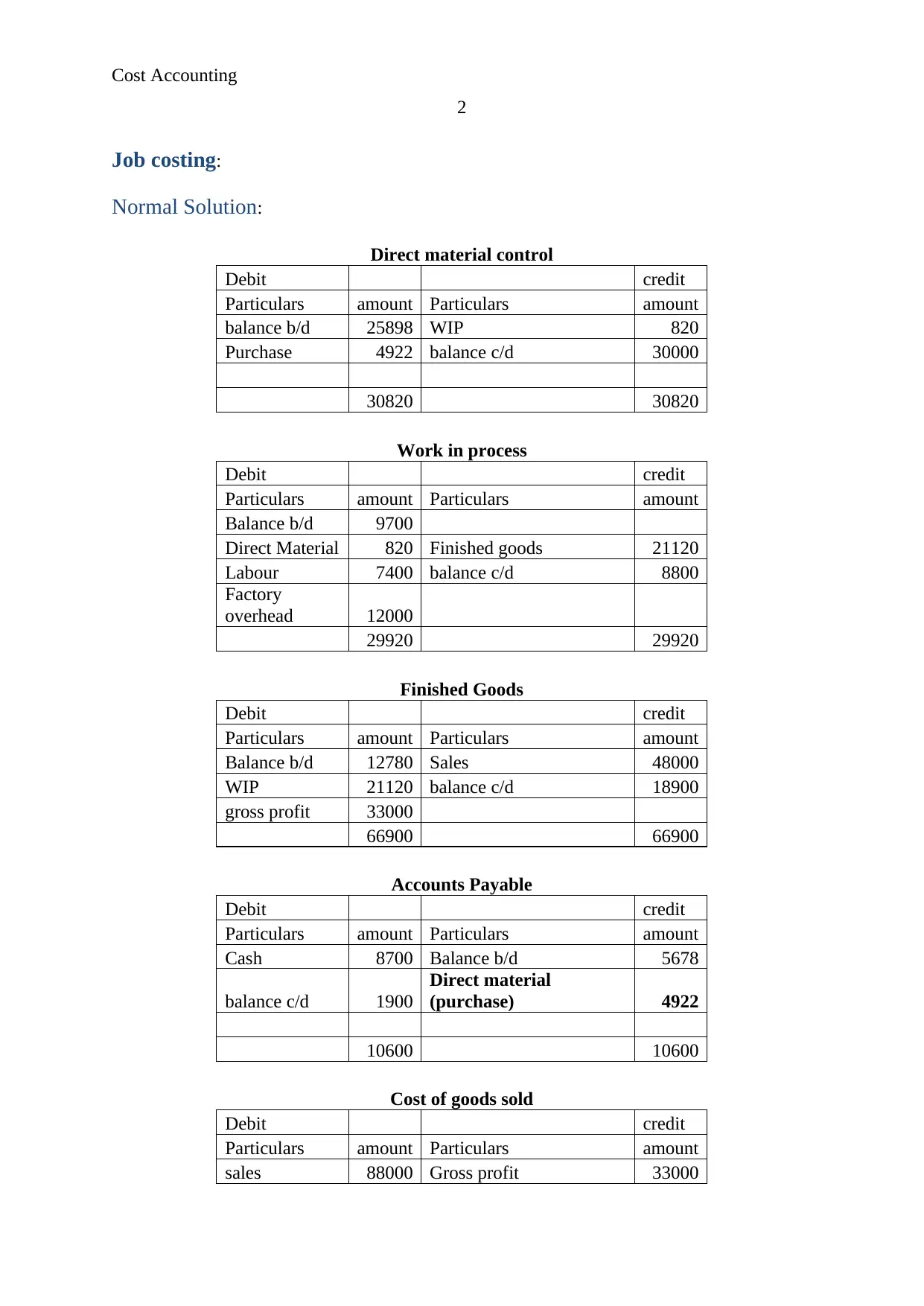

Direct material control

Debit credit

Particulars amount Particulars amount

balance b/d 25898 WIP 820

Purchase 4922 balance c/d 30000

30820 30820

Work in process

Debit credit

Particulars amount Particulars amount

Balance b/d 9700

Direct Material 820 Finished goods 21120

Labour 7400 balance c/d 8800

Factory

overhead 12000

29920 29920

Finished Goods

Debit credit

Particulars amount Particulars amount

Balance b/d 12780 Sales 48000

WIP 21120 balance c/d 18900

gross profit 33000

66900 66900

Accounts Payable

Debit credit

Particulars amount Particulars amount

Cash 8700 Balance b/d 5678

balance c/d 1900

Direct material

(purchase) 4922

10600 10600

Cost of goods sold

Debit credit

Particulars amount Particulars amount

sales 88000 Gross profit 33000

2

Job costing:

Normal Solution:

Direct material control

Debit credit

Particulars amount Particulars amount

balance b/d 25898 WIP 820

Purchase 4922 balance c/d 30000

30820 30820

Work in process

Debit credit

Particulars amount Particulars amount

Balance b/d 9700

Direct Material 820 Finished goods 21120

Labour 7400 balance c/d 8800

Factory

overhead 12000

29920 29920

Finished Goods

Debit credit

Particulars amount Particulars amount

Balance b/d 12780 Sales 48000

WIP 21120 balance c/d 18900

gross profit 33000

66900 66900

Accounts Payable

Debit credit

Particulars amount Particulars amount

Cash 8700 Balance b/d 5678

balance c/d 1900

Direct material

(purchase) 4922

10600 10600

Cost of goods sold

Debit credit

Particulars amount Particulars amount

sales 88000 Gross profit 33000

Cost Accounting

3

Balance c/d 55000

88000 88000

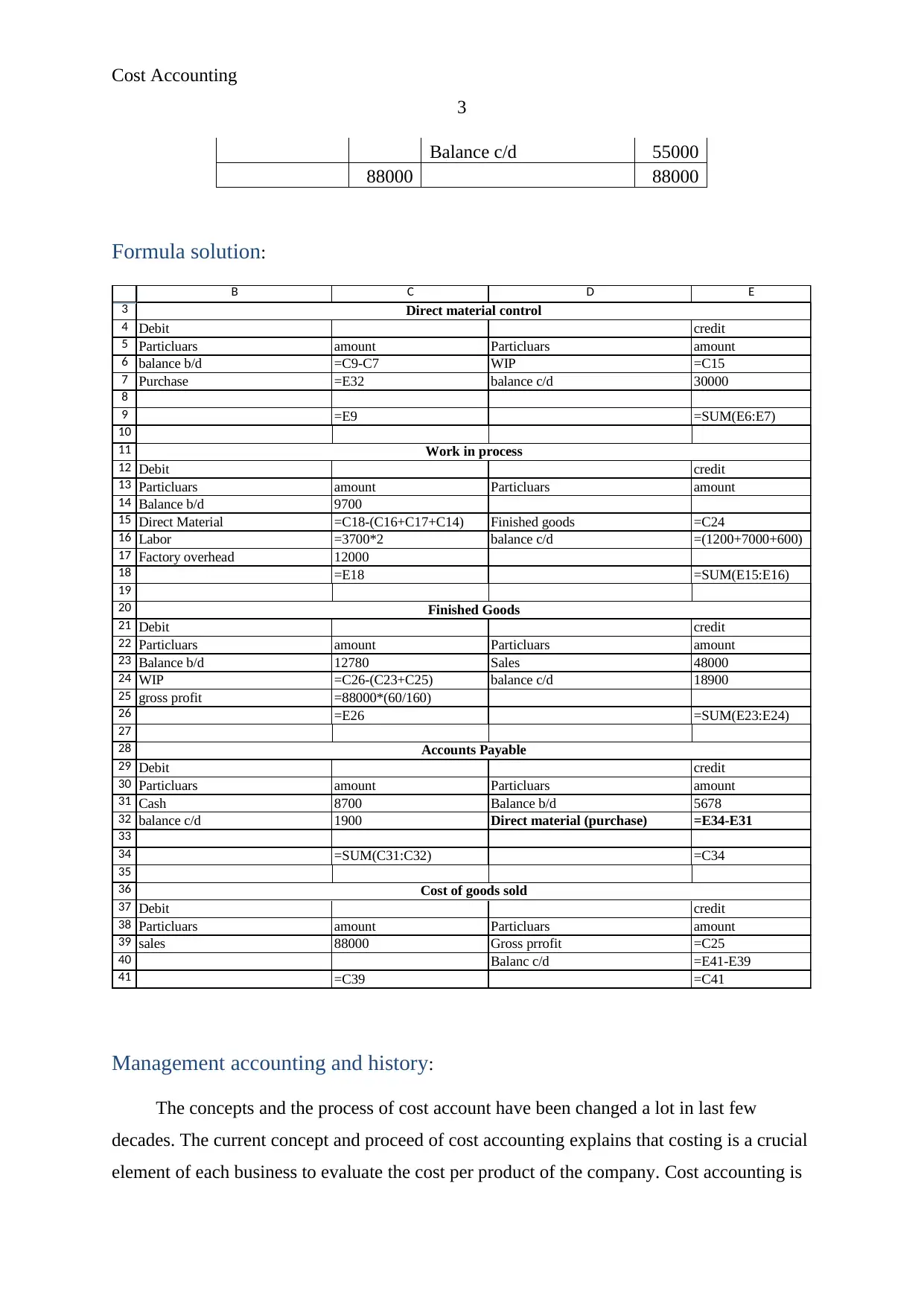

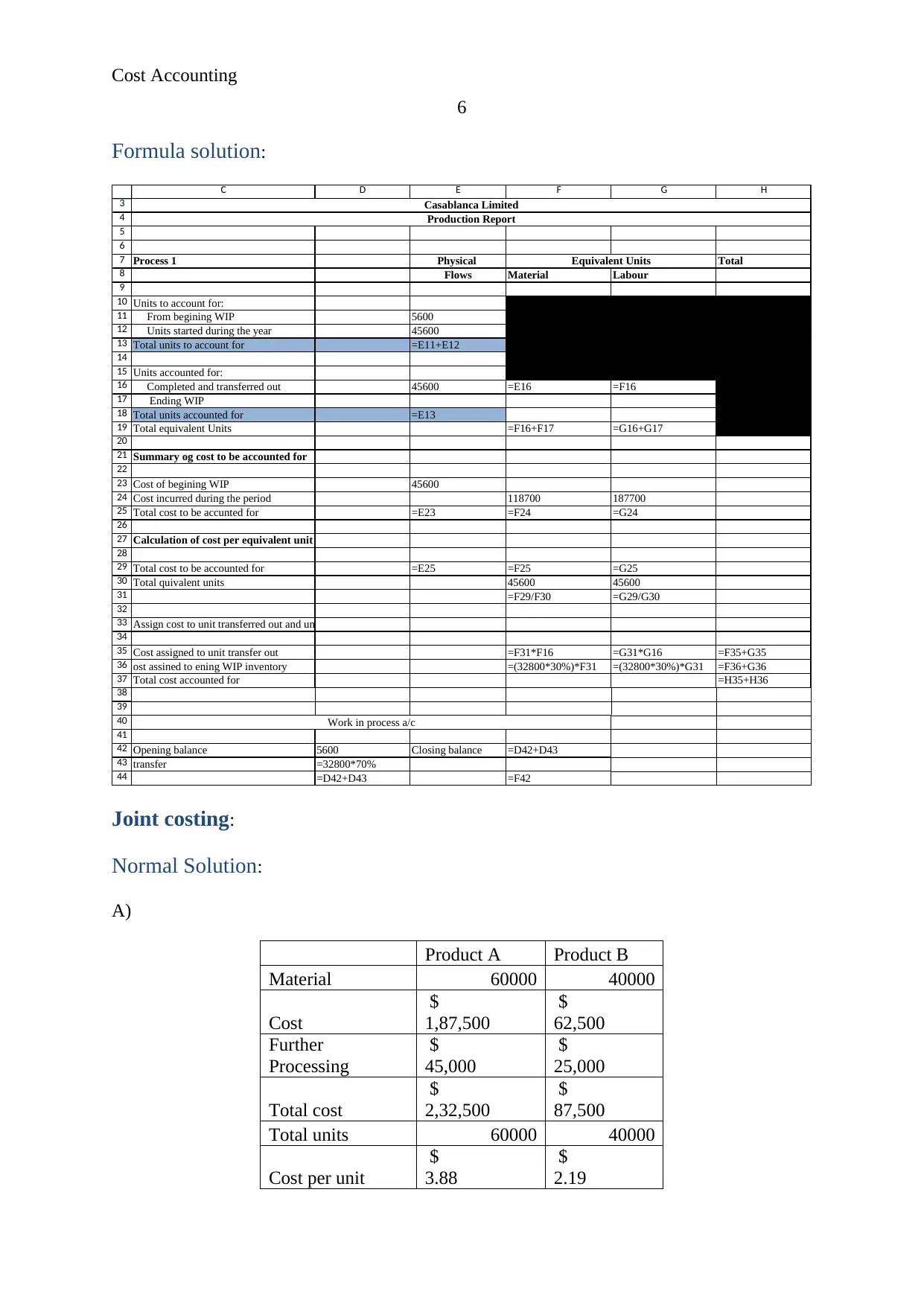

Formula solution:

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

B C D E

Debit credit

Particluars amount Particluars amount

balance b/d =C9-C7 WIP =C15

Purchase =E32 balance c/d 30000

=E9 =SUM(E6:E7)

Debit credit

Particluars amount Particluars amount

Balance b/d 9700

Direct Material =C18-(C16+C17+C14) Finished goods =C24

Labor =3700*2 balance c/d =(1200+7000+600)

Factory overhead 12000

=E18 =SUM(E15:E16)

Debit credit

Particluars amount Particluars amount

Balance b/d 12780 Sales 48000

WIP =C26-(C23+C25) balance c/d 18900

gross profit =88000*(60/160)

=E26 =SUM(E23:E24)

Debit credit

Particluars amount Particluars amount

Cash 8700 Balance b/d 5678

balance c/d 1900 Direct material (purchase) =E34-E31

=SUM(C31:C32) =C34

Debit credit

Particluars amount Particluars amount

sales 88000 Gross prrofit =C25

Balanc c/d =E41-E39

=C39 =C41

Direct material control

Work in process

Finished Goods

Accounts Payable

Cost of goods sold

Management accounting and history:

The concepts and the process of cost account have been changed a lot in last few

decades. The current concept and proceed of cost accounting explains that costing is a crucial

element of each business to evaluate the cost per product of the company. Cost accounting is

3

Balance c/d 55000

88000 88000

Formula solution:

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

B C D E

Debit credit

Particluars amount Particluars amount

balance b/d =C9-C7 WIP =C15

Purchase =E32 balance c/d 30000

=E9 =SUM(E6:E7)

Debit credit

Particluars amount Particluars amount

Balance b/d 9700

Direct Material =C18-(C16+C17+C14) Finished goods =C24

Labor =3700*2 balance c/d =(1200+7000+600)

Factory overhead 12000

=E18 =SUM(E15:E16)

Debit credit

Particluars amount Particluars amount

Balance b/d 12780 Sales 48000

WIP =C26-(C23+C25) balance c/d 18900

gross profit =88000*(60/160)

=E26 =SUM(E23:E24)

Debit credit

Particluars amount Particluars amount

Cash 8700 Balance b/d 5678

balance c/d 1900 Direct material (purchase) =E34-E31

=SUM(C31:C32) =C34

Debit credit

Particluars amount Particluars amount

sales 88000 Gross prrofit =C25

Balanc c/d =E41-E39

=C39 =C41

Direct material control

Work in process

Finished Goods

Accounts Payable

Cost of goods sold

Management accounting and history:

The concepts and the process of cost account have been changed a lot in last few

decades. The current concept and proceed of cost accounting explains that costing is a crucial

element of each business to evaluate the cost per product of the company. Cost accounting is

Cost Accounting

4

proceeding by the companies through evaluating all the related aspect and the performance of

the company (Weygandt, Kimmel & Kieso, 2015). Current modern concept of accounting

explains about process of the company, it is a better way to identify the profit percentage as

well as it briefs about the variances which have occurred into the business in a particular time

period.

Figure 1

The Roman Coliseum has been studied further to evaluate the concept of cost

accounting and the structure of cost accounting. The Roman Coliseum is one of the big and

great buildings of the country; the structure of the building has been prepared by the

architecture after evaluating and figuring out all the related factors. The study on Roman

Coliseum explains that the process of cost accounting should be in a manner that it could

attract the people as well as the internal strength of the company could also be built. Thus, it

has been found that the modern accounting could be applied in current scenario of the

business to make the changes into the structure of the company for good

Process costing:

Normal Solution:

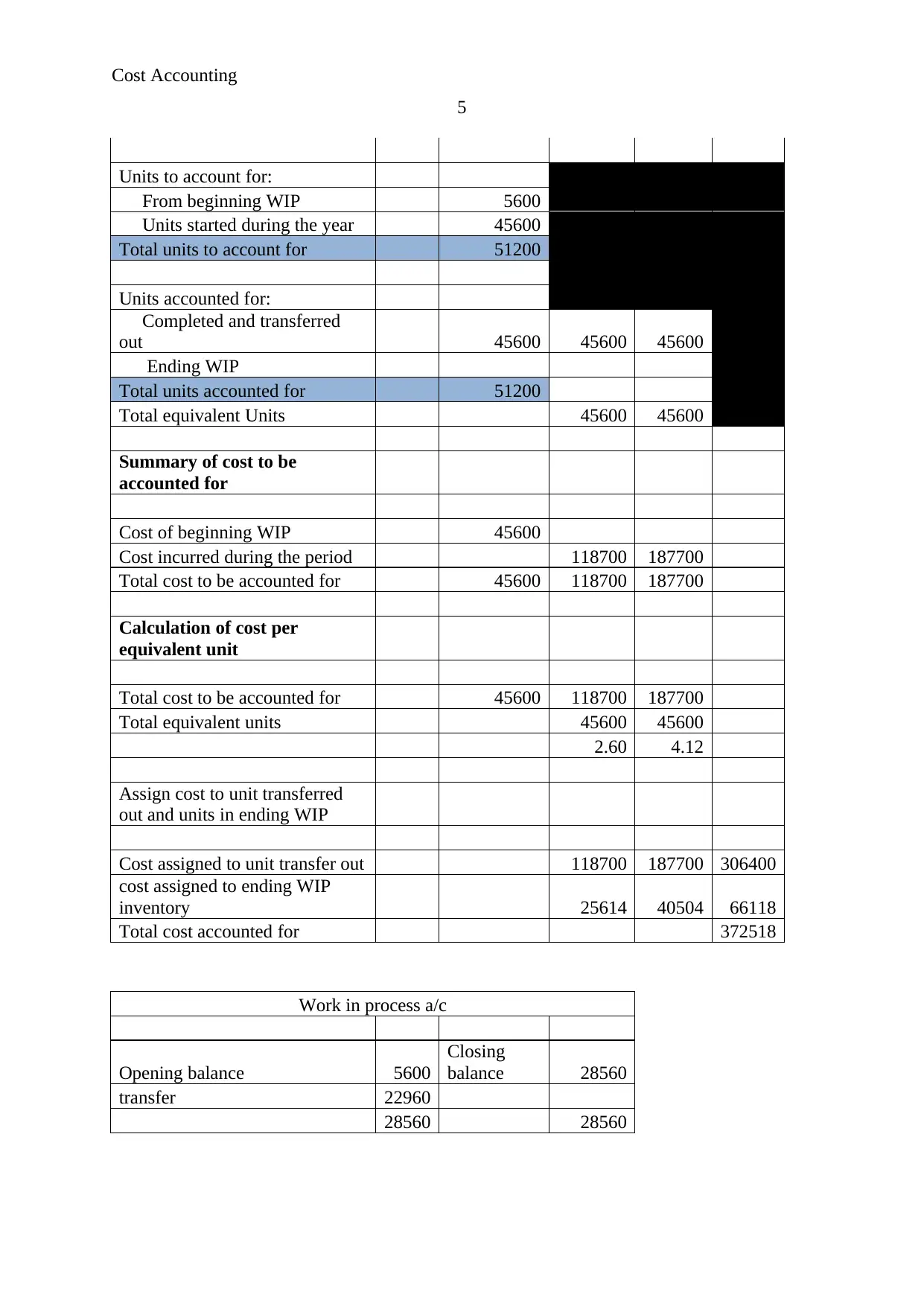

Casablanca Limited

Production Report

Process 1 Physical Equivalent Units Total

Flows Material Labour

4

proceeding by the companies through evaluating all the related aspect and the performance of

the company (Weygandt, Kimmel & Kieso, 2015). Current modern concept of accounting

explains about process of the company, it is a better way to identify the profit percentage as

well as it briefs about the variances which have occurred into the business in a particular time

period.

Figure 1

The Roman Coliseum has been studied further to evaluate the concept of cost

accounting and the structure of cost accounting. The Roman Coliseum is one of the big and

great buildings of the country; the structure of the building has been prepared by the

architecture after evaluating and figuring out all the related factors. The study on Roman

Coliseum explains that the process of cost accounting should be in a manner that it could

attract the people as well as the internal strength of the company could also be built. Thus, it

has been found that the modern accounting could be applied in current scenario of the

business to make the changes into the structure of the company for good

Process costing:

Normal Solution:

Casablanca Limited

Production Report

Process 1 Physical Equivalent Units Total

Flows Material Labour

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost Accounting

5

Units to account for:

From beginning WIP 5600

Units started during the year 45600

Total units to account for 51200

Units accounted for:

Completed and transferred

out 45600 45600 45600

Ending WIP

Total units accounted for 51200

Total equivalent Units 45600 45600

Summary of cost to be

accounted for

Cost of beginning WIP 45600

Cost incurred during the period 118700 187700

Total cost to be accounted for 45600 118700 187700

Calculation of cost per

equivalent unit

Total cost to be accounted for 45600 118700 187700

Total equivalent units 45600 45600

2.60 4.12

Assign cost to unit transferred

out and units in ending WIP

Cost assigned to unit transfer out 118700 187700 306400

cost assigned to ending WIP

inventory 25614 40504 66118

Total cost accounted for 372518

Work in process a/c

Opening balance 5600

Closing

balance 28560

transfer 22960

28560 28560

5

Units to account for:

From beginning WIP 5600

Units started during the year 45600

Total units to account for 51200

Units accounted for:

Completed and transferred

out 45600 45600 45600

Ending WIP

Total units accounted for 51200

Total equivalent Units 45600 45600

Summary of cost to be

accounted for

Cost of beginning WIP 45600

Cost incurred during the period 118700 187700

Total cost to be accounted for 45600 118700 187700

Calculation of cost per

equivalent unit

Total cost to be accounted for 45600 118700 187700

Total equivalent units 45600 45600

2.60 4.12

Assign cost to unit transferred

out and units in ending WIP

Cost assigned to unit transfer out 118700 187700 306400

cost assigned to ending WIP

inventory 25614 40504 66118

Total cost accounted for 372518

Work in process a/c

Opening balance 5600

Closing

balance 28560

transfer 22960

28560 28560

Cost Accounting

6

Formula solution:

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

C D E F G H

Process 1 Physical Total

Flows Material Labour

Units to account for:

From begining WIP 5600

Units started during the year 45600

Total units to account for =E11+E12

Units accounted for:

Completed and transferred out 45600 =E16 =F16

Ending WIP

Total units accounted for =E13

Total equivalent Units =F16+F17 =G16+G17

Summary og cost to be accounted for

Cost of begining WIP 45600

Cost incurred during the period 118700 187700

Total cost to be accunted for =E23 =F24 =G24

Calculation of cost per equivalent unit

Total cost to be accounted for =E25 =F25 =G25

Total quivalent units 45600 45600

=F29/F30 =G29/G30

Assign cost to unit transferred out and units in ending WIP

Cost assigned to unit transfer out =F31*F16 =G31*G16 =F35+G35

ost assined to ening WIP inventory =(32800*30%)*F31 =(32800*30%)*G31 =F36+G36

Total cost accounted for =H35+H36

Opening balance 5600 Closing balance =D42+D43

transfer =32800*70%

=D42+D43 =F42

Casablanca Limited

Production Report

Equivalent Units

Work in process a/c

Joint costing:

Normal Solution:

A)

Product A Product B

Material 60000 40000

Cost

$

1,87,500

$

62,500

Further

Processing

$

45,000

$

25,000

Total cost

$

2,32,500

$

87,500

Total units 60000 40000

Cost per unit

$

3.88

$

2.19

6

Formula solution:

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

C D E F G H

Process 1 Physical Total

Flows Material Labour

Units to account for:

From begining WIP 5600

Units started during the year 45600

Total units to account for =E11+E12

Units accounted for:

Completed and transferred out 45600 =E16 =F16

Ending WIP

Total units accounted for =E13

Total equivalent Units =F16+F17 =G16+G17

Summary og cost to be accounted for

Cost of begining WIP 45600

Cost incurred during the period 118700 187700

Total cost to be accunted for =E23 =F24 =G24

Calculation of cost per equivalent unit

Total cost to be accounted for =E25 =F25 =G25

Total quivalent units 45600 45600

=F29/F30 =G29/G30

Assign cost to unit transferred out and units in ending WIP

Cost assigned to unit transfer out =F31*F16 =G31*G16 =F35+G35

ost assined to ening WIP inventory =(32800*30%)*F31 =(32800*30%)*G31 =F36+G36

Total cost accounted for =H35+H36

Opening balance 5600 Closing balance =D42+D43

transfer =32800*70%

=D42+D43 =F42

Casablanca Limited

Production Report

Equivalent Units

Work in process a/c

Joint costing:

Normal Solution:

A)

Product A Product B

Material 60000 40000

Cost

$

1,87,500

$

62,500

Further

Processing

$

45,000

$

25,000

Total cost

$

2,32,500

$

87,500

Total units 60000 40000

Cost per unit

$

3.88

$

2.19

Cost Accounting

7

Selling price per

unit

$

4.50

$

2.54

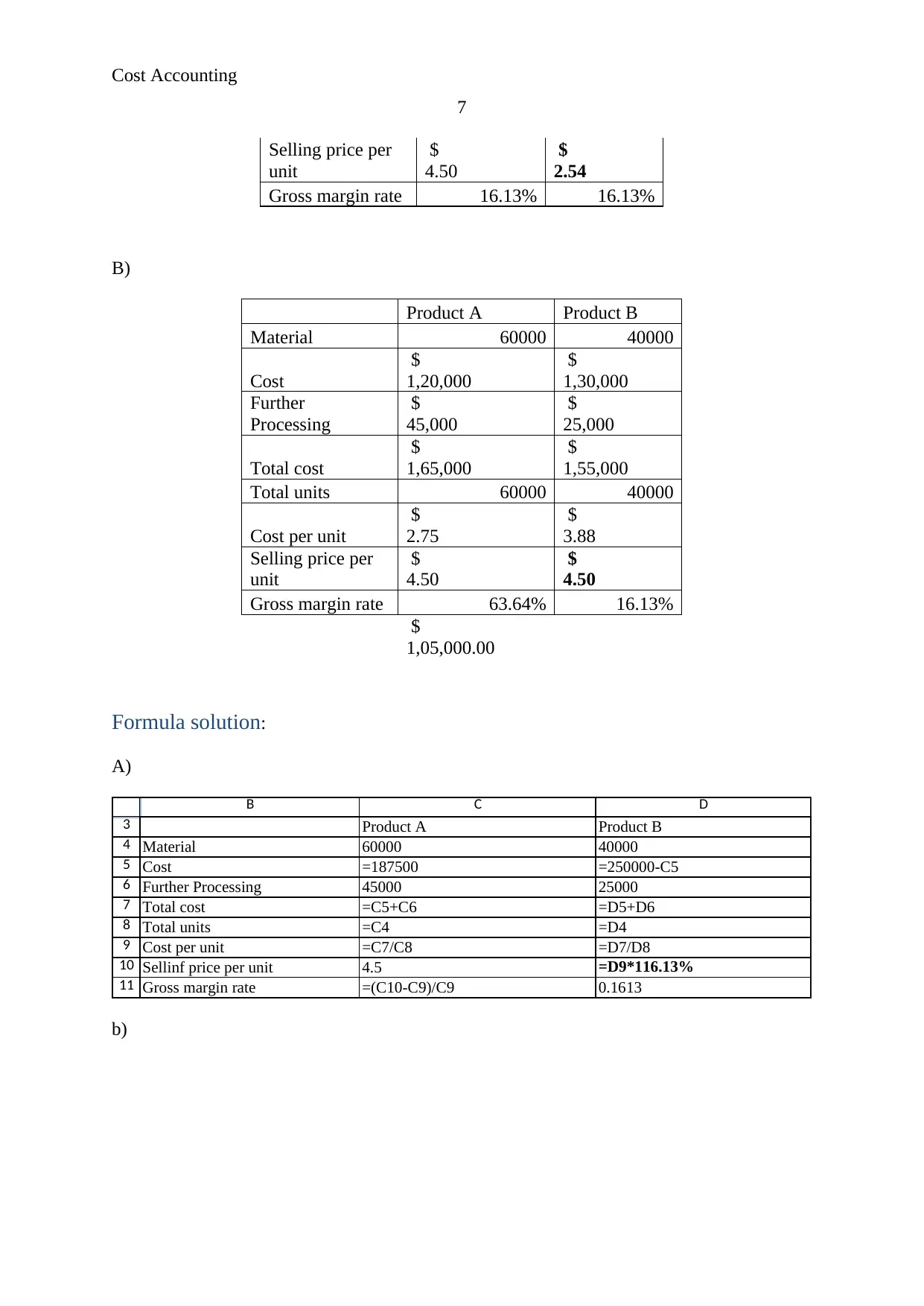

Gross margin rate 16.13% 16.13%

B)

Product A Product B

Material 60000 40000

Cost

$

1,20,000

$

1,30,000

Further

Processing

$

45,000

$

25,000

Total cost

$

1,65,000

$

1,55,000

Total units 60000 40000

Cost per unit

$

2.75

$

3.88

Selling price per

unit

$

4.50

$

4.50

Gross margin rate 63.64% 16.13%

$

1,05,000.00

Formula solution:

A)

3

4

5

6

7

8

9

10

11

B C D

Product A Product B

Material 60000 40000

Cost =187500 =250000-C5

Further Processing 45000 25000

Total cost =C5+C6 =D5+D6

Total units =C4 =D4

Cost per unit =C7/C8 =D7/D8

Sellinf price per unit 4.5 =D9*116.13%

Gross margin rate =(C10-C9)/C9 0.1613

b)

7

Selling price per

unit

$

4.50

$

2.54

Gross margin rate 16.13% 16.13%

B)

Product A Product B

Material 60000 40000

Cost

$

1,20,000

$

1,30,000

Further

Processing

$

45,000

$

25,000

Total cost

$

1,65,000

$

1,55,000

Total units 60000 40000

Cost per unit

$

2.75

$

3.88

Selling price per

unit

$

4.50

$

4.50

Gross margin rate 63.64% 16.13%

$

1,05,000.00

Formula solution:

A)

3

4

5

6

7

8

9

10

11

B C D

Product A Product B

Material 60000 40000

Cost =187500 =250000-C5

Further Processing 45000 25000

Total cost =C5+C6 =D5+D6

Total units =C4 =D4

Cost per unit =C7/C8 =D7/D8

Sellinf price per unit 4.5 =D9*116.13%

Gross margin rate =(C10-C9)/C9 0.1613

b)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost Accounting

8

3

4

5

6

7

8

9

10

11

12

G H I

Product A Product B

Material 60000 40000

Cost 120000 =250000-H5

Further Processing 45000 25000

Total cost =H5+H6 =I5+I6

Total units =H4 =I4

Cost per unit =H7/H8 =I7/I8

Sellinf price per unit 4.5 =I9*116.13%

Gross margin rate =(H10-H9)/H9 0.1613

=H8*(H10-H9)

Suggestions:

through the above calculations, it has been found that if the company gets an offer

about buying the material for product A is $ 2 per Kg only than it would lead to the total cost

of the product A to $ 1,20,000 and it would lead to the sales price of the product to $ 4.5 per

unit. On the other hand, the current level of cost of product A is $ 2,32,500. It further

explains that if the product C would be manufactured than the total cost of the product C

would be $ 1,65,000 and at this level, the profit of the company would be $ 1,05,000. It

explains that the company should accept the project and must further process the product to

get higher returns.

Variance analysis:

Normal Solution:

Standard cost variance analysis - JEDI limited

Data

Standards

Kg/ hour Per unit Total

Material 12

$

7

$

84

Direct Labour 3

$

30

$

90

Monthly Production Data

Units Produced 22,000

Material Used 2,03,000 kg

Labour Worked Hours

8

3

4

5

6

7

8

9

10

11

12

G H I

Product A Product B

Material 60000 40000

Cost 120000 =250000-H5

Further Processing 45000 25000

Total cost =H5+H6 =I5+I6

Total units =H4 =I4

Cost per unit =H7/H8 =I7/I8

Sellinf price per unit 4.5 =I9*116.13%

Gross margin rate =(H10-H9)/H9 0.1613

=H8*(H10-H9)

Suggestions:

through the above calculations, it has been found that if the company gets an offer

about buying the material for product A is $ 2 per Kg only than it would lead to the total cost

of the product A to $ 1,20,000 and it would lead to the sales price of the product to $ 4.5 per

unit. On the other hand, the current level of cost of product A is $ 2,32,500. It further

explains that if the product C would be manufactured than the total cost of the product C

would be $ 1,65,000 and at this level, the profit of the company would be $ 1,05,000. It

explains that the company should accept the project and must further process the product to

get higher returns.

Variance analysis:

Normal Solution:

Standard cost variance analysis - JEDI limited

Data

Standards

Kg/ hour Per unit Total

Material 12

$

7

$

84

Direct Labour 3

$

30

$

90

Monthly Production Data

Units Produced 22,000

Material Used 2,03,000 kg

Labour Worked Hours

Cost Accounting

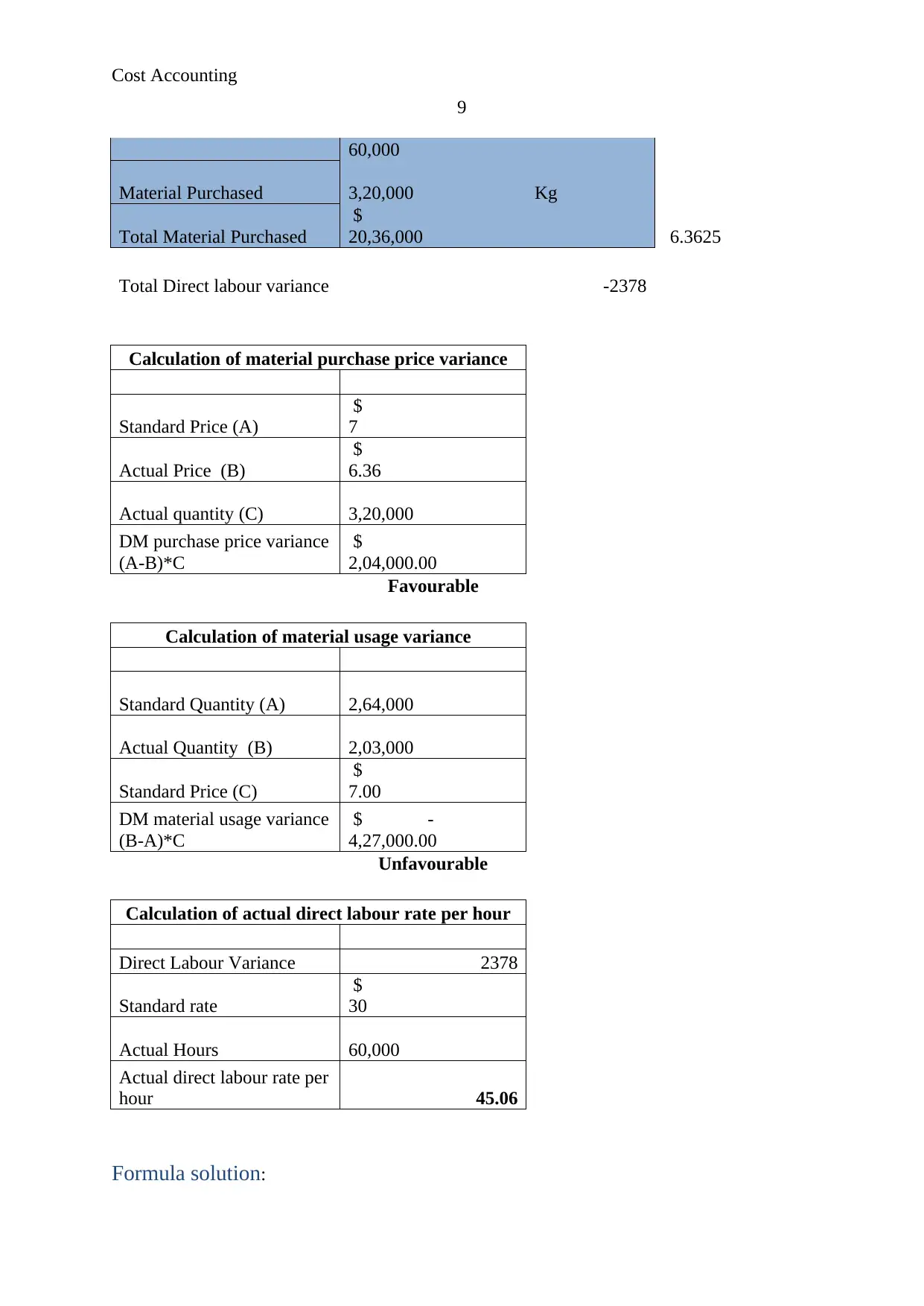

9

60,000

Material Purchased 3,20,000 Kg

Total Material Purchased

$

20,36,000 6.3625

Total Direct labour variance -2378

Calculation of material purchase price variance

Standard Price (A)

$

7

Actual Price (B)

$

6.36

Actual quantity (C) 3,20,000

DM purchase price variance

(A-B)*C

$

2,04,000.00

Favourable

Calculation of material usage variance

Standard Quantity (A) 2,64,000

Actual Quantity (B) 2,03,000

Standard Price (C)

$

7.00

DM material usage variance

(B-A)*C

$ -

4,27,000.00

Unfavourable

Calculation of actual direct labour rate per hour

Direct Labour Variance 2378

Standard rate

$

30

Actual Hours 60,000

Actual direct labour rate per

hour 45.06

Formula solution:

9

60,000

Material Purchased 3,20,000 Kg

Total Material Purchased

$

20,36,000 6.3625

Total Direct labour variance -2378

Calculation of material purchase price variance

Standard Price (A)

$

7

Actual Price (B)

$

6.36

Actual quantity (C) 3,20,000

DM purchase price variance

(A-B)*C

$

2,04,000.00

Favourable

Calculation of material usage variance

Standard Quantity (A) 2,64,000

Actual Quantity (B) 2,03,000

Standard Price (C)

$

7.00

DM material usage variance

(B-A)*C

$ -

4,27,000.00

Unfavourable

Calculation of actual direct labour rate per hour

Direct Labour Variance 2378

Standard rate

$

30

Actual Hours 60,000

Actual direct labour rate per

hour 45.06

Formula solution:

Cost Accounting

10

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

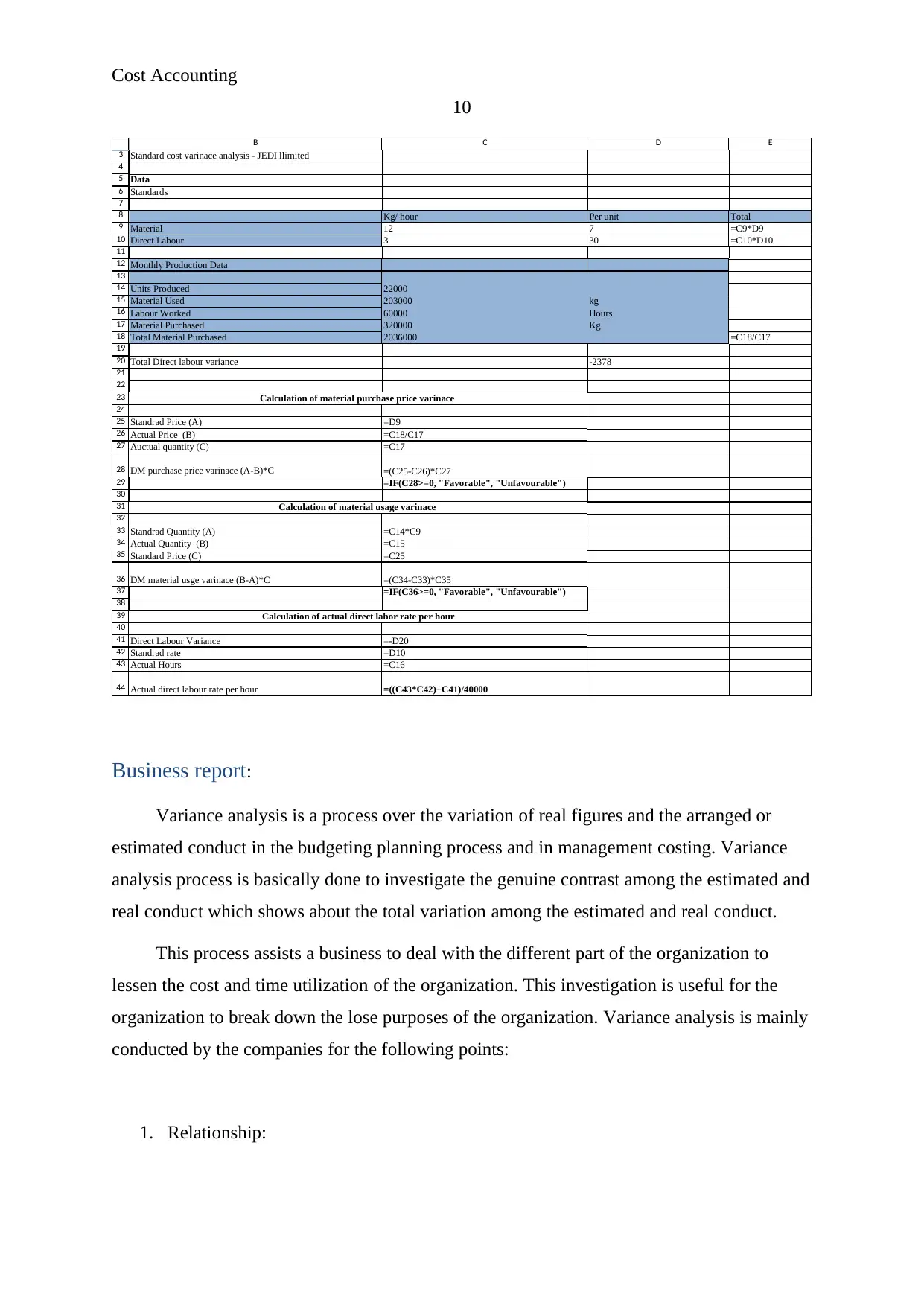

B C D E

Standard cost varinace analysis - JEDI llimited

Data

Standards

Kg/ hour Per unit Total

Material 12 7 =C9*D9

Direct Labour 3 30 =C10*D10

Monthly Production Data

Units Produced 22000

Material Used 203000 kg

Labour Worked 60000 Hours

Material Purchased 320000 Kg

Total Material Purchased 2036000 =C18/C17

Total Direct labour variance -2378

Standrad Price (A) =D9

Actual Price (B) =C18/C17

Auctual quantity (C) =C17

DM purchase price varinace (A-B)*C =(C25-C26)*C27

=IF(C28>=0, "Favorable", "Unfavourable")

Standrad Quantity (A) =C14*C9

Actual Quantity (B) =C15

Standard Price (C) =C25

DM material usge varinace (B-A)*C =(C34-C33)*C35

=IF(C36>=0, "Favorable", "Unfavourable")

Direct Labour Variance =-D20

Standrad rate =D10

Actual Hours =C16

Actual direct labour rate per hour =((C43*C42)+C41)/40000

Calculation of material purchase price varinace

Calculation of material usage varinace

Calculation of actual direct labor rate per hour

Business report:

Variance analysis is a process over the variation of real figures and the arranged or

estimated conduct in the budgeting planning process and in management costing. Variance

analysis process is basically done to investigate the genuine contrast among the estimated and

real conduct which shows about the total variation among the estimated and real conduct.

This process assists a business to deal with the different part of the organization to

lessen the cost and time utilization of the organization. This investigation is useful for the

organization to break down the lose purposes of the organization. Variance analysis is mainly

conducted by the companies for the following points:

1. Relationship:

10

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

B C D E

Standard cost varinace analysis - JEDI llimited

Data

Standards

Kg/ hour Per unit Total

Material 12 7 =C9*D9

Direct Labour 3 30 =C10*D10

Monthly Production Data

Units Produced 22000

Material Used 203000 kg

Labour Worked 60000 Hours

Material Purchased 320000 Kg

Total Material Purchased 2036000 =C18/C17

Total Direct labour variance -2378

Standrad Price (A) =D9

Actual Price (B) =C18/C17

Auctual quantity (C) =C17

DM purchase price varinace (A-B)*C =(C25-C26)*C27

=IF(C28>=0, "Favorable", "Unfavourable")

Standrad Quantity (A) =C14*C9

Actual Quantity (B) =C15

Standard Price (C) =C25

DM material usge varinace (B-A)*C =(C34-C33)*C35

=IF(C36>=0, "Favorable", "Unfavourable")

Direct Labour Variance =-D20

Standrad rate =D10

Actual Hours =C16

Actual direct labour rate per hour =((C43*C42)+C41)/40000

Calculation of material purchase price varinace

Calculation of material usage varinace

Calculation of actual direct labor rate per hour

Business report:

Variance analysis is a process over the variation of real figures and the arranged or

estimated conduct in the budgeting planning process and in management costing. Variance

analysis process is basically done to investigate the genuine contrast among the estimated and

real conduct which shows about the total variation among the estimated and real conduct.

This process assists a business to deal with the different part of the organization to

lessen the cost and time utilization of the organization. This investigation is useful for the

organization to break down the lose purposes of the organization. Variance analysis is mainly

conducted by the companies for the following points:

1. Relationship:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Cost Accounting

11

The analysis on the actual and estimated figures sets a good relationship between

various factors of an organization so that all the operations could be done perfectly as well as

the cost management could also be done. Through this study, it turns out to be simple for the

organization to deal with the related variables of the organization (Rasiah, 2011)

2. Forecasting:

The analysis think about causes the organization to anticipate the future changes into

the outer market and inside in the organization. Through this investigation, it turns out to be

simple for the organization to break down the progressions which could occur into the

execution of the organization.

3. Performance:

The study of variance analysis explains that the process of production and other

management of the company could be considered through the variance analysis study.

Through this examination, it turns out to be simple for the organization to break down the

execution of the organization based on different angles (Weygandt, Kimmel and Kieso,

2015).

4. Maintain the cost:

Variance analysis thinks about encourages the organization to evaluate and keep up the

cost and income of the organization. Through this investigation, it turns out to be simple for

the organization to break down the progressions which has been occurred into the activities of

the organization and accordingly it turns out to be simple for the organization.

5. Competitive pros of the company:

The analysis think about encourages the organization to anticipate the future changes

into the outside market and inside in the organization. Through this examination, it turns out

to be simple for the organization to maintain the position and competitive level (Garrison et

al, 2010).

11

The analysis on the actual and estimated figures sets a good relationship between

various factors of an organization so that all the operations could be done perfectly as well as

the cost management could also be done. Through this study, it turns out to be simple for the

organization to deal with the related variables of the organization (Rasiah, 2011)

2. Forecasting:

The analysis think about causes the organization to anticipate the future changes into

the outer market and inside in the organization. Through this investigation, it turns out to be

simple for the organization to break down the progressions which could occur into the

execution of the organization.

3. Performance:

The study of variance analysis explains that the process of production and other

management of the company could be considered through the variance analysis study.

Through this examination, it turns out to be simple for the organization to break down the

execution of the organization based on different angles (Weygandt, Kimmel and Kieso,

2015).

4. Maintain the cost:

Variance analysis thinks about encourages the organization to evaluate and keep up the

cost and income of the organization. Through this investigation, it turns out to be simple for

the organization to break down the progressions which has been occurred into the activities of

the organization and accordingly it turns out to be simple for the organization.

5. Competitive pros of the company:

The analysis think about encourages the organization to anticipate the future changes

into the outside market and inside in the organization. Through this examination, it turns out

to be simple for the organization to maintain the position and competitive level (Garrison et

al, 2010).

Cost Accounting

12

Further, it has been analyzed that different classes of difference examination are

accessible for the organization to settle on a superior choice and utilize the fluctuation

investigation in a legitimate way. Overhead difference examination is additionally one of the

parts of the fluctuation investigation which encourages the organization to make a control

over all the indirect costs of the organization.

The above are the few formulas of variances of overheads. This causes the organization

to oversee over the whole circuitous costs, for example, aberrant material, backhanded work

and other roundabout costs these formals and he overhead cost variance analysis assist and

organization to measure the total difference and their favourability in the organization. In this

manner it has been discovered that investigation of variance analysis is critical for an

organization to diminish the level of costs.

Budgeting:

Normal Solution:

Cost of goods sold

Mar June Sept Total

Total Sales 1,37,500 1,09,346 1,19,456 3,66,302

Cost of goods sold (Sales

*60%) 82,500.0 65,607.6 71,673.6 2,19,781

Purchase Budget

Mar June Sept Total

Total Cost of goods sold 82,500 65,608 71,674 2,19,781

12

Further, it has been analyzed that different classes of difference examination are

accessible for the organization to settle on a superior choice and utilize the fluctuation

investigation in a legitimate way. Overhead difference examination is additionally one of the

parts of the fluctuation investigation which encourages the organization to make a control

over all the indirect costs of the organization.

The above are the few formulas of variances of overheads. This causes the organization

to oversee over the whole circuitous costs, for example, aberrant material, backhanded work

and other roundabout costs these formals and he overhead cost variance analysis assist and

organization to measure the total difference and their favourability in the organization. In this

manner it has been discovered that investigation of variance analysis is critical for an

organization to diminish the level of costs.

Budgeting:

Normal Solution:

Cost of goods sold

Mar June Sept Total

Total Sales 1,37,500 1,09,346 1,19,456 3,66,302

Cost of goods sold (Sales

*60%) 82,500.0 65,607.6 71,673.6 2,19,781

Purchase Budget

Mar June Sept Total

Total Cost of goods sold 82,500 65,608 71,674 2,19,781

Cost Accounting

13

Less: Opening inventory

-

47,890

-

54,682

-

56,502

-

1,59,074

Ass: closing inventory

(35000+ 30% of next month

sales) 54,682 56,502 56,600 1,67,784

Total Purchase amount 89,292 67,427 71,772 2,28,491

Inventory Budget

Mar June Sept Total

Opening inventory 47,890 54,682 56,502 1,59,074

Add: Purchase 89,292 67,427 71,772 2,28,491

Less: Cost of goods sold

-

82,500.0

-

65,607.6

-

71,673.6

-

2,19,781.2

Closing inventory 54,682 56,502 56,600 1,67,784

Formula solution:

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

C D E F G

Mar June Sept Total

Total Sales =D7 =E7 =F7 =SUM(D16:F16)

Cost of goods sold (Sales *60%)=D16*0.6 =E16*0.6 =F16*0.6 =SUM(D17:F17)

Mar June Sept Total

Total Cost of goods sold =D17 =E17 =F17 =SUM(D23:F23)

Less: Opening inventory -47890 =-D25 =-E25 =SUM(D24:F24)

Ass: closing inventory (35000+ 30% of next month sales)=35000+(30%*E23) =35000+(30%*F23) =35000+(30%*(60%*120000))=SUM(D25:F25)

Total Purchase amount =SUM(D23:D25) =SUM(E23:E25) =SUM(F23:F25) =SUM(G23:G25)

Mar June Sept Total

Opening inventory =-D24 =-E24 =-F24 =-G24

Add: Purchase =D27 =E27 =F27 =G27

Less: Cost of goods sold =-D17 =-E17 =-F17 =-G17

Closing inventory =SUM(D33:D35) =SUM(E33:E35) =SUM(F33:F35) =SUM(G33:G35)

Purchase Budget

Cost of goods sold

Inventory Budget

13

Less: Opening inventory

-

47,890

-

54,682

-

56,502

-

1,59,074

Ass: closing inventory

(35000+ 30% of next month

sales) 54,682 56,502 56,600 1,67,784

Total Purchase amount 89,292 67,427 71,772 2,28,491

Inventory Budget

Mar June Sept Total

Opening inventory 47,890 54,682 56,502 1,59,074

Add: Purchase 89,292 67,427 71,772 2,28,491

Less: Cost of goods sold

-

82,500.0

-

65,607.6

-

71,673.6

-

2,19,781.2

Closing inventory 54,682 56,502 56,600 1,67,784

Formula solution:

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

C D E F G

Mar June Sept Total

Total Sales =D7 =E7 =F7 =SUM(D16:F16)

Cost of goods sold (Sales *60%)=D16*0.6 =E16*0.6 =F16*0.6 =SUM(D17:F17)

Mar June Sept Total

Total Cost of goods sold =D17 =E17 =F17 =SUM(D23:F23)

Less: Opening inventory -47890 =-D25 =-E25 =SUM(D24:F24)

Ass: closing inventory (35000+ 30% of next month sales)=35000+(30%*E23) =35000+(30%*F23) =35000+(30%*(60%*120000))=SUM(D25:F25)

Total Purchase amount =SUM(D23:D25) =SUM(E23:E25) =SUM(F23:F25) =SUM(G23:G25)

Mar June Sept Total

Opening inventory =-D24 =-E24 =-F24 =-G24

Add: Purchase =D27 =E27 =F27 =G27

Less: Cost of goods sold =-D17 =-E17 =-F17 =-G17

Closing inventory =SUM(D33:D35) =SUM(E33:E35) =SUM(F33:F35) =SUM(G33:G35)

Purchase Budget

Cost of goods sold

Inventory Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost Accounting

14

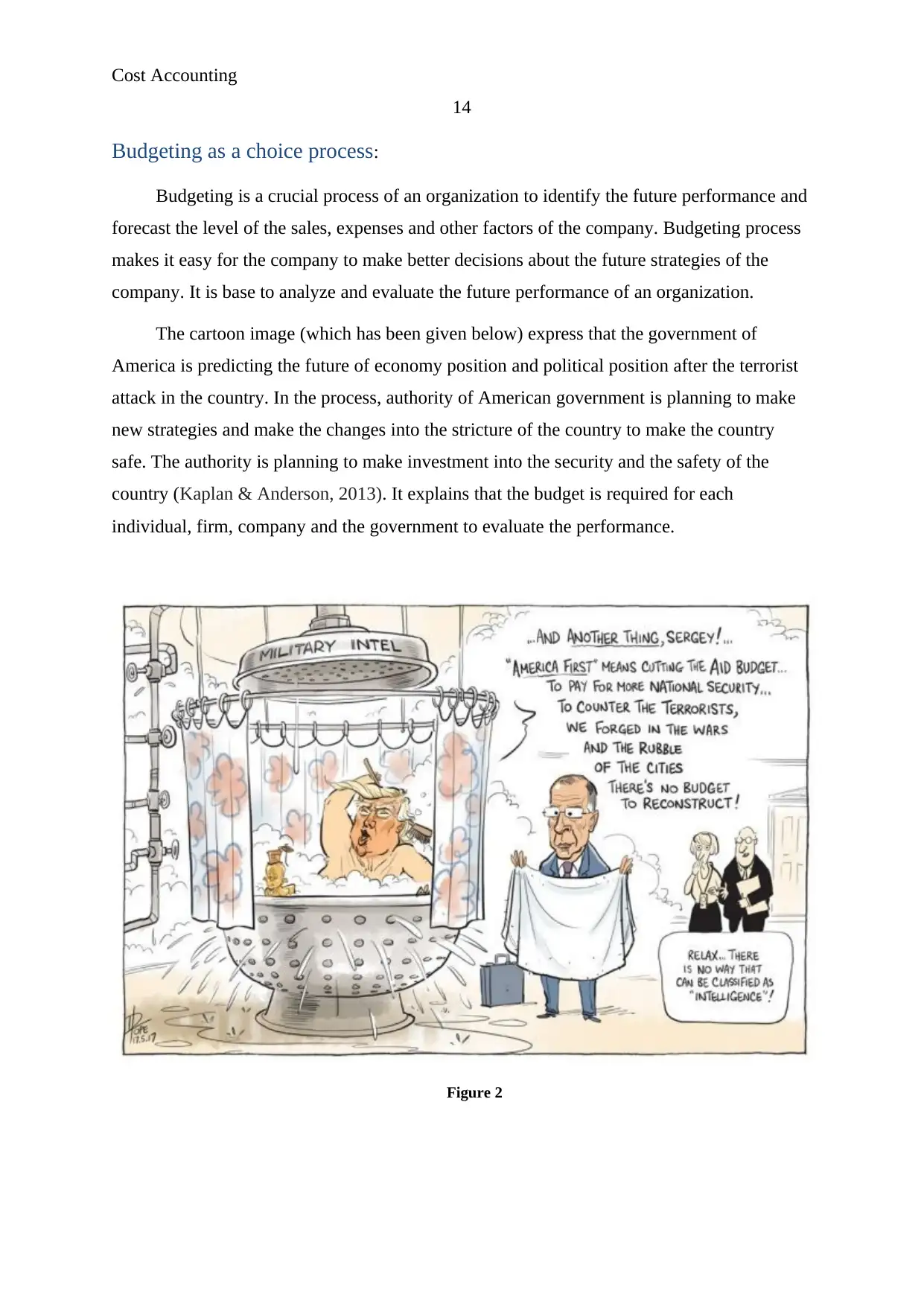

Budgeting as a choice process:

Budgeting is a crucial process of an organization to identify the future performance and

forecast the level of the sales, expenses and other factors of the company. Budgeting process

makes it easy for the company to make better decisions about the future strategies of the

company. It is base to analyze and evaluate the future performance of an organization.

The cartoon image (which has been given below) express that the government of

America is predicting the future of economy position and political position after the terrorist

attack in the country. In the process, authority of American government is planning to make

new strategies and make the changes into the stricture of the country to make the country

safe. The authority is planning to make investment into the security and the safety of the

country (Kaplan & Anderson, 2013). It explains that the budget is required for each

individual, firm, company and the government to evaluate the performance.

Figure 2

14

Budgeting as a choice process:

Budgeting is a crucial process of an organization to identify the future performance and

forecast the level of the sales, expenses and other factors of the company. Budgeting process

makes it easy for the company to make better decisions about the future strategies of the

company. It is base to analyze and evaluate the future performance of an organization.

The cartoon image (which has been given below) express that the government of

America is predicting the future of economy position and political position after the terrorist

attack in the country. In the process, authority of American government is planning to make

new strategies and make the changes into the stricture of the country to make the country

safe. The authority is planning to make investment into the security and the safety of the

country (Kaplan & Anderson, 2013). It explains that the budget is required for each

individual, firm, company and the government to evaluate the performance.

Figure 2

Cost Accounting

15

Reference:

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Kaplan, R., & Anderson, S. R. (2013). Time-driven activity-based costing: a simpler and

more powerful path to higher profits. Harvard business press.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

15

Reference:

Garrison, R. H., Noreen, E. W., Brewer, P. C., & McGowan, A. (2010). Managerial

accounting. Issues in Accounting Education, 25(4), 792-793.

Kaplan, R., & Anderson, S. R. (2013). Time-driven activity-based costing: a simpler and

more powerful path to higher profits. Harvard business press.

Rasiah, D. (2011). Why Activity Based Costing (ABC) is still tagging behind the traditional

costing in Malaysia?. Journal of Applied Finance and Banking, 1(1), 83.

Weygandt, J. J., Kimmel, P. D., & Kieso, D. E. (2015). Financial & Managerial Accounting.

John Wiley & Sons.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.