Contemporary Accounting Theory

VerifiedAdded on 2023/04/04

|21

|4336

|411

AI Summary

This paper provides an evaluation of the Conceptual Framework for Financial Reporting and its application in Australian companies. It discusses the history and development of the framework, the concerns of the Australian accounting profession, and the qualitative characteristics of information in financial reports. The paper also examines the application of the framework by a selected Australian company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ACCOUNTING THEORY 1

ACCT20074 Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

ACCT20074 Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 2

1. Executive Summary

Concepts Statement, which is also known as Conceptual Frameworks, is a field of

accounting composed of inter-related fundamentals and objectives. The main objective of

these frameworks is identifying the purposes or goals of various financial fundamentals and

reporting of various companies, which evaluate the critical concepts used to achieve specific

objectives. In that case, this critical analysis, in part A, provides an evaluation of conceptual

framework and how the Jupiter Mines (JMS), in the Material Sector, utilizes this framework

in the selection of financial statements, circumstances and evens, which are speculated to be

reported or summarized. The section B of this paper compares the international integrated

reporting system against the sustainability reporting protocol, including the analysis of the

relevant limitations and strengths of conventional accounting in reference to the conceptual

framework. To effectively comprehend the rational of this report, theories will be applied to

illustrate and define the sustainability guidelines and integrated reporting. Lastly, the paper

will critically compare and evaluate the reporting practices of the Kumba Iron Ore Limited,

on an index, against the company’s integrated reporting.

1. Executive Summary

Concepts Statement, which is also known as Conceptual Frameworks, is a field of

accounting composed of inter-related fundamentals and objectives. The main objective of

these frameworks is identifying the purposes or goals of various financial fundamentals and

reporting of various companies, which evaluate the critical concepts used to achieve specific

objectives. In that case, this critical analysis, in part A, provides an evaluation of conceptual

framework and how the Jupiter Mines (JMS), in the Material Sector, utilizes this framework

in the selection of financial statements, circumstances and evens, which are speculated to be

reported or summarized. The section B of this paper compares the international integrated

reporting system against the sustainability reporting protocol, including the analysis of the

relevant limitations and strengths of conventional accounting in reference to the conceptual

framework. To effectively comprehend the rational of this report, theories will be applied to

illustrate and define the sustainability guidelines and integrated reporting. Lastly, the paper

will critically compare and evaluate the reporting practices of the Kumba Iron Ore Limited,

on an index, against the company’s integrated reporting.

CONTEMPORARY ACCOUNTING THEORY 3

2. Introduction

The framework documentation is mandated to present the fundamental concepts,

which underlie and govern the presentation and preparation of a company’s financial

statements. These statements are utilized by external users to formulate a Conceptual

Framework (CF) fundamental for financial evaluation. Thus, it relevant to comprehend the

documentation serves a critical aim of assisting the IASB to formulate revised financial

standards, which is relevant for financial statements applicable by companies when applying

financial protocols or handling problems evident in the compliance activities to specific

accounting standards. In that regard, this paper analyses the conceptual framework purposed

for financial reporting and its relevance and application in an Australian Company i.e. The

Jupiter Mines (JMS). The second paper of this paper will evaluate the sustainability and

integrated reporting frameworks applicable in a South African Company i.e. The Kumba Iron

Ore Limited.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

The development of the Conceptual Framework in the US, UK and globally started in

1976 and introduced by the FASB in the United States. This framework was formulated as a

basic for outlaying the relevant financial rules and mitigating the present accounting reporting

issues. From 1978 to 2010, the governing entity has issues 8 accounting statements regarding

the relevant financial reporting applied by various companies, including one SFAC No. 4,

which is a reporting that applies to non-business enterprises. However, SFACs No. 1, 2 and 3

have already been replaced, which leave only 5 as valid SFAC Nos. The reporting is the

SFAC No. 4, which represent the belated frameworks considered by the International

2. Introduction

The framework documentation is mandated to present the fundamental concepts,

which underlie and govern the presentation and preparation of a company’s financial

statements. These statements are utilized by external users to formulate a Conceptual

Framework (CF) fundamental for financial evaluation. Thus, it relevant to comprehend the

documentation serves a critical aim of assisting the IASB to formulate revised financial

standards, which is relevant for financial statements applicable by companies when applying

financial protocols or handling problems evident in the compliance activities to specific

accounting standards. In that regard, this paper analyses the conceptual framework purposed

for financial reporting and its relevance and application in an Australian Company i.e. The

Jupiter Mines (JMS). The second paper of this paper will evaluate the sustainability and

integrated reporting frameworks applicable in a South African Company i.e. The Kumba Iron

Ore Limited.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

The development of the Conceptual Framework in the US, UK and globally started in

1976 and introduced by the FASB in the United States. This framework was formulated as a

basic for outlaying the relevant financial rules and mitigating the present accounting reporting

issues. From 1978 to 2010, the governing entity has issues 8 accounting statements regarding

the relevant financial reporting applied by various companies, including one SFAC No. 4,

which is a reporting that applies to non-business enterprises. However, SFACs No. 1, 2 and 3

have already been replaced, which leave only 5 as valid SFAC Nos. The reporting is the

SFAC No. 4, which represent the belated frameworks considered by the International

CONTEMPORARY ACCOUNTING THEORY 4

Accounting Standards Committee (IASC). This accounting body was established in 1973,

which represented a predecessor entity of the accounting standards body globally. By 1st

April 2010, the accounting entity (IASB) assumed the role of IASC obliged to set out the

global accounting frameworks, despite the current standards being reference to as the

International Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In 1975, the

entity presented its initial reporting of the IAS, which represented the accounting policy

disclosure (Crombie, 2012). The IASC presented its 28th IAS by April 1989, which

represented the financial statements for investment in the relevant associates. In that case, the

conceptual framework developed for the presentation and preparation of accounting

frameworks had been approved by April 1989 by the IASC.

This CF, in United Kingdom, was therefore published in 1989 and applied by the

IASB in 2001, despite its relevance in formulating and unindustrialized the IAS framework.

For the purpose of delayed issuance of the standard, the fundamental purpose of the CF is to

assist the financial entity to formulate International Accounting Standards in the future; and

allow the review of the present Standards paragraphs (IASB, 2010b and B1713) signifying

this framework. The accounting body committed itself into an agreement with the United

States’ FASB, which was referred as the 2nd Norwalk Agreement by 2002; and mandating

that two accounting entities would principally consider removing its present differences and

merge on the basis of the quality conceptual framework (Ehoff, 2010).

As for Australia, the CF was formulated by the AASB and AARF dated from 1985 to

1995. The accounting concepts considering the financial statement had been delivered before

2002, the moment when FRC decide to implement the International Accounting Standard in

Australia (Ehoff, 2010). The accounting statements included SAC 1, 2, 3 and 4.

Accounting Standards Committee (IASC). This accounting body was established in 1973,

which represented a predecessor entity of the accounting standards body globally. By 1st

April 2010, the accounting entity (IASB) assumed the role of IASC obliged to set out the

global accounting frameworks, despite the current standards being reference to as the

International Financial Reporting Standards (IFRS) (Timbate & Park, 2018). In 1975, the

entity presented its initial reporting of the IAS, which represented the accounting policy

disclosure (Crombie, 2012). The IASC presented its 28th IAS by April 1989, which

represented the financial statements for investment in the relevant associates. In that case, the

conceptual framework developed for the presentation and preparation of accounting

frameworks had been approved by April 1989 by the IASC.

This CF, in United Kingdom, was therefore published in 1989 and applied by the

IASB in 2001, despite its relevance in formulating and unindustrialized the IAS framework.

For the purpose of delayed issuance of the standard, the fundamental purpose of the CF is to

assist the financial entity to formulate International Accounting Standards in the future; and

allow the review of the present Standards paragraphs (IASB, 2010b and B1713) signifying

this framework. The accounting body committed itself into an agreement with the United

States’ FASB, which was referred as the 2nd Norwalk Agreement by 2002; and mandating

that two accounting entities would principally consider removing its present differences and

merge on the basis of the quality conceptual framework (Ehoff, 2010).

As for Australia, the CF was formulated by the AASB and AARF dated from 1985 to

1995. The accounting concepts considering the financial statement had been delivered before

2002, the moment when FRC decide to implement the International Accounting Standard in

Australia (Ehoff, 2010). The accounting statements included SAC 1, 2, 3 and 4.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 5

Following the joint project in 2004, the accounting bodies (FASB and IASB) had

agreed to include respective key components and concerns as an interlinked project to

formulate a single Conceptual Framework. This initiative as governed and established based

on the original FASB’s conceptual framework and the IASB’s framework. All the two boards

utilized the developed framework as a foundation of their accounting standards for financial

report.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The Australian accounting profession has a different concern regarding the CF. The

Quasi-legislation denotes that the necessity for the Constitution-centred CF in Australia

makes it nearly impossible to ensure that documented accounting frameworks are consistent

and have been formulated logically (Chen, Ahmad & Kalra, 2018). According to Graymore

(2014), despite the fact that it is seemingly convenient to evaluate the fundamentals of

accounting in the term ‘objectives’ of the relevant accounting statements, the professions

claims that the looseness of the standards in Australia has presented more potential

accounting problems. The Australian Accounting Profession is more concerned with

evaluation the CF functions instead of its objectives in the evaluation of an entity’s financial

statements (Alfiero, Cane, Doronzo & Esposito, 2018). This further implies that the

professions currently rejects the reference and reasoning lines of CF on the basis on

accounting ’objectives’ in the evaluation of financial statements. As argued by Ehoff (2010),

the main reason for this is that the existence of CF is to establish the under-pinning

accounting frameworks, which enables the company to attain short-term accounting

objectives.

Following the joint project in 2004, the accounting bodies (FASB and IASB) had

agreed to include respective key components and concerns as an interlinked project to

formulate a single Conceptual Framework. This initiative as governed and established based

on the original FASB’s conceptual framework and the IASB’s framework. All the two boards

utilized the developed framework as a foundation of their accounting standards for financial

report.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The Australian accounting profession has a different concern regarding the CF. The

Quasi-legislation denotes that the necessity for the Constitution-centred CF in Australia

makes it nearly impossible to ensure that documented accounting frameworks are consistent

and have been formulated logically (Chen, Ahmad & Kalra, 2018). According to Graymore

(2014), despite the fact that it is seemingly convenient to evaluate the fundamentals of

accounting in the term ‘objectives’ of the relevant accounting statements, the professions

claims that the looseness of the standards in Australia has presented more potential

accounting problems. The Australian Accounting Profession is more concerned with

evaluation the CF functions instead of its objectives in the evaluation of an entity’s financial

statements (Alfiero, Cane, Doronzo & Esposito, 2018). This further implies that the

professions currently rejects the reference and reasoning lines of CF on the basis on

accounting ’objectives’ in the evaluation of financial statements. As argued by Ehoff (2010),

the main reason for this is that the existence of CF is to establish the under-pinning

accounting frameworks, which enables the company to attain short-term accounting

objectives.

CONTEMPORARY ACCOUNTING THEORY 6

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential benefits and limitations to consider as an academic concern.

Academic are concerned with accounting logic and consistency, which implies that

accounting standards established following the application of CF should be logical and

consistent (Ehoff, 2010).

Since many nations have established CF, which is similar globally (or might have

alternatively adopted the IASC frameworks), there is the need for countries to embrace

considerable global compatibility on the basic of various accounting standards (Prosic, 2015).

In that case, academic’s concern on quality features on the standard’s comparability and

consistency over the global financial reporting (whereby professions argues that it is relevant

for the evaluation of foreign investment capitals and flows. CF provides the global

fundamentals of accounting systems. In that case, the standard-setters are expected to be

accountable for all their financial decisions (Romolini, Fissi & Gori, 2017). In case these

decisions are retrieved from key concerns evaluated in the CF, the accounting professions

expect the standards to be clear thereby necessitating more explanation prior the

implementation.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the best

guidance for entities to reports on particular accounting standards and evaluation any

financial concern (Crombie, 2012). Accounting-setters will experience minimal political

pressure during the formulation of more accounting standards since the relevant concerns like

the objectives of financial reports, criterion to recognition have been considered following the

establishment of the CF (Alfiero, Cane, Doronzo & Esposito, 2018).

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential benefits and limitations to consider as an academic concern.

Academic are concerned with accounting logic and consistency, which implies that

accounting standards established following the application of CF should be logical and

consistent (Ehoff, 2010).

Since many nations have established CF, which is similar globally (or might have

alternatively adopted the IASC frameworks), there is the need for countries to embrace

considerable global compatibility on the basic of various accounting standards (Prosic, 2015).

In that case, academic’s concern on quality features on the standard’s comparability and

consistency over the global financial reporting (whereby professions argues that it is relevant

for the evaluation of foreign investment capitals and flows. CF provides the global

fundamentals of accounting systems. In that case, the standard-setters are expected to be

accountable for all their financial decisions (Romolini, Fissi & Gori, 2017). In case these

decisions are retrieved from key concerns evaluated in the CF, the accounting professions

expect the standards to be clear thereby necessitating more explanation prior the

implementation.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides the best

guidance for entities to reports on particular accounting standards and evaluation any

financial concern (Crombie, 2012). Accounting-setters will experience minimal political

pressure during the formulation of more accounting standards since the relevant concerns like

the objectives of financial reports, criterion to recognition have been considered following the

establishment of the CF (Alfiero, Cane, Doronzo & Esposito, 2018).

CONTEMPORARY ACCOUNTING THEORY 7

A portion of the limitations that have been related to conceptual frameworks of

bookkeeping include: Conceptual frameworks are outrageous to formulate; the enhancement

of the CF is affected by the governmental actions (Ehoff, 2010). With this, some accountants

present the concern that CFs is more inclined to political procedures; Linked to the limitation

outlined above, whenever the CF considers involving accounting concerns, there is always an

issue of financial estimation of given assets as argued by (Molyneux & Wilson, 2017). The

CFs considers more on financial-related matters. In that case, this framework will consider

disregarding various execution segments such as ecological and social revealing components

(Alfiero, Cane, Doronzo & Esposito, 2018).. Moreover, through the evaluation of financial

execution, CFs critically transits the consideration of financial analysts based on corporate

execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

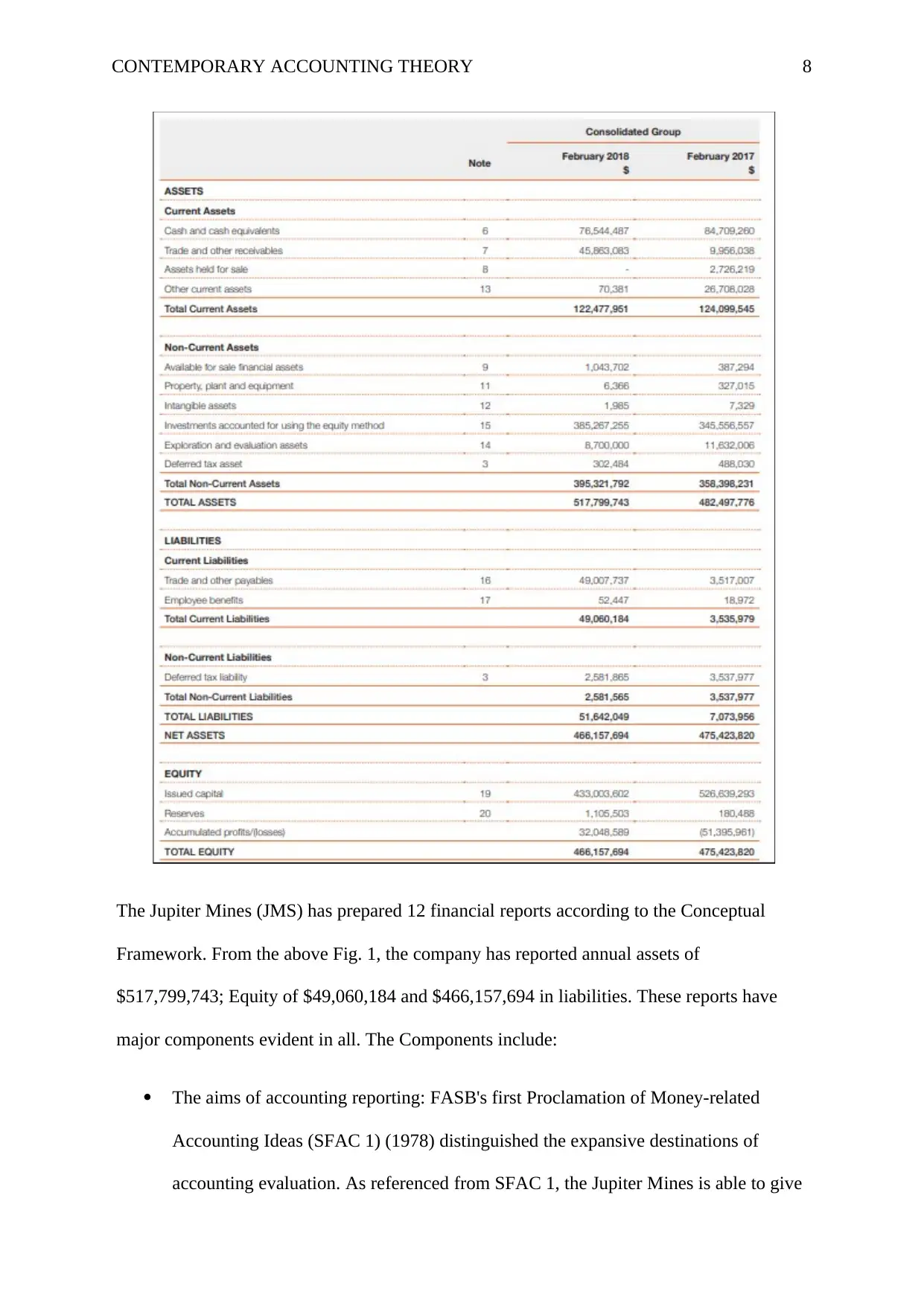

Fig. 1: Consolidate Financial Statement Position of JMS (28th Feb 2018)

A portion of the limitations that have been related to conceptual frameworks of

bookkeeping include: Conceptual frameworks are outrageous to formulate; the enhancement

of the CF is affected by the governmental actions (Ehoff, 2010). With this, some accountants

present the concern that CFs is more inclined to political procedures; Linked to the limitation

outlined above, whenever the CF considers involving accounting concerns, there is always an

issue of financial estimation of given assets as argued by (Molyneux & Wilson, 2017). The

CFs considers more on financial-related matters. In that case, this framework will consider

disregarding various execution segments such as ecological and social revealing components

(Alfiero, Cane, Doronzo & Esposito, 2018).. Moreover, through the evaluation of financial

execution, CFs critically transits the consideration of financial analysts based on corporate

execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

(i) How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

Fig. 1: Consolidate Financial Statement Position of JMS (28th Feb 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

The Jupiter Mines (JMS) has prepared 12 financial reports according to the Conceptual

Framework. From the above Fig. 1, the company has reported annual assets of

$517,799,743; Equity of $49,060,184 and $466,157,694 in liabilities. These reports have

major components evident in all. The Components include:

The aims of accounting reporting: FASB's first Proclamation of Money-related

Accounting Ideas (SFAC 1) (1978) distinguished the expansive destinations of

accounting evaluation. As referenced from SFAC 1, the Jupiter Mines is able to give

The Jupiter Mines (JMS) has prepared 12 financial reports according to the Conceptual

Framework. From the above Fig. 1, the company has reported annual assets of

$517,799,743; Equity of $49,060,184 and $466,157,694 in liabilities. These reports have

major components evident in all. The Components include:

The aims of accounting reporting: FASB's first Proclamation of Money-related

Accounting Ideas (SFAC 1) (1978) distinguished the expansive destinations of

accounting evaluation. As referenced from SFAC 1, the Jupiter Mines is able to give

CONTEMPORARY ACCOUNTING THEORY 9

data that is helpful to present to potential speculators and different clients in making

the balanced venture, credit, and comparable choices. From this starting point in

SFAC 1, the JMS communicated other progressively explicit targets.

The company has applied the CF into its efforts to determine the Fundamentals of Useful

Financial Data: The second component in the conceptual framework, according to the

company’s financial report is the characteristics (or subjective attributes) that budgetary data

ought to have in the event that it is to be valuable in basic leadership. In SFAC 2, the FASB

said that data is helpful on the off chance that it is (I) important, (ii) dependable, and (iii)

tantamount (Carnevale & Mazzuca, 2012). Data is pertinent on the off chance that it can have

any kind of effect in a choice. The data has this quality when it enables clients to anticipate

the future or assess the past and is gotten so as to influence their choices.

Moreover, the CF has been applied in the Financial Statement Elements. This is another

significant advancement in building up a conceptual framework, which focusses on deciding

the components of financial reports in the company. This includes characterizing the classes

of JMS’s data that ought to be contained in monetary reports. FASB's exchange of fiscal

summary components incorporates meanings of significant components, for example,

resources, liabilities, value, incomes, costs, additions, and misfortunes (Crombie, 2012).

Financial Measurement and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for choosing (1) when things

ought to be introduced (or perceived) in the budget summaries, and (2) how to allocate or

measure financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

data that is helpful to present to potential speculators and different clients in making

the balanced venture, credit, and comparable choices. From this starting point in

SFAC 1, the JMS communicated other progressively explicit targets.

The company has applied the CF into its efforts to determine the Fundamentals of Useful

Financial Data: The second component in the conceptual framework, according to the

company’s financial report is the characteristics (or subjective attributes) that budgetary data

ought to have in the event that it is to be valuable in basic leadership. In SFAC 2, the FASB

said that data is helpful on the off chance that it is (I) important, (ii) dependable, and (iii)

tantamount (Carnevale & Mazzuca, 2012). Data is pertinent on the off chance that it can have

any kind of effect in a choice. The data has this quality when it enables clients to anticipate

the future or assess the past and is gotten so as to influence their choices.

Moreover, the CF has been applied in the Financial Statement Elements. This is another

significant advancement in building up a conceptual framework, which focusses on deciding

the components of financial reports in the company. This includes characterizing the classes

of JMS’s data that ought to be contained in monetary reports. FASB's exchange of fiscal

summary components incorporates meanings of significant components, for example,

resources, liabilities, value, incomes, costs, additions, and misfortunes (Crombie, 2012).

Financial Measurement and Recognition: In SFAC 5, ‘Acknowledgment and Estimation in

Fiscal summaries of Business Ventures’, the FASB set up ideas for choosing (1) when things

ought to be introduced (or perceived) in the budget summaries, and (2) how to allocate or

measure financial items.

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

CONTEMPORARY ACCOUNTING THEORY 10

Generally, the FASB argues that reporting on a company’s financial statements ought to be

perceived in the fiscal summaries in the event that they meet the accompanying recognition

principles and measurement bases:

Definitions: The thing meets the meaning of a component of budget reports;

Measurability: It has an important quality quantifiable with adequate dependability

Importance: The data about it is equipped for having any kind of effect on client

choices; and

Reliability: The JMS’s data is illustratively resolute, irrefutable, and impartial.

In SFAC 5, the FASB has expressed that a full arrangement of budget summaries should

appear: Money related position toward the finish of the period, Profit for the period and

Exhaustive salary for the period. This new idea is more extensive than profit and incorporates

all adjustments in proprietors' value other than those that came about because of exchanges

with the proprietors (Hodge, Rajgopal & Shevlin, 2009). A few changes in resource esteems

are incorporated into this idea however are barred from JMS income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

The quantitative characteristics include:

Operationalization of the subjective attributes: To build an estimation apparatus, we

use earlier writing which characterizes money related detailing quality as far as the crucial

and upgrading subjective attributes fundamental choice convenience as characterized in the

ED. The basic subjective attributes (for example significance and loyal portrayal) are most

significant and decide the substance of money related detailing data (Alfiero, Cane, Doronzo

& Esposito, 2018). The improving subjective attributes (for example equivalence,

Generally, the FASB argues that reporting on a company’s financial statements ought to be

perceived in the fiscal summaries in the event that they meet the accompanying recognition

principles and measurement bases:

Definitions: The thing meets the meaning of a component of budget reports;

Measurability: It has an important quality quantifiable with adequate dependability

Importance: The data about it is equipped for having any kind of effect on client

choices; and

Reliability: The JMS’s data is illustratively resolute, irrefutable, and impartial.

In SFAC 5, the FASB has expressed that a full arrangement of budget summaries should

appear: Money related position toward the finish of the period, Profit for the period and

Exhaustive salary for the period. This new idea is more extensive than profit and incorporates

all adjustments in proprietors' value other than those that came about because of exchanges

with the proprietors (Hodge, Rajgopal & Shevlin, 2009). A few changes in resource esteems

are incorporated into this idea however are barred from JMS income.

(iii) What qualitative characteristics of information exhibit in company’s various financial

reports?

The quantitative characteristics include:

Operationalization of the subjective attributes: To build an estimation apparatus, we

use earlier writing which characterizes money related detailing quality as far as the crucial

and upgrading subjective attributes fundamental choice convenience as characterized in the

ED. The basic subjective attributes (for example significance and loyal portrayal) are most

significant and decide the substance of money related detailing data (Alfiero, Cane, Doronzo

& Esposito, 2018). The improving subjective attributes (for example equivalence,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 11

understand-ability, practicality and unquestionable status) can improve choice value when the

crucial subjective attributes are set up. Be that as it may, they cannot decide accounting

detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to

comprehend various concerns raised by clients as suppliers of capital in the company.

Considering the past literature, the relevance of operationalized applying various accounting

elements denotes corroborative and prescient framework. As discussed earlier in this paper,

accountants will critically evaluate the quality of financial earnings instead of accounting

reporting and its quality. This aspect is restrained due to the fact that it ignores non-financial

information and future financial-connected data that is accessible by shareholders (Mostyn,

2012). In order to enhance the quality extend, extensive and prescient analysis of the JMS;’s

financial statement is required.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are

applicable in the business world today (Pérez-López, Moreno-Romero, & Barkemeyer,

2013). The role of businesses in the society today is gradually increasing, as compared its

initial obligation of evaluating its profitability or recording its finances. Therefore,

Sustainability Reporting Guideline presents the relevant standards applicable to the help

companies to enhance competitive advantage (Ceulemans, Lozano & Alonso-Almeida,

2015). Moreover, the component of environmental sustainability in the guideline is critically

recommended for firms to apply the world today compared to the integrated reporting.

However, this form of reporting concentrates more on a selected segment of the entity’s

understand-ability, practicality and unquestionable status) can improve choice value when the

crucial subjective attributes are set up. Be that as it may, they cannot decide accounting

detailing quality all alone.

Importance: ‘Significance’ feature of the company refers to its capability to

comprehend various concerns raised by clients as suppliers of capital in the company.

Considering the past literature, the relevance of operationalized applying various accounting

elements denotes corroborative and prescient framework. As discussed earlier in this paper,

accountants will critically evaluate the quality of financial earnings instead of accounting

reporting and its quality. This aspect is restrained due to the fact that it ignores non-financial

information and future financial-connected data that is accessible by shareholders (Mostyn,

2012). In order to enhance the quality extend, extensive and prescient analysis of the JMS;’s

financial statement is required.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

Both the sustainability and international integrated reporting frameworks are

applicable in the business world today (Pérez-López, Moreno-Romero, & Barkemeyer,

2013). The role of businesses in the society today is gradually increasing, as compared its

initial obligation of evaluating its profitability or recording its finances. Therefore,

Sustainability Reporting Guideline presents the relevant standards applicable to the help

companies to enhance competitive advantage (Ceulemans, Lozano & Alonso-Almeida,

2015). Moreover, the component of environmental sustainability in the guideline is critically

recommended for firms to apply the world today compared to the integrated reporting.

However, this form of reporting concentrates more on a selected segment of the entity’s

CONTEMPORARY ACCOUNTING THEORY 12

status but unable to indicated the specific and relevant climatic transitions and environmental

factors (Crombie, 2012).

On the other hand, International Integrated Reporting Framework improves the firms’

reputation; thus, the profitability of the firm can be evaluated based on global norms and laws

(Messner, 2010). The reporting necessitates investors to build the relationship with both the

accounting and non-accounting data analysts to be able to effectively evaluate potential risks.

Numerous organizations have energetically begun to get readily integrated reports in different

configurations and each report has been shaped as per the requirements of business

properties. Moreover, integrated announcing standards and rules have been distributed by the

Worldwide Integrated Detailing Board, so as to give direction to report evaluators (Soyka,

2013).

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The Convectional Accounting is a significant tool that is applicable in the management of

businesses today. According to Ehoff (2010), convectional accounting is relevant because it

enables companies to report on financial profitability and performance, which also enables

investors to determine the internal financial health of the company. The conventional

accounting, centred on the CF provides a firm foundation for formulating future financial

statement standards, which enhance the sustainability status of specific companies (Alfiero,

Cane, Doronzo & Esposito, 2018). The strength evident in this framework is to permit the

introduction of accounting standards and international integrated reports, which clarify the

status but unable to indicated the specific and relevant climatic transitions and environmental

factors (Crombie, 2012).

On the other hand, International Integrated Reporting Framework improves the firms’

reputation; thus, the profitability of the firm can be evaluated based on global norms and laws

(Messner, 2010). The reporting necessitates investors to build the relationship with both the

accounting and non-accounting data analysts to be able to effectively evaluate potential risks.

Numerous organizations have energetically begun to get readily integrated reports in different

configurations and each report has been shaped as per the requirements of business

properties. Moreover, integrated announcing standards and rules have been distributed by the

Worldwide Integrated Detailing Board, so as to give direction to report evaluators (Soyka,

2013).

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The Convectional Accounting is a significant tool that is applicable in the management of

businesses today. According to Ehoff (2010), convectional accounting is relevant because it

enables companies to report on financial profitability and performance, which also enables

investors to determine the internal financial health of the company. The conventional

accounting, centred on the CF provides a firm foundation for formulating future financial

statement standards, which enhance the sustainability status of specific companies (Alfiero,

Cane, Doronzo & Esposito, 2018). The strength evident in this framework is to permit the

introduction of accounting standards and international integrated reports, which clarify the

CONTEMPORARY ACCOUNTING THEORY 13

key matters in financial statements. Conventional accounting also evaluates key material

concerns, i.e. both positive and negative, in financial statements.

Limitations

Debilitated Basic leadership: Convectional accounting offers decision chiefs little data on an

association's specialties. This is on the grounds that the sort of use the planning procedure

tasks is theoretical and is not solid for settling on specific elements in an convectional

accounting (Alfiero, Cane, Doronzo & Esposito, 2018). This powers chiefs in governments

and associations utilizing traditional planning strategies to change their arrangements

regularly, in order to reinforce their choices.

c) Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Organization financial analysists around the globe utilize institutional hypothesis or

neo-institutional theory in their exploration to demonstrate that establishments of monetary,

social, instructive, money related, and political nature keeps up a huge impact upon overall

associations. Badiyani (2012) directs exact research upon 309 organizations chose from

different sources, in particular, GRI reports list, GRI dataset with best customary

sustainability reports, CRRA Reporting Award 2010. Results demonstrate that integrated

revealing is exceedingly associated with the phase of monetary improvement, national

corporate duty, nations' qualities framework, worker's guilds, the private use of tertiary

training, proprietorship scattering.

Another theory is the accountability theory, which signifies the ideology of corporate

governance, which fundamentally enhances sustainability in the company. Moreover, this

theory enables the company to acknowledge its responsibilities, actions, policies and

key matters in financial statements. Conventional accounting also evaluates key material

concerns, i.e. both positive and negative, in financial statements.

Limitations

Debilitated Basic leadership: Convectional accounting offers decision chiefs little data on an

association's specialties. This is on the grounds that the sort of use the planning procedure

tasks is theoretical and is not solid for settling on specific elements in an convectional

accounting (Alfiero, Cane, Doronzo & Esposito, 2018). This powers chiefs in governments

and associations utilizing traditional planning strategies to change their arrangements

regularly, in order to reinforce their choices.

c) Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

Organization financial analysists around the globe utilize institutional hypothesis or

neo-institutional theory in their exploration to demonstrate that establishments of monetary,

social, instructive, money related, and political nature keeps up a huge impact upon overall

associations. Badiyani (2012) directs exact research upon 309 organizations chose from

different sources, in particular, GRI reports list, GRI dataset with best customary

sustainability reports, CRRA Reporting Award 2010. Results demonstrate that integrated

revealing is exceedingly associated with the phase of monetary improvement, national

corporate duty, nations' qualities framework, worker's guilds, the private use of tertiary

training, proprietorship scattering.

Another theory is the accountability theory, which signifies the ideology of corporate

governance, which fundamentally enhances sustainability in the company. Moreover, this

theory enables the company to acknowledge its responsibilities, actions, policies and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 14

products. Users and the relevant key stakeholders of companies have certain expectations,

which include motivating the firm to consider its implication of actions in a systematic,

transparent and broad manner. In the firm’s integrated report, the theories enable the

company to effectively portray its picture as a major actor in the society today.

d) Preparation of an index (a table or checklist) of various components (criteria) of

an integrated report, and discussion of whether and how the selected South

African Company has disclosed information against each of those components

(criteria)

The integrated reporting considers providing companies with the sufficient

understanding of liabilities and assets, and how they will utilize this data to enhance

profitability (Faria, 2016). These capitals can be money-related, made, scholarly, human, and

social and relationship, and normal capital, yet organizations need not embrace these key

components. Integrated announcing is worked around the accompanying key segments,

which are applicable in the Kumba Iron Ore Ltd.

Table 1: Checklist of Key Components

Checklist No. Key Component

#1 Environment

An integrated report includes the company’s summary of the relevant

compliance to environmental frameworks. These frameworks are

implemented and varied based on specific geographies to which the

company is located.

#2

Socio-Political

The report should include the structure of the federal governance, which

enables the firms to create its anticipated value in the market.

#3 Production

Includes available opportunities and risks required for dealing with an

products. Users and the relevant key stakeholders of companies have certain expectations,

which include motivating the firm to consider its implication of actions in a systematic,

transparent and broad manner. In the firm’s integrated report, the theories enable the

company to effectively portray its picture as a major actor in the society today.

d) Preparation of an index (a table or checklist) of various components (criteria) of

an integrated report, and discussion of whether and how the selected South

African Company has disclosed information against each of those components

(criteria)

The integrated reporting considers providing companies with the sufficient

understanding of liabilities and assets, and how they will utilize this data to enhance

profitability (Faria, 2016). These capitals can be money-related, made, scholarly, human, and

social and relationship, and normal capital, yet organizations need not embrace these key

components. Integrated announcing is worked around the accompanying key segments,

which are applicable in the Kumba Iron Ore Ltd.

Table 1: Checklist of Key Components

Checklist No. Key Component

#1 Environment

An integrated report includes the company’s summary of the relevant

compliance to environmental frameworks. These frameworks are

implemented and varied based on specific geographies to which the

company is located.

#2

Socio-Political

The report should include the structure of the federal governance, which

enables the firms to create its anticipated value in the market.

#3 Production

Includes available opportunities and risks required for dealing with an

CONTEMPORARY ACCOUNTING THEORY 15

entity’s concerns on boosting its productivity.

#4 Financial Evaluation of Costs

This deals with the applied strategies and the means of allocating the

company’s resource for productivity (Ivan, 2018).

#5 People

This aspect is critical for the achievement and performance of strategic

aims to financial outcomes and periods. With the right people, an entity

is capable of establishing a competitive advantage (Graymore, 2014).

#6 Health & Safety (H&S)

An integrated report includes the relevant regulations on Health and

Safety, which helps the company to control its strategies concerning the

mitigation of its strategies challenges on HS.

The Kumba Iron Ore Limited has disclosed the six key components in the checklist,

which underpins all the activities undertaken in the company. Every pillar

(Environment, Socio-Political, Production, Financial Evaluation of Costs, People, and

Health & Safety) defines the Key Performance Indicator (KPI), including the

fundamental targets set by the firm to evaluate its accounting and non-accounting

performance.

e) Comparison of Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African Company

In comparison to the reporting the Jupiter Mines, based on the provided index of key

components, which include Environment, Socio-Political, Production, Financial Evaluation

of Costs, People and Health & Safety (H&S, it is evident that the relative strategies

concerning corporate strategies, operating framework, opportunity analysis, and risk

management required thorough analysis. The annual reports of both companies cover the

obligation, including the financial operation, which have a fundamental control on business

entity’s concerns on boosting its productivity.

#4 Financial Evaluation of Costs

This deals with the applied strategies and the means of allocating the

company’s resource for productivity (Ivan, 2018).

#5 People

This aspect is critical for the achievement and performance of strategic

aims to financial outcomes and periods. With the right people, an entity

is capable of establishing a competitive advantage (Graymore, 2014).

#6 Health & Safety (H&S)

An integrated report includes the relevant regulations on Health and

Safety, which helps the company to control its strategies concerning the

mitigation of its strategies challenges on HS.

The Kumba Iron Ore Limited has disclosed the six key components in the checklist,

which underpins all the activities undertaken in the company. Every pillar

(Environment, Socio-Political, Production, Financial Evaluation of Costs, People, and

Health & Safety) defines the Key Performance Indicator (KPI), including the

fundamental targets set by the firm to evaluate its accounting and non-accounting

performance.

e) Comparison of Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African Company

In comparison to the reporting the Jupiter Mines, based on the provided index of key

components, which include Environment, Socio-Political, Production, Financial Evaluation

of Costs, People and Health & Safety (H&S, it is evident that the relative strategies

concerning corporate strategies, operating framework, opportunity analysis, and risk

management required thorough analysis. The annual reports of both companies cover the

obligation, including the financial operation, which have a fundamental control on business

CONTEMPORARY ACCOUNTING THEORY 16

processes. For instance, the Kumba’s report considers the Centurion corporate management

office, Saldanha’s port operation and the marketing segment that the company operates in.

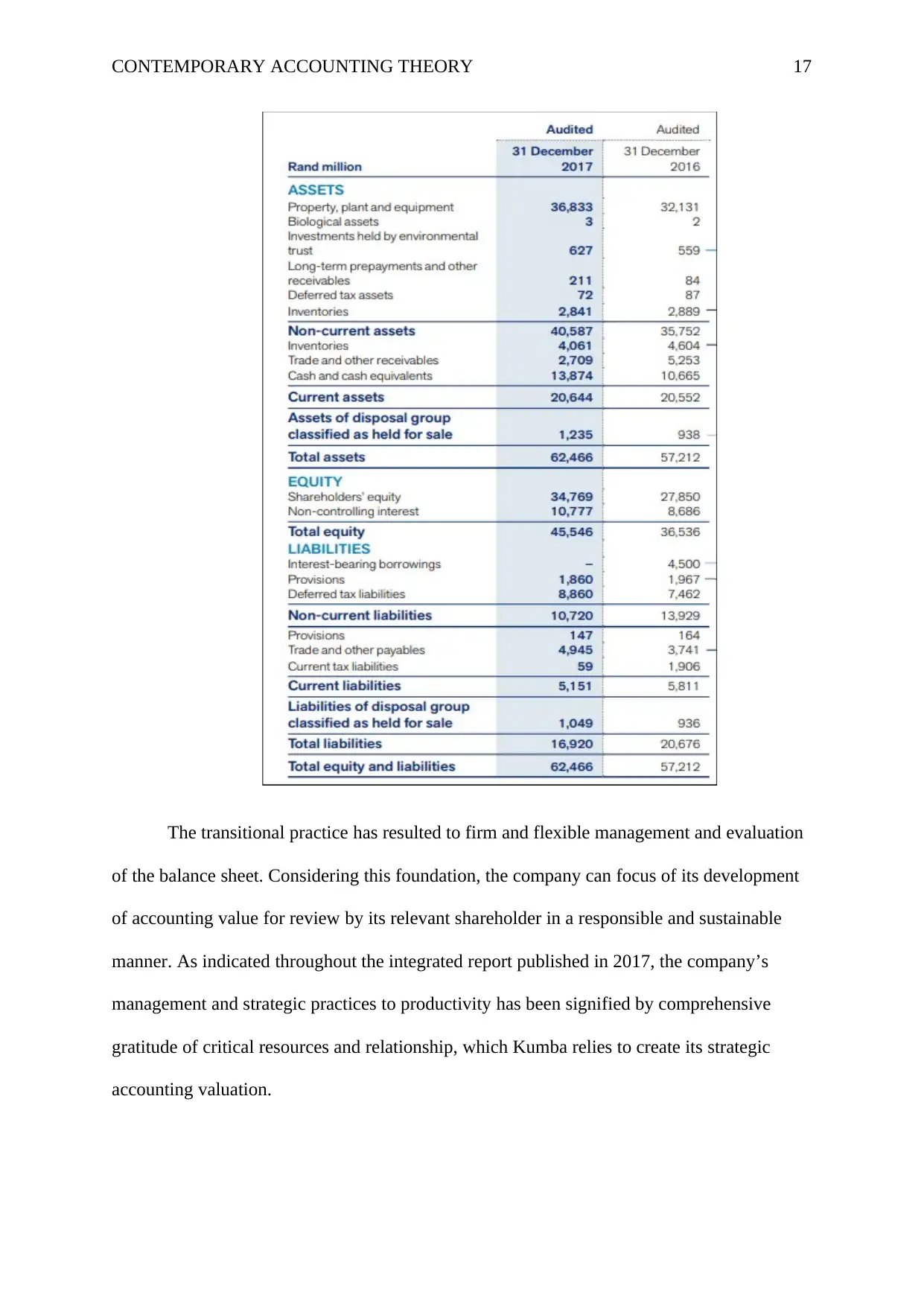

Based on the index of key components (Environment, Socio-Political, Production,

Financial Evaluation of Costs, People, and Health & Safety) in an integrated report, it is

evident that the Kumba Iron Ore Limited prepares an integrated report. All the key

components have been considered in the 2017 financial report shown in Figure 2 below. The

integrated report presented in 2017 was written basically for prospective and current

stakeholders, who consider demonstrating that the company has effective strategies that are

capable of delivering and optimizing production value. From 2017 until the present, Kumba

has implemented targeted transitions to the relevant changes in its accounting strategies to

enhance sustainability within its competitive environment.

Figure 2: Consolidated Statements of Kumba’s Financial Position (31st December

2017)

processes. For instance, the Kumba’s report considers the Centurion corporate management

office, Saldanha’s port operation and the marketing segment that the company operates in.

Based on the index of key components (Environment, Socio-Political, Production,

Financial Evaluation of Costs, People, and Health & Safety) in an integrated report, it is

evident that the Kumba Iron Ore Limited prepares an integrated report. All the key

components have been considered in the 2017 financial report shown in Figure 2 below. The

integrated report presented in 2017 was written basically for prospective and current

stakeholders, who consider demonstrating that the company has effective strategies that are

capable of delivering and optimizing production value. From 2017 until the present, Kumba

has implemented targeted transitions to the relevant changes in its accounting strategies to

enhance sustainability within its competitive environment.

Figure 2: Consolidated Statements of Kumba’s Financial Position (31st December

2017)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 17

The transitional practice has resulted to firm and flexible management and evaluation

of the balance sheet. Considering this foundation, the company can focus of its development

of accounting value for review by its relevant shareholder in a responsible and sustainable

manner. As indicated throughout the integrated report published in 2017, the company’s

management and strategic practices to productivity has been signified by comprehensive

gratitude of critical resources and relationship, which Kumba relies to create its strategic

accounting valuation.

The transitional practice has resulted to firm and flexible management and evaluation

of the balance sheet. Considering this foundation, the company can focus of its development

of accounting value for review by its relevant shareholder in a responsible and sustainable

manner. As indicated throughout the integrated report published in 2017, the company’s

management and strategic practices to productivity has been signified by comprehensive

gratitude of critical resources and relationship, which Kumba relies to create its strategic

accounting valuation.

CONTEMPORARY ACCOUNTING THEORY 18

Another significant practice evident from the companies is the evaluation of

productivity, which considers evaluating potential outcomes, opportunities and risks in the

company’s operations. The financial outcomes are helpful for the various stakeholders who

need this information to monitor their investment in the company (Adams & Simnett, 2011).

The evaluation of potential and principle outcomes of the company’s obligations has been

evaluation in pages 10-11 for the Kumba Iron Ore Limited. Moreover, the company has also

published the sustainability reports, Ore Reserve and Mineral Resource Report and the annual

financial report. The process of financial reporting for the two companies is government by

the requirements and principles in the IFRS, GRA framework and the JSE listing requirement

based on key components in an integrated report.

5. Conclusion

In conclusion, the conceptual framework addresses the central concern of accounting

professionals regarding the preparation and monitoring of financial statements. The founding

answer to academic’s concern is that this framework is effective for the provision of

accounting information for integrated and sustainability documentation, which is useful for

potential lenders, investors and stakeholders. Resultantly, the framework presents the

necessary data that can be used as a basis for financial decision for companies since the

information is relevant, applicable and error-free. Thus, the financial frameworks have

enabled the Kumba and Jupiter Mines to enable its sustainability in the competitive world.

Another significant practice evident from the companies is the evaluation of

productivity, which considers evaluating potential outcomes, opportunities and risks in the

company’s operations. The financial outcomes are helpful for the various stakeholders who

need this information to monitor their investment in the company (Adams & Simnett, 2011).

The evaluation of potential and principle outcomes of the company’s obligations has been

evaluation in pages 10-11 for the Kumba Iron Ore Limited. Moreover, the company has also

published the sustainability reports, Ore Reserve and Mineral Resource Report and the annual

financial report. The process of financial reporting for the two companies is government by

the requirements and principles in the IFRS, GRA framework and the JSE listing requirement

based on key components in an integrated report.

5. Conclusion

In conclusion, the conceptual framework addresses the central concern of accounting

professionals regarding the preparation and monitoring of financial statements. The founding

answer to academic’s concern is that this framework is effective for the provision of

accounting information for integrated and sustainability documentation, which is useful for

potential lenders, investors and stakeholders. Resultantly, the framework presents the

necessary data that can be used as a basis for financial decision for companies since the

information is relevant, applicable and error-free. Thus, the financial frameworks have

enabled the Kumba and Jupiter Mines to enable its sustainability in the competitive world.

CONTEMPORARY ACCOUNTING THEORY 19

References

Adams, S., & Simnett, R. (2011). Integrated Reporting: An Opportunity for Australia's Not-

for-Profit Sector. Australian Accounting Review, 21(3), 292-301. doi: 10.1111/j.1835-

2561.2011.00143.x

Alfiero, S., Cane, M., Doronzo, R., & Esposito, A. (2018). Determining characteristics of

boards adopting Integrated Reporting. FINANCIAL REPORTING, 1(2), 37-71. doi:

10.3280/fr2018-002003

Badiyani, B. (2012). Four Critical Issues in Contemporary Accounting. Global Journal For

Research Analysis, 2(2), 1-2. doi: 10.15373/22778160/february2013/1

Carnevale, C., & Mazzuca, M. (2012). Sustainability Reporting and Varieties of

Capitalism. Sustainable Development, 22(6), 361-376. doi: 10.1002/sd.1554

Ceulemans, K., Lozano, R., & Alonso-Almeida, M. (2015). Sustainability Reporting in

Higher Education: Interconnecting the Reporting Process and Organisational Change

Management for Sustainability. Sustainability, 7(7), 8881-8903. doi:

10.3390/su7078881

Chen, C., Ahmad, S., & Kalra, A. (2018). A Conceptual Framework for Integration

Development of GSFLOW Model: Concerns and Issues Identified and Addressed for

Model Development Efficiency. Geoscientific Model Development Discussions, 2(2),

1-18. doi: 10.5194/gmd-2018-268

Crombie, N. (2012). Contemporary Issues in International Corporate

Governance20122Edited by Suzanne Young. Contemporary Issues in International

Corporate Governance. Prahran: Tilde University Press 2009. 228 pp., ISBN: 978‐0‐

References

Adams, S., & Simnett, R. (2011). Integrated Reporting: An Opportunity for Australia's Not-

for-Profit Sector. Australian Accounting Review, 21(3), 292-301. doi: 10.1111/j.1835-

2561.2011.00143.x

Alfiero, S., Cane, M., Doronzo, R., & Esposito, A. (2018). Determining characteristics of

boards adopting Integrated Reporting. FINANCIAL REPORTING, 1(2), 37-71. doi:

10.3280/fr2018-002003

Badiyani, B. (2012). Four Critical Issues in Contemporary Accounting. Global Journal For

Research Analysis, 2(2), 1-2. doi: 10.15373/22778160/february2013/1

Carnevale, C., & Mazzuca, M. (2012). Sustainability Reporting and Varieties of

Capitalism. Sustainable Development, 22(6), 361-376. doi: 10.1002/sd.1554

Ceulemans, K., Lozano, R., & Alonso-Almeida, M. (2015). Sustainability Reporting in

Higher Education: Interconnecting the Reporting Process and Organisational Change

Management for Sustainability. Sustainability, 7(7), 8881-8903. doi:

10.3390/su7078881

Chen, C., Ahmad, S., & Kalra, A. (2018). A Conceptual Framework for Integration

Development of GSFLOW Model: Concerns and Issues Identified and Addressed for

Model Development Efficiency. Geoscientific Model Development Discussions, 2(2),

1-18. doi: 10.5194/gmd-2018-268

Crombie, N. (2012). Contemporary Issues in International Corporate

Governance20122Edited by Suzanne Young. Contemporary Issues in International

Corporate Governance. Prahran: Tilde University Press 2009. 228 pp., ISBN: 978‐0‐

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 20

7346‐1071‐3. Pacific Accounting Review, 24(1), 104-106. doi:

10.1108/01140581211221588

Ehoff, Jr., C. (2010). Notes On Accounting Capstone Course Design: Contemporary Issues

Versus Case Analysis Enhances Student Interest And Learning. Contemporary Issues

In Education Research (CIER), 3(3), 59. doi: 10.19030/cier.v3i3.188

Faria, M. (2016). A New Form of Reporting For Companies. The Integrated

Reporting. International Journal Of Management And Economics Invention, 32(12),

24. doi: 10.18535/ijmei/v2i11.02

Graymore, M. (2014). Sustainability Reporting: An Approach to Get the Right Mix of Theory

and Practicality for Local Actors. Sustainability, 6(6), 3145-3170. doi:

10.3390/su6063145

Hodge, F., Rajgopal, S., & Shevlin, T. (2009). Do Managers Value Stock Options and

Restricted Stock Consistent with Economic Theory?. Contemporary Accounting

Research, 26(3), 899-932. doi: 10.1506/car.26.3.11

Ivan, O. (2018). Integrated Reporting in the Context of Corporate Governance. Case study on

the Adoption of Integrated Reporting of Romanian Companies listed on BSE. Valahian

Journal Of Economic Studies, 9(2), 127-138. doi: 10.2478/vjes-2018-0024

Messner, M. (2010). Contemporary Issues in Accounting. European Accounting

Review, 19(1), 191-192. doi: 10.1080/09638181003714622

Molyneux, P., & Wilson, J. (2017). Contemporary issues in banking. The British Accounting

Review, 49(2), 117-120. doi: 10.1016/j.bar.2016.10.004

7346‐1071‐3. Pacific Accounting Review, 24(1), 104-106. doi:

10.1108/01140581211221588

Ehoff, Jr., C. (2010). Notes On Accounting Capstone Course Design: Contemporary Issues

Versus Case Analysis Enhances Student Interest And Learning. Contemporary Issues

In Education Research (CIER), 3(3), 59. doi: 10.19030/cier.v3i3.188

Faria, M. (2016). A New Form of Reporting For Companies. The Integrated

Reporting. International Journal Of Management And Economics Invention, 32(12),

24. doi: 10.18535/ijmei/v2i11.02

Graymore, M. (2014). Sustainability Reporting: An Approach to Get the Right Mix of Theory

and Practicality for Local Actors. Sustainability, 6(6), 3145-3170. doi:

10.3390/su6063145

Hodge, F., Rajgopal, S., & Shevlin, T. (2009). Do Managers Value Stock Options and

Restricted Stock Consistent with Economic Theory?. Contemporary Accounting

Research, 26(3), 899-932. doi: 10.1506/car.26.3.11

Ivan, O. (2018). Integrated Reporting in the Context of Corporate Governance. Case study on

the Adoption of Integrated Reporting of Romanian Companies listed on BSE. Valahian

Journal Of Economic Studies, 9(2), 127-138. doi: 10.2478/vjes-2018-0024

Messner, M. (2010). Contemporary Issues in Accounting. European Accounting

Review, 19(1), 191-192. doi: 10.1080/09638181003714622

Molyneux, P., & Wilson, J. (2017). Contemporary issues in banking. The British Accounting

Review, 49(2), 117-120. doi: 10.1016/j.bar.2016.10.004

CONTEMPORARY ACCOUNTING THEORY 21

Mostyn, G. (2012). Cognitive Load Theory: What It Is, Why It's Important for Accounting

Instruction and Research. Issues In Accounting Education, 27(1), 227-245. doi:

10.2308/iace-50099

Pérez-López, D., Moreno-Romero, A., & Barkemeyer, R. (2013). Exploring the Relationship

between Sustainability Reporting and Sustainability Management Practices. Business

Strategy And The Environment, 24(8), 720-734. doi: 10.1002/bse.1841

Prosic, D. (2015). Integrated reporting: A new approach to corporate reporting and

management. Bankarstvo, 44(4), 62-87. doi: 10.5937/bankarstvo1504062p

Romolini, A., Fissi, S., & Gori, E. (2017). Exploring Integrated Reporting Research: Results

and Perspectives. International Journal Of Accounting And Financial Reporting, 7(1),

12. doi: 10.5296/ijafr.v7i1.10630

Soyka, P. (2013). The International Integrated Reporting Council (IIRC) Integrated Reporting

Framework: Toward Better Sustainability Reporting and (Way) Beyond. Environmental

Quality Management, 23(2), 1-14. doi: 10.1002/tqem.21357

Timbate, L., & Park, C. (2018). CSR Performance, Financial Reporting, and Investors’

Perception on Financial Reporting. Sustainability, 10(2), 522. doi: 10.3390/su10020522

Mostyn, G. (2012). Cognitive Load Theory: What It Is, Why It's Important for Accounting

Instruction and Research. Issues In Accounting Education, 27(1), 227-245. doi:

10.2308/iace-50099

Pérez-López, D., Moreno-Romero, A., & Barkemeyer, R. (2013). Exploring the Relationship

between Sustainability Reporting and Sustainability Management Practices. Business

Strategy And The Environment, 24(8), 720-734. doi: 10.1002/bse.1841

Prosic, D. (2015). Integrated reporting: A new approach to corporate reporting and

management. Bankarstvo, 44(4), 62-87. doi: 10.5937/bankarstvo1504062p

Romolini, A., Fissi, S., & Gori, E. (2017). Exploring Integrated Reporting Research: Results

and Perspectives. International Journal Of Accounting And Financial Reporting, 7(1),

12. doi: 10.5296/ijafr.v7i1.10630

Soyka, P. (2013). The International Integrated Reporting Council (IIRC) Integrated Reporting

Framework: Toward Better Sustainability Reporting and (Way) Beyond. Environmental

Quality Management, 23(2), 1-14. doi: 10.1002/tqem.21357

Timbate, L., & Park, C. (2018). CSR Performance, Financial Reporting, and Investors’

Perception on Financial Reporting. Sustainability, 10(2), 522. doi: 10.3390/su10020522

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.