Consolidated Financial Statements: Preparation and Evaluation

VerifiedAdded on 2023/06/18

|11

|1625

|228

AI Summary

This article discusses the preparation and evaluation of consolidated financial statements with solved examples. It covers topics such as the importance of consolidation, calculation of goodwill and non-controlling interest, and the preparation of a consolidated balance sheet. The subject is relevant for courses in accounting and finance, and the content is suitable for students at the college and university level.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Online Exam

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................8

QUESTION 3...................................................................................................................................9

REFERENCES..............................................................................................................................11

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................8

QUESTION 3...................................................................................................................................9

REFERENCES..............................................................................................................................11

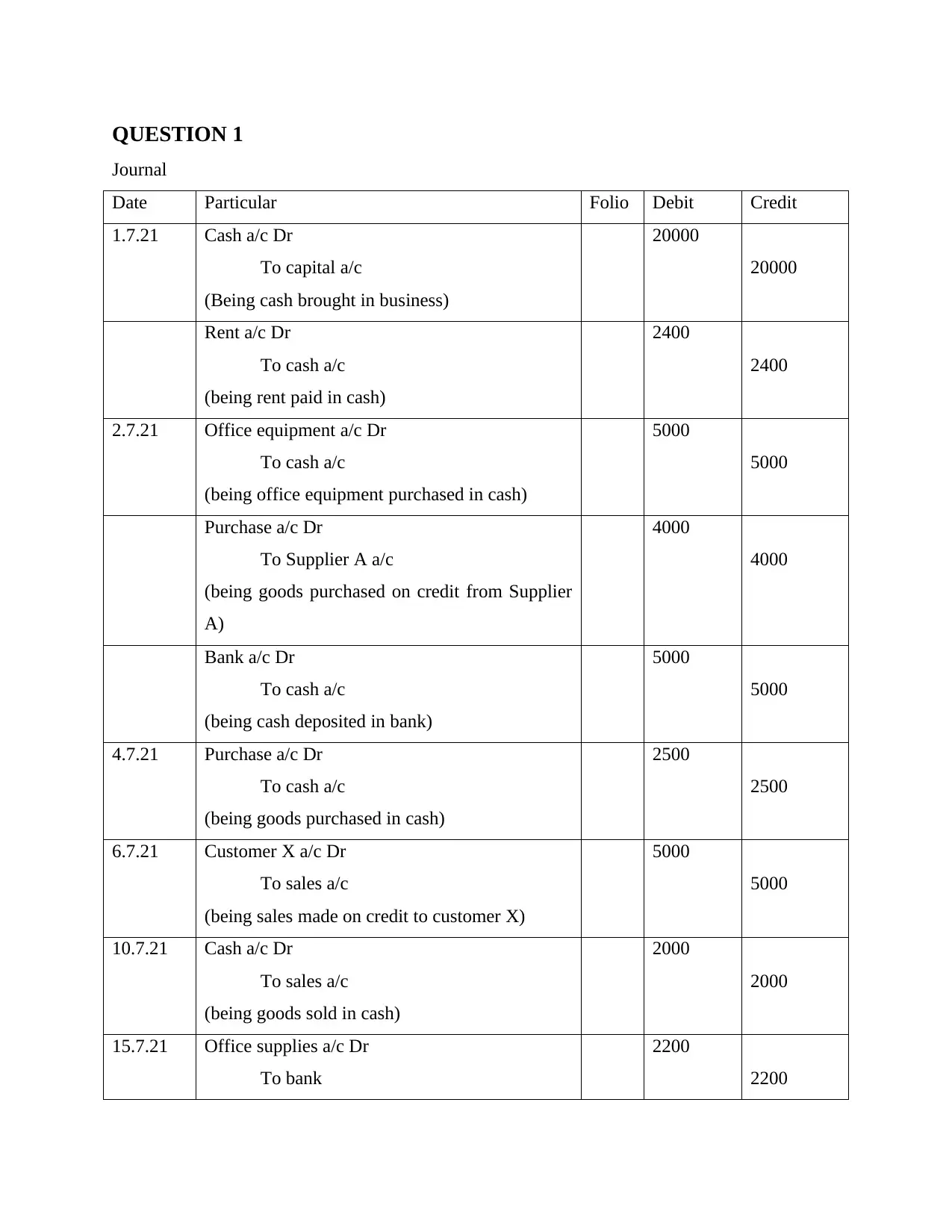

QUESTION 1

Journal

Date Particular Folio Debit Credit

1.7.21 Cash a/c Dr

To capital a/c

(Being cash brought in business)

20000

20000

Rent a/c Dr

To cash a/c

(being rent paid in cash)

2400

2400

2.7.21 Office equipment a/c Dr

To cash a/c

(being office equipment purchased in cash)

5000

5000

Purchase a/c Dr

To Supplier A a/c

(being goods purchased on credit from Supplier

A)

4000

4000

Bank a/c Dr

To cash a/c

(being cash deposited in bank)

5000

5000

4.7.21 Purchase a/c Dr

To cash a/c

(being goods purchased in cash)

2500

2500

6.7.21 Customer X a/c Dr

To sales a/c

(being sales made on credit to customer X)

5000

5000

10.7.21 Cash a/c Dr

To sales a/c

(being goods sold in cash)

2000

2000

15.7.21 Office supplies a/c Dr

To bank

2200

2200

Journal

Date Particular Folio Debit Credit

1.7.21 Cash a/c Dr

To capital a/c

(Being cash brought in business)

20000

20000

Rent a/c Dr

To cash a/c

(being rent paid in cash)

2400

2400

2.7.21 Office equipment a/c Dr

To cash a/c

(being office equipment purchased in cash)

5000

5000

Purchase a/c Dr

To Supplier A a/c

(being goods purchased on credit from Supplier

A)

4000

4000

Bank a/c Dr

To cash a/c

(being cash deposited in bank)

5000

5000

4.7.21 Purchase a/c Dr

To cash a/c

(being goods purchased in cash)

2500

2500

6.7.21 Customer X a/c Dr

To sales a/c

(being sales made on credit to customer X)

5000

5000

10.7.21 Cash a/c Dr

To sales a/c

(being goods sold in cash)

2000

2000

15.7.21 Office supplies a/c Dr

To bank

2200

2200

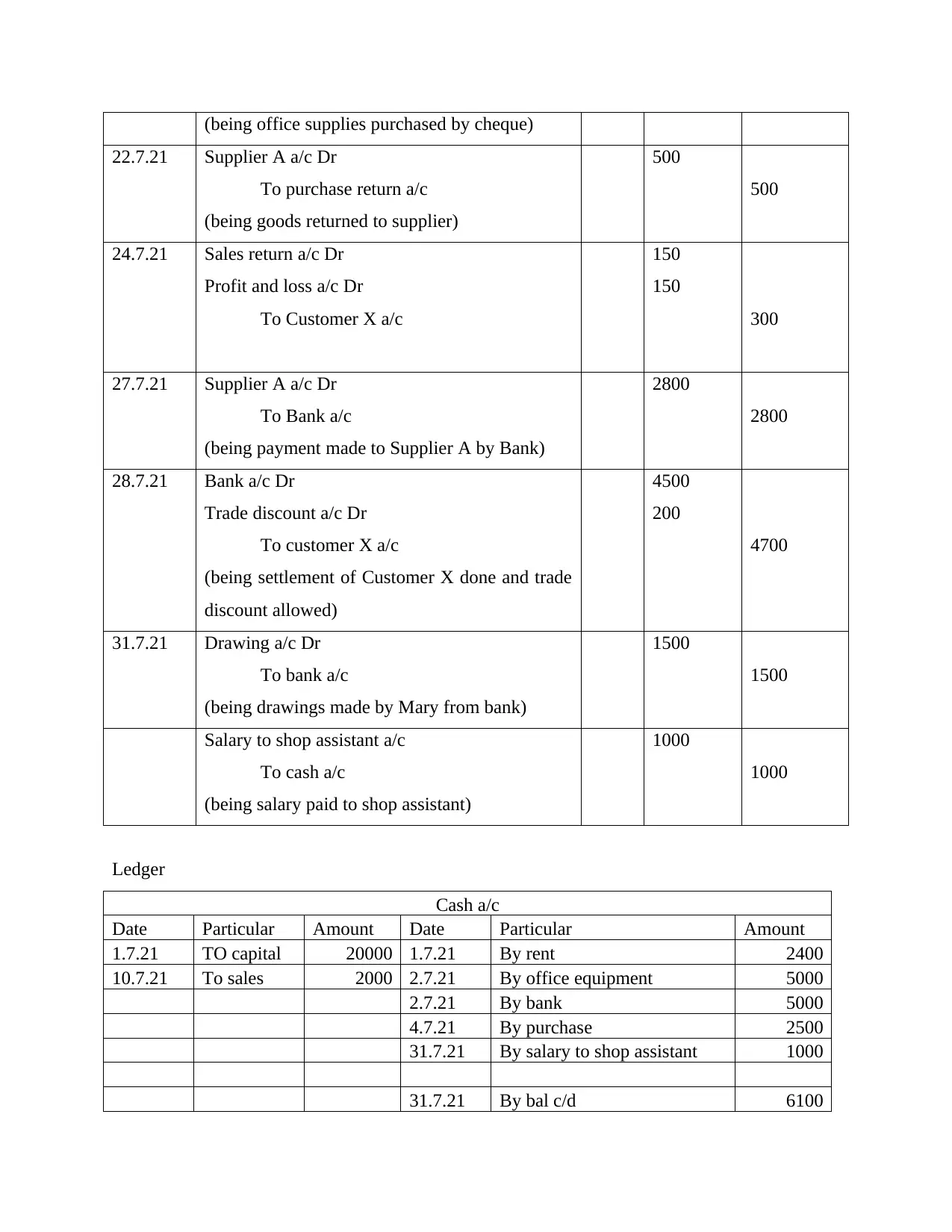

(being office supplies purchased by cheque)

22.7.21 Supplier A a/c Dr

To purchase return a/c

(being goods returned to supplier)

500

500

24.7.21 Sales return a/c Dr

Profit and loss a/c Dr

To Customer X a/c

150

150

300

27.7.21 Supplier A a/c Dr

To Bank a/c

(being payment made to Supplier A by Bank)

2800

2800

28.7.21 Bank a/c Dr

Trade discount a/c Dr

To customer X a/c

(being settlement of Customer X done and trade

discount allowed)

4500

200

4700

31.7.21 Drawing a/c Dr

To bank a/c

(being drawings made by Mary from bank)

1500

1500

Salary to shop assistant a/c

To cash a/c

(being salary paid to shop assistant)

1000

1000

Ledger

Cash a/c

Date Particular Amount Date Particular Amount

1.7.21 TO capital 20000 1.7.21 By rent 2400

10.7.21 To sales 2000 2.7.21 By office equipment 5000

2.7.21 By bank 5000

4.7.21 By purchase 2500

31.7.21 By salary to shop assistant 1000

31.7.21 By bal c/d 6100

22.7.21 Supplier A a/c Dr

To purchase return a/c

(being goods returned to supplier)

500

500

24.7.21 Sales return a/c Dr

Profit and loss a/c Dr

To Customer X a/c

150

150

300

27.7.21 Supplier A a/c Dr

To Bank a/c

(being payment made to Supplier A by Bank)

2800

2800

28.7.21 Bank a/c Dr

Trade discount a/c Dr

To customer X a/c

(being settlement of Customer X done and trade

discount allowed)

4500

200

4700

31.7.21 Drawing a/c Dr

To bank a/c

(being drawings made by Mary from bank)

1500

1500

Salary to shop assistant a/c

To cash a/c

(being salary paid to shop assistant)

1000

1000

Ledger

Cash a/c

Date Particular Amount Date Particular Amount

1.7.21 TO capital 20000 1.7.21 By rent 2400

10.7.21 To sales 2000 2.7.21 By office equipment 5000

2.7.21 By bank 5000

4.7.21 By purchase 2500

31.7.21 By salary to shop assistant 1000

31.7.21 By bal c/d 6100

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

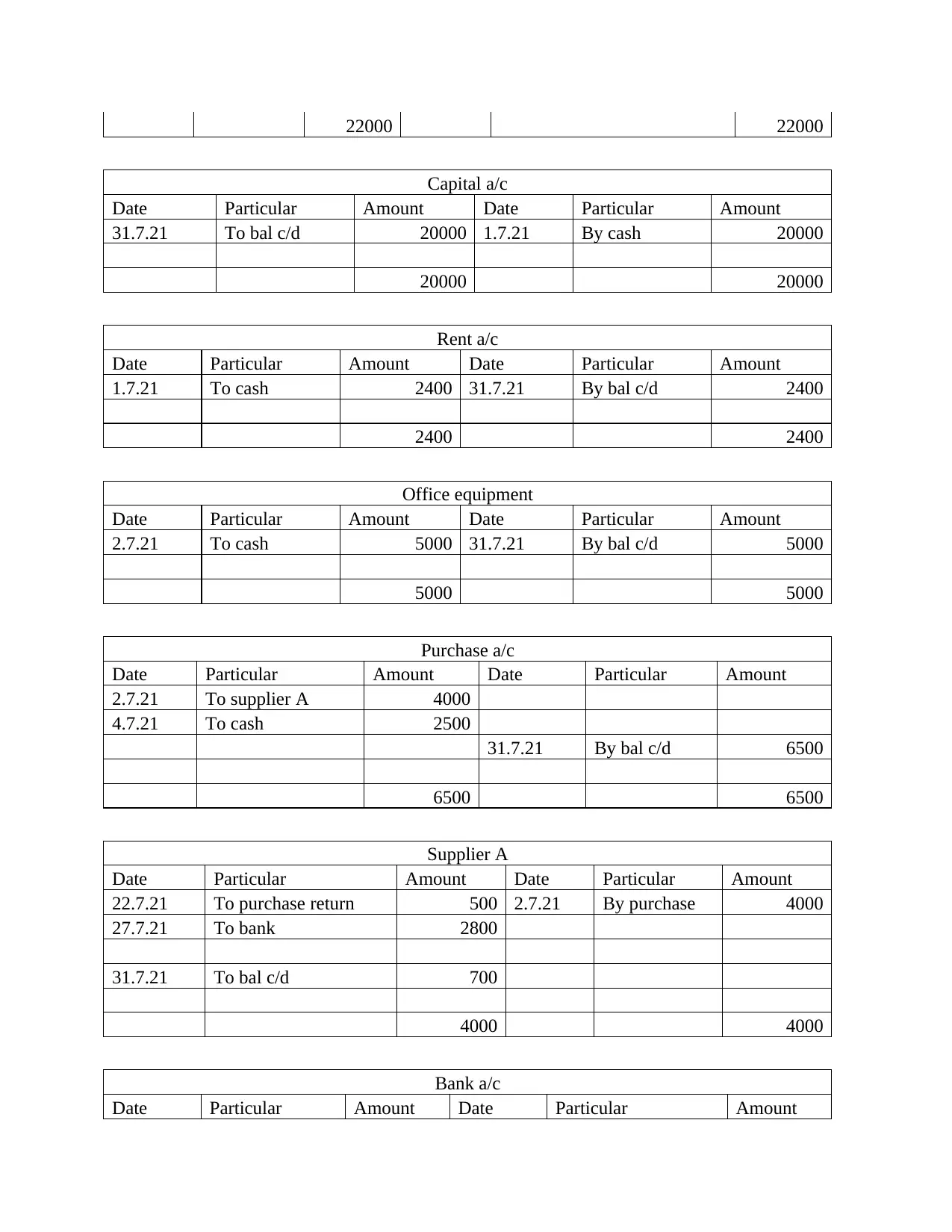

22000 22000

Capital a/c

Date Particular Amount Date Particular Amount

31.7.21 To bal c/d 20000 1.7.21 By cash 20000

20000 20000

Rent a/c

Date Particular Amount Date Particular Amount

1.7.21 To cash 2400 31.7.21 By bal c/d 2400

2400 2400

Office equipment

Date Particular Amount Date Particular Amount

2.7.21 To cash 5000 31.7.21 By bal c/d 5000

5000 5000

Purchase a/c

Date Particular Amount Date Particular Amount

2.7.21 To supplier A 4000

4.7.21 To cash 2500

31.7.21 By bal c/d 6500

6500 6500

Supplier A

Date Particular Amount Date Particular Amount

22.7.21 To purchase return 500 2.7.21 By purchase 4000

27.7.21 To bank 2800

31.7.21 To bal c/d 700

4000 4000

Bank a/c

Date Particular Amount Date Particular Amount

Capital a/c

Date Particular Amount Date Particular Amount

31.7.21 To bal c/d 20000 1.7.21 By cash 20000

20000 20000

Rent a/c

Date Particular Amount Date Particular Amount

1.7.21 To cash 2400 31.7.21 By bal c/d 2400

2400 2400

Office equipment

Date Particular Amount Date Particular Amount

2.7.21 To cash 5000 31.7.21 By bal c/d 5000

5000 5000

Purchase a/c

Date Particular Amount Date Particular Amount

2.7.21 To supplier A 4000

4.7.21 To cash 2500

31.7.21 By bal c/d 6500

6500 6500

Supplier A

Date Particular Amount Date Particular Amount

22.7.21 To purchase return 500 2.7.21 By purchase 4000

27.7.21 To bank 2800

31.7.21 To bal c/d 700

4000 4000

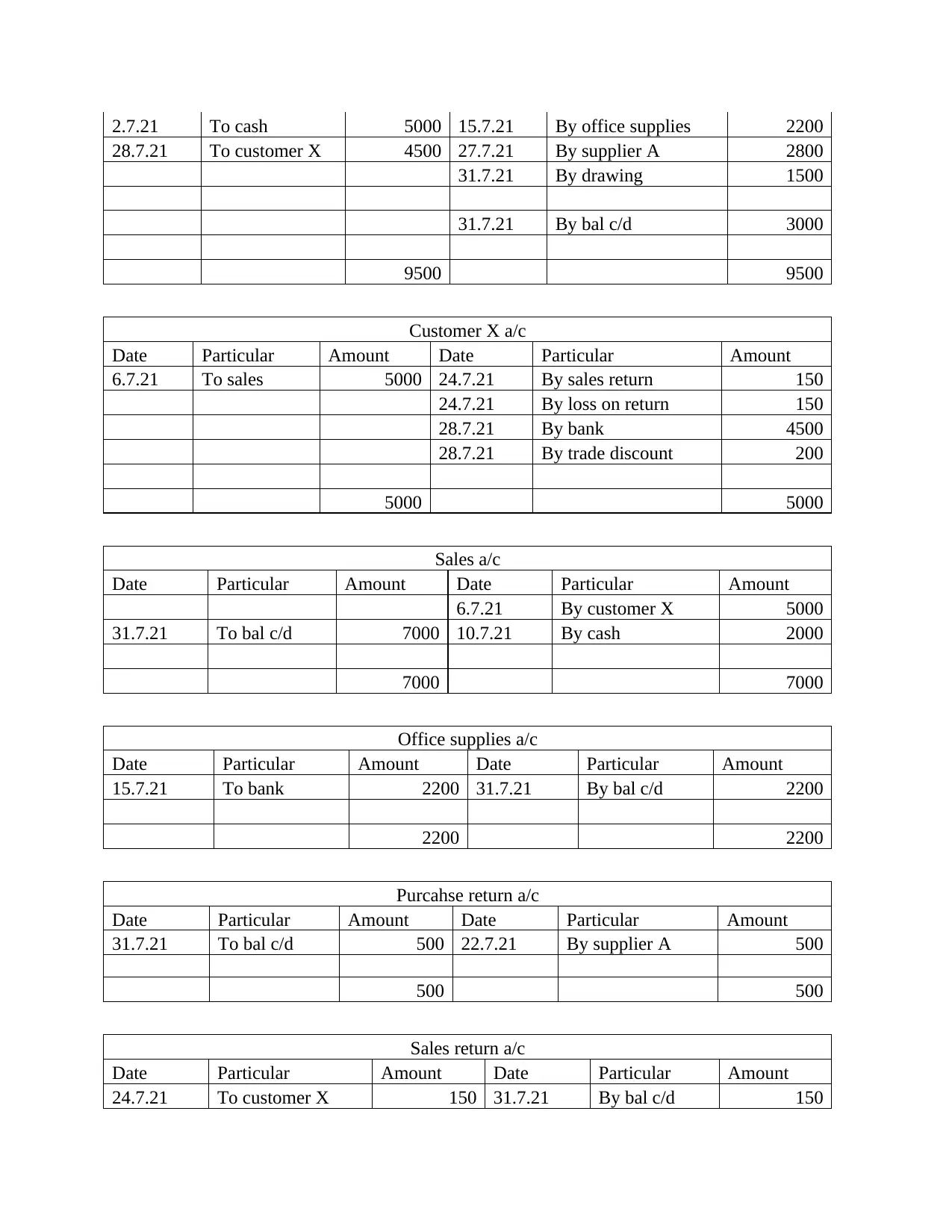

Bank a/c

Date Particular Amount Date Particular Amount

2.7.21 To cash 5000 15.7.21 By office supplies 2200

28.7.21 To customer X 4500 27.7.21 By supplier A 2800

31.7.21 By drawing 1500

31.7.21 By bal c/d 3000

9500 9500

Customer X a/c

Date Particular Amount Date Particular Amount

6.7.21 To sales 5000 24.7.21 By sales return 150

24.7.21 By loss on return 150

28.7.21 By bank 4500

28.7.21 By trade discount 200

5000 5000

Sales a/c

Date Particular Amount Date Particular Amount

6.7.21 By customer X 5000

31.7.21 To bal c/d 7000 10.7.21 By cash 2000

7000 7000

Office supplies a/c

Date Particular Amount Date Particular Amount

15.7.21 To bank 2200 31.7.21 By bal c/d 2200

2200 2200

Purcahse return a/c

Date Particular Amount Date Particular Amount

31.7.21 To bal c/d 500 22.7.21 By supplier A 500

500 500

Sales return a/c

Date Particular Amount Date Particular Amount

24.7.21 To customer X 150 31.7.21 By bal c/d 150

28.7.21 To customer X 4500 27.7.21 By supplier A 2800

31.7.21 By drawing 1500

31.7.21 By bal c/d 3000

9500 9500

Customer X a/c

Date Particular Amount Date Particular Amount

6.7.21 To sales 5000 24.7.21 By sales return 150

24.7.21 By loss on return 150

28.7.21 By bank 4500

28.7.21 By trade discount 200

5000 5000

Sales a/c

Date Particular Amount Date Particular Amount

6.7.21 By customer X 5000

31.7.21 To bal c/d 7000 10.7.21 By cash 2000

7000 7000

Office supplies a/c

Date Particular Amount Date Particular Amount

15.7.21 To bank 2200 31.7.21 By bal c/d 2200

2200 2200

Purcahse return a/c

Date Particular Amount Date Particular Amount

31.7.21 To bal c/d 500 22.7.21 By supplier A 500

500 500

Sales return a/c

Date Particular Amount Date Particular Amount

24.7.21 To customer X 150 31.7.21 By bal c/d 150

150 150

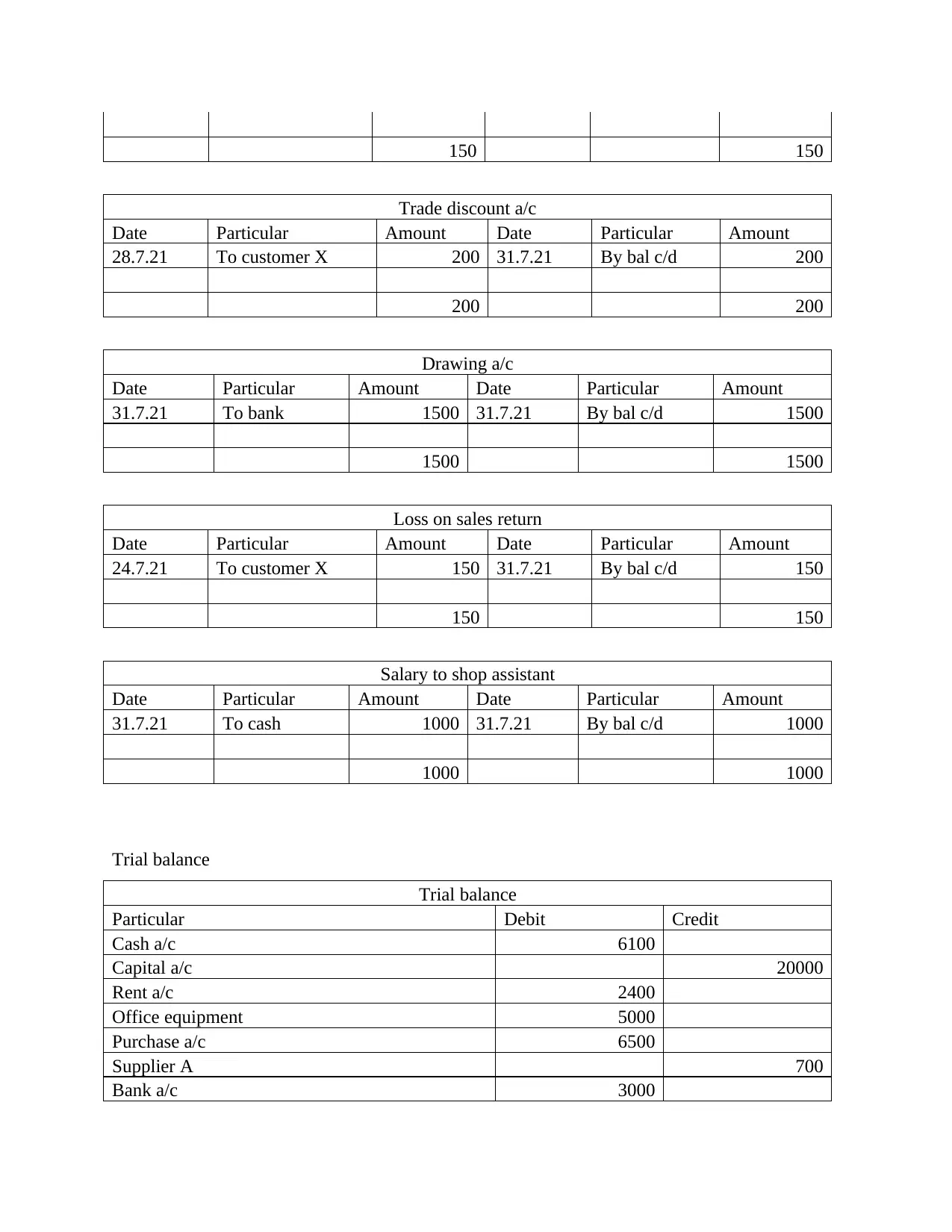

Trade discount a/c

Date Particular Amount Date Particular Amount

28.7.21 To customer X 200 31.7.21 By bal c/d 200

200 200

Drawing a/c

Date Particular Amount Date Particular Amount

31.7.21 To bank 1500 31.7.21 By bal c/d 1500

1500 1500

Loss on sales return

Date Particular Amount Date Particular Amount

24.7.21 To customer X 150 31.7.21 By bal c/d 150

150 150

Salary to shop assistant

Date Particular Amount Date Particular Amount

31.7.21 To cash 1000 31.7.21 By bal c/d 1000

1000 1000

Trial balance

Trial balance

Particular Debit Credit

Cash a/c 6100

Capital a/c 20000

Rent a/c 2400

Office equipment 5000

Purchase a/c 6500

Supplier A 700

Bank a/c 3000

Trade discount a/c

Date Particular Amount Date Particular Amount

28.7.21 To customer X 200 31.7.21 By bal c/d 200

200 200

Drawing a/c

Date Particular Amount Date Particular Amount

31.7.21 To bank 1500 31.7.21 By bal c/d 1500

1500 1500

Loss on sales return

Date Particular Amount Date Particular Amount

24.7.21 To customer X 150 31.7.21 By bal c/d 150

150 150

Salary to shop assistant

Date Particular Amount Date Particular Amount

31.7.21 To cash 1000 31.7.21 By bal c/d 1000

1000 1000

Trial balance

Trial balance

Particular Debit Credit

Cash a/c 6100

Capital a/c 20000

Rent a/c 2400

Office equipment 5000

Purchase a/c 6500

Supplier A 700

Bank a/c 3000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loss on sales return 150

Sales a/c 7000

Office supplies a/c 2200

Purchase return a/c 500

Sales return a/c 150

Trade discount a/c 200

Drawing a/c 1500

Salary to shop assistant 1000

Total 28200 28200

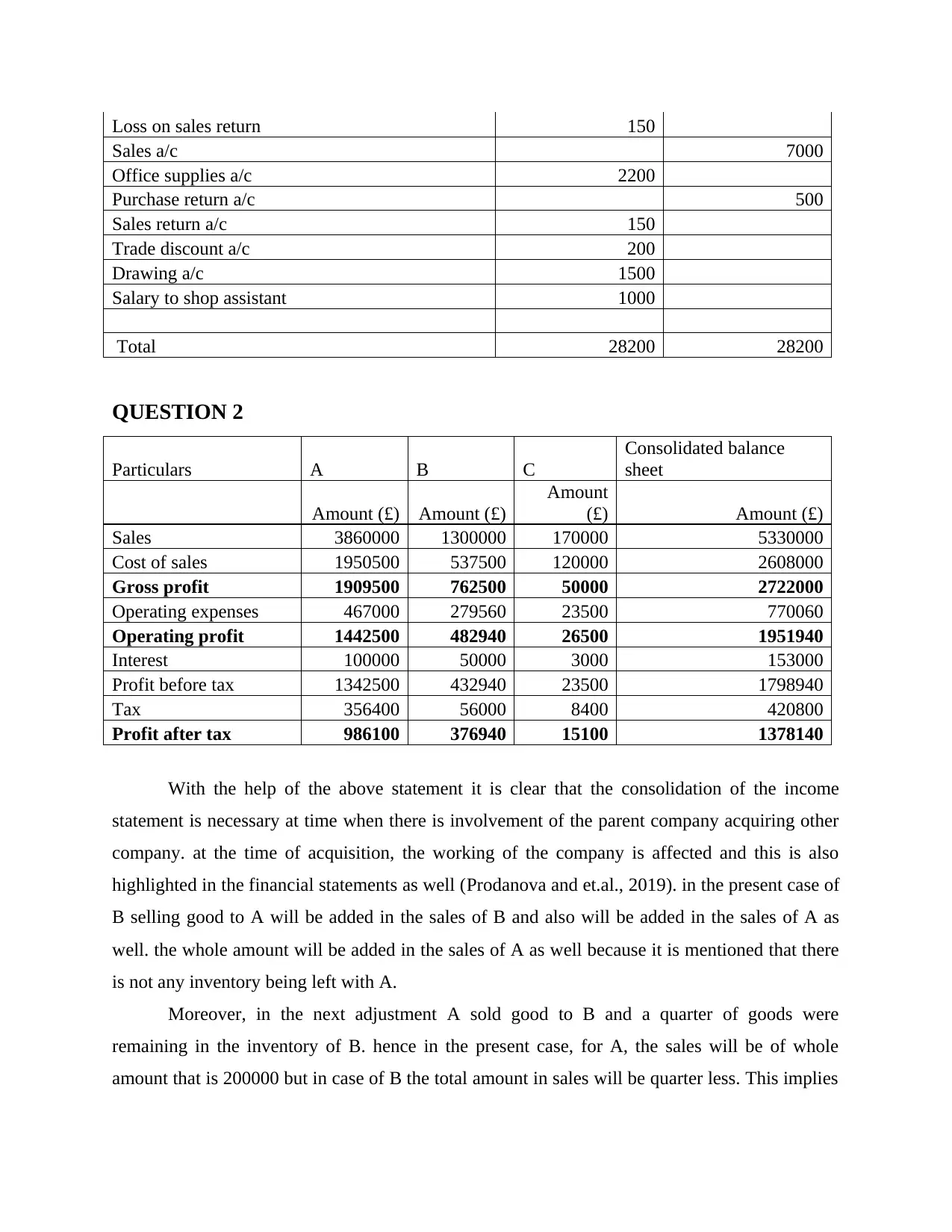

QUESTION 2

Particulars A B C

Consolidated balance

sheet

Amount (£) Amount (£)

Amount

(£) Amount (£)

Sales 3860000 1300000 170000 5330000

Cost of sales 1950500 537500 120000 2608000

Gross profit 1909500 762500 50000 2722000

Operating expenses 467000 279560 23500 770060

Operating profit 1442500 482940 26500 1951940

Interest 100000 50000 3000 153000

Profit before tax 1342500 432940 23500 1798940

Tax 356400 56000 8400 420800

Profit after tax 986100 376940 15100 1378140

With the help of the above statement it is clear that the consolidation of the income

statement is necessary at time when there is involvement of the parent company acquiring other

company. at the time of acquisition, the working of the company is affected and this is also

highlighted in the financial statements as well (Prodanova and et.al., 2019). in the present case of

B selling good to A will be added in the sales of B and also will be added in the sales of A as

well. the whole amount will be added in the sales of A as well because it is mentioned that there

is not any inventory being left with A.

Moreover, in the next adjustment A sold good to B and a quarter of goods were

remaining in the inventory of B. hence in the present case, for A, the sales will be of whole

amount that is 200000 but in case of B the total amount in sales will be quarter less. This implies

Sales a/c 7000

Office supplies a/c 2200

Purchase return a/c 500

Sales return a/c 150

Trade discount a/c 200

Drawing a/c 1500

Salary to shop assistant 1000

Total 28200 28200

QUESTION 2

Particulars A B C

Consolidated balance

sheet

Amount (£) Amount (£)

Amount

(£) Amount (£)

Sales 3860000 1300000 170000 5330000

Cost of sales 1950500 537500 120000 2608000

Gross profit 1909500 762500 50000 2722000

Operating expenses 467000 279560 23500 770060

Operating profit 1442500 482940 26500 1951940

Interest 100000 50000 3000 153000

Profit before tax 1342500 432940 23500 1798940

Tax 356400 56000 8400 420800

Profit after tax 986100 376940 15100 1378140

With the help of the above statement it is clear that the consolidation of the income

statement is necessary at time when there is involvement of the parent company acquiring other

company. at the time of acquisition, the working of the company is affected and this is also

highlighted in the financial statements as well (Prodanova and et.al., 2019). in the present case of

B selling good to A will be added in the sales of B and also will be added in the sales of A as

well. the whole amount will be added in the sales of A as well because it is mentioned that there

is not any inventory being left with A.

Moreover, in the next adjustment A sold good to B and a quarter of goods were

remaining in the inventory of B. hence in the present case, for A, the sales will be of whole

amount that is 200000 but in case of B the total amount in sales will be quarter less. This implies

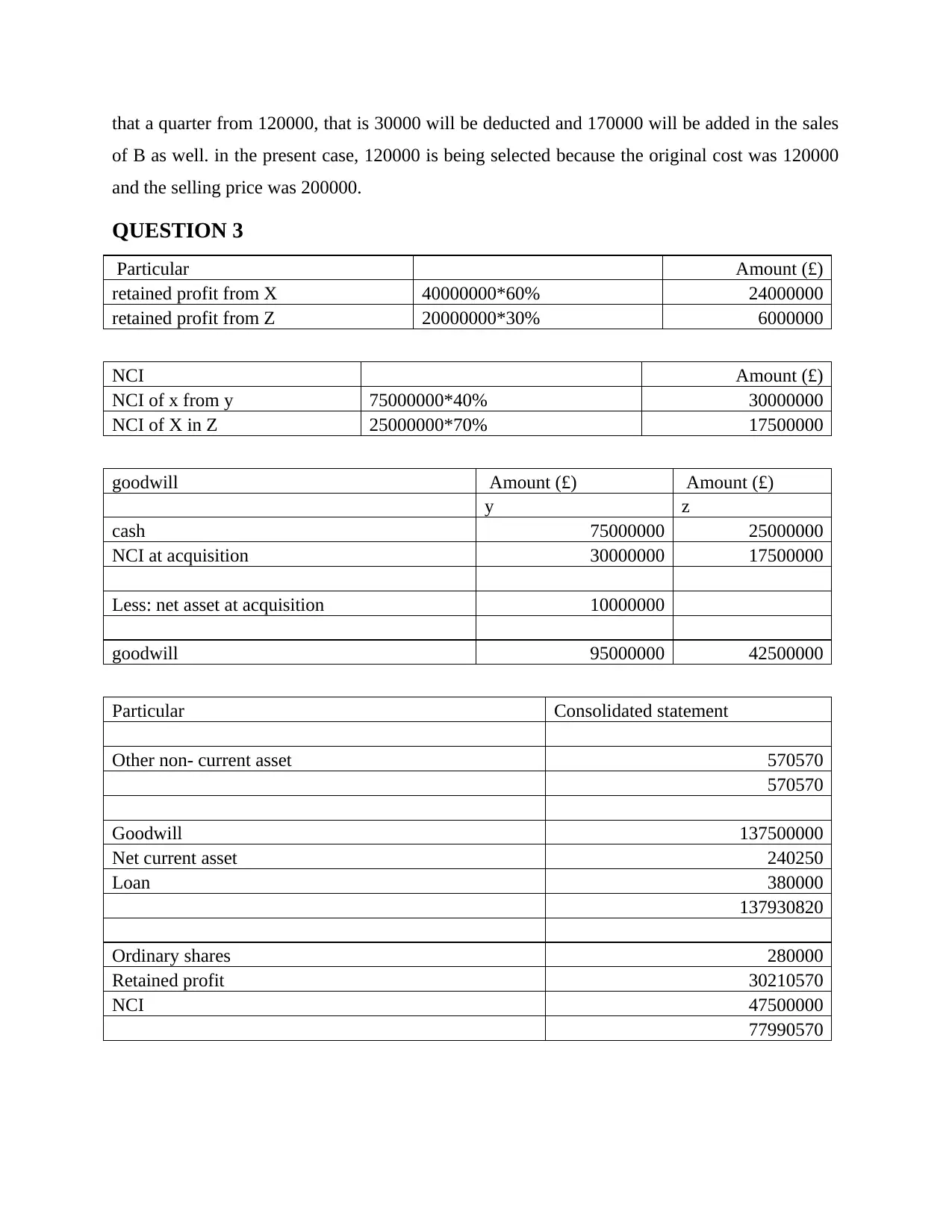

that a quarter from 120000, that is 30000 will be deducted and 170000 will be added in the sales

of B as well. in the present case, 120000 is being selected because the original cost was 120000

and the selling price was 200000.

QUESTION 3

Particular Amount (£)

retained profit from X 40000000*60% 24000000

retained profit from Z 20000000*30% 6000000

NCI Amount (£)

NCI of x from y 75000000*40% 30000000

NCI of X in Z 25000000*70% 17500000

goodwill Amount (£) Amount (£)

y z

cash 75000000 25000000

NCI at acquisition 30000000 17500000

Less: net asset at acquisition 10000000

goodwill 95000000 42500000

Particular Consolidated statement

Other non- current asset 570570

570570

Goodwill 137500000

Net current asset 240250

Loan 380000

137930820

Ordinary shares 280000

Retained profit 30210570

NCI 47500000

77990570

of B as well. in the present case, 120000 is being selected because the original cost was 120000

and the selling price was 200000.

QUESTION 3

Particular Amount (£)

retained profit from X 40000000*60% 24000000

retained profit from Z 20000000*30% 6000000

NCI Amount (£)

NCI of x from y 75000000*40% 30000000

NCI of X in Z 25000000*70% 17500000

goodwill Amount (£) Amount (£)

y z

cash 75000000 25000000

NCI at acquisition 30000000 17500000

Less: net asset at acquisition 10000000

goodwill 95000000 42500000

Particular Consolidated statement

Other non- current asset 570570

570570

Goodwill 137500000

Net current asset 240250

Loan 380000

137930820

Ordinary shares 280000

Retained profit 30210570

NCI 47500000

77990570

In the present case, the consolidated financial position statement is being prepared. Under

this the company X is acquiring some of the shares in remaining both company that is Y and Z.

The consolidated statement is being prepared at time when two or more company merge their

operations. Hence, as a result of this, the single balance sheet is being prepared by merging the

operations of the all the companies (Santis, Grossi and Bisogno, 2019). For this purpose, the first

thing evaluated is the share of goodwill within the company. this is necessary pertaining to the

fact that in case there will be difference between the book value and the purchase price paid.

Thus, this is being calculated in order to analyse the goodwill which X will get in order to

acquire the control in Y and Z. also, at time of acquisition the NCI is also being calculated and it

is necessary to be calculated. This NCI that is non- controlling interest is also known as the

minority interest is the ownership position, wherein the shareholder is having less than 50 % of

the outstanding shares and is not having any control within the decisions of the company

(Gavana, Gottardo and Moisello, 2020). further the NCI will be added in the liabilities side

within the consolidated financial statement of all the three companies. This is very important to

include all the working in better and effective manner within the acquisition of the project. This

is necessary for the reason that it will outline better and effective position of the combined

company.

this the company X is acquiring some of the shares in remaining both company that is Y and Z.

The consolidated statement is being prepared at time when two or more company merge their

operations. Hence, as a result of this, the single balance sheet is being prepared by merging the

operations of the all the companies (Santis, Grossi and Bisogno, 2019). For this purpose, the first

thing evaluated is the share of goodwill within the company. this is necessary pertaining to the

fact that in case there will be difference between the book value and the purchase price paid.

Thus, this is being calculated in order to analyse the goodwill which X will get in order to

acquire the control in Y and Z. also, at time of acquisition the NCI is also being calculated and it

is necessary to be calculated. This NCI that is non- controlling interest is also known as the

minority interest is the ownership position, wherein the shareholder is having less than 50 % of

the outstanding shares and is not having any control within the decisions of the company

(Gavana, Gottardo and Moisello, 2020). further the NCI will be added in the liabilities side

within the consolidated financial statement of all the three companies. This is very important to

include all the working in better and effective manner within the acquisition of the project. This

is necessary for the reason that it will outline better and effective position of the combined

company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Gavana, G., Gottardo, P. and Moisello, A.M., 2020. Did the switch to IFRS 11 for joint ventures

affect the value relevance of corporate consolidated financial statements? Evidence from

France and Italy. Journal of International Accounting, Auditing and Taxation. 38.

p.100300.

Kamburova, L., 2020. The Development of Practices for the Preparation of Consolidated

Financial Statements. Ikonomiceski i Sotsialni Alternativi. (1). pp.123-133.

Prodanova, N.A., and et.al., 2019. Methodology for assessing control in the formation of

financial statements of a consolidated business. International Journal of Recent

Technology and Engineering. 8(1). pp.2696-2702.

Santis, S., Grossi, G. and Bisogno, M., 2019. Drivers for the voluntary adoption of consolidated

financial statements in local governments. Public Money & Management. 39(8). pp.534-

543.

Books and Journals

Gavana, G., Gottardo, P. and Moisello, A.M., 2020. Did the switch to IFRS 11 for joint ventures

affect the value relevance of corporate consolidated financial statements? Evidence from

France and Italy. Journal of International Accounting, Auditing and Taxation. 38.

p.100300.

Kamburova, L., 2020. The Development of Practices for the Preparation of Consolidated

Financial Statements. Ikonomiceski i Sotsialni Alternativi. (1). pp.123-133.

Prodanova, N.A., and et.al., 2019. Methodology for assessing control in the formation of

financial statements of a consolidated business. International Journal of Recent

Technology and Engineering. 8(1). pp.2696-2702.

Santis, S., Grossi, G. and Bisogno, M., 2019. Drivers for the voluntary adoption of consolidated

financial statements in local governments. Public Money & Management. 39(8). pp.534-

543.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.