Accounting and Sustainability Report Analysis

VerifiedAdded on 2021/02/22

|18

|5052

|61

AI Summary

This assignment involves a comprehensive review and analysis of accounting and sustainability reports from different sources, including International Financial Reporting Standards (IFRS), Financial Accounting Standards Board (FASB), and corporate sustainability assessments. The analysis will delve into the consequences of mandatory corporate sustainability reporting, the impact of IFRS adoption on earnings management, and the role of integrated reporting in communicating corporate sustainability management. Additionally, the assignment will examine the responsiveness of international accounting regulation to challenges, the effectiveness of FASB's disclosure standards, and the importance of sustainability management and reporting tools. The report will provide a detailed summary of these analyses, highlighting key findings and implications for businesses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CONTEMPORARY

ACCOUNTING THEORY

ACCOUNTING THEORY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EXECUTIVE SUMMARY

Conceptual framework is a set of rules or interrelated fundamentals. The objectives of

conceptual framework is to determine the goals of financial reporting, These framework

facilitate the guidelines regarding how transactions should be recognised & measured, and in

what they shall be reported and communicated. The report will include history and development

of conceptual framework for financial reporting in USA, Australia, UK and globally under

IASB, Australian accounting profession's concerns about the quality of conceptual framework.

A checklist is prepared for determining whether South African Harmony Gold Mining Company

Ltd., has disclosed information regarding such contents of integrated report.

In Australia, International Financial Reporting Standards(IFRS) came into effect in 2005,

accounting standards considered as entirely equivalent to IFRS. Interpretation of accounting and

financial reporting standards issued by IASB is considered as a critical matter in respect of both

international and Australian context which was a concern of accounting professionals in

Australia. Qualitative characteristics of information are reliability, understandability, relevance.

Guidelines of Global Reporting Initiative asserts on what the organisation is doing to the world

and environment which renders it less or more sustainable. International Integrated Reporting

Council which was established in 2010 August has an objective of developing a globally

accredited and accepted set of rules that results in organisation's communication regarding its

value creation over passage of time.

Conceptual framework is a set of rules or interrelated fundamentals. The objectives of

conceptual framework is to determine the goals of financial reporting, These framework

facilitate the guidelines regarding how transactions should be recognised & measured, and in

what they shall be reported and communicated. The report will include history and development

of conceptual framework for financial reporting in USA, Australia, UK and globally under

IASB, Australian accounting profession's concerns about the quality of conceptual framework.

A checklist is prepared for determining whether South African Harmony Gold Mining Company

Ltd., has disclosed information regarding such contents of integrated report.

In Australia, International Financial Reporting Standards(IFRS) came into effect in 2005,

accounting standards considered as entirely equivalent to IFRS. Interpretation of accounting and

financial reporting standards issued by IASB is considered as a critical matter in respect of both

international and Australian context which was a concern of accounting professionals in

Australia. Qualitative characteristics of information are reliability, understandability, relevance.

Guidelines of Global Reporting Initiative asserts on what the organisation is doing to the world

and environment which renders it less or more sustainable. International Integrated Reporting

Council which was established in 2010 August has an objective of developing a globally

accredited and accepted set of rules that results in organisation's communication regarding its

value creation over passage of time.

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A: CONCEPTUAL FRAMEWORK....................................................................................4

a.) History of conceptual framework in UK, USA, Australia and globally under International

Accounting Standard Board (IASB).......................................................................................4

b.) Discussing Australian accounting profession's concern regarding application of

IASB/IFRS conceptual framework.........................................................................................6

c.) On the basis of Journal articles review, critically discussing about the quality of

Conceptual Framework for Financial Reporting....................................................................7

d.) Application of conceptual framework in Rio Tinto Ltd in its financial reporting............8

PART B : INTEGRATED / SUSTAINABILITY REPORTING..................................................10

a.) Comparing and contrasting the sustainability reporting of Global Reporting Initiative

(GRI) and International Integrated Reporting Framework of (IIRC)...................................10

b.) Explaining strengths and limitations of conventional accounting based upon conceptual

framework.............................................................................................................................10

c.) Discussing the applicability of the theories learned to explain the contents of sustainability

as well as integrated reports.................................................................................................12

d.) Preparation of a check list that contains the components of integrated report................13

e.) Comparison of Australian company' s sustainability reporting and South African corporate

social reporting.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A: CONCEPTUAL FRAMEWORK....................................................................................4

a.) History of conceptual framework in UK, USA, Australia and globally under International

Accounting Standard Board (IASB).......................................................................................4

b.) Discussing Australian accounting profession's concern regarding application of

IASB/IFRS conceptual framework.........................................................................................6

c.) On the basis of Journal articles review, critically discussing about the quality of

Conceptual Framework for Financial Reporting....................................................................7

d.) Application of conceptual framework in Rio Tinto Ltd in its financial reporting............8

PART B : INTEGRATED / SUSTAINABILITY REPORTING..................................................10

a.) Comparing and contrasting the sustainability reporting of Global Reporting Initiative

(GRI) and International Integrated Reporting Framework of (IIRC)...................................10

b.) Explaining strengths and limitations of conventional accounting based upon conceptual

framework.............................................................................................................................10

c.) Discussing the applicability of the theories learned to explain the contents of sustainability

as well as integrated reports.................................................................................................12

d.) Preparation of a check list that contains the components of integrated report................13

e.) Comparison of Australian company' s sustainability reporting and South African corporate

social reporting.....................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Conceptual framework for financial reporting can be described as set of objectives,

policies and fundamental established by International Accounting Standard Board (IASB). The

purpose of conceptual framework for reporting is to bring uniformity in the interpretation of

different methodologies of accounting (Abdel-Khalik, 2019). The present project report will

highlight the concept framework in Rio Tinto Ltd, which is a multinational Anglo-Australian

public company trading on LSE, ASX, NYSE and FTSE 100 Component. The organisation

belongs to metals, mining and materials industry. It is headquartered in London and Melbourne,

founded in 1873 and is currently world's one of the largest metal and mining business entities.

The report will include history and development of conceptual framework for financial

reporting in USA, Australia, UK and globally under IASB, Australian accounting profession's

concerns about the quality of conceptual framework. The report will highlight how Rio Tinto has

applied principles and fundamentals of IASB in its reporting. Further, in the next segment of

report, integrated or sustainability reporting guidelines will be discussed, strengths and

limitations of conventional accounting in order to understand the contents of sustainability and

integrated reports. A checklist will be prepared for determining whether South African Harmony

Gold Mining Company Ltd., has disclosed information regarding such contents of integrated

report.

PART A: CONCEPTUAL FRAMEWORK

a.) History of conceptual framework in UK, USA, Australia and globally under International

Accounting Standard Board (IASB)

Before 1929, there were no accounting standards either for public or private companies.

But later, after the crash of stock market in 1929, an act was passed in USA for regulating the

secondary market called as Securities and Exchange Act 1934. The commission of Securities and

Exchange designated Financial Accounting Standards Boards which was given the responsibility

of setting up of the accounting standards within United States. The aim of FASB is to set and

improve Generally Accepted Principles (GAAP). The conceptual Framework of FASB was

started in 1973 for the purpose of establishing sound literature on accounting standards in USA.

From the year 1978 to 2010, many concept statements were published by FASB such as

Conceptual framework for financial reporting can be described as set of objectives,

policies and fundamental established by International Accounting Standard Board (IASB). The

purpose of conceptual framework for reporting is to bring uniformity in the interpretation of

different methodologies of accounting (Abdel-Khalik, 2019). The present project report will

highlight the concept framework in Rio Tinto Ltd, which is a multinational Anglo-Australian

public company trading on LSE, ASX, NYSE and FTSE 100 Component. The organisation

belongs to metals, mining and materials industry. It is headquartered in London and Melbourne,

founded in 1873 and is currently world's one of the largest metal and mining business entities.

The report will include history and development of conceptual framework for financial

reporting in USA, Australia, UK and globally under IASB, Australian accounting profession's

concerns about the quality of conceptual framework. The report will highlight how Rio Tinto has

applied principles and fundamentals of IASB in its reporting. Further, in the next segment of

report, integrated or sustainability reporting guidelines will be discussed, strengths and

limitations of conventional accounting in order to understand the contents of sustainability and

integrated reports. A checklist will be prepared for determining whether South African Harmony

Gold Mining Company Ltd., has disclosed information regarding such contents of integrated

report.

PART A: CONCEPTUAL FRAMEWORK

a.) History of conceptual framework in UK, USA, Australia and globally under International

Accounting Standard Board (IASB)

Before 1929, there were no accounting standards either for public or private companies.

But later, after the crash of stock market in 1929, an act was passed in USA for regulating the

secondary market called as Securities and Exchange Act 1934. The commission of Securities and

Exchange designated Financial Accounting Standards Boards which was given the responsibility

of setting up of the accounting standards within United States. The aim of FASB is to set and

improve Generally Accepted Principles (GAAP). The conceptual Framework of FASB was

started in 1973 for the purpose of establishing sound literature on accounting standards in USA.

From the year 1978 to 2010, many concept statements were published by FASB such as

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

qualitative characteristics of financial information, objectives of financial reporting by NPOs etc

(Morley, 2016).

In United Kingdom, Taxation and Financial Relations committee of ICAEW was created

in 1942 for the making recommendations on various aspects regarding the accounts of business

organisations. In the year 1990, government of UK established Financial Reporting Council

(FRC) which was responsible for promoting financial reporting by the medium of its bodies

which are Accounting Standards Board (ASB) and Financial Reporting Review Panel (FRRP). In

year 2004, UK's government made the regulatory system more strict after the major collapses of

organisations in US. It made FRC the sole regulator of accounting and auditing profession and

was made responsible for issuance of accounting and auditing standards in UK (Hashim, Li &

O’Hanlon, 2016).

In Australia, the conceptual framework of financial reporting and development of

accounting standards is the responsibility of Australian Accounting Standards Board (AASB).

This board derives its functions, responsibilities and powers from Australian Securities and

Investments Commission Act 2001. Australia followed the footsteps of UK and US regarding the

establishment of independent regulating and accounting standards establishment body within the

country along with various nations across the world.

At the global level, International Accounting Standard Board (IASB) is an accounting

standard body which founded the International Financial Reporting Standards (IFRS) in the year

2001. This is a non profit organisation who is responsible for developing set of high quality and

easily understandable IFRS standards which are based on accounting's articulated principles

(Conceptual Framework for Financial Reporting, 2018). In 2018 Conceptual Framework for

financial reporting was revised by IASB which has set out:

Guidance on presentation and disclosure

standards related to measurements and guidance relating to how to use them

qualitative characteristics of information of financial nature

definitions of liability, expenses, assets, equity and income

recognition and derecognition

(Morley, 2016).

In United Kingdom, Taxation and Financial Relations committee of ICAEW was created

in 1942 for the making recommendations on various aspects regarding the accounts of business

organisations. In the year 1990, government of UK established Financial Reporting Council

(FRC) which was responsible for promoting financial reporting by the medium of its bodies

which are Accounting Standards Board (ASB) and Financial Reporting Review Panel (FRRP). In

year 2004, UK's government made the regulatory system more strict after the major collapses of

organisations in US. It made FRC the sole regulator of accounting and auditing profession and

was made responsible for issuance of accounting and auditing standards in UK (Hashim, Li &

O’Hanlon, 2016).

In Australia, the conceptual framework of financial reporting and development of

accounting standards is the responsibility of Australian Accounting Standards Board (AASB).

This board derives its functions, responsibilities and powers from Australian Securities and

Investments Commission Act 2001. Australia followed the footsteps of UK and US regarding the

establishment of independent regulating and accounting standards establishment body within the

country along with various nations across the world.

At the global level, International Accounting Standard Board (IASB) is an accounting

standard body which founded the International Financial Reporting Standards (IFRS) in the year

2001. This is a non profit organisation who is responsible for developing set of high quality and

easily understandable IFRS standards which are based on accounting's articulated principles

(Conceptual Framework for Financial Reporting, 2018). In 2018 Conceptual Framework for

financial reporting was revised by IASB which has set out:

Guidance on presentation and disclosure

standards related to measurements and guidance relating to how to use them

qualitative characteristics of information of financial nature

definitions of liability, expenses, assets, equity and income

recognition and derecognition

description about the reporting business entity and its limits (Eisenschmidt & Schmidt,

2016)

b.) Discussing Australian accounting profession's concern regarding application of IASB/IFRS

conceptual framework

In Australia, International Financial Reporting Standards(IFRS) came into effect in 2005,

accounting standards considered as entirely equivalent to IFRS. However, the country changed

the name of standards, its textual language and deleted some options which resulted the

documents to be visibly different from the original standards issued by IASB (Harmon & Ntseh,

2016).

Australia's Implementation of IFRS :

The accounting professionals have commented on the implementation of IFRS in Australia

which states that:

It was matter of concern when it was commented that many of the international standards

are very rarely used by the Australian public companies in practice which leaves those

standards untested.

Interpretation of accounting and financial reporting standards issued by IASB is

considered as a critical matter in respect of both international and Australian contexts.

For example, IFRS are based on articulated accounting principles which should not be

interpreted on technical term that does not considers the capital market realities.

However, IFRS adopted by Australia are included in country's legislation according to

which Australian Securities and Investments Commission (ASIC) and other players in

corporate world are required to interpret the international standards on technical terms

(Harmon & Ntseh, 2016).

Another concern related to the implementation of IFRS by the accounting profession is

that country's interpretative body is designed in such a way that it responds to the

accounting issues very rapidly usually within 4 meetings. The same is not in case in case

of IFRIC which is the interpretative body of IASB, that takes around 12 months for

responding on the issues regarding the interpretation and implementation of international

2016)

b.) Discussing Australian accounting profession's concern regarding application of IASB/IFRS

conceptual framework

In Australia, International Financial Reporting Standards(IFRS) came into effect in 2005,

accounting standards considered as entirely equivalent to IFRS. However, the country changed

the name of standards, its textual language and deleted some options which resulted the

documents to be visibly different from the original standards issued by IASB (Harmon & Ntseh,

2016).

Australia's Implementation of IFRS :

The accounting professionals have commented on the implementation of IFRS in Australia

which states that:

It was matter of concern when it was commented that many of the international standards

are very rarely used by the Australian public companies in practice which leaves those

standards untested.

Interpretation of accounting and financial reporting standards issued by IASB is

considered as a critical matter in respect of both international and Australian contexts.

For example, IFRS are based on articulated accounting principles which should not be

interpreted on technical term that does not considers the capital market realities.

However, IFRS adopted by Australia are included in country's legislation according to

which Australian Securities and Investments Commission (ASIC) and other players in

corporate world are required to interpret the international standards on technical terms

(Harmon & Ntseh, 2016).

Another concern related to the implementation of IFRS by the accounting profession is

that country's interpretative body is designed in such a way that it responds to the

accounting issues very rapidly usually within 4 meetings. The same is not in case in case

of IFRIC which is the interpretative body of IASB, that takes around 12 months for

responding on the issues regarding the interpretation and implementation of international

accounting standards and financial reporting standards (Australian Implementation of

International Financial Reporting Standards IFRS, 2017)

c.) On the basis of Journal articles review, critically discussing about the quality of Conceptual

Framework for Financial Reporting

The primary aim of financial reporting standards is to facilitate high quality reporting of

financial information of corporations which is of utmost importance for decision making

different stakeholders of an economic entity.

An article was published in which it was said that “Financial Accounting Standards

Board (FASB) is taking crucial actions for enhancing the effectiveness of disclosure in financial

reporting” (FASB takes big steps on disclosure effectiveness, 2018).

Quality of conceptual framework depends upon two fundamental characteristics :

Relevance : the information reported in the financial statements shall be relevant , meaning of

which is that it must be capable of affecting the decisions of its users.

Faithful & honest disclosures : It means the information in financial reporting must be fair,

honest complete and must be free from any kind of error such as omission (Christensen & et.al.,

2015).

The accounting standard board of US has made two changes in its conceptual framework

for improving the disclosure of material information in the financial statements of company. By

reviewing the article, various benefits and limitations of the quality of conceptual framework for

financial reporting has been discovered. They are discussed in brief below :

Benefits

Quality of conceptual framework enhances the conference of users of financial

information of a company. It assists in changing the perception of people towards the

financial health of a corporate.

The conceptual framework of financial reporting facilitates a base against which the

major and core accounting practises can be measured and tested in an objective way

(Pichler, Cordazzo & Rossi, 2018).

International Financial Reporting Standards IFRS, 2017)

c.) On the basis of Journal articles review, critically discussing about the quality of Conceptual

Framework for Financial Reporting

The primary aim of financial reporting standards is to facilitate high quality reporting of

financial information of corporations which is of utmost importance for decision making

different stakeholders of an economic entity.

An article was published in which it was said that “Financial Accounting Standards

Board (FASB) is taking crucial actions for enhancing the effectiveness of disclosure in financial

reporting” (FASB takes big steps on disclosure effectiveness, 2018).

Quality of conceptual framework depends upon two fundamental characteristics :

Relevance : the information reported in the financial statements shall be relevant , meaning of

which is that it must be capable of affecting the decisions of its users.

Faithful & honest disclosures : It means the information in financial reporting must be fair,

honest complete and must be free from any kind of error such as omission (Christensen & et.al.,

2015).

The accounting standard board of US has made two changes in its conceptual framework

for improving the disclosure of material information in the financial statements of company. By

reviewing the article, various benefits and limitations of the quality of conceptual framework for

financial reporting has been discovered. They are discussed in brief below :

Benefits

Quality of conceptual framework enhances the conference of users of financial

information of a company. It assists in changing the perception of people towards the

financial health of a corporate.

The conceptual framework of financial reporting facilitates a base against which the

major and core accounting practises can be measured and tested in an objective way

(Pichler, Cordazzo & Rossi, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It often leads to more enhanced communication between the accounting standards setting

bodies and the accountants

It facilitates decision making with a constant approach. One of the major benefit of executive of conceptual framework is that it increases the

reliability and credibility of the financial reporting of the organisations throughout the

world.

Limitations

Integrating the IFRS completely is extremely a complex task for the nations. This is

because of the reason that developed countries have their own well established

conceptual frameworks while the countries which are in still in developing phase finding

it very costly and time consuming affair (Capkun, Collins & Jeanjean, 2016).

Rigidity is one of the limitation of conceptual framework, according to which only

standardised accounting practices are to be followed by corporates, this hinders the

possibility of introducing new ideas into accounting system.

Conflicts generally arise between the new accounting standards of IASB and the

standards which are already existing. The difference could be due to accounting practises

provided in different accounting standards of different accounting standards setting

bodies.

d.) Application of conceptual framework in Rio Tinto Ltd in its financial reporting

Australia is one of the first country in the world which adopted the entire IFRS

framework for financial reporting. All the public companies in Australia have to compulsorily

follow the IFRS standards while preparing their financial statements.

Rio Tinto Lt being a public Limited company has applied conceptual framework which

was known through its annual report of the year 2018. From the annual report, it has been known

that company is following IFRS and IAS in its accounting practice (Ioannou & Serafeim, 2017).

i) Different types of statements

Corporations listed on ASX needs to consider corporation act, accounting standard and IFRS

requirements. According to conceptual framework, it has to prepare following statements :

bodies and the accountants

It facilitates decision making with a constant approach. One of the major benefit of executive of conceptual framework is that it increases the

reliability and credibility of the financial reporting of the organisations throughout the

world.

Limitations

Integrating the IFRS completely is extremely a complex task for the nations. This is

because of the reason that developed countries have their own well established

conceptual frameworks while the countries which are in still in developing phase finding

it very costly and time consuming affair (Capkun, Collins & Jeanjean, 2016).

Rigidity is one of the limitation of conceptual framework, according to which only

standardised accounting practices are to be followed by corporates, this hinders the

possibility of introducing new ideas into accounting system.

Conflicts generally arise between the new accounting standards of IASB and the

standards which are already existing. The difference could be due to accounting practises

provided in different accounting standards of different accounting standards setting

bodies.

d.) Application of conceptual framework in Rio Tinto Ltd in its financial reporting

Australia is one of the first country in the world which adopted the entire IFRS

framework for financial reporting. All the public companies in Australia have to compulsorily

follow the IFRS standards while preparing their financial statements.

Rio Tinto Lt being a public Limited company has applied conceptual framework which

was known through its annual report of the year 2018. From the annual report, it has been known

that company is following IFRS and IAS in its accounting practice (Ioannou & Serafeim, 2017).

i) Different types of statements

Corporations listed on ASX needs to consider corporation act, accounting standard and IFRS

requirements. According to conceptual framework, it has to prepare following statements :

Statement of financial position : Balance sheet contains all the assets and liabilities of

company

Profit /Loss Statement and other comprehensive income : It includes all the income

earned during the year and all the manufacturing, operating, interests and taxes incurred

during the year.

Statement of changes in equity : It contains changes in shareholder's equity, dividend

payments made during a year, effect of variations due to different accounting policies etc. Cash flow statement : cash inflow/outflow from operating activities, cash flow finance

activities and cash flow from investing activities are the major components of cash flow

statement.

ii) Recognition and Measurement :

Revenue from sales is recognised when there is transfer of goods and services promised

by the company to its customers. The amount collected as revenue signifies the

consideration which the company is or expects to be entitled in lieu for goods and

services.

Assets : Fixed assets of the company are stated at cost which is based on IAS 16 which is

the amount after deduction of accumulated depreciation and accumulated impairment

losses. It has applied straight line method for depreciating non current assets.

Inventories are valued at cost or market value whichever is lower as per the

conceptual framework. Liabilities : Uncertain tax positions is recognised and measured under IFRIC 23 in which

weighted average approach has been applied. For Post employment benefits, IAS 19 has

been applied which considers the difference between fair value of plan assets and current

value of plan liability/obligations is recognised in balance sheet.

iii) Qualitative characteristics of information

Materiality : All the relevant and material information was disclosed as per the IFRS

standards.

company

Profit /Loss Statement and other comprehensive income : It includes all the income

earned during the year and all the manufacturing, operating, interests and taxes incurred

during the year.

Statement of changes in equity : It contains changes in shareholder's equity, dividend

payments made during a year, effect of variations due to different accounting policies etc. Cash flow statement : cash inflow/outflow from operating activities, cash flow finance

activities and cash flow from investing activities are the major components of cash flow

statement.

ii) Recognition and Measurement :

Revenue from sales is recognised when there is transfer of goods and services promised

by the company to its customers. The amount collected as revenue signifies the

consideration which the company is or expects to be entitled in lieu for goods and

services.

Assets : Fixed assets of the company are stated at cost which is based on IAS 16 which is

the amount after deduction of accumulated depreciation and accumulated impairment

losses. It has applied straight line method for depreciating non current assets.

Inventories are valued at cost or market value whichever is lower as per the

conceptual framework. Liabilities : Uncertain tax positions is recognised and measured under IFRIC 23 in which

weighted average approach has been applied. For Post employment benefits, IAS 19 has

been applied which considers the difference between fair value of plan assets and current

value of plan liability/obligations is recognised in balance sheet.

iii) Qualitative characteristics of information

Materiality : All the relevant and material information was disclosed as per the IFRS

standards.

Reliability : From the auditor report, it was observed that company applied the IFRS,

IAS and provisions of corporation act correctly without any errors and has declared the

report to be completely reliable (2018 Annual report, 2018)

PART B : INTEGRATED / SUSTAINABILITY REPORTING

a.) Comparing and contrasting the sustainability reporting of Global Reporting Initiative (GRI)

and International Integrated Reporting Framework of (IIRC)

Comparison between GRI and IIRC guidelines for sustainability reporting

Guidelines of Global Reporting Initiative asserts on what the organisation is doing to the

world and environment which renders it less or more sustainable. It is a non profit company

which operates with a network supported structure. The mission or primary aim of this body is

to make the sustainability reporting a uniform and standard practice (Maas, Schaltegger &

Crutzen, 2016).

Whereas the International Integrated Reporting Council which was established in 2010

August has an objective of developing a globally accredited and accepted set of rules that results

in organisation's communication regarding its value creation over passage of time. IIRC is more

focussed on matters regarding what shall an investor must know for making more money so that

value could be created.

b.) Explaining strengths and limitations of conventional accounting based upon conceptual

framework

Primary objective of conventional accounting is measuring and reporting economic

results of the company. While in the sustainability reports, it generally measures the socio-

economic non - financial effects along with the financial performance of the company.

Strengths of conventional accounting :

Provides the financial information in the most meaningful way when statements are

prepared under conceptual frameworks such as IAS, IFRS etc.

Provides the basis for comparison to users Helps in decision making in respect of investors regarding the matter such as investment

in the company would be a profitable venture for them or not. This is only when the

IAS and provisions of corporation act correctly without any errors and has declared the

report to be completely reliable (2018 Annual report, 2018)

PART B : INTEGRATED / SUSTAINABILITY REPORTING

a.) Comparing and contrasting the sustainability reporting of Global Reporting Initiative (GRI)

and International Integrated Reporting Framework of (IIRC)

Comparison between GRI and IIRC guidelines for sustainability reporting

Guidelines of Global Reporting Initiative asserts on what the organisation is doing to the

world and environment which renders it less or more sustainable. It is a non profit company

which operates with a network supported structure. The mission or primary aim of this body is

to make the sustainability reporting a uniform and standard practice (Maas, Schaltegger &

Crutzen, 2016).

Whereas the International Integrated Reporting Council which was established in 2010

August has an objective of developing a globally accredited and accepted set of rules that results

in organisation's communication regarding its value creation over passage of time. IIRC is more

focussed on matters regarding what shall an investor must know for making more money so that

value could be created.

b.) Explaining strengths and limitations of conventional accounting based upon conceptual

framework

Primary objective of conventional accounting is measuring and reporting economic

results of the company. While in the sustainability reports, it generally measures the socio-

economic non - financial effects along with the financial performance of the company.

Strengths of conventional accounting :

Provides the financial information in the most meaningful way when statements are

prepared under conceptual frameworks such as IAS, IFRS etc.

Provides the basis for comparison to users Helps in decision making in respect of investors regarding the matter such as investment

in the company would be a profitable venture for them or not. This is only when the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

company presents the financial reporting in the most accurate and fair form with the

application of accounting and reporting standards.

Limitation of conventional accounting :

Conventional accounting records less details of financial information. It does not take into account the socio-economic factors of the business

Contents of Sustainability and integrated reports :

Sustainability reporting can be described as the communication and revealing &

communication of company's environmental, social and governance report goals along with

organisation's success towards achieving them. The major advantages of sustainability reporting

is the increased acceptance from the society, more confidence of investors, higher room for

innovation and enhanced reputation of the business entity in the market (Stacchezzini, Melloni,

& Lai, 2016).

Integrated reporting can be described as the presentation of non financial and financial

information of a business concern in one single report. It is not only attaching the sustainability

report within the financial report of the company but it has a more wider meaning. It properly

aligns and link the activities of financial nature with the non financial activities and goals of the

company. The major benefit of integrated reporting is that it effectively communicates the

impact of operations of a firm on society and environment and a description of organisation's

commitment for reducing the negative or adverse impact if it had on the community and

ecosystem.

The basic components in both the type of reporting are :

Impact on environment

Impact on community

Impact on stakeholders including shareholders, investors and employees

Governance which includes ethics and code of conduct (Siew, 2015)

application of accounting and reporting standards.

Limitation of conventional accounting :

Conventional accounting records less details of financial information. It does not take into account the socio-economic factors of the business

Contents of Sustainability and integrated reports :

Sustainability reporting can be described as the communication and revealing &

communication of company's environmental, social and governance report goals along with

organisation's success towards achieving them. The major advantages of sustainability reporting

is the increased acceptance from the society, more confidence of investors, higher room for

innovation and enhanced reputation of the business entity in the market (Stacchezzini, Melloni,

& Lai, 2016).

Integrated reporting can be described as the presentation of non financial and financial

information of a business concern in one single report. It is not only attaching the sustainability

report within the financial report of the company but it has a more wider meaning. It properly

aligns and link the activities of financial nature with the non financial activities and goals of the

company. The major benefit of integrated reporting is that it effectively communicates the

impact of operations of a firm on society and environment and a description of organisation's

commitment for reducing the negative or adverse impact if it had on the community and

ecosystem.

The basic components in both the type of reporting are :

Impact on environment

Impact on community

Impact on stakeholders including shareholders, investors and employees

Governance which includes ethics and code of conduct (Siew, 2015)

c.) Discussing the applicability of the theories learned to explain the contents

of sustainability as well as integrated reports

Sustainability and integrated reporting is all about the non financial activities undertaken

by a company for achieving its environmental, social and governance goals. Large number of

corporations are publishing their sustainability or integrated reports so consistently that it has

become their standard procedure of preparing annual reports every year. Many organizations

follows the guidelines of Global Reporting Initiative (Hashim, Li & O’Hanlon, 2016). Over the

time, the names of such reports have transformed from corporate citizenship report to corporate

social responsibility then finally to integrated or sustainability reports. Different learnings

observed from the theories of sustainability and integrated reports. They are:

Assisting in maintaining trust factor : One of the benefits of sustainability reporting is

that it helps companies in enhancing the level of transparency between the business

operations and company’s stakeholders. It assists the firms in seeking feedbacks and

recommendations from investors and clients in declining their reputation-al risks. The

sustainability reports does the work of enhancing brand image in the market.\

Enhancing the strength of decision making : Maintaining sustainability while

conducting business encourages the organisations in introducing innovative process and

products of reducing their risks. This helps them in grabbing various opportunities

through innovation which in turn make those companies innovators and leaders. Reduce cost of compliance : Sustainability reporting is useful for companies because it

helps them in declining their cost of compliance.

Limitations of sustainability/ integrated reporting

Variation in the enforcement of reports relating to sustainability : There is no such

compulsion of preparing sustainability report which is the reason that standardisation can

not be achieved. It is an optional thing for the corporations and non compliance of this,

does not make them guilty of not adhering to the accounting legislation.

Most of the time, companies prepares sustainability reports only for the purpose of

promoting themselves for the good work they did. It should rather be more balanced like

the impact company's operations had on environment and society and how did they desire

of sustainability as well as integrated reports

Sustainability and integrated reporting is all about the non financial activities undertaken

by a company for achieving its environmental, social and governance goals. Large number of

corporations are publishing their sustainability or integrated reports so consistently that it has

become their standard procedure of preparing annual reports every year. Many organizations

follows the guidelines of Global Reporting Initiative (Hashim, Li & O’Hanlon, 2016). Over the

time, the names of such reports have transformed from corporate citizenship report to corporate

social responsibility then finally to integrated or sustainability reports. Different learnings

observed from the theories of sustainability and integrated reports. They are:

Assisting in maintaining trust factor : One of the benefits of sustainability reporting is

that it helps companies in enhancing the level of transparency between the business

operations and company’s stakeholders. It assists the firms in seeking feedbacks and

recommendations from investors and clients in declining their reputation-al risks. The

sustainability reports does the work of enhancing brand image in the market.\

Enhancing the strength of decision making : Maintaining sustainability while

conducting business encourages the organisations in introducing innovative process and

products of reducing their risks. This helps them in grabbing various opportunities

through innovation which in turn make those companies innovators and leaders. Reduce cost of compliance : Sustainability reporting is useful for companies because it

helps them in declining their cost of compliance.

Limitations of sustainability/ integrated reporting

Variation in the enforcement of reports relating to sustainability : There is no such

compulsion of preparing sustainability report which is the reason that standardisation can

not be achieved. It is an optional thing for the corporations and non compliance of this,

does not make them guilty of not adhering to the accounting legislation.

Most of the time, companies prepares sustainability reports only for the purpose of

promoting themselves for the good work they did. It should rather be more balanced like

the impact company's operations had on environment and society and how did they desire

to increase or decrease positive/negative impacts respectively (Maas, Schaltegger &

Crutzen, 2016).

Institutional theory:

It is comprised of social behaviours where guidelines for structures, rules, norms,

schemes as well as routine schedule has been determined under the organisation. Therefore, it

can be said that such theory funnels the managerial professionals in analysing and making a

corrective decision for scheduling the operational practices in industry.

Legitimacy theory:

This is entitled with the CSR responsibilities of an organisation towards the disclosure

practices, recent research as well as ascertainment of environmental requirements. However,

analysing the current operating state of the business as per the market desires would lead the firm

in retaining the adequate gains.

Stakeholder Theory:

It is based on the theory used for organisational management as well as ascertainment of

business ethics would lead the firm in constituting the accounts for business entities such as

employees, local communities, creditors and suppliers.

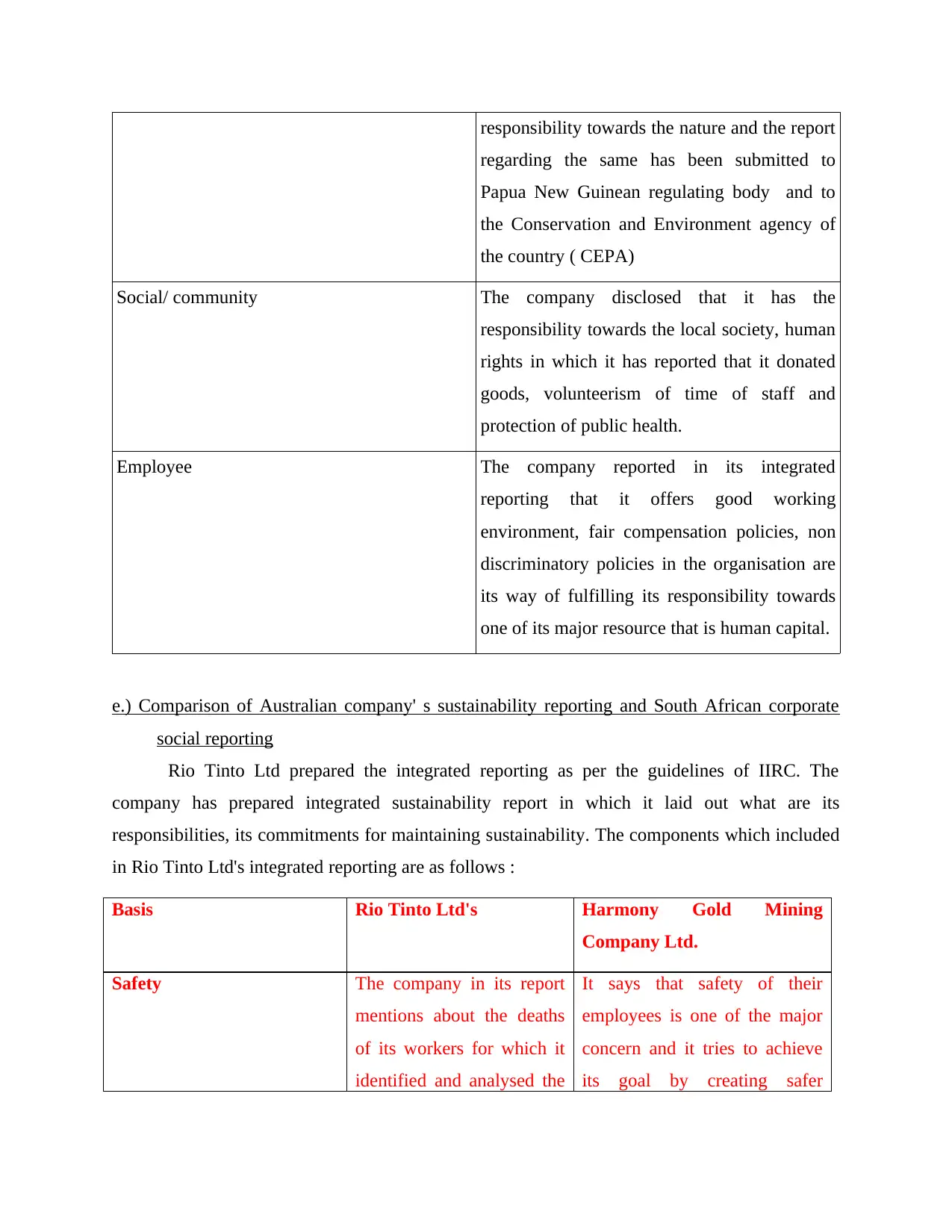

d.) Preparation of a check list that contains the components of integrated report

Integrated reporting states different components that will be discussed through a

checklist.

Components of sustainability reporting How South African company Harmony

Gold Mine has disclosed information

Voluntary and mandatory Corporate

governance

Harmony Gold mine has disclosed in its

annual report that it has followed the South

African Code for reporting Mineral resources

and reserves of mineral.

Safety

Environmental impact The chief executive officer of the company

told in the annual report that it is fulfilling its

Crutzen, 2016).

Institutional theory:

It is comprised of social behaviours where guidelines for structures, rules, norms,

schemes as well as routine schedule has been determined under the organisation. Therefore, it

can be said that such theory funnels the managerial professionals in analysing and making a

corrective decision for scheduling the operational practices in industry.

Legitimacy theory:

This is entitled with the CSR responsibilities of an organisation towards the disclosure

practices, recent research as well as ascertainment of environmental requirements. However,

analysing the current operating state of the business as per the market desires would lead the firm

in retaining the adequate gains.

Stakeholder Theory:

It is based on the theory used for organisational management as well as ascertainment of

business ethics would lead the firm in constituting the accounts for business entities such as

employees, local communities, creditors and suppliers.

d.) Preparation of a check list that contains the components of integrated report

Integrated reporting states different components that will be discussed through a

checklist.

Components of sustainability reporting How South African company Harmony

Gold Mine has disclosed information

Voluntary and mandatory Corporate

governance

Harmony Gold mine has disclosed in its

annual report that it has followed the South

African Code for reporting Mineral resources

and reserves of mineral.

Safety

Environmental impact The chief executive officer of the company

told in the annual report that it is fulfilling its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

responsibility towards the nature and the report

regarding the same has been submitted to

Papua New Guinean regulating body and to

the Conservation and Environment agency of

the country ( CEPA)

Social/ community The company disclosed that it has the

responsibility towards the local society, human

rights in which it has reported that it donated

goods, volunteerism of time of staff and

protection of public health.

Employee The company reported in its integrated

reporting that it offers good working

environment, fair compensation policies, non

discriminatory policies in the organisation are

its way of fulfilling its responsibility towards

one of its major resource that is human capital.

e.) Comparison of Australian company' s sustainability reporting and South African corporate

social reporting

Rio Tinto Ltd prepared the integrated reporting as per the guidelines of IIRC. The

company has prepared integrated sustainability report in which it laid out what are its

responsibilities, its commitments for maintaining sustainability. The components which included

in Rio Tinto Ltd's integrated reporting are as follows :

Basis Rio Tinto Ltd's Harmony Gold Mining

Company Ltd.

Safety The company in its report

mentions about the deaths

of its workers for which it

identified and analysed the

It says that safety of their

employees is one of the major

concern and it tries to achieve

its goal by creating safer

regarding the same has been submitted to

Papua New Guinean regulating body and to

the Conservation and Environment agency of

the country ( CEPA)

Social/ community The company disclosed that it has the

responsibility towards the local society, human

rights in which it has reported that it donated

goods, volunteerism of time of staff and

protection of public health.

Employee The company reported in its integrated

reporting that it offers good working

environment, fair compensation policies, non

discriminatory policies in the organisation are

its way of fulfilling its responsibility towards

one of its major resource that is human capital.

e.) Comparison of Australian company' s sustainability reporting and South African corporate

social reporting

Rio Tinto Ltd prepared the integrated reporting as per the guidelines of IIRC. The

company has prepared integrated sustainability report in which it laid out what are its

responsibilities, its commitments for maintaining sustainability. The components which included

in Rio Tinto Ltd's integrated reporting are as follows :

Basis Rio Tinto Ltd's Harmony Gold Mining

Company Ltd.

Safety The company in its report

mentions about the deaths

of its workers for which it

identified and analysed the

It says that safety of their

employees is one of the major

concern and it tries to achieve

its goal by creating safer

causes behind such deaths

so that lesson can be

learned and effective

correction actions could be

taken in the future for

mitigating such incidents.

working environment.

Environment The provided in its annual

report that internal audit

team reviewed the internal

control measures'

effectiveness.

Tailings and water waste

activities were some

environmental issues which

were highlighted in internal

audit review. The company

focussed on effective tailing

management.

Communities The company desires to

maintain healthy

relationships with

communities, society,

employees and also its

supply chain.

Harmony has been entitled with

imposing various regulatory

costs relevant with the

royalties, mining taxes. It has

affected the business in

operations and in profitability.

Closure and remediation The organisation

communicated that it

requires to manage

diligently the impact of

closure with its business

communities.

The rehabilitation and closure

costs are significant which is

generally based on current legal

and legislative requirements

that may affect a change in

materiality.

Governance and reporting The company

communicated that it

follows the code of conduct

of both UK corporate code

It has been complied with

reformative variations in the

governance as well as public

disclosure that adds uncertainty

so that lesson can be

learned and effective

correction actions could be

taken in the future for

mitigating such incidents.

working environment.

Environment The provided in its annual

report that internal audit

team reviewed the internal

control measures'

effectiveness.

Tailings and water waste

activities were some

environmental issues which

were highlighted in internal

audit review. The company

focussed on effective tailing

management.

Communities The company desires to

maintain healthy

relationships with

communities, society,

employees and also its

supply chain.

Harmony has been entitled with

imposing various regulatory

costs relevant with the

royalties, mining taxes. It has

affected the business in

operations and in profitability.

Closure and remediation The organisation

communicated that it

requires to manage

diligently the impact of

closure with its business

communities.

The rehabilitation and closure

costs are significant which is

generally based on current legal

and legislative requirements

that may affect a change in

materiality.

Governance and reporting The company

communicated that it

follows the code of conduct

of both UK corporate code

It has been complied with

reformative variations in the

governance as well as public

disclosure that adds uncertainty

of governance and ASX

corporate governance.

to compliance policies and

affect a increase in such costs.

CONCLUSION

From the above project report, it can be summarised that conceptual framework is a set of

rules that lays down the standards for reporting and disclosing the financial information of the

company. This a global accounting body called as International Accounting Standards Board

(IASB) which is concerned with the formulation of accounting standards and improvisation of

the same. This body has laid out IFRS which are the standards for financial reporting and

Australia was first nation which adopted the entire IFRS standards in its accounting framework.

However, the accounting professional had some concerns regarding the implementation of the

IFRS like it was matter of concern when it was commented that many of the international

standards are very rarely used by the Australian public companies in practice which leaves those

standards untested. Further, in the report it was highlighted that company are increasingly using

sustainability reporting due to its benefits such as it assists in maintaining trust factor, enhancing

the strength of decision making and reducing the cost of compliance.

corporate governance.

to compliance policies and

affect a increase in such costs.

CONCLUSION

From the above project report, it can be summarised that conceptual framework is a set of

rules that lays down the standards for reporting and disclosing the financial information of the

company. This a global accounting body called as International Accounting Standards Board

(IASB) which is concerned with the formulation of accounting standards and improvisation of

the same. This body has laid out IFRS which are the standards for financial reporting and

Australia was first nation which adopted the entire IFRS standards in its accounting framework.

However, the accounting professional had some concerns regarding the implementation of the

IFRS like it was matter of concern when it was commented that many of the international

standards are very rarely used by the Australian public companies in practice which leaves those

standards untested. Further, in the report it was highlighted that company are increasingly using

sustainability reporting due to its benefits such as it assists in maintaining trust factor, enhancing

the strength of decision making and reducing the cost of compliance.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Abdel-Khalik, A. R. (2019). The FASB and IASB Achilles Heel: Unfaithful Representations of

Financial Instruments. Available at SSRN 3357733.

Morley, J. (2016). Internal lobbying at the IASB. Journal of Accounting and Public Policy. 35(3).

224-255.\

Hashim, N., Li, W., & O’Hanlon, J. (2016). Expected-loss-based accounting for impairment of

financial instruments: The FASB and IASB proposals 2009–2016. Accounting in

Europe. 13(2). 229-267.\

Eisenschmidt, K., & Schmidt, M. (2016). Responsiveness as a challenge for the legitimacy of the

IASB-An evaluation of current international accounting regulation and of alternative

approaches. Available at SSRN 2772445.

Harmon, F., & Ntseh, D. (2016). The New FASB & IASB Revenue Recognition Standards;

Implementation and Effects.

Christensen, H. B & et.al., (2015). Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). 31-61.

Pichler, S., Cordazzo, M., & Rossi, P. (2018). An analysis of the firms-specific determinants

influencing the voluntary IFRS adoption: evidence from Italian private firms. International

Journal of Accounting, Auditing and Performance Evaluation. 14(1). 85-104.

Capkun, V., Collins, D., & Jeanjean, T. (2016). The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting

and Public Policy, 35(4), 352-394.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting. Harvard Business School research working paper, (11-100).

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136. 237-

248.\

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability

management. Journal of Cleaner Production. 136. 102-110.

Siew, R. Y. (2015). A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management. 164. 180-195.

Online

Conceptual Framework for Financial Reporting.2018. [Online]. Available through

<https://www.ifrs.org/-/media/project/conceptual-framework/fact-sheet-project-summary-

and-feedback-statement/conceptual-framework-project-summary.pdf>

Australian Implementation of International Financial Reporting Standards IFRS. 2017. [Online].

Available through

<http://www.companydirectors.com.au/Director-Resource-Centre/Policy-on-director-

Books and Journals

Abdel-Khalik, A. R. (2019). The FASB and IASB Achilles Heel: Unfaithful Representations of

Financial Instruments. Available at SSRN 3357733.

Morley, J. (2016). Internal lobbying at the IASB. Journal of Accounting and Public Policy. 35(3).

224-255.\

Hashim, N., Li, W., & O’Hanlon, J. (2016). Expected-loss-based accounting for impairment of

financial instruments: The FASB and IASB proposals 2009–2016. Accounting in

Europe. 13(2). 229-267.\

Eisenschmidt, K., & Schmidt, M. (2016). Responsiveness as a challenge for the legitimacy of the

IASB-An evaluation of current international accounting regulation and of alternative

approaches. Available at SSRN 2772445.

Harmon, F., & Ntseh, D. (2016). The New FASB & IASB Revenue Recognition Standards;

Implementation and Effects.

Christensen, H. B & et.al., (2015). Incentives or standards: What determines accounting quality

changes around IFRS adoption?. European Accounting Review. 24(1). 31-61.

Pichler, S., Cordazzo, M., & Rossi, P. (2018). An analysis of the firms-specific determinants

influencing the voluntary IFRS adoption: evidence from Italian private firms. International

Journal of Accounting, Auditing and Performance Evaluation. 14(1). 85-104.

Capkun, V., Collins, D., & Jeanjean, T. (2016). The effect of IAS/IFRS adoption on earnings

management (smoothing): A closer look at competing explanations. Journal of Accounting

and Public Policy, 35(4), 352-394.

Ioannou, I., & Serafeim, G. (2017). The consequences of mandatory corporate sustainability

reporting. Harvard Business School research working paper, (11-100).

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production. 136. 237-

248.\

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability

management. Journal of Cleaner Production. 136. 102-110.

Siew, R. Y. (2015). A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management. 164. 180-195.

Online

Conceptual Framework for Financial Reporting.2018. [Online]. Available through

<https://www.ifrs.org/-/media/project/conceptual-framework/fact-sheet-project-summary-

and-feedback-statement/conceptual-framework-project-summary.pdf>

Australian Implementation of International Financial Reporting Standards IFRS. 2017. [Online].

Available through

<http://www.companydirectors.com.au/Director-Resource-Centre/Policy-on-director-

issues/Policy-Submissions/2005/Australian-Implementation-of-International-Financial-

Reporting-S>

FASB takes big steps on disclosure effectiveness. 2018. [Online]. Available through

<https://www.journalofaccountancy.com/news/2018/aug/fasb-disclosure-effectiveness-

201819617.html>

2018 Annual report. 2018. [Online]. Available through

<http://www.riotinto.com/documents/RT_2018_annual_report.pdf>

Reporting-S>

FASB takes big steps on disclosure effectiveness. 2018. [Online]. Available through

<https://www.journalofaccountancy.com/news/2018/aug/fasb-disclosure-effectiveness-

201819617.html>

2018 Annual report. 2018. [Online]. Available through

<http://www.riotinto.com/documents/RT_2018_annual_report.pdf>

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.