CONTEMPORARY ACCOUNTING THEORY.

VerifiedAdded on 2023/03/30

|18

|3550

|62

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ACCOUNTING THEORY

CONTEMPORARY ACCOUNTING THEORY

Name of the Student:

Name of the University:

Author Note

CONTEMPORARY ACCOUNTING THEORY

Name of the Student:

Name of the University:

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CONTEMPORARY ACCOUNTING THEORY

Executive Summery

The report is prepared to provide the brief concept about the conceptual framework and the

integrated or sustainability reporting of the firm. The main objective of the report is to discuss

the every element of the conceptual framework and the sustainability reporting of the

financial information reporting of the companies. The report have the two parts, the first part

discuss about the conceptual framework while the second part of the report discuss about the

sustainability reporting of the company. The report also use the annual report of the two

companies explain the conceptual framework and sustainability reporting concept in more

clear way.

Executive Summery

The report is prepared to provide the brief concept about the conceptual framework and the

integrated or sustainability reporting of the firm. The main objective of the report is to discuss

the every element of the conceptual framework and the sustainability reporting of the

financial information reporting of the companies. The report have the two parts, the first part

discuss about the conceptual framework while the second part of the report discuss about the

sustainability reporting of the company. The report also use the annual report of the two

companies explain the conceptual framework and sustainability reporting concept in more

clear way.

2CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

PART A......................................................................................................................................4

Requirement A.......................................................................................................................4

Requirement B.......................................................................................................................4

Requirement C.......................................................................................................................7

Requirement D.......................................................................................................................7

Part B..........................................................................................................................................8

Requirement A.......................................................................................................................8

Requirement B.......................................................................................................................9

Requirement C.....................................................................................................................10

Requirement D.....................................................................................................................10

Requirement E......................................................................................................................13

Conclusion................................................................................................................................14

References and Bibliography...................................................................................................15

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................4

PART A......................................................................................................................................4

Requirement A.......................................................................................................................4

Requirement B.......................................................................................................................4

Requirement C.......................................................................................................................7

Requirement D.......................................................................................................................7

Part B..........................................................................................................................................8

Requirement A.......................................................................................................................8

Requirement B.......................................................................................................................9

Requirement C.....................................................................................................................10

Requirement D.....................................................................................................................10

Requirement E......................................................................................................................13

Conclusion................................................................................................................................14

References and Bibliography...................................................................................................15

3CONTEMPORARY ACCOUNTING THEORY

Introduction

The report titled “Contemporary Accounting Theory” is prepared to analyse the

theory of conceptual framework and sustainability reporting of the companies. In the first part

of the report that is for conceptual framework, discuss the history and the development of the

conceptual framework considering the International Accounting Standards Boards (IASB).

The paper also analyse the profession’s concern regarding the application of the conceptual

framework in the financial reporting of the companies. This also discuss the concern of the

quality of conceptual framework. Lastly, the first part of the report analyse the annual report

of the Ramsay Health Care to know how many financial statement the company prepared and

the implementing the principle in the several accounting aspects. The second part of the

report, discuss the sustainability reporting guidelines of the global reporting initiative and the

international integrated reporting framework of the international integrated reporting council.

Further, this part of the report discuss about the advantages and the disadvantages of the

conventional accounting based on the conceptual framework for financial reporting along

with the usefulness and the limitation of the contents of the sustainability as well as

integrated reports. Lastly, this second part of the report analyse the financial annual report of

the Adcock Ingram to compare the content of the Australian corporate’s social responsibility

with the Australian corporate’s social responsibilities. Hence, the main objective of the report

is to provide the clear view of the conceptual framework and the sustainability of the

company’s information reporting.

Introduction

The report titled “Contemporary Accounting Theory” is prepared to analyse the

theory of conceptual framework and sustainability reporting of the companies. In the first part

of the report that is for conceptual framework, discuss the history and the development of the

conceptual framework considering the International Accounting Standards Boards (IASB).

The paper also analyse the profession’s concern regarding the application of the conceptual

framework in the financial reporting of the companies. This also discuss the concern of the

quality of conceptual framework. Lastly, the first part of the report analyse the annual report

of the Ramsay Health Care to know how many financial statement the company prepared and

the implementing the principle in the several accounting aspects. The second part of the

report, discuss the sustainability reporting guidelines of the global reporting initiative and the

international integrated reporting framework of the international integrated reporting council.

Further, this part of the report discuss about the advantages and the disadvantages of the

conventional accounting based on the conceptual framework for financial reporting along

with the usefulness and the limitation of the contents of the sustainability as well as

integrated reports. Lastly, this second part of the report analyse the financial annual report of

the Adcock Ingram to compare the content of the Australian corporate’s social responsibility

with the Australian corporate’s social responsibilities. Hence, the main objective of the report

is to provide the clear view of the conceptual framework and the sustainability of the

company’s information reporting.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CONTEMPORARY ACCOUNTING THEORY

Discussion

PART A

Requirement A

In the basis of the various articles, the conceptual framework come up with the vast

history. The history of the conceptual framework starts from the 1929. From the 1929, the

various developments have been observed in the conceptual framework of the financial

reporting of the firm. The first theory of the conceptual framework is developed in 1929 and

then in 1934 the principles of U.S. Securities and Exchange Commission is developed. In

1973, the Financial Accounting Standards Boards is set up to monitor and enhance the

financial reporting of the companies. Then, the various developments in the conceptual

framework are observed till now (ACCA Global, 2019). The revolution in the conceptual

framework can be highly identified between the 1978 to 2010 as in between this the several

principles are developed in the conceptual framework of the financial information reporting

of the firm. The each countries also developed their own guidelines and policies of the

conceptual framework regarding the financial reporting of the firm in the basis of the

international standards. This standards and the guidelines helps the firms in their financial

reporting and be implemented in their financial information reporting.

Requirement B

The International Financial Reporting Standards (IFRS) are the accounting rules of

the company that provides the guidelines regarding the accounting treatments of the

transaction. These standards also provide the guidelines to the company in relation to the

financial information reporting of the firm (Cheng et al., 2014). This is an unitary set of the

standards that help the firm to solve the various problems of the firm regarding the

accounting treatment and the reporting. This is an international standard of preparing the

Discussion

PART A

Requirement A

In the basis of the various articles, the conceptual framework come up with the vast

history. The history of the conceptual framework starts from the 1929. From the 1929, the

various developments have been observed in the conceptual framework of the financial

reporting of the firm. The first theory of the conceptual framework is developed in 1929 and

then in 1934 the principles of U.S. Securities and Exchange Commission is developed. In

1973, the Financial Accounting Standards Boards is set up to monitor and enhance the

financial reporting of the companies. Then, the various developments in the conceptual

framework are observed till now (ACCA Global, 2019). The revolution in the conceptual

framework can be highly identified between the 1978 to 2010 as in between this the several

principles are developed in the conceptual framework of the financial information reporting

of the firm. The each countries also developed their own guidelines and policies of the

conceptual framework regarding the financial reporting of the firm in the basis of the

international standards. This standards and the guidelines helps the firms in their financial

reporting and be implemented in their financial information reporting.

Requirement B

The International Financial Reporting Standards (IFRS) are the accounting rules of

the company that provides the guidelines regarding the accounting treatments of the

transaction. These standards also provide the guidelines to the company in relation to the

financial information reporting of the firm (Cheng et al., 2014). This is an unitary set of the

standards that help the firm to solve the various problems of the firm regarding the

accounting treatment and the reporting. This is an international standard of preparing the

5CONTEMPORARY ACCOUNTING THEORY

accounting entries of the firm hence adopted by the various countries. The many countries

developed its own principle and the guideline for the company accounting and discloser of

the accounting information in the basis of the International Financial Reporting Standards.

The followings are the some advantages of the International Financial Reporting Standards in

context of applying the conceptual framework in the financial reporting of the firm: -

Uniformity: - The International Financial Reporting Standards create a single set

of accounting standards around the world. This ensure the uniformity in the

financial information reporting of the firm (Collings & Profile, 2019). This helps

the user of the financial report to easily understand the financial report of the any

company.

Time, effort and expense: - This International Financial Reporting Standards

provides the frame- work and the guidelines to the company relating the

reporting the financial information of the company, helps the company to prepare

the financial report of the company. This reduces the time of preparing the

financial statement with the less efforts. This also helps the firms to reduce the

cost of preparing the financial report.

Controlling the subsidiaries: - As the International Financial Reporting

Standards provides uniformity in preparing the financial report of the company

that means the all companies of different company follows the same rule of the

accounting to prepare the financial statement of the firm (Danilenko, 2018).

Hence, the large companies can easily monitor the financial operation of its

subsidiaries of the different countries.

Flexibility: - The International Financial Reporting Standards is more flexible

than the other financial standards. This is appropriate for all the firm as per their

requirements. As the objective of the International Financial Reporting Standards

accounting entries of the firm hence adopted by the various countries. The many countries

developed its own principle and the guideline for the company accounting and discloser of

the accounting information in the basis of the International Financial Reporting Standards.

The followings are the some advantages of the International Financial Reporting Standards in

context of applying the conceptual framework in the financial reporting of the firm: -

Uniformity: - The International Financial Reporting Standards create a single set

of accounting standards around the world. This ensure the uniformity in the

financial information reporting of the firm (Collings & Profile, 2019). This helps

the user of the financial report to easily understand the financial report of the any

company.

Time, effort and expense: - This International Financial Reporting Standards

provides the frame- work and the guidelines to the company relating the

reporting the financial information of the company, helps the company to prepare

the financial report of the company. This reduces the time of preparing the

financial statement with the less efforts. This also helps the firms to reduce the

cost of preparing the financial report.

Controlling the subsidiaries: - As the International Financial Reporting

Standards provides uniformity in preparing the financial report of the company

that means the all companies of different company follows the same rule of the

accounting to prepare the financial statement of the firm (Danilenko, 2018).

Hence, the large companies can easily monitor the financial operation of its

subsidiaries of the different countries.

Flexibility: - The International Financial Reporting Standards is more flexible

than the other financial standards. This is appropriate for all the firm as per their

requirements. As the objective of the International Financial Reporting Standards

6CONTEMPORARY ACCOUNTING THEORY

is to reach at the reasonable valuation considering the goal of the financial

reporting.

As discussed above, the International Financial Reporting Standards have the several

advantages in the financial reporting of the firm. Although, the firm faces some issues in

implication of the framework in the preparation and reporting the financial statement of the

company. The followings are the main issues and disadvantages of the International Financial

Reporting Standards in respect of the conceptual framework in the financial reporting: -

Cost of implementation: - The major disadvantage of the International Financial

Reporting Standards in respect of the implementing in the financial reporting of the

company is it increases the cost of the company (Henderson et al., 2015). As the

implementation cost of the new frame- work in the accounting standards of the

company is high.

Standards manipulation: - As mentioned above the International Financial

Reporting Standards is a flexible standard that have the several advantages for the

companies but it also increase the chances of the manipulating the standards. In

simple words, as this have the flexibility hence, this company can easily manipulate

the standards.

Requirement of Auditing: - As this increase the chances of manipulating the

financial information of the firm (Integrated Reporting, 2019). Hence, this frame-

work requires auditing and enforcement to ensure the trueness and the fairness of the

information in the financial reporting of the company.

Accountant’s work: - As the accountant need to perform the extensive research and

analysis of the financial performance of the company for the reporting purpose hence,

this increase the work- load of the accountant of the firm.

is to reach at the reasonable valuation considering the goal of the financial

reporting.

As discussed above, the International Financial Reporting Standards have the several

advantages in the financial reporting of the firm. Although, the firm faces some issues in

implication of the framework in the preparation and reporting the financial statement of the

company. The followings are the main issues and disadvantages of the International Financial

Reporting Standards in respect of the conceptual framework in the financial reporting: -

Cost of implementation: - The major disadvantage of the International Financial

Reporting Standards in respect of the implementing in the financial reporting of the

company is it increases the cost of the company (Henderson et al., 2015). As the

implementation cost of the new frame- work in the accounting standards of the

company is high.

Standards manipulation: - As mentioned above the International Financial

Reporting Standards is a flexible standard that have the several advantages for the

companies but it also increase the chances of the manipulating the standards. In

simple words, as this have the flexibility hence, this company can easily manipulate

the standards.

Requirement of Auditing: - As this increase the chances of manipulating the

financial information of the firm (Integrated Reporting, 2019). Hence, this frame-

work requires auditing and enforcement to ensure the trueness and the fairness of the

information in the financial reporting of the company.

Accountant’s work: - As the accountant need to perform the extensive research and

analysis of the financial performance of the company for the reporting purpose hence,

this increase the work- load of the accountant of the firm.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ACCOUNTING THEORY

Apart from the above- mentioned disadvantages, the International Financial Reporting

Standards also have the several other issues in regarding the implementation of the

conceptual frame- work in the financial reporting of the company.

Requirement C

The academic’s concerns about the quality of the conceptual framework can be

discussed by discussing the benefits and the limitations of the conceptual framework. The

conceptual framework in the financial reporting provides the guidelines to the company to

report the financial information of the company. The conceptual framework helps the

companies in their financial reporting by providing the framework of the reporting (Herath &

Albarqi, 2017). This is also provides various principles, rules and framework that helps the

company to do the accounting treatment of the transaction of the company and duly report

them in the annual report of the financial report. This conceptual framework helps to ensure

the uniformity in the financial reporting of the companies that helps the readers of the

financial information to understand the information more clearly. Apart from the above

advantages, the conceptual framework have some issues too. The company faces the several

issues in the initial stage of implementing the conceptual framework in the accounting system

of the company. The company need to need to change the existing accounting policy for the

implication of the conceptual framework that requires lots of hard work as well as the funds

(Macve, 2015). The implication process of the conceptual frame- work is the also a time

consuming process as this require many researches regarding the financial accounting of the

firm.

Requirement D

The chosen Australian company for this report is the Ramsay Health Care Limited. In

the basis of the annual report of the company for the year 2018, the company mainly provides

the four financial statements those are Income Statement, Balance Sheet Statement, Cash

Apart from the above- mentioned disadvantages, the International Financial Reporting

Standards also have the several other issues in regarding the implementation of the

conceptual frame- work in the financial reporting of the company.

Requirement C

The academic’s concerns about the quality of the conceptual framework can be

discussed by discussing the benefits and the limitations of the conceptual framework. The

conceptual framework in the financial reporting provides the guidelines to the company to

report the financial information of the company. The conceptual framework helps the

companies in their financial reporting by providing the framework of the reporting (Herath &

Albarqi, 2017). This is also provides various principles, rules and framework that helps the

company to do the accounting treatment of the transaction of the company and duly report

them in the annual report of the financial report. This conceptual framework helps to ensure

the uniformity in the financial reporting of the companies that helps the readers of the

financial information to understand the information more clearly. Apart from the above

advantages, the conceptual framework have some issues too. The company faces the several

issues in the initial stage of implementing the conceptual framework in the accounting system

of the company. The company need to need to change the existing accounting policy for the

implication of the conceptual framework that requires lots of hard work as well as the funds

(Macve, 2015). The implication process of the conceptual frame- work is the also a time

consuming process as this require many researches regarding the financial accounting of the

firm.

Requirement D

The chosen Australian company for this report is the Ramsay Health Care Limited. In

the basis of the annual report of the company for the year 2018, the company mainly provides

the four financial statements those are Income Statement, Balance Sheet Statement, Cash

8CONTEMPORARY ACCOUNTING THEORY

Flow Statement and the Change in equity statement (Ramsayhealth, 2019). The Income

statement of the firm includes the details of all the income and the expenses of the firm for

the year 2018. The main components of the income statement is the revenue, cost of goods

sold, profit before interest, tax, depreciation and amortisation, and the net profit for the period

of the company. The balance sheet statement of the company contents the details of the

current and non- current assets, current and non- current liabilities and the equity of the

company. Further, the cash flow statement of the company shows the details of the cash paid

by the company and cash received by the company in the accounting period along with the

net cash flow. Lastly, change in equity statement of the firm contents the details of the equity

capital of the firm. The company used the Australian Accounting Standard board’s regulation

for the preparing and reporting the accounting information of the company. The company, as

per the requirement of the quality of conceptual framework truly and fairly report the

financial information in their annual report.

Part B

Requirement A

The GRI has the guidelines, which is used by the organizations in order to disclose the

important critical impacts on the environment, society and the economy. The guidelines helps

the organizations in generating reliable, relevant and standardized information for risks and

opportunities assessment and then enabling more detailed and informed information (Global

Reporting Initiative, 2019). This enhances the decision-making, which is beneficial for the

stakeholders and the organizations. These guidelines are designed and applied universally to

all the sectors and to all the types as well as size of the organization.

The guidelines of sustainability reporting are divided into two parts. Under the first

part there is standard disclosures and reporting principles that includes standardized

Flow Statement and the Change in equity statement (Ramsayhealth, 2019). The Income

statement of the firm includes the details of all the income and the expenses of the firm for

the year 2018. The main components of the income statement is the revenue, cost of goods

sold, profit before interest, tax, depreciation and amortisation, and the net profit for the period

of the company. The balance sheet statement of the company contents the details of the

current and non- current assets, current and non- current liabilities and the equity of the

company. Further, the cash flow statement of the company shows the details of the cash paid

by the company and cash received by the company in the accounting period along with the

net cash flow. Lastly, change in equity statement of the firm contents the details of the equity

capital of the firm. The company used the Australian Accounting Standard board’s regulation

for the preparing and reporting the accounting information of the company. The company, as

per the requirement of the quality of conceptual framework truly and fairly report the

financial information in their annual report.

Part B

Requirement A

The GRI has the guidelines, which is used by the organizations in order to disclose the

important critical impacts on the environment, society and the economy. The guidelines helps

the organizations in generating reliable, relevant and standardized information for risks and

opportunities assessment and then enabling more detailed and informed information (Global

Reporting Initiative, 2019). This enhances the decision-making, which is beneficial for the

stakeholders and the organizations. These guidelines are designed and applied universally to

all the sectors and to all the types as well as size of the organization.

The guidelines of sustainability reporting are divided into two parts. Under the first

part there is standard disclosures and reporting principles that includes standardized

9CONTEMPORARY ACCOUNTING THEORY

disclosures, criteria for preparing the report of sustainability and the reporting principles.

However, the second part is the implementation manual, which includes the explanations of

applying principles of reporting, the way in which there is disclosure of the information and

interpretations of different concepts in given guidelines.

Framework of International Integrated Reporting

For accelerating integrated reporting adoption, the framework of International

integrated reporting are used. It establishes the purpose of providing the rules and guiding

principles, which helps in governing the explanation of basic concepts and overall integrated

report contents. Integrated reporting is the process that results in periodically issuing of the

integrated report by company, which is about the communicating the different aspects of the

company and creation of the value. The communication through the integrated report is

generally concise that covers generally the performance, governance, strategy and the

prospects of the organization, which creates short, medium and long term value.

Hence, the sustainability reporting is the communication of the company about the

social and environmental aspects facing the organization and their management. However,

integrated report is concerned with the communication of the company regarding all the

aspects such as sustainability, organizational and financial performance, governance and so

on.

Requirement B

Conventional Accounting is also referred as historical accounting is defined as the

accounting system, which is considered to be the powerful tool in order to report the

performances in regards to loss or profit to the stakeholders.

Conventional Accounting has the strength of maintaining the accounting information

that has objectivity and depicts reliability (Tschopp & Huefner, 2015). Under this the

disclosures, criteria for preparing the report of sustainability and the reporting principles.

However, the second part is the implementation manual, which includes the explanations of

applying principles of reporting, the way in which there is disclosure of the information and

interpretations of different concepts in given guidelines.

Framework of International Integrated Reporting

For accelerating integrated reporting adoption, the framework of International

integrated reporting are used. It establishes the purpose of providing the rules and guiding

principles, which helps in governing the explanation of basic concepts and overall integrated

report contents. Integrated reporting is the process that results in periodically issuing of the

integrated report by company, which is about the communicating the different aspects of the

company and creation of the value. The communication through the integrated report is

generally concise that covers generally the performance, governance, strategy and the

prospects of the organization, which creates short, medium and long term value.

Hence, the sustainability reporting is the communication of the company about the

social and environmental aspects facing the organization and their management. However,

integrated report is concerned with the communication of the company regarding all the

aspects such as sustainability, organizational and financial performance, governance and so

on.

Requirement B

Conventional Accounting is also referred as historical accounting is defined as the

accounting system, which is considered to be the powerful tool in order to report the

performances in regards to loss or profit to the stakeholders.

Conventional Accounting has the strength of maintaining the accounting information

that has objectivity and depicts reliability (Tschopp & Huefner, 2015). Under this the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CONTEMPORARY ACCOUNTING THEORY

manipulations of data is not possible. This is the simple concept as on the original amount,

transactions are recorded. In this, restatements of financial statement is not have to be done

for the reflection of the changes in values.

Conventional accounting suffers from so many drawbacks. Under this, changes in the

level of price is not taken into consideration (Innovation for sustainability, 2019). Other

drawbacks includes mixing up of losses or gains of holding inventories, levied of the taxes on

money profit, charging historical costs on the assets.

Hence, it promotes sustainability and contribution of sustainability of globalized

economy. For the welfare of the society, conventional accounting play vital role. Moreover,

integrated accounting with conventional accounting helps in the enhancement of decision

making power of the stakeholders and the investors.

Requirement C

The determination of the report content is done by the help of conducting internal

evaluation, by following the standards as well as by other methods. Sustainability reports

development has helped in identifying the challenges such as collecting data, selection of the

data and appropriate balance in reporting. Further, there are potential future for sustainability

uses such as improvements in the tracking performance ability of real time. The effectiveness

of Integrated Reporting is measured in terms of its effectiveness from stakeholders’

perspectives. However, very few stakeholders uses integrated reports as the main source of

their investment and financial information. Although, various opportunities are available in

future for integrated reporting.

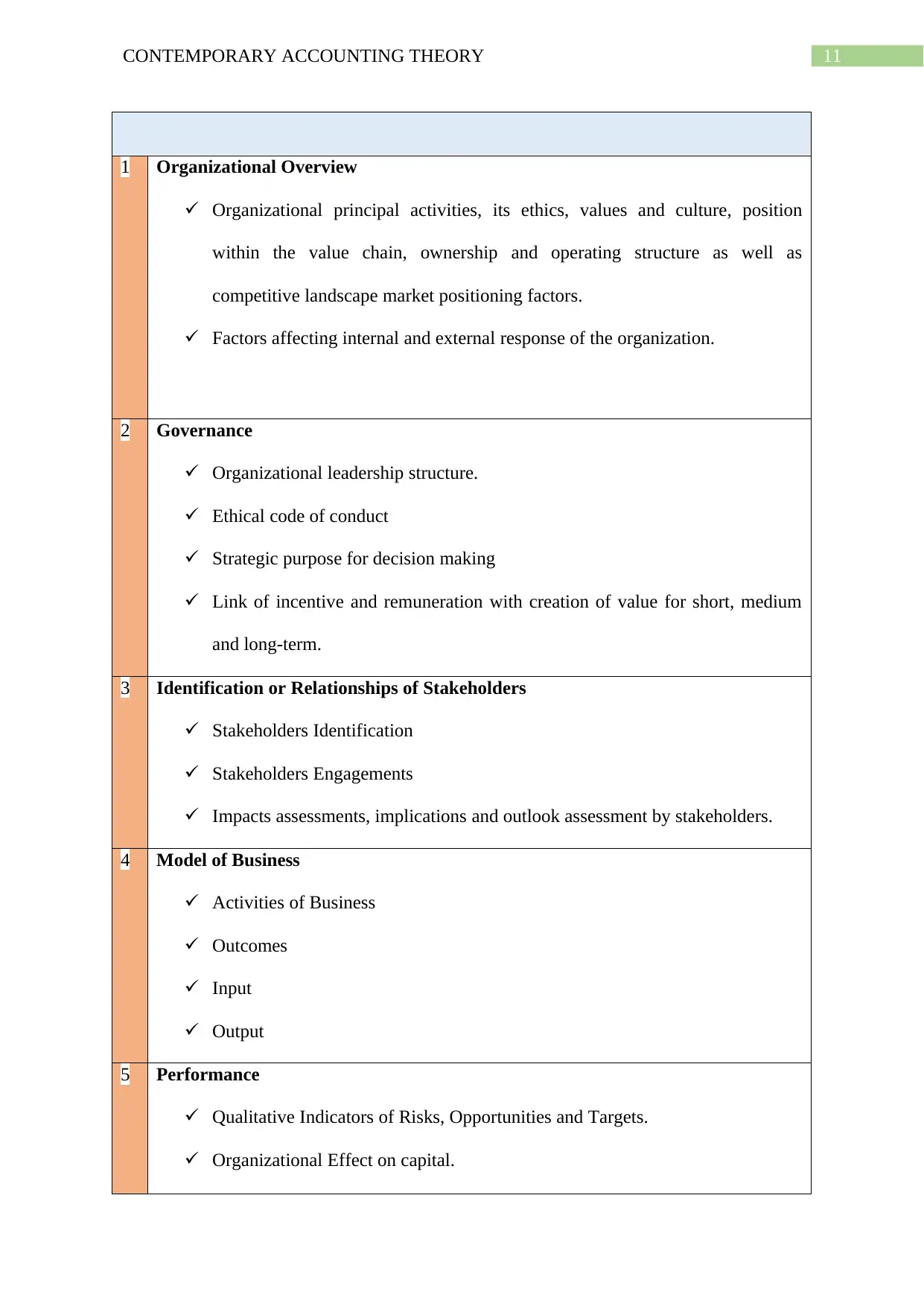

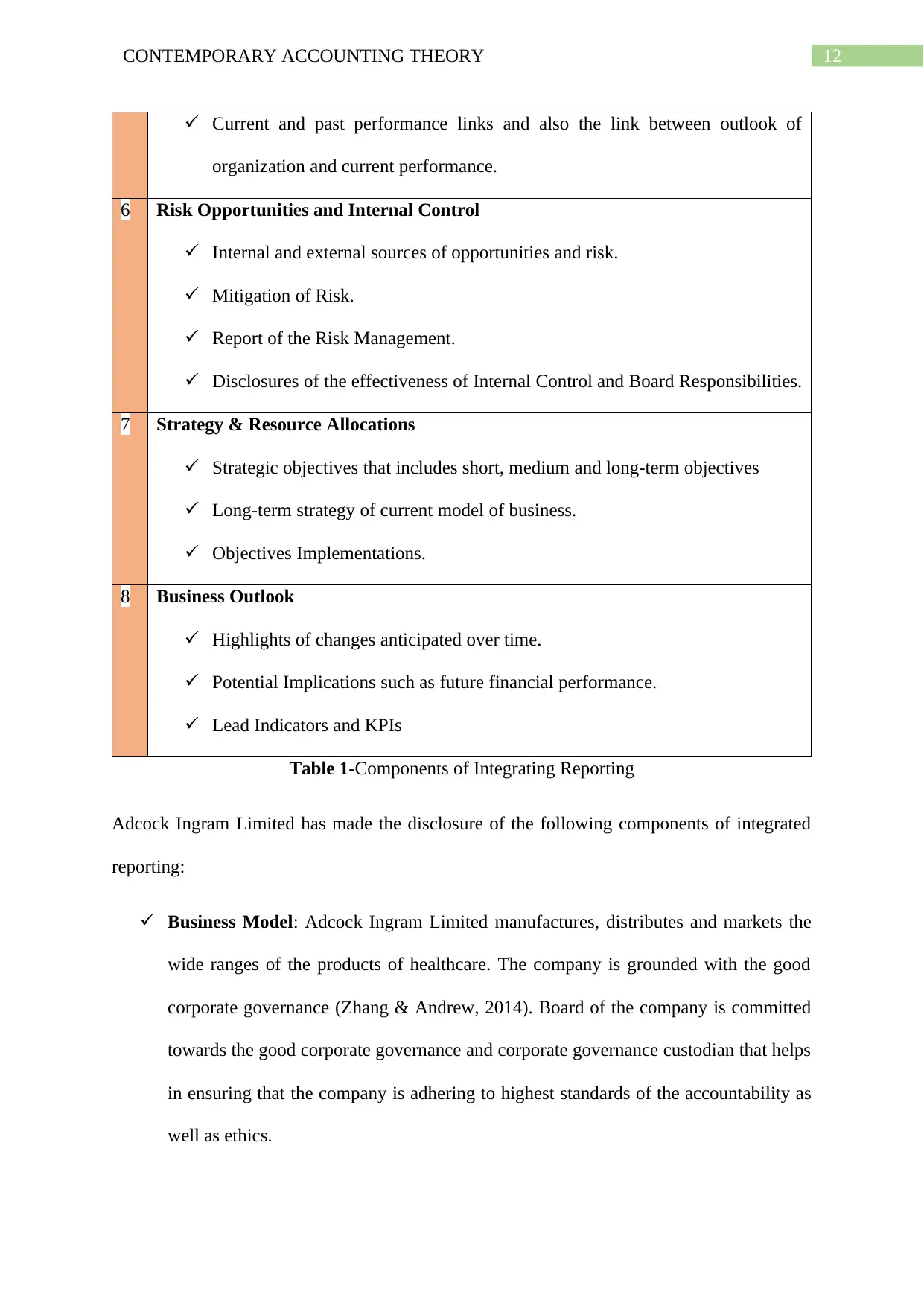

Requirement D

Integrated Report Components

Integrated Report Components

manipulations of data is not possible. This is the simple concept as on the original amount,

transactions are recorded. In this, restatements of financial statement is not have to be done

for the reflection of the changes in values.

Conventional accounting suffers from so many drawbacks. Under this, changes in the

level of price is not taken into consideration (Innovation for sustainability, 2019). Other

drawbacks includes mixing up of losses or gains of holding inventories, levied of the taxes on

money profit, charging historical costs on the assets.

Hence, it promotes sustainability and contribution of sustainability of globalized

economy. For the welfare of the society, conventional accounting play vital role. Moreover,

integrated accounting with conventional accounting helps in the enhancement of decision

making power of the stakeholders and the investors.

Requirement C

The determination of the report content is done by the help of conducting internal

evaluation, by following the standards as well as by other methods. Sustainability reports

development has helped in identifying the challenges such as collecting data, selection of the

data and appropriate balance in reporting. Further, there are potential future for sustainability

uses such as improvements in the tracking performance ability of real time. The effectiveness

of Integrated Reporting is measured in terms of its effectiveness from stakeholders’

perspectives. However, very few stakeholders uses integrated reports as the main source of

their investment and financial information. Although, various opportunities are available in

future for integrated reporting.

Requirement D

Integrated Report Components

Integrated Report Components

11CONTEMPORARY ACCOUNTING THEORY

1 Organizational Overview

Organizational principal activities, its ethics, values and culture, position

within the value chain, ownership and operating structure as well as

competitive landscape market positioning factors.

Factors affecting internal and external response of the organization.

2 Governance

Organizational leadership structure.

Ethical code of conduct

Strategic purpose for decision making

Link of incentive and remuneration with creation of value for short, medium

and long-term.

3 Identification or Relationships of Stakeholders

Stakeholders Identification

Stakeholders Engagements

Impacts assessments, implications and outlook assessment by stakeholders.

4 Model of Business

Activities of Business

Outcomes

Input

Output

5 Performance

Qualitative Indicators of Risks, Opportunities and Targets.

Organizational Effect on capital.

1 Organizational Overview

Organizational principal activities, its ethics, values and culture, position

within the value chain, ownership and operating structure as well as

competitive landscape market positioning factors.

Factors affecting internal and external response of the organization.

2 Governance

Organizational leadership structure.

Ethical code of conduct

Strategic purpose for decision making

Link of incentive and remuneration with creation of value for short, medium

and long-term.

3 Identification or Relationships of Stakeholders

Stakeholders Identification

Stakeholders Engagements

Impacts assessments, implications and outlook assessment by stakeholders.

4 Model of Business

Activities of Business

Outcomes

Input

Output

5 Performance

Qualitative Indicators of Risks, Opportunities and Targets.

Organizational Effect on capital.

12CONTEMPORARY ACCOUNTING THEORY

Current and past performance links and also the link between outlook of

organization and current performance.

6 Risk Opportunities and Internal Control

Internal and external sources of opportunities and risk.

Mitigation of Risk.

Report of the Risk Management.

Disclosures of the effectiveness of Internal Control and Board Responsibilities.

7 Strategy & Resource Allocations

Strategic objectives that includes short, medium and long-term objectives

Long-term strategy of current model of business.

Objectives Implementations.

8 Business Outlook

Highlights of changes anticipated over time.

Potential Implications such as future financial performance.

Lead Indicators and KPIs

Table 1-Components of Integrating Reporting

Adcock Ingram Limited has made the disclosure of the following components of integrated

reporting:

Business Model: Adcock Ingram Limited manufactures, distributes and markets the

wide ranges of the products of healthcare. The company is grounded with the good

corporate governance (Zhang & Andrew, 2014). Board of the company is committed

towards the good corporate governance and corporate governance custodian that helps

in ensuring that the company is adhering to highest standards of the accountability as

well as ethics.

Current and past performance links and also the link between outlook of

organization and current performance.

6 Risk Opportunities and Internal Control

Internal and external sources of opportunities and risk.

Mitigation of Risk.

Report of the Risk Management.

Disclosures of the effectiveness of Internal Control and Board Responsibilities.

7 Strategy & Resource Allocations

Strategic objectives that includes short, medium and long-term objectives

Long-term strategy of current model of business.

Objectives Implementations.

8 Business Outlook

Highlights of changes anticipated over time.

Potential Implications such as future financial performance.

Lead Indicators and KPIs

Table 1-Components of Integrating Reporting

Adcock Ingram Limited has made the disclosure of the following components of integrated

reporting:

Business Model: Adcock Ingram Limited manufactures, distributes and markets the

wide ranges of the products of healthcare. The company is grounded with the good

corporate governance (Zhang & Andrew, 2014). Board of the company is committed

towards the good corporate governance and corporate governance custodian that helps

in ensuring that the company is adhering to highest standards of the accountability as

well as ethics.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CONTEMPORARY ACCOUNTING THEORY

Leadership review of CEO and Chairman: The board of directors of the company

continues for accessing the effectiveness of process, structures and practices of the

organization that helps in managing the operations of the company.

Financial Performance: The Company is satisfied with the set of the financial results

that shows growth in the turnover, headline earnings and trading profit from the

continuing operations.

Operational Performance: It includes over the counter performance, prescription

and hospitals. OTC supplies the medications for the patients in the private and public

sector of South Africa (Searcy & Buslovich, 2013). The division of prescription is

focused on the offering and building of the broad range of the quality and medicines

that are affordable. The company is leading supplier and manufacturer of critical care

products and hospitals.

Shareholders Information: It includes analysis of shareholders. The company

discloses additional information in relation to the shareholders and stakeholders.

Strategic Performance: It includes mapping out of the integrated thinking approach.

Sustainability: This includes manufactured capital, intellectual capital, human

capital, natural capital and social and relationships capital.

Governance: This includes risks management, remuneration, directors’ responsibility

and report as well as consolidated financial statements.

Requirement E

Ramsay Health Care Limited does not prepares integrated report rather than company

prepares the statement of corporate governance. Under the corporate governance statement,

the way in which the business is managed, the way in which business of the company is

carried out as per stakeholders desires, conducted by board of directors and committee

concerned. Further annual report is prepared for disclosing company’s financial performances

Leadership review of CEO and Chairman: The board of directors of the company

continues for accessing the effectiveness of process, structures and practices of the

organization that helps in managing the operations of the company.

Financial Performance: The Company is satisfied with the set of the financial results

that shows growth in the turnover, headline earnings and trading profit from the

continuing operations.

Operational Performance: It includes over the counter performance, prescription

and hospitals. OTC supplies the medications for the patients in the private and public

sector of South Africa (Searcy & Buslovich, 2013). The division of prescription is

focused on the offering and building of the broad range of the quality and medicines

that are affordable. The company is leading supplier and manufacturer of critical care

products and hospitals.

Shareholders Information: It includes analysis of shareholders. The company

discloses additional information in relation to the shareholders and stakeholders.

Strategic Performance: It includes mapping out of the integrated thinking approach.

Sustainability: This includes manufactured capital, intellectual capital, human

capital, natural capital and social and relationships capital.

Governance: This includes risks management, remuneration, directors’ responsibility

and report as well as consolidated financial statements.

Requirement E

Ramsay Health Care Limited does not prepares integrated report rather than company

prepares the statement of corporate governance. Under the corporate governance statement,

the way in which the business is managed, the way in which business of the company is

carried out as per stakeholders desires, conducted by board of directors and committee

concerned. Further annual report is prepared for disclosing company’s financial performances

14CONTEMPORARY ACCOUNTING THEORY

(Kirkman, 2014). Corporate Governance report consists of the board of directors that includes

independence, skill, competency, composition, risk management, financial reporting integrity

and sustainability and accounting policies (Adcock, 2019).

Therefore, differences between sustainability reporting and integrating reporting is

that integrated reporting helps in summarizing all information of the sustainability report and

annual report in one report.

Conclusion

The paper concludes that the conceptual framework has the very vast and long history

of development. The Australian accounting have the several advantages and the

disadvantages of the International Financial Reporting Standards. The conceptual framework

also have various benefits and the limitation regarding the financial information reporting of

the company. The Sustainability Guidelines of the Global Reporting Initiative and the

International Integrated Reporting framework of the International Integrated Reporting

Council almost give the same point of the regarding the corporate social responsibility

reporting. The conventional accounting have the various strength and limitation in the

conceptual framework for financial reporting. Lastly, the sustainability report as well as the

integrated report have the various usefulness as well as the limitation regarding the

implementation in the financial reporting of the firm.

(Kirkman, 2014). Corporate Governance report consists of the board of directors that includes

independence, skill, competency, composition, risk management, financial reporting integrity

and sustainability and accounting policies (Adcock, 2019).

Therefore, differences between sustainability reporting and integrating reporting is

that integrated reporting helps in summarizing all information of the sustainability report and

annual report in one report.

Conclusion

The paper concludes that the conceptual framework has the very vast and long history

of development. The Australian accounting have the several advantages and the

disadvantages of the International Financial Reporting Standards. The conceptual framework

also have various benefits and the limitation regarding the financial information reporting of

the company. The Sustainability Guidelines of the Global Reporting Initiative and the

International Integrated Reporting framework of the International Integrated Reporting

Council almost give the same point of the regarding the corporate social responsibility

reporting. The conventional accounting have the various strength and limitation in the

conceptual framework for financial reporting. Lastly, the sustainability report as well as the

integrated report have the various usefulness as well as the limitation regarding the

implementation in the financial reporting of the firm.

15CONTEMPORARY ACCOUNTING THEORY

References and Bibliography

ACCA Global. (2019) www.accaglobal.com, A. Conceptual frameworks | F7 Financial

Reporting | ACCA Qualification | Students. Accaglobal.com. Retrieved 27 May 2019,

from

https://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-

exams-study-resources/f7/technical-articles/conceptual-framework-need.html

Adcock. (2019). Retrieved from http://www.adcock.com/Content/pdf/Adcock_A5_Booklet_6.pdf

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal

of International Financial Management & Accounting, 25(1), 90-119.

Collings, S., & Profile, A. (2019).Conceptual Framework for Financial Reporting: an

overview : Steve Collings. Stevecollings.co.uk. Retrieved 27 May 2019, from

http://stevecollings.co.uk/conceptual-framework-for-financial-reporting-an-overview/

Danilenko, O. (2018). The revised Conceptual Framework: new ground rules - KPMG

Luxembourg. KPMG Luxembourg. Retrieved 27 May 2019, from

https://blog.kpmg.lu/the-revised-conceptual-framework-new-ground-rules/

Global Reporting Initiative . (2019). Globalreporting.org. Retrieved 27 May 2019, from

https://www.globalreporting.org/Pages/default.aspx

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Herath, S.K. & Albarqi, N. (2017). Financial reporting quality: A literature

review. International Business Management and Commerce, 2(2).

References and Bibliography

ACCA Global. (2019) www.accaglobal.com, A. Conceptual frameworks | F7 Financial

Reporting | ACCA Qualification | Students. Accaglobal.com. Retrieved 27 May 2019,

from

https://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-

exams-study-resources/f7/technical-articles/conceptual-framework-need.html

Adcock. (2019). Retrieved from http://www.adcock.com/Content/pdf/Adcock_A5_Booklet_6.pdf

Cheng, M., Green, W., Conradie, P., Konishi, N., & Romi, A. (2014). The international

integrated reporting framework: key issues and future research opportunities. Journal

of International Financial Management & Accounting, 25(1), 90-119.

Collings, S., & Profile, A. (2019).Conceptual Framework for Financial Reporting: an

overview : Steve Collings. Stevecollings.co.uk. Retrieved 27 May 2019, from

http://stevecollings.co.uk/conceptual-framework-for-financial-reporting-an-overview/

Danilenko, O. (2018). The revised Conceptual Framework: new ground rules - KPMG

Luxembourg. KPMG Luxembourg. Retrieved 27 May 2019, from

https://blog.kpmg.lu/the-revised-conceptual-framework-new-ground-rules/

Global Reporting Initiative . (2019). Globalreporting.org. Retrieved 27 May 2019, from

https://www.globalreporting.org/Pages/default.aspx

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Herath, S.K. & Albarqi, N. (2017). Financial reporting quality: A literature

review. International Business Management and Commerce, 2(2).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CONTEMPORARY ACCOUNTING THEORY

Innovation for sustainability (2019). Innovation for sustainability: a conceptual framework |

Journal of Management Development | Vol 36, No 1.. Journal Of Management

Development. Retrieved from

https://www.emeraldinsight.com/doi/full/10.1108/JMD-09-2014-0099

Integrated Reporting. (2019) International <IR> Framework . Integratedreporting.org.

Retrieved 27 May 2019, from http://integratedreporting.org/resource/international-ir-

framework/

Kirkman, P. (2014). Accounting Under Inflationary Conditions (RLE Accounting).

Routledge.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Ramsayhealth. (2019). Retrieved from

http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf

Rensburg, R., & Botha, E. (2014). Is Integrated Reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152. doi:10.1016/j.pubrev.2013.11.016

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Searcy, C., & Buslovich, R. (2013). Corporate Perspectives on the Development and Use of

Sustainability Reports. Journal Of Business Ethics, 121(2), 149-169.

doi:10.1007/s10551-013-1701-7

The IIRC | Integrated Reporting. (2019). Integratedreporting.org. Retrieved 27 May 2019,

from https://integratedreporting.org/the-iirc-2/

Innovation for sustainability (2019). Innovation for sustainability: a conceptual framework |

Journal of Management Development | Vol 36, No 1.. Journal Of Management

Development. Retrieved from

https://www.emeraldinsight.com/doi/full/10.1108/JMD-09-2014-0099

Integrated Reporting. (2019) International <IR> Framework . Integratedreporting.org.

Retrieved 27 May 2019, from http://integratedreporting.org/resource/international-ir-

framework/

Kirkman, P. (2014). Accounting Under Inflationary Conditions (RLE Accounting).

Routledge.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Ramsayhealth. (2019). Retrieved from

http://www.ramsayhealth.com/common/emag/rhc/annualreport2018/RHC-AR2018.pdf

Rensburg, R., & Botha, E. (2014). Is Integrated Reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152. doi:10.1016/j.pubrev.2013.11.016

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Searcy, C., & Buslovich, R. (2013). Corporate Perspectives on the Development and Use of

Sustainability Reports. Journal Of Business Ethics, 121(2), 149-169.

doi:10.1007/s10551-013-1701-7

The IIRC | Integrated Reporting. (2019). Integratedreporting.org. Retrieved 27 May 2019,

from https://integratedreporting.org/the-iirc-2/

17CONTEMPORARY ACCOUNTING THEORY

THEORETICAL AND CONCEPTUAL FRAMEWORK: MANDATORY INGREDIENTS

OF A QUALITY RESEARCH. (2019). Retrieved from

https://www.researchgate.net/publication/322204158_THEORETICAL_AND_CONC

EPTUAL_FRAMEWORK_MANDATORY_INGREDIENTS_OF_A_QUALITY_R

ESEARCH

Truworths | Online Fashion & Trends. (2019). Truworths. Retrieved 27 May 2019, from

https://www.truworths.co.za/

Tschopp, D., & Huefner, R. J. (2015). Comparing the evolution of CSR reporting to that of

financial reporting. Journal of Business Ethics, 127(3), 565-577.

Zhang, Y., & Andrew, J. (2014). Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), 17-26.

THEORETICAL AND CONCEPTUAL FRAMEWORK: MANDATORY INGREDIENTS

OF A QUALITY RESEARCH. (2019). Retrieved from

https://www.researchgate.net/publication/322204158_THEORETICAL_AND_CONC

EPTUAL_FRAMEWORK_MANDATORY_INGREDIENTS_OF_A_QUALITY_R

ESEARCH

Truworths | Online Fashion & Trends. (2019). Truworths. Retrieved 27 May 2019, from

https://www.truworths.co.za/

Tschopp, D., & Huefner, R. J. (2015). Comparing the evolution of CSR reporting to that of

financial reporting. Journal of Business Ethics, 127(3), 565-577.

Zhang, Y., & Andrew, J. (2014). Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), 17-26.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.