Contemporary Accounting Theory

VerifiedAdded on 2023/04/04

|28

|5583

|402

AI Summary

This paper provides a literature review of the history and development of the conceptual framework in financial accounting, focusing on Australia, USA, and UK. It discusses the concerns raised by academics and accounting professionals about the applicability of the framework. It also explores the strengths and limitations of conventional accounting and integrated reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: CONTEMPORARY ACCOUNTING THEORY 1

Contemporary Accounting Theory

Name

Date

Affiliation

Contemporary Accounting Theory

Name

Date

Affiliation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 2

Contemporary Accounting Theory

Executive Summary

This paper comprises of two parts, A and B. Part A provides a literature review about the

history of the conceptual framework in financial accounting and its development in Australia,

USA and UK. According to researchers, accounting standards settles were operating without a

conceptual framework. There were therefore several scandals in financial accounting and the

entire system was disorganized. However, the introduction of the conceptual framework in 1989

resulted into establishment of a one set of accounting standards that govern the operations of the

accounting sector. The financial accounting field even further improved as the conceptual

framework was revised in 2001. As a result, there have been several concerns raised by both

academics and accounting professionals about the applicability of the framework. Part B of the

report discusses sustainability and integrated reporting and the strengths as well as limitations of

conventional accounting. According to the integrated report presented by Discovery Limited, the

company disclosed all the information of the elements of an integrated report. Both companies

have several things in common including the way they present their financial positions.

However, AUB Group Limited comprises of an interactive annual report whereas Discovery

Limited comprises of an integrated report.

Introduction

Conceptual framework is one of the most important systems in accounting which

comprises of fundamentals and inter-related objectives that facilitate issuing of consistent

standards which describe nature and control preparation and presentation of financial statements

as well financial accounting as a whole (IFRS Foundation,2017). The framework plays a vital

Contemporary Accounting Theory

Executive Summary

This paper comprises of two parts, A and B. Part A provides a literature review about the

history of the conceptual framework in financial accounting and its development in Australia,

USA and UK. According to researchers, accounting standards settles were operating without a

conceptual framework. There were therefore several scandals in financial accounting and the

entire system was disorganized. However, the introduction of the conceptual framework in 1989

resulted into establishment of a one set of accounting standards that govern the operations of the

accounting sector. The financial accounting field even further improved as the conceptual

framework was revised in 2001. As a result, there have been several concerns raised by both

academics and accounting professionals about the applicability of the framework. Part B of the

report discusses sustainability and integrated reporting and the strengths as well as limitations of

conventional accounting. According to the integrated report presented by Discovery Limited, the

company disclosed all the information of the elements of an integrated report. Both companies

have several things in common including the way they present their financial positions.

However, AUB Group Limited comprises of an interactive annual report whereas Discovery

Limited comprises of an integrated report.

Introduction

Conceptual framework is one of the most important systems in accounting which

comprises of fundamentals and inter-related objectives that facilitate issuing of consistent

standards which describe nature and control preparation and presentation of financial statements

as well financial accounting as a whole (IFRS Foundation,2017). The framework plays a vital

CONTEMPORARY ACCOUNTING THEORY 3

role in financial accounting as it lays foundation for better understanding and evaluation of

accounting information. Following the important role played by this system, it is currently

adopted by multiple countries in the world. This paper provides research about the numerous

corporate external reporting aspects. It reviews the available literature about the history and

advancement of the conceptual framework, the concerns raised by the accounting professionals,

as well as the concerns of academics about its application. The report is to be presented in two

parts, A and B. Part A provides literature about the conceptual framework and its applicability in

AUB Group Limited, an Australian company. Part B discusses sustainability and integrated

reporting and its applicability in Discovery Limited, a South African company (IFRS

Foundation,2017).

Part A: Conceptual Framework

A ) Literature review of the history and development of the Conceptual Framework for

Financial Reporting

Conceptual framework is a system of objectives and ideas that facilitates the creation of

standards and rules. In Financial accounting, a conceptual framework is mainly developed to

provide a framework for setting the foundation of solving accounting disputes, accounting

standards and fundamental principles (Dennis, 2018). Conceptual framework is a very important

system in accounting as it helps in providing a better understanding of financial reports. Very

many years back, setters of accounting standards were operating without a conceptual

framework. As a result, scandals were the order of the day and accounting standards were

disorganized (Sori, 2017).

role in financial accounting as it lays foundation for better understanding and evaluation of

accounting information. Following the important role played by this system, it is currently

adopted by multiple countries in the world. This paper provides research about the numerous

corporate external reporting aspects. It reviews the available literature about the history and

advancement of the conceptual framework, the concerns raised by the accounting professionals,

as well as the concerns of academics about its application. The report is to be presented in two

parts, A and B. Part A provides literature about the conceptual framework and its applicability in

AUB Group Limited, an Australian company. Part B discusses sustainability and integrated

reporting and its applicability in Discovery Limited, a South African company (IFRS

Foundation,2017).

Part A: Conceptual Framework

A ) Literature review of the history and development of the Conceptual Framework for

Financial Reporting

Conceptual framework is a system of objectives and ideas that facilitates the creation of

standards and rules. In Financial accounting, a conceptual framework is mainly developed to

provide a framework for setting the foundation of solving accounting disputes, accounting

standards and fundamental principles (Dennis, 2018). Conceptual framework is a very important

system in accounting as it helps in providing a better understanding of financial reports. Very

many years back, setters of accounting standards were operating without a conceptual

framework. As a result, scandals were the order of the day and accounting standards were

disorganized (Sori, 2017).

CONTEMPORARY ACCOUNTING THEORY 4

Additionally, the absence of the conceptual framework increased inconsistence in the

accounting standards and the overall purpose of preparing and presenting financial statements.

The International Accounting Standards Committee (IASC) in 1989 (Silva, 2018), issued

conceptual framework. Since then, it had been left unchanged until the International Accounting

Standards Board in 2001, an organization that replaced IASC, adopted it. IASB is an

independent organization whose main goal is to establish a single set of accounting standards

that govern all international companies across the globe. The organization deals in capital and

capital maintenance concepts, the objectives of preparing and presenting financial statements,

qualitative traits which determine how important the information in financial statements is, and

defining as well as measuring the elements which provide a basis for constructing financial

statements (Sori, 2017).

In U.K, conceptual framework was developed by the nation in 1999. It was referred to as

the Statement of Principles and was approved by the Accounting Standards Board. Following the

several gains such as globalization, which were realized by U.S after adoption of its conceptual

framework, United Kingdom also aimed at decreasing any form of prospects of staying behind as

far as accounting is concerned through developing its own conceptual framework, (Becker,

2010). Considering the above, there exists consistence between the Statement of Principles and

the statements of the conceptual framework, which were issued by several nations including

United States and New Zealand (Carrahera and Auken, 2013). The Financial statements elements

were the foundation for the development of the Statement of principles in U.K. These included

ownership interest, losses and gains, assets and liabilities. These principles are applied to the

financial statements which are included in the constitution of the interim reports and initial

announcements of the listed companies in U.K (Becker, 2010).

Additionally, the absence of the conceptual framework increased inconsistence in the

accounting standards and the overall purpose of preparing and presenting financial statements.

The International Accounting Standards Committee (IASC) in 1989 (Silva, 2018), issued

conceptual framework. Since then, it had been left unchanged until the International Accounting

Standards Board in 2001, an organization that replaced IASC, adopted it. IASB is an

independent organization whose main goal is to establish a single set of accounting standards

that govern all international companies across the globe. The organization deals in capital and

capital maintenance concepts, the objectives of preparing and presenting financial statements,

qualitative traits which determine how important the information in financial statements is, and

defining as well as measuring the elements which provide a basis for constructing financial

statements (Sori, 2017).

In U.K, conceptual framework was developed by the nation in 1999. It was referred to as

the Statement of Principles and was approved by the Accounting Standards Board. Following the

several gains such as globalization, which were realized by U.S after adoption of its conceptual

framework, United Kingdom also aimed at decreasing any form of prospects of staying behind as

far as accounting is concerned through developing its own conceptual framework, (Becker,

2010). Considering the above, there exists consistence between the Statement of Principles and

the statements of the conceptual framework, which were issued by several nations including

United States and New Zealand (Carrahera and Auken, 2013). The Financial statements elements

were the foundation for the development of the Statement of principles in U.K. These included

ownership interest, losses and gains, assets and liabilities. These principles are applied to the

financial statements which are included in the constitution of the interim reports and initial

announcements of the listed companies in U.K (Becker, 2010).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 5

In Australia, the conceptual framework was initially observed as a package that consisted

of several concepts of accounting statements. These statements provided the definition of

subject, purpose and nature of the significance of financial reporting in both private and public

companies (Carrahera and Auken, 2013). In 2004, the Australian Accounting Standards

Board(AASB) developed the conceptual framework for financial reporting. The framework was

then implemented in 2005 and it served the purpose of improving and regulating accounting

practices and financial reporting of all public companies in the country. The main aim of the

framework was to assists financial statement users and auditors to interpret and form opinions on

the financial information contained in the financial statements as per the AASB (Carrahera and

Auken, 2013).

Globally, the conceptual framework was first introduced in 1989. It was authorized by

Inter-Agency Standing Committee (IASC) and was initially adopted by IASB in 2005.The

accounting standards that were established by IASC are currently still in use and are referred to

as the International Accounting Standards(IAS) (Daske et al, 2013). On the other side standards

developed by IASB are referred to as International Financial Reporting standards. In 2004, the

conceptual framework was reviewed and revised by the Financial Accounting Standards Board

(FASB) and IASB. However, slow progress and change in the priorities resulted into abandoning

of the project after 6 years when only the first phase (Phase A) of the project was finalized

(Flower, 2015). Phase D was not finalized even after viewing the exposure draft and discussion

paper publication. Phases B and C were extensively discussed by the board without issuing any

consultation document. Other phases were never touched. In March 2018, the revised version of

the conceptual framework was issued which effective for companies which apply the conceptual

framework to establish accounting policies especially when there is no IFRS standard that

In Australia, the conceptual framework was initially observed as a package that consisted

of several concepts of accounting statements. These statements provided the definition of

subject, purpose and nature of the significance of financial reporting in both private and public

companies (Carrahera and Auken, 2013). In 2004, the Australian Accounting Standards

Board(AASB) developed the conceptual framework for financial reporting. The framework was

then implemented in 2005 and it served the purpose of improving and regulating accounting

practices and financial reporting of all public companies in the country. The main aim of the

framework was to assists financial statement users and auditors to interpret and form opinions on

the financial information contained in the financial statements as per the AASB (Carrahera and

Auken, 2013).

Globally, the conceptual framework was first introduced in 1989. It was authorized by

Inter-Agency Standing Committee (IASC) and was initially adopted by IASB in 2005.The

accounting standards that were established by IASC are currently still in use and are referred to

as the International Accounting Standards(IAS) (Daske et al, 2013). On the other side standards

developed by IASB are referred to as International Financial Reporting standards. In 2004, the

conceptual framework was reviewed and revised by the Financial Accounting Standards Board

(FASB) and IASB. However, slow progress and change in the priorities resulted into abandoning

of the project after 6 years when only the first phase (Phase A) of the project was finalized

(Flower, 2015). Phase D was not finalized even after viewing the exposure draft and discussion

paper publication. Phases B and C were extensively discussed by the board without issuing any

consultation document. Other phases were never touched. In March 2018, the revised version of

the conceptual framework was issued which effective for companies which apply the conceptual

framework to establish accounting policies especially when there is no IFRS standard that

CONTEMPORARY ACCOUNTING THEORY 6

applies to a given transaction. The new version of the conceptual framework will only be applied

for annual reporting periods starting from 1st January 2020. The revised version of the conceptual

framework comprises of significant concepts of financial reporting that provide guidance to

IASB while establishing IFRS standards (Armstrong, 2013). It plays a vital role in ensuring that

all similar transactions are handled in the same way and consistence in the set standards. This

helps to give important information to lenders, investors and other creditors. Additionally, the

new version of the conceptual framework also helps companies in formulating accounting

policies when there exists no IFRS standard relevant to a particular transaction and more

importantly, it assists stakeholders to interpret standards. IASB issued an accompanying

document " Amendments to References" to help companies to clearly understand the transition

(Daske et al, 2013).

B) Discussion of the Australian accounting profession`s concerns on the application of the

Conceptual Framework

The Australian accounting profession is specifically concerned with the multiple political

interferences which have been expressed about the implementation of the conceptual framework

of financial reporting. A significant number of professions are taking part in debates about the

generation and implementation of the elements of the financial statements since conceptual

framework entails formulation of ideas and objectives (Armstrong, 2013). On several occasions,

the stage of decision making is the one most interfered by politics especially among members of

the board. Some great ideas are sometimes ignored because of the selfish interests of the IASB

members. This is evident specifically when the frame work is applied to resolve issues associated

with several disagreements among board members (Humayun and Asheq, 2018). Due to the

rapidly changing economic conditions in different parts of the world, IFRS members may also

applies to a given transaction. The new version of the conceptual framework will only be applied

for annual reporting periods starting from 1st January 2020. The revised version of the conceptual

framework comprises of significant concepts of financial reporting that provide guidance to

IASB while establishing IFRS standards (Armstrong, 2013). It plays a vital role in ensuring that

all similar transactions are handled in the same way and consistence in the set standards. This

helps to give important information to lenders, investors and other creditors. Additionally, the

new version of the conceptual framework also helps companies in formulating accounting

policies when there exists no IFRS standard relevant to a particular transaction and more

importantly, it assists stakeholders to interpret standards. IASB issued an accompanying

document " Amendments to References" to help companies to clearly understand the transition

(Daske et al, 2013).

B) Discussion of the Australian accounting profession`s concerns on the application of the

Conceptual Framework

The Australian accounting profession is specifically concerned with the multiple political

interferences which have been expressed about the implementation of the conceptual framework

of financial reporting. A significant number of professions are taking part in debates about the

generation and implementation of the elements of the financial statements since conceptual

framework entails formulation of ideas and objectives (Armstrong, 2013). On several occasions,

the stage of decision making is the one most interfered by politics especially among members of

the board. Some great ideas are sometimes ignored because of the selfish interests of the IASB

members. This is evident specifically when the frame work is applied to resolve issues associated

with several disagreements among board members (Humayun and Asheq, 2018). Due to the

rapidly changing economic conditions in different parts of the world, IFRS members may also

CONTEMPORARY ACCOUNTING THEORY 7

fail to develop a similar solution towards the measurement of assets. More so, members may

raise different views on both the present and historical costs of assets due to their political

interests (Flower, 2015).

Over the past years, there have been several concerns that have been raised by the

accounting professionals in Australia about the application of the conceptual framework.

According to Wayne Lonergan, a professor of Business and Economics in the University of

Sydney, adoption of international accounting standards by Australia has significant outcomes for

the Australian economy as whole (Humayun and Asheq, 2018). Primarily, the process of setting

accounting standards in Australia was weakened by the policy of adopting the international

accounting standards. The introduction of this system did not only emasculate the setting process

of accounting standards in Australia but also weakened Australia`s setting capacity of accounting

standards and its position as the foundation for accounting excellence. Professionals explain that

less quality financial reports are produced by Australian companies as a result of the adoption of

IAS (Gordon et al, 2015). According to some of the accounting professionals in Australia, the

adoption of IAS created financial stability in corporate government. Currently, most of the

efforts employed by the corporate government are focused on ensuring increase in independence,

disclosure and practice of best guidelines which entail disclosure of failure to comply with the

required standards of annual reports. The major objective of the corporate government is to

develop a culture of trust and integrity between stakeholders and relevant parties such as fund

managers, company directors, auditors and other shareholders. The current reforms are mainly

focusing on making right the symptoms instead of finding solutions for the root causes of the

problems. The back bone of financial reporting are the accounting standards. In Australia, the

regime of financial reporting still has significant deficiencies and limitations. Recently, it was

fail to develop a similar solution towards the measurement of assets. More so, members may

raise different views on both the present and historical costs of assets due to their political

interests (Flower, 2015).

Over the past years, there have been several concerns that have been raised by the

accounting professionals in Australia about the application of the conceptual framework.

According to Wayne Lonergan, a professor of Business and Economics in the University of

Sydney, adoption of international accounting standards by Australia has significant outcomes for

the Australian economy as whole (Humayun and Asheq, 2018). Primarily, the process of setting

accounting standards in Australia was weakened by the policy of adopting the international

accounting standards. The introduction of this system did not only emasculate the setting process

of accounting standards in Australia but also weakened Australia`s setting capacity of accounting

standards and its position as the foundation for accounting excellence. Professionals explain that

less quality financial reports are produced by Australian companies as a result of the adoption of

IAS (Gordon et al, 2015). According to some of the accounting professionals in Australia, the

adoption of IAS created financial stability in corporate government. Currently, most of the

efforts employed by the corporate government are focused on ensuring increase in independence,

disclosure and practice of best guidelines which entail disclosure of failure to comply with the

required standards of annual reports. The major objective of the corporate government is to

develop a culture of trust and integrity between stakeholders and relevant parties such as fund

managers, company directors, auditors and other shareholders. The current reforms are mainly

focusing on making right the symptoms instead of finding solutions for the root causes of the

problems. The back bone of financial reporting are the accounting standards. In Australia, the

regime of financial reporting still has significant deficiencies and limitations. Recently, it was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

recognized as one of the most powerful financial reporting regimes in the entire world. It is one

of the remarkable achievements Australia has ever got despite the fact that the country comprises

of a small economy size and capital markets as compared to the economies of UK, US, Asia and

Europe. The Australian Accounting Standards Board (AASB) was initially responsible for

issuing and preparing of accounting standards to both the public and private sector (Humayun

and Asheq, 2018). However, complying with the accounting standards set by AASB was

mandatory according to the Corporations act. Although, there were few financial resources

provided by the Federal government and the accounting bodies, the setting process of accounting

standards was operating independently. The main objective of the former system was to improve

quality of auditing and financial reporting in Australia for both the end users and the preparing

organizations. The former system managed to develop a globally recognized core of excellence

in financial reporting. Adopting of International accounting standards overshadowed the policies

of AASB despite the fact that the organization also had its own priorities. AASB was made

irrelevant especially for the private sector since accounting standards were no longer issued by

the AASB but instead issued by IASB hence eliminating the need for AASB (Gordon et al,

2015).

C) Explanation of the academics` concerns regarding the benefits and limitations of the

Conceptual Framework

The conceptual framework provides concepts, which are developed in an orderly manner

that make reporting and financial accounting logical and consistent. Through the created

consistency, the framework increases compatibility of the standards both nationally and

internationally (Al-Dmour, 2018). Conceptual framework also facilitates development of the

accounting department as a whole and enhances communication. Development of accounting

recognized as one of the most powerful financial reporting regimes in the entire world. It is one

of the remarkable achievements Australia has ever got despite the fact that the country comprises

of a small economy size and capital markets as compared to the economies of UK, US, Asia and

Europe. The Australian Accounting Standards Board (AASB) was initially responsible for

issuing and preparing of accounting standards to both the public and private sector (Humayun

and Asheq, 2018). However, complying with the accounting standards set by AASB was

mandatory according to the Corporations act. Although, there were few financial resources

provided by the Federal government and the accounting bodies, the setting process of accounting

standards was operating independently. The main objective of the former system was to improve

quality of auditing and financial reporting in Australia for both the end users and the preparing

organizations. The former system managed to develop a globally recognized core of excellence

in financial reporting. Adopting of International accounting standards overshadowed the policies

of AASB despite the fact that the organization also had its own priorities. AASB was made

irrelevant especially for the private sector since accounting standards were no longer issued by

the AASB but instead issued by IASB hence eliminating the need for AASB (Gordon et al,

2015).

C) Explanation of the academics` concerns regarding the benefits and limitations of the

Conceptual Framework

The conceptual framework provides concepts, which are developed in an orderly manner

that make reporting and financial accounting logical and consistent. Through the created

consistency, the framework increases compatibility of the standards both nationally and

internationally (Al-Dmour, 2018). Conceptual framework also facilitates development of the

accounting department as a whole and enhances communication. Development of accounting

CONTEMPORARY ACCOUNTING THEORY 9

standards with the help of the conceptual framework is more economical and is made easier. This

is because the basic principles have already been established (Adams, 2015). The already

debated principles can even be applied in situations, which do not have any accounting standards

relevant to them and where there are conflicts of interests on the principles and policies to apply

in particular situations. Additionally, the already established policies, which are obtained from

the conceptual framework, are less criticized. Without development of the conceptual

framework, the organizations setting the standards were most likely to make decisions basing on

the demand of the companies, which would result into issuing of ambiguous and haphazard rules.

However, with the presence of a conceptual framework, the reason behind the establishment of

specific standards is clarified and the standard setters are made accountable to financial

statement users. Generally, the conceptual framework has significantly contributed to public

confidence and credibility of financial reporting with relevance, consistence and reliability

through the use of distinctly defined principles (Adams, 2017). However, the conceptual

framework greatly relies on assumptions, which makes it of less help while preparing financial

statements. As a result, the accounting standards developed are very theoretical, academic and

can easily be exposed to fraud. Practically, these standards make financial information more

complex for users and preparers of the financial reports. Although concepts may be refined and

pure, the difficulty and complexity in understanding the importance of the financial statements

may render the conceptual framework irrelevant. In addition, the framework does not cater for

the interest on information, which facilitates stewardship management assessment. More

criticisms are raised about the emphasis of accounting principles on only economic transactions

and phenomena. There are also diverse user requirements and there may as well be need for

other standards which the conceptual framework cannot cover (Al-Dmour,2018).

standards with the help of the conceptual framework is more economical and is made easier. This

is because the basic principles have already been established (Adams, 2015). The already

debated principles can even be applied in situations, which do not have any accounting standards

relevant to them and where there are conflicts of interests on the principles and policies to apply

in particular situations. Additionally, the already established policies, which are obtained from

the conceptual framework, are less criticized. Without development of the conceptual

framework, the organizations setting the standards were most likely to make decisions basing on

the demand of the companies, which would result into issuing of ambiguous and haphazard rules.

However, with the presence of a conceptual framework, the reason behind the establishment of

specific standards is clarified and the standard setters are made accountable to financial

statement users. Generally, the conceptual framework has significantly contributed to public

confidence and credibility of financial reporting with relevance, consistence and reliability

through the use of distinctly defined principles (Adams, 2017). However, the conceptual

framework greatly relies on assumptions, which makes it of less help while preparing financial

statements. As a result, the accounting standards developed are very theoretical, academic and

can easily be exposed to fraud. Practically, these standards make financial information more

complex for users and preparers of the financial reports. Although concepts may be refined and

pure, the difficulty and complexity in understanding the importance of the financial statements

may render the conceptual framework irrelevant. In addition, the framework does not cater for

the interest on information, which facilitates stewardship management assessment. More

criticisms are raised about the emphasis of accounting principles on only economic transactions

and phenomena. There are also diverse user requirements and there may as well be need for

other standards which the conceptual framework cannot cover (Al-Dmour,2018).

CONTEMPORARY ACCOUNTING THEORY 10

D) Explanation of the applicability of the conceptual framework by AUB Group Limited

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components?

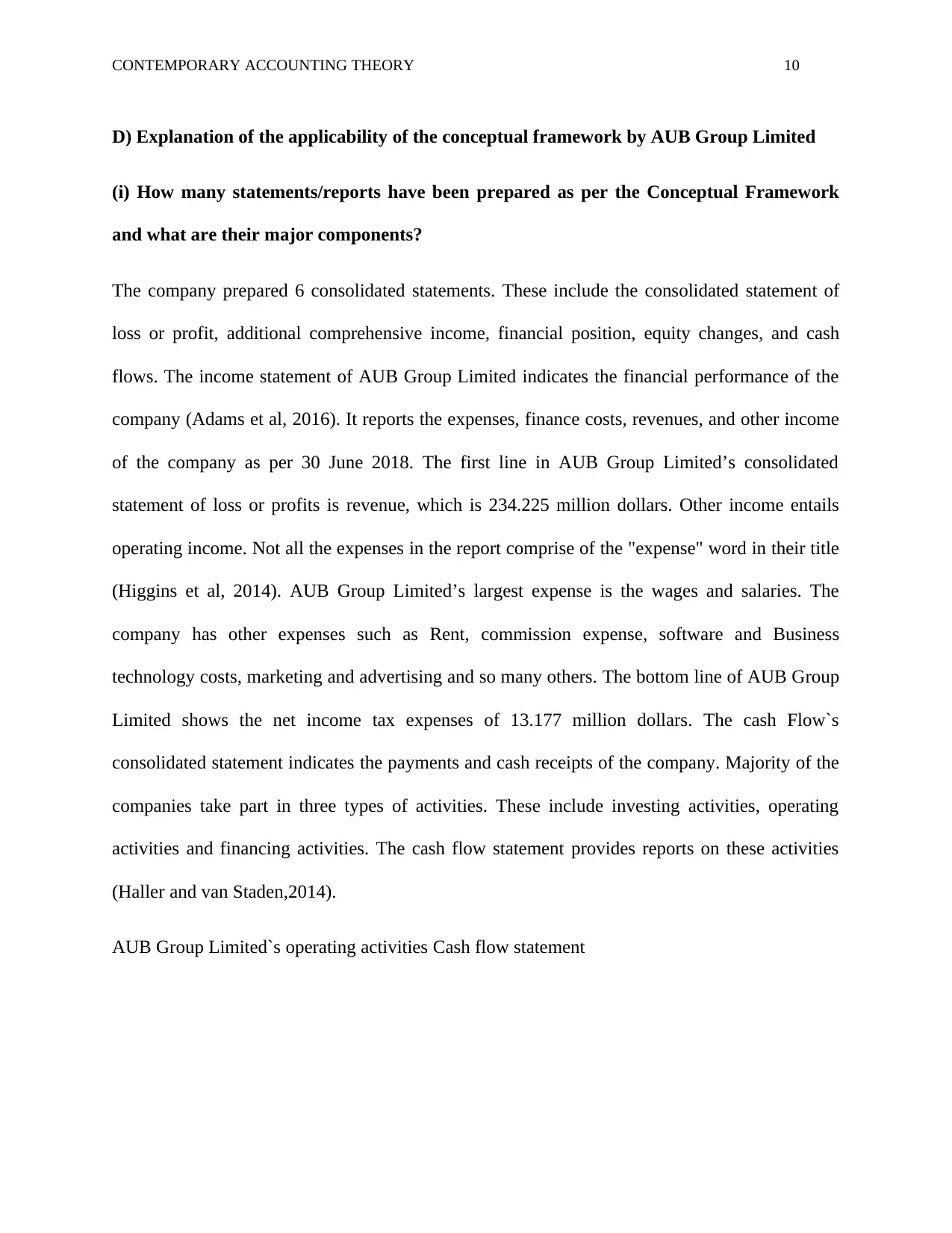

The company prepared 6 consolidated statements. These include the consolidated statement of

loss or profit, additional comprehensive income, financial position, equity changes, and cash

flows. The income statement of AUB Group Limited indicates the financial performance of the

company (Adams et al, 2016). It reports the expenses, finance costs, revenues, and other income

of the company as per 30 June 2018. The first line in AUB Group Limited’s consolidated

statement of loss or profits is revenue, which is 234.225 million dollars. Other income entails

operating income. Not all the expenses in the report comprise of the "expense" word in their title

(Higgins et al, 2014). AUB Group Limited’s largest expense is the wages and salaries. The

company has other expenses such as Rent, commission expense, software and Business

technology costs, marketing and advertising and so many others. The bottom line of AUB Group

Limited shows the net income tax expenses of 13.177 million dollars. The cash Flow`s

consolidated statement indicates the payments and cash receipts of the company. Majority of the

companies take part in three types of activities. These include investing activities, operating

activities and financing activities. The cash flow statement provides reports on these activities

(Haller and van Staden,2014).

AUB Group Limited`s operating activities Cash flow statement

D) Explanation of the applicability of the conceptual framework by AUB Group Limited

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components?

The company prepared 6 consolidated statements. These include the consolidated statement of

loss or profit, additional comprehensive income, financial position, equity changes, and cash

flows. The income statement of AUB Group Limited indicates the financial performance of the

company (Adams et al, 2016). It reports the expenses, finance costs, revenues, and other income

of the company as per 30 June 2018. The first line in AUB Group Limited’s consolidated

statement of loss or profits is revenue, which is 234.225 million dollars. Other income entails

operating income. Not all the expenses in the report comprise of the "expense" word in their title

(Higgins et al, 2014). AUB Group Limited’s largest expense is the wages and salaries. The

company has other expenses such as Rent, commission expense, software and Business

technology costs, marketing and advertising and so many others. The bottom line of AUB Group

Limited shows the net income tax expenses of 13.177 million dollars. The cash Flow`s

consolidated statement indicates the payments and cash receipts of the company. Majority of the

companies take part in three types of activities. These include investing activities, operating

activities and financing activities. The cash flow statement provides reports on these activities

(Haller and van Staden,2014).

AUB Group Limited`s operating activities Cash flow statement

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 11

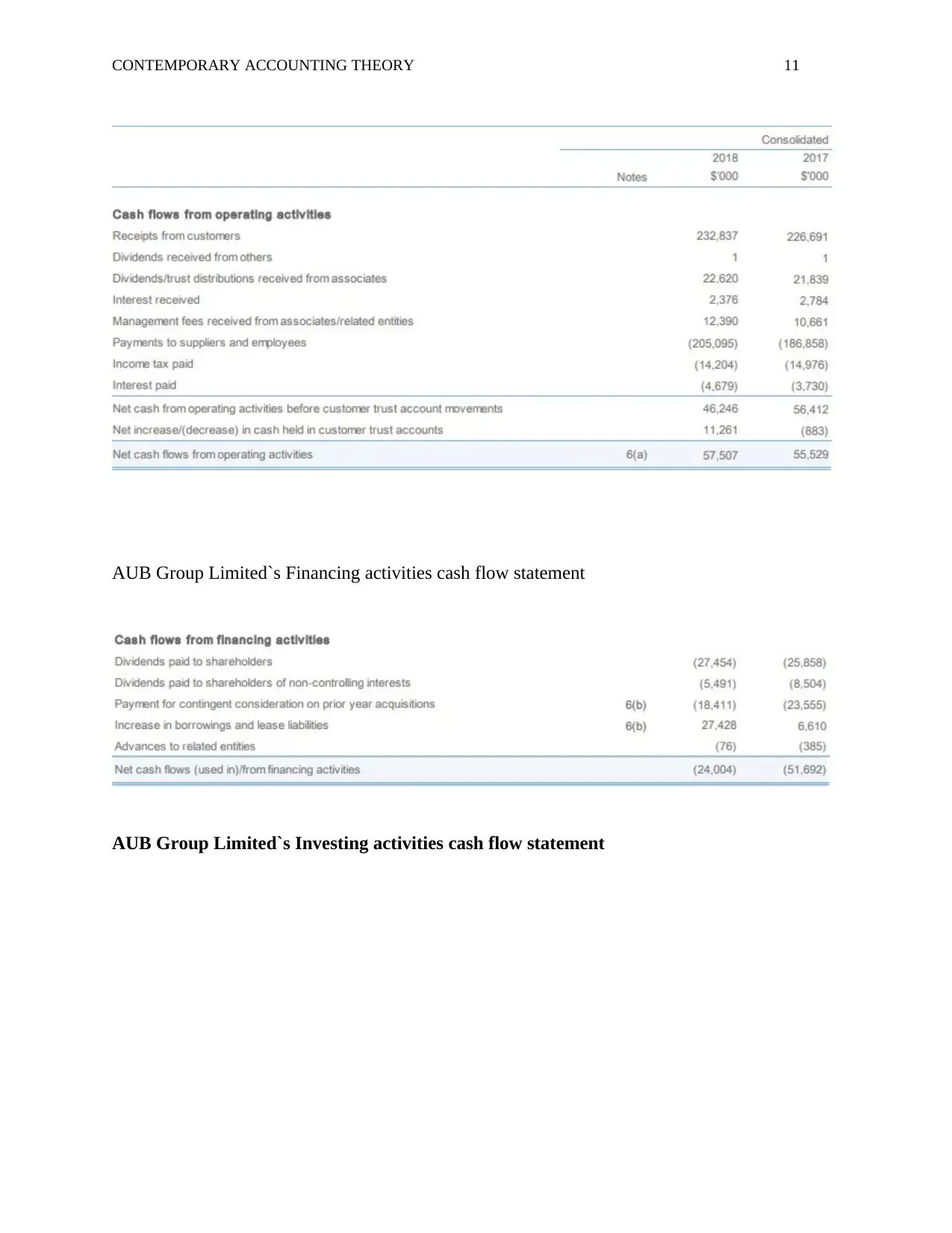

AUB Group Limited`s Financing activities cash flow statement

AUB Group Limited`s Investing activities cash flow statement

AUB Group Limited`s Financing activities cash flow statement

AUB Group Limited`s Investing activities cash flow statement

CONTEMPORARY ACCOUNTING THEORY 12

The Equity changes` consolidated statement indicates the transactions of AUB Limited with its

owners. The profits that are generated by the company are taken up by the company owners. It is

usually after the company obtains its net income that the board of directors make decisions on

whether to give dividends to its stakeholders or not, (Haji and Hossain,2016)

The Equity changes` consolidated statement indicates the transactions of AUB Limited with its

owners. The profits that are generated by the company are taken up by the company owners. It is

usually after the company obtains its net income that the board of directors make decisions on

whether to give dividends to its stakeholders or not, (Haji and Hossain,2016)

CONTEMPORARY ACCOUNTING THEORY 13

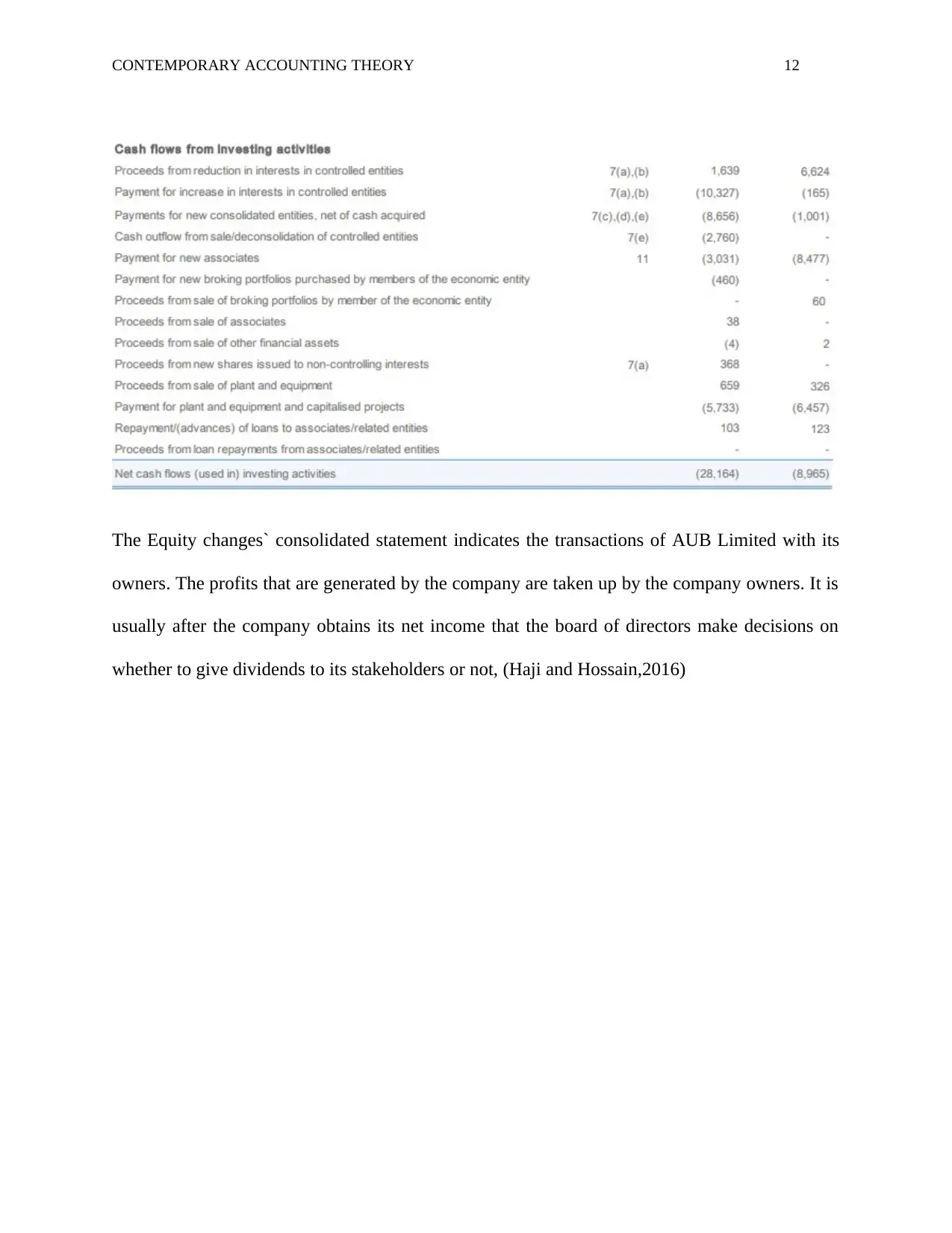

Equity changes` consolidated statement

The financial position of AUB Group limited is indicated in its financial position consolidated

statement. This statement reported three categories of items. These include assets, liabilities and

equity.

Equity changes` consolidated statement

The financial position of AUB Group limited is indicated in its financial position consolidated

statement. This statement reported three categories of items. These include assets, liabilities and

equity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 14

Assets are categorized into two groups, that is to say current and non-current. Current assets

include cash and its equivalents, trade and other financial assets. Non-current assets include

Assets are categorized into two groups, that is to say current and non-current. Current assets

include cash and its equivalents, trade and other financial assets. Non-current assets include

CONTEMPORARY ACCOUNTING THEORY 15

property, equipment and plant, good will and intangible assets and so many others. Liabilities are

also divided into two categories, that is to say current and non-current liabilities. Equity included

retained earnings, issued capital and others (Haji and Anifowose,2016)

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets, and liabilities?

The measurement bases used in the conceptual framework include historical and current

costs. Under the historical cost, the company recorded its liabilities at the proceeds amount

received, (AUB Group Limited, 2018). The income taxes were also considered under this aspect

to come up with a clearer report. For the current cost measurement, the company considered the

cash amount equal to the one that has to be paid in real time to purchase a similar asset currently.

The respective amounts were considered undiscounted (AUB Group Limited, 2018).

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

The features exhibited in the AUB financial reports include reliability, comparability, and

understandability.

Reliability: The financial reports of any given company have to be represented faithfully and

must contain relevant data. this helps the decision makers to come up with informed decisions

regarding the company planning process. in this case, the company clearly exhibited the feature.

its financial reports have clear and relevant information (AUB Group Limited, 2018).

Understandability: This feature targets the managers responsible for making decisions in the

company. Regardless of the professional qualification of the managers, the reports should be

property, equipment and plant, good will and intangible assets and so many others. Liabilities are

also divided into two categories, that is to say current and non-current liabilities. Equity included

retained earnings, issued capital and others (Haji and Anifowose,2016)

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets, and liabilities?

The measurement bases used in the conceptual framework include historical and current

costs. Under the historical cost, the company recorded its liabilities at the proceeds amount

received, (AUB Group Limited, 2018). The income taxes were also considered under this aspect

to come up with a clearer report. For the current cost measurement, the company considered the

cash amount equal to the one that has to be paid in real time to purchase a similar asset currently.

The respective amounts were considered undiscounted (AUB Group Limited, 2018).

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

The features exhibited in the AUB financial reports include reliability, comparability, and

understandability.

Reliability: The financial reports of any given company have to be represented faithfully and

must contain relevant data. this helps the decision makers to come up with informed decisions

regarding the company planning process. in this case, the company clearly exhibited the feature.

its financial reports have clear and relevant information (AUB Group Limited, 2018).

Understandability: This feature targets the managers responsible for making decisions in the

company. Regardless of the professional qualification of the managers, the reports should be

CONTEMPORARY ACCOUNTING THEORY 16

presented in an easily understand form to cover all key decision makers. For AUB, this feature

was fulfilled (AUB Group Limited, 2018).

Comparability: The criterion in which a given company presents its financial reports determines

the extent to which the reports can be compared with another firm. For AUB Group Company,

the reports were presented in a format that can easily be compared with other firms (AUB Group

Limited, 2018).

Part B: Integrated/sustainability reporting

A) Comparing Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Global Reporting Initiative (GRI) is a non-profit organization that mainly focuses on

facilitating use of sustainability reporting by different companies to add something on the

sustainable economy and as well attain their own sustainability. International Integrated

Reporting Council (IIRC) is a committee, which was formed to formulate a framework

which is acceptable by all companies around the world for processes that encourages

companies to communicate the means through which they create value after a given time.

Similarities

Both IIR and sustainability reporting guidelines focus on the strategies used by

the organization to ensure value creation and sustainability in the short and long run

(Eccles and Krzus, 2010). Additionally, GRI and IIRC provide several options of

reporting in order to express the highest levels of transparency. GRI is positioned in a

very strategic and unique place which makes it easy for the organization to provide

effective alignment between different frameworks. According to the KPMG survey

presented in an easily understand form to cover all key decision makers. For AUB, this feature

was fulfilled (AUB Group Limited, 2018).

Comparability: The criterion in which a given company presents its financial reports determines

the extent to which the reports can be compared with another firm. For AUB Group Company,

the reports were presented in a format that can easily be compared with other firms (AUB Group

Limited, 2018).

Part B: Integrated/sustainability reporting

A) Comparing Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Global Reporting Initiative (GRI) is a non-profit organization that mainly focuses on

facilitating use of sustainability reporting by different companies to add something on the

sustainable economy and as well attain their own sustainability. International Integrated

Reporting Council (IIRC) is a committee, which was formed to formulate a framework

which is acceptable by all companies around the world for processes that encourages

companies to communicate the means through which they create value after a given time.

Similarities

Both IIR and sustainability reporting guidelines focus on the strategies used by

the organization to ensure value creation and sustainability in the short and long run

(Eccles and Krzus, 2010). Additionally, GRI and IIRC provide several options of

reporting in order to express the highest levels of transparency. GRI is positioned in a

very strategic and unique place which makes it easy for the organization to provide

effective alignment between different frameworks. According to the KPMG survey

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 17

carried out in 2017 about reporting on corporate social responsibility, 63% of the N100

and 75% of the G250 report using the framework of Global Reporting Initiative. The

sustainability reporting guidelines and the IIRC standards are established for different

purposes (Ahmed et al, 2016). However, these purposes are contemporary.

Differences

GRI observes the impact of the company on the world as a whole whereas as

IIRC observes the impacts of the world on the company, (Barth et al, 2017). The

framework of International Integrated Reporting provides a clear and concise template

which should be used by companies to report the ways through which they sustain the

activities they carry out especially during times when the rate of population growth is

drawing tight the reserves of nature. There is a strong belief that the two frameworks can

work jointly to provide companies as well as their stakeholders with a wider view of how

shareholder value can be created by businesses and how companies can achieve

sustainable development (ldowu et al, 2016). Additionally, GRI also mainly focuses on

the impact of the company on the economy, society and environment. Generally,

sustainability reporting has played a vital role in creating a signi9ficant difference in the

ways companies use to approach their outcomes (Rinaldi et al, 2018).

B) Strengths and Limitations of Conventional accounting according to the

Conceptual Framework

Conventional accounting is a very important tool that is used for developing reports on

the injections performance by investors into a given company. It assists an organization in

obtaining internal controls that help it maximize its performance hence reducing costs incurred

by the company and increase profits (Miller, 2017).One of the major benefits of this tool is its

carried out in 2017 about reporting on corporate social responsibility, 63% of the N100

and 75% of the G250 report using the framework of Global Reporting Initiative. The

sustainability reporting guidelines and the IIRC standards are established for different

purposes (Ahmed et al, 2016). However, these purposes are contemporary.

Differences

GRI observes the impact of the company on the world as a whole whereas as

IIRC observes the impacts of the world on the company, (Barth et al, 2017). The

framework of International Integrated Reporting provides a clear and concise template

which should be used by companies to report the ways through which they sustain the

activities they carry out especially during times when the rate of population growth is

drawing tight the reserves of nature. There is a strong belief that the two frameworks can

work jointly to provide companies as well as their stakeholders with a wider view of how

shareholder value can be created by businesses and how companies can achieve

sustainable development (ldowu et al, 2016). Additionally, GRI also mainly focuses on

the impact of the company on the economy, society and environment. Generally,

sustainability reporting has played a vital role in creating a signi9ficant difference in the

ways companies use to approach their outcomes (Rinaldi et al, 2018).

B) Strengths and Limitations of Conventional accounting according to the

Conceptual Framework

Conventional accounting is a very important tool that is used for developing reports on

the injections performance by investors into a given company. It assists an organization in

obtaining internal controls that help it maximize its performance hence reducing costs incurred

by the company and increase profits (Miller, 2017).One of the major benefits of this tool is its

CONTEMPORARY ACCOUNTING THEORY 18

high adaptability level and its ability to increase the flexibility of the company in adjusting to the

present requirements of integrated and sustainability reporting. Conventional accounting entails

addition of resources to the budget of the previous year with an aim of completing or expanding

the projects. Comprehensiveness of the system is one of the strength of conventional accounting.

The system is designed in a way that it records all the estimable and currently identified costs.

Additionally, conventional accounting comprises of a corporate policy which traces all the

incurred costs such as the environmental costs. Managers also clearly understand the costs for

which they are held responsible for. Allocation of joint costs are also subjected to review after a

given time interval (Miller, 2017).

However, the tool has a limitation of being costly to implement and as well be maintained

since it needs highly skilled personnel to undertake the procedures of financial reporting.

Additionally, conventional accounting is also very complex since it comprises of several

procedures that need to be critically examined in order to derive the necessary reports as far as

the conceptual framework is concerned. It is also limited by the absence of a robust principle

which can be applied to determine exactly what should be mentioned in the income statement

and what should not be included (Miller, 2017). Therefore, losses which are brought about by the

noncurrent assets impairment are usually included in the income statement. However, losses

which are incurred as a result of translating the asset value expressed in foreign currency are not

included. It is always difficult to justify the different treatment that is entailed in conventional

accounting. All losses and gains whether realized or not are reported in a single statement as

required by the comprehensive income statement (Baboukardos and Rimmel,2016). This can

only be possible by widening the conventional income statement which includes both unrealized

losses and unrealized gains that are not reported before the annual profits are reported. In

high adaptability level and its ability to increase the flexibility of the company in adjusting to the

present requirements of integrated and sustainability reporting. Conventional accounting entails

addition of resources to the budget of the previous year with an aim of completing or expanding

the projects. Comprehensiveness of the system is one of the strength of conventional accounting.

The system is designed in a way that it records all the estimable and currently identified costs.

Additionally, conventional accounting comprises of a corporate policy which traces all the

incurred costs such as the environmental costs. Managers also clearly understand the costs for

which they are held responsible for. Allocation of joint costs are also subjected to review after a

given time interval (Miller, 2017).

However, the tool has a limitation of being costly to implement and as well be maintained

since it needs highly skilled personnel to undertake the procedures of financial reporting.

Additionally, conventional accounting is also very complex since it comprises of several

procedures that need to be critically examined in order to derive the necessary reports as far as

the conceptual framework is concerned. It is also limited by the absence of a robust principle

which can be applied to determine exactly what should be mentioned in the income statement

and what should not be included (Miller, 2017). Therefore, losses which are brought about by the

noncurrent assets impairment are usually included in the income statement. However, losses

which are incurred as a result of translating the asset value expressed in foreign currency are not

included. It is always difficult to justify the different treatment that is entailed in conventional

accounting. All losses and gains whether realized or not are reported in a single statement as

required by the comprehensive income statement (Baboukardos and Rimmel,2016). This can

only be possible by widening the conventional income statement which includes both unrealized

losses and unrealized gains that are not reported before the annual profits are reported. In

CONTEMPORARY ACCOUNTING THEORY 19

addition, some costs such as historical costs and out of pocket costs are not maintained in the

reporting process and aggregation (Miller, 2017).

C) Applicability of the theories in explaining the contents of sustainability and

integrated reports

Better Integrated reporting and sustainability enhances legitimacy and governance, gives

more accountability, minimizes information symmetry and improves performance as well as

profitability (Atkins and Maroun, 2015). The non-profit sector and the public form a vital part of

the economy. As a result, most of the integrated reporting and sustainability determinants

explored in the private sector are also applicable to the non-profit and public sector.

Sustainability objectives are usually incorporated in management control systems of various

companies. This is because reporting is usually mainstreamed which brings about the realization

that reporting is not based on end minute scramble and periodic procedures for the relevant

information to be incorporated in the report. Besides supporting integrated reporting and

sustainability, these systems also encourage consistent behaviors with the sustainability

objectives of the organization. Integrated reporting and sustainability is also used Assurance to

influence the perceptions of the general public by the organizations and for portraying

themselves in the possible light (Dumay,2018). Integrated reporting and sustainability also

enhances research opportunities. This particular theory provides comprehensive understanding of

the complexity in setting standards. With the establishment of reporting practices, conducted

research mainly focuses on the actual processes and changes instead of speculative analysis

(Dumay,2018).

addition, some costs such as historical costs and out of pocket costs are not maintained in the

reporting process and aggregation (Miller, 2017).

C) Applicability of the theories in explaining the contents of sustainability and

integrated reports

Better Integrated reporting and sustainability enhances legitimacy and governance, gives

more accountability, minimizes information symmetry and improves performance as well as

profitability (Atkins and Maroun, 2015). The non-profit sector and the public form a vital part of

the economy. As a result, most of the integrated reporting and sustainability determinants

explored in the private sector are also applicable to the non-profit and public sector.

Sustainability objectives are usually incorporated in management control systems of various

companies. This is because reporting is usually mainstreamed which brings about the realization

that reporting is not based on end minute scramble and periodic procedures for the relevant

information to be incorporated in the report. Besides supporting integrated reporting and

sustainability, these systems also encourage consistent behaviors with the sustainability

objectives of the organization. Integrated reporting and sustainability is also used Assurance to

influence the perceptions of the general public by the organizations and for portraying

themselves in the possible light (Dumay,2018). Integrated reporting and sustainability also

enhances research opportunities. This particular theory provides comprehensive understanding of

the complexity in setting standards. With the establishment of reporting practices, conducted

research mainly focuses on the actual processes and changes instead of speculative analysis

(Dumay,2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 20

However, organizations tend to use integrated reports to emphasize on only their positive

activities. It is therefore recommended for users to be aware of this such that they do not always

consider these reports as credible sources of information about a given organization. On the other

side, organizations also exhibit assurance to facilitate credibility of their reports. The market for

integrated reports and sustainability assurance expands especially when reporting rises public

knowledge and prevalence of the disclosure biases of the organization (Loprevite et al, 2018).

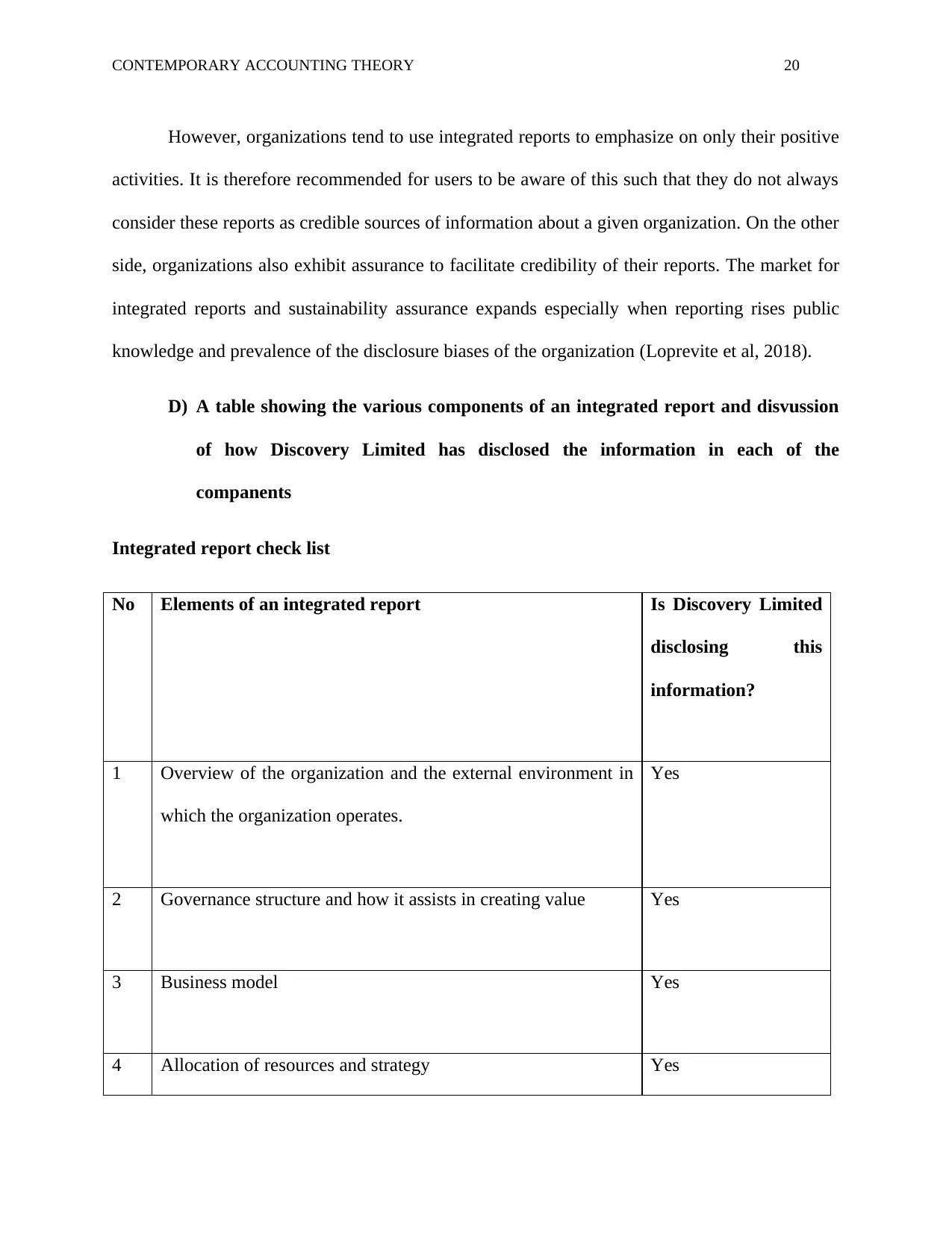

D) A table showing the various components of an integrated report and disvussion

of how Discovery Limited has disclosed the information in each of the

companents

Integrated report check list

No Elements of an integrated report Is Discovery Limited

disclosing this

information?

1 Overview of the organization and the external environment in

which the organization operates.

Yes

2 Governance structure and how it assists in creating value Yes

3 Business model Yes

4 Allocation of resources and strategy Yes

However, organizations tend to use integrated reports to emphasize on only their positive

activities. It is therefore recommended for users to be aware of this such that they do not always

consider these reports as credible sources of information about a given organization. On the other

side, organizations also exhibit assurance to facilitate credibility of their reports. The market for

integrated reports and sustainability assurance expands especially when reporting rises public

knowledge and prevalence of the disclosure biases of the organization (Loprevite et al, 2018).

D) A table showing the various components of an integrated report and disvussion

of how Discovery Limited has disclosed the information in each of the

companents

Integrated report check list

No Elements of an integrated report Is Discovery Limited

disclosing this

information?

1 Overview of the organization and the external environment in

which the organization operates.

Yes

2 Governance structure and how it assists in creating value Yes

3 Business model Yes

4 Allocation of resources and strategy Yes

CONTEMPORARY ACCOUNTING THEORY 21

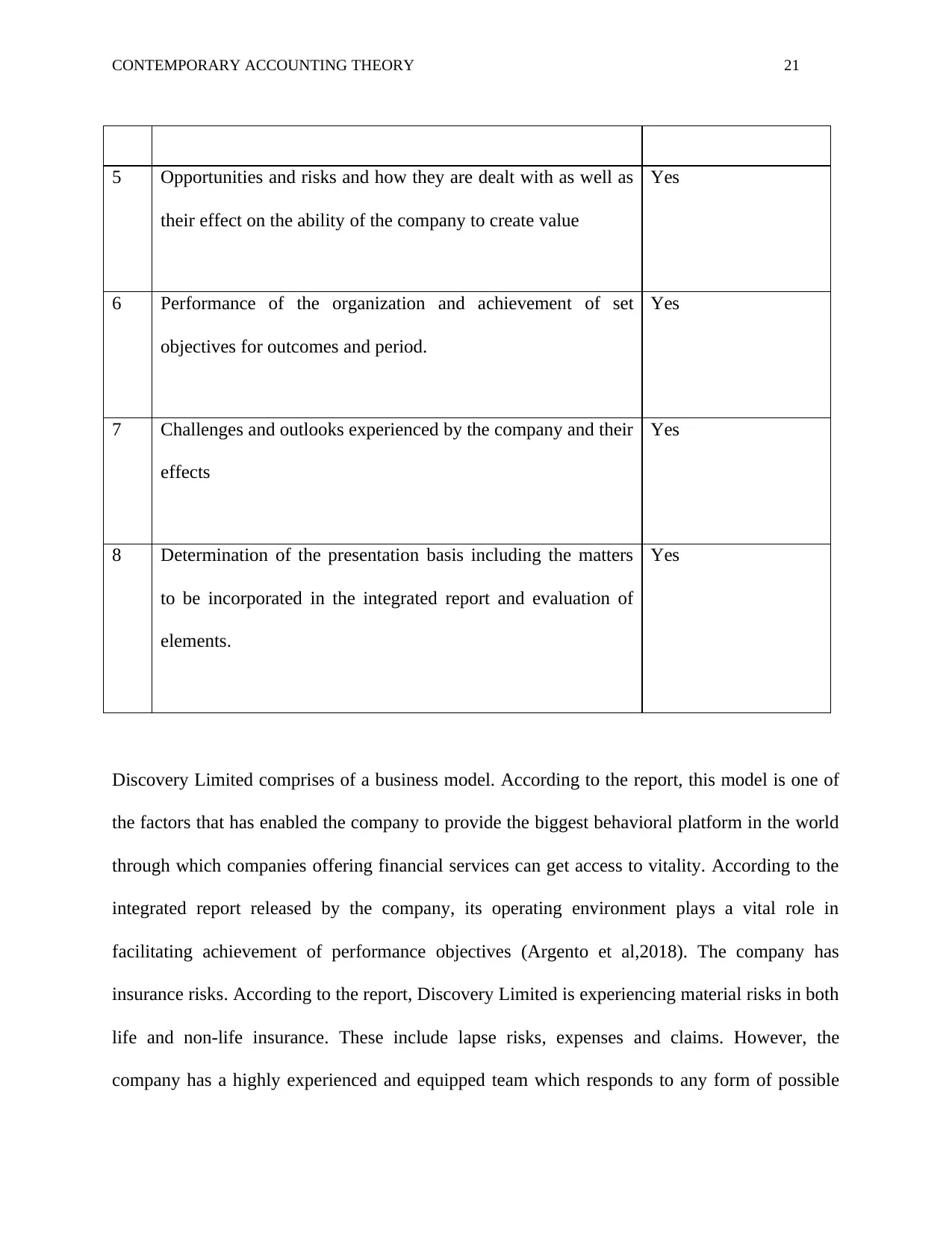

5 Opportunities and risks and how they are dealt with as well as

their effect on the ability of the company to create value

Yes

6 Performance of the organization and achievement of set

objectives for outcomes and period.

Yes

7 Challenges and outlooks experienced by the company and their

effects

Yes

8 Determination of the presentation basis including the matters

to be incorporated in the integrated report and evaluation of

elements.

Yes

Discovery Limited comprises of a business model. According to the report, this model is one of

the factors that has enabled the company to provide the biggest behavioral platform in the world

through which companies offering financial services can get access to vitality. According to the

integrated report released by the company, its operating environment plays a vital role in

facilitating achievement of performance objectives (Argento et al,2018). The company has

insurance risks. According to the report, Discovery Limited is experiencing material risks in both

life and non-life insurance. These include lapse risks, expenses and claims. However, the

company has a highly experienced and equipped team which responds to any form of possible

5 Opportunities and risks and how they are dealt with as well as

their effect on the ability of the company to create value

Yes

6 Performance of the organization and achievement of set

objectives for outcomes and period.

Yes

7 Challenges and outlooks experienced by the company and their

effects

Yes

8 Determination of the presentation basis including the matters

to be incorporated in the integrated report and evaluation of

elements.

Yes

Discovery Limited comprises of a business model. According to the report, this model is one of

the factors that has enabled the company to provide the biggest behavioral platform in the world

through which companies offering financial services can get access to vitality. According to the

integrated report released by the company, its operating environment plays a vital role in

facilitating achievement of performance objectives (Argento et al,2018). The company has

insurance risks. According to the report, Discovery Limited is experiencing material risks in both

life and non-life insurance. These include lapse risks, expenses and claims. However, the

company has a highly experienced and equipped team which responds to any form of possible

CONTEMPORARY ACCOUNTING THEORY 22

risks. The company comprises of the growth strategy which is mainly implemented to expand

into other industries (IRRC Institute, 2018). It also comprises of a network of global vitality, a

system which supports that the wider business strategy of Discovery through creating its

opportunities for growth and integration. The report provides an overview of its group structure

which entails the partnerships the company has made in different countries including Canada,

United States, Japan, Europe, South Africa and Pan-Asia. In the company`s outlook, it explains

how the network of growth Vitality will help the company develop its capabilities through

focusing on establishment of global partnerships as well as developing functions and programs

that are vitality core in all the company`s markets (IRRC Institute, 2018).

E) Comparison of the reporting practices of AUB Group Limited and the

integrated reporting practices of Discovery Limited.

AUB Group Limited did not prepare an integrated report. The company rather prepared

financial reports and annual reports to report its social responsibility. Like AUB Group Limited,

Discovery limited also provides an overview of its operating environment, equity and how its

values lead to achievement of positive outcomes for stakeholders, clients and the business as a

whole (Erol & Demirel,2016). However, AUB Group Limited provides financial position and

cash flow consolidated statements which indicate the performance of the company. In the

integrated report of Discovery Limited, the performance position of the company is indicated by

its market position, embedded value, solvency, new business entities and other factors (Erol &

Demirel,2016).

Conclusion

risks. The company comprises of the growth strategy which is mainly implemented to expand

into other industries (IRRC Institute, 2018). It also comprises of a network of global vitality, a

system which supports that the wider business strategy of Discovery through creating its

opportunities for growth and integration. The report provides an overview of its group structure

which entails the partnerships the company has made in different countries including Canada,

United States, Japan, Europe, South Africa and Pan-Asia. In the company`s outlook, it explains

how the network of growth Vitality will help the company develop its capabilities through

focusing on establishment of global partnerships as well as developing functions and programs

that are vitality core in all the company`s markets (IRRC Institute, 2018).

E) Comparison of the reporting practices of AUB Group Limited and the

integrated reporting practices of Discovery Limited.

AUB Group Limited did not prepare an integrated report. The company rather prepared

financial reports and annual reports to report its social responsibility. Like AUB Group Limited,

Discovery limited also provides an overview of its operating environment, equity and how its

values lead to achievement of positive outcomes for stakeholders, clients and the business as a

whole (Erol & Demirel,2016). However, AUB Group Limited provides financial position and

cash flow consolidated statements which indicate the performance of the company. In the

integrated report of Discovery Limited, the performance position of the company is indicated by

its market position, embedded value, solvency, new business entities and other factors (Erol &

Demirel,2016).

Conclusion

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 23

Conceptual framework is currently one of the most important system in financial

accounting. The system is also acting as a foundation for the future development of accounting

standards and subjective judgment regulator for the decisions made by management when

preparing and presenting financial statements. Despite the several concerns raised about the

applicability of conceptual framework of which some are negative and others are positive, the

system has greatly contributed to the growth of the financial accounting department across the

globe.

Conceptual framework is currently one of the most important system in financial

accounting. The system is also acting as a foundation for the future development of accounting

standards and subjective judgment regulator for the decisions made by management when

preparing and presenting financial statements. Despite the several concerns raised about the

applicability of conceptual framework of which some are negative and others are positive, the

system has greatly contributed to the growth of the financial accounting department across the

globe.

CONTEMPORARY ACCOUNTING THEORY 24

References

Adams, C. A. (2015), “The international integrated reporting council: A call to action”, Critical

Perspectives on Accounting, Vol. 27, pp. 23-28.

Adams, C. A. (2017), “Conceptualizing the contemporary corporate value creation process”,n

Accounting, Auditing and Accountability Journal, Vol. 30 No. 4, pp. 906-931.

Adams, C. A., Potter, B., Singh, P. J. and York, J. (2016), “Exploring the implications of

integrated reporting for social investment (disclosures)”, British Accounting Review,

Vol. 48 No. 3, pp. 283-296.

Ahmed Haji, A. and Anifowose, M. (2016), “The trend of integrated reporting practice in South

Africa: ceremonial or substantive?”, Sustainability Accounting, Management and Policy

Journal, Vol. 7 No. 2, pp. 190-224.

Al-Dmour,A.H. (2018), The Impact Of The Quality Of Financial reporting On Non-Financial

Business Performance And The Role Of Organizations Demographic' Attributes (Type,

Size And Experience). Academy of Accounting and Financial Studies Journal.

Argento, D., Culasso, F., Truant, E. (2018). From Sustainability to Integrated Reporting: The

Legitimizing Role of the CSR Manager. Retrieved from

https://journals.sagepub.com/doi/abs/10.1177/1086026618769487

Armstrong, C (2013). Competence or flexibility? Survival and growth implications of

competitive strategy preferences among small US businesses: Journal of Strategy and

Management, 6; p. 377-398

References

Adams, C. A. (2015), “The international integrated reporting council: A call to action”, Critical

Perspectives on Accounting, Vol. 27, pp. 23-28.

Adams, C. A. (2017), “Conceptualizing the contemporary corporate value creation process”,n

Accounting, Auditing and Accountability Journal, Vol. 30 No. 4, pp. 906-931.

Adams, C. A., Potter, B., Singh, P. J. and York, J. (2016), “Exploring the implications of

integrated reporting for social investment (disclosures)”, British Accounting Review,

Vol. 48 No. 3, pp. 283-296.

Ahmed Haji, A. and Anifowose, M. (2016), “The trend of integrated reporting practice in South

Africa: ceremonial or substantive?”, Sustainability Accounting, Management and Policy

Journal, Vol. 7 No. 2, pp. 190-224.

Al-Dmour,A.H. (2018), The Impact Of The Quality Of Financial reporting On Non-Financial

Business Performance And The Role Of Organizations Demographic' Attributes (Type,

Size And Experience). Academy of Accounting and Financial Studies Journal.

Argento, D., Culasso, F., Truant, E. (2018). From Sustainability to Integrated Reporting: The

Legitimizing Role of the CSR Manager. Retrieved from

https://journals.sagepub.com/doi/abs/10.1177/1086026618769487

Armstrong, C (2013). Competence or flexibility? Survival and growth implications of

competitive strategy preferences among small US businesses: Journal of Strategy and

Management, 6; p. 377-398

CONTEMPORARY ACCOUNTING THEORY 25

Atkins, J. and Maroun, W. (2015), “Integrated reporting in South Africa in 2012: Perspectives

from South African institutional investors”, Meditari Accountancy Research, Vol. 23

No. 2, pp. 197-221.

AUB Group Limited. (2018). Annual reports. Retrieved from

https://www.aubgroup.com.au/site/investor/results-centre/annual-reports

Baboukardos, D. and Rimmel, G. (2016), “Value relevance of accounting information under an

integrated reporting approach: A research note”, Journal of Accounting and Public

Policy, Vol. 35 No. 4, pp. 437-452.

Barth, M. E., Cahan, S. F., Chen, L. and Venter, E. R. (2017), "The economic consequences

associated with integrated report quality: Capital market and real effects", Accounting,

Organizations and Society, Vol. 62, pp. 43-64.

Becker, C (2010). The Conceptual Framework in the United Kingdom and the Introduction of

the Statement of Principles, Munich, GRIN Verlag, p. 1-14

Carrahera, S and Auken, H (2013). The use of financial statements for decision making by small

firms: Journal of Small Business and Entrepreneurship, 26(3), p. 323-336

Daske, H., Hail., Leuz, C., and Verdi, R. (2013), Adopting a Label: Heterogeneity in the

Economic Consequences Around IAS/IFRS Adoptions. Journal of Accounting Research,

51: 495-547.

Dennis,I. (2018).What is a Conceptual Framework for Financial Reporting? Journal of

Accounting in Europe

Atkins, J. and Maroun, W. (2015), “Integrated reporting in South Africa in 2012: Perspectives

from South African institutional investors”, Meditari Accountancy Research, Vol. 23

No. 2, pp. 197-221.

AUB Group Limited. (2018). Annual reports. Retrieved from

https://www.aubgroup.com.au/site/investor/results-centre/annual-reports

Baboukardos, D. and Rimmel, G. (2016), “Value relevance of accounting information under an

integrated reporting approach: A research note”, Journal of Accounting and Public

Policy, Vol. 35 No. 4, pp. 437-452.

Barth, M. E., Cahan, S. F., Chen, L. and Venter, E. R. (2017), "The economic consequences

associated with integrated report quality: Capital market and real effects", Accounting,

Organizations and Society, Vol. 62, pp. 43-64.

Becker, C (2010). The Conceptual Framework in the United Kingdom and the Introduction of

the Statement of Principles, Munich, GRIN Verlag, p. 1-14

Carrahera, S and Auken, H (2013). The use of financial statements for decision making by small

firms: Journal of Small Business and Entrepreneurship, 26(3), p. 323-336

Daske, H., Hail., Leuz, C., and Verdi, R. (2013), Adopting a Label: Heterogeneity in the

Economic Consequences Around IAS/IFRS Adoptions. Journal of Accounting Research,

51: 495-547.

Dennis,I. (2018).What is a Conceptual Framework for Financial Reporting? Journal of

Accounting in Europe

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 26

Dumay, J. C. (2018). Sustainability accounting and integrated reporting. Retrieved from

https://www.researchgate.net/publication/327303501_Sustainability_accounting_and_int

egrated_reporting

Eccles, R and Krzus, M. (2010). One Report: Integrated Reporting for a Sustainable Strategy,

Wiley, New Jersey, USA

Erol,I & Demirel,B.(2016). Investigation of Integrated Reporting As a New Approach of

Corporate Reporting. International Journal of Business and Social Research.

Flower, J (2015). But does sustainability need capitalism or an integrated report: Critical

Perspectives on Accounting, Volume 27, p. 18-22

Gordon, EA., Bischof, J., Daske, H., Munter, P., Saka, C., Smith, KJ., and Venter, ER.

(2015). The IASB's Discussion Paper on the Conceptual Framework for Financial

Reporting: A Commentary and Research Review. Journal of International Financial

Management and amp.

Haji, A. A. and Anifowose, M. (2016), “Audit committee and integrated reporting practice: does

internal assurance matter?”, Managerial Auditing Journal, Vol. 31 No. 8-9, pp. 915-948.

Haji, A. A. and Hossain, D. M. (2016), “Exploring the implications of integrated reporting on

organizational reporting practice: Evidence from highly regarded integrated reporters”,

Qualitative Research in Accounting and Management, Vol. 13 No. 4, pp. 415-444.

Haller, A. and van Staden, C. (2014), “The value added statement – an appropriate instrument for

integrated reporting”, Accounting, Auditing and Accountability Journal, Vol. 27 No. 7,

pp. 1190-1216.

Dumay, J. C. (2018). Sustainability accounting and integrated reporting. Retrieved from

https://www.researchgate.net/publication/327303501_Sustainability_accounting_and_int

egrated_reporting

Eccles, R and Krzus, M. (2010). One Report: Integrated Reporting for a Sustainable Strategy,

Wiley, New Jersey, USA

Erol,I & Demirel,B.(2016). Investigation of Integrated Reporting As a New Approach of

Corporate Reporting. International Journal of Business and Social Research.

Flower, J (2015). But does sustainability need capitalism or an integrated report: Critical

Perspectives on Accounting, Volume 27, p. 18-22

Gordon, EA., Bischof, J., Daske, H., Munter, P., Saka, C., Smith, KJ., and Venter, ER.

(2015). The IASB's Discussion Paper on the Conceptual Framework for Financial

Reporting: A Commentary and Research Review. Journal of International Financial

Management and amp.

Haji, A. A. and Anifowose, M. (2016), “Audit committee and integrated reporting practice: does

internal assurance matter?”, Managerial Auditing Journal, Vol. 31 No. 8-9, pp. 915-948.

Haji, A. A. and Hossain, D. M. (2016), “Exploring the implications of integrated reporting on

organizational reporting practice: Evidence from highly regarded integrated reporters”,

Qualitative Research in Accounting and Management, Vol. 13 No. 4, pp. 415-444.