Report on Contemporary Accounting Issues: Anchor Resources Limited

VerifiedAdded on 2023/05/27

|17

|2540

|313

Report

AI Summary

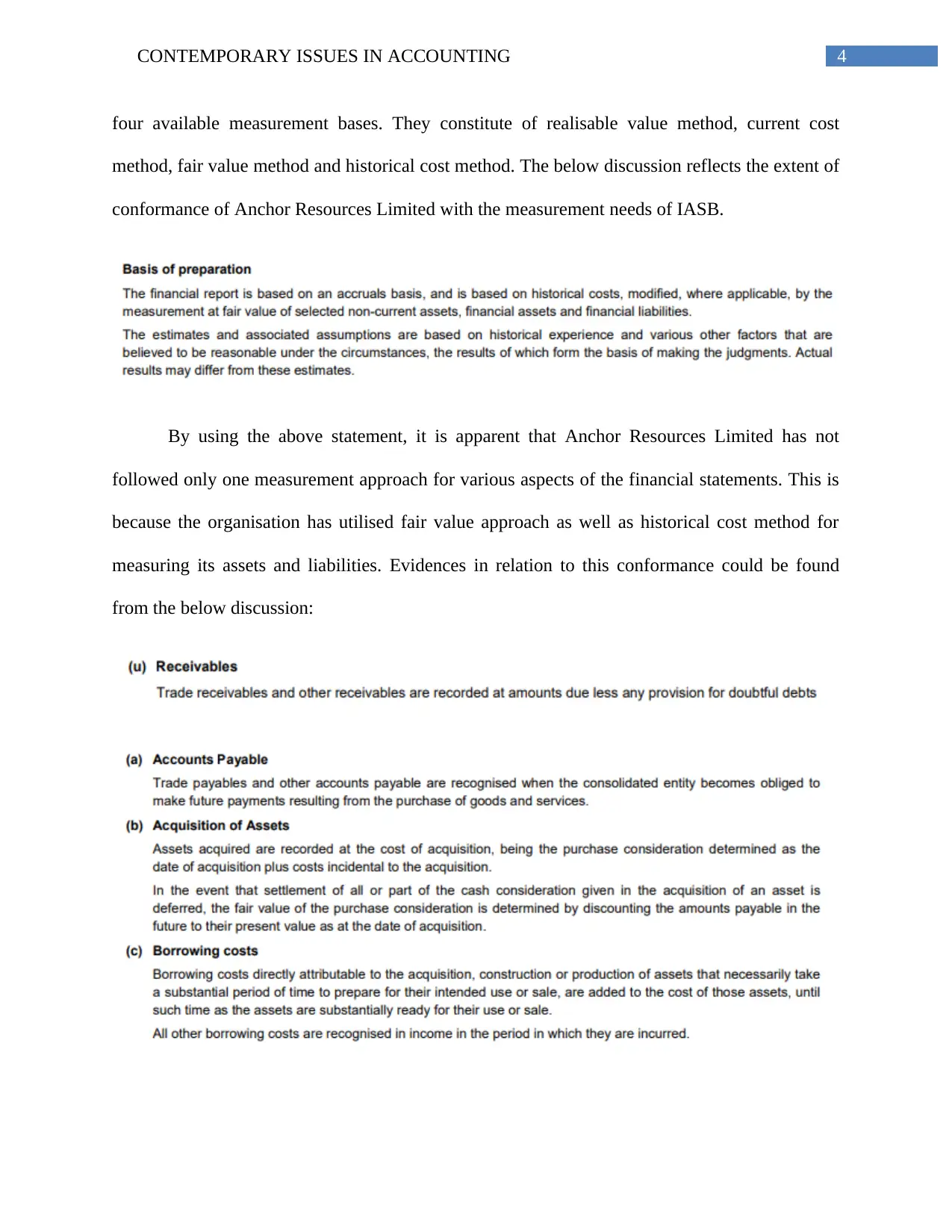

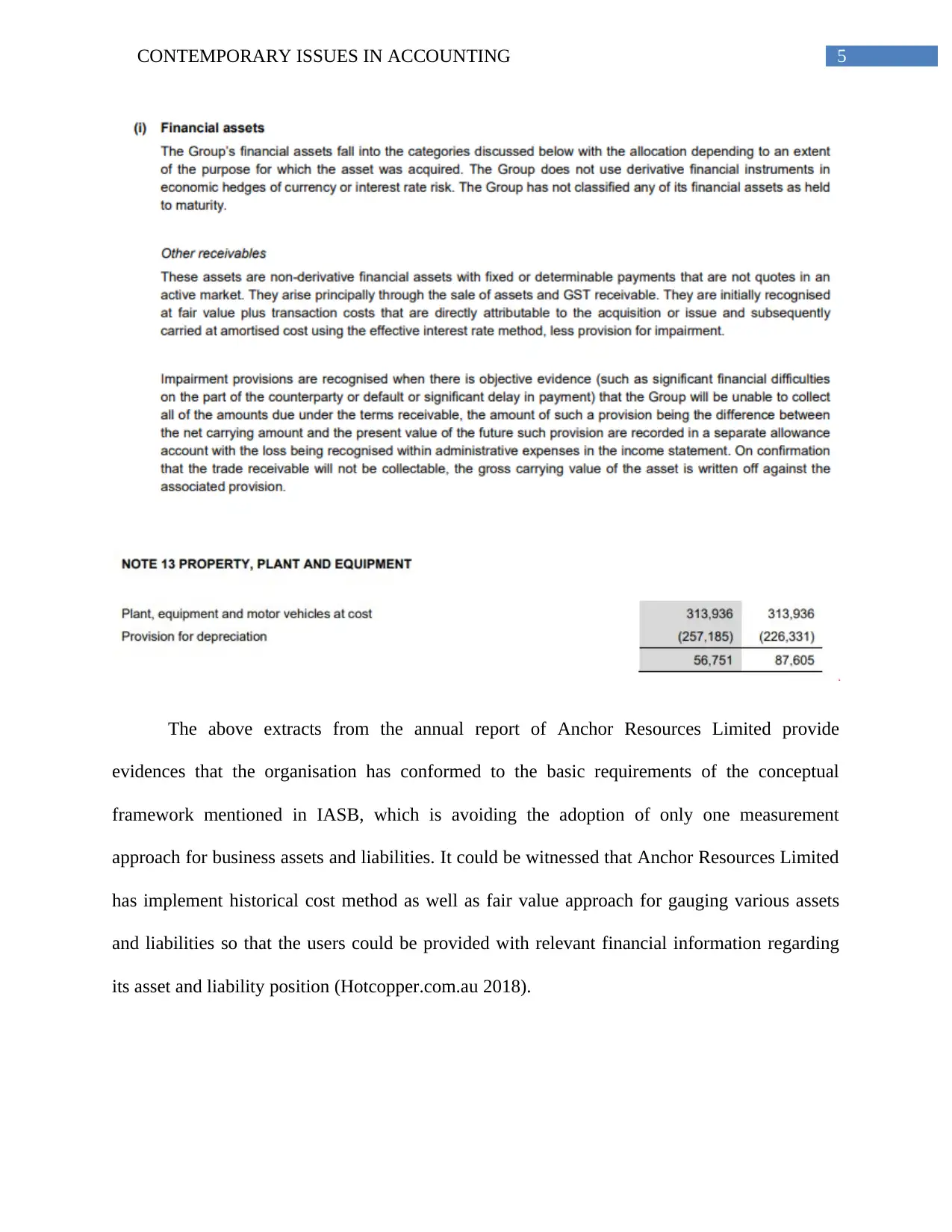

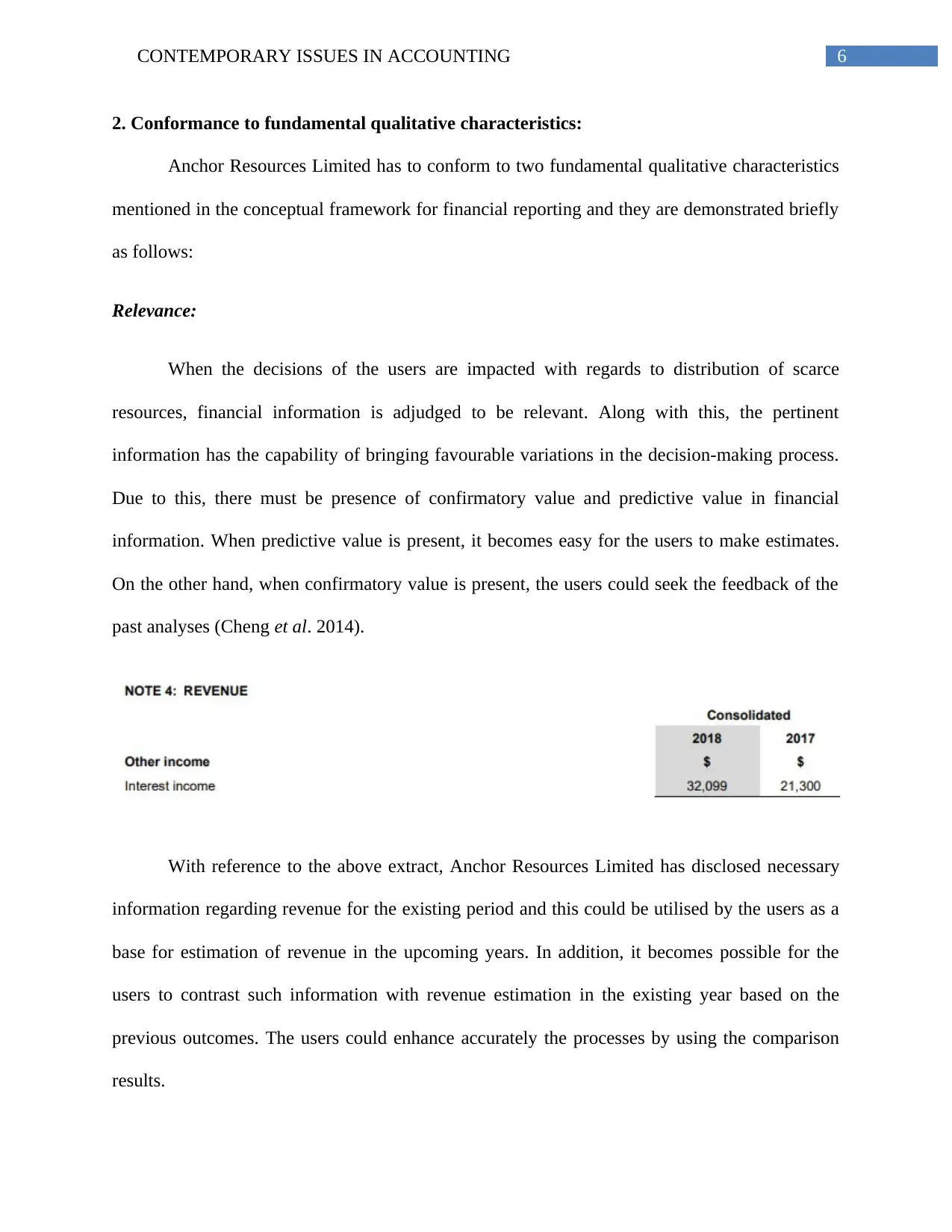

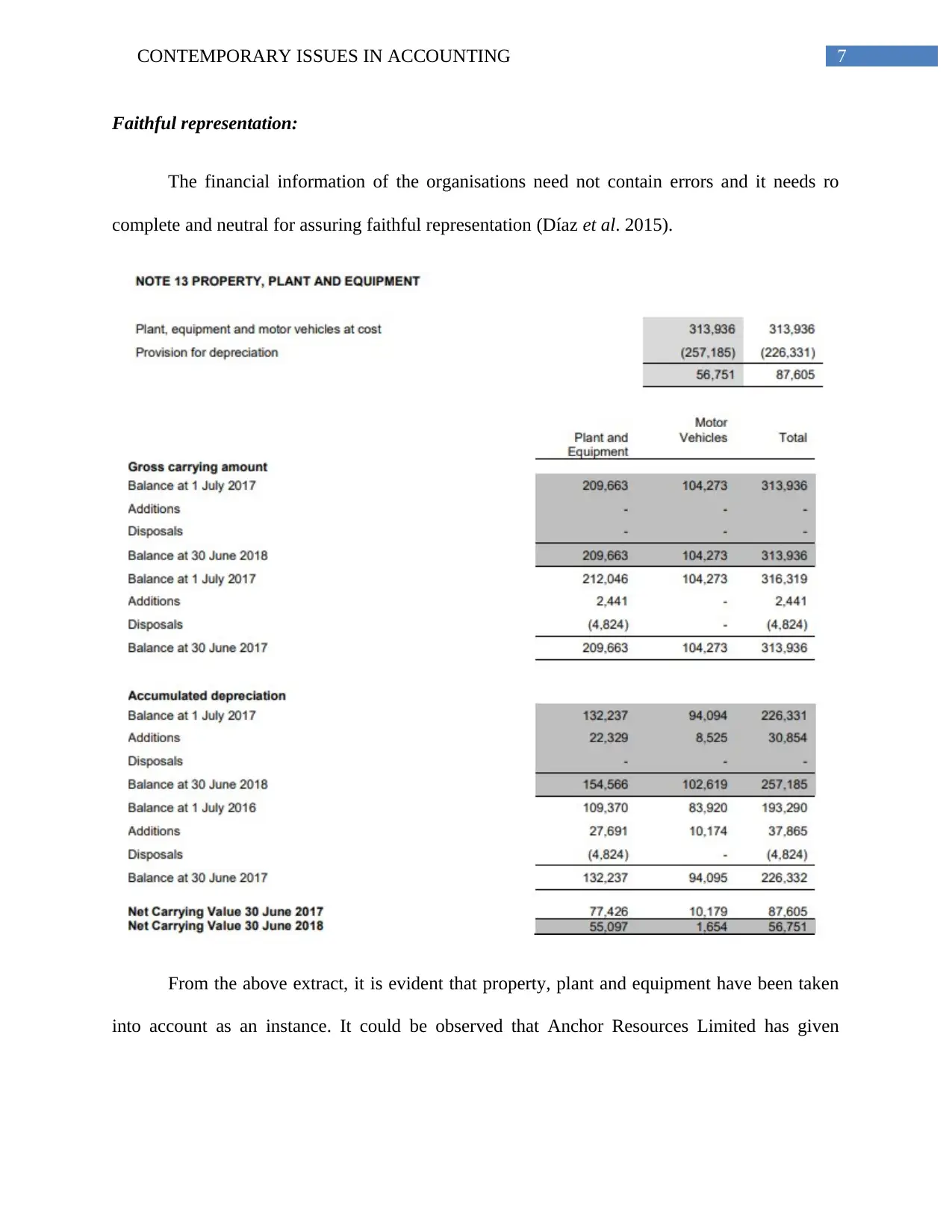

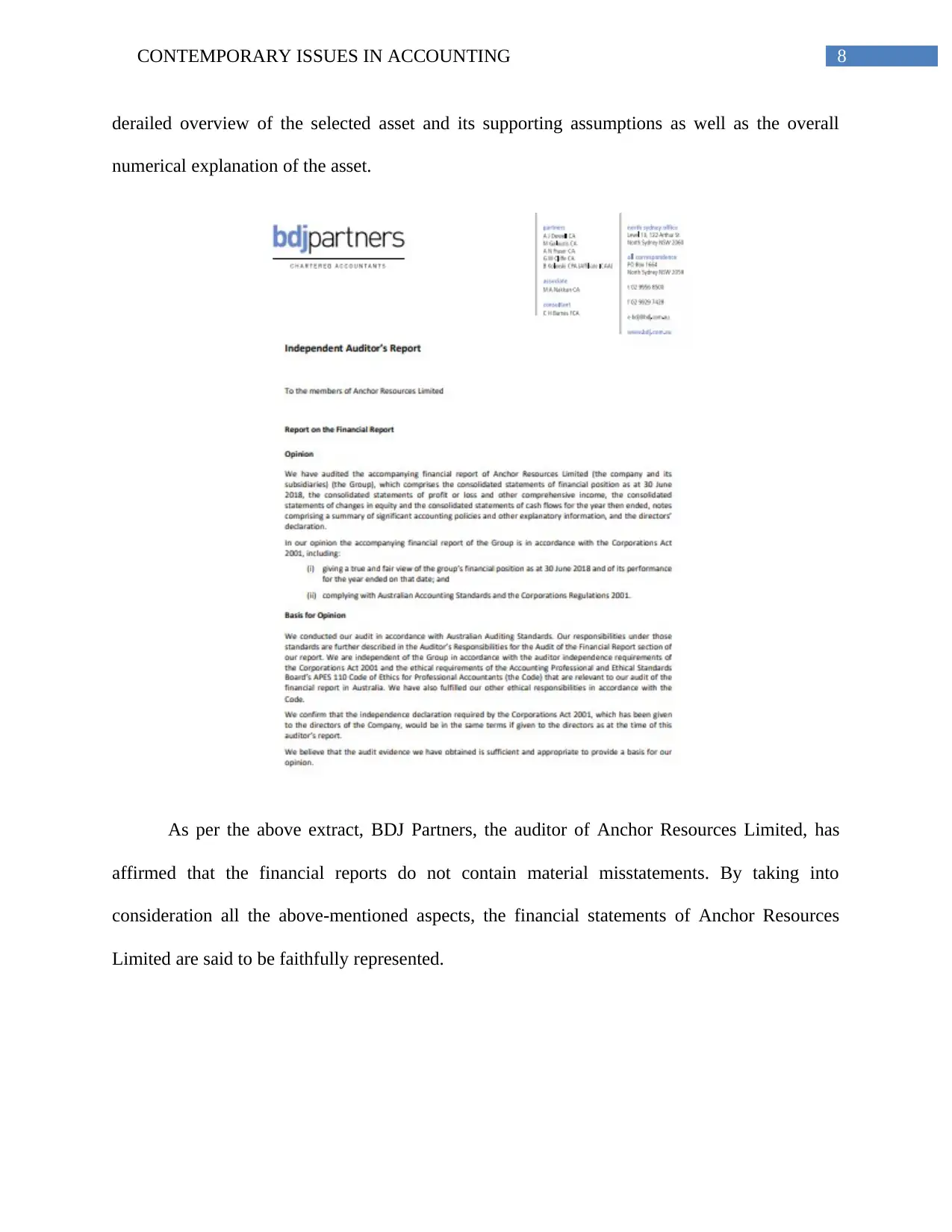

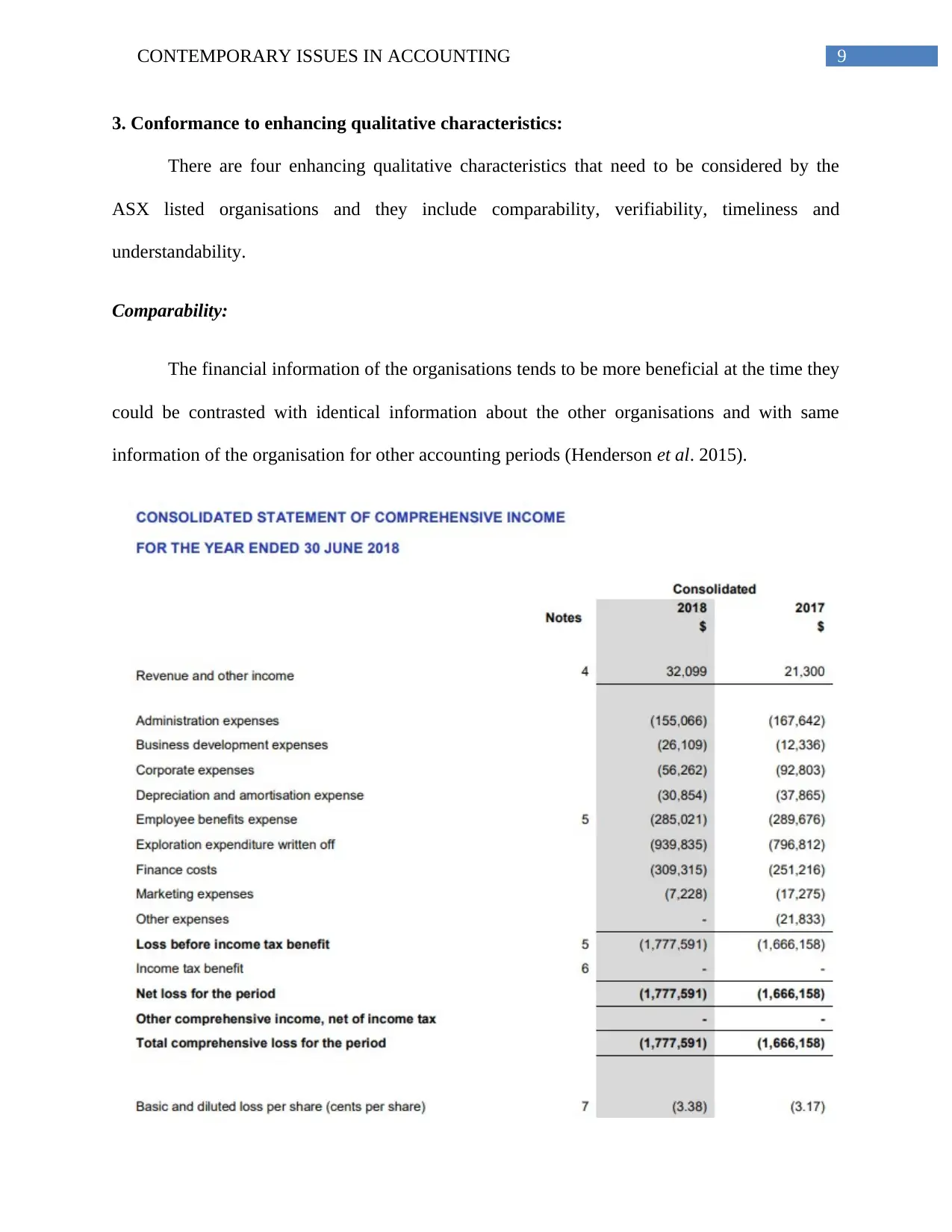

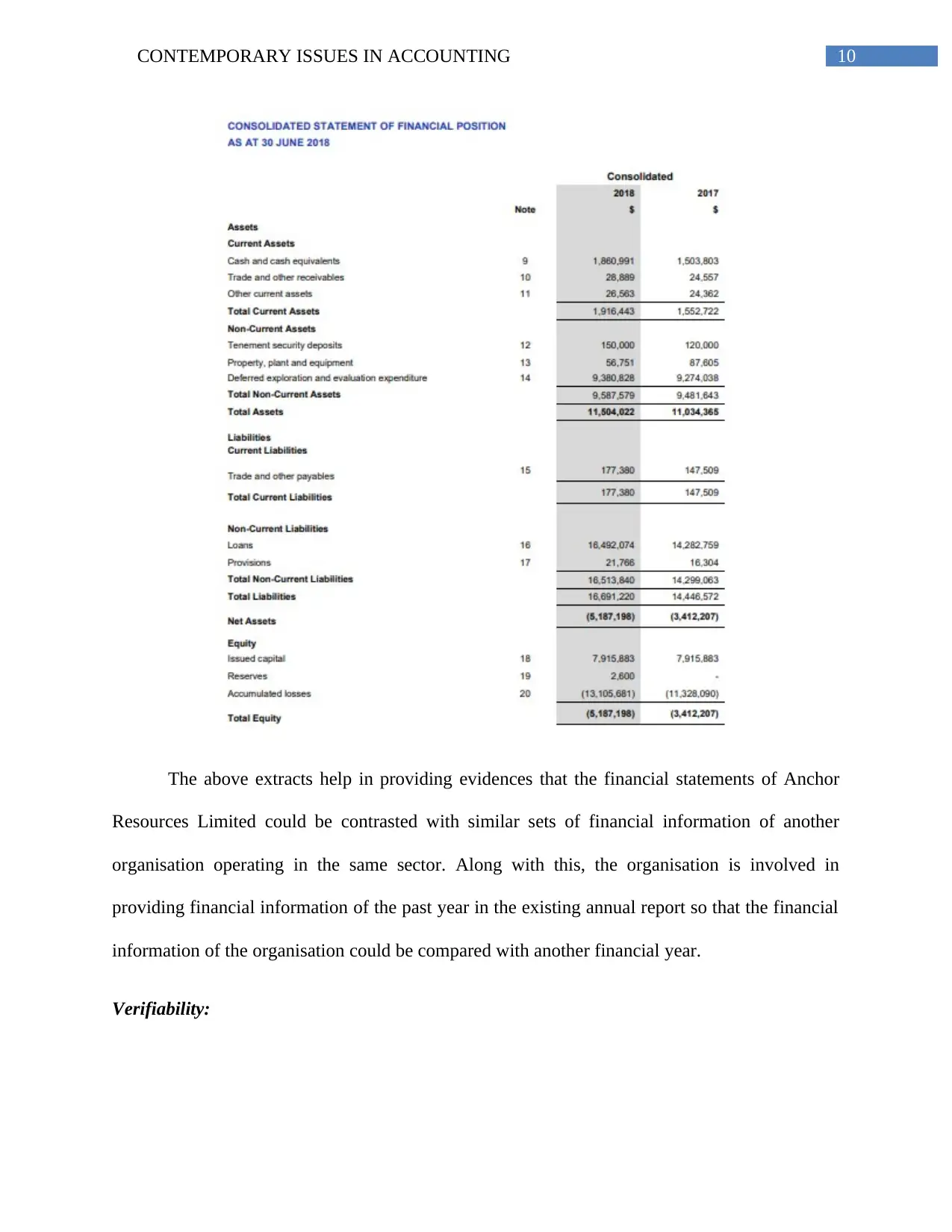

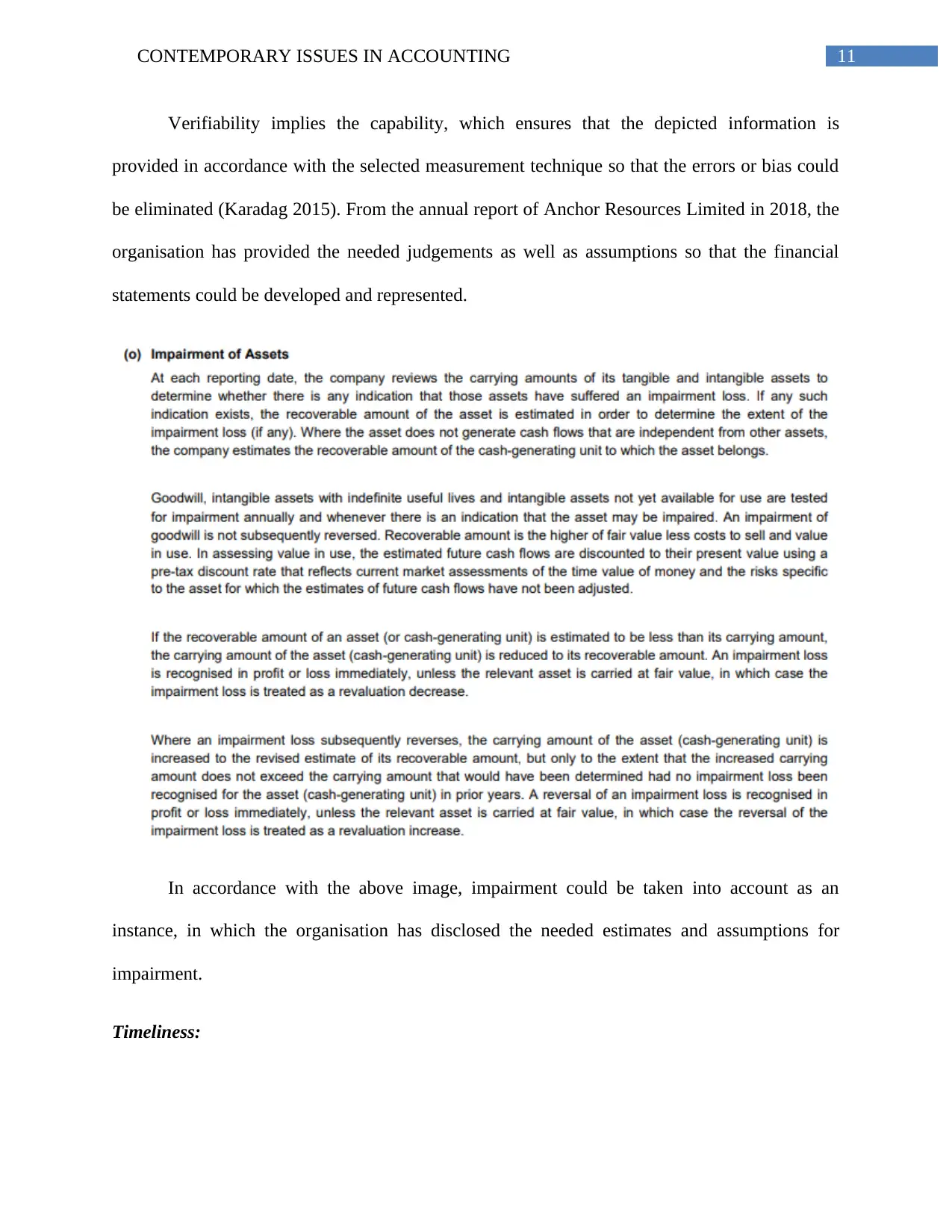

This report provides an in-depth analysis of contemporary issues in accounting, specifically focusing on how an ASX-listed organization, Anchor Resources Limited, conforms to the guidelines of the conceptual framework for financial reporting. The report examines the company's adherence to measurement requirements, fundamental and enhancing qualitative characteristics, and general-purpose financial reporting requirements. It explores how the company utilizes different measurement bases for assets and liabilities, ensuring relevance and faithful representation in its financial statements. The report also assesses the ability of financial statement users to make informed decisions based on the information provided, including the availability of financial statements like income statements, cash flow statements, and statements of changes in equity. The conclusion highlights that Anchor Resources Limited adheres to the conceptual framework by employing a mix of historical cost and fair value methods and disclosing all necessary financial statements to facilitate informed decision-making by investors and creditors.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.