Acquisition Analysis, Consolidation Entries in Financial Accounting

VerifiedAdded on 2023/06/05

|8

|1025

|431

Practical Assignment

AI Summary

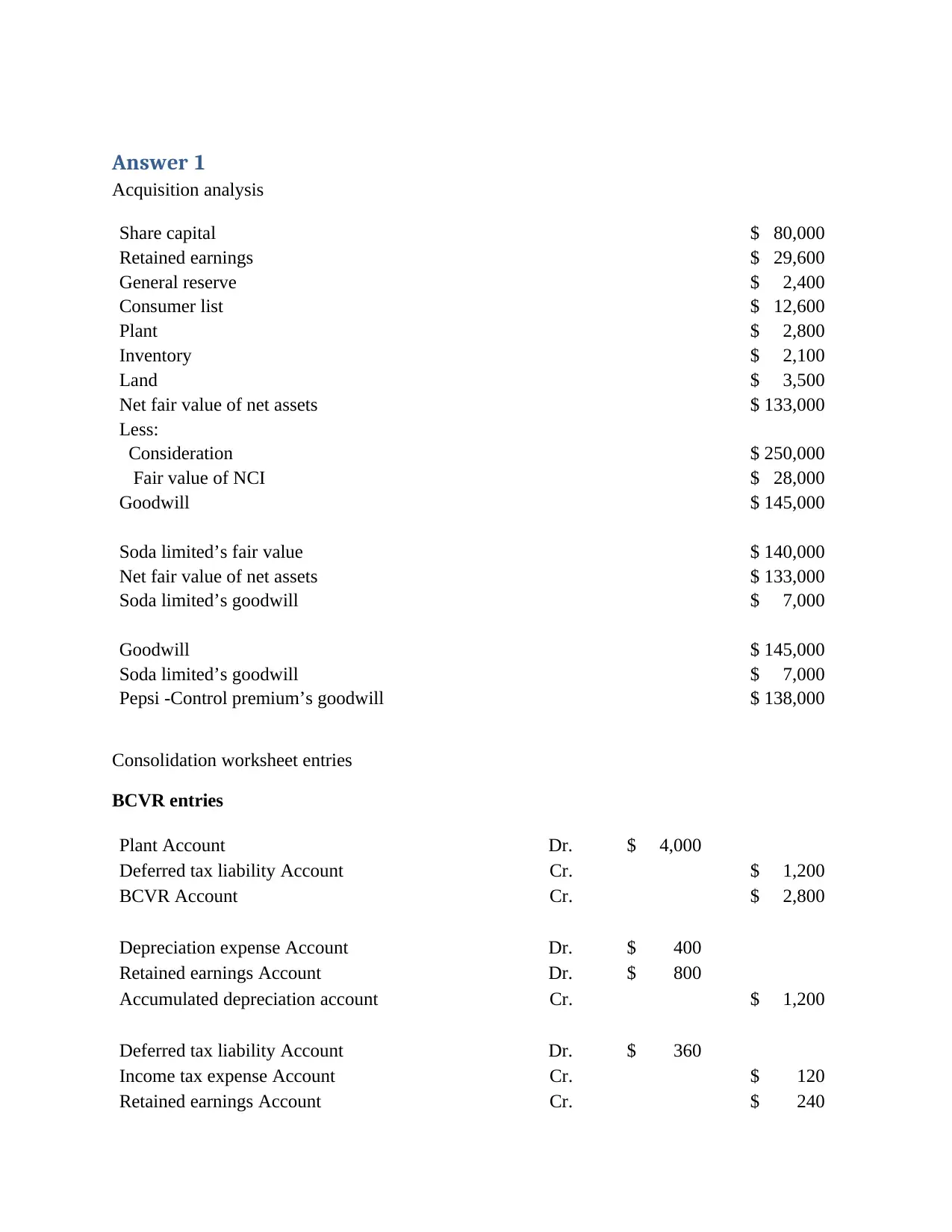

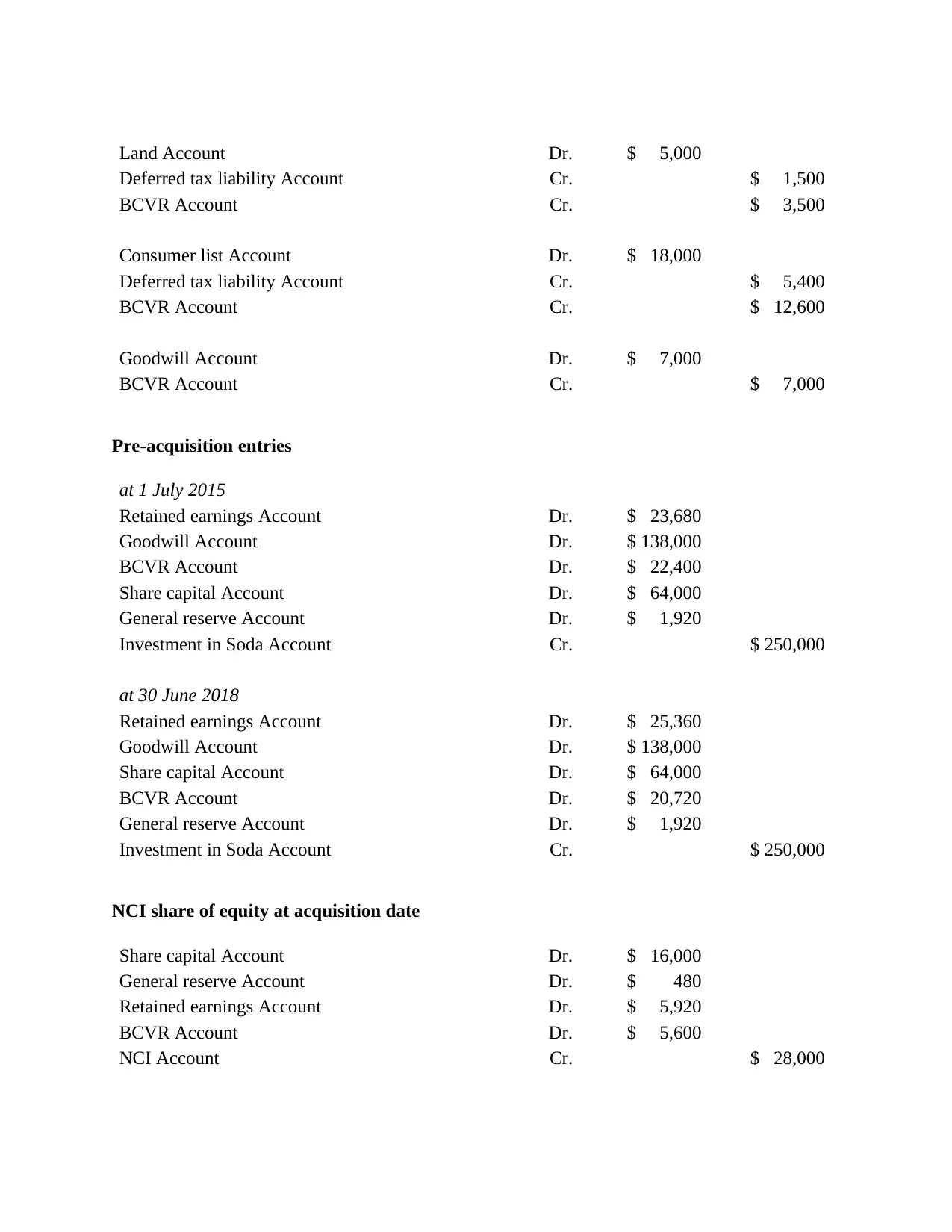

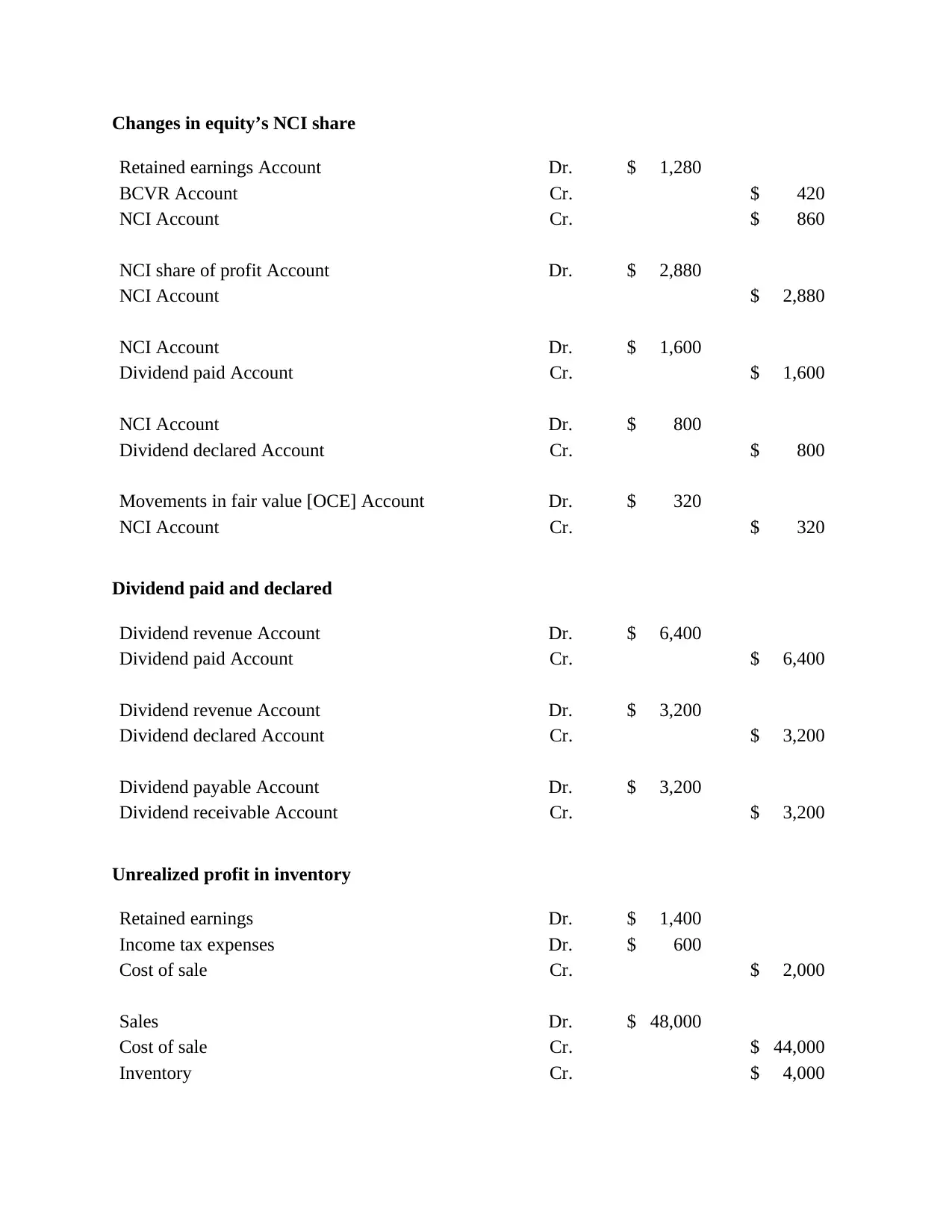

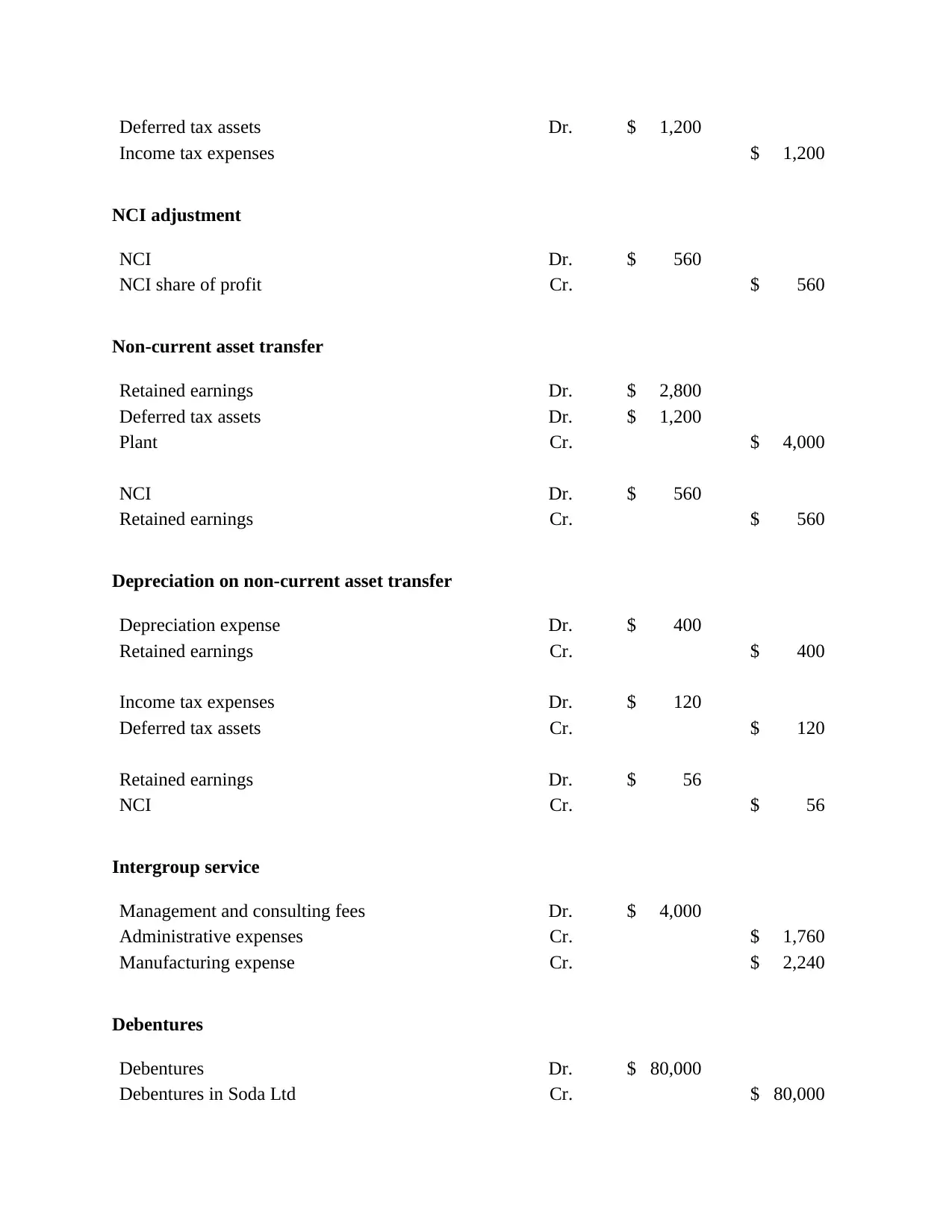

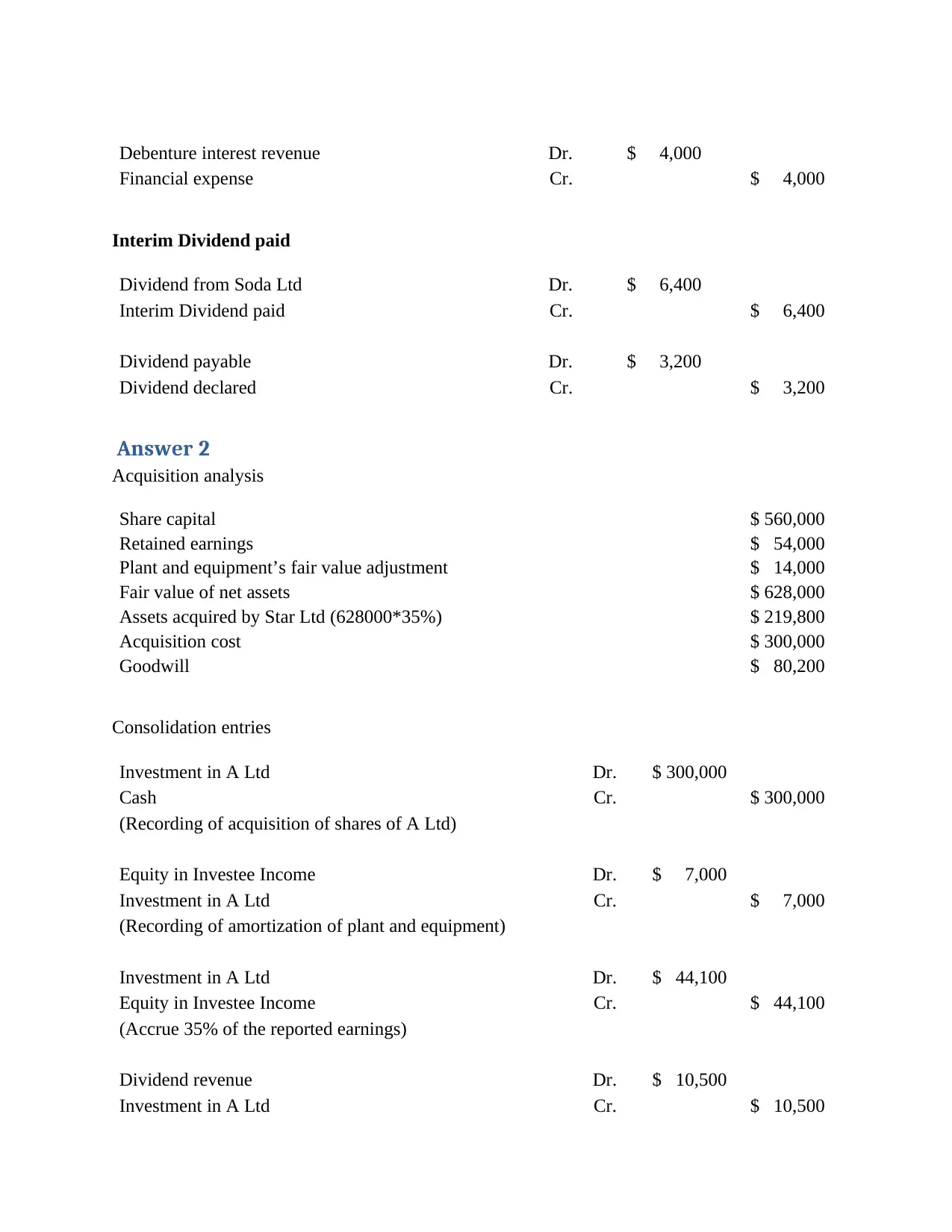

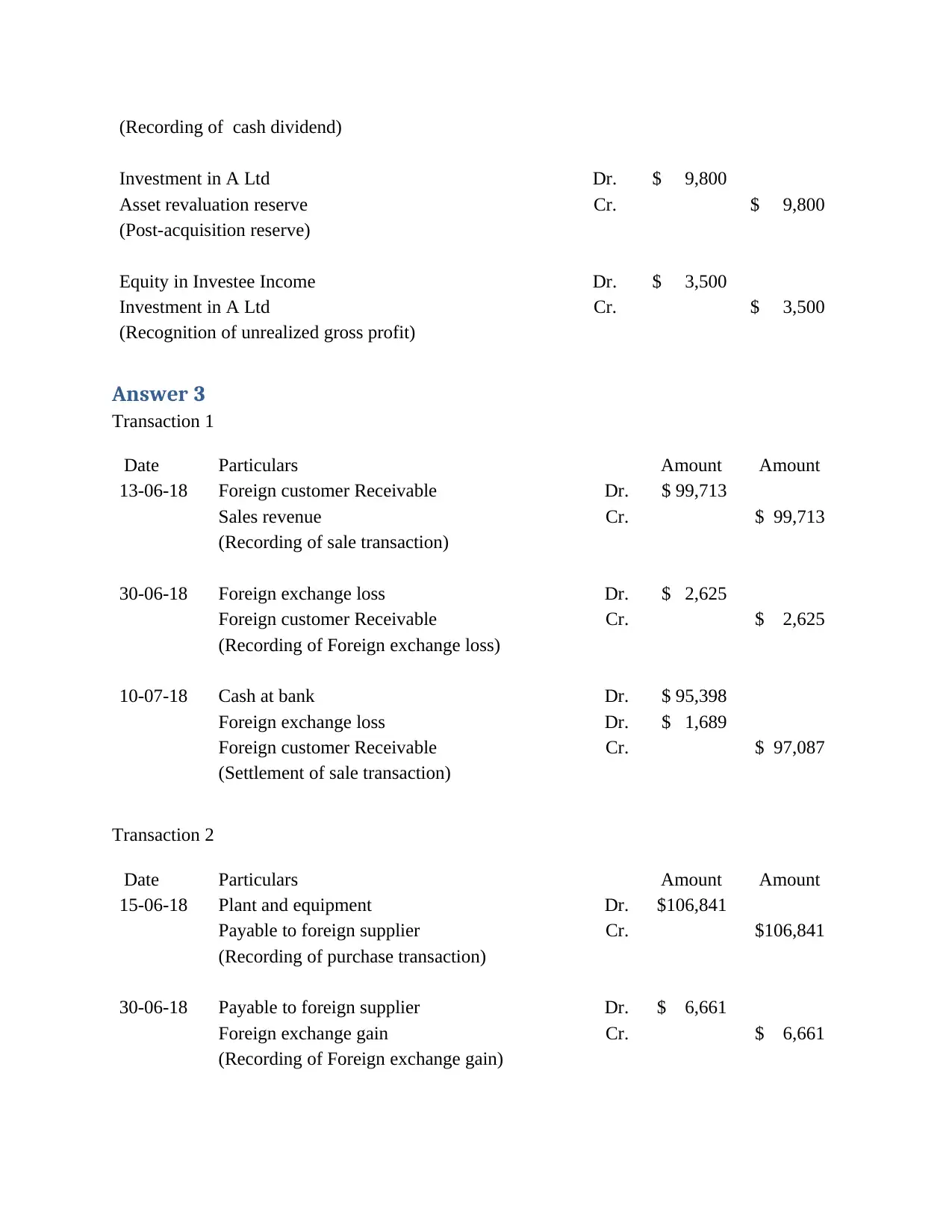

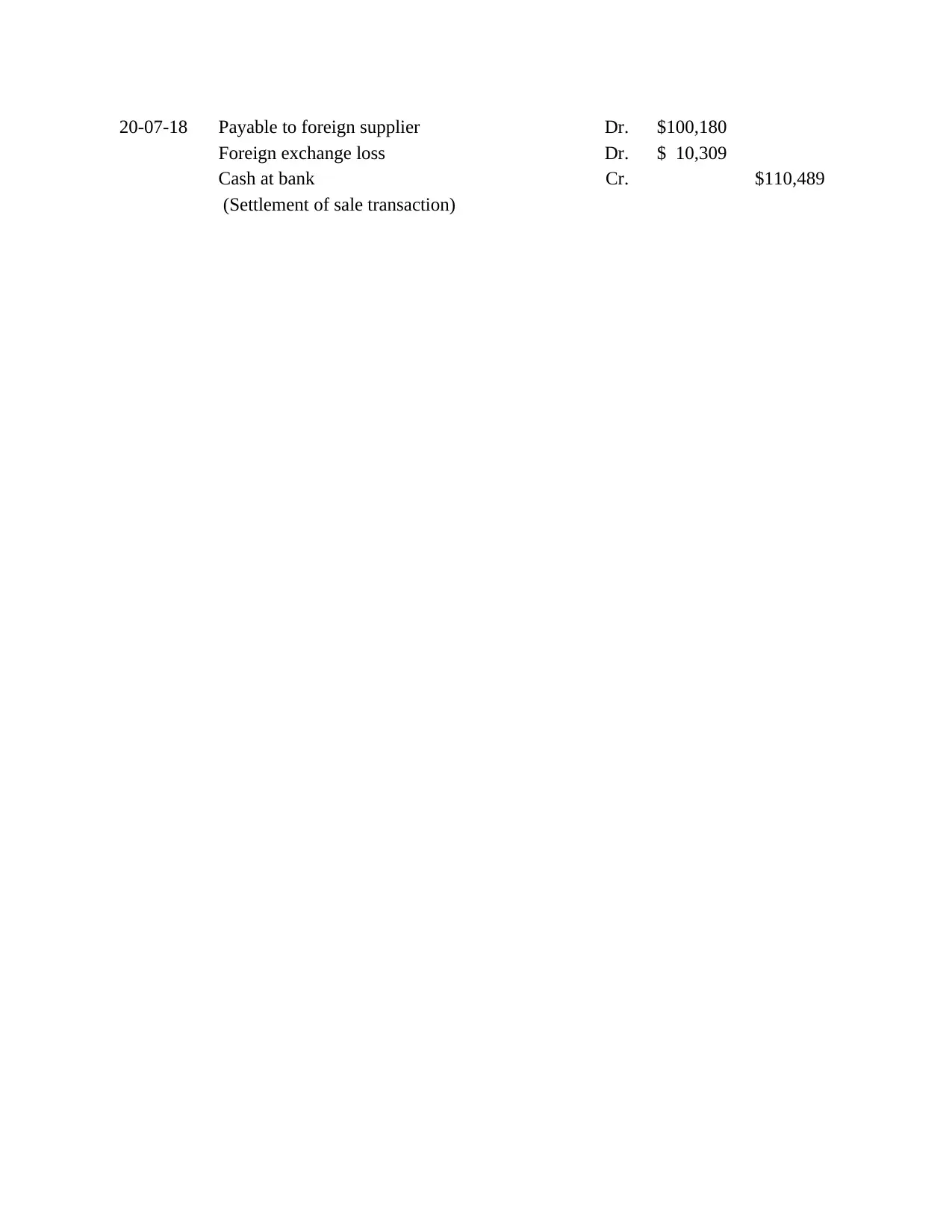

This assignment provides detailed solutions for several financial accounting problems. It includes an acquisition analysis calculating goodwill and fair value of net assets, followed by consolidation worksheet entries addressing BCVR (Bargain Purchase Option Reserve) adjustments for plant, land, consumer lists, and goodwill. Pre-acquisition and NCI (Non-Controlling Interest) share calculations are presented, along with adjustments for dividends, unrealized profits in inventory, and non-current asset transfers. The assignment also covers intergroup services, debentures, and dividend transactions. Furthermore, it demonstrates consolidation entries for investment in an associate, amortization of plant and equipment, and recognition of unrealized gross profit. Finally, the assignment addresses foreign currency transactions, detailing the accounting for sales and purchases involving foreign customers and suppliers, including the recognition of foreign exchange gains and losses upon settlement. The document is available on Desklib, a platform offering a wide range of study resources for students.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.