Conceptual Framework in Accounting: RIO TINTO and Glen Core Analysis

VerifiedAdded on 2023/03/23

Contemporary Accounting Theory (Part A and B)

Student’s Name

Institution Affiliation

Date

1

Paraphrase This Document

1. Executive Summary

The main rationale behind the creation of the Conceptual Framework in the

accounting sector is the aim to identify fundamental concerns; which are relevant when

evaluating financial statements. As such, the framework enables the firm’s managers to

evaluate their financial health hence assuring the company’s profitability. In that regard, this

paper will critically consider applying the framework on an Australian company: RIO

TINTO, which further explains, in section A, how the selected company applies this

framework when selecting financial statements, key concerns and events. In section B, a

comparison of the sustainability reporting and the international integration reporting

framework will be evaluated. Moreover, this segment includes an evaluation of the strengths

and limitations of financial statements considering the conceptual framework. To critically

evaluate the rationale intended by the section B, a South African Country named Glen Core

PLC will be used, based on a provided index of components available in an integrated report.

2

Table of Contents

1. Executive Summary.......................................................................................................................2

2. Introduction...................................................................................................................................4

3. Part A.............................................................................................................................................4

a) Review of the history and development of the Conceptual Framework for Financial Reporting

4

b) Explanation of Australian accounting profession’s concerns regarding Conceptual Framework

5

c) Discussion of academic’s concerns about the quality (potential benefits and limitations) of

the Conceptual Framework...............................................................................................................6

d) Explanation of how the conceptual framework has been applied by the selected Australian

Company...........................................................................................................................................7

i. How many statements/reports have been prepared as per the Conceptual Framework and

what are their major components...................................................................................................7

ii. Which recognition principles and measurement bases have been applied for revenue, assets

and liabilities.................................................................................................................................9

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?........................................................................................................................................10

4. Part B...........................................................................................................................................11

a) Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework......................................................................................................................................11

b) Rigour (strength & limitations) of the conventional accounting, based upon the Conceptual

Framework for contents of sustainability as well as integrated reports..........................................12

c) Applicability (usefulness of limitations) of the theories to explain contents of sustainability as

well as integrated reports................................................................................................................14

d) Preparation of an index (a table or checklist) of various components (criteria) of an integrated

report, and discussion of whether and how the selected South African Company has disclosed

information against each of those components (criteria)...............................................................15

e) Comparison of Australian company’s reporting practices with the index and the integrated

reporting practices in the selected South African Company............................................................17

5. Conclusion...................................................................................................................................19

References...........................................................................................................................................20

Appendix.............................................................................................................................................23

List of Abbreviations........................................................................................................................23

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Introduction

The Conceptual Framework (CF) is essential for the formulation of standardized

financial protocols that enable auditors and accountants to determine and monitor the

company’s financial statements, which is significant for evaluating the company’s

profitability. Thus, the financial statements are applicable by company’s users and the

relevant key stakeholders to fundamentally create the conceptual framework, which aid in the

purposes of evaluating the company’s finances. This paper considers approaching the thesis

on CF application on two companies: RIO TINTO and the Glen Core PLC. The International

Accounting Standards Board (IASB) plays a significant mandate in the formation of

standardize and revised financial guidelines that also play a crucial obligation to help analysts

to managing and solving financial issues. In that case, the framework enables managers to

make the necessary decisions, which are in compliance with specific protocols.

3. Part A

a) Review of the history and development of the Conceptual Framework for

Financial Reporting

According to literature review concerning the history and development of the

Conceptual Framework for financial reporting, in reference to IASB denote that there is a

standardized purpose, which contribute to the introduction of the CF for financial reporting

by businesses in United Kingdom (UK), United States (US), Australia, among other nations.

According to Ehoff (2010), the CF was formulated by the AASB dated from 1985 to 1995.

The accounting concepts considering the financial statement had been delivered before 2002,

the moment when FRC decide to implement the International Accounting Standard in

Australia (Ehoff, 2010). The accounting statements included c1, 2, 3 and 4 Romolini, Fissi &

Gori, 2017). Following the joint project in 2004, the accounting bodies agreed to include

respective key components and concerns as an interlinked project to formulate a single

4

Paraphrase This Document

Conceptual Framework. This initiative as governed and established based on the original

IASB conceptual framework (Timbate & Park, 2018). All the two boards utilized the

developed framework as a foundation of their accounting standards for financial reporting.

b) Explanation of Australian accounting profession’s concerns regarding

Conceptual Framework

The introduction and implementation of the conceptual framework for financial reporting has

presented some concerns denoted by the Australian profession (Aasb.gov.au, 2019). These

profession’s concerns include:

Unpredictability concerning the standardized value measurement introduced on

assets, liabilities and revenue. This is a major concern presented by the accounting

profession in Australia concerning the conceptual framework. Moreover, the

emphasis on valuation of intangible company’s assets has also been reconsidered as a

concern by the relevant stakeholders when it comes to fair value determination

(Aasb.gov.au, 2019).

The negative implications relating to the introduction of the IASB conceptual

framework for financial reporting is another concern expressed by the Australian

accounting profession. This concern relates to the measuring and recognition of assets

and liabilities of businesses. Indeed, this is a significant concern to consider because

businesses are subjected to negative economic effects due to rapidly transforming

measurement and recognition criteria of assets, liabilities and revenue (Graymore,

2014)

The introduction and implementation of the conceptual framework for financial

reporting affect non-profit businesses in Australia, which presents another concern for

the Accounting profession. It is significant to note that the conceptual framework of

the IASB was introduced and implemented for profit organization; however, there is a

5

legal necessity to separate the financial guidelines for various companies in Australia

(Timbate & Park, 2018).

c) Discussion of academic’s concerns about the quality (potential benefits and

limitations) of the Conceptual Framework

The CF has potential benefits and limitations to consider as an academic concern.

Academic are concerned with accounting logic and consistency, which implies that

accounting standards established following the application of CF should be logical and

consistent (Ehoff, 2010).

Potential benefits include:

Since many nations have established CF, which is similar globally (or might have

alternatively adopted the IASC frameworks), there is the need for countries to

embrace considerable global compatibility on the basic of various accounting

standards (Prosic, 2015). In that case, academic’s concern on quality features on the

standard’s comparability and consistency over the global financial reporting (whereby

professions argues that it is relevant for the evaluation of foreign investment capitals

and flows. CF provides the global fundamentals of accounting systems. In that case,

the standard-setters are expected to be accountable for all their financial decisions

(Romolini, Fissi & Gori, 2017). In case these decisions are retrieved from key

concerns evaluated in the CF, the accounting professions expect the standards to be

clear thereby necessitating more explanation prior the implementation.

The CF establishes an appropriate methodology of communicating the fundamental

concepts based on the present financial reports. Therefore, this framework provides

the best guidance for entities to reports on particular accounting standards and

evaluation any financial concern (Crombie, 2012).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting-setters will experience minimal political pressure during the formulation

of more accounting standards since the relevant concerns like the objectives of

financial reports, criterion to recognition have been considered following the

establishment of the CF.

A portion of the limitations that have been related to conceptual frameworks of bookkeeping

include:

Conceptual frameworks are outrageous to formulate.

The enhancement of the CF is affected by the governmental actions. With this, some

accountants present the concern that CFs is more inclined to political procedures.

Linked to the limitation outlined above, whenever the CF considers involving

accounting concerns, there is always an issue of financial estimation of given assets as

argued by (Molyneux & Wilson, 2017).

The CFs considers more on financial-related matters. In that case, this framework will

consider disregarding various execution segments such as ecological and social revealing

components (Timbate & Park, 2018). Moreover, through the evaluation of financial

execution, CFs critically transits the consideration of financial analysts based on corporate

execution.

d) Explanation of how the conceptual framework has been applied by the selected

Australian Company

i. How many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

7

Paraphrase This Document

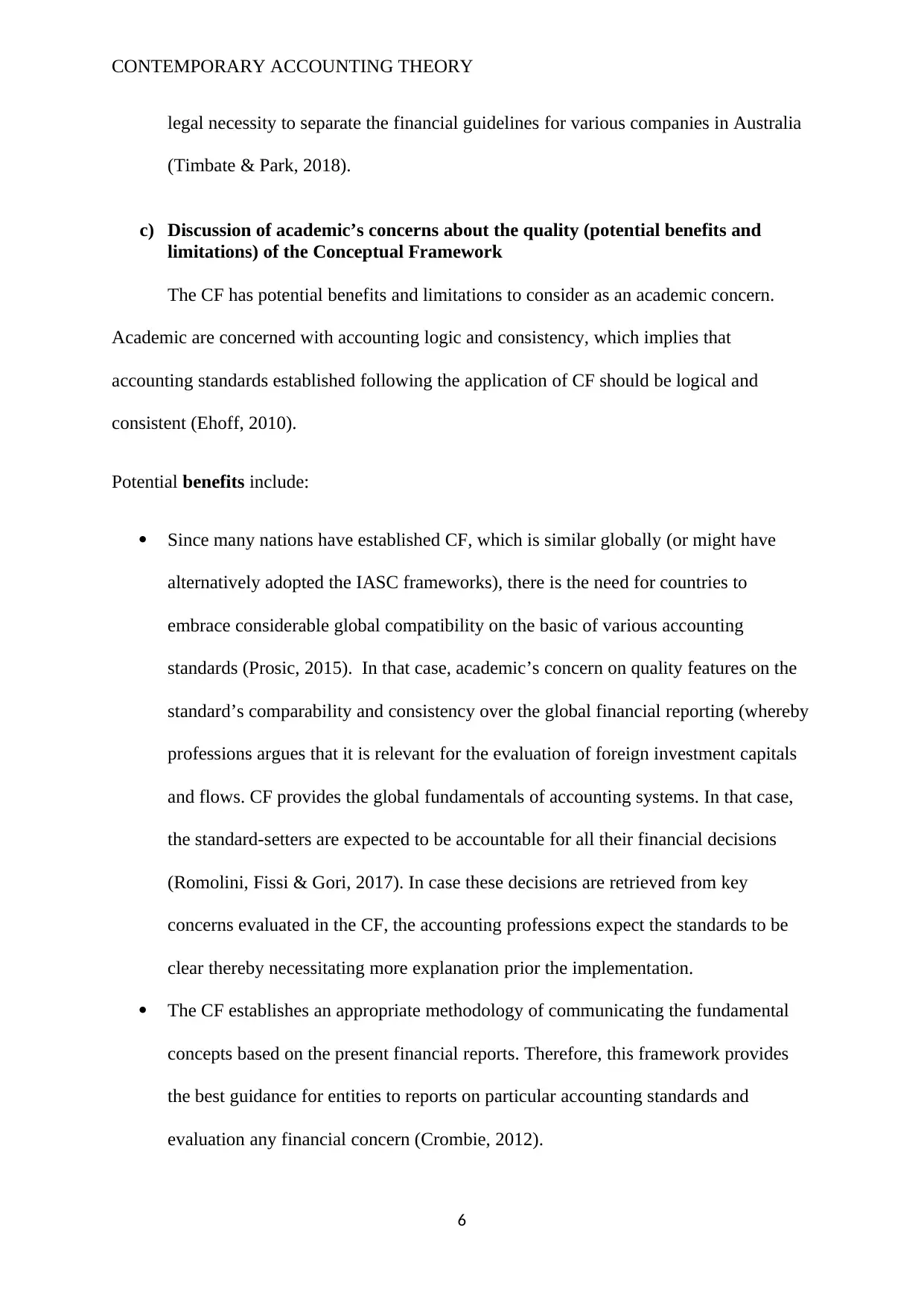

Fig. 1: Consolidate Financial Statement Position of RIO TINTO

Conferring to the Fig. 1 above, the company has prepared 11 financial reports considering

the components in financial reporting based on the CF; the components include: assets,

liabilities, and equity.

Information retrieved from the "Global home" (2019), published in 2018, signify the

obligation of RIO TINTO to prepare its consolidated accounts considering the conceptual

framework under the Australian business laws. The financial reports, especially the 2018

statements disclose the implication of adjusting the company’s consolidated revenues, assets

and liabilities as shown in page 149. The valuations, as organized under the IFRS would

8

necessitate the IFRS version applied in Australia, denoted as the Australian Accounting

Standard (AAS) (Carnevale & Mazzuca, 2012).

ii. Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

The recognition principle and measurement for assets, liabilities and revenue is based on

a criterion that focusses on recognizing if the benefits of sale or sure are likely (Hodge,

Rajgopal & Shevlin, 2009).

Assets: The RIO TINTO recognizes its financial assets by evaluating them into

categories. Thus, the assets are now measured at a fair valuation through

comprehensive income Fair Value through Other Comprehensive Income (FVOCI),

including the one help at an amortised cost. The recognition principle and

measurement for this case depends on the company’s business model that signifies the

management of contractual agreements and financial assets of cash flows. The

management obligation controls the categorization of financial assets upon

recognition. As indicated in Note 30, the company clearly included the relevant

financial risk management frameworks following the recognition of the financial

statements.

Liabilities: All the RIO TINTO’s financial liabilities and borrowings, which include

the trade payables, are recognized based on the principle of fair value and overall

amount of transaction recorded. These valuations are subsequently determined at an

amortized cost. The company also participates in supply chain financial management,

which enables vendors to elect to obtain payments from banks through factoring

receivables from the company. This form of arrangement does not modify the

agreement of initial liability, which imply that financial liabilities from the supply

chain can progressively be recognized under the categorization of trade payables.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revenue: The RIO TINTO recognizes its revenue connected to the transfers of good

and services whenever the products pass to the clients. The valuation of these

revenues denoted reflect the deliberation to which the company is, including its state

it desires to entitle its exchange of products. Revenues are also recognizes under

individual sales whenever control is assigned to the clients. In most cases, the sales

revenues and control passes are recognizes when the goods and services are delivered

to client’s premises.

iii. What qualitative characteristics of information exhibit in company’s various financial

reports?

The qualitative characteristics of information exhibited in company’s various financial

reports include:

Understandability: The RIO TINTO presents its financial statements, which are

readily understandable by its users. The company also ensured to clearly present its

data, including additional information supported by past financial reports and

reference documentation, which aid in clarification.

Relevance: According to Crombie (2012), financial information must be relevant to

users especially when it significantly impact the financial decision of the company’s

users. In that case, the RIO TINTO ensures to report on particular relevant financial

data, or information whose misstatement and omission might have a significant

impact on economic planning of users.

Reliability: Financial information has to be free from bias and material errors. In that

case, the company ensures that the data released is not misleading and faithfully

presented of its financial statements and transactions. The valuation of statements for

this case ensures that information consider underlying events, uncertainties and

estimates in appropriate disclosure.

10

Paraphrase This Document

Comparability: According to Alfiero, Cane, Doronzo & Esposito (2018), an entity’s

information must be comparable to financial data retrieved from other consecutive

financial periods. The RIO TINTO’s users are able to identify the performance trends

of the company since the company considers evaluating the past financial reports

when preparing new reports.

Timeliness: Financial information must be produced within the scheduled time span

(Mostyn, 2012). RIO TINTO’s disclosures are produced in time and not delayed,

since the information is relevant for users to make the necessary decisions about

profitability or sustainability.

4. Part B

a) Comparison of Sustainability Reporting Guidelines and International Integrated

Reporting Framework

There has been a significant inception of the sustainability reporting under the Global

Reporting Initiative (GRI) and the integrated reporting framework under the International

Integrated Reporting Council (IIRC), which can be evident for the aims of corporate social

responsibility of evaluating a company’s financial performance. Nonetheless, it is vital to

note that there are particular difference between the sustainability and integrated reporting as

analysed below:

Sustainability Reporting

The Sustainability Reporting Guideline presents the relevant standards, under the GRI

applicable to the help companies to enhance competitive advantage (Ceulemans, Lozano &

Alonso-Almeida, 2015). Moreover, the component of environmental sustainability in the

guideline is critically recommended for firms to apply the world today. However, this form of

reporting concentrates more on a selected segment of the entity’s status but unable to

11

indicated the specific and relevant climatic transitions and environmental factors (Crombie,

2012). Apart from that sustainability reports do not effectively indicated financial information

relevant for evaluating the opportunities and risks of an entity.

International Integrated Reporting

On the other hand, International Integrated Reporting Framework, under the IIRC,

improves the corporation’s reputation; thus, the profitability of the firm can be evaluated

based on global norms and laws (Messner, 2010). The reporting necessitates investors to

build the relationship with both the accounting and non-accounting data analysts to be able to

effectively evaluate potential risks. Numerous organizations have energetically begun to get

readily integrated reports in different configurations and each report has been shaped as per

the requirements of business properties. Moreover, integrated announcing standards and rules

have been distributed by the Worldwide Integrated Detailing Board, so as to give direction to

report evaluators (Soyka, 2013). With the expanding significance and spread of integrated

detailing, banters about the advantages and issues experienced in the readiness expanded. In

this investigation, the followings are clarified: the terms of monetary announcing,

sustainability analysis, and accounting detailing; the development of these terms; advantages

of integrated revealing and issues that might be experienced while readiness; and the

connection between budgetary announcing and integrated detailing.

b) Rigour (strength & limitations) of the conventional accounting, based upon the

Conceptual Framework for contents of sustainability as well as integrated

reports

Strengths

The Convectional Accounting is a significant tool that is applicable in the management of

businesses today (Graymore, 2014). The conventional accounting, centred on the CF provides

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a firm foundation for formulating future financial statement standards, which enhance the

sustainability status of specific companies (Romolini, Fissi & Gori, 2017).

For integrated reporting, a significant tool is presented that fundamentally enhances the vital

connection between non-financial and financial factors, which determine the performance of

the company. Moreover, this tool determines how businesses formulate their sustainable

valuation to achieve long-term stability. According to Pérez-López, Moreno-Romero, &

Barkemeyer (2013), integrated reporting enables users to effectively understand the manner

in which the company is supposed to address its present and future financial challenges,

including the means in which resources will be utilized.

Sustainability reporting is a vital tool that enables organizations to prepare information

concerning social, economic, environment and governance performance. Therefore,

sustainability reporting does not only report on collected data from past year, but also a

methodology that ensures the internalization of the company’s obligation to assure the

sustainable development aspired by both the internal and external key stakeholders.

Limitations

Debilitated Basic leadership: Convectional accounting offers decision chiefs inefficient data

on an association's specialties. This is on the grounds that the sort of use the planning

procedure tasks is theoretical and isn't solid for settling on specific choices (Ivan, 2018). This

powers chiefs in governments and associations utilizing traditional planning strategies to

change their arrangements regularly, in order to emphasize their selections.

The integrated reporting is limited to the continuous challenge of transitioning the old annual

reports, which has to focus on key financial merits. Moreover, integrated reports have

considered past disclosures connected to the company that again have to be understood by the

13

Paraphrase This Document

users.

Sustainability reports is limited to the major differentiation issues concerned with the

enforcement of the report. This implies that if preserving sustainable reporting is

discretionary, there are no authorities to penalize companies for non-compliance. Moreover, a

company may formulate its unique framework for the purposeful sustainability reporting.

However, no penalties will be imposed in case of misstatements from such companies.

c) Applicability (usefulness of limitations) of the theories to explain contents of

sustainability as well as integrated reports

The Agency theory applies in the evaluation integration reports. During the financial

period recorded in 2017, the Glen Core PLC attained its targeted zero catastrophic

environmental cases Graymore, 2014). In the report the company classifies the severity of

sustainability-centred cased based on five-pointer scales (which read from negligible to

catastrophic). The agency theory is applied in the response to catastrophic events, which such

cases have a significant consequence on financial health of the company.

Secondly the stakeholder theory has been applied by the company to regulate its

activities. According to the sustainability report of the company, national or local policies,

legislations and international guidelines can significantly affect the company’s operations. In

that case, the company focusses on ensuring that there is a constructive connection with the

relevant stakeholders and the government as evident in the company’s integration reports.

This in turn results to the formulation of legislations, which enhance the sustainability of

business (Badiyani, 2012)

The legitimacy theory is also applicable in the sustainability and integrated reports of

the company. Legitimacy is the overall assumption and perception, which signify that the

activities of a company are proper, desirable and appropriate within a social-centred

framework (Ivan, 2018). In the company’s conception, legitimacy theory is applicable in

14

illustrating the conduct of the management in developing and implementing voluntary

environmental and social disclosure of data in ensuring social projects are fulfilled.

d) Preparation of an index (a table or checklist) of various components (criteria) of

an integrated report, and discussion of whether and how the selected South

African Company has disclosed information against each of those components

(criteria)

Table 1: Integrated Reporting Index

Sl. No. Indexes

1 Responsibility of Integrated Report Represents the information of

individuals obliged for governance

2 Strategic focus and future

orientation

Shows the relevant information on

strategies used by the company

3 Stakeholder Relationship Data on the stakeholders engagement

with the company

4 Materiality Information in the company’s material

concerns

5 Organizational Overview and

External environment

Concerns the activities of the company

under the umbrella of operation and

external environment (Faria, 2016)

6 Governance Information concerning the corporate

governance in the business

7 Business model Presents the definition and model of

business operated by the company

8 Risk and Opportunities Information on risk and opportunity in

value creation

Presents the relevant risks and

opportunities critical for value creation

(Graymore, 2014)

9 Performance Data of financial and non-financial

presentation

10 Basic method of preparation and

presentation

Reflect the significant matters that

should be considered in an integrated

report.

According to the Glen Core PLC official website, the company has its integrated reports

considering with principles and guidelines of the IIRC.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to the 1st index, responsibility of integrated report published by the company in

2018, the company has clearly outlined its fundamental purpose of evaluating its financial

statements. The responsibilities of the reports have been presented in accordance to the IIRC,

which strategically outlines its uncertainties and risks that are relevant for assuring the

companies sustainability in the business world. The basic method of preparation and

presentation of the integration reports is meant to signify that the company ensures diversity

in its production, activities, and defining its geographic frameworks clearly.

Moreover, the integrated reports are presented in a manner to ensure that the industrial and

marketing strategies are clearly defines. This ensures that the competitors of the company are

clearly defined hence assuring the stability of the company is also attained for strategic focus

and future orientation in business. Moreover, the component on stakeholder relationship

in an integrated report ensures that the company clearly defines the relationship of

stakeholders with the company. With this, the company’s users are involved in decision-

making, especially in issues related to resource identification, profit maximization, and value

creation. The Glencore PLC, based on the component of materiality, maintain to be the

world’s integrated and diversified producer. In that case, the assessment of materiality is

conducted in every year to establish and clearly define its material.

Organizational Overview and External environment is another critical component in an

integrated report, which clearly defines the company’s overview and environment

considering its competitors. From the integrated report published in 2018, the company has

considered applying the technological steps in undelaying its core strategies to ensure

profitability and sustainability.

The component on governance enables the company to clearly define its operation means

and assets in its geographical location in an integrated report. In the 2018 integrated report,

16

Paraphrase This Document

the company outlines its business model of approach concerning various environments i.e.

economic, political, social, tax and regulatory environments. The environments, according to

Soyka, (2013), may present the risks and opportunities, which might be reflected in an

integrated report. The Glencore PLC takes note of the relevant uncertainties and risks that

have a significant implication in the business, including legal, financial and competitive risks.

The performance component has been presented clearly in the company’s 2018 integrated

report. This component has enabled the Glencore PLC to update its relevant explanations,

which reflect on the present outlook of the company. The performance of the company

outlines its success in ensuring certain uncertainties and risks have been mitigated effectively.

e) Comparison of Australian company’s reporting practices with the index and the

integrated reporting practices in the selected South African Company

In comparison to the corporate governance and performance of the Rio Tinto, based on the

provided index of key components, it is evident that the relative strategies concerning

corporate strategies, operating framework, opportunity analysis, and risk management

required thorough analysis. The annual reports of both companies cover the obligation,

including the financial operation, which have a fundamental control on business processes

(Adams & Simnett, 2011). For instance, the Glen Core PLC report considers the Centurion

corporate management office, Saldanha’s port operation and the marketing segment that the

company operates in.

On the other hand, the business models of the two companies are distinct. Based on the index

of key components (Environment, Socio-Political, Production, Financial Evaluation of Costs,

People, and Health & Safety) in an integrated report, it is evident that the Glen Core PLC

prepares an integrated report, which outlines its core strategies for successful operations.

With this, the company is able to identify its resources of revenues, products and financial

details. The sustainability report of the Rio Tinto, prepared in 2017, was written basically for

17

prospective and current stakeholders, who consider demonstrating that the company has

effective strategies that are capable of delivering and optimizing production value (Adams &

Simnett, 2011). From 2017 until the present, Rio has implemented targeted transitions to the

relevant changes in its accounting strategies to enhance sustainability within its competitive

environment.

The transitional practice has resulted to firm and flexible management and evaluation of the

balance sheet. Considering this foundation, the company can focus of its development of

accounting value for review by its relevant shareholder in a responsible and sustainable

manner (Adams & Simnett, 2011). As indicated throughout the integrated report published in

2017, the company’s management and strategic practices to productivity has been signified

by comprehensive gratitude of critical resources and relationship, which Glen relies to create

its strategic accounting valuation.

Another significant practice evident from the companies is the evaluation of productivity,

which considers evaluating potential outcomes, opportunities and risks in the company’s

operations. The financial outcomes are helpful for the various stakeholders who need this

information to monitor their investment in the company (Adams & Simnett, 2011).

Moreover, the company has also published the sustainability reports and the annual financial

report. The process of financial reporting for the two companies is government by the

requirements and principles in the IFRS and GRI framework based on key components in an

integrated report.

18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. Conclusion

The CF enables the firm’s managers to evaluate their financial health hence assuring

the company’s profitability. The conceptual framework signifies a critical concern in the

financial accounting field, which fundamentally deals with the monitoring and preparation of

audited financial statements. The founding concern of the CF and Integrated Reports is

crucial for key stakeholders and company users to retried data concerning the company’s

profitability. Resultantly, the structure presents the necessary data that can be used as a basis

for financial decision for companies since the information is relevant, applicable and error-

free. Thus, the financial frameworks have enabled the Glen Core PLC and Jupiter Mines to

enable its profitability in the world of accounting.

19

Paraphrase This Document

References

Aasb.gov.au. (2019). Accounting standards. [online] Available at:

https://www.aasb.gov.au/Pronouncements/Current-standards.aspx [Accessed 6 Jun.

2019].

Adams, S., & Simnett, R. (2011). Integrated Reporting: An Opportunity for Australia's Not-

for-Profit Sector. Australian Accounting Review, 21(3), 292-301. doi: 10.1111/j.1835-

2561.2011.00143.x

Alfiero, S., Cane, M., Doronzo, R., & Esposito, A. (2018). Determining characteristics of

boards adopting Integrated Reporting. FINANCIAL REPORTING, 1(2), 37-71. doi:

10.3280/fr2018-002003

Badiyani, B. (2012). Four Critical Issues in Contemporary Accounting. Global Journal For

Research Analysis, 2(2), 1-2. doi: 10.15373/22778160/february2013/1

Carnevale, C., & Mazzuca, M. (2012). Sustainability Reporting and Varieties of

Capitalism. Sustainable Development, 22(6), 361-376. doi: 10.1002/sd.1554

Ceulemans, K., Lozano, R., & Alonso-Almeida, M. (2015). Sustainability Reporting in

Higher Education: Interconnecting the Reporting Process and Organisational Change

Management for Sustainability. Sustainability, 7(7), 8881-8903. doi:

10.3390/su7078881

Crombie, N. (2012). Contemporary Issues in International Corporate

Governance20122Edited by Suzanne Young. Contemporary Issues in International

Corporate Governance. Prahran: Tilde University Press 2009. 228 pp., ISBN: 978‐0‐

7346‐1071‐3. Pacific Accounting Review, 24(1), 104-106. doi:

10.1108/01140581211221588

20

Ehoff, Jr., C. (2010). Notes On Accounting Capstone Course Design: Contemporary Issues

Versus Case Analysis Enhances Student Interest And Learning. Contemporary Issues

In Education Research (CIER), 3(3), 59. doi: 10.19030/cier.v3i3.188

Faria, M. (2016). A New Form of Reporting For Companies. The Integrated

Reporting. International Journal Of Management And Economics Invention, 32(12),

24. doi: 10.18535/ijmei/v2i11.02

Global home. (2019). Retrieved from http://www.riotinto.com/

Graymore, M. (2014). Sustainability Reporting: An Approach to Get the Right Mix of Theory

and Practicality for Local Actors. Sustainability, 6(6), 3145-3170. doi:

10.3390/su6063145

Hodge, F., Rajgopal, S., & Shevlin, T. (2009). Do Managers Value Stock Options and

Restricted Stock Consistent with Economic Theory?. Contemporary Accounting

Research, 26(3), 899-932. doi: 10.1506/car.26.3.11

Ivan, O. (2018). Integrated Reporting in the Context of Corporate Governance. Case study on

the Adoption of Integrated Reporting of Romanian Companies listed on BSE. Valahian

Journal Of Economic Studies, 9(2), 127-138. doi: 10.2478/vjes-2018-0024

Messner, M. (2010). Contemporary Issues in Accounting. European Accounting

Review, 19(1), 191-192. doi: 10.1080/09638181003714622

Molyneux, P., & Wilson, J. (2017). Contemporary issues in banking. The British Accounting

Review, 49(2), 117-120. doi: 10.1016/j.bar.2016.10.004

Mostyn, G. (2012). Cognitive Load Theory: What It Is, Why It's Important for Accounting

Instruction and Research. Issues In Accounting Education, 27(1), 227-245. doi:

10.2308/iace-50099

21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pérez-López, D., Moreno-Romero, A., & Barkemeyer, R. (2013). Exploring the Relationship

between Sustainability Reporting and Sustainability Management Practices. Business

Strategy And The Environment, 24(8), 720-734. doi: 10.1002/bse.1841

Prosic, D. (2015). Integrated reporting: A new approach to corporate reporting and

management. Bankarstvo, 44(4), 62-87. doi: 10.5937/bankarstvo1504062p

Romolini, A., Fissi, S., & Gori, E. (2017). Exploring Integrated Reporting Research: Results

and Perspectives. International Journal Of Accounting And Financial Reporting, 7(1),

12. doi: 10.5296/ijafr.v7i1.10630

Soyka, P. (2013). The International Integrated Reporting Council (IIRC) Integrated Reporting

Framework: Toward Better Sustainability Reporting and (Way) Beyond. Environmental

Quality Management, 23(2), 1-14. doi: 10.1002/tqem.21357

Timbate, L., & Park, C. (2018). CSR Performance, Financial Reporting, and Investors’

Perception on Financial Reporting. Sustainability, 10(2), 522. doi: 10.3390/su10020522

22

Paraphrase This Document

Appendix

List of Abbreviations

Abbreviation Meaning

CF Conceptual Framework

IASB International Accounting Standards Board

FVOCI Fair Value through Other Comprehensive

Income

GRI Global Reporting Initiative

IIRC International Integrated Reporting Council

23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.