Contemporary Accounting Theory: Report

VerifiedAdded on 2021/02/20

|18

|5216

|36

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

CONTEMPORARY

ACCOUNTING THEORY

ACCOUNTING THEORY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................3

PART A ..........................................................................................................................................3

a. History and development of the Conceptual Framework for Financial Reporting in the

USA, UK, Australia under the International Accounting Standards Board (IASB)...................3

b. Defining application of the International Accounting Standard Board / International

Financial Reporting Standard in Conceptual Framework for Financial Reporting....................4

c. Discussion regarding the advantages and the disadvantages of the conceptual framework in

respect of the financial reporting.................................................................................................5

d. Case.........................................................................................................................................6

(i) Statements or reports prepared as per the Conceptual Framework along with their major

components.................................................................................................................................6

(ii) Recognition principles and measurement bases applied for revenue, assets and liabilities..7

(iii) Qualitative characteristics of information exhibit in company’s various financial reports.

.....................................................................................................................................................7

PART B............................................................................................................................................8

a. Defining broader view of corporate social responsibility reporting in addition to reporting

of corporate financial performance.............................................................................................8

b. Defining strengths and limitations of the conventional accounting based on the Conceptual

Framework for Financial Reporting............................................................................................9

c. Applicability of the theories of sustainability as well as integrated reports..........................10

d. Preparing an index of various components of an integrated report......................................11

e. Comparing the contents of corporate social responsibility reporting & integrated reporting

Tabcorp Holdings Ltd with Curro Holdings Ltd. .....................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................2

MAIN BODY...................................................................................................................................3

PART A ..........................................................................................................................................3

a. History and development of the Conceptual Framework for Financial Reporting in the

USA, UK, Australia under the International Accounting Standards Board (IASB)...................3

b. Defining application of the International Accounting Standard Board / International

Financial Reporting Standard in Conceptual Framework for Financial Reporting....................4

c. Discussion regarding the advantages and the disadvantages of the conceptual framework in

respect of the financial reporting.................................................................................................5

d. Case.........................................................................................................................................6

(i) Statements or reports prepared as per the Conceptual Framework along with their major

components.................................................................................................................................6

(ii) Recognition principles and measurement bases applied for revenue, assets and liabilities..7

(iii) Qualitative characteristics of information exhibit in company’s various financial reports.

.....................................................................................................................................................7

PART B............................................................................................................................................8

a. Defining broader view of corporate social responsibility reporting in addition to reporting

of corporate financial performance.............................................................................................8

b. Defining strengths and limitations of the conventional accounting based on the Conceptual

Framework for Financial Reporting............................................................................................9

c. Applicability of the theories of sustainability as well as integrated reports..........................10

d. Preparing an index of various components of an integrated report......................................11

e. Comparing the contents of corporate social responsibility reporting & integrated reporting

Tabcorp Holdings Ltd with Curro Holdings Ltd. .....................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

EXECUTIVE SUMMARY

With the help of accounting standards and policies, a company can make proper and effective

financial statements. The report is based on the application of International Accounting standards

and procedures. The report will discuss about two companies named as Tabcorp Holdings

Limited and Curro holdings Limited. In the report, history and development related to the

conceptual framework for financial reporting will be described. Also, it will discuss about the

integrated and the sustainability of the reporting with appropriate guidelines.

INTRODUCTION

Accounting theory refers to the set of the assumptions, methodologies and the framework

that has been used for making the study. The application of the financial principles in respect of

reporting are also called as the accounting theories. Contemporary accounting theory include a

review of the historical foundations relating to the practices of the accounting and the ways by

which these practices are been changed and entered in the regulatory framework which governs

the financial reporting and the statements. Moreover, accounting theory is said to be the logical

reasoning which helps in evaluating and guiding the accounting practices. It also helps in

developing the new practices and the procedures for the accounting. The present study is based

on the two companies one is Australian company and other is South African company named as

Tabcorp Holdings Limited which is engaged in the business of entertainment and gambling

across the world. Another company is Curro holdings limited the largest private company

dealing in education sector. Furthermore, the report will include the conceptual framework in

relation to the international accounting standards for the board. The study also describes the

integrated and the sustainability of the reporting with appropriate guidelines.

With the help of accounting standards and policies, a company can make proper and effective

financial statements. The report is based on the application of International Accounting standards

and procedures. The report will discuss about two companies named as Tabcorp Holdings

Limited and Curro holdings Limited. In the report, history and development related to the

conceptual framework for financial reporting will be described. Also, it will discuss about the

integrated and the sustainability of the reporting with appropriate guidelines.

INTRODUCTION

Accounting theory refers to the set of the assumptions, methodologies and the framework

that has been used for making the study. The application of the financial principles in respect of

reporting are also called as the accounting theories. Contemporary accounting theory include a

review of the historical foundations relating to the practices of the accounting and the ways by

which these practices are been changed and entered in the regulatory framework which governs

the financial reporting and the statements. Moreover, accounting theory is said to be the logical

reasoning which helps in evaluating and guiding the accounting practices. It also helps in

developing the new practices and the procedures for the accounting. The present study is based

on the two companies one is Australian company and other is South African company named as

Tabcorp Holdings Limited which is engaged in the business of entertainment and gambling

across the world. Another company is Curro holdings limited the largest private company

dealing in education sector. Furthermore, the report will include the conceptual framework in

relation to the international accounting standards for the board. The study also describes the

integrated and the sustainability of the reporting with appropriate guidelines.

MAIN BODY

PART A

a. History and development of the Conceptual Framework for Financial Reporting in the USA,

UK, Australia under the International Accounting Standards Board (IASB).

The international Accounting standard committee has published conceptual framework

for financial reporting in the year 1989. The main objective behind framing of these frameworks

is to provide guidance for both international as well as national standard framers related to

standard setting (Flower, 2018). This also helps in resolving issues related to accounting

transaction which is not provided by these standards as well.

Development of these standard has been made because of following reasons:

For providing a better framework as well as norms with the aim of framing of better

accounting standards.

For resolving all the disputes related to accounting transactions.

With the aim of defining fundamental principles which are not to be repeated in

accounting standards again.

The conceptual Framework is a system or concept related to meaningful ideas, thoughts

and objectives which can assist every business organisation by creating a definite as well as

consistent set of rules, standards and norms (Leuz and Wysocki, 2016). These frameworks are

specifically related to accounting and financial management system of the company. With the

help of the set defined rules and standards in context of accounting, it lays down the nature,

function, concept for Financial Reporting. It also defines the limits in case of preparation of

financial accounting and statements of the company. These Conceptual Framework sets out the

relevant fundamental concepts which are considered as essential for making of the financial

reporting. It also helps in providing proper guidance to the International Accounting Standards

Board which further helps in developing International Financial Reporting Standards.

With on the going amendments and development of these standards, it has also helps in

ensuring that standards are more conceptually framed. Also, it has emphasized that there is a

proper consistency in treating of all the similar transactions in the same way, so as to provide

PART A

a. History and development of the Conceptual Framework for Financial Reporting in the USA,

UK, Australia under the International Accounting Standards Board (IASB).

The international Accounting standard committee has published conceptual framework

for financial reporting in the year 1989. The main objective behind framing of these frameworks

is to provide guidance for both international as well as national standard framers related to

standard setting (Flower, 2018). This also helps in resolving issues related to accounting

transaction which is not provided by these standards as well.

Development of these standard has been made because of following reasons:

For providing a better framework as well as norms with the aim of framing of better

accounting standards.

For resolving all the disputes related to accounting transactions.

With the aim of defining fundamental principles which are not to be repeated in

accounting standards again.

The conceptual Framework is a system or concept related to meaningful ideas, thoughts

and objectives which can assist every business organisation by creating a definite as well as

consistent set of rules, standards and norms (Leuz and Wysocki, 2016). These frameworks are

specifically related to accounting and financial management system of the company. With the

help of the set defined rules and standards in context of accounting, it lays down the nature,

function, concept for Financial Reporting. It also defines the limits in case of preparation of

financial accounting and statements of the company. These Conceptual Framework sets out the

relevant fundamental concepts which are considered as essential for making of the financial

reporting. It also helps in providing proper guidance to the International Accounting Standards

Board which further helps in developing International Financial Reporting Standards.

With on the going amendments and development of these standards, it has also helps in

ensuring that standards are more conceptually framed. Also, it has emphasized that there is a

proper consistency in treating of all the similar transactions in the same way, so as to provide

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

more meaningful as well as useful information to all the investors, suppliers, lenders, creditors

and other stakeholders.

The Conceptual Framework for financial reporting also assists many companies in

developing as well as framing of better and effective accounting policies in case when no

International Financial Reporting Standard applies to a specific accounting transaction. With the

development of these standards it has helped various stakeholders in making proper and better

understanding and interpreting of the applicable accounting Standards (Beaulieu, Sarker and

Sarker, 2015). The main aim behind development of this standard is to provide better system or

framework to company for framing of accounting standards necessary for resolving issues

related to accounting transactions etc.

b. Defining application of the International Accounting Standard Board / International Financial

Reporting Standard in Conceptual Framework for Financial Reporting.

The application of this framework in business organisation plays a very important role in

the framing as well as development of the accounting standards. These conceptual frameworks

form a basis mainly theoretical in nature, for ascertaining how accounting transactions of the

business to be measured, analysed and reported. It also helps in defining the manner in which

these are presented in the financial statement & thus communicated to its end users for

interpretation. These frameworks provides a better understanding of relevant accounting

practices, concepts, standards, norms to its users and also assist in preparation of financial

statements of the company (Cho and et.al., 2015). With the application of this conceptual

framework for financial reporting, it provides following uses to companies which are as follows:

1. Conceptual Framework related to financial reporting focuses on framing of meaningful

and relevant definitions which aids in making important discussion related to

accounting issues. This issue are further supported by resolution.

2. It helps in providing better and important guidance to all the framers of accounting

standard at the time of developing and reviewing of the financial reporting rules.

3. This framework designed helps the company by ensuring that accounting standards of

the company are internally consistent and followed properly.

and other stakeholders.

The Conceptual Framework for financial reporting also assists many companies in

developing as well as framing of better and effective accounting policies in case when no

International Financial Reporting Standard applies to a specific accounting transaction. With the

development of these standards it has helped various stakeholders in making proper and better

understanding and interpreting of the applicable accounting Standards (Beaulieu, Sarker and

Sarker, 2015). The main aim behind development of this standard is to provide better system or

framework to company for framing of accounting standards necessary for resolving issues

related to accounting transactions etc.

b. Defining application of the International Accounting Standard Board / International Financial

Reporting Standard in Conceptual Framework for Financial Reporting.

The application of this framework in business organisation plays a very important role in

the framing as well as development of the accounting standards. These conceptual frameworks

form a basis mainly theoretical in nature, for ascertaining how accounting transactions of the

business to be measured, analysed and reported. It also helps in defining the manner in which

these are presented in the financial statement & thus communicated to its end users for

interpretation. These frameworks provides a better understanding of relevant accounting

practices, concepts, standards, norms to its users and also assist in preparation of financial

statements of the company (Cho and et.al., 2015). With the application of this conceptual

framework for financial reporting, it provides following uses to companies which are as follows:

1. Conceptual Framework related to financial reporting focuses on framing of meaningful

and relevant definitions which aids in making important discussion related to

accounting issues. This issue are further supported by resolution.

2. It helps in providing better and important guidance to all the framers of accounting

standard at the time of developing and reviewing of the financial reporting rules.

3. This framework designed helps the company by ensuring that accounting standards of

the company are internally consistent and followed properly.

4. Sometime, it helps in the preparation of financial statements to its maker as well as to

auditors of the company by resolving all the issues and problems related to the

financial reporting in the absence of proper accounting standard.

5. It also assist the company in setting the limit related to the volume of accounting

standards by giving proper definition, concepts and theory related to accounting

transactions (Corporate Financial Reporting, 2019). This further supports company in

applying of these frameworks in case of specific financial reporting problems.

c. Discussion regarding the advantages and the disadvantages of the conceptual framework in

respect of the financial reporting.

Conceptual framework in the context of the financial reporting is defined as the system of

the objectives and the ideas which results in developing the consistent set of the standards and

the rules (Chih and Zwikael, 2015). These rules and standards are applied in preparation of the

financial statements so that reporting can be made in compliance with all the regulations. There

are various benefits and the limitations that are present in the conceptual framework as follows-

Benefits - Creating the conceptual framework for reporting facilitates adequate

definitions relating to the concepts which in turn provides for the adequate measurement. An

individual can generate many ideas through the conceptual framework. It allows for the effective

communication in between the academics as some individual communicate in the different

languages and on the basis of that make the implicit assumptions and the concepts unconsciously

by not considering the other readers (Osanaiye, Choo and Dlodlo, 2016). Moreover, Conceptual

framework for the reporting allows for the clarification relating to the assumptions, implied

variables and the frames of the reference. It provides for the fixed set of the rules which in turn

leads consistency in the financial reporting.

Limitations - The major limitation that are associated with conceptual framework are that

it is dynamic in nature which means keeps on changing which leads in lack of consistency and

timely changes has to be made by the practitioner (Ovaskainen and et.al., 2017). Furthermore,

Until this framework are not tested empirically, it results in inadequacy regarding its application

in the practice, subjective perspective and limited reporting can be presented.

auditors of the company by resolving all the issues and problems related to the

financial reporting in the absence of proper accounting standard.

5. It also assist the company in setting the limit related to the volume of accounting

standards by giving proper definition, concepts and theory related to accounting

transactions (Corporate Financial Reporting, 2019). This further supports company in

applying of these frameworks in case of specific financial reporting problems.

c. Discussion regarding the advantages and the disadvantages of the conceptual framework in

respect of the financial reporting.

Conceptual framework in the context of the financial reporting is defined as the system of

the objectives and the ideas which results in developing the consistent set of the standards and

the rules (Chih and Zwikael, 2015). These rules and standards are applied in preparation of the

financial statements so that reporting can be made in compliance with all the regulations. There

are various benefits and the limitations that are present in the conceptual framework as follows-

Benefits - Creating the conceptual framework for reporting facilitates adequate

definitions relating to the concepts which in turn provides for the adequate measurement. An

individual can generate many ideas through the conceptual framework. It allows for the effective

communication in between the academics as some individual communicate in the different

languages and on the basis of that make the implicit assumptions and the concepts unconsciously

by not considering the other readers (Osanaiye, Choo and Dlodlo, 2016). Moreover, Conceptual

framework for the reporting allows for the clarification relating to the assumptions, implied

variables and the frames of the reference. It provides for the fixed set of the rules which in turn

leads consistency in the financial reporting.

Limitations - The major limitation that are associated with conceptual framework are that

it is dynamic in nature which means keeps on changing which leads in lack of consistency and

timely changes has to be made by the practitioner (Ovaskainen and et.al., 2017). Furthermore,

Until this framework are not tested empirically, it results in inadequacy regarding its application

in the practice, subjective perspective and limited reporting can be presented.

Financial reporting is a report in which company makes disclosure about all its financial

as well as business transaction which has taken place during a specific period of time.

Benefits – With this report business organization can make comparison of their

individual performance with its rivalry firm of same industry. This assist companies in

improving their overall business performance level and increase profitability. Can be used as a

basis for formulation of budget of next as well as current year.

Limitations – For preparing the financial statements proper compliance with set of

accounting standards, rules, procedures has to be made by company (Henderson and et.al.,

2015). Also, for preparing this expertise is needed as a result of which organization has to

employ highly qualified professionals which in turn increase their cost.

d. Case

(i) Statements or reports prepared as per the Conceptual Framework along with their major

components.

Tabcorp Holdings Limited is a company which is limited by shares being traded on the

Australian Securities Exchange. This Company is incorporated in Australia with the aim of

earning more profit (Tabcorp holdings limited annual report, 2018). The Financial Report of the

Company prepared for the year ended 30 June 2018 comprises of the Parent Company and its

subsidiaries known as the Group along with the interest factor of the Group in the joint

arrangements and associates.

The authorisation for issuing of the Financial Report prepared as per the Conceptual

Framework was given by the Board of Directors on 8 August 2018. The Financial Report of the

company has been prepared in accordance with compliance of the Corporations Act 2001,

Australian Accounting Standards (issued by the Australian Accounting Standards Board) and

other norms related to the financial reporting requirements in Australia.

Also, it has complied with the provisions of International Financial Reporting Standards

issued by the International Accounting Standards Board. Major components of report are:

1. Income Statement – Revenue and expenditure

2. Balance Sheet – assets and liabilities

3. Cash Flow Statement – inflow and outflow of money

as well as business transaction which has taken place during a specific period of time.

Benefits – With this report business organization can make comparison of their

individual performance with its rivalry firm of same industry. This assist companies in

improving their overall business performance level and increase profitability. Can be used as a

basis for formulation of budget of next as well as current year.

Limitations – For preparing the financial statements proper compliance with set of

accounting standards, rules, procedures has to be made by company (Henderson and et.al.,

2015). Also, for preparing this expertise is needed as a result of which organization has to

employ highly qualified professionals which in turn increase their cost.

d. Case

(i) Statements or reports prepared as per the Conceptual Framework along with their major

components.

Tabcorp Holdings Limited is a company which is limited by shares being traded on the

Australian Securities Exchange. This Company is incorporated in Australia with the aim of

earning more profit (Tabcorp holdings limited annual report, 2018). The Financial Report of the

Company prepared for the year ended 30 June 2018 comprises of the Parent Company and its

subsidiaries known as the Group along with the interest factor of the Group in the joint

arrangements and associates.

The authorisation for issuing of the Financial Report prepared as per the Conceptual

Framework was given by the Board of Directors on 8 August 2018. The Financial Report of the

company has been prepared in accordance with compliance of the Corporations Act 2001,

Australian Accounting Standards (issued by the Australian Accounting Standards Board) and

other norms related to the financial reporting requirements in Australia.

Also, it has complied with the provisions of International Financial Reporting Standards

issued by the International Accounting Standards Board. Major components of report are:

1. Income Statement – Revenue and expenditure

2. Balance Sheet – assets and liabilities

3. Cash Flow Statement – inflow and outflow of money

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Statement of changes in equity – equity portion

5. Notes to the financial statements – detail explanation about statements made

6. Directors’ declaration – interest and power of directors

7. Independent auditor’s report – provides details about audit by auditor in his audit report

The report is presented in Australian dollars with dollar amounts rounded to the nearest

hundred thousand. Also, focus is made at the time of report preparation on the historical cost

except derivative financial instruments and financial assets available for sale measured at fair

value. Also, compliance has been made related to use of accounting policies consistently by all

the Group for preparing the Financial Report.

(ii) Recognition principles and measurement bases applied for revenue, assets and liabilities.

The revenue recognition principle of accounting states that revenue are recognised at the

time when they are realized and are earned. It doesn’t get affected by period when the cash will

be received. The company has recorded its revenue when it has been earned by the business and

not when it is collected. Its assets and liabilities are recorded at fair value as well. Also, the

company has follows cost concept, going concern concept, consistency concept and materiality

concept for preparing its financials.

(iii) Qualitative characteristics of information exhibit in company’s various financial reports.

The qualitative characteristics used by the company in its financial report are:

1. Relevance – Information provided in financial statement should be of relevant nature

from the perspective of end user. It must assist its user in decision making process.

2. Materiality – Any omission or error at the time of recording of financial transaction if is

of material nature should be disclosed properly.

3. Reliability – Information presented in company financial report must be free from all

material error and biases so that it can become reliable. All the information should depict

true and fair picture about company.

5. Notes to the financial statements – detail explanation about statements made

6. Directors’ declaration – interest and power of directors

7. Independent auditor’s report – provides details about audit by auditor in his audit report

The report is presented in Australian dollars with dollar amounts rounded to the nearest

hundred thousand. Also, focus is made at the time of report preparation on the historical cost

except derivative financial instruments and financial assets available for sale measured at fair

value. Also, compliance has been made related to use of accounting policies consistently by all

the Group for preparing the Financial Report.

(ii) Recognition principles and measurement bases applied for revenue, assets and liabilities.

The revenue recognition principle of accounting states that revenue are recognised at the

time when they are realized and are earned. It doesn’t get affected by period when the cash will

be received. The company has recorded its revenue when it has been earned by the business and

not when it is collected. Its assets and liabilities are recorded at fair value as well. Also, the

company has follows cost concept, going concern concept, consistency concept and materiality

concept for preparing its financials.

(iii) Qualitative characteristics of information exhibit in company’s various financial reports.

The qualitative characteristics used by the company in its financial report are:

1. Relevance – Information provided in financial statement should be of relevant nature

from the perspective of end user. It must assist its user in decision making process.

2. Materiality – Any omission or error at the time of recording of financial transaction if is

of material nature should be disclosed properly.

3. Reliability – Information presented in company financial report must be free from all

material error and biases so that it can become reliable. All the information should depict

true and fair picture about company.

PART B

a. Defining broader view of corporate social responsibility reporting in addition to reporting of

corporate financial performance.

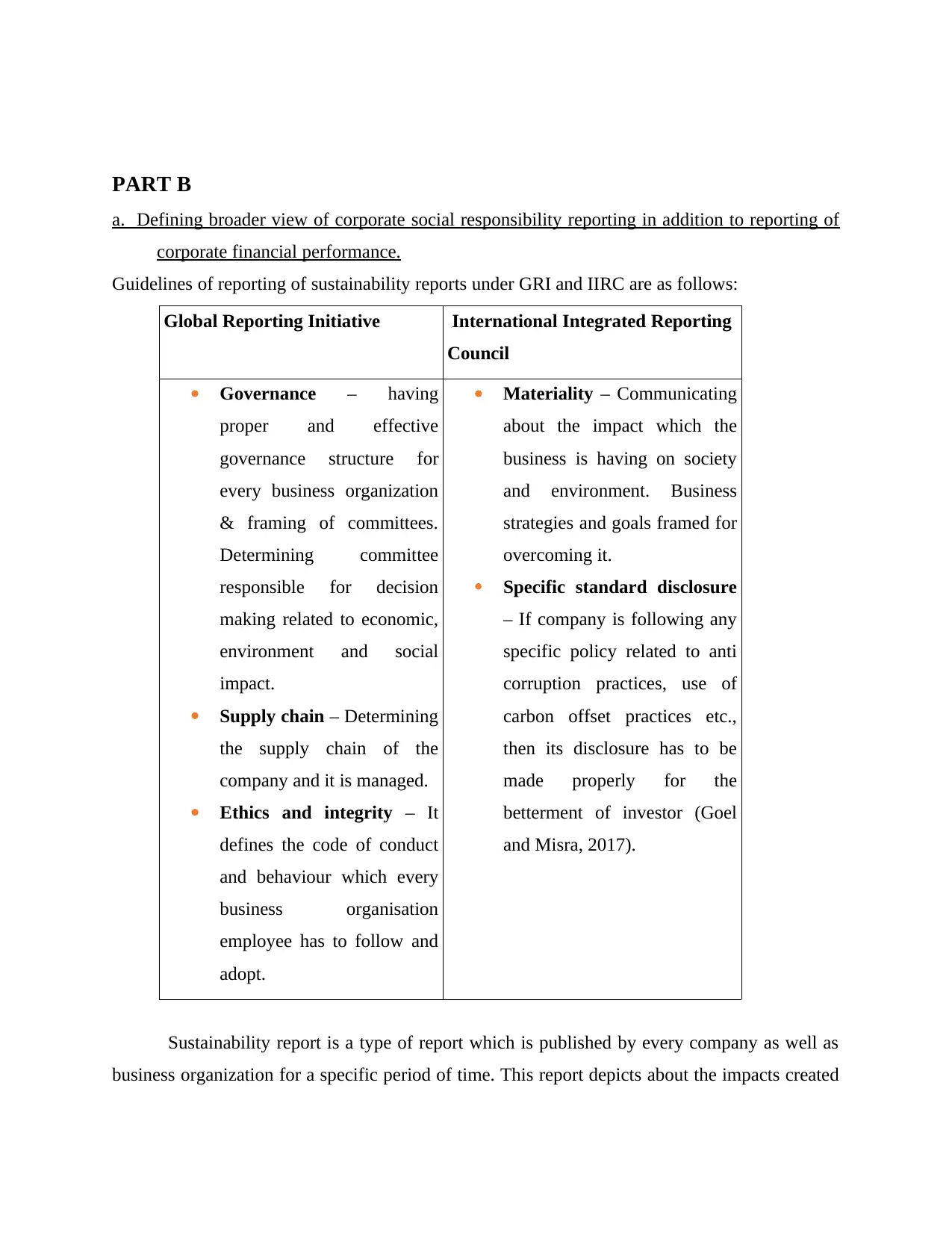

Guidelines of reporting of sustainability reports under GRI and IIRC are as follows:

Global Reporting Initiative International Integrated Reporting

Council

Governance – having

proper and effective

governance structure for

every business organization

& framing of committees.

Determining committee

responsible for decision

making related to economic,

environment and social

impact.

Supply chain – Determining

the supply chain of the

company and it is managed.

Ethics and integrity – It

defines the code of conduct

and behaviour which every

business organisation

employee has to follow and

adopt.

Materiality – Communicating

about the impact which the

business is having on society

and environment. Business

strategies and goals framed for

overcoming it.

Specific standard disclosure

– If company is following any

specific policy related to anti

corruption practices, use of

carbon offset practices etc.,

then its disclosure has to be

made properly for the

betterment of investor (Goel

and Misra, 2017).

Sustainability report is a type of report which is published by every company as well as

business organization for a specific period of time. This report depicts about the impacts created

a. Defining broader view of corporate social responsibility reporting in addition to reporting of

corporate financial performance.

Guidelines of reporting of sustainability reports under GRI and IIRC are as follows:

Global Reporting Initiative International Integrated Reporting

Council

Governance – having

proper and effective

governance structure for

every business organization

& framing of committees.

Determining committee

responsible for decision

making related to economic,

environment and social

impact.

Supply chain – Determining

the supply chain of the

company and it is managed.

Ethics and integrity – It

defines the code of conduct

and behaviour which every

business organisation

employee has to follow and

adopt.

Materiality – Communicating

about the impact which the

business is having on society

and environment. Business

strategies and goals framed for

overcoming it.

Specific standard disclosure

– If company is following any

specific policy related to anti

corruption practices, use of

carbon offset practices etc.,

then its disclosure has to be

made properly for the

betterment of investor (Goel

and Misra, 2017).

Sustainability report is a type of report which is published by every company as well as

business organization for a specific period of time. This report depicts about the impacts created

on economic, environmental as well as social factors because of business operations and

activities.

This sustainability report helps the company in defining the values, beliefs of an

organization and governance model it follows. It also provides an effective link between the

strategies framed by company and its commitment so as to maintain sustainable global economy.

Both the corporate social responsibility report and sustainability report are considered as

synonym as both takes into account financial as well as non financial information.

Corporate social responsibility and Sustainability reporting aimed at betterment of society

as well business. It helps business organization in measuring, understanding and communicating

the importance of economic, environmental, social and governance performance and impact

caused by business activities on it. By setting goals and objective, the management of company

can bring changes in its business operations more effectively.

b. Defining strengths and limitations of the conventional accounting based on the Conceptual

Framework for Financial Reporting.

Strengths of conventional accounting based on the Conceptual Framework for Financial

Reporting are as follows: Facilitates solution – On assessing of a particular accounting problem, all the business

resources are used properly with standardized solution developed on the basis of

patchwork. Not influenced by political factors - At the time of framing and development of effective

accounting standards for preparation of financial report, these are not influenced by

political conflicts and changes in policies. Policies framed in context with the conceptual

framework are not affected by criticism created by the maker of standards (Laskar and

Maji, 2016).

Concentration - Accounting standards provides main focus on the income statement of

the company along with concentration on the valuation of net assets of the company. It

helps in depicting correct statement of financial position of business for a specific time

period.

Conceptual framework also have following disadvantages:

activities.

This sustainability report helps the company in defining the values, beliefs of an

organization and governance model it follows. It also provides an effective link between the

strategies framed by company and its commitment so as to maintain sustainable global economy.

Both the corporate social responsibility report and sustainability report are considered as

synonym as both takes into account financial as well as non financial information.

Corporate social responsibility and Sustainability reporting aimed at betterment of society

as well business. It helps business organization in measuring, understanding and communicating

the importance of economic, environmental, social and governance performance and impact

caused by business activities on it. By setting goals and objective, the management of company

can bring changes in its business operations more effectively.

b. Defining strengths and limitations of the conventional accounting based on the Conceptual

Framework for Financial Reporting.

Strengths of conventional accounting based on the Conceptual Framework for Financial

Reporting are as follows: Facilitates solution – On assessing of a particular accounting problem, all the business

resources are used properly with standardized solution developed on the basis of

patchwork. Not influenced by political factors - At the time of framing and development of effective

accounting standards for preparation of financial report, these are not influenced by

political conflicts and changes in policies. Policies framed in context with the conceptual

framework are not affected by criticism created by the maker of standards (Laskar and

Maji, 2016).

Concentration - Accounting standards provides main focus on the income statement of

the company along with concentration on the valuation of net assets of the company. It

helps in depicting correct statement of financial position of business for a specific time

period.

Conceptual framework also have following disadvantages:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Applicability - Financial statements of the company are prepared with the intention of

serving its end users for making crucial decisions. But sometimes a single conceptual

framework can’t be suitable for all the other user. Based on different concepts – Accounting standard devised for a particular transaction is

not always useful in other accounting treatment. Variety of accounting standards is

designed for different purpose and goals having different concept for meeting the user

requirements.

Not sure about ease of process – By using conceptual framework, it is not always possible

to make process of preparing and framing of financial report by implementing standards

easy in comparison with not using such framework.

c. Applicability of the theories of sustainability as well as integrated reports.

It is the duty of many business organisation to make full disclosure of all the material

information either of financial as well as non financial nature which are having influence on the

decision making process of investors as well as other stakeholders. Many business organisations

are increasingly disclosing financial and non financial performance in its financial reports. This

information must have qualitative characteristics such as reliable, relevance etc. and should be

more accountable and transparent to its investors and other interested parties.

Integrated report of the company clearly specify the content related to environmental, social and

governance aspects as their corporate material disclosures in report. Uses of this report are as

follows:

Helps in mitigating and reversing all the negative impacts caused on environment, social and

governance model.

It also assists company in making their performance better and thereby improving business

reputation and creates brand loyalty.

This report helps in enabling all the external stakeholders and investors in understanding and

interpreting true as well as correct value about the business organization.

serving its end users for making crucial decisions. But sometimes a single conceptual

framework can’t be suitable for all the other user. Based on different concepts – Accounting standard devised for a particular transaction is

not always useful in other accounting treatment. Variety of accounting standards is

designed for different purpose and goals having different concept for meeting the user

requirements.

Not sure about ease of process – By using conceptual framework, it is not always possible

to make process of preparing and framing of financial report by implementing standards

easy in comparison with not using such framework.

c. Applicability of the theories of sustainability as well as integrated reports.

It is the duty of many business organisation to make full disclosure of all the material

information either of financial as well as non financial nature which are having influence on the

decision making process of investors as well as other stakeholders. Many business organisations

are increasingly disclosing financial and non financial performance in its financial reports. This

information must have qualitative characteristics such as reliable, relevance etc. and should be

more accountable and transparent to its investors and other interested parties.

Integrated report of the company clearly specify the content related to environmental, social and

governance aspects as their corporate material disclosures in report. Uses of this report are as

follows:

Helps in mitigating and reversing all the negative impacts caused on environment, social and

governance model.

It also assists company in making their performance better and thereby improving business

reputation and creates brand loyalty.

This report helps in enabling all the external stakeholders and investors in understanding and

interpreting true as well as correct value about the business organization.

Institutional theory – It relates with the firm behaviour governed in context with institutional

environment. This theory provides a deep insight about influences of different market forces,

economic changes, social as well as cultural factors on framing of corporate governance

practices in the business (Kostova and Marano, 2019).

Legitimacy Theory – This theory states that it is the duty of every business organisation to

continually ensure that its business operation are being carried on within the bounds, norms and

interest of the society.

Stakeholder Theory – Under corporate social responsibility, one of the main priority of business

is toward the society and community in which the business is conducting its business operation

at large. This theory relates to social orientation as one of its business responsibilities.

Stakeholder theory states that success of a business primarily depends on building & maintaining

of strong relationship, creating value for stakeholders.

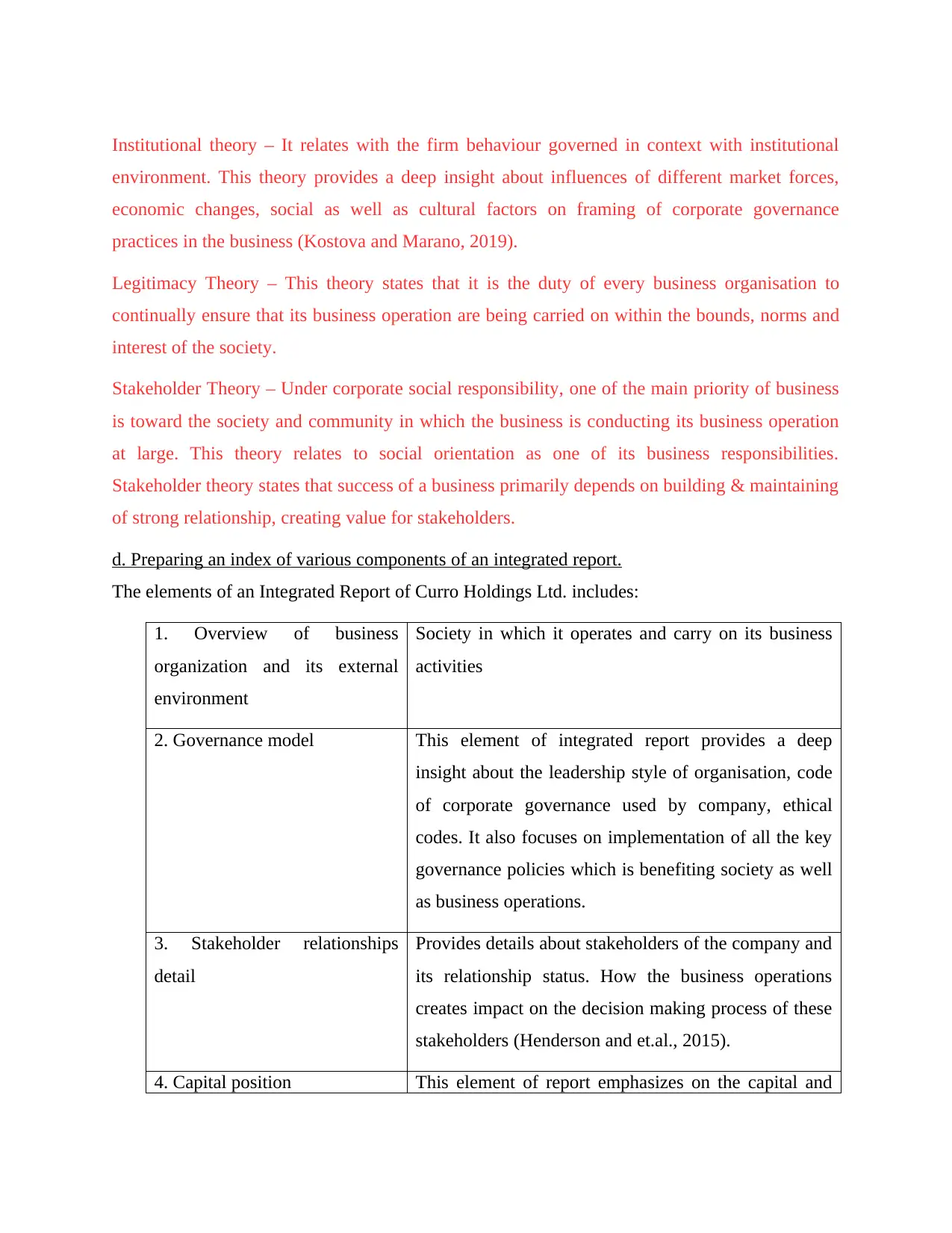

d. Preparing an index of various components of an integrated report.

The elements of an Integrated Report of Curro Holdings Ltd. includes:

1. Overview of business

organization and its external

environment

Society in which it operates and carry on its business

activities

2. Governance model This element of integrated report provides a deep

insight about the leadership style of organisation, code

of corporate governance used by company, ethical

codes. It also focuses on implementation of all the key

governance policies which is benefiting society as well

as business operations.

3. Stakeholder relationships

detail

Provides details about stakeholders of the company and

its relationship status. How the business operations

creates impact on the decision making process of these

stakeholders (Henderson and et.al., 2015).

4. Capital position This element of report emphasizes on the capital and

environment. This theory provides a deep insight about influences of different market forces,

economic changes, social as well as cultural factors on framing of corporate governance

practices in the business (Kostova and Marano, 2019).

Legitimacy Theory – This theory states that it is the duty of every business organisation to

continually ensure that its business operation are being carried on within the bounds, norms and

interest of the society.

Stakeholder Theory – Under corporate social responsibility, one of the main priority of business

is toward the society and community in which the business is conducting its business operation

at large. This theory relates to social orientation as one of its business responsibilities.

Stakeholder theory states that success of a business primarily depends on building & maintaining

of strong relationship, creating value for stakeholders.

d. Preparing an index of various components of an integrated report.

The elements of an Integrated Report of Curro Holdings Ltd. includes:

1. Overview of business

organization and its external

environment

Society in which it operates and carry on its business

activities

2. Governance model This element of integrated report provides a deep

insight about the leadership style of organisation, code

of corporate governance used by company, ethical

codes. It also focuses on implementation of all the key

governance policies which is benefiting society as well

as business operations.

3. Stakeholder relationships

detail

Provides details about stakeholders of the company and

its relationship status. How the business operations

creates impact on the decision making process of these

stakeholders (Henderson and et.al., 2015).

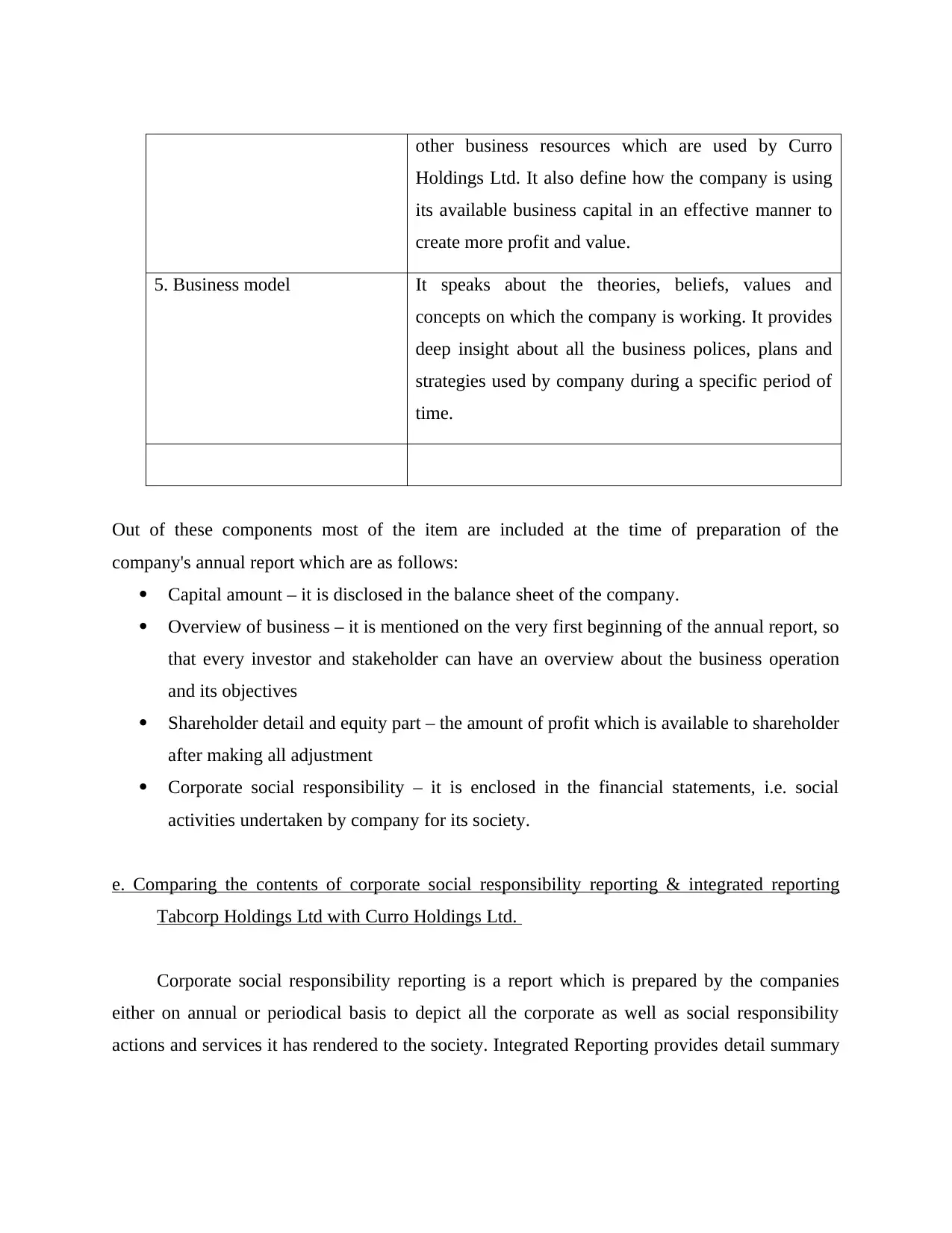

4. Capital position This element of report emphasizes on the capital and

other business resources which are used by Curro

Holdings Ltd. It also define how the company is using

its available business capital in an effective manner to

create more profit and value.

5. Business model It speaks about the theories, beliefs, values and

concepts on which the company is working. It provides

deep insight about all the business polices, plans and

strategies used by company during a specific period of

time.

Out of these components most of the item are included at the time of preparation of the

company's annual report which are as follows:

Capital amount – it is disclosed in the balance sheet of the company.

Overview of business – it is mentioned on the very first beginning of the annual report, so

that every investor and stakeholder can have an overview about the business operation

and its objectives

Shareholder detail and equity part – the amount of profit which is available to shareholder

after making all adjustment

Corporate social responsibility – it is enclosed in the financial statements, i.e. social

activities undertaken by company for its society.

e. Comparing the contents of corporate social responsibility reporting & integrated reporting

Tabcorp Holdings Ltd with Curro Holdings Ltd.

Corporate social responsibility reporting is a report which is prepared by the companies

either on annual or periodical basis to depict all the corporate as well as social responsibility

actions and services it has rendered to the society. Integrated Reporting provides detail summary

Holdings Ltd. It also define how the company is using

its available business capital in an effective manner to

create more profit and value.

5. Business model It speaks about the theories, beliefs, values and

concepts on which the company is working. It provides

deep insight about all the business polices, plans and

strategies used by company during a specific period of

time.

Out of these components most of the item are included at the time of preparation of the

company's annual report which are as follows:

Capital amount – it is disclosed in the balance sheet of the company.

Overview of business – it is mentioned on the very first beginning of the annual report, so

that every investor and stakeholder can have an overview about the business operation

and its objectives

Shareholder detail and equity part – the amount of profit which is available to shareholder

after making all adjustment

Corporate social responsibility – it is enclosed in the financial statements, i.e. social

activities undertaken by company for its society.

e. Comparing the contents of corporate social responsibility reporting & integrated reporting

Tabcorp Holdings Ltd with Curro Holdings Ltd.

Corporate social responsibility reporting is a report which is prepared by the companies

either on annual or periodical basis to depict all the corporate as well as social responsibility

actions and services it has rendered to the society. Integrated Reporting provides detail summary

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

about the strategy, concept, governance model, performance level etc. of the business assist in

the creation of value over a period of time. Comparison are as follows:

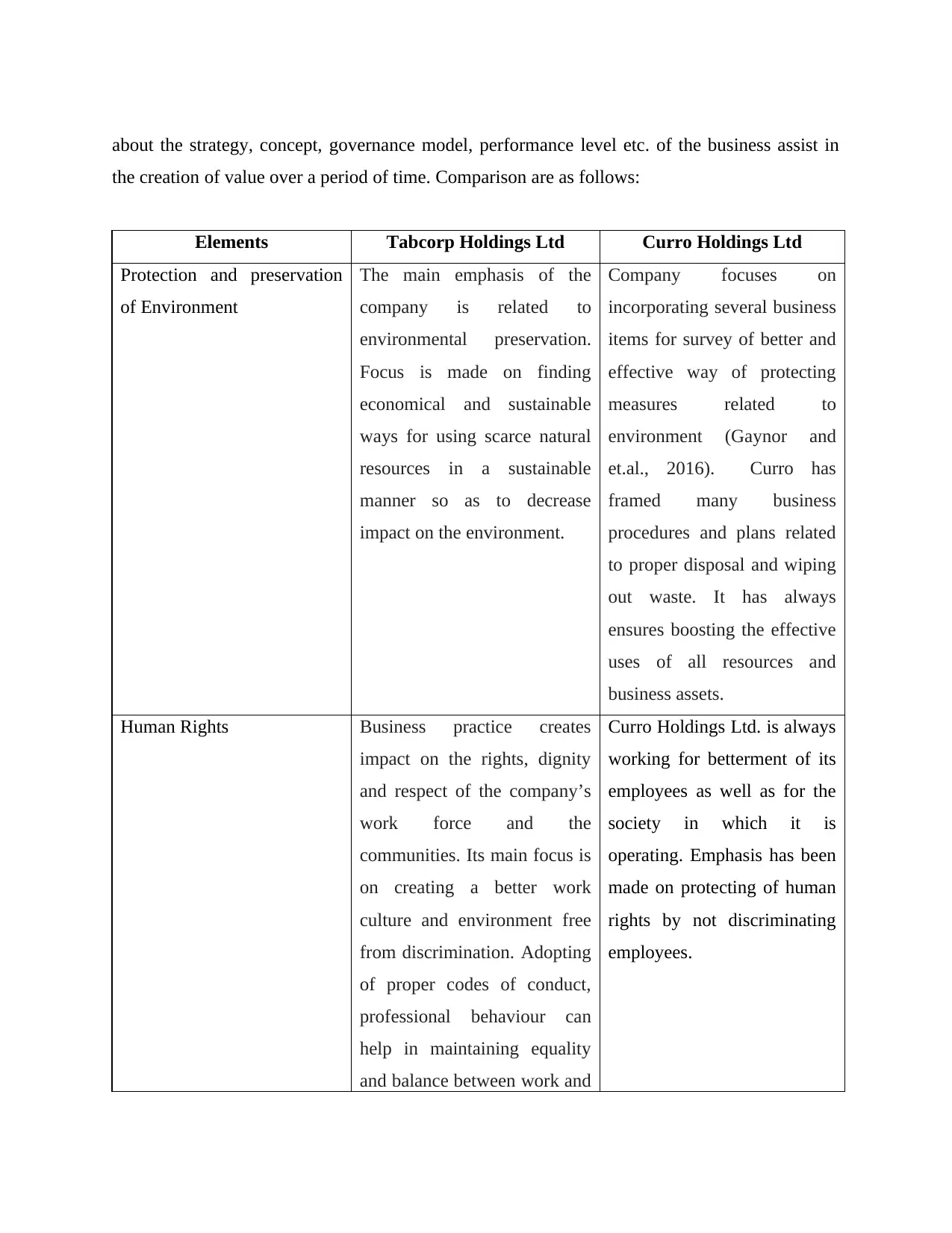

Elements Tabcorp Holdings Ltd Curro Holdings Ltd

Protection and preservation

of Environment

The main emphasis of the

company is related to

environmental preservation.

Focus is made on finding

economical and sustainable

ways for using scarce natural

resources in a sustainable

manner so as to decrease

impact on the environment.

Company focuses on

incorporating several business

items for survey of better and

effective way of protecting

measures related to

environment (Gaynor and

et.al., 2016). Curro has

framed many business

procedures and plans related

to proper disposal and wiping

out waste. It has always

ensures boosting the effective

uses of all resources and

business assets.

Human Rights Business practice creates

impact on the rights, dignity

and respect of the company’s

work force and the

communities. Its main focus is

on creating a better work

culture and environment free

from discrimination. Adopting

of proper codes of conduct,

professional behaviour can

help in maintaining equality

and balance between work and

Curro Holdings Ltd. is always

working for betterment of its

employees as well as for the

society in which it is

operating. Emphasis has been

made on protecting of human

rights by not discriminating

employees.

the creation of value over a period of time. Comparison are as follows:

Elements Tabcorp Holdings Ltd Curro Holdings Ltd

Protection and preservation

of Environment

The main emphasis of the

company is related to

environmental preservation.

Focus is made on finding

economical and sustainable

ways for using scarce natural

resources in a sustainable

manner so as to decrease

impact on the environment.

Company focuses on

incorporating several business

items for survey of better and

effective way of protecting

measures related to

environment (Gaynor and

et.al., 2016). Curro has

framed many business

procedures and plans related

to proper disposal and wiping

out waste. It has always

ensures boosting the effective

uses of all resources and

business assets.

Human Rights Business practice creates

impact on the rights, dignity

and respect of the company’s

work force and the

communities. Its main focus is

on creating a better work

culture and environment free

from discrimination. Adopting

of proper codes of conduct,

professional behaviour can

help in maintaining equality

and balance between work and

Curro Holdings Ltd. is always

working for betterment of its

employees as well as for the

society in which it is

operating. Emphasis has been

made on protecting of human

rights by not discriminating

employees.

business life. Donations to

charities and community

organisations has been made

of around total $1.9 million.

Growth of business as well

as economy

The main aim of this company

is to promote growth of

company as well as of the

society as a whole. This

company ensures that the

business activities undertaken

by it are not hampering society

and economy.

It emphasizes on maintaining

of equality in the growth

perspective at both business

as well as economy level. It

works on the belief that with

business development

economy will also develop.

Promoting better health

standards

The environment in which the

company is performing its

business operations has to

always ensure that proper

health standards are

maintained and followed.

Many business organisation

and sector are playing

predominant role in context

with the global economic

development and globalization

of healthy economy.

Complying with best business

practices and standards can

help Curro Holdings Ltd. in

making more profit as well as

in improving g its business

performance level. Company

has to maintain healthy

business environment for its

employees as well as for the

society in which it is

operating.

Participation of Community

or society

By inviting suggestions and

feedbacks about the business

products and services can help

the company in achieving

higher success (Warren,

2016). Every business

This company has always

focuses on making active

participation of its society in

the business decisions. It has

always ensures that money

and time spend by the

charities and community

organisations has been made

of around total $1.9 million.

Growth of business as well

as economy

The main aim of this company

is to promote growth of

company as well as of the

society as a whole. This

company ensures that the

business activities undertaken

by it are not hampering society

and economy.

It emphasizes on maintaining

of equality in the growth

perspective at both business

as well as economy level. It

works on the belief that with

business development

economy will also develop.

Promoting better health

standards

The environment in which the

company is performing its

business operations has to

always ensure that proper

health standards are

maintained and followed.

Many business organisation

and sector are playing

predominant role in context

with the global economic

development and globalization

of healthy economy.

Complying with best business

practices and standards can

help Curro Holdings Ltd. in

making more profit as well as

in improving g its business

performance level. Company

has to maintain healthy

business environment for its

employees as well as for the

society in which it is

operating.

Participation of Community

or society

By inviting suggestions and

feedbacks about the business

products and services can help

the company in achieving

higher success (Warren,

2016). Every business

This company has always

focuses on making active

participation of its society in

the business decisions. It has

always ensures that money

and time spend by the

organisation should focus on

active participation of its

community as well as society

in decision making process.

company on society is fruitful

for both.

CONCLUSION

From the above report it has been concluded that by adhering to all the accounting standards and

principles, every business organisation can grow with high profits and improves its performance

level as well. It is very important on part of every company to conduct some social activities in

the society in which it is conducting its business operations. Also report has discuss that financial

statement of company should contain all the material information which are relevant and going

to influence the decision making process of any investors or stakeholders.

active participation of its

community as well as society

in decision making process.

company on society is fruitful

for both.

CONCLUSION

From the above report it has been concluded that by adhering to all the accounting standards and

principles, every business organisation can grow with high profits and improves its performance

level as well. It is very important on part of every company to conduct some social activities in

the society in which it is conducting its business operations. Also report has discuss that financial

statement of company should contain all the material information which are relevant and going

to influence the decision making process of any investors or stakeholders.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals

Chih, Y. Y. and Zwikael, O., 2015. Project benefit management: A conceptual framework of

target benefit formulation. International Journal of Project Management. 33(2). pp.352-362.

Osanaiye, O., Choo, K. K. R. and Dlodlo, M., 2016. Distributed denial of service (DDoS)

resilience in cloud: review and conceptual cloud DDoS mitigation framework. Journal of

Network and Computer Applications. 67. pp.147-165.

Ovaskainen, O. and et.al., 2017. How to make more out of community data? A conceptual

framework and its implementation as models and software. Ecology Letters. 20(5). pp.561-

576.

Warren, C. M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial ReportingStandard 16 (IFRS 16). Property

Management. 34(3).

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Gaynor, L. M., and et.al., 2016. Understanding the relation between financial reporting quality

and audit quality. Auditing: A Journal of Practice & Theor. 35(4). pp.1-22.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Beaulieu, T., Sarker, S. and Sarker, S., 2015. A Conceptual Framework for Understanding

Crowdfunding. CAIS. 37. p.1.

Crowther, D. and Seifi, S. eds., 2018. Redefining Corporate Social Responsibility. Emerald

Group Publishing.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research.

54(2). pp.525-622.

Cho, C. H., and et.al., 2015. Organized hypocrisy, organizational façades, and sustainability

reporting. Accounting, Organizations and Society., 40. pp.78-94.

Books and journals

Chih, Y. Y. and Zwikael, O., 2015. Project benefit management: A conceptual framework of

target benefit formulation. International Journal of Project Management. 33(2). pp.352-362.

Osanaiye, O., Choo, K. K. R. and Dlodlo, M., 2016. Distributed denial of service (DDoS)

resilience in cloud: review and conceptual cloud DDoS mitigation framework. Journal of

Network and Computer Applications. 67. pp.147-165.

Ovaskainen, O. and et.al., 2017. How to make more out of community data? A conceptual

framework and its implementation as models and software. Ecology Letters. 20(5). pp.561-

576.

Warren, C. M., 2016. The impact of International Accounting Standards Board

(IASB)/International Financial ReportingStandard 16 (IFRS 16). Property

Management. 34(3).

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Gaynor, L. M., and et.al., 2016. Understanding the relation between financial reporting quality

and audit quality. Auditing: A Journal of Practice & Theor. 35(4). pp.1-22.

Flower, J., 2018. Global financial reporting. Macmillan International Higher Education.

Henderson, S., and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Beaulieu, T., Sarker, S. and Sarker, S., 2015. A Conceptual Framework for Understanding

Crowdfunding. CAIS. 37. p.1.

Crowther, D. and Seifi, S. eds., 2018. Redefining Corporate Social Responsibility. Emerald

Group Publishing.

Leuz, C. and Wysocki, P. D., 2016. The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting Research.

54(2). pp.525-622.

Cho, C. H., and et.al., 2015. Organized hypocrisy, organizational façades, and sustainability

reporting. Accounting, Organizations and Society., 40. pp.78-94.

Schaltegger, S., Etxeberria, I. Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2).

pp.113-122.

Laskar, N. and Maji, S.G., 2016. Corporate sustainability reporting practices in India: myth or

reality?. Social Responsibility Journal. 12(4). pp.625-641.

Goel, P. and Misra, R., 2017. Sustainability reporting in India: Exploring sectoral differences

and linkages with financial performance. Vision. 21(2). pp.214-224.

Kostova, T. and Marano, V., 2019. Institutional Theory Perspectives on Emerging Markets. The

Oxford Handbook of Management in Emerging Markets. p.99.

Online

Conceptual framework for financial reporting. 2019. [Online]. Available through:

<https://specialties.bayt.com/en/specialties/q/347887/explain-the-role-of-a-conceptual-

framework-in-the-development-of-financial-reporting-standards/>.

Tabcorp holdings limited annual report. 2018. [Online]. Available through:

<https://www.tabcorp.com.au/TabCorp/media/TabCorp/Investors/Annual%20Report/

Tabcorp-Annual-Report-2018_1.pdf>.

Sustainability Reporting Guidelines. 2015. [Online]. Available through:

<https://www.ey.com/Publication/vwLUAssets/G4-Sustainability-Reporting-Guidelines/

$FILE/G4-Sustainability-Reporting-Guidelines.pdf>.

Corporate Financial Reporting. 2019. [Online]. Available through:

<http://www.monistrics.ga/2018/01/the-advantages-and-disadvantages-of-corporate-

financial-reporting.html>.

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2).

pp.113-122.

Laskar, N. and Maji, S.G., 2016. Corporate sustainability reporting practices in India: myth or

reality?. Social Responsibility Journal. 12(4). pp.625-641.

Goel, P. and Misra, R., 2017. Sustainability reporting in India: Exploring sectoral differences

and linkages with financial performance. Vision. 21(2). pp.214-224.

Kostova, T. and Marano, V., 2019. Institutional Theory Perspectives on Emerging Markets. The

Oxford Handbook of Management in Emerging Markets. p.99.

Online

Conceptual framework for financial reporting. 2019. [Online]. Available through:

<https://specialties.bayt.com/en/specialties/q/347887/explain-the-role-of-a-conceptual-

framework-in-the-development-of-financial-reporting-standards/>.

Tabcorp holdings limited annual report. 2018. [Online]. Available through:

<https://www.tabcorp.com.au/TabCorp/media/TabCorp/Investors/Annual%20Report/

Tabcorp-Annual-Report-2018_1.pdf>.

Sustainability Reporting Guidelines. 2015. [Online]. Available through:

<https://www.ey.com/Publication/vwLUAssets/G4-Sustainability-Reporting-Guidelines/

$FILE/G4-Sustainability-Reporting-Guidelines.pdf>.

Corporate Financial Reporting. 2019. [Online]. Available through:

<http://www.monistrics.ga/2018/01/the-advantages-and-disadvantages-of-corporate-

financial-reporting.html>.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.