Conceptual Framework in Accounting and Quality of Financial Reporting

VerifiedAdded on 2023/06/07

|15

|3073

|64

AI Summary

This proposal discusses the importance of conceptual framework in accounting and quality of financial reporting. It identifies the various aspects of the conceptual framework of accounting and the importance in the financial report preparations in the organizations.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Conceptual Framework in Accounting and Quality of Financial Reporting

CONCEPTUAL FRAMEWORK IN ACCOUNTING AND QUALITY OF FINANCIAL

REPORTING

Name:

Institution:

Course:

Tutor:

Date:

CONCEPTUAL FRAMEWORK IN ACCOUNTING AND QUALITY OF FINANCIAL

REPORTING

Name:

Institution:

Course:

Tutor:

Date:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conceptual Framework in Accounting and Quality of Financial Reporting 2

Introduction

In the past decade, the conceptual framework in Accounting and Quality of Financial Reporting

has become a vital aspect in accounting and management of financial reporting system of

organization. Without a useful conceptual framework, organizations face challenges in the

maintainer of the financial reports. The conceptual framework in accounting and quality

financial reporting was developed to guide users and prepares of the financial reports, and this

has been made mandatory by the IFRS to all organizations across the world (Krippendorff 2018,

p.1229). Organizations such as Financial Accounting Standards Board (FASB), Australia

Accounting Standard Board (AASB), International Standard Board (IASB), and many others

maintain that the financial accounting and quality reporting provide accurate and fair information

and financial position and economic status of an organization, therefore, have developed

different frameworks to facilitate the same (Avran et al. 2015, p.383). The proposal entails the

identification of the various aspects of the conceptual framework of accounting and the

importance in the financial report preparations in the organizations. This is achievable through

the review of the relevant literature and collection of primary data from the most relevant

sources.

Project Objective

Several surveys have found financial statement fraud as the most significant contributor to the

loss of funds in many organizations (Tribuzi 2018, p.821). The frauds committed through

misreporting of the available and used funds come as a result of the inadequate or poor

framework. These poor financial reports tend to deter investors away from focusing on the

development of the organization, as they lack a proper framework to use in making strategic

Introduction

In the past decade, the conceptual framework in Accounting and Quality of Financial Reporting

has become a vital aspect in accounting and management of financial reporting system of

organization. Without a useful conceptual framework, organizations face challenges in the

maintainer of the financial reports. The conceptual framework in accounting and quality

financial reporting was developed to guide users and prepares of the financial reports, and this

has been made mandatory by the IFRS to all organizations across the world (Krippendorff 2018,

p.1229). Organizations such as Financial Accounting Standards Board (FASB), Australia

Accounting Standard Board (AASB), International Standard Board (IASB), and many others

maintain that the financial accounting and quality reporting provide accurate and fair information

and financial position and economic status of an organization, therefore, have developed

different frameworks to facilitate the same (Avran et al. 2015, p.383). The proposal entails the

identification of the various aspects of the conceptual framework of accounting and the

importance in the financial report preparations in the organizations. This is achievable through

the review of the relevant literature and collection of primary data from the most relevant

sources.

Project Objective

Several surveys have found financial statement fraud as the most significant contributor to the

loss of funds in many organizations (Tribuzi 2018, p.821). The frauds committed through

misreporting of the available and used funds come as a result of the inadequate or poor

framework. These poor financial reports tend to deter investors away from focusing on the

development of the organization, as they lack a proper framework to use in making strategic

Conceptual Framework in Accounting and Quality of Financial Reporting 3

decisions. The conceptual framework in accounting has been efficient in enhancing the

qualitative aspects of the financial statements of most of the organizations across the world

through proper decision making. Different kinds of decision making aspects such as buying and

selling of shares, assessment of shares and their returns, and investment of shares in the

organization.

Project Scope

The conceptual framework in accounting is a new and dynamic approach towards creating

quality-based financial reports. Financial reports are not merely used to understand the net cash

flow and inflow; various other aspects make financial reports a significant aspect of an

organization. The project tries to identify various aspects such as:

• The significance of the conceptual framework in accounting and role it plays in

enhancing the quality of the financial reports.

• The significance of the conceptual framework in accounting

• The significance of financial reporting

• Analyzing the effectiveness of the conceptual framework in accounting through the

stakeholder theory

Literature Review

From the onset of the industrial; revolution, the financial accounting and reporting regulation

was majorly centered on profit as investors protection was required to safeguard from

unscrupulous reports by the agents. Accurate information helps in enhancing the organization

reputation, and make the business profitable (Rayman 2013, p.652). Every shareholder of

organizations always embraces accurate information especially in the matters of finance. Many

decisions. The conceptual framework in accounting has been efficient in enhancing the

qualitative aspects of the financial statements of most of the organizations across the world

through proper decision making. Different kinds of decision making aspects such as buying and

selling of shares, assessment of shares and their returns, and investment of shares in the

organization.

Project Scope

The conceptual framework in accounting is a new and dynamic approach towards creating

quality-based financial reports. Financial reports are not merely used to understand the net cash

flow and inflow; various other aspects make financial reports a significant aspect of an

organization. The project tries to identify various aspects such as:

• The significance of the conceptual framework in accounting and role it plays in

enhancing the quality of the financial reports.

• The significance of the conceptual framework in accounting

• The significance of financial reporting

• Analyzing the effectiveness of the conceptual framework in accounting through the

stakeholder theory

Literature Review

From the onset of the industrial; revolution, the financial accounting and reporting regulation

was majorly centered on profit as investors protection was required to safeguard from

unscrupulous reports by the agents. Accurate information helps in enhancing the organization

reputation, and make the business profitable (Rayman 2013, p.652). Every shareholder of

organizations always embraces accurate information especially in the matters of finance. Many

Conceptual Framework in Accounting and Quality of Financial Reporting 4

countries have embraced international Financial Reporting Standards (IFRS) and due to the

conceptual framework. Accounting and the financial reporting does not only determine the

reputation of the organizations but also offer accurate information for better decision making that

continues to steer forward the objectives(Avran et al. 2015, p.386). The conceptual framework in

accounting, therefore, has been made compulsory in organizations by the IFRS across the world

to revolutionize the reporting system after understanding the significance of the conceptual

framework in accounting and quality in finance report.

Krippendorff (2018,p.1231) indicates that different working accounting standards in different

countries pose difficulty for many organizations to work across the world as the managers are

unable to plan for the future strategic actions. Due to this every organization and country have

revised the standards to enable effective operations: AASB in Australia controls the working

standards of organizations in accordance to the conceptual framework by the IFRS such as

relevance, comparability, understandability, timelessness and faithfulness representation

Reliability

Reliability is a critical factor in accounting and financial reporting quality. The provide

information must be reliable to be useful to the organization since the users depend on it to make

a sound judgment (Figlioli,Lemes & Lima 2017, p.339). The information is required to entirely

free from the material mistakes, verifiable and the information must be neutral.

Understandability

The information provided must be of high understandability and this achievable through

effective communication. According to Pounder (2013, p.31),understandability is one of the

enhancing aspects that improve the information presented and therefore, makes it easier for the

countries have embraced international Financial Reporting Standards (IFRS) and due to the

conceptual framework. Accounting and the financial reporting does not only determine the

reputation of the organizations but also offer accurate information for better decision making that

continues to steer forward the objectives(Avran et al. 2015, p.386). The conceptual framework in

accounting, therefore, has been made compulsory in organizations by the IFRS across the world

to revolutionize the reporting system after understanding the significance of the conceptual

framework in accounting and quality in finance report.

Krippendorff (2018,p.1231) indicates that different working accounting standards in different

countries pose difficulty for many organizations to work across the world as the managers are

unable to plan for the future strategic actions. Due to this every organization and country have

revised the standards to enable effective operations: AASB in Australia controls the working

standards of organizations in accordance to the conceptual framework by the IFRS such as

relevance, comparability, understandability, timelessness and faithfulness representation

Reliability

Reliability is a critical factor in accounting and financial reporting quality. The provide

information must be reliable to be useful to the organization since the users depend on it to make

a sound judgment (Figlioli,Lemes & Lima 2017, p.339). The information is required to entirely

free from the material mistakes, verifiable and the information must be neutral.

Understandability

The information provided must be of high understandability and this achievable through

effective communication. According to Pounder (2013, p.31),understandability is one of the

enhancing aspects that improve the information presented and therefore, makes it easier for the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conceptual Framework in Accounting and Quality of Financial Reporting 5

users to comprehend what the reports entails and needs. The understandability can also be

enhanced through the use of tables, graphs to help the dissemination of the information more

clearly.

Timelessness

Timelessness insists that the financial information provided must be available to the users before

losing the power and influence .the quality of accounting and financial report is always based

and evaluated on the period between the year-end and the date of issuance by the auditor.

Faithful representation

Faithful representation is an aspect that requires representing the real economic status of the

financial information after the auditing (Khanna 2017, p.26). The representation entails how

economic resources such as transactions have taken place and therefore, needs high quality and

neutrality.

Comparability

Comparability allows the report users to compare the financial statements against the

achievements, and other organizations to determine the position of the organization (Caneghen

2016, p. 2686). For an adequate comparison, two identical situations are always represented in

the accounting facts and figures to explain the changes that have taken place during that specific

period, therefore, ease the understanding of the similarities and differences.

The financial information contains all these qualities enables the investors and the stakeholders

to predict the future outcomes and their returns, eventually enhancing the decision making

process. The conceptual framework also works alongside Stakeholder theory that states that the

users to comprehend what the reports entails and needs. The understandability can also be

enhanced through the use of tables, graphs to help the dissemination of the information more

clearly.

Timelessness

Timelessness insists that the financial information provided must be available to the users before

losing the power and influence .the quality of accounting and financial report is always based

and evaluated on the period between the year-end and the date of issuance by the auditor.

Faithful representation

Faithful representation is an aspect that requires representing the real economic status of the

financial information after the auditing (Khanna 2017, p.26). The representation entails how

economic resources such as transactions have taken place and therefore, needs high quality and

neutrality.

Comparability

Comparability allows the report users to compare the financial statements against the

achievements, and other organizations to determine the position of the organization (Caneghen

2016, p. 2686). For an adequate comparison, two identical situations are always represented in

the accounting facts and figures to explain the changes that have taken place during that specific

period, therefore, ease the understanding of the similarities and differences.

The financial information contains all these qualities enables the investors and the stakeholders

to predict the future outcomes and their returns, eventually enhancing the decision making

process. The conceptual framework also works alongside Stakeholder theory that states that the

Conceptual Framework in Accounting and Quality of Financial Reporting 6

purposes of the business are to create value for anybody that affects and is affected by the

business (Thomas & Thompson 2012, p.1761). These people entail suppliers, employees,

communities and the shareholders; the theory is significant as it stresses the importance of

financial report through various aspects and enhances the understanding of responsibilities of

every stakeholder in holding the entity accountable regarding resources invested. These

qualitative features should always be maximized in the financial report as this can attract more

investors in an organization (Sinclair & Bolt 2017, p.777).To achieve this, the organization will

have to spend a considerable amount of money and time in preparing the accounting and the

financial report.

Limitations

The literature reviews inevitably contain abstracts descriptions of the conceptual frameworks that

cannot be used as standards across all countries. The conceptual framework keeps on changing to

accommodate all the countries and therefore, an individual is required to make interpretations of

the contents whenever auditing is supposed to take place.

Research Questions/Hypothesis

Primary Question

Do accounting and financial reporting frameworks impact the quality of the financial reports in

Australia Organizations as measured by quality measuring tools?

Secondary Questions

Do the international financial reporting frameworks affect the quality of the financial reports of

Australia organizations?

purposes of the business are to create value for anybody that affects and is affected by the

business (Thomas & Thompson 2012, p.1761). These people entail suppliers, employees,

communities and the shareholders; the theory is significant as it stresses the importance of

financial report through various aspects and enhances the understanding of responsibilities of

every stakeholder in holding the entity accountable regarding resources invested. These

qualitative features should always be maximized in the financial report as this can attract more

investors in an organization (Sinclair & Bolt 2017, p.777).To achieve this, the organization will

have to spend a considerable amount of money and time in preparing the accounting and the

financial report.

Limitations

The literature reviews inevitably contain abstracts descriptions of the conceptual frameworks that

cannot be used as standards across all countries. The conceptual framework keeps on changing to

accommodate all the countries and therefore, an individual is required to make interpretations of

the contents whenever auditing is supposed to take place.

Research Questions/Hypothesis

Primary Question

Do accounting and financial reporting frameworks impact the quality of the financial reports in

Australia Organizations as measured by quality measuring tools?

Secondary Questions

Do the international financial reporting frameworks affect the quality of the financial reports of

Australia organizations?

Conceptual Framework in Accounting and Quality of Financial Reporting 7

Hypothesis

Based on the primary and the secondary research questions, the following hypothesis is guided

by the study.

• HO1: the conceptual framework does not have a significant impact on the quality of the

accounting and financial reports as measured by the quality measuring tools(FPO and

NFPOs).

• HO2: Internationally designed and accepted financial reporting systems do not have a

considerable impact on the quality of the financial report as measured by the quality

tools.

Methodology

The study adopts both the qualitative and quantitative research designs. The mixed method is

chosen base on the objectives to establish the impact of the conceptual framework on the quality

of the financial and accounting reports in Australia.

Research Design and justification

In this study, the accounting and the financial reporting frameworks are the independent

variables, which are considered in two categories. The categories are internationally accepted

IFRS and IASB. The dependent variable is the quality of the accounting and the financial report

as determined by the framework and measured by the quality tools.

The qualitative research design is appropriate for the study as it provides the basic understanding

of the topic. The review of the literature provides information on the evolution of the conceptual

frameworks, the importance, and the qualities aspects.

Hypothesis

Based on the primary and the secondary research questions, the following hypothesis is guided

by the study.

• HO1: the conceptual framework does not have a significant impact on the quality of the

accounting and financial reports as measured by the quality measuring tools(FPO and

NFPOs).

• HO2: Internationally designed and accepted financial reporting systems do not have a

considerable impact on the quality of the financial report as measured by the quality

tools.

Methodology

The study adopts both the qualitative and quantitative research designs. The mixed method is

chosen base on the objectives to establish the impact of the conceptual framework on the quality

of the financial and accounting reports in Australia.

Research Design and justification

In this study, the accounting and the financial reporting frameworks are the independent

variables, which are considered in two categories. The categories are internationally accepted

IFRS and IASB. The dependent variable is the quality of the accounting and the financial report

as determined by the framework and measured by the quality tools.

The qualitative research design is appropriate for the study as it provides the basic understanding

of the topic. The review of the literature provides information on the evolution of the conceptual

frameworks, the importance, and the qualities aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conceptual Framework in Accounting and Quality of Financial Reporting 8

The quantitative research design is more appropriate for the study as it analyzes the relationship

between the financial reporting frameworks and the quality of the financial reporting of the IFRS

and IASB. The approach will help in testing the objectives through the casual-comparative of the

impacts of the past, current, and future of the framework on the organization financial position.

Population, sampling and sampling procedure

Australia contains a large number of organizations that are both national, and international. Some

of these organizations are profit-based while some are non-profit based. The lists of all these

organizations with relevant information are, therefore, obtainable from the Ministry of Internal

Affairs. From the list, there are approximately 3,500 registered organizations: given the

population the estimated sample size is about 130(power {1-β } =0.80;α=0.05;effect size-0.03;

(Conde et al. 2018, p.18).

The researcher will employ a purposive nonprobability sampling method to identify respondents

and participants. The sampling design is chosen based on the complex nature of establishing the

degree of chance to which a unit sample can be drawn from the entire population. Purposive

sampling is more appropriate when specific characteristics are required within the sample unit

such as in this study that might not be well represented through random sampling.

Data collection

Introductory letters will be disseminated to the selected organizations to request their consent to

the participation of the research study, the purpose and assurance of the confidentiality. The

financial reports from the selected companies are critically evaluated with the assistance of the

managers or representative from the organizations (Kilinc & Firat 2017,p.1464). Thereafter, the

participants are interviewed using a designed questionnaire that ensures all the data are collected.

The quantitative research design is more appropriate for the study as it analyzes the relationship

between the financial reporting frameworks and the quality of the financial reporting of the IFRS

and IASB. The approach will help in testing the objectives through the casual-comparative of the

impacts of the past, current, and future of the framework on the organization financial position.

Population, sampling and sampling procedure

Australia contains a large number of organizations that are both national, and international. Some

of these organizations are profit-based while some are non-profit based. The lists of all these

organizations with relevant information are, therefore, obtainable from the Ministry of Internal

Affairs. From the list, there are approximately 3,500 registered organizations: given the

population the estimated sample size is about 130(power {1-β } =0.80;α=0.05;effect size-0.03;

(Conde et al. 2018, p.18).

The researcher will employ a purposive nonprobability sampling method to identify respondents

and participants. The sampling design is chosen based on the complex nature of establishing the

degree of chance to which a unit sample can be drawn from the entire population. Purposive

sampling is more appropriate when specific characteristics are required within the sample unit

such as in this study that might not be well represented through random sampling.

Data collection

Introductory letters will be disseminated to the selected organizations to request their consent to

the participation of the research study, the purpose and assurance of the confidentiality. The

financial reports from the selected companies are critically evaluated with the assistance of the

managers or representative from the organizations (Kilinc & Firat 2017,p.1464). Thereafter, the

participants are interviewed using a designed questionnaire that ensures all the data are collected.

Conceptual Framework in Accounting and Quality of Financial Reporting 9

Data analysis

Qualitative data analysis

The qualitative data will be analyzed through the content analysis method-Thematic analysis

(Jaranowski & Krolak 2012, p.21). The choice is based on the available themes under the study:

the impact of the conceptual framework on the quality of the accounting and financial report.

Quantitative data analysis

The study applies both content analysis and one-way analysis of covariance (ANCOVA) for the

data analysis. ANCOVA is chosen to test the hypothesis differences that exist in one independent

variable and has more than two categories grouped by one quantitative dependent variable (Lai

& Kelley 2012, p.352). The independent variable in the study is the financial reporting

frameworks that are grouped into two categories that are: IFRS and AASB. The two variables

will be analyzed against the dependent variable which is the quality of the accounting and the

financial reports.

Limitations

The purposive sampling of the participants might provide low validity and enhance data

manipulation. In this proposal, there are assumptions made. The first assumptions are that quality

is influenced by the class of audit firm irrespective of the geographical position since big firms

tend to use the designed conceptual framework to make the reports: however, this might not be

the case, as no familiar framework guides on the same.

Conclusion

Data analysis

Qualitative data analysis

The qualitative data will be analyzed through the content analysis method-Thematic analysis

(Jaranowski & Krolak 2012, p.21). The choice is based on the available themes under the study:

the impact of the conceptual framework on the quality of the accounting and financial report.

Quantitative data analysis

The study applies both content analysis and one-way analysis of covariance (ANCOVA) for the

data analysis. ANCOVA is chosen to test the hypothesis differences that exist in one independent

variable and has more than two categories grouped by one quantitative dependent variable (Lai

& Kelley 2012, p.352). The independent variable in the study is the financial reporting

frameworks that are grouped into two categories that are: IFRS and AASB. The two variables

will be analyzed against the dependent variable which is the quality of the accounting and the

financial reports.

Limitations

The purposive sampling of the participants might provide low validity and enhance data

manipulation. In this proposal, there are assumptions made. The first assumptions are that quality

is influenced by the class of audit firm irrespective of the geographical position since big firms

tend to use the designed conceptual framework to make the reports: however, this might not be

the case, as no familiar framework guides on the same.

Conclusion

Conceptual Framework in Accounting and Quality of Financial Reporting 10

Every organization depends on the financial statement and accountability to make a strategic

decision; therefore, fraud statements tend to deter investments. Misreport of financial status has

been a problem for many leading to the development of the conceptual framework by IFRS, to

aid in making appropriate, reliable, relevance, and comparable reports. These reports in Australia

are measured through the use of quality tools developed by AASB and IASB.

The study, therefore, aims to determine the level to which the conceptual framework of

accounting and financial reports is affected by, both the national and the international conceptual

frameworks such as IFRS. The study predicts that the IFRS have direct impacts on the quality of

the financial report, and is also determined by the class and level of the auditing firm. The

qualities of the financial report eventually keep the organization reputation, and enhance future

development.

Every organization depends on the financial statement and accountability to make a strategic

decision; therefore, fraud statements tend to deter investments. Misreport of financial status has

been a problem for many leading to the development of the conceptual framework by IFRS, to

aid in making appropriate, reliable, relevance, and comparable reports. These reports in Australia

are measured through the use of quality tools developed by AASB and IASB.

The study, therefore, aims to determine the level to which the conceptual framework of

accounting and financial reports is affected by, both the national and the international conceptual

frameworks such as IFRS. The study predicts that the IFRS have direct impacts on the quality of

the financial report, and is also determined by the class and level of the auditing firm. The

qualities of the financial report eventually keep the organization reputation, and enhance future

development.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conceptual Framework in Accounting and Quality of Financial Reporting 11

List of References

Avram, C, B, Grosanu, A , & Rachisan, P 2015,’ Does country-level governance influence

auditing and financial reporting standards? Evidence from a cross-country analysis, Current

Science ,45, 4, p. 381-386,Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Caneghem, T 2016,’ NPO Financial Statement Quality: An Empirical Analysis Based on

Benford's Law. Voluntas: International Journal Of Voluntary & Nonprofit Organizations, 27,6,,

p.2685-2708, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Conde, S, Xu, X, Guo, H, Perola, M, Fazia, T, Bernardinelli, L, & Berzuini, C 2018), ‘Mendelian

randomization, analysis of clustered causal effects of body mass on cardiometabolic biomarkers,

BMC Bioinformatics, 13, p. 1-36, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Figlioli, B, Lemes, S, & Lima, F 2017,’ IFRS, synchronicity, and financial crisis: the dynamics

of accounting information for the Brazilian capital market, Revista Contabilidade & Finanças -

USP, 28,75, p.326-343, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Jaranowski, P, & Królak, A 2012,’ Gravitational-Wave Data Analysis. Formalism and Sample

Applications: The Gaussian Case, Living Reviews In Relativity, 15,4, p. 1-47, Academic Search

Premier, EBSCOhost, viewed 17 September 2018.

Khanna, P 2017,’A conceptual framework for achieving good governance at open and distance

learning institutions, Open Learning, 32,1,p. 21-35, Academic Search Premier, EBSCOhost,

viewed 17 September 2018.

List of References

Avram, C, B, Grosanu, A , & Rachisan, P 2015,’ Does country-level governance influence

auditing and financial reporting standards? Evidence from a cross-country analysis, Current

Science ,45, 4, p. 381-386,Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Caneghem, T 2016,’ NPO Financial Statement Quality: An Empirical Analysis Based on

Benford's Law. Voluntas: International Journal Of Voluntary & Nonprofit Organizations, 27,6,,

p.2685-2708, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Conde, S, Xu, X, Guo, H, Perola, M, Fazia, T, Bernardinelli, L, & Berzuini, C 2018), ‘Mendelian

randomization, analysis of clustered causal effects of body mass on cardiometabolic biomarkers,

BMC Bioinformatics, 13, p. 1-36, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Figlioli, B, Lemes, S, & Lima, F 2017,’ IFRS, synchronicity, and financial crisis: the dynamics

of accounting information for the Brazilian capital market, Revista Contabilidade & Finanças -

USP, 28,75, p.326-343, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Jaranowski, P, & Królak, A 2012,’ Gravitational-Wave Data Analysis. Formalism and Sample

Applications: The Gaussian Case, Living Reviews In Relativity, 15,4, p. 1-47, Academic Search

Premier, EBSCOhost, viewed 17 September 2018.

Khanna, P 2017,’A conceptual framework for achieving good governance at open and distance

learning institutions, Open Learning, 32,1,p. 21-35, Academic Search Premier, EBSCOhost,

viewed 17 September 2018.

Conceptual Framework in Accounting and Quality of Financial Reporting 12

Kılınç, H, & Fırat, M 2017, ‘Opinions of Expert Academicians on Online Data Collection and

Voluntary Participation in Social Sciences Research, Educational Sciences: Theory &

Practice, 17,5, p.1461-1486, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Krippendorff , K. 2018,’ Content Analysis: An Introduction to Its Methodology, SAGE

Publications, 106, 7, p. 1227-1240 , Academic Search Premier, EBSCOhost, viewed 17

September 2018.

Lai, K, & Kelley, K 2012, ‘Accuracy in parameter estimation for ANCOVA and ANOVA

contrasts: Sample size planning via narrow confidence intervals, British Journal Of

Mathematical & Statistical Psychology, 65,2, p.350-370, Academic Search Premier,

EBSCOhost, viewed 17 September 2018.

Pounder, B, 2013, ‘A Common Framework for Accounting Standards, Strategic Finance, 92,5,

p.20-61, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Rayman, A 2013.,’Accounting Standards: True or False? Routledge. Stata Journal, 16,3, p.650-

661, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Sinclair, R, & Bolt, R 2013,’ Third Sector Accounting Standard Setting: Do Third Sector

Stakeholders Have Voice?. Voluntas: International Journal Of Voluntary & Nonprofit

Organizations, 24,3, p.760-784, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Kılınç, H, & Fırat, M 2017, ‘Opinions of Expert Academicians on Online Data Collection and

Voluntary Participation in Social Sciences Research, Educational Sciences: Theory &

Practice, 17,5, p.1461-1486, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Krippendorff , K. 2018,’ Content Analysis: An Introduction to Its Methodology, SAGE

Publications, 106, 7, p. 1227-1240 , Academic Search Premier, EBSCOhost, viewed 17

September 2018.

Lai, K, & Kelley, K 2012, ‘Accuracy in parameter estimation for ANCOVA and ANOVA

contrasts: Sample size planning via narrow confidence intervals, British Journal Of

Mathematical & Statistical Psychology, 65,2, p.350-370, Academic Search Premier,

EBSCOhost, viewed 17 September 2018.

Pounder, B, 2013, ‘A Common Framework for Accounting Standards, Strategic Finance, 92,5,

p.20-61, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Rayman, A 2013.,’Accounting Standards: True or False? Routledge. Stata Journal, 16,3, p.650-

661, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Sinclair, R, & Bolt, R 2013,’ Third Sector Accounting Standard Setting: Do Third Sector

Stakeholders Have Voice?. Voluntas: International Journal Of Voluntary & Nonprofit

Organizations, 24,3, p.760-784, Academic Search Premier, EBSCOhost, viewed 17 September

2018.

Conceptual Framework in Accounting and Quality of Financial Reporting 13

Thomas, R, S, & Thompson, R, B 2012, ‘A Theory Of Representative Shareholder Suits And Its

Application To Multi Jurisdictional Litigation, Northwestern University Law Review, 106,4, p.

1753-1819, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Tribuzi, E, 2018, ‘The Inevitable United States Adoption of IFRS: How and Why the United

States Should Be Prepared, Indiana Journal Of Global Legal Studies, 25, 2, p.817-839,

Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Thomas, R, S, & Thompson, R, B 2012, ‘A Theory Of Representative Shareholder Suits And Its

Application To Multi Jurisdictional Litigation, Northwestern University Law Review, 106,4, p.

1753-1819, Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Tribuzi, E, 2018, ‘The Inevitable United States Adoption of IFRS: How and Why the United

States Should Be Prepared, Indiana Journal Of Global Legal Studies, 25, 2, p.817-839,

Academic Search Premier, EBSCOhost, viewed 17 September 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conceptual Framework in Accounting and Quality of Financial Reporting 14

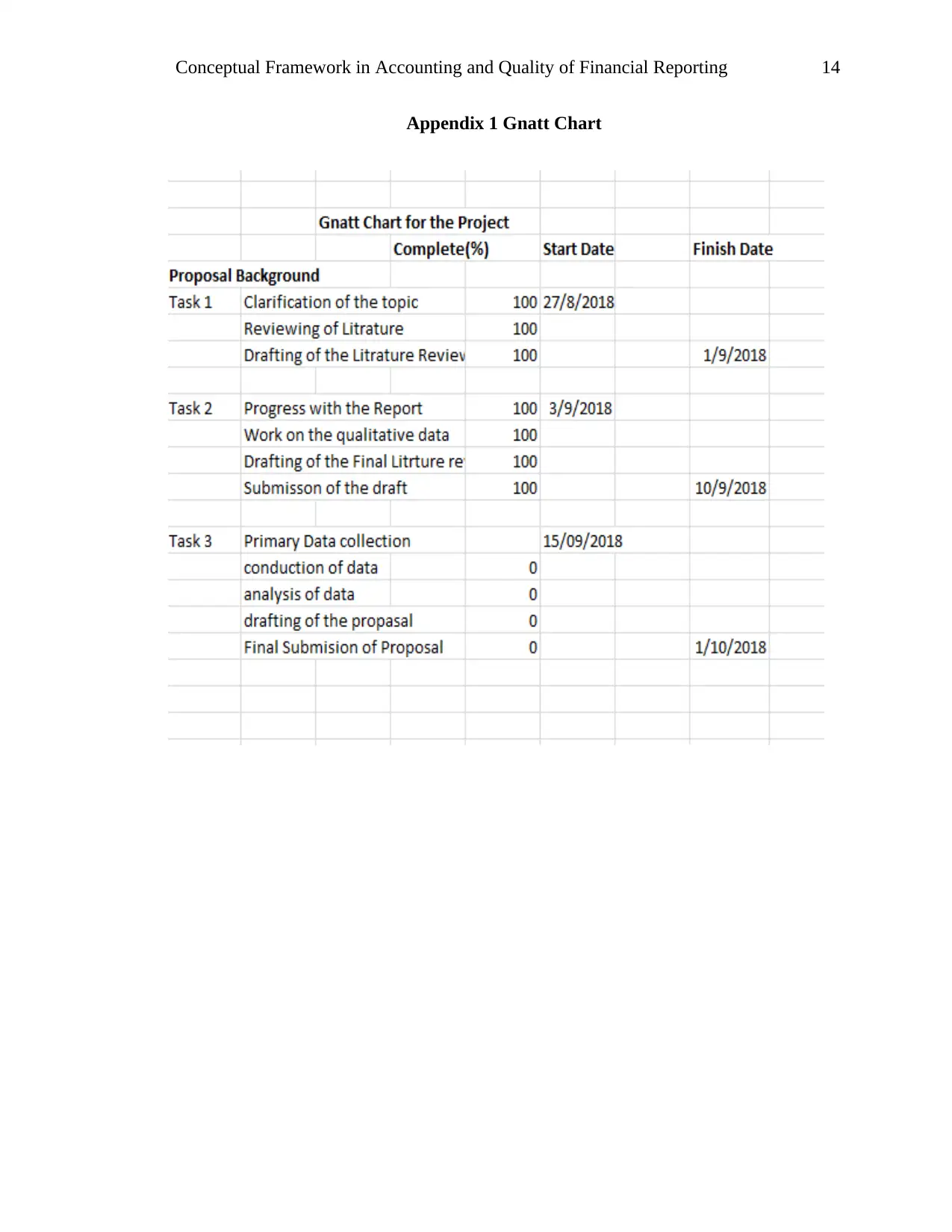

Appendix 1 Gnatt Chart

Appendix 1 Gnatt Chart

Conceptual Framework in Accounting and Quality of Financial Reporting 15

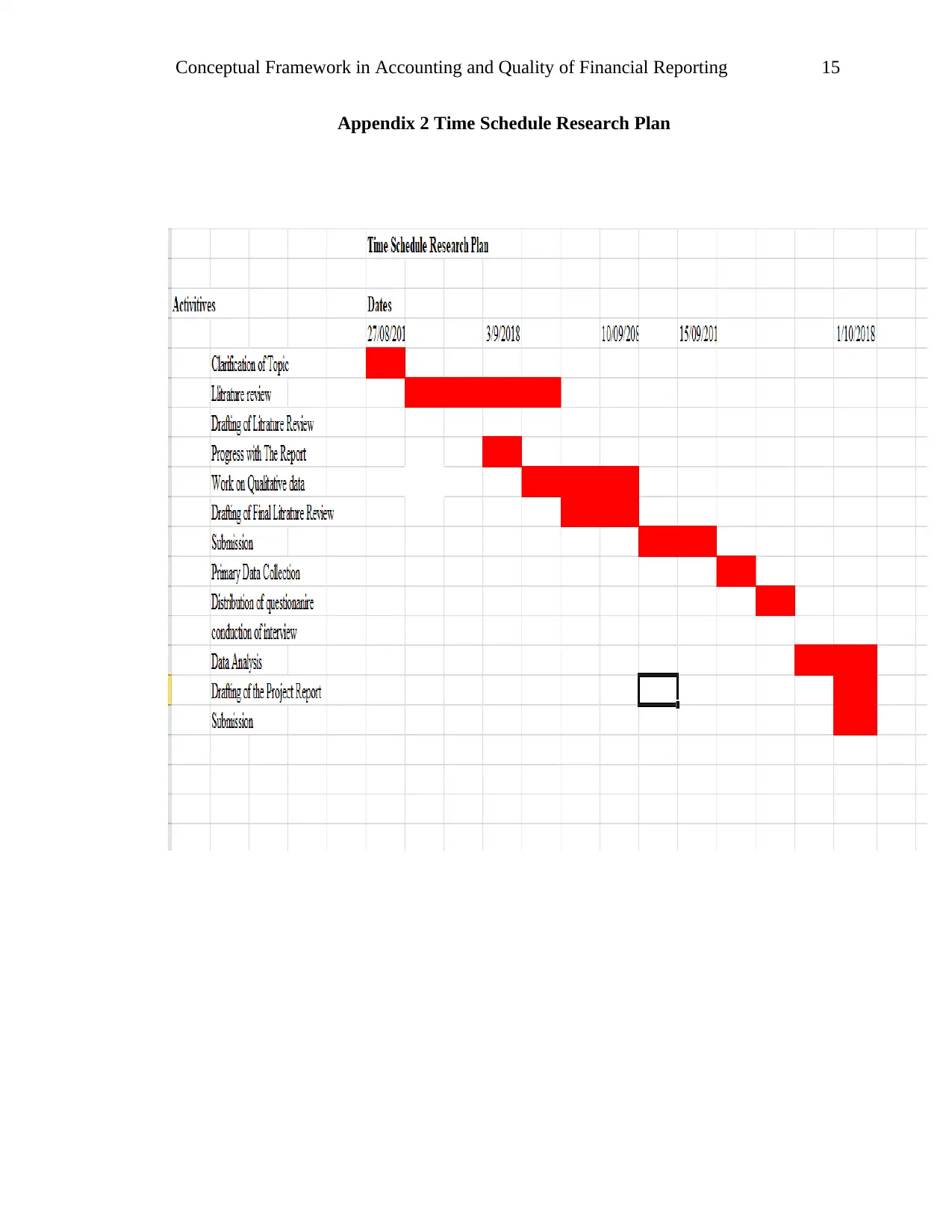

Appendix 2 Time Schedule Research Plan

Appendix 2 Time Schedule Research Plan

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.