Comprehensive Report: Indirect Tax, VAT Regulations and Compliance

VerifiedAdded on 2020/12/24

|14

|4255

|291

Report

AI Summary

This report provides a comprehensive overview of indirect tax, specifically focusing on Value Added Tax (VAT) regulations in the UK. It begins by identifying various sources of VAT information, primarily the HMRC website, and outlines how organizations should interact with the relevant government agency. The report details VAT registration requirements, including thresholds and necessary documentation. It explains the information that must be included on VAT invoices and the requirements and frequency of reporting for different VAT schemes such as annual accounting, cash accounting, flat-rate, and standard schemes. The report further emphasizes the importance of maintaining up-to-date knowledge of changes in codes of practice, regulations, and legislation. It then delves into the practical aspects of VAT, including extracting data from accounting records, classifying inputs and outputs, and calculating VAT due to or from the tax authority. The report concludes by discussing the implications and penalties for non-compliance with VAT regulations, along with the procedures for correcting errors and communicating VAT information to managers and relevant stakeholders.

Indirect tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Identification of sources of information on VAT..................................................................4

1.2 How an organisation should interact with the relevant government agency.........................4

1.3 VAT registration requirements..............................................................................................5

1.4 The information that must be included on business documentation of VAT.......................6

registered businesses....................................................................................................................6

1.5 The requirements and the frequency of reporting for VAT schemes...................................7

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

......................................................................................................................................................8

TASK 2............................................................................................................................................8

2.1 Extraction of relevant data for a specific period from accounting records............................8

2.2 Relevant inputs and outputs using these VAT classifications...............................................9

2.3 VAT due to, or from, the relevant tax authority..................................................................11

2.4 VAT return and any associated payment within the statutory time limits..........................11

TASK 3..........................................................................................................................................12

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations..................................................................................................................................12

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods........................................................................................................................................13

TASK 4..........................................................................................................................................13

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.......................................................................................................13

4.2 Relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems...............................................................................................13

CONCLUSION..............................................................................................................................14

REFRENCESS...............................................................................................................................15

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Identification of sources of information on VAT..................................................................4

1.2 How an organisation should interact with the relevant government agency.........................4

1.3 VAT registration requirements..............................................................................................5

1.4 The information that must be included on business documentation of VAT.......................6

registered businesses....................................................................................................................6

1.5 The requirements and the frequency of reporting for VAT schemes...................................7

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

......................................................................................................................................................8

TASK 2............................................................................................................................................8

2.1 Extraction of relevant data for a specific period from accounting records............................8

2.2 Relevant inputs and outputs using these VAT classifications...............................................9

2.3 VAT due to, or from, the relevant tax authority..................................................................11

2.4 VAT return and any associated payment within the statutory time limits..........................11

TASK 3..........................................................................................................................................12

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations..................................................................................................................................12

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT

periods........................................................................................................................................13

TASK 4..........................................................................................................................................13

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts.......................................................................................................13

4.2 Relevant people of changes in VAT legislation which would have an effect on an

organisation’s recording systems...............................................................................................13

CONCLUSION..............................................................................................................................14

REFRENCESS...............................................................................................................................15

INTRODUCTION

An indirect tax is a tax which is collected by one entity in the supply chain process and

paid to the government of the country, but it is passed to the customer as part of the purchase

price of a product or service. The customer is ultimately pays the tax by spending more for the

goods and service (Emran and Stiglitz, 2005). Value added tax, service tax, goods and service

tax etc. are some of the examples of the indirect taxes. Value added tax (VAT) was introduced in

1973 and it is now third largest source of revenue for the government after income tax and

national insurance. The given project is divided into four tasks. First task involves information

regarding VAT sources, registration requirements etc. Second task includes information

regarding VAT returns, third task involves VAT penalties and adjustments for earlier errors and

the last task contains the details regarding communication of VAT informations. Paper base

sources are also introduced in a wide number of range for help to taxpayers. These published

papers can be requested to sent by contacting at HMRC website.

TASK 1

1.1 Identification of sources of information on VAT

VAT is levied on most of the goods which are provided by registered entity in the UK

and some of the goods and services which are imported from outside the European Union. For

levying the VAT and other legal requirements, it is very important to identify the various sources

of information on VAT. The major sources of information on VAT are HMRC website

www.hmrc.gov.uk, where all the information on VAT is available. At this website advice notes,

magazines, publication and guidance are available. Usually taxpayers find information on this

website but there are a telephone helpline also available for instant advice and guidance.

Taxpayers also can acquire informations by email and write on the website. The Govt. also set up

as distinct website in addition to HMRC which is www.businesslink.gov.uk. (Boadway,

Marchand and Pestieau, 1946). there is a very helpful section for taxpayers on VAT. Mainly it

can be say that Govt. of UK is a major source of information on VAT because most of sources

are provided by Govt. to taxpayers.

An indirect tax is a tax which is collected by one entity in the supply chain process and

paid to the government of the country, but it is passed to the customer as part of the purchase

price of a product or service. The customer is ultimately pays the tax by spending more for the

goods and service (Emran and Stiglitz, 2005). Value added tax, service tax, goods and service

tax etc. are some of the examples of the indirect taxes. Value added tax (VAT) was introduced in

1973 and it is now third largest source of revenue for the government after income tax and

national insurance. The given project is divided into four tasks. First task involves information

regarding VAT sources, registration requirements etc. Second task includes information

regarding VAT returns, third task involves VAT penalties and adjustments for earlier errors and

the last task contains the details regarding communication of VAT informations. Paper base

sources are also introduced in a wide number of range for help to taxpayers. These published

papers can be requested to sent by contacting at HMRC website.

TASK 1

1.1 Identification of sources of information on VAT

VAT is levied on most of the goods which are provided by registered entity in the UK

and some of the goods and services which are imported from outside the European Union. For

levying the VAT and other legal requirements, it is very important to identify the various sources

of information on VAT. The major sources of information on VAT are HMRC website

www.hmrc.gov.uk, where all the information on VAT is available. At this website advice notes,

magazines, publication and guidance are available. Usually taxpayers find information on this

website but there are a telephone helpline also available for instant advice and guidance.

Taxpayers also can acquire informations by email and write on the website. The Govt. also set up

as distinct website in addition to HMRC which is www.businesslink.gov.uk. (Boadway,

Marchand and Pestieau, 1946). there is a very helpful section for taxpayers on VAT. Mainly it

can be say that Govt. of UK is a major source of information on VAT because most of sources

are provided by Govt. to taxpayers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 How an organisation should interact with the relevant government agency

The VAT administration is deal by the HMRC department. Various VAT offices deal

with the VAT matters as specified by relevant department. The central office at Southend

concerns with the general VAT matters. It includes issuing guidelines specific type of supply.

The local officers are appointed to deal with local administration. It provide guideline to

registered business whose principle place of transactions are situated in this respective area. The

regional collectors control whole the process. For checking whether the appropriate rules are

followed by registered persons or not, staff of HMRC will visit timely the registered entities. If

any business person don't agree with the applicable VAT rules then he can ask his local officer in

local authority. It is not compulsory every time to appeal formally (Virmani, 1989.). Where it

settled by an agreement, written statement is issued by normal appeal process. The time limit for

every process is fixed under the department sections.

1.3 VAT registration requirements

A trader may be registered under VAT system may be voluntary or compulsory. A

business must register for VAT with HM Revenue and Customs ( HMRC ) if its VAT taxable

turnover is more than £85,000 per financial year. And the business is require to inform the

HMRC department within 30 days from end of month in which he become liable to VAT

payment. If the department of revenue and custom satisfy that the supply of goods not exceeds

from British pound 81000, registration will not be required under VAT system. And if the

registration is not done at appropriate time then vat is payable from the preceding date from

which he is liable to pay VAT or registration. Organization/person would also need to register

for VAT if receive products that are bought and sold in the UK from the EU worth more than

British pounds 83,000 or expect to go over the dividing line/point where something begins or

changes in a single 30 day period (Hatzipanayotou, Michael and Miller, 1994). A separate

definition is stated by the HMRC department, if any business entity doesn't meet that definition

then it can't be registered under VAT scheme. Business entities which are engaged in the

business of goods and services those exempted from tax also exempted from VAT registration.

There are always need of supporting evidence such as invoices, bank statement etc. for

registration under VAT. The registration under VAT may be voluntary or compulsory as per the

rules of department. Following documents/information are needed to register for VAT:

National Insurance (NI) number.

The VAT administration is deal by the HMRC department. Various VAT offices deal

with the VAT matters as specified by relevant department. The central office at Southend

concerns with the general VAT matters. It includes issuing guidelines specific type of supply.

The local officers are appointed to deal with local administration. It provide guideline to

registered business whose principle place of transactions are situated in this respective area. The

regional collectors control whole the process. For checking whether the appropriate rules are

followed by registered persons or not, staff of HMRC will visit timely the registered entities. If

any business person don't agree with the applicable VAT rules then he can ask his local officer in

local authority. It is not compulsory every time to appeal formally (Virmani, 1989.). Where it

settled by an agreement, written statement is issued by normal appeal process. The time limit for

every process is fixed under the department sections.

1.3 VAT registration requirements

A trader may be registered under VAT system may be voluntary or compulsory. A

business must register for VAT with HM Revenue and Customs ( HMRC ) if its VAT taxable

turnover is more than £85,000 per financial year. And the business is require to inform the

HMRC department within 30 days from end of month in which he become liable to VAT

payment. If the department of revenue and custom satisfy that the supply of goods not exceeds

from British pound 81000, registration will not be required under VAT system. And if the

registration is not done at appropriate time then vat is payable from the preceding date from

which he is liable to pay VAT or registration. Organization/person would also need to register

for VAT if receive products that are bought and sold in the UK from the EU worth more than

British pounds 83,000 or expect to go over the dividing line/point where something begins or

changes in a single 30 day period (Hatzipanayotou, Michael and Miller, 1994). A separate

definition is stated by the HMRC department, if any business entity doesn't meet that definition

then it can't be registered under VAT scheme. Business entities which are engaged in the

business of goods and services those exempted from tax also exempted from VAT registration.

There are always need of supporting evidence such as invoices, bank statement etc. for

registration under VAT. The registration under VAT may be voluntary or compulsory as per the

rules of department. Following documents/information are needed to register for VAT:

National Insurance (NI) number.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax identifier i.e. Unique Taxpayer’s reference (UTR) number.

Certificate of incorporation/incorporation details.

Business bank accounts details.

Information on all associated businesses within the last two years.

Zero rated supplier not required to register under VAT.

1.4 The information that must be included on business documentation of VAT

registered businesses

A VAT registered business making a supply to another VAT registered person then it must have

to issue a VAT invoice within 30 days of tax point. A VAT registered trader must keep records

for 6 years and the records may be in form of paper or in digital (Creedy, 2001). VAT registered

businesses includes various informations in documentation which are as followings:

1. Registration number provided at time of VAT registration.

2. The date of issuing invoices.

3. VAT rate for each supply.

4. The VAT exclusive amount for each supply

5. The total VAT exclusive amount

6. The amount of VAT payable

7. The invoice date and invoice number

8. The type of supply

9. The quantity and description of the goods supplied

10. The company’s name and address

11. The name and address of the customer

If a sales invoice is meant to be valid for VAT purposes i.e. a separate VAT invoice does

not need to be issued, then all of the above needs to be included in the sales invoice. Apart from

that, a separate VAT invoice will need to be issued. A less detailed invoice is also issued by a

taxable person which include less information than a full documented invoice. In that situation

the invoice is for a total including VAT of up to £250 (Kakwani, 1977). The less informational

invoice include only necessary information such as :

The supplier’s name, address and registration number.

The date of the supply.

A description of the goods or services supplied.

Certificate of incorporation/incorporation details.

Business bank accounts details.

Information on all associated businesses within the last two years.

Zero rated supplier not required to register under VAT.

1.4 The information that must be included on business documentation of VAT

registered businesses

A VAT registered business making a supply to another VAT registered person then it must have

to issue a VAT invoice within 30 days of tax point. A VAT registered trader must keep records

for 6 years and the records may be in form of paper or in digital (Creedy, 2001). VAT registered

businesses includes various informations in documentation which are as followings:

1. Registration number provided at time of VAT registration.

2. The date of issuing invoices.

3. VAT rate for each supply.

4. The VAT exclusive amount for each supply

5. The total VAT exclusive amount

6. The amount of VAT payable

7. The invoice date and invoice number

8. The type of supply

9. The quantity and description of the goods supplied

10. The company’s name and address

11. The name and address of the customer

If a sales invoice is meant to be valid for VAT purposes i.e. a separate VAT invoice does

not need to be issued, then all of the above needs to be included in the sales invoice. Apart from

that, a separate VAT invoice will need to be issued. A less detailed invoice is also issued by a

taxable person which include less information than a full documented invoice. In that situation

the invoice is for a total including VAT of up to £250 (Kakwani, 1977). The less informational

invoice include only necessary information such as :

The supplier’s name, address and registration number.

The date of the supply.

A description of the goods or services supplied.

The rate of VAT chargeable.

The total amount chargeable including VAT.

1.5 The requirements and the frequency of reporting for VAT schemes

Some of the special schemes are available to small business for reducing work and

payable amount of VAT. These schemes are such as Annual accounting, Cash accounting, Flat-

rate scheme and Standard scheme. These schemes includes different standards and operations.

Category wise description of VAT special schemes as follows:

Annual accounting scheme: The annual accounting scheme allows you to complete just

one VAT return each year, instead of four (Joseph, 1939). VAT is paid by instalments, either

three quarterly instalments or nine monthly instalments as per the rules of revenue and custom

department. These must be paid by direct debit, standing order or other electronic means. After

joining the big plan, HMRC calculates and tells the business of the instalment amounts and the

dates they are due. The business can pay added something you choose to do, but is not required

payments. At the end of the year the business submits its VAT return and any balance

outstanding. If too much money has been paid throughout the year, HMRC will refund the

excess. The due date for once-a-year returns is in a common and regular way two months after

the end of the once-a-year accounting year. Both the dates for the start and end of the VAT

period and the due dates will be shown on the VAT return. The ability to be picked to participate

conditions are just like the 'cash accounting scheme' in that the big plan is available if taxable

supplies will be no more than British pounds 1,350,000 in the next year. The business will need

to leave the scheme if its taxable sales keeping out VAT go beyond British pounds 1,600,000 for

the year.

Flat rate scheme : The big layout plan allows a business to apply a fixed flat-rate

percentage to the gross turnover to arrive at the at due (Keen, 2013). Fixed-rate percentages

change/differ depending on the type of business. Subject to certain conditions, the layout is for

businesses with turnover of no more than British pounds 150,000 a year, leaving out VAT. The

business will stop to be able to participate to use the big layout if the total value of income for

the year ending is more than British pounds 230,000. Farmers also certified under that scheme

not account for VAT, or require to submit return. They may have to be charge flat 4% rate. The

farmer will not be eligible to join the flat-rate scheme unless:

The total amount chargeable including VAT.

1.5 The requirements and the frequency of reporting for VAT schemes

Some of the special schemes are available to small business for reducing work and

payable amount of VAT. These schemes are such as Annual accounting, Cash accounting, Flat-

rate scheme and Standard scheme. These schemes includes different standards and operations.

Category wise description of VAT special schemes as follows:

Annual accounting scheme: The annual accounting scheme allows you to complete just

one VAT return each year, instead of four (Joseph, 1939). VAT is paid by instalments, either

three quarterly instalments or nine monthly instalments as per the rules of revenue and custom

department. These must be paid by direct debit, standing order or other electronic means. After

joining the big plan, HMRC calculates and tells the business of the instalment amounts and the

dates they are due. The business can pay added something you choose to do, but is not required

payments. At the end of the year the business submits its VAT return and any balance

outstanding. If too much money has been paid throughout the year, HMRC will refund the

excess. The due date for once-a-year returns is in a common and regular way two months after

the end of the once-a-year accounting year. Both the dates for the start and end of the VAT

period and the due dates will be shown on the VAT return. The ability to be picked to participate

conditions are just like the 'cash accounting scheme' in that the big plan is available if taxable

supplies will be no more than British pounds 1,350,000 in the next year. The business will need

to leave the scheme if its taxable sales keeping out VAT go beyond British pounds 1,600,000 for

the year.

Flat rate scheme : The big layout plan allows a business to apply a fixed flat-rate

percentage to the gross turnover to arrive at the at due (Keen, 2013). Fixed-rate percentages

change/differ depending on the type of business. Subject to certain conditions, the layout is for

businesses with turnover of no more than British pounds 150,000 a year, leaving out VAT. The

business will stop to be able to participate to use the big layout if the total value of income for

the year ending is more than British pounds 230,000. Farmers also certified under that scheme

not account for VAT, or require to submit return. They may have to be charge flat 4% rate. The

farmer will not be eligible to join the flat-rate scheme unless:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The non-farming activities are zero-rated, in which case the farmer may ask for

exemption from registration and join the scheme; or

The non-farming business is run as a separate business by a different legal entity e.g. a

person could run his farming activities as a sole proprietor and a bed and breakfast

business in partnership with another person.

Standard scheme: Under this scheme VAT is paid on the time when invoices are issued.

VAT return is filled four times per year under that scheme (FitzGerald, Johnston and Williams,

1995). VAT amount is calculate for payment by comparing the VAT due on the cost and owed

on sales volume. HMRC will refund and acquire the due VAT amount after comparing the above

terms.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintaining an up to date knowledge of changes to code of practice, regulations or

legislation will help the business organization at a wider context. HMRC announces various

changes VAT regulation and legislation, some of are as follows:

Digital records maintenance will be compulsory for VAT calculation, manual records

are not further valid. So if a businesses organization keep it in consideration with up to

date then it have to very easy to face challenges in future.

Changes are announced in VAT return submission that returns must be submitted to

HMRC by means of a business’s functional compatible software communicating

digitally via HMRC’s API platform, and not by manually entering the VAT return

figures onto the HMRC portal. So VAT registered business organization must be

considered this upcoming change so that in future return can be submitted very easily

and without any errors.

TASK 2

2.1 Extraction of relevant data for a specific period from accounting records

VAT returns can be submitted either monthly or quarterly in In the UK. Most of the

returns are filled on a quarterly basis. Once registered, a business will be assigned to a “VAT

stagger group”. Let us assume stagger group on which quarters ends on March, June, September

and December. Following are the details for the extraction of relevant data for filing the return of

the VAT for the quarter ending 31st December, 2018:

exemption from registration and join the scheme; or

The non-farming business is run as a separate business by a different legal entity e.g. a

person could run his farming activities as a sole proprietor and a bed and breakfast

business in partnership with another person.

Standard scheme: Under this scheme VAT is paid on the time when invoices are issued.

VAT return is filled four times per year under that scheme (FitzGerald, Johnston and Williams,

1995). VAT amount is calculate for payment by comparing the VAT due on the cost and owed

on sales volume. HMRC will refund and acquire the due VAT amount after comparing the above

terms.

1.6 Maintain an up-to-date knowledge of changes to codes of practice, regulation or legislation

Maintaining an up to date knowledge of changes to code of practice, regulations or

legislation will help the business organization at a wider context. HMRC announces various

changes VAT regulation and legislation, some of are as follows:

Digital records maintenance will be compulsory for VAT calculation, manual records

are not further valid. So if a businesses organization keep it in consideration with up to

date then it have to very easy to face challenges in future.

Changes are announced in VAT return submission that returns must be submitted to

HMRC by means of a business’s functional compatible software communicating

digitally via HMRC’s API platform, and not by manually entering the VAT return

figures onto the HMRC portal. So VAT registered business organization must be

considered this upcoming change so that in future return can be submitted very easily

and without any errors.

TASK 2

2.1 Extraction of relevant data for a specific period from accounting records

VAT returns can be submitted either monthly or quarterly in In the UK. Most of the

returns are filled on a quarterly basis. Once registered, a business will be assigned to a “VAT

stagger group”. Let us assume stagger group on which quarters ends on March, June, September

and December. Following are the details for the extraction of relevant data for filing the return of

the VAT for the quarter ending 31st December, 2018:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

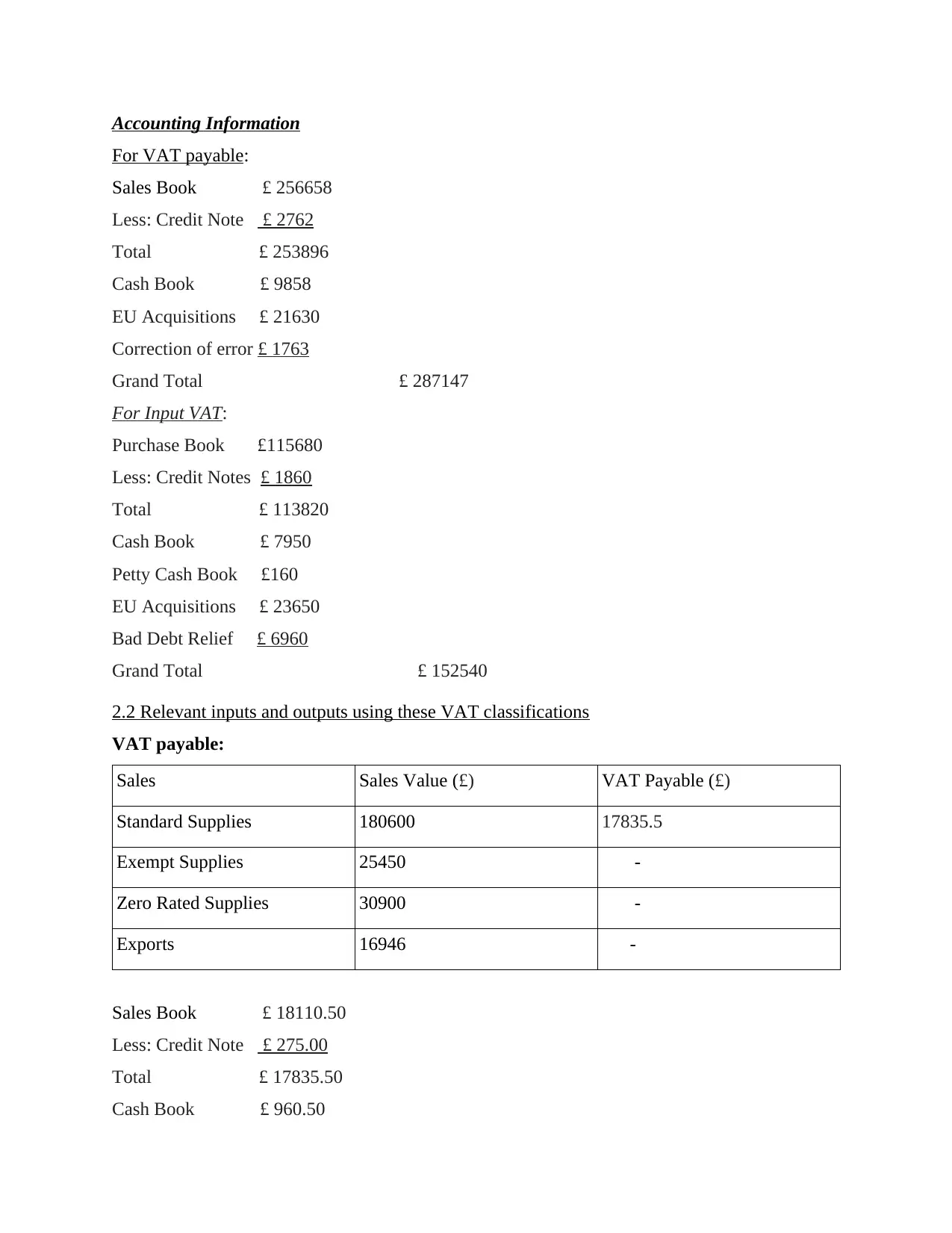

Accounting Information

For VAT payable:

Sales Book £ 256658

Less: Credit Note £ 2762

Total £ 253896

Cash Book £ 9858

EU Acquisitions £ 21630

Correction of error £ 1763

Grand Total £ 287147

For Input VAT:

Purchase Book £115680

Less: Credit Notes £ 1860

Total £ 113820

Cash Book £ 7950

Petty Cash Book £160

EU Acquisitions £ 23650

Bad Debt Relief £ 6960

Grand Total £ 152540

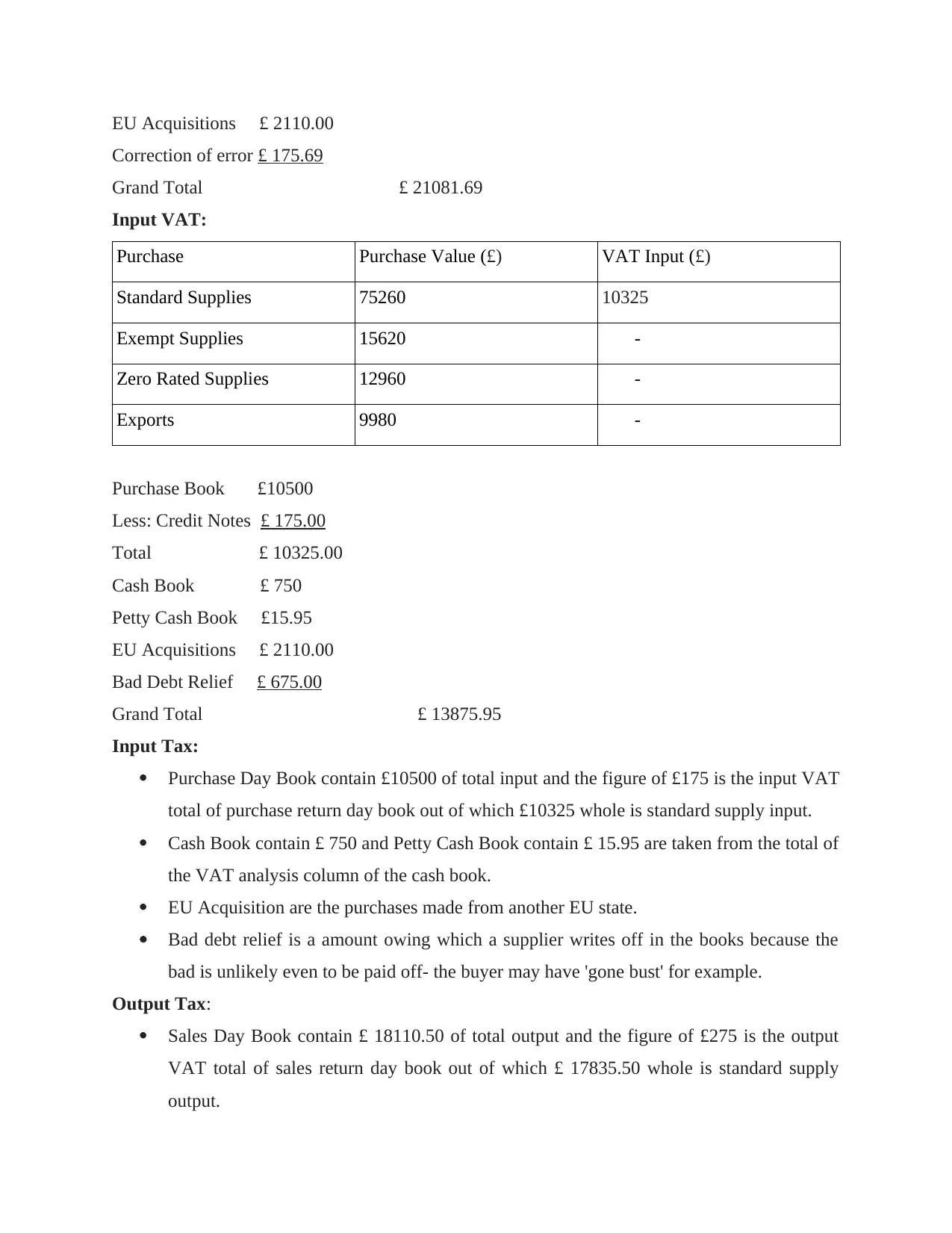

2.2 Relevant inputs and outputs using these VAT classifications

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 180600 17835.5

Exempt Supplies 25450 -

Zero Rated Supplies 30900 -

Exports 16946 -

Sales Book £ 18110.50

Less: Credit Note £ 275.00

Total £ 17835.50

Cash Book £ 960.50

For VAT payable:

Sales Book £ 256658

Less: Credit Note £ 2762

Total £ 253896

Cash Book £ 9858

EU Acquisitions £ 21630

Correction of error £ 1763

Grand Total £ 287147

For Input VAT:

Purchase Book £115680

Less: Credit Notes £ 1860

Total £ 113820

Cash Book £ 7950

Petty Cash Book £160

EU Acquisitions £ 23650

Bad Debt Relief £ 6960

Grand Total £ 152540

2.2 Relevant inputs and outputs using these VAT classifications

VAT payable:

Sales Sales Value (£) VAT Payable (£)

Standard Supplies 180600 17835.5

Exempt Supplies 25450 -

Zero Rated Supplies 30900 -

Exports 16946 -

Sales Book £ 18110.50

Less: Credit Note £ 275.00

Total £ 17835.50

Cash Book £ 960.50

EU Acquisitions £ 2110.00

Correction of error £ 175.69

Grand Total £ 21081.69

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 75260 10325

Exempt Supplies 15620 -

Zero Rated Supplies 12960 -

Exports 9980 -

Purchase Book £10500

Less: Credit Notes £ 175.00

Total £ 10325.00

Cash Book £ 750

Petty Cash Book £15.95

EU Acquisitions £ 2110.00

Bad Debt Relief £ 675.00

Grand Total £ 13875.95

Input Tax:

Purchase Day Book contain £10500 of total input and the figure of £175 is the input VAT

total of purchase return day book out of which £10325 whole is standard supply input.

Cash Book contain £ 750 and Petty Cash Book contain £ 15.95 are taken from the total of

the VAT analysis column of the cash book.

EU Acquisition are the purchases made from another EU state.

Bad debt relief is a amount owing which a supplier writes off in the books because the

bad is unlikely even to be paid off- the buyer may have 'gone bust' for example.

Output Tax:

Sales Day Book contain £ 18110.50 of total output and the figure of £275 is the output

VAT total of sales return day book out of which £ 17835.50 whole is standard supply

output.

Correction of error £ 175.69

Grand Total £ 21081.69

Input VAT:

Purchase Purchase Value (£) VAT Input (£)

Standard Supplies 75260 10325

Exempt Supplies 15620 -

Zero Rated Supplies 12960 -

Exports 9980 -

Purchase Book £10500

Less: Credit Notes £ 175.00

Total £ 10325.00

Cash Book £ 750

Petty Cash Book £15.95

EU Acquisitions £ 2110.00

Bad Debt Relief £ 675.00

Grand Total £ 13875.95

Input Tax:

Purchase Day Book contain £10500 of total input and the figure of £175 is the input VAT

total of purchase return day book out of which £10325 whole is standard supply input.

Cash Book contain £ 750 and Petty Cash Book contain £ 15.95 are taken from the total of

the VAT analysis column of the cash book.

EU Acquisition are the purchases made from another EU state.

Bad debt relief is a amount owing which a supplier writes off in the books because the

bad is unlikely even to be paid off- the buyer may have 'gone bust' for example.

Output Tax:

Sales Day Book contain £ 18110.50 of total output and the figure of £275 is the output

VAT total of sales return day book out of which £ 17835.50 whole is standard supply

output.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Book contain £ 960.50 which are taken from the total of the VAT analysis column

of the cash book.

Correction of error is the case in which business owes a net £ 175.69 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low.

2.3 VAT due to, or from, the relevant tax authority

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

2.4 VAT return and any associated payment within the statutory time limits

Particulars Amount (£)

of the cash book.

Correction of error is the case in which business owes a net £ 175.69 which could be

caused due to amount of input VAT included has been too high or amount of output VAT

included has been too low.

2.3 VAT due to, or from, the relevant tax authority

The authority for VAT and custom in UK is HM Revenue and Custom. The VAT due to

or from is analysed by HMRC only. The calculations of VAT due to or from HMRC in the given

case are as follows:

Particulars Amount (£)

VAT output:

Sales 17835.5

Cash Book 960.5

EU Acquisitions 2110

Correction of error 175.69

Total VAT output 21081.69

VAT Input:

Purchase 10325

Cash Book 750

Petty Cash Book 15.95

EU Acquisition 2110

Bad Debts Relief 675

Total VAT Input 13875.95

Net VAT Payable to HMRC 7205.74

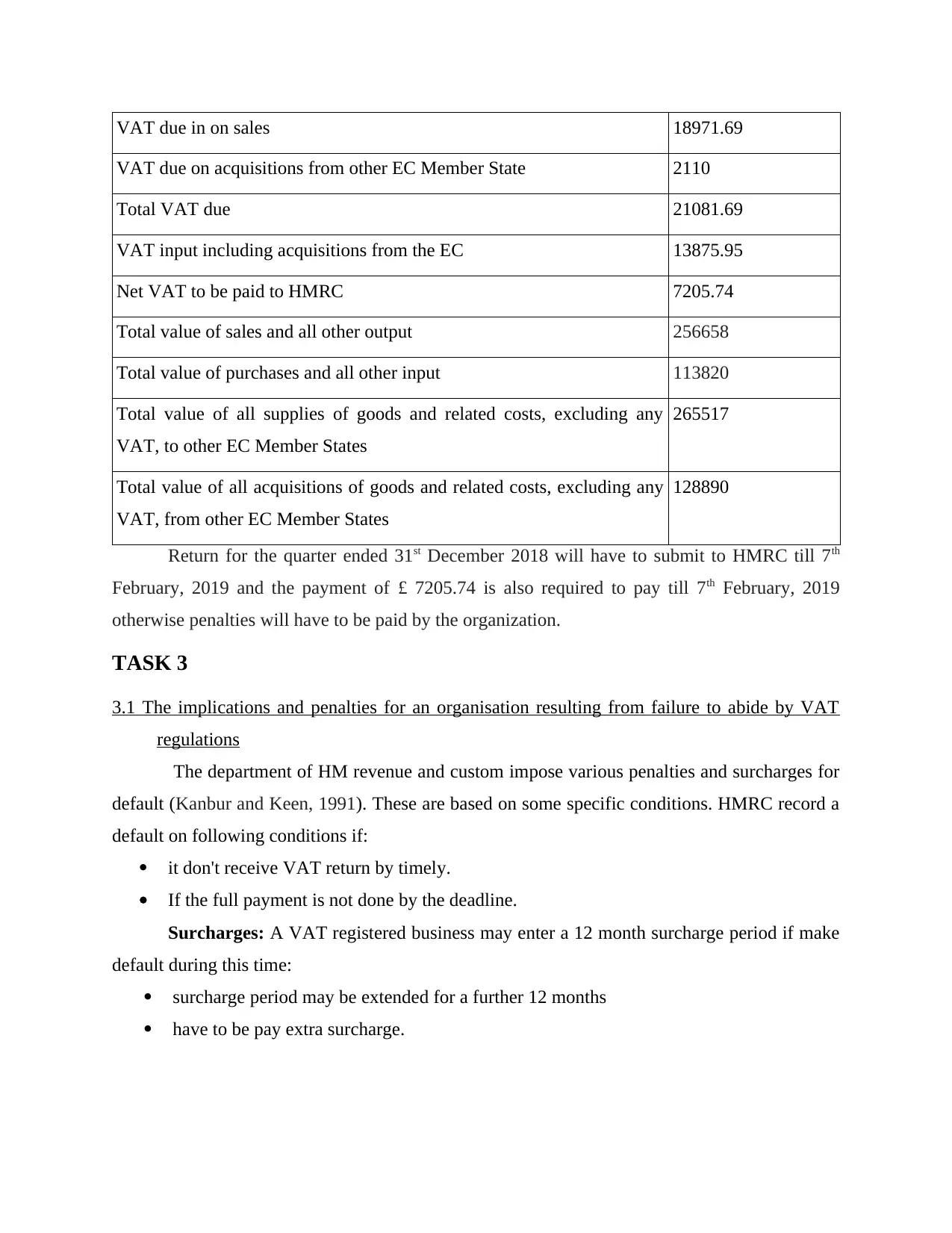

2.4 VAT return and any associated payment within the statutory time limits

Particulars Amount (£)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VAT due in on sales 18971.69

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

Return for the quarter ended 31st December 2018 will have to submit to HMRC till 7th

February, 2019 and the payment of £ 7205.74 is also required to pay till 7th February, 2019

otherwise penalties will have to be paid by the organization.

TASK 3

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations

The department of HM revenue and custom impose various penalties and surcharges for

default (Kanbur and Keen, 1991). These are based on some specific conditions. HMRC record a

default on following conditions if:

it don't receive VAT return by timely.

If the full payment is not done by the deadline.

Surcharges: A VAT registered business may enter a 12 month surcharge period if make

default during this time:

surcharge period may be extended for a further 12 months

have to be pay extra surcharge.

VAT due on acquisitions from other EC Member State 2110

Total VAT due 21081.69

VAT input including acquisitions from the EC 13875.95

Net VAT to be paid to HMRC 7205.74

Total value of sales and all other output 256658

Total value of purchases and all other input 113820

Total value of all supplies of goods and related costs, excluding any

VAT, to other EC Member States

265517

Total value of all acquisitions of goods and related costs, excluding any

VAT, from other EC Member States

128890

Return for the quarter ended 31st December 2018 will have to submit to HMRC till 7th

February, 2019 and the payment of £ 7205.74 is also required to pay till 7th February, 2019

otherwise penalties will have to be paid by the organization.

TASK 3

3.1 The implications and penalties for an organisation resulting from failure to abide by VAT

regulations

The department of HM revenue and custom impose various penalties and surcharges for

default (Kanbur and Keen, 1991). These are based on some specific conditions. HMRC record a

default on following conditions if:

it don't receive VAT return by timely.

If the full payment is not done by the deadline.

Surcharges: A VAT registered business may enter a 12 month surcharge period if make

default during this time:

surcharge period may be extended for a further 12 months

have to be pay extra surcharge.

If some time late return is filled then surcharge not imposed in some specific cases such

as vat pay in full timely, due a repayment. Surcharge is not applicable for first default. With in

12 months surcharge rate is fixed for every default according to time.

Penalties: HMRC charge the penalties as follows for making default:

100% of any tax under-stated or over-claimed if you send a return that contains a careless

or deliberate inaccuracy

30% of an assessment if sends you one that’s too low and you do not tell them it’s wrong

within 30 days

£400 if you submit a paper Return, unless has told you you’re exempt from submitting

your return online (VAT Returns. 2019).

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

The errors or omission identified in previous period of VAT then HMRC can charge

penalty for the errors. These errors are divided into various categories. If errors are done

intentionally or due to careless behaviour then decisions will be different from other situation of

making errors. Section 4 deal with the various type of errors and their adjustments after

identifying these in previous periods (Rajemison and Younger, 2000). There are 2 methods

described in the HMRC rules for rectifying errors. These methods are differentiated on the basis

of errors amount.

TASK 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

A business have a wide impact of the VAT payment on cash flow an financial forecast. it

is a substantial payment for every business entity registered under VAT system, so provisions

should be made for the surety of payment in future. If the VAT payment £1.35 million or less

than, then it may pay on the basis of cash received and pay. And payment of VAT effect the flow

of cash in cash flow statement. It will help the managers that payment is not done to HMRC on

invoice. Financial forecast can be done through help of VAT payment, if it will be done in partial

payment then cash flow can't effected at single point and at wide level. So managers must

consider the payment points and amounts for less effected cash flow and financial forecast.

as vat pay in full timely, due a repayment. Surcharge is not applicable for first default. With in

12 months surcharge rate is fixed for every default according to time.

Penalties: HMRC charge the penalties as follows for making default:

100% of any tax under-stated or over-claimed if you send a return that contains a careless

or deliberate inaccuracy

30% of an assessment if sends you one that’s too low and you do not tell them it’s wrong

within 30 days

£400 if you submit a paper Return, unless has told you you’re exempt from submitting

your return online (VAT Returns. 2019).

3.2 Adjustments and declarations for any errors or omissions identified in previous VAT periods

The errors or omission identified in previous period of VAT then HMRC can charge

penalty for the errors. These errors are divided into various categories. If errors are done

intentionally or due to careless behaviour then decisions will be different from other situation of

making errors. Section 4 deal with the various type of errors and their adjustments after

identifying these in previous periods (Rajemison and Younger, 2000). There are 2 methods

described in the HMRC rules for rectifying errors. These methods are differentiated on the basis

of errors amount.

TASK 4

4.1 Inform managers of the impact that the VAT payment may have on an organisation’s cash

flow and financial forecasts

A business have a wide impact of the VAT payment on cash flow an financial forecast. it

is a substantial payment for every business entity registered under VAT system, so provisions

should be made for the surety of payment in future. If the VAT payment £1.35 million or less

than, then it may pay on the basis of cash received and pay. And payment of VAT effect the flow

of cash in cash flow statement. It will help the managers that payment is not done to HMRC on

invoice. Financial forecast can be done through help of VAT payment, if it will be done in partial

payment then cash flow can't effected at single point and at wide level. So managers must

consider the payment points and amounts for less effected cash flow and financial forecast.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.