Project Evaluation Report for Greenacre Hospice: Finance for Managers

VerifiedAdded on 2020/01/06

|13

|1937

|463

Report

AI Summary

This report evaluates potential projects for Greenacre Hospice, focusing on financial analysis and non-financial factors. The analysis includes three proposals: running a cafe with volunteers, leasing the cafe to external vendors, and modernizing the cafe for hospital management. The report emphasizes the importance of Net Present Value (NPV) in project selection, highlighting the third option as the most viable due to its higher NPV. It also stresses the significance of considering various financial parameters, such as growth rates, assumptions, and interest rates, and the impact of these factors on project profitability. The report further discusses the importance of different financial areas, including the cost of capital and the balance between financing sources. Non-financial factors, such as employee availability and allocation, are also considered. The report concludes with recommendations on evaluating projects, including determining NPV, analyzing finance costs, and considering the impact of employee allocation on catering operations. The report uses sensitivity analysis with varying interest rates to assess the robustness of the project's financial viability.

FINANCE FOR MANAGERS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

(1) Preferred option for the hospital and parameters for evaluation.....................................3

(2) Importance of different financial areas.............................................................................4

(3) Evaluation of option and other non-financial factors that need to be considered while

making decisions....................................................................................................................5

(4) Recommendations of the ways in which organization can evaluate a project .................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

INTRODUCTION...........................................................................................................................3

(1) Preferred option for the hospital and parameters for evaluation.....................................3

(2) Importance of different financial areas.............................................................................4

(3) Evaluation of option and other non-financial factors that need to be considered while

making decisions....................................................................................................................5

(4) Recommendations of the ways in which organization can evaluate a project .................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

APPENDIX......................................................................................................................................8

To

The Top managers of Greenacre Hospice

Date: 17-08-2016

Subject: Evaluate of projects

INTRODUCTION

Project evaluation is a difficult task and for selecting the most appropriate one, lots of

things are needed to be considered. In this report, results produced by excel sheet are evaluated.

Apart from that, non-financial factors are identified that may affect the profitability of project.

At the end of report, conclusion is prepared on the basis of entire work.

(1) Preferred option for the hospital and parameters for evaluation

Proposals that are put forth by management accountant are given below.

Proposal 1- Cafe will be run continuously be volunteers

Proposal 2- Giving cafe on lease either to Starbucks or Greasy Joe's

Proposal 3- Modernizing cafe which will be run by hospital department

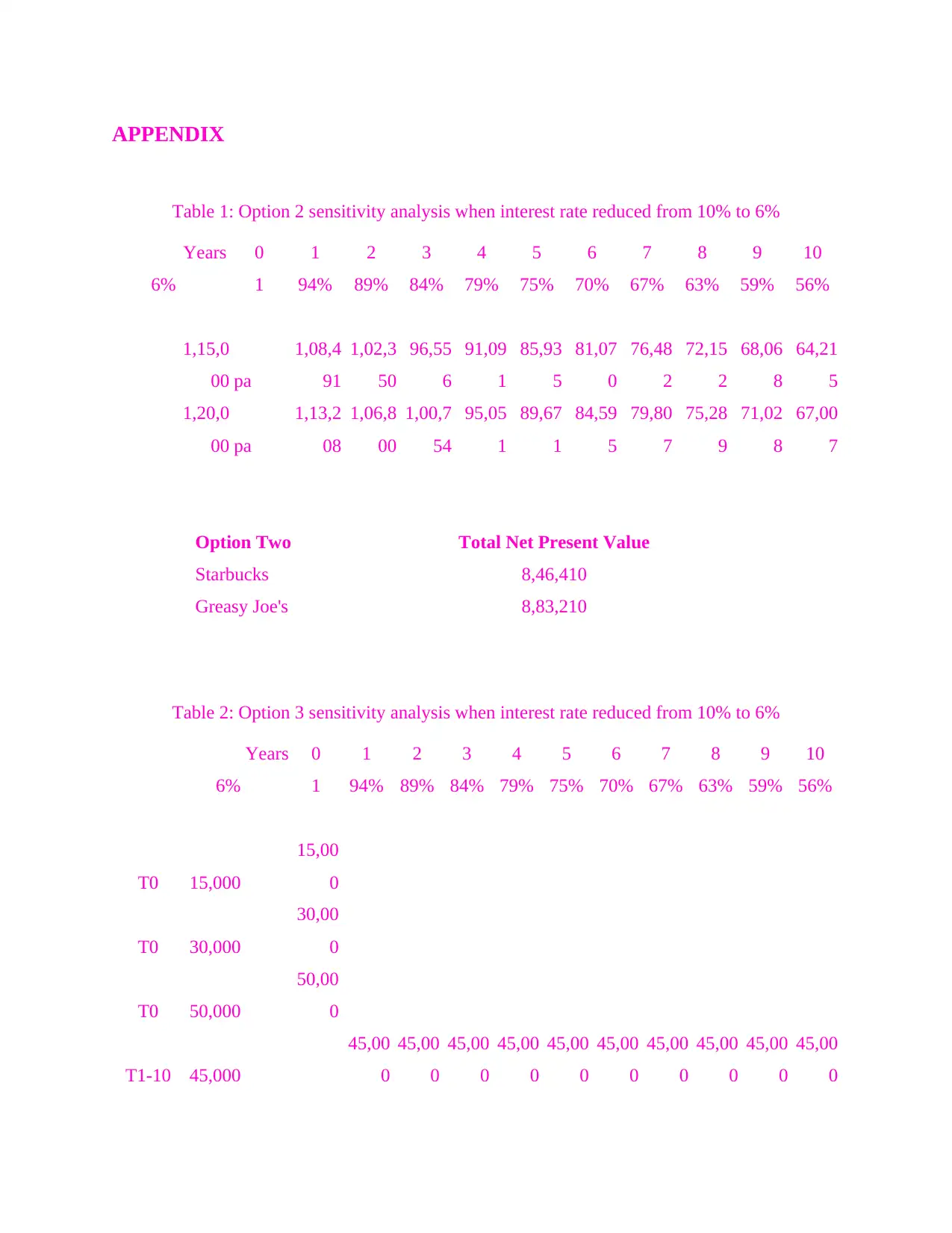

On analysis of all three options that are available, third alternative seems to be viable for

the hospital. This is because; net present value of third alternative is higher than the second

option. From the spreadsheet provided by management accountant, it can be observed that net

present value of second alternative is 7, 06,625 and same of other project that comes in these

options is 7,37,348. Net present value of third option under which cafe will be modernized is 8,

08,251. On the basis of higher NPV, third option is assumed to be the preferred alternative from

outside (Net present value, 2013). There are number of parameters that must be considered for

the evaluation of project. Some of them are given as below:

For the estimation of cash flows, growth rate is assumed and used for the calculation. In

meeting, it is important to make sure that annual growth rate that is taken for projection

of cash flows is reliable. It is practically possible to earn profit at the rate that is selected

for computing future cash flows.

There are many assumptions that are made by the management accountant for making

projections (Bamber, Jiang and Wang, 2010). Detailed analysis of these assumptions

must be another parameter for evaluation. This is because; if things that are assumed

The Top managers of Greenacre Hospice

Date: 17-08-2016

Subject: Evaluate of projects

INTRODUCTION

Project evaluation is a difficult task and for selecting the most appropriate one, lots of

things are needed to be considered. In this report, results produced by excel sheet are evaluated.

Apart from that, non-financial factors are identified that may affect the profitability of project.

At the end of report, conclusion is prepared on the basis of entire work.

(1) Preferred option for the hospital and parameters for evaluation

Proposals that are put forth by management accountant are given below.

Proposal 1- Cafe will be run continuously be volunteers

Proposal 2- Giving cafe on lease either to Starbucks or Greasy Joe's

Proposal 3- Modernizing cafe which will be run by hospital department

On analysis of all three options that are available, third alternative seems to be viable for

the hospital. This is because; net present value of third alternative is higher than the second

option. From the spreadsheet provided by management accountant, it can be observed that net

present value of second alternative is 7, 06,625 and same of other project that comes in these

options is 7,37,348. Net present value of third option under which cafe will be modernized is 8,

08,251. On the basis of higher NPV, third option is assumed to be the preferred alternative from

outside (Net present value, 2013). There are number of parameters that must be considered for

the evaluation of project. Some of them are given as below:

For the estimation of cash flows, growth rate is assumed and used for the calculation. In

meeting, it is important to make sure that annual growth rate that is taken for projection

of cash flows is reliable. It is practically possible to earn profit at the rate that is selected

for computing future cash flows.

There are many assumptions that are made by the management accountant for making

projections (Bamber, Jiang and Wang, 2010). Detailed analysis of these assumptions

must be another parameter for evaluation. This is because; if things that are assumed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will be wrong then non-viable project can be selected for the hospital.

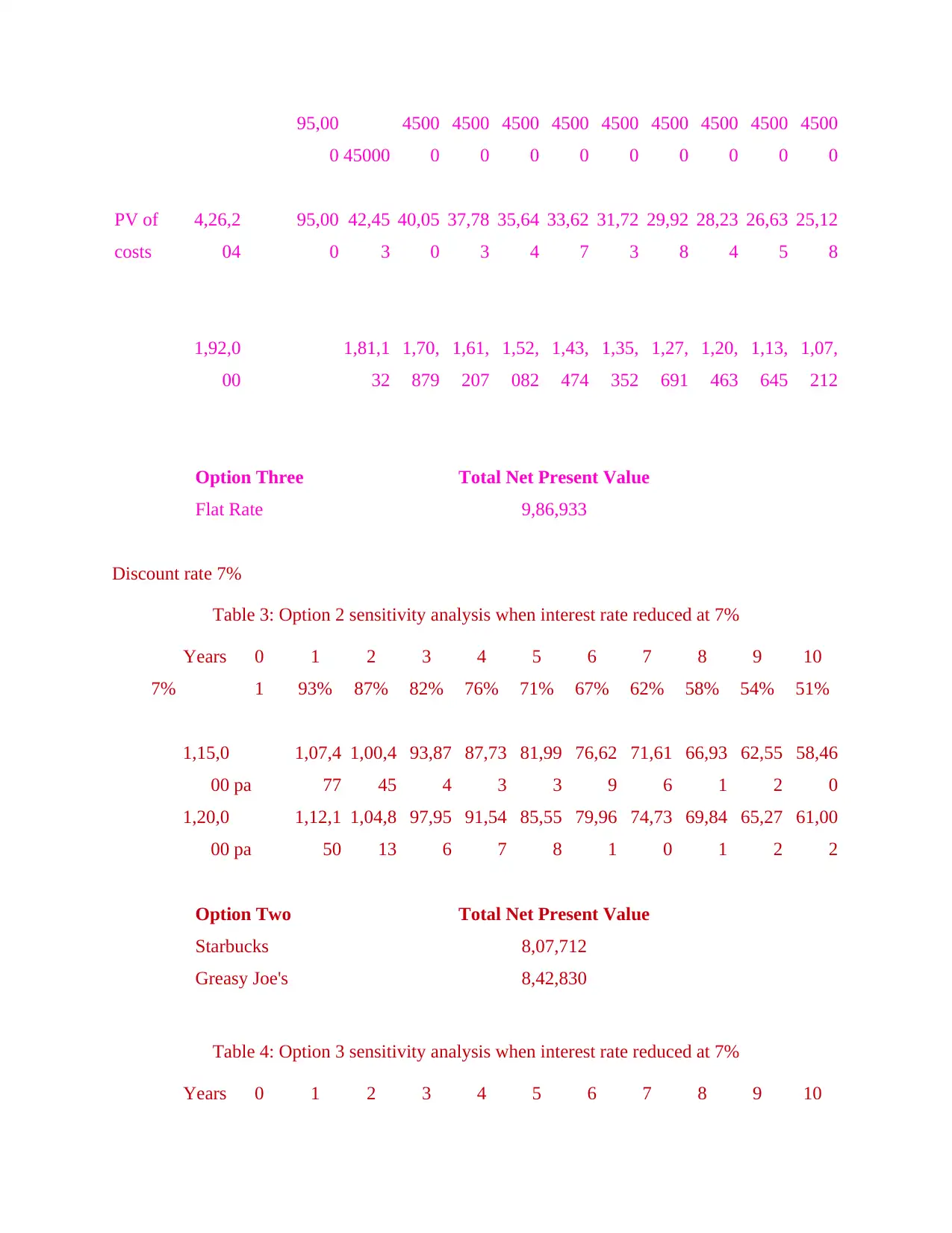

Interest rate that is taken in to computation that is challenged from outside. It is also one

of the most important parameter of project evaluation. In projections interest rate is 10%

which is loan rate for debt taken for 2-3 years. Here, property is given on lease for 10

years. For such duration loans are available at 6%. Hence, under sensitivity analysis

from 6-10% interest rate is considered and present values cash flows are again computed

at different interest rates. Due reduction in interest rates profitability of both options also

increases.

(2) Importance of different financial areas

There are different financial areas that must be kept in mind while deciding whether

specific proposal must be selected and if so, then on what basis it should be run have to be

determined. The first financial area that needs to be considered is cost of capital that hospital

needs to pay in case if it takes debt from bank. Some objectives and limitations in this regard

are given as below:

Objectives

Main objective while taking loan must raise debt at minimum interest rate so that cost of

finance can be kept low to maximum possible level.

Limitations

If loan will be taken then it may badly affect the hospital’s financial condition. In case if

hospital will face any financial crunch due to low profitability or sudden plunge in operating

cost then finance cost may further bring down its profit (Kolk and Pinkse, 2010). Hence, in the

future, condition may become worse. This is evidenced from current financial condition of

Tesco.

Hospital needs to evaluate its sources of finance and to meet the financial requirement, it

needs to prepare a balance between them so that cost of finance can be minimized as much as

possible. In order to finance entire capital investment, some amount that is received through

donations and banks can be used in specific proportion. This will certainly help the firm in

controlling its cost. Objectives and limitations are given as below:

Objectives

To finance the investment amount in 50:50 ratio by using bank loan and amount

Interest rate that is taken in to computation that is challenged from outside. It is also one

of the most important parameter of project evaluation. In projections interest rate is 10%

which is loan rate for debt taken for 2-3 years. Here, property is given on lease for 10

years. For such duration loans are available at 6%. Hence, under sensitivity analysis

from 6-10% interest rate is considered and present values cash flows are again computed

at different interest rates. Due reduction in interest rates profitability of both options also

increases.

(2) Importance of different financial areas

There are different financial areas that must be kept in mind while deciding whether

specific proposal must be selected and if so, then on what basis it should be run have to be

determined. The first financial area that needs to be considered is cost of capital that hospital

needs to pay in case if it takes debt from bank. Some objectives and limitations in this regard

are given as below:

Objectives

Main objective while taking loan must raise debt at minimum interest rate so that cost of

finance can be kept low to maximum possible level.

Limitations

If loan will be taken then it may badly affect the hospital’s financial condition. In case if

hospital will face any financial crunch due to low profitability or sudden plunge in operating

cost then finance cost may further bring down its profit (Kolk and Pinkse, 2010). Hence, in the

future, condition may become worse. This is evidenced from current financial condition of

Tesco.

Hospital needs to evaluate its sources of finance and to meet the financial requirement, it

needs to prepare a balance between them so that cost of finance can be minimized as much as

possible. In order to finance entire capital investment, some amount that is received through

donations and banks can be used in specific proportion. This will certainly help the firm in

controlling its cost. Objectives and limitations are given as below:

Objectives

To finance the investment amount in 50:50 ratio by using bank loan and amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

received from other authorities and To minimize finance cost to 1-2% of total expected revenue (Irwin and Scott, 2010)

Limitations

Amount received from other authorities will not be utilized appropriately then they may

abstain from giving a financial support to the hospital. Further, image of hospital can tarnish

among the stakeholders.

(3) Evaluation of option and other non-financial factors that need to be considered while

making decisions

As mentioned earlier, on the basis of available options, third alternative is modernization

of cafe which will be run by the hospital’s catering department seems to be viable. On the basis

of higher NPV, this alternative is assumed to be profitable for the hospital. Some non-financial

factors that need to be considered are given as below:

First of all, it must be identified that whether in accordance with the catering work, there

are sufficient number of employees in hospital or not. If there are abundant number of

employees then it is necessary to identify the person who will work in cafe (Simons,

2013). If there is less number of employees in the catering department then it is

important to make projections salary that will be given to them for working in cafe. New

employees will be hired then again financial projections need to be made.

The second non-financial factor that which needs to be considered is that if employee

for cafe will be picked up from the current workforce of catering department, then how

much allocation of same will be done for cafe so that operations of catering department

would not get affected and will be performed smoothly.

(4) Recommendations of the ways in which organization can evaluate a project

Some recommendations on the ways in which hospital can evaluate a project is given as

below:

Number of employees that are currently in catering department must be identified and it

must find out that if some of them are employed in cafe then whether such kind of

decision will hamper the operations of catering department or not.

Managers must determine the net present value that project must have. By comparing

the standard NPV value with same project, more wise decision can be taken by the

Limitations

Amount received from other authorities will not be utilized appropriately then they may

abstain from giving a financial support to the hospital. Further, image of hospital can tarnish

among the stakeholders.

(3) Evaluation of option and other non-financial factors that need to be considered while

making decisions

As mentioned earlier, on the basis of available options, third alternative is modernization

of cafe which will be run by the hospital’s catering department seems to be viable. On the basis

of higher NPV, this alternative is assumed to be profitable for the hospital. Some non-financial

factors that need to be considered are given as below:

First of all, it must be identified that whether in accordance with the catering work, there

are sufficient number of employees in hospital or not. If there are abundant number of

employees then it is necessary to identify the person who will work in cafe (Simons,

2013). If there is less number of employees in the catering department then it is

important to make projections salary that will be given to them for working in cafe. New

employees will be hired then again financial projections need to be made.

The second non-financial factor that which needs to be considered is that if employee

for cafe will be picked up from the current workforce of catering department, then how

much allocation of same will be done for cafe so that operations of catering department

would not get affected and will be performed smoothly.

(4) Recommendations of the ways in which organization can evaluate a project

Some recommendations on the ways in which hospital can evaluate a project is given as

below:

Number of employees that are currently in catering department must be identified and it

must find out that if some of them are employed in cafe then whether such kind of

decision will hamper the operations of catering department or not.

Managers must determine the net present value that project must have. By comparing

the standard NPV value with same project, more wise decision can be taken by the

management.

Finance cost as the percentage of revenue must be determined to maximize profits and

to ensure that reasonable amount of interest is paid to the bank (Shiller, 2013). Finance

cost as a percentage of revenue may breach the determined level. If this will happen then

to some extent, project’s profitability will be declined by extra percentage that is

covered by the finance cost of revenue above breached level.

CONCLUSION

On the basis of above discussion, it is concluded that project must be selected on the

basis of results produced by project evaluation methods. Along with that, report shows that

there are number of non-financial factors that need to be considered while evaluating a project

to make a wise decision. These factors may affect the profitability of project.

Finance cost as the percentage of revenue must be determined to maximize profits and

to ensure that reasonable amount of interest is paid to the bank (Shiller, 2013). Finance

cost as a percentage of revenue may breach the determined level. If this will happen then

to some extent, project’s profitability will be declined by extra percentage that is

covered by the finance cost of revenue above breached level.

CONCLUSION

On the basis of above discussion, it is concluded that project must be selected on the

basis of results produced by project evaluation methods. Along with that, report shows that

there are number of non-financial factors that need to be considered while evaluating a project

to make a wise decision. These factors may affect the profitability of project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bamber, L. S., Jiang, J. and Wang, I. Y., 2010. What's my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review. 85(4). pp.1131-1162.

Irwin, D. and Scott, J. M., 2010. Barriers faced by SMEs in raising bank finance. International

journal of entrepreneurial behavior & research. 16(3). pp.245-259.

Kolk, A. and Pinkse, J., 2010. The integration of corporate governance in corporate social

responsibility disclosures. Corporate Social Responsibility and Environmental

Management. 17(1). pp.15-26.

Shiller, R. J., 2013. Finance and the good society. Princeton University Press.

Simons, R., 2013. Levers of organization design: How managers use accountability systems for

greater performance and commitment. Harvard Business Press.

Online

Net present value. 2013. [Online]. Available through: <http://www.mathsisfun.com/money/net-

present-value.html>. [Accessed on 16th August 2016].

Books and Journals

Bamber, L. S., Jiang, J. and Wang, I. Y., 2010. What's my style? The influence of top managers

on voluntary corporate financial disclosure. The accounting review. 85(4). pp.1131-1162.

Irwin, D. and Scott, J. M., 2010. Barriers faced by SMEs in raising bank finance. International

journal of entrepreneurial behavior & research. 16(3). pp.245-259.

Kolk, A. and Pinkse, J., 2010. The integration of corporate governance in corporate social

responsibility disclosures. Corporate Social Responsibility and Environmental

Management. 17(1). pp.15-26.

Shiller, R. J., 2013. Finance and the good society. Princeton University Press.

Simons, R., 2013. Levers of organization design: How managers use accountability systems for

greater performance and commitment. Harvard Business Press.

Online

Net present value. 2013. [Online]. Available through: <http://www.mathsisfun.com/money/net-

present-value.html>. [Accessed on 16th August 2016].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Table 1: Option 2 sensitivity analysis when interest rate reduced from 10% to 6%

Years 0 1 2 3 4 5 6 7 8 9 10

6% 1 94% 89% 84% 79% 75% 70% 67% 63% 59% 56%

1,15,0

00 pa

1,08,4

91

1,02,3

50

96,55

6

91,09

1

85,93

5

81,07

0

76,48

2

72,15

2

68,06

8

64,21

5

1,20,0

00 pa

1,13,2

08

1,06,8

00

1,00,7

54

95,05

1

89,67

1

84,59

5

79,80

7

75,28

9

71,02

8

67,00

7

Option Two Total Net Present Value

Starbucks 8,46,410

Greasy Joe's 8,83,210

Table 2: Option 3 sensitivity analysis when interest rate reduced from 10% to 6%

Years 0 1 2 3 4 5 6 7 8 9 10

6% 1 94% 89% 84% 79% 75% 70% 67% 63% 59% 56%

T0 15,000

15,00

0

T0 30,000

30,00

0

T0 50,000

50,00

0

T1-10 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

Table 1: Option 2 sensitivity analysis when interest rate reduced from 10% to 6%

Years 0 1 2 3 4 5 6 7 8 9 10

6% 1 94% 89% 84% 79% 75% 70% 67% 63% 59% 56%

1,15,0

00 pa

1,08,4

91

1,02,3

50

96,55

6

91,09

1

85,93

5

81,07

0

76,48

2

72,15

2

68,06

8

64,21

5

1,20,0

00 pa

1,13,2

08

1,06,8

00

1,00,7

54

95,05

1

89,67

1

84,59

5

79,80

7

75,28

9

71,02

8

67,00

7

Option Two Total Net Present Value

Starbucks 8,46,410

Greasy Joe's 8,83,210

Table 2: Option 3 sensitivity analysis when interest rate reduced from 10% to 6%

Years 0 1 2 3 4 5 6 7 8 9 10

6% 1 94% 89% 84% 79% 75% 70% 67% 63% 59% 56%

T0 15,000

15,00

0

T0 30,000

30,00

0

T0 50,000

50,00

0

T1-10 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

PV of

costs

4,26,2

04

95,00

0

42,45

3

40,05

0

37,78

3

35,64

4

33,62

7

31,72

3

29,92

8

28,23

4

26,63

5

25,12

8

1,92,0

00

1,81,1

32

1,70,

879

1,61,

207

1,52,

082

1,43,

474

1,35,

352

1,27,

691

1,20,

463

1,13,

645

1,07,

212

Option Three Total Net Present Value

Flat Rate 9,86,933

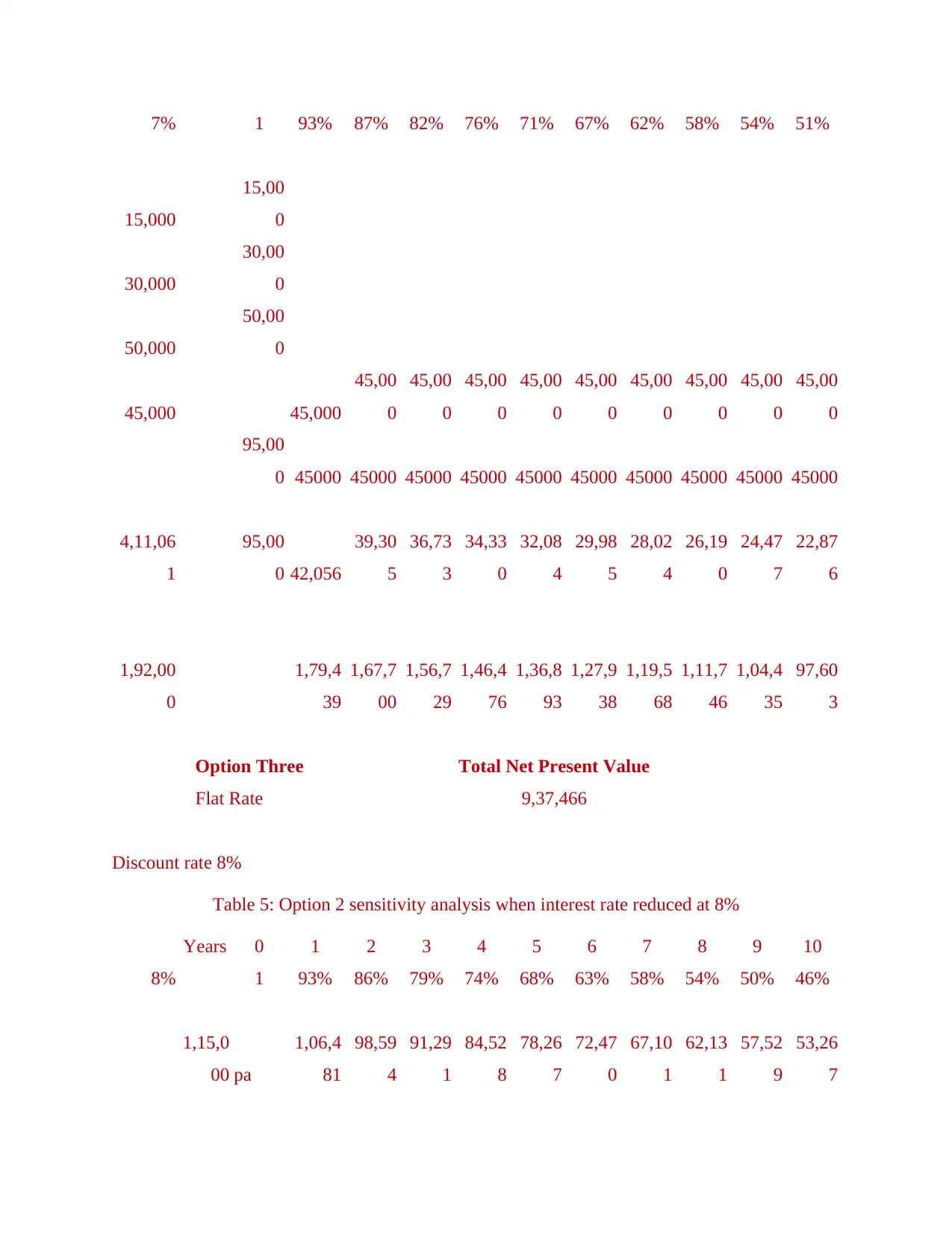

Discount rate 7%

Table 3: Option 2 sensitivity analysis when interest rate reduced at 7%

Years 0 1 2 3 4 5 6 7 8 9 10

7% 1 93% 87% 82% 76% 71% 67% 62% 58% 54% 51%

1,15,0

00 pa

1,07,4

77

1,00,4

45

93,87

4

87,73

3

81,99

3

76,62

9

71,61

6

66,93

1

62,55

2

58,46

0

1,20,0

00 pa

1,12,1

50

1,04,8

13

97,95

6

91,54

7

85,55

8

79,96

1

74,73

0

69,84

1

65,27

2

61,00

2

Option Two Total Net Present Value

Starbucks 8,07,712

Greasy Joe's 8,42,830

Table 4: Option 3 sensitivity analysis when interest rate reduced at 7%

Years 0 1 2 3 4 5 6 7 8 9 10

0 45000

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

4500

0

PV of

costs

4,26,2

04

95,00

0

42,45

3

40,05

0

37,78

3

35,64

4

33,62

7

31,72

3

29,92

8

28,23

4

26,63

5

25,12

8

1,92,0

00

1,81,1

32

1,70,

879

1,61,

207

1,52,

082

1,43,

474

1,35,

352

1,27,

691

1,20,

463

1,13,

645

1,07,

212

Option Three Total Net Present Value

Flat Rate 9,86,933

Discount rate 7%

Table 3: Option 2 sensitivity analysis when interest rate reduced at 7%

Years 0 1 2 3 4 5 6 7 8 9 10

7% 1 93% 87% 82% 76% 71% 67% 62% 58% 54% 51%

1,15,0

00 pa

1,07,4

77

1,00,4

45

93,87

4

87,73

3

81,99

3

76,62

9

71,61

6

66,93

1

62,55

2

58,46

0

1,20,0

00 pa

1,12,1

50

1,04,8

13

97,95

6

91,54

7

85,55

8

79,96

1

74,73

0

69,84

1

65,27

2

61,00

2

Option Two Total Net Present Value

Starbucks 8,07,712

Greasy Joe's 8,42,830

Table 4: Option 3 sensitivity analysis when interest rate reduced at 7%

Years 0 1 2 3 4 5 6 7 8 9 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7% 1 93% 87% 82% 76% 71% 67% 62% 58% 54% 51%

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

4,11,06

1

95,00

0 42,056

39,30

5

36,73

3

34,33

0

32,08

4

29,98

5

28,02

4

26,19

0

24,47

7

22,87

6

1,92,00

0

1,79,4

39

1,67,7

00

1,56,7

29

1,46,4

76

1,36,8

93

1,27,9

38

1,19,5

68

1,11,7

46

1,04,4

35

97,60

3

Option Three Total Net Present Value

Flat Rate 9,37,466

Discount rate 8%

Table 5: Option 2 sensitivity analysis when interest rate reduced at 8%

Years 0 1 2 3 4 5 6 7 8 9 10

8% 1 93% 86% 79% 74% 68% 63% 58% 54% 50% 46%

1,15,0

00 pa

1,06,4

81

98,59

4

91,29

1

84,52

8

78,26

7

72,47

0

67,10

1

62,13

1

57,52

9

53,26

7

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

4,11,06

1

95,00

0 42,056

39,30

5

36,73

3

34,33

0

32,08

4

29,98

5

28,02

4

26,19

0

24,47

7

22,87

6

1,92,00

0

1,79,4

39

1,67,7

00

1,56,7

29

1,46,4

76

1,36,8

93

1,27,9

38

1,19,5

68

1,11,7

46

1,04,4

35

97,60

3

Option Three Total Net Present Value

Flat Rate 9,37,466

Discount rate 8%

Table 5: Option 2 sensitivity analysis when interest rate reduced at 8%

Years 0 1 2 3 4 5 6 7 8 9 10

8% 1 93% 86% 79% 74% 68% 63% 58% 54% 50% 46%

1,15,0

00 pa

1,06,4

81

98,59

4

91,29

1

84,52

8

78,26

7

72,47

0

67,10

1

62,13

1

57,52

9

53,26

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1,20,0

00 pa

1,11,1

11

1,02,8

81

95,26

0

88,20

4

81,67

0

75,62

0

70,01

9

64,83

2

60,03

0

55,58

3

Option Two Total Net Present Value

Starbucks 7,71,659

Greasy Joe's 8,05,210

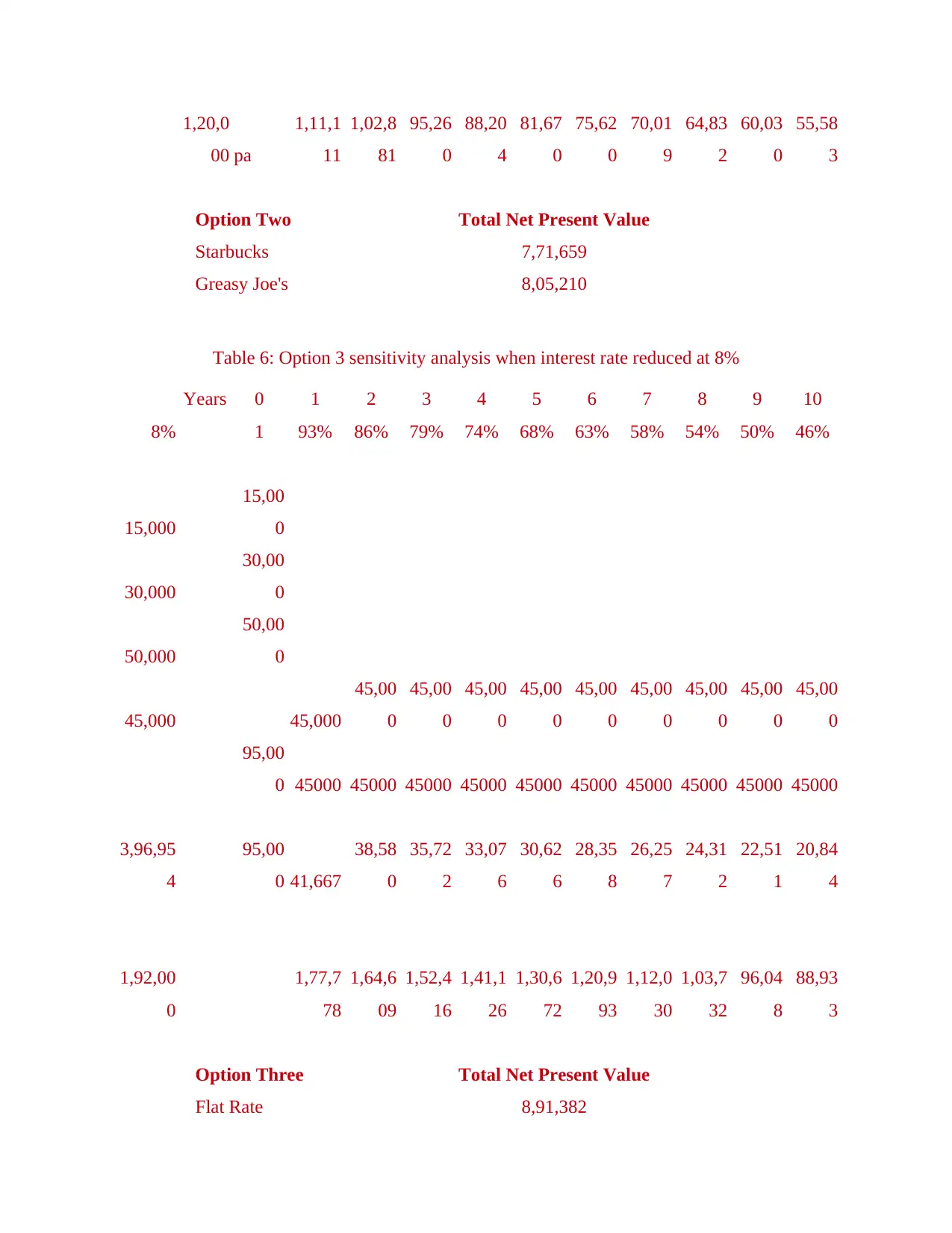

Table 6: Option 3 sensitivity analysis when interest rate reduced at 8%

Years 0 1 2 3 4 5 6 7 8 9 10

8% 1 93% 86% 79% 74% 68% 63% 58% 54% 50% 46%

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

3,96,95

4

95,00

0 41,667

38,58

0

35,72

2

33,07

6

30,62

6

28,35

8

26,25

7

24,31

2

22,51

1

20,84

4

1,92,00

0

1,77,7

78

1,64,6

09

1,52,4

16

1,41,1

26

1,30,6

72

1,20,9

93

1,12,0

30

1,03,7

32

96,04

8

88,93

3

Option Three Total Net Present Value

Flat Rate 8,91,382

00 pa

1,11,1

11

1,02,8

81

95,26

0

88,20

4

81,67

0

75,62

0

70,01

9

64,83

2

60,03

0

55,58

3

Option Two Total Net Present Value

Starbucks 7,71,659

Greasy Joe's 8,05,210

Table 6: Option 3 sensitivity analysis when interest rate reduced at 8%

Years 0 1 2 3 4 5 6 7 8 9 10

8% 1 93% 86% 79% 74% 68% 63% 58% 54% 50% 46%

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

3,96,95

4

95,00

0 41,667

38,58

0

35,72

2

33,07

6

30,62

6

28,35

8

26,25

7

24,31

2

22,51

1

20,84

4

1,92,00

0

1,77,7

78

1,64,6

09

1,52,4

16

1,41,1

26

1,30,6

72

1,20,9

93

1,12,0

30

1,03,7

32

96,04

8

88,93

3

Option Three Total Net Present Value

Flat Rate 8,91,382

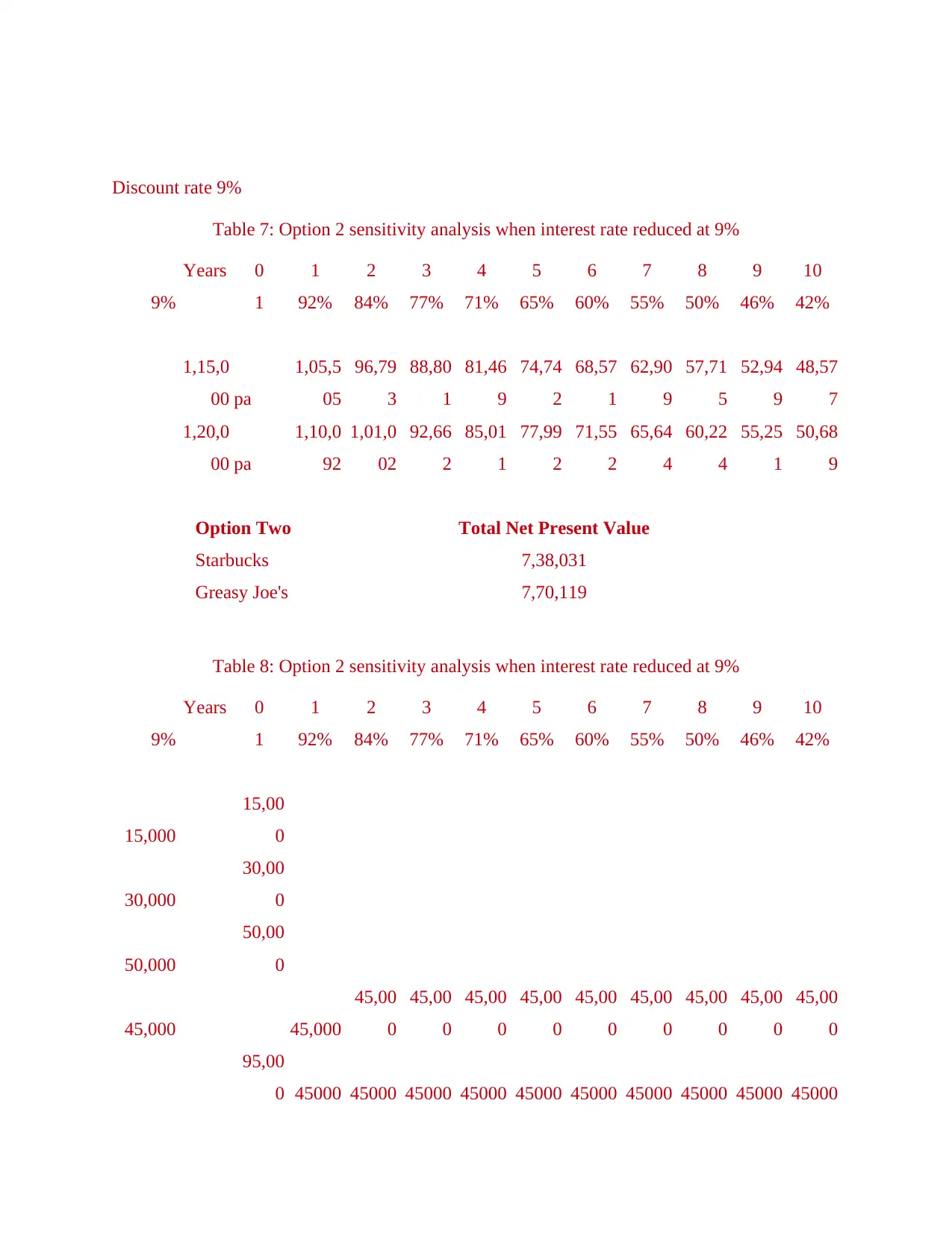

Discount rate 9%

Table 7: Option 2 sensitivity analysis when interest rate reduced at 9%

Years 0 1 2 3 4 5 6 7 8 9 10

9% 1 92% 84% 77% 71% 65% 60% 55% 50% 46% 42%

1,15,0

00 pa

1,05,5

05

96,79

3

88,80

1

81,46

9

74,74

2

68,57

1

62,90

9

57,71

5

52,94

9

48,57

7

1,20,0

00 pa

1,10,0

92

1,01,0

02

92,66

2

85,01

1

77,99

2

71,55

2

65,64

4

60,22

4

55,25

1

50,68

9

Option Two Total Net Present Value

Starbucks 7,38,031

Greasy Joe's 7,70,119

Table 8: Option 2 sensitivity analysis when interest rate reduced at 9%

Years 0 1 2 3 4 5 6 7 8 9 10

9% 1 92% 84% 77% 71% 65% 60% 55% 50% 46% 42%

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

Table 7: Option 2 sensitivity analysis when interest rate reduced at 9%

Years 0 1 2 3 4 5 6 7 8 9 10

9% 1 92% 84% 77% 71% 65% 60% 55% 50% 46% 42%

1,15,0

00 pa

1,05,5

05

96,79

3

88,80

1

81,46

9

74,74

2

68,57

1

62,90

9

57,71

5

52,94

9

48,57

7

1,20,0

00 pa

1,10,0

92

1,01,0

02

92,66

2

85,01

1

77,99

2

71,55

2

65,64

4

60,22

4

55,25

1

50,68

9

Option Two Total Net Present Value

Starbucks 7,38,031

Greasy Joe's 7,70,119

Table 8: Option 2 sensitivity analysis when interest rate reduced at 9%

Years 0 1 2 3 4 5 6 7 8 9 10

9% 1 92% 84% 77% 71% 65% 60% 55% 50% 46% 42%

15,000

15,00

0

30,000

30,00

0

50,000

50,00

0

45,000 45,000

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

95,00

0 45000 45000 45000 45000 45000 45000 45000 45000 45000 45000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3,83,79

5

95,00

0 41,284

37,87

6

34,74

8

31,87

9

29,24

7

26,83

2

24,61

7

22,58

4

20,71

9

19,00

8

1,92,00

0

1,76,1

47

1,61,6

03

1,48,2

59

1,36,0

18

1,24,7

87

1,14,4

83

1,05,0

31

96,35

8

88,40

2

81,10

3

Option Three Total Net Present Value

Flat Rate 8,48,396

Discount rate 10%

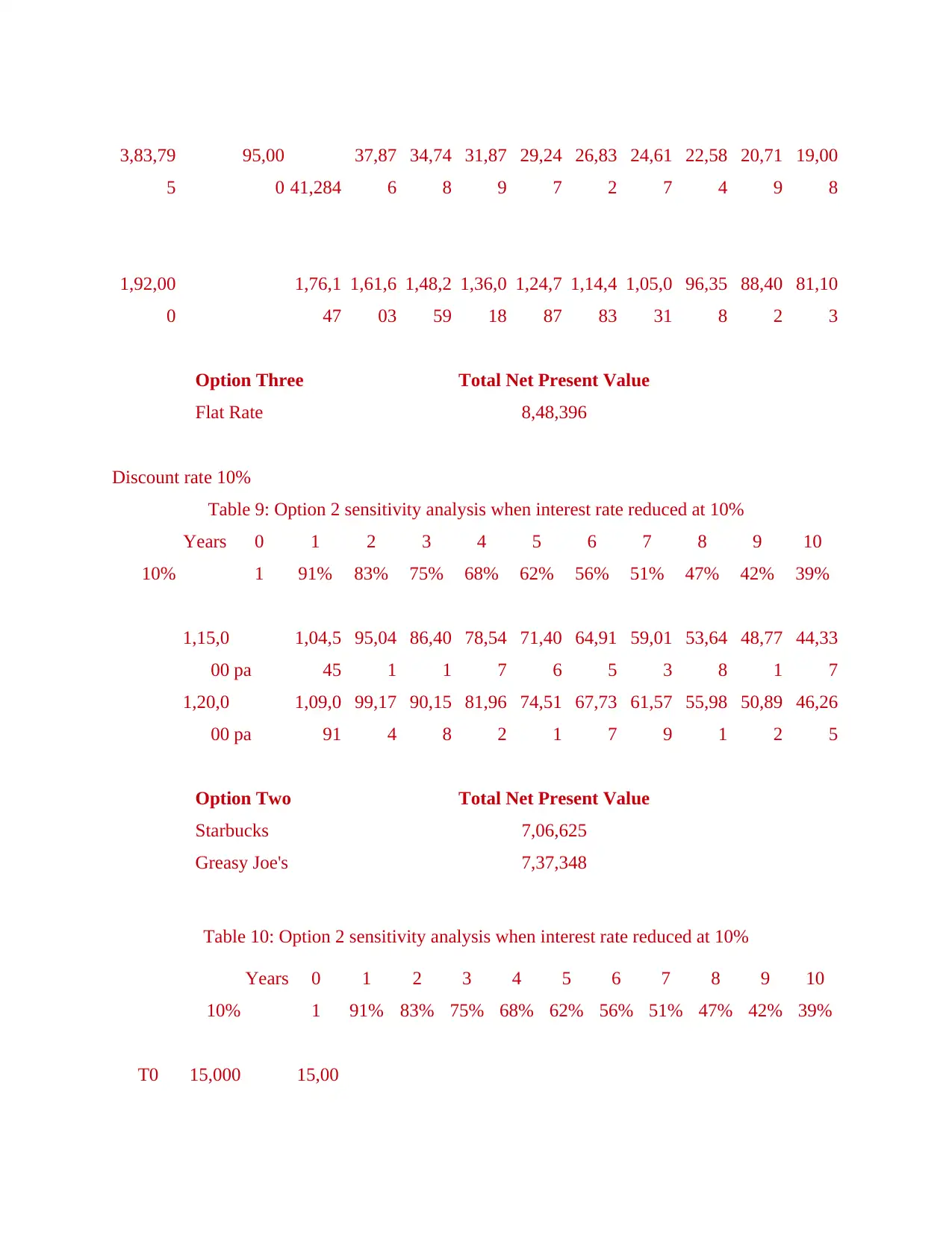

Table 9: Option 2 sensitivity analysis when interest rate reduced at 10%

Years 0 1 2 3 4 5 6 7 8 9 10

10% 1 91% 83% 75% 68% 62% 56% 51% 47% 42% 39%

1,15,0

00 pa

1,04,5

45

95,04

1

86,40

1

78,54

7

71,40

6

64,91

5

59,01

3

53,64

8

48,77

1

44,33

7

1,20,0

00 pa

1,09,0

91

99,17

4

90,15

8

81,96

2

74,51

1

67,73

7

61,57

9

55,98

1

50,89

2

46,26

5

Option Two Total Net Present Value

Starbucks 7,06,625

Greasy Joe's 7,37,348

Table 10: Option 2 sensitivity analysis when interest rate reduced at 10%

Years 0 1 2 3 4 5 6 7 8 9 10

10% 1 91% 83% 75% 68% 62% 56% 51% 47% 42% 39%

T0 15,000 15,00

5

95,00

0 41,284

37,87

6

34,74

8

31,87

9

29,24

7

26,83

2

24,61

7

22,58

4

20,71

9

19,00

8

1,92,00

0

1,76,1

47

1,61,6

03

1,48,2

59

1,36,0

18

1,24,7

87

1,14,4

83

1,05,0

31

96,35

8

88,40

2

81,10

3

Option Three Total Net Present Value

Flat Rate 8,48,396

Discount rate 10%

Table 9: Option 2 sensitivity analysis when interest rate reduced at 10%

Years 0 1 2 3 4 5 6 7 8 9 10

10% 1 91% 83% 75% 68% 62% 56% 51% 47% 42% 39%

1,15,0

00 pa

1,04,5

45

95,04

1

86,40

1

78,54

7

71,40

6

64,91

5

59,01

3

53,64

8

48,77

1

44,33

7

1,20,0

00 pa

1,09,0

91

99,17

4

90,15

8

81,96

2

74,51

1

67,73

7

61,57

9

55,98

1

50,89

2

46,26

5

Option Two Total Net Present Value

Starbucks 7,06,625

Greasy Joe's 7,37,348

Table 10: Option 2 sensitivity analysis when interest rate reduced at 10%

Years 0 1 2 3 4 5 6 7 8 9 10

10% 1 91% 83% 75% 68% 62% 56% 51% 47% 42% 39%

T0 15,000 15,00

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.