Contemporary Accounting Theory

VerifiedAdded on 2023/04/03

|20

|3796

|249

AI Summary

This report focuses on the development and history of conceptual framework, concerns of Australian accounting profession, and academic concerns regarding quality of conceptual framework for financial reporting. It also discusses sustainability reporting guidelines and the strengths and limitations of conventional accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ACCOUNTING THEORY

Contemporary accounting theory

Name of the student

Name of the university

Student ID

Author note

Contemporary accounting theory

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CONTEMPORARY ACCOUNTING THEORY

Executive summary

From the report presented below it can be sated that background of conceptual framework is that

each country including UK, USA, Australia and on global basis the accountants are going

through the same thought process regarding accounting. Large numbers of stakeholders are

interested in understandable, reliable and comparable financial statements that can be used by

large numbers of users. Main objective of sustainability reporting is to establish the guiding

principles and content element that governs the entire substance of the integrated reporting.

Further, it explains fundamental concepts required for strengthening the same. Considering the

integrated reporting index it is found that Iress Ltd from Australia does not prepare integrated

report whereas South African company Naspers Ltd prepares the same and covers all the

required aspects.

Executive summary

From the report presented below it can be sated that background of conceptual framework is that

each country including UK, USA, Australia and on global basis the accountants are going

through the same thought process regarding accounting. Large numbers of stakeholders are

interested in understandable, reliable and comparable financial statements that can be used by

large numbers of users. Main objective of sustainability reporting is to establish the guiding

principles and content element that governs the entire substance of the integrated reporting.

Further, it explains fundamental concepts required for strengthening the same. Considering the

integrated reporting index it is found that Iress Ltd from Australia does not prepare integrated

report whereas South African company Naspers Ltd prepares the same and covers all the

required aspects.

2CONTEMPORARY ACCOUNTING THEORY

Table of Contents

Introduction......................................................................................................................................3

Part A – Conceptual framework......................................................................................................3

(a) Literature review regarding development and history of conceptual framework.............3

(b) Concerns of Australian accounting profession regarding application of conceptual

framework....................................................................................................................................4

(c) Academic concerns regarding quality of conceptual framework for the financial

reporting.......................................................................................................................................5

(d) Application of conceptual framework...............................................................................7

Part B – Integrated / sustainability reporting...................................................................................9

(a) Sustainability reporting guidelines as per GRI and IIRC.................................................9

(b) Strengths and limitations of conventional accounting....................................................10

(c) Theories for explaining the contents of sustainability and integrated reports................12

(d) Index of different components of integrated report........................................................12

(e) Integrated report of Iress Ltd..........................................................................................14

Conclusion.................................................................................................................................14

Reference.......................................................................................................................................16

Table of Contents

Introduction......................................................................................................................................3

Part A – Conceptual framework......................................................................................................3

(a) Literature review regarding development and history of conceptual framework.............3

(b) Concerns of Australian accounting profession regarding application of conceptual

framework....................................................................................................................................4

(c) Academic concerns regarding quality of conceptual framework for the financial

reporting.......................................................................................................................................5

(d) Application of conceptual framework...............................................................................7

Part B – Integrated / sustainability reporting...................................................................................9

(a) Sustainability reporting guidelines as per GRI and IIRC.................................................9

(b) Strengths and limitations of conventional accounting....................................................10

(c) Theories for explaining the contents of sustainability and integrated reports................12

(d) Index of different components of integrated report........................................................12

(e) Integrated report of Iress Ltd..........................................................................................14

Conclusion.................................................................................................................................14

Reference.......................................................................................................................................16

3CONTEMPORARY ACCOUNTING THEORY

Introduction

Purpose of the study is to concentrate on development and history of conceptual

framework. It will further, highlight the concerns of Australian accounting profession regarding

application of conceptual framework and will list down the academic concerns regarding quality

of conceptual framework for the financial reporting. In the next segment the report will focus on

sustainability reporting guidelines as per GRI and IIRC and will list down the strengths and

limitations of conventional accounting. It will further focus on the Theories for explaining the

contents of sustainability and integrated reports. The report will also present the index of

different components of integrated report and whether the companies are following the same.

Part A – Conceptual framework

(a) Literature review regarding development and history of conceptual framework

Conceptual framework for the purpose of financial reporting is issued by IASB

(international accounting standard board) in 1989 for assisting in the presentation along with

preparation of the annual statements. It sets out concept that is used for shaping presentation and

preparation of the financial statements for the purpose of using it by the external users. In USA

the conceptual framework is proposed to rule the environment of financial reporting through

defining the purpose, nature, content and subject of financial reporting environment applied for

general purposes stipulating the function, limits and nature of the financial reporting and

accounting (Díaz et al., 2015). As stated by Stephen Zeff, over the past few years various

accounting standards in UK were rule based as against principle based. The accounting standards

based on rule offers exceptionally detailed rules that virtually contemplate all the application of

Introduction

Purpose of the study is to concentrate on development and history of conceptual

framework. It will further, highlight the concerns of Australian accounting profession regarding

application of conceptual framework and will list down the academic concerns regarding quality

of conceptual framework for the financial reporting. In the next segment the report will focus on

sustainability reporting guidelines as per GRI and IIRC and will list down the strengths and

limitations of conventional accounting. It will further focus on the Theories for explaining the

contents of sustainability and integrated reports. The report will also present the index of

different components of integrated report and whether the companies are following the same.

Part A – Conceptual framework

(a) Literature review regarding development and history of conceptual framework

Conceptual framework for the purpose of financial reporting is issued by IASB

(international accounting standard board) in 1989 for assisting in the presentation along with

preparation of the annual statements. It sets out concept that is used for shaping presentation and

preparation of the financial statements for the purpose of using it by the external users. In USA

the conceptual framework is proposed to rule the environment of financial reporting through

defining the purpose, nature, content and subject of financial reporting environment applied for

general purposes stipulating the function, limits and nature of the financial reporting and

accounting (Díaz et al., 2015). As stated by Stephen Zeff, over the past few years various

accounting standards in UK were rule based as against principle based. The accounting standards

based on rule offers exceptionally detailed rules that virtually contemplate all the application of

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CONTEMPORARY ACCOUNTING THEORY

the standard. It makes the standards more difficult for the preparers as well as the auditors in

evaluating consistency of overall impact with objectives of the standards (Eizenberg & Jabareen,

2017). Hence, requirement was there for creating the conceptual framework. Growing

international needs for accounting, influence on USA and the growth in global economic

cooperation made development of statement important for UK (Lewandowski, 2016). Australia

started developing conceptual framework during the year 1970 however main work associated

with conceptual framework did not started till the year 1980. The accepted objectives for

financial accounting in Australian conceptual statement are prepared on the basis of the work of

AICPA (Researchbank.rmit.edu.au, 2019). As per Caroline Becker, background of conceptual

framework is that each country including UK, USA, Australia and on global basis the

accountants are going through the same thought process regarding accounting. Large numbers of

stakeholders are engrossed in understandable, reliable and comparable financial statements that

can be used by large numbers of users.

(b) Concerns of Australian accounting profession regarding application of conceptual

framework

Some issues are involved with the conceptual framework which is of major concerns for

the accounting profession in Australia. These issues are as follows –

It is exceptionally difficult to establish the framework. The developed and the rich

countries may set up the own conceptual framework. However, the countries those are

still in developing stage that is extremely (Aasb.gov.au, 2019).

It is rigid as it creeps into the practices of standard accounting owing to framework

implementation. It makes introduction of new ideas impossible into system. Further, the

the standard. It makes the standards more difficult for the preparers as well as the auditors in

evaluating consistency of overall impact with objectives of the standards (Eizenberg & Jabareen,

2017). Hence, requirement was there for creating the conceptual framework. Growing

international needs for accounting, influence on USA and the growth in global economic

cooperation made development of statement important for UK (Lewandowski, 2016). Australia

started developing conceptual framework during the year 1970 however main work associated

with conceptual framework did not started till the year 1980. The accepted objectives for

financial accounting in Australian conceptual statement are prepared on the basis of the work of

AICPA (Researchbank.rmit.edu.au, 2019). As per Caroline Becker, background of conceptual

framework is that each country including UK, USA, Australia and on global basis the

accountants are going through the same thought process regarding accounting. Large numbers of

stakeholders are engrossed in understandable, reliable and comparable financial statements that

can be used by large numbers of users.

(b) Concerns of Australian accounting profession regarding application of conceptual

framework

Some issues are involved with the conceptual framework which is of major concerns for

the accounting profession in Australia. These issues are as follows –

It is exceptionally difficult to establish the framework. The developed and the rich

countries may set up the own conceptual framework. However, the countries those are

still in developing stage that is extremely (Aasb.gov.au, 2019).

It is rigid as it creeps into the practices of standard accounting owing to framework

implementation. It makes introduction of new ideas impossible into system. Further, the

5CONTEMPORARY ACCOUNTING THEORY

conceptual accounting is involved with various inflexibility as some of the aspects is not

able to provide much direction for accounting (Aasb.gov.au, 2019).

Another concern with the conceptual framework is following its concept may create

conflict among the practice that is prescribed by previous accounting standards and latest

conceptual framework. Moreover, the existing standards vary with fundamental

conceptual framework that leads to conflict.

Apart from above, another concern is that it may be the case that the opportunity

provided by conceptual framework may be rejected by some of the parties. It may be

beneficial to some interested groups only who are identified as the users. Conversely,

conceptual framework may offer some opportunities those are not acceptable to the other

parties. Hence, the same conceptual framework may not work for all parties

(Aasb.gov.au, 2019).

(c) Academic concerns regarding quality of conceptual framework for the financial

reporting

Potential advantages of conceptual framework in context of academics are as follows –

Developments of the concepts are made in orderly manner that makes the financial

reporting as well as accounting logical and consistent that will increase the compatibility

of the standard internationally and the same is facilitated through economic development

and consistency of accounting and the overall improved communication (Maas,

Schaltegger & Crutzen, 2016).

Development of the standard with backing of the conceptual framework is become easier

as well as more economical in context of cost as founding the basic principles are debated

as well as established already. These principles can be successfully applied under the

conceptual accounting is involved with various inflexibility as some of the aspects is not

able to provide much direction for accounting (Aasb.gov.au, 2019).

Another concern with the conceptual framework is following its concept may create

conflict among the practice that is prescribed by previous accounting standards and latest

conceptual framework. Moreover, the existing standards vary with fundamental

conceptual framework that leads to conflict.

Apart from above, another concern is that it may be the case that the opportunity

provided by conceptual framework may be rejected by some of the parties. It may be

beneficial to some interested groups only who are identified as the users. Conversely,

conceptual framework may offer some opportunities those are not acceptable to the other

parties. Hence, the same conceptual framework may not work for all parties

(Aasb.gov.au, 2019).

(c) Academic concerns regarding quality of conceptual framework for the financial

reporting

Potential advantages of conceptual framework in context of academics are as follows –

Developments of the concepts are made in orderly manner that makes the financial

reporting as well as accounting logical and consistent that will increase the compatibility

of the standard internationally and the same is facilitated through economic development

and consistency of accounting and the overall improved communication (Maas,

Schaltegger & Crutzen, 2016).

Development of the standard with backing of the conceptual framework is become easier

as well as more economical in context of cost as founding the basic principles are debated

as well as established already. These principles can be successfully applied under the

6CONTEMPORARY ACCOUNTING THEORY

circumstances where the pertinent accounting standards or related guide do not exist and

where interest conflict may arise regarding the application of policies in specific

instances. However, the policies established under conceptual framework will be less

criticised.

Without the conceptual Framework, the standard setters will be exposed to external

pressure from the interest groups that will lead to ambiguous as well as hazard guidelines

and rules. However, with the defined framework and the explanation of reasoning behind

particular standard the standard setters will become more accountable to the users of

financial reporting and statement as with these users will be aware and will be able in

recognising the departure from the set out principles (Morioka & de Carvalho, 2016).

Overall, conceptual framework significantly contributes to the academic credibility as

well as public confidence regarding the financial reporting with regard to reliability, relevance

and consistency through employing the uniform as well as clearly defined principles.

Potential limitations of conceptual framework in context of academics are as follows –

Conceptual framework can be considered as too general by its nature and the principal

are relied upon on wide range of assumptions. Hence, it may be less valuable while

producing the financial statement actually and it may result into development of the

accounting standards that are very academic, susceptible to fraud and theoretical. This

standard however in practice makes the provisions of the financial information complex

for the preparers as well as for the users of financial statements. Moreover the concepts

may be refined and can be pure however as these are involved with difficulty and

circumstances where the pertinent accounting standards or related guide do not exist and

where interest conflict may arise regarding the application of policies in specific

instances. However, the policies established under conceptual framework will be less

criticised.

Without the conceptual Framework, the standard setters will be exposed to external

pressure from the interest groups that will lead to ambiguous as well as hazard guidelines

and rules. However, with the defined framework and the explanation of reasoning behind

particular standard the standard setters will become more accountable to the users of

financial reporting and statement as with these users will be aware and will be able in

recognising the departure from the set out principles (Morioka & de Carvalho, 2016).

Overall, conceptual framework significantly contributes to the academic credibility as

well as public confidence regarding the financial reporting with regard to reliability, relevance

and consistency through employing the uniform as well as clearly defined principles.

Potential limitations of conceptual framework in context of academics are as follows –

Conceptual framework can be considered as too general by its nature and the principal

are relied upon on wide range of assumptions. Hence, it may be less valuable while

producing the financial statement actually and it may result into development of the

accounting standards that are very academic, susceptible to fraud and theoretical. This

standard however in practice makes the provisions of the financial information complex

for the preparers as well as for the users of financial statements. Moreover the concepts

may be refined and can be pure however as these are involved with difficulty and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ACCOUNTING THEORY

complexity to understand usefulness of the financial statement can be viewed as less

valuable (Botosan, 2019).

Requirements of the users are wide and hence there is requirement for wide variety of

standard where the conceptual framework cannot cover the wide range of requirements

without involving complexities. In search for the common ground as well as simplicity

and gaining the desired wide level of acceptance conceptual Framework is required to

cover various generalizations that suffer inadequacies. This requires the development of

particular rules for governing instances involving the inadequacies (Macve, 2015).

(d) Application of conceptual framework

(i) Statements or report prepared by the entities

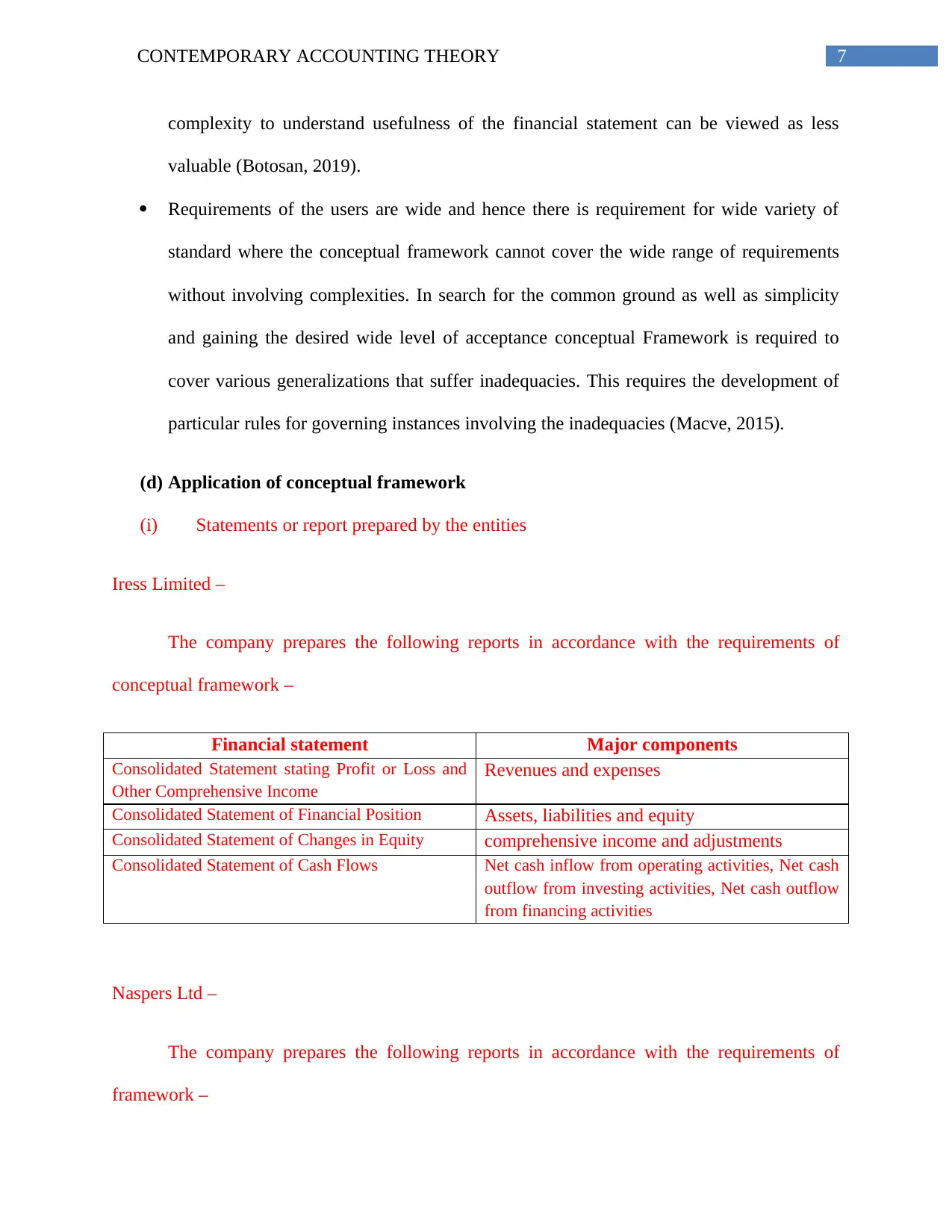

Iress Limited –

The company prepares the following reports in accordance with the requirements of

conceptual framework –

Financial statement Major components

Consolidated Statement stating Profit or Loss and

Other Comprehensive Income

Revenues and expenses

Consolidated Statement of Financial Position Assets, liabilities and equity

Consolidated Statement of Changes in Equity comprehensive income and adjustments

Consolidated Statement of Cash Flows Net cash inflow from operating activities, Net cash

outflow from investing activities, Net cash outflow

from financing activities

Naspers Ltd –

The company prepares the following reports in accordance with the requirements of

framework –

complexity to understand usefulness of the financial statement can be viewed as less

valuable (Botosan, 2019).

Requirements of the users are wide and hence there is requirement for wide variety of

standard where the conceptual framework cannot cover the wide range of requirements

without involving complexities. In search for the common ground as well as simplicity

and gaining the desired wide level of acceptance conceptual Framework is required to

cover various generalizations that suffer inadequacies. This requires the development of

particular rules for governing instances involving the inadequacies (Macve, 2015).

(d) Application of conceptual framework

(i) Statements or report prepared by the entities

Iress Limited –

The company prepares the following reports in accordance with the requirements of

conceptual framework –

Financial statement Major components

Consolidated Statement stating Profit or Loss and

Other Comprehensive Income

Revenues and expenses

Consolidated Statement of Financial Position Assets, liabilities and equity

Consolidated Statement of Changes in Equity comprehensive income and adjustments

Consolidated Statement of Cash Flows Net cash inflow from operating activities, Net cash

outflow from investing activities, Net cash outflow

from financing activities

Naspers Ltd –

The company prepares the following reports in accordance with the requirements of

framework –

8CONTEMPORARY ACCOUNTING THEORY

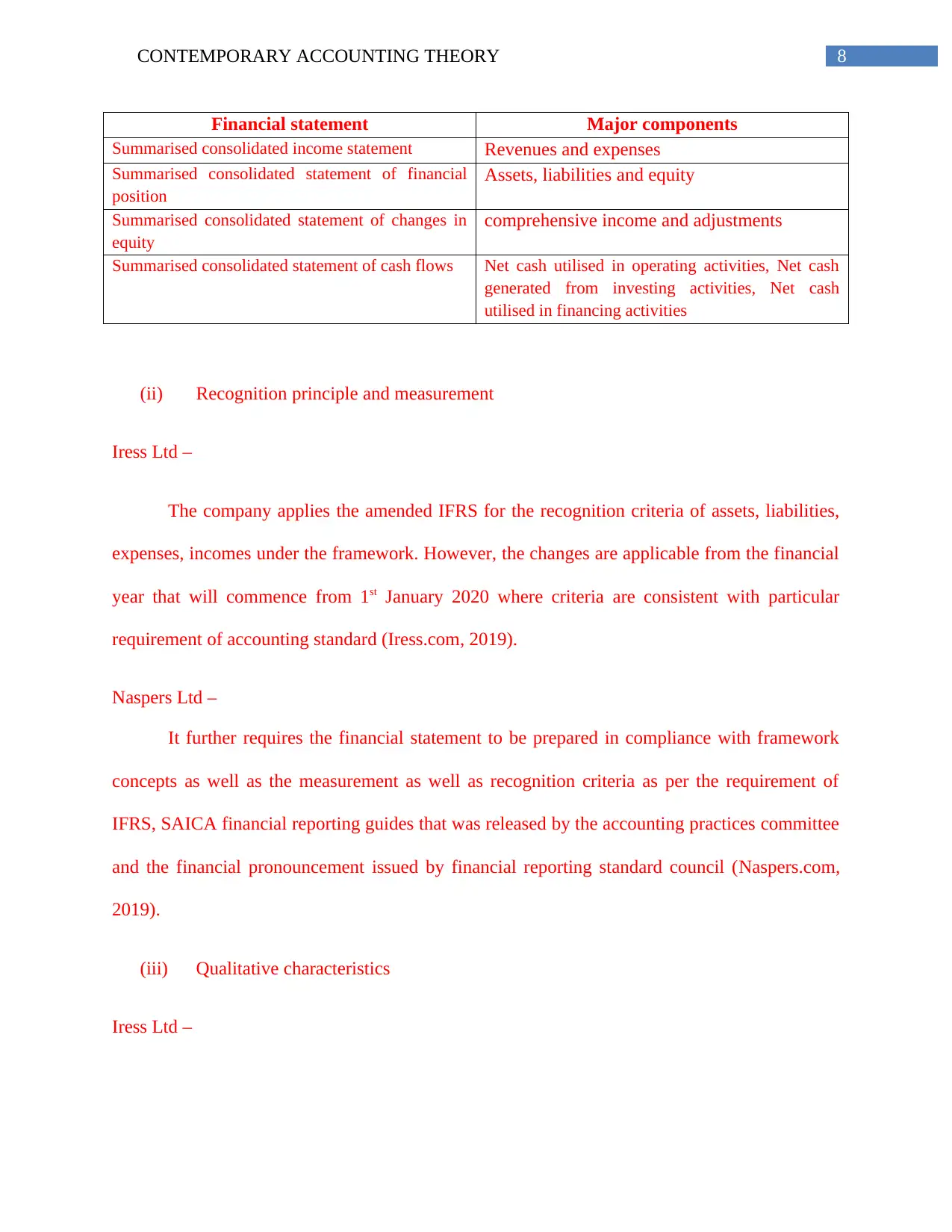

Financial statement Major components

Summarised consolidated income statement Revenues and expenses

Summarised consolidated statement of financial

position

Assets, liabilities and equity

Summarised consolidated statement of changes in

equity

comprehensive income and adjustments

Summarised consolidated statement of cash flows Net cash utilised in operating activities, Net cash

generated from investing activities, Net cash

utilised in financing activities

(ii) Recognition principle and measurement

Iress Ltd –

The company applies the amended IFRS for the recognition criteria of assets, liabilities,

expenses, incomes under the framework. However, the changes are applicable from the financial

year that will commence from 1st January 2020 where criteria are consistent with particular

requirement of accounting standard (Iress.com, 2019).

Naspers Ltd –

It further requires the financial statement to be prepared in compliance with framework

concepts as well as the measurement as well as recognition criteria as per the requirement of

IFRS, SAICA financial reporting guides that was released by the accounting practices committee

and the financial pronouncement issued by financial reporting standard council (Naspers.com,

2019).

(iii) Qualitative characteristics

Iress Ltd –

Financial statement Major components

Summarised consolidated income statement Revenues and expenses

Summarised consolidated statement of financial

position

Assets, liabilities and equity

Summarised consolidated statement of changes in

equity

comprehensive income and adjustments

Summarised consolidated statement of cash flows Net cash utilised in operating activities, Net cash

generated from investing activities, Net cash

utilised in financing activities

(ii) Recognition principle and measurement

Iress Ltd –

The company applies the amended IFRS for the recognition criteria of assets, liabilities,

expenses, incomes under the framework. However, the changes are applicable from the financial

year that will commence from 1st January 2020 where criteria are consistent with particular

requirement of accounting standard (Iress.com, 2019).

Naspers Ltd –

It further requires the financial statement to be prepared in compliance with framework

concepts as well as the measurement as well as recognition criteria as per the requirement of

IFRS, SAICA financial reporting guides that was released by the accounting practices committee

and the financial pronouncement issued by financial reporting standard council (Naspers.com,

2019).

(iii) Qualitative characteristics

Iress Ltd –

9CONTEMPORARY ACCOUNTING THEORY

The company is for profit organisation that is Australian domiciled. The entire year’s

financial report is the general purpose financial report comprised of the entity and its

subsidiaries. For the year closed at 31st December 2018 the entity’s annual statement has been

prepared with the required of Corporation Act AAS and its interpretation and IFRS. Further, the

company’s financial statements are prepared with true and fair manner (Iress.com, 2019).

Naspers Ltd –

The consolidated financial statement of the entity is prepared in compliance with the

requirement of JSE Limited listing that is relevant to provisions of Companies Act. Accounting

policies are applied consistently while the consolidated annual statements are prepared from

which summarised consolidated financial results are derived. Further, the company’s financial

statements are prepared with true and fair manner (Naspers.com, 2019).

The company is for profit organisation that is Australian domiciled. The entire year’s

financial report is the general purpose financial report comprised of the entity and its

subsidiaries. For the year closed at 31st December 2018 the entity’s annual statement has been

prepared with the required of Corporation Act AAS and its interpretation and IFRS. Further, the

company’s financial statements are prepared with true and fair manner (Iress.com, 2019).

Naspers Ltd –

The consolidated financial statement of the entity is prepared in compliance with the

requirement of JSE Limited listing that is relevant to provisions of Companies Act. Accounting

policies are applied consistently while the consolidated annual statements are prepared from

which summarised consolidated financial results are derived. Further, the company’s financial

statements are prepared with true and fair manner (Naspers.com, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CONTEMPORARY ACCOUNTING THEORY

Part B – Integrated / sustainability reporting

(a) Sustainability reporting guidelines as per GRI and IIRC

Integrated reporting offers the entities with the broad perspective regarding risks and the

GRI encourages using the GRI standards who wants to do the integrated reporting. United

through the shared vision that the businesses shall focus on the value creation over long, medium

as well as shorter term, IIRC as well as GRI both continue working together with the alignment

of GRI standards and international framework for improving the corporate reporting (Global

Reporting Initiative, 2019).

IIRC and GRI both work together as the strategic partner and share the common vision

for analysis of Corporate reporting under which the clarity as well as the alignment of Corporate

reporting framework, requirements and the standard drive consistency and comparability that

leads to improve effectiveness and efficiency in practice of corporate

reporting(Integratedreporting.org, 2019). Further, both the organisations identify significance of

the corporate reporting while promoting the sustainable development. IIRC and GRE accepts the

complementarity of respective roles based on that sustainability reporting that is the central part

for integrated reporting G4 of GIR is the crucial starting point that ensure that the strong

sustainability metrics are involved under the integrated reports on the basis of international

Framework where the material is to create value over the time period. Both the organisations are

committed in identifying the approaches for alignment with the objectives of strengthening the

corporate reporting (Integratedreporting.org, 2019). Further, they will continue to

communicating proactively with the market regarding the nature, role and alignment of each

other frameworks standard and guidelines to facilitate understanding as well as clarity in the

Part B – Integrated / sustainability reporting

(a) Sustainability reporting guidelines as per GRI and IIRC

Integrated reporting offers the entities with the broad perspective regarding risks and the

GRI encourages using the GRI standards who wants to do the integrated reporting. United

through the shared vision that the businesses shall focus on the value creation over long, medium

as well as shorter term, IIRC as well as GRI both continue working together with the alignment

of GRI standards and international framework for improving the corporate reporting (Global

Reporting Initiative, 2019).

IIRC and GRI both work together as the strategic partner and share the common vision

for analysis of Corporate reporting under which the clarity as well as the alignment of Corporate

reporting framework, requirements and the standard drive consistency and comparability that

leads to improve effectiveness and efficiency in practice of corporate

reporting(Integratedreporting.org, 2019). Further, both the organisations identify significance of

the corporate reporting while promoting the sustainable development. IIRC and GRE accepts the

complementarity of respective roles based on that sustainability reporting that is the central part

for integrated reporting G4 of GIR is the crucial starting point that ensure that the strong

sustainability metrics are involved under the integrated reports on the basis of international

Framework where the material is to create value over the time period. Both the organisations are

committed in identifying the approaches for alignment with the objectives of strengthening the

corporate reporting (Integratedreporting.org, 2019). Further, they will continue to

communicating proactively with the market regarding the nature, role and alignment of each

other frameworks standard and guidelines to facilitate understanding as well as clarity in the

11CONTEMPORARY ACCOUNTING THEORY

environment of corporate reporting. Through the continuing collaboration their main objective is

to express possible common voice, wherever possible, regarding relevant aspects of the

respective activities and other associated matters regarding mutual interest.

Under GRI the presentation is segregated into 2 parts as follows –

1st part comprised of the principles for reporting and the standards disclosure

requirements including standardised disclosures, reporting principles and criteria required

for the preparation of the sustainability reporting as per the requirements of the guidelines

2nd part states the manual for implementation including the explanations regarding

application of reporting principles, interpretation of various concepts and preparation of

disclosures for disclosing material information as per the required guidelines (Global Reporting

Initiative, 2019).

On the other hand, the IIRF is used for improving the integrated reporting as per of IIRC.

Its main objective is to establish the guiding principles and content element that governs the

entire substance of the integrated reporting. Further, it explains fundamental concepts required

for strengthening the same (Integratedreporting.org, 2019).

(b) Strengths and limitations of conventional accounting

Conventional accounting system involves traditional method for recording the accounting

information. It covers less detail regarding the transactions and the mathematical accuracy are

not guaranteed. Only 2 books that are the ledger and cash books are prepared under this

approach.

Advantages –

environment of corporate reporting. Through the continuing collaboration their main objective is

to express possible common voice, wherever possible, regarding relevant aspects of the

respective activities and other associated matters regarding mutual interest.

Under GRI the presentation is segregated into 2 parts as follows –

1st part comprised of the principles for reporting and the standards disclosure

requirements including standardised disclosures, reporting principles and criteria required

for the preparation of the sustainability reporting as per the requirements of the guidelines

2nd part states the manual for implementation including the explanations regarding

application of reporting principles, interpretation of various concepts and preparation of

disclosures for disclosing material information as per the required guidelines (Global Reporting

Initiative, 2019).

On the other hand, the IIRF is used for improving the integrated reporting as per of IIRC.

Its main objective is to establish the guiding principles and content element that governs the

entire substance of the integrated reporting. Further, it explains fundamental concepts required

for strengthening the same (Integratedreporting.org, 2019).

(b) Strengths and limitations of conventional accounting

Conventional accounting system involves traditional method for recording the accounting

information. It covers less detail regarding the transactions and the mathematical accuracy are

not guaranteed. Only 2 books that are the ledger and cash books are prepared under this

approach.

Advantages –

12CONTEMPORARY ACCOUNTING THEORY

It can be used on consistent basis over the time period that improves the financial

statements comparability within as well as outside of the organisation

It assists to maintain reliability along with objectivity of accounting information. It

prevents the data manipulation as the transactions are recorded on the objective basis

(Schaltegger & Burritt, 2017)

Conventional accounting concept is simple and easy to use. Further, as the transactions

are reported at the original amount at which the same was acquired restatement in each

accounting period is not necessary.

Disadvantages –

Losses or gains made on account of inventory holding can be associated with the

operating losses and gains that make it difficult to measure the actual operating

performances of the entity as holding losses and gains shall be excluded from operating

income or losses.

Changes in the price level are not taken into consideration which in turn does not reflect

the true value of the entity (Kirkman, 2014)

Fixed assets reported under the financial statement are reported at cost less accumulated

depreciation. It makes difficult for segregating the new assets purchased by the entity or

sold by it.

As the conventional accounting approach does not reflect the actual profit, applicability

of tax becomes difficult. Hence, under the inflationary situation the profits as well as

value of assets are overstated.

It can be used on consistent basis over the time period that improves the financial

statements comparability within as well as outside of the organisation

It assists to maintain reliability along with objectivity of accounting information. It

prevents the data manipulation as the transactions are recorded on the objective basis

(Schaltegger & Burritt, 2017)

Conventional accounting concept is simple and easy to use. Further, as the transactions

are reported at the original amount at which the same was acquired restatement in each

accounting period is not necessary.

Disadvantages –

Losses or gains made on account of inventory holding can be associated with the

operating losses and gains that make it difficult to measure the actual operating

performances of the entity as holding losses and gains shall be excluded from operating

income or losses.

Changes in the price level are not taken into consideration which in turn does not reflect

the true value of the entity (Kirkman, 2014)

Fixed assets reported under the financial statement are reported at cost less accumulated

depreciation. It makes difficult for segregating the new assets purchased by the entity or

sold by it.

As the conventional accounting approach does not reflect the actual profit, applicability

of tax becomes difficult. Hence, under the inflationary situation the profits as well as

value of assets are overstated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CONTEMPORARY ACCOUNTING THEORY

Hence, though the conventional accounting approach plays significant role in overall

welfare of society in accounting context, integrated reporting in association with conventional

accounting will improve the decision making procedures of the stakeholders, investors and other

users of the financial statements.

(c) Theories for explaining the contents of sustainability and integrated reports

Big entities are disclosing the material information on increasing basis regarding their

financial as well as non-financial capitals under the integrated reports. Main objective behind this

is to improve the legitimacy with the stakeholders and institutions as they are required to

communicate regarding all the aspects of the activities those create values, strategic priorities and

business models. As per the research conducted by Cory Searcy, among 20 entities only 5

entities were in practice of developing the fully integrated reports whereas rest 15 are in practice

of incorporating some of the sustainability aspects of in the annual reports (Deegan & Islam,

2012). Major challenges found in incorporating the sustainability reports are collection of data,

selection of content, timing and reporting the items at appropriate amount. It was further found

by the study of Ronel Rensburg, that the only few stakeholders apply the integrated reports as the

major source of investment.

(d) Index of different components of integrated report

Naspers Ltd disclosed the following in its integrated report –

Organizational overview - under this it discussed about the review of the chair and review

of the CEO.

Governance – under this it discussed about the board, governance for sustainable

business and remuneration report

Hence, though the conventional accounting approach plays significant role in overall

welfare of society in accounting context, integrated reporting in association with conventional

accounting will improve the decision making procedures of the stakeholders, investors and other

users of the financial statements.

(c) Theories for explaining the contents of sustainability and integrated reports

Big entities are disclosing the material information on increasing basis regarding their

financial as well as non-financial capitals under the integrated reports. Main objective behind this

is to improve the legitimacy with the stakeholders and institutions as they are required to

communicate regarding all the aspects of the activities those create values, strategic priorities and

business models. As per the research conducted by Cory Searcy, among 20 entities only 5

entities were in practice of developing the fully integrated reports whereas rest 15 are in practice

of incorporating some of the sustainability aspects of in the annual reports (Deegan & Islam,

2012). Major challenges found in incorporating the sustainability reports are collection of data,

selection of content, timing and reporting the items at appropriate amount. It was further found

by the study of Ronel Rensburg, that the only few stakeholders apply the integrated reports as the

major source of investment.

(d) Index of different components of integrated report

Naspers Ltd disclosed the following in its integrated report –

Organizational overview - under this it discussed about the review of the chair and review

of the CEO.

Governance – under this it discussed about the board, governance for sustainable

business and remuneration report

14CONTEMPORARY ACCOUNTING THEORY

Business model – under this it discussed about how they add value and the resources

they require (Naspers.com, 2019).

Managing opportunities and risks – under this it discussed about key risks to the company

and how it manages the risks

Performance – under this it talked about the performance of internet, media, video

entertainment, people and financial review

Basis of preparation - under this it discussed about basis on which the financial

statements are prepared (Naspers.com, 2019).

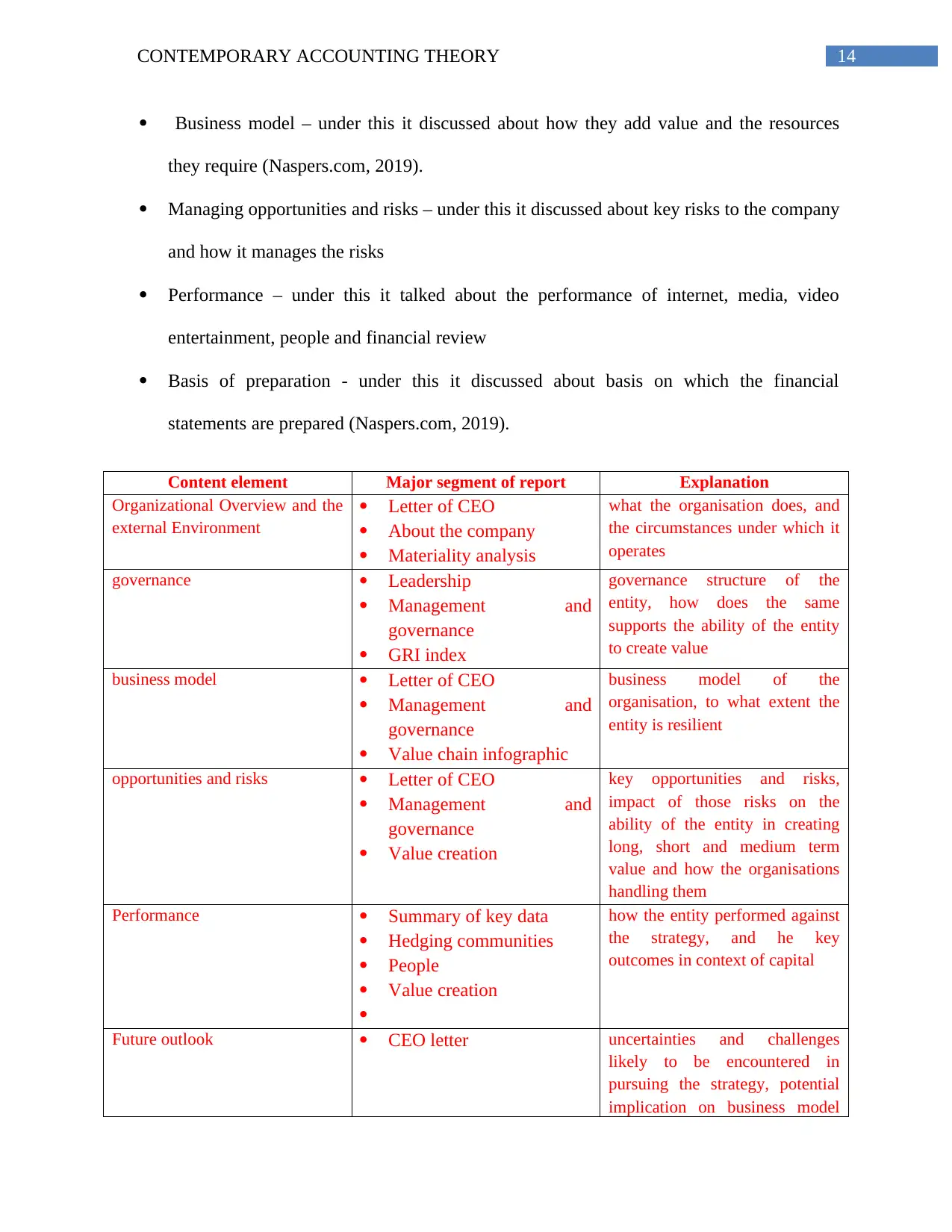

Content element Major segment of report Explanation

Organizational Overview and the

external Environment

Letter of CEO

About the company

Materiality analysis

what the organisation does, and

the circumstances under which it

operates

governance Leadership

Management and

governance

GRI index

governance structure of the

entity, how does the same

supports the ability of the entity

to create value

business model Letter of CEO

Management and

governance

Value chain infographic

business model of the

organisation, to what extent the

entity is resilient

opportunities and risks Letter of CEO

Management and

governance

Value creation

key opportunities and risks,

impact of those risks on the

ability of the entity in creating

long, short and medium term

value and how the organisations

handling them

Performance Summary of key data

Hedging communities

People

Value creation

how the entity performed against

the strategy, and he key

outcomes in context of capital

Future outlook CEO letter uncertainties and challenges

likely to be encountered in

pursuing the strategy, potential

implication on business model

Business model – under this it discussed about how they add value and the resources

they require (Naspers.com, 2019).

Managing opportunities and risks – under this it discussed about key risks to the company

and how it manages the risks

Performance – under this it talked about the performance of internet, media, video

entertainment, people and financial review

Basis of preparation - under this it discussed about basis on which the financial

statements are prepared (Naspers.com, 2019).

Content element Major segment of report Explanation

Organizational Overview and the

external Environment

Letter of CEO

About the company

Materiality analysis

what the organisation does, and

the circumstances under which it

operates

governance Leadership

Management and

governance

GRI index

governance structure of the

entity, how does the same

supports the ability of the entity

to create value

business model Letter of CEO

Management and

governance

Value chain infographic

business model of the

organisation, to what extent the

entity is resilient

opportunities and risks Letter of CEO

Management and

governance

Value creation

key opportunities and risks,

impact of those risks on the

ability of the entity in creating

long, short and medium term

value and how the organisations

handling them

Performance Summary of key data

Hedging communities

People

Value creation

how the entity performed against

the strategy, and he key

outcomes in context of capital

Future outlook CEO letter uncertainties and challenges

likely to be encountered in

pursuing the strategy, potential

implication on business model

15CONTEMPORARY ACCOUNTING THEORY

and future outcomes and

performance

basis of preparation and

presentation

Management and

governance

Value chain infographic

Materiality analysis

how the company determine the

material matters on material

matters regarding KPIs and

characteristics

(e) Integrated report of Iress Ltd

Iress Ltd does not prepare the integrated report rather it prepare the annual report that

includes the following aspects of integrated reporting –

Organizational overview - under this it discussed about the review of the chair and review

of the CEO (Iress.com, 2019).

Governance – under this it discussed about the board, governance for sustainable

business and remuneration report

Managing opportunities and risks – under this it discussed about key risks to the

company and how it manages the risks (Iress.com, 2019).

Performance – under this it talked about the financial performance of

Basis of preparation - under this it discussed about basis on which the financial

statements are prepared.

On the other hand, Naspers Limited’s integrated report provides the details regarding

organizational overview, Governance, Business model, Managing opportunities and risks,

Performance and Basis of preparation (Naspers.com, 2019).

Hence, if both the above mentioned entities are compared it can be stated that the

Australian company does not prepare separate integrated report and includes the same under the

and future outcomes and

performance

basis of preparation and

presentation

Management and

governance

Value chain infographic

Materiality analysis

how the company determine the

material matters on material

matters regarding KPIs and

characteristics

(e) Integrated report of Iress Ltd

Iress Ltd does not prepare the integrated report rather it prepare the annual report that

includes the following aspects of integrated reporting –

Organizational overview - under this it discussed about the review of the chair and review

of the CEO (Iress.com, 2019).

Governance – under this it discussed about the board, governance for sustainable

business and remuneration report

Managing opportunities and risks – under this it discussed about key risks to the

company and how it manages the risks (Iress.com, 2019).

Performance – under this it talked about the financial performance of

Basis of preparation - under this it discussed about basis on which the financial

statements are prepared.

On the other hand, Naspers Limited’s integrated report provides the details regarding

organizational overview, Governance, Business model, Managing opportunities and risks,

Performance and Basis of preparation (Naspers.com, 2019).

Hence, if both the above mentioned entities are compared it can be stated that the

Australian company does not prepare separate integrated report and includes the same under the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16CONTEMPORARY ACCOUNTING THEORY

annual report whereas South African company prepares the same and covers all the aspects.

However, both the companies cover the same aspects under their respective integrated report.

Conclusion

From the above it can be concluded that conceptual framework sets out concept that is

used for shaping presentation and preparation of the financial statements for the purpose of using

it by the external users. It significantly contributes to the academic credibility as well as public

confidence regarding the financial reporting with regard to reliability, relevance and consistency

through employing the uniform as well as clearly defined principles. Further, if the guidelines for

sustainability reporting is considered it can be stated that both IIRC as well as GRI both continue

working together with the alignment of GRI standards and international framework for

improving the corporate reporting.

annual report whereas South African company prepares the same and covers all the aspects.

However, both the companies cover the same aspects under their respective integrated report.

Conclusion

From the above it can be concluded that conceptual framework sets out concept that is

used for shaping presentation and preparation of the financial statements for the purpose of using

it by the external users. It significantly contributes to the academic credibility as well as public

confidence regarding the financial reporting with regard to reliability, relevance and consistency

through employing the uniform as well as clearly defined principles. Further, if the guidelines for

sustainability reporting is considered it can be stated that both IIRC as well as GRI both continue

working together with the alignment of GRI standards and international framework for

improving the corporate reporting.

17CONTEMPORARY ACCOUNTING THEORY

Reference

Aasb.gov.au. (2019). Retrieved 27 May 2019, from https://www.aasb.gov.au/Work-In-

Progress/Submissions-from-AASB.aspx

Botosan, C. (2019). Pathway to an Integrated Conceptual Framework for Financial

Reporting. The Accounting Review, Forthcoming July.

Caroline B. (2019). GRIN - The Conceptual Framework in the United Kingdom and the

Introduction of the Statement of Principles. Grin.com. Retrieved 27 May 2019, from

https://www.grin.com/document/37091

Deegan, C. & Islam, M.A., (2012), ‘Corporate Commitment to Sustainability—Is It All Hot Air?

An Australian Review of the Linkage between Executive Pay and Sustainable

Performance’, Australian Accounting Review, vol. 22, no. 4, pp 384–97.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., ... & Bartuska, A. (2015).

The IPBES Conceptual Framework—connecting nature and people. Current Opinion in

Environmental Sustainability, 14, 1-16.

Eizenberg, E., & Jabareen, Y. (2017). Social sustainability: A new conceptual

framework. Sustainability, 9(1), 68.

Global Reporting Initiative . (2019). Globalreporting.org. Retrieved 27 May 2019, from

https://www.globalreporting.org/Pages/default.aspx

Integratedreporting.org. (2019). Retrieved 27 May 2019, from https://integratedreporting.org/

Iress.com. (2019). Australia. Retrieved 27 May 2019, from https://www.iress.com/au/

Reference

Aasb.gov.au. (2019). Retrieved 27 May 2019, from https://www.aasb.gov.au/Work-In-

Progress/Submissions-from-AASB.aspx

Botosan, C. (2019). Pathway to an Integrated Conceptual Framework for Financial

Reporting. The Accounting Review, Forthcoming July.

Caroline B. (2019). GRIN - The Conceptual Framework in the United Kingdom and the

Introduction of the Statement of Principles. Grin.com. Retrieved 27 May 2019, from

https://www.grin.com/document/37091

Deegan, C. & Islam, M.A., (2012), ‘Corporate Commitment to Sustainability—Is It All Hot Air?

An Australian Review of the Linkage between Executive Pay and Sustainable

Performance’, Australian Accounting Review, vol. 22, no. 4, pp 384–97.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., ... & Bartuska, A. (2015).

The IPBES Conceptual Framework—connecting nature and people. Current Opinion in

Environmental Sustainability, 14, 1-16.

Eizenberg, E., & Jabareen, Y. (2017). Social sustainability: A new conceptual

framework. Sustainability, 9(1), 68.

Global Reporting Initiative . (2019). Globalreporting.org. Retrieved 27 May 2019, from

https://www.globalreporting.org/Pages/default.aspx

Integratedreporting.org. (2019). Retrieved 27 May 2019, from https://integratedreporting.org/

Iress.com. (2019). Australia. Retrieved 27 May 2019, from https://www.iress.com/au/

18CONTEMPORARY ACCOUNTING THEORY

Kirkman, P. (2014). Accounting Under Inflationary Conditions (RLE Accounting). Routledge.

Lewandowski, M. (2016). Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), 43.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136,

237-248.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Morioka, S. N., & de Carvalho, M. M. (2016). A systematic literature review towards a

conceptual framework for integrating sustainability performance into business. Journal of

Cleaner Production, 136, 134-146.

Naspers.com. (2019). Home | Naspers . Retrieved 27 May 2019, from https://www.naspers.com/

Rensburg, R., & Botha, E. (2014). Is Integrated Reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152. doi:10.1016/j.pubrev.2013.11.016

Researchbank.rmit.edu.au. (2019). Retrieved 29 May 2019, from

https://researchbank.rmit.edu.au/eserv/rmit:9813/Myers.pdf

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Kirkman, P. (2014). Accounting Under Inflationary Conditions (RLE Accounting). Routledge.

Lewandowski, M. (2016). Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), 43.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner Production, 136,

237-248.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Morioka, S. N., & de Carvalho, M. M. (2016). A systematic literature review towards a

conceptual framework for integrating sustainability performance into business. Journal of

Cleaner Production, 136, 134-146.

Naspers.com. (2019). Home | Naspers . Retrieved 27 May 2019, from https://www.naspers.com/

Rensburg, R., & Botha, E. (2014). Is Integrated Reporting the silver bullet of financial

communication? A stakeholder perspective from South Africa. Public Relations

Review, 40(2), 144-152. doi:10.1016/j.pubrev.2013.11.016

Researchbank.rmit.edu.au. (2019). Retrieved 29 May 2019, from

https://researchbank.rmit.edu.au/eserv/rmit:9813/Myers.pdf

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19CONTEMPORARY ACCOUNTING THEORY

Searcy, C., &Buslovich, R. (2013). Corporate Perspectives on the Development and Use of

Sustainability Reports. Journal Of Business Ethics, 121(2), 149-169.

doi:10.1007/s10551-013-1701-7

Searcy, C., &Buslovich, R. (2013). Corporate Perspectives on the Development and Use of

Sustainability Reports. Journal Of Business Ethics, 121(2), 149-169.

doi:10.1007/s10551-013-1701-7

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.