Consolidation Statements and Financial Analysis of ABC & XYZ Ltd

VerifiedAdded on 2023/06/11

|12

|1556

|89

Case Study

AI Summary

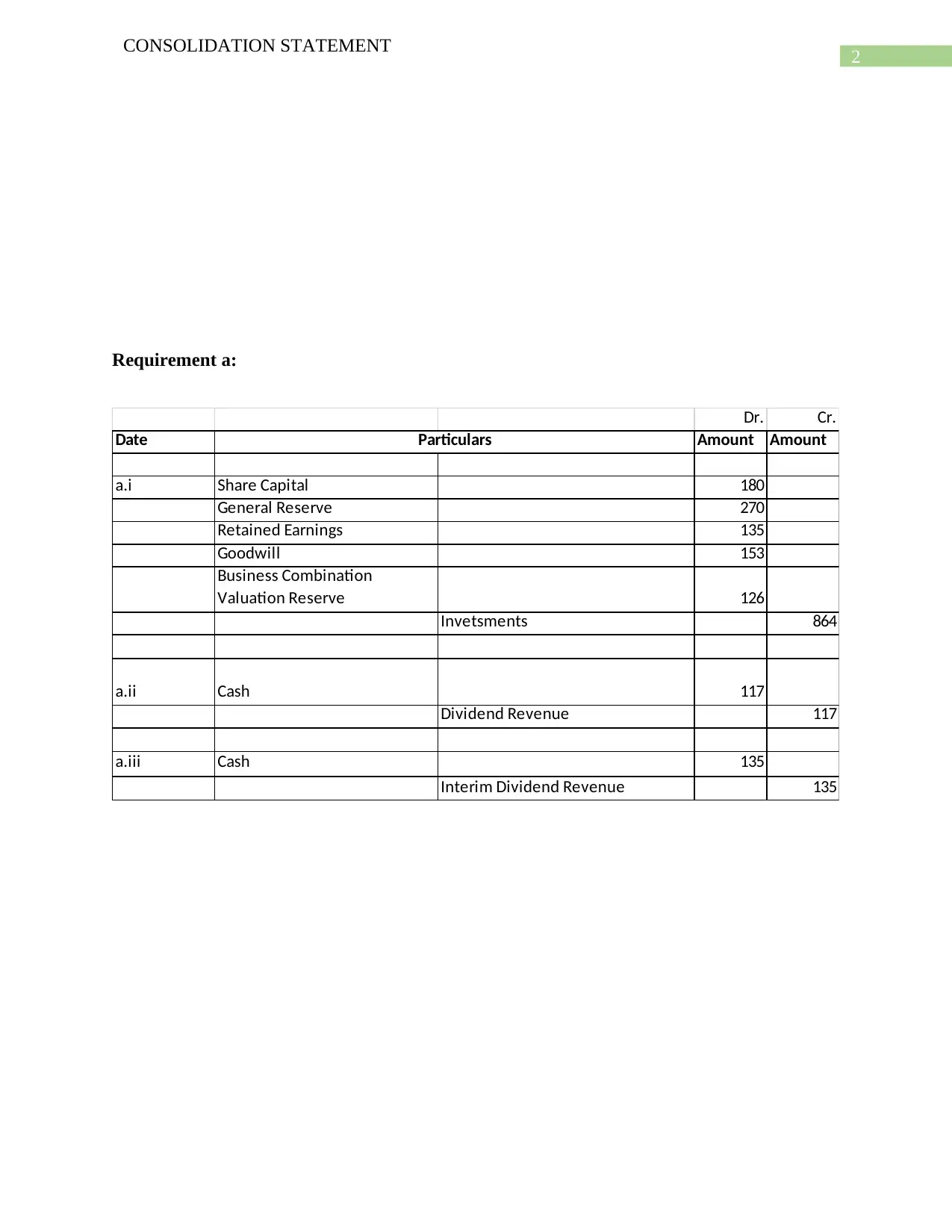

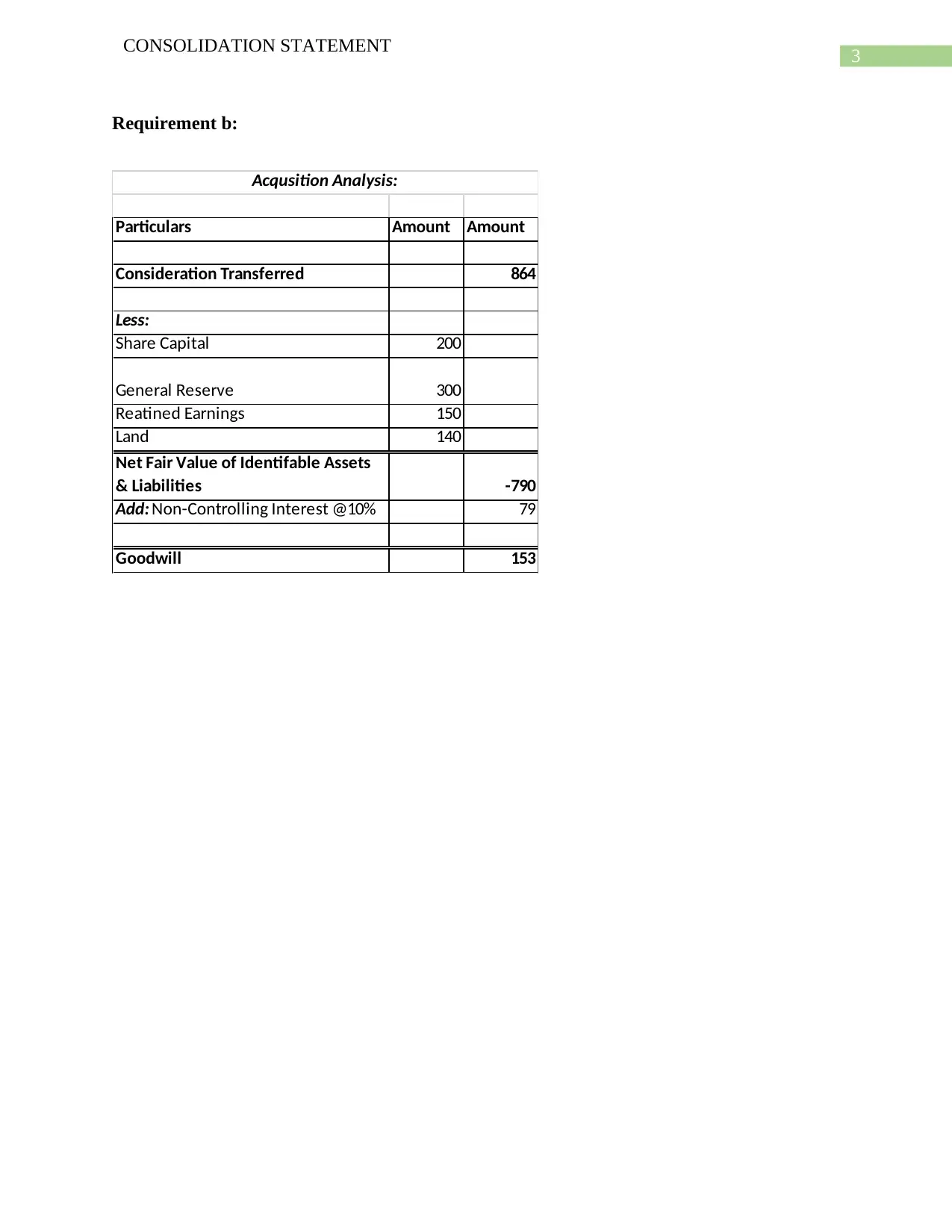

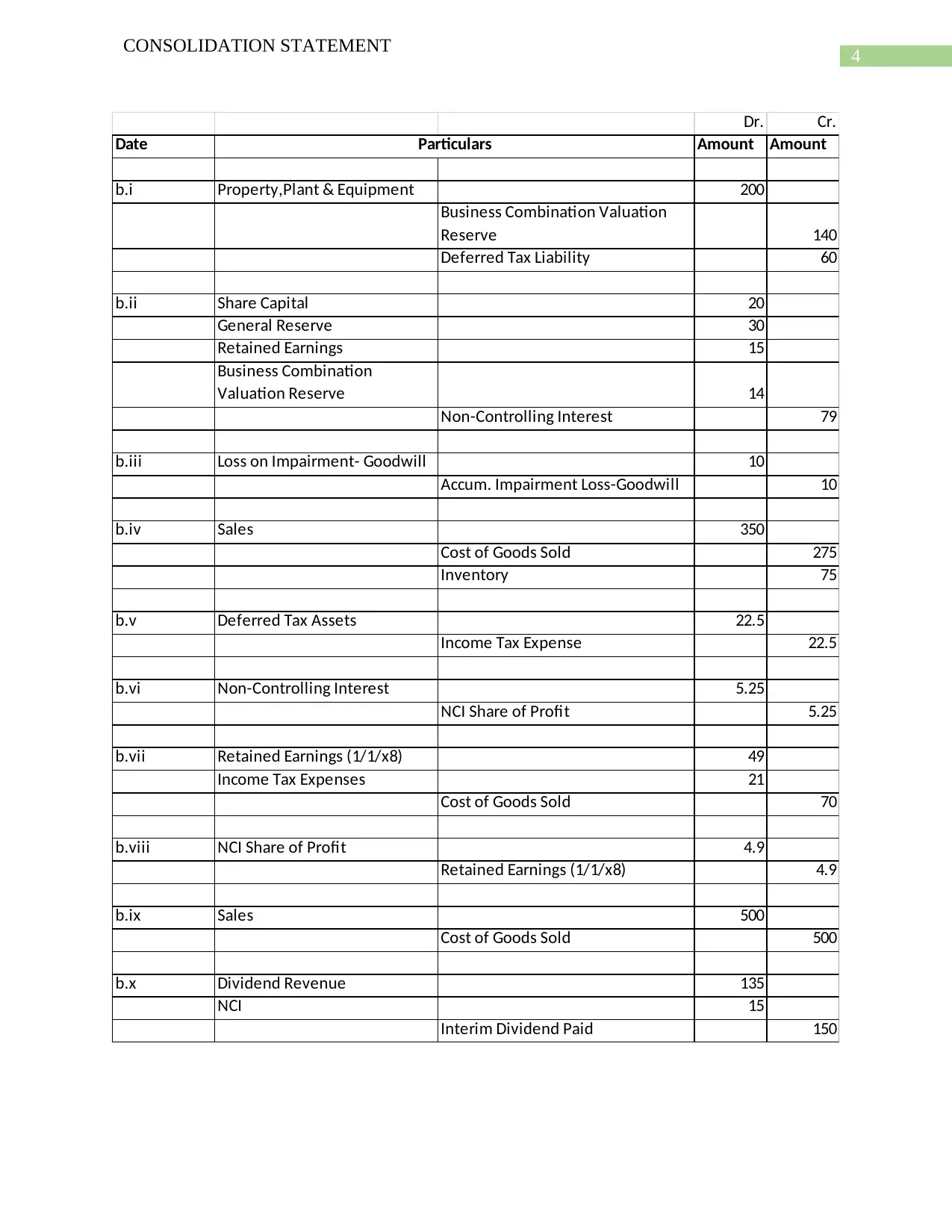

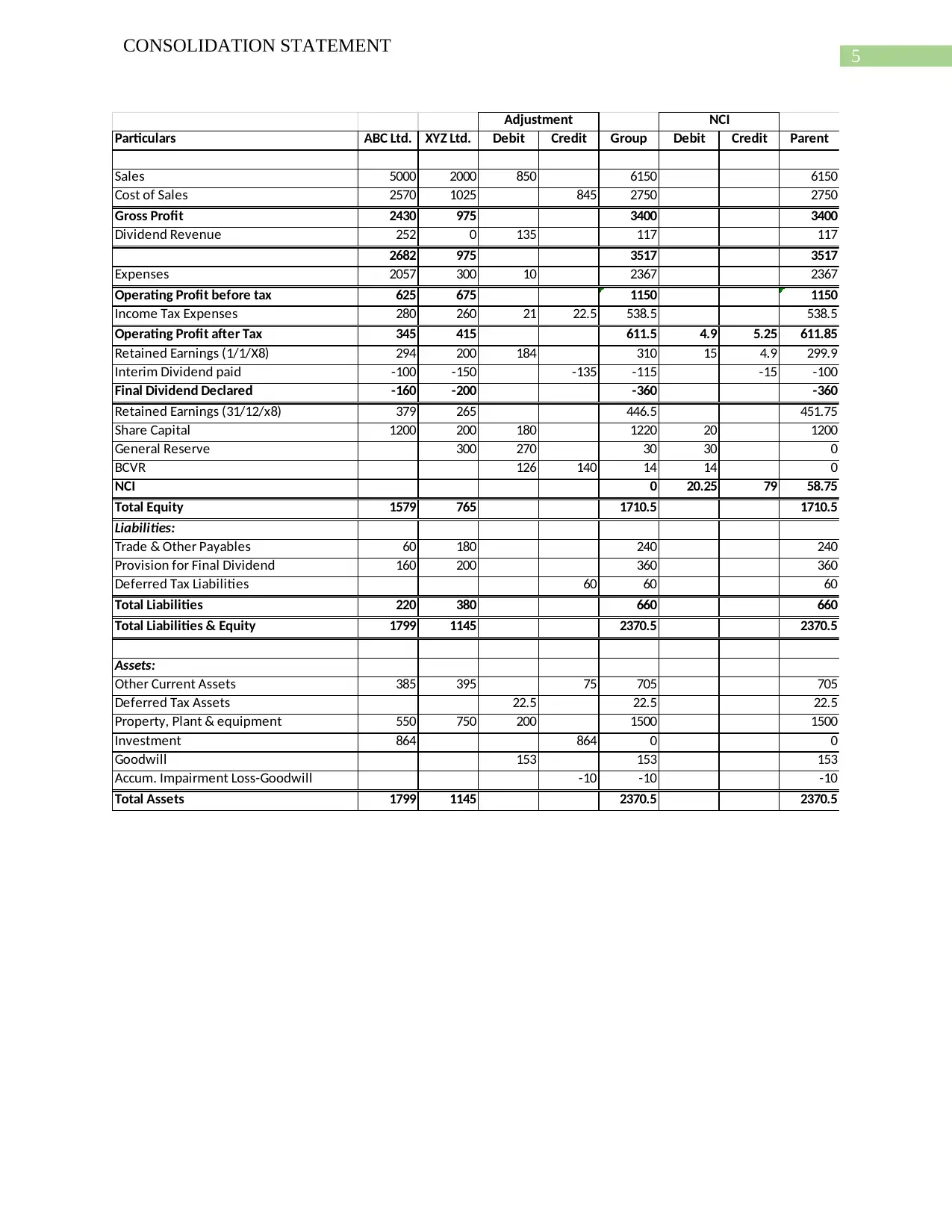

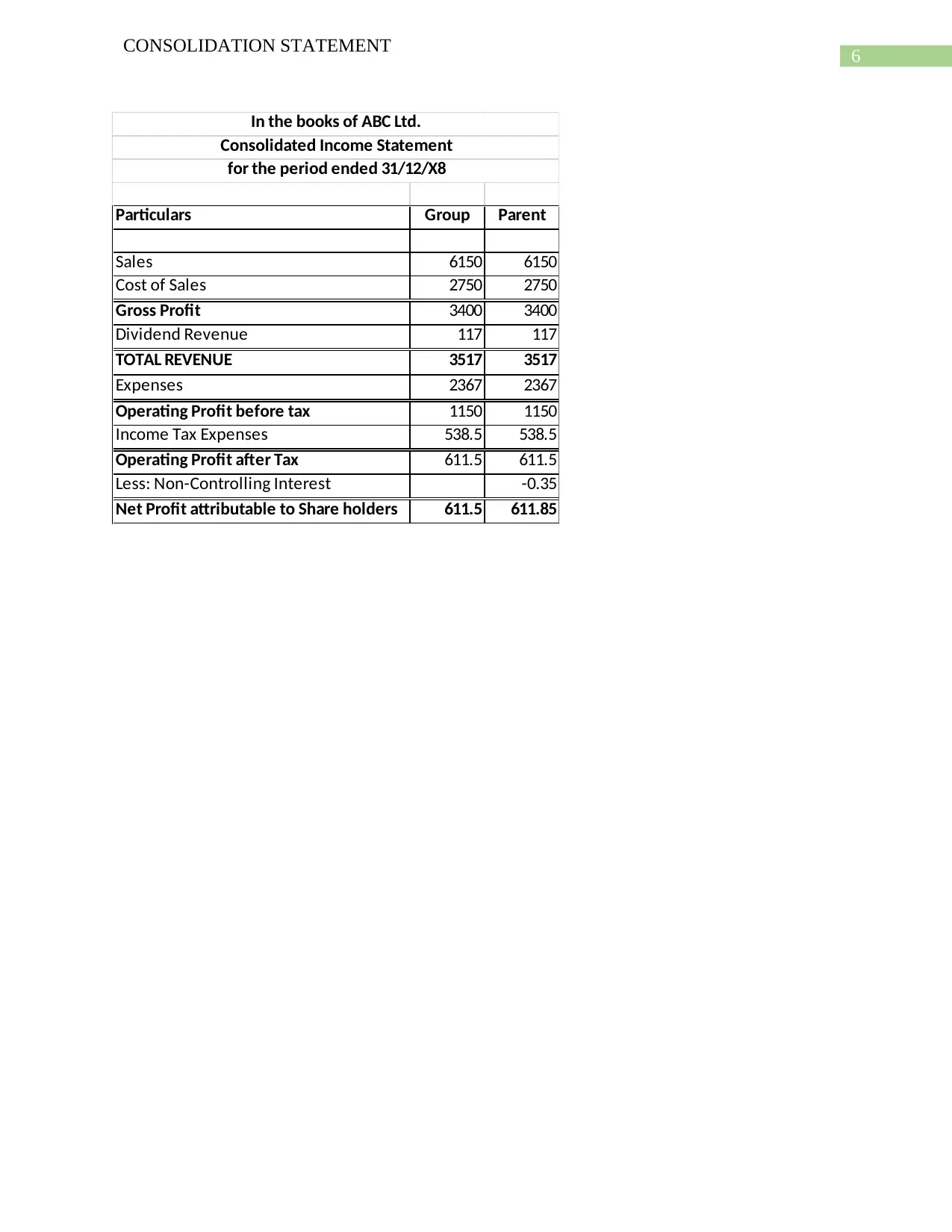

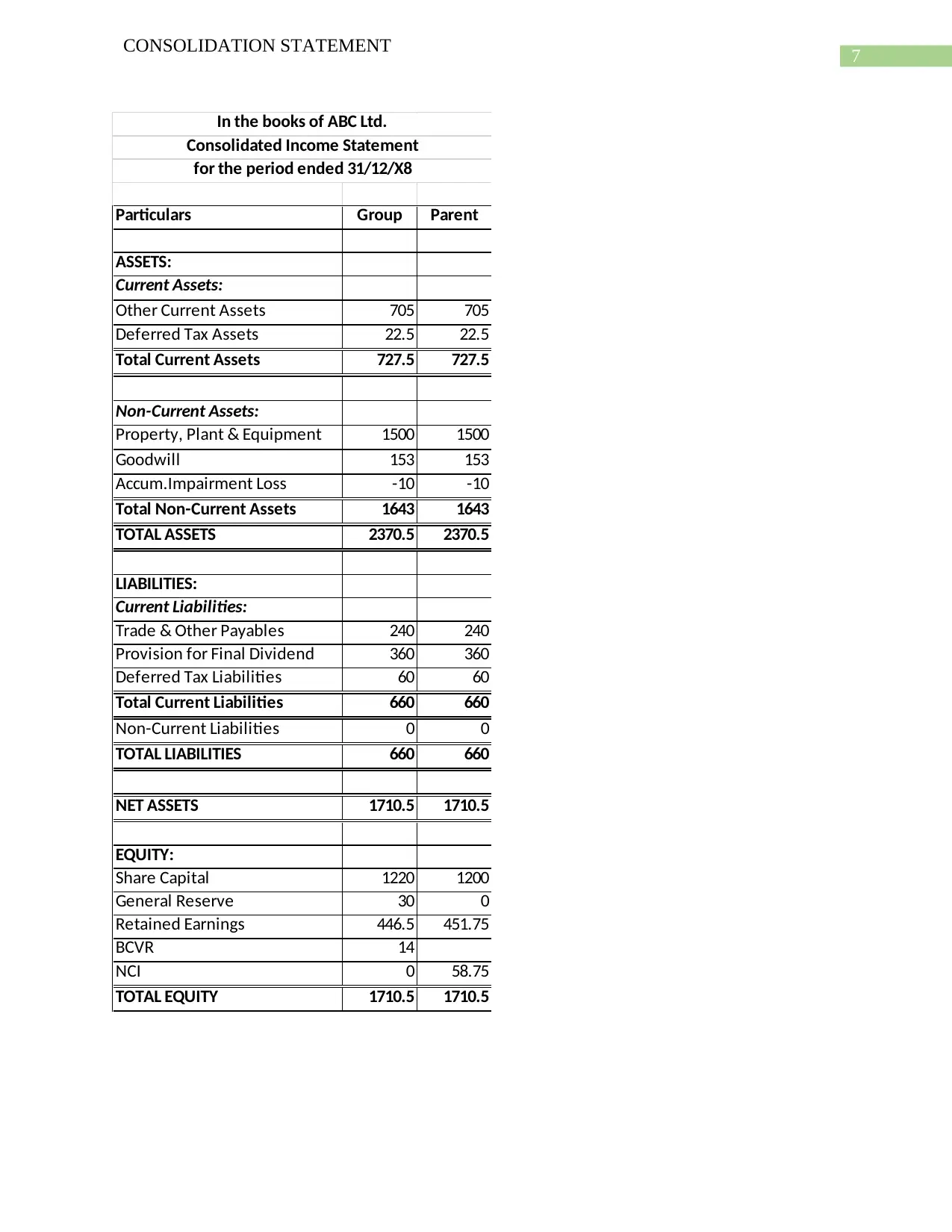

This assignment presents a detailed case study involving the consolidation of financial statements for ABC Ltd and XYZ Ltd following a takeover bid. It includes an acquisition analysis, journal entries, and the preparation of consolidated financial statements. The analysis covers key aspects such as consideration transferred, fair value adjustments, goodwill calculation, and non-controlling interest. The document also discusses the partial and full goodwill methods, highlighting their advantages and disadvantages under both IFRS and US GAAP frameworks. The assignment concludes with consolidated income statements and balance sheets, providing a comprehensive view of the post-acquisition financial position. Desklib offers similar solved assignments and past papers for students.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.