Consolidated Worksheet: Sisters Ltd and Brothers Ltd - Year Ended 2017

VerifiedAdded on 2021/05/31

|3

|822

|104

Project

AI Summary

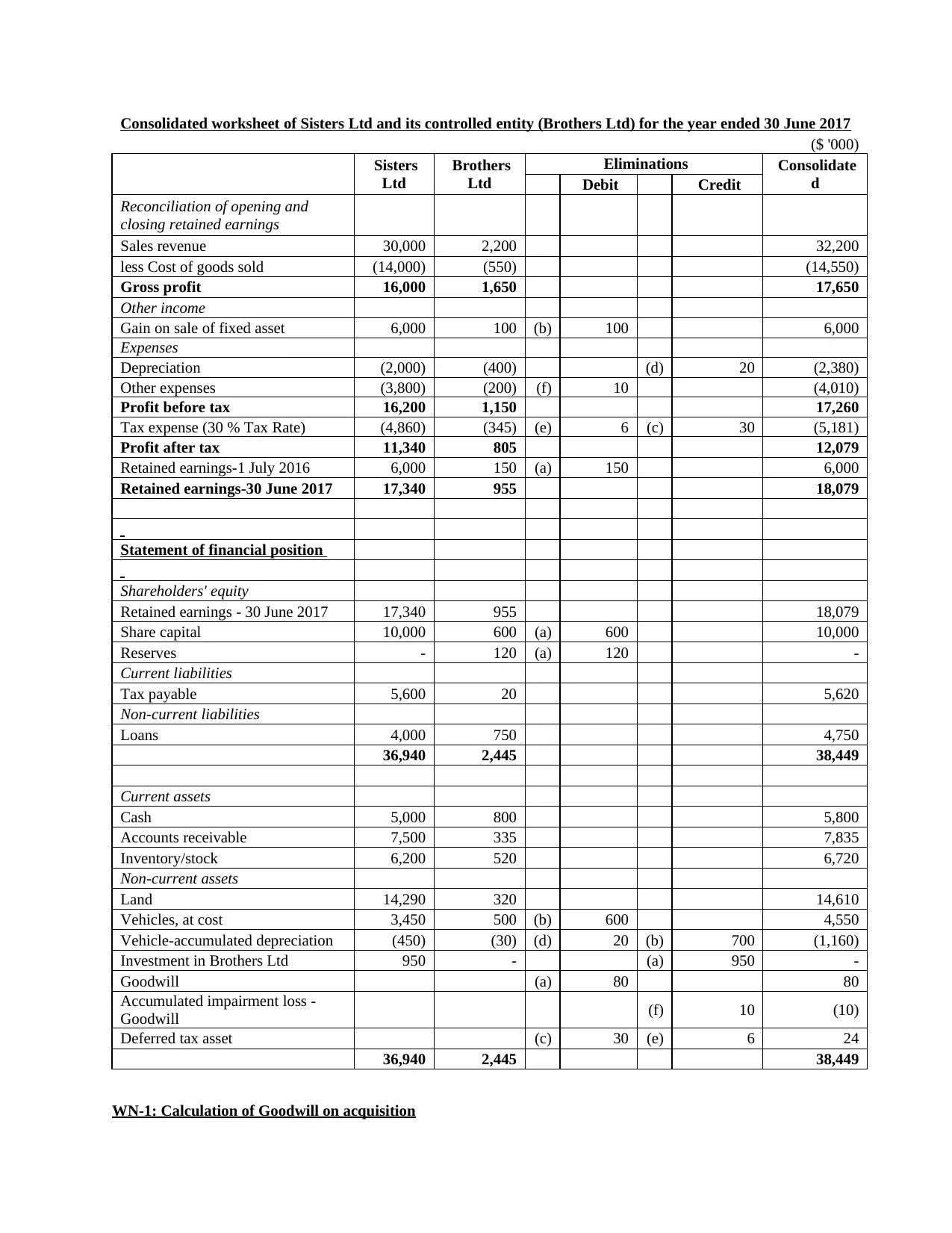

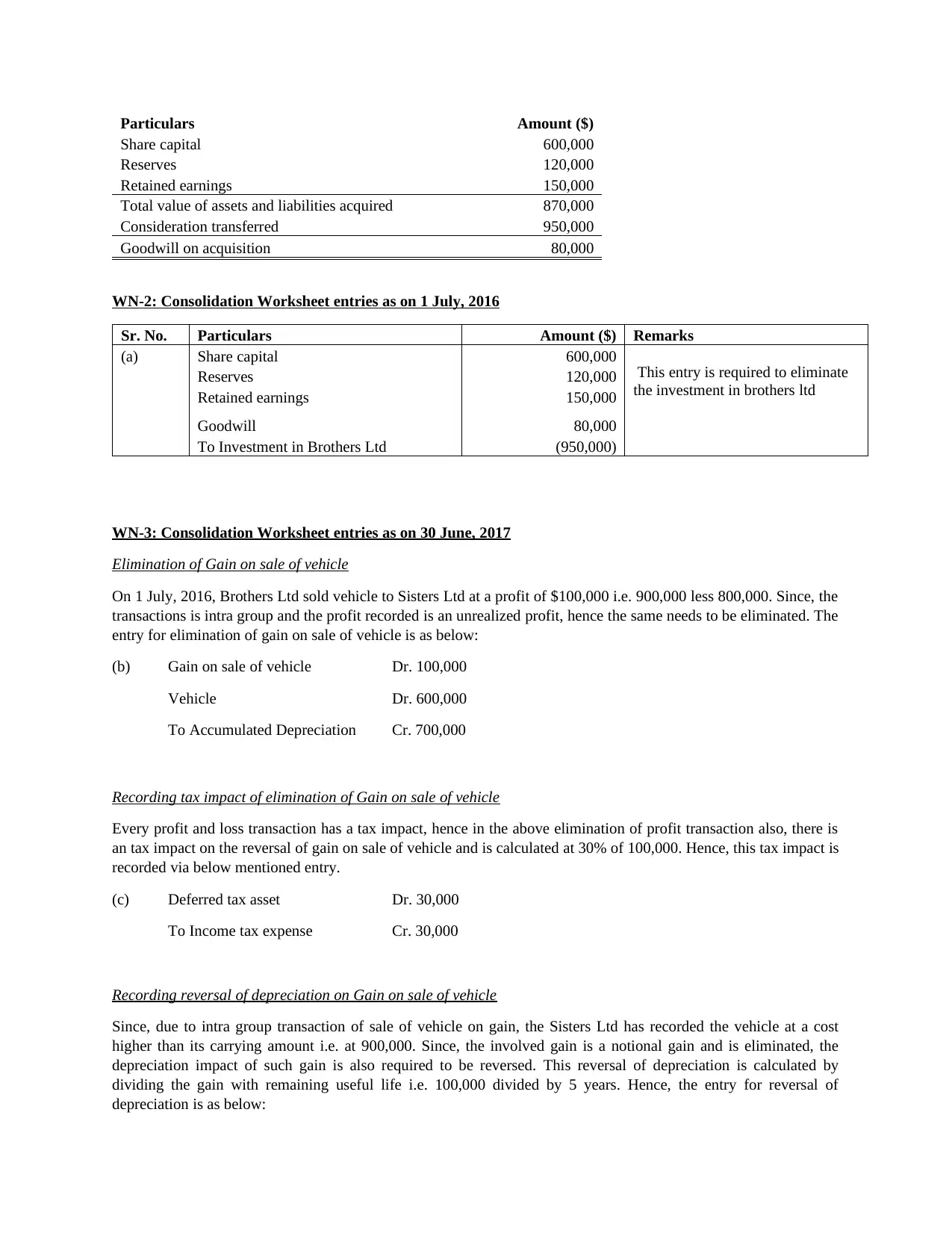

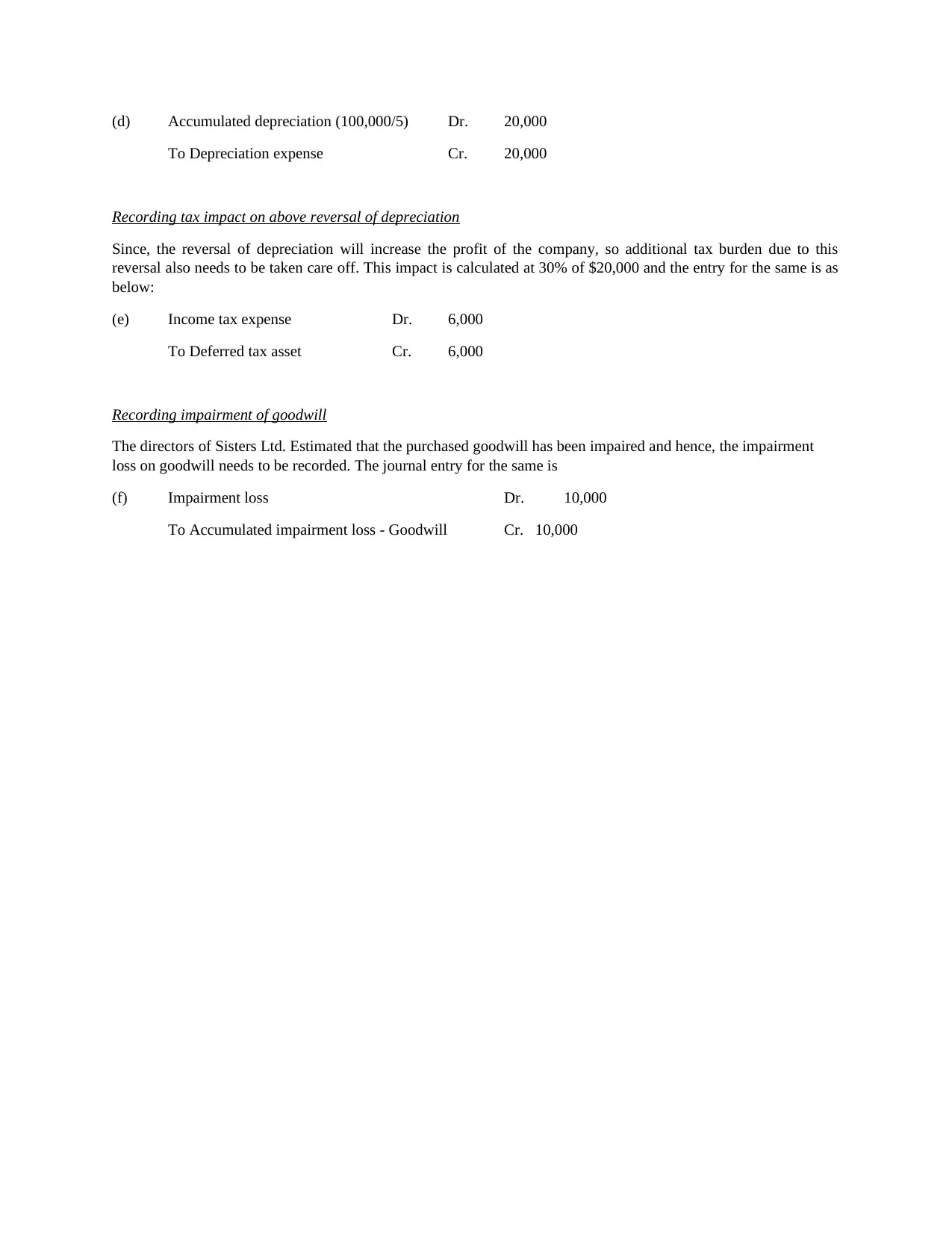

The assignment presents a consolidated worksheet for Sisters Ltd and its controlled entity, Brothers Ltd, for the year ended June 30, 2017. The worksheet includes the income statement, statement of financial position, and supporting schedules. It details the process of consolidating the financial statements, including eliminations of intercompany transactions, such as the sale of a vehicle, and the recognition of goodwill. The document provides calculations for goodwill on acquisition, consolidation worksheet entries, and adjustments for unrealized profits, depreciation, and tax impacts. It also addresses the impairment of goodwill. The worksheet demonstrates the steps necessary to prepare consolidated financial statements, ensuring that the financial performance and position of the group are accurately reflected, and that the financial statements are compliant with accounting standards. The solution provides a comprehensive overview of the consolidation process, including all necessary adjustments and eliminations.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.