Corporate Social Responsibility and Sustainability Reporting: A Case Study of ASX: QUB

VerifiedAdded on 2022/10/01

|16

|4263

|316

AI Summary

This research report analyzes the importance of Corporate Social Responsibility (CSR) and sustainability reporting in enabling a firm to operate within its financial objectives. The report also presents a case study of ASX: QUB, analyzing its history, ownership, governance, and financial performance. The report applies the Institutional and Legitimacy theories to explain the essence of sustainability reporting. The report concludes that CSR plays a significant role in enabling a company to become socially responsible and operate within a strategized financial planning that enables the achievement of the strategized goals and objectives.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ACCOUNTING THEORY 1

ACCT20074 Contemporary Accounting Theory

QUB Research Report

Student’s Name

Institution Affiliation

Date

ACCT20074 Contemporary Accounting Theory

QUB Research Report

Student’s Name

Institution Affiliation

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 2

Executive Summary

The concept of Corporate Social Responsibility (CSR) is an organizational model that

enables companies to regulate its activities, in terms of being socially accountable to the

community and relevant stakeholders. The practice of CSR, which is also referred as corporate

citizenship, makes it possible for firms to impact the community socially, economically and

environmentally. The QUB, an ASX-listed company manages its business in manner that assures

social responsibility, which is focused to engage the holding’s term to enable the production of

quality services to the community within which the company operates. Thus, CSR plays a

significant role in not only enabling a company to become socially responsible, but also to

operate within a strategized financial planning that enables the achievement of the strategized

goals and objectives. A sustainability reporting, with the inclusion of the relevant reporting

concepts, allows the QUB to embrace CSR to the community. The institutional and legitimacy

theories provide the essence of sustainability reporting, which apply to the ASX: QUB in

enabling the logistic firm to evaluate its strategic approach that assure long-term availability of

services to customers.

Executive Summary

The concept of Corporate Social Responsibility (CSR) is an organizational model that

enables companies to regulate its activities, in terms of being socially accountable to the

community and relevant stakeholders. The practice of CSR, which is also referred as corporate

citizenship, makes it possible for firms to impact the community socially, economically and

environmentally. The QUB, an ASX-listed company manages its business in manner that assures

social responsibility, which is focused to engage the holding’s term to enable the production of

quality services to the community within which the company operates. Thus, CSR plays a

significant role in not only enabling a company to become socially responsible, but also to

operate within a strategized financial planning that enables the achievement of the strategized

goals and objectives. A sustainability reporting, with the inclusion of the relevant reporting

concepts, allows the QUB to embrace CSR to the community. The institutional and legitimacy

theories provide the essence of sustainability reporting, which apply to the ASX: QUB in

enabling the logistic firm to evaluate its strategic approach that assure long-term availability of

services to customers.

CONTEMPORARY ACCOUNTING THEORY 3

Introduction

The ASX: QUB is committed to managing its business in a responsible and safe manner.

This corporate social responsibility enables the company to ensure that its team is engaged,

diverse and empowered to provide quality services to its potential customers and community

within which the holding operates. This research report is divided into two sections (parts A and

B). In the first part, a critical literature review of the importance of Corporate Social

Responsibility (CSR) in enabling a firm to operate within its financial objectives is provided.

Part A also elaborates if sustainability reporting, in consideration to the relevant reporting

concepts represent a holistic view of corporate social responsibility. Moreover, part A identifies

and explains two relevant theories that explain the essence of sustainability reporting. In part B,

the ASX: QUB is analyzed, in reference to its history, ownership, governance and financial

performance. In this section, a sustainability reporting scoring index, in reference to the Global

Reporting Initiative (GRI) rules is presented. The reporting also examines the quality and extent

of the ASX: QUB according to the scoring index.

Part A: Theoretical Knowledge

Literature Review of the Importance of Corporate Social Responsibility

The importance of Corporate Social Responsibility (CSR), in reference to the vitality of

enabling firms to achieve their financial objectives, has been postulated for decades now.

According to research done by Bellantuono, Pontrandolfo & Scozzi (2016), CSR is fundamental

in enabling a company to enhance its Corporate Financial Performance (CFP) and to be

competitive in any market. In that case, there are a lot of competing theories that purpose to

develop a significant explanation of the varied connections between the CSR and CFP. When a

Introduction

The ASX: QUB is committed to managing its business in a responsible and safe manner.

This corporate social responsibility enables the company to ensure that its team is engaged,

diverse and empowered to provide quality services to its potential customers and community

within which the holding operates. This research report is divided into two sections (parts A and

B). In the first part, a critical literature review of the importance of Corporate Social

Responsibility (CSR) in enabling a firm to operate within its financial objectives is provided.

Part A also elaborates if sustainability reporting, in consideration to the relevant reporting

concepts represent a holistic view of corporate social responsibility. Moreover, part A identifies

and explains two relevant theories that explain the essence of sustainability reporting. In part B,

the ASX: QUB is analyzed, in reference to its history, ownership, governance and financial

performance. In this section, a sustainability reporting scoring index, in reference to the Global

Reporting Initiative (GRI) rules is presented. The reporting also examines the quality and extent

of the ASX: QUB according to the scoring index.

Part A: Theoretical Knowledge

Literature Review of the Importance of Corporate Social Responsibility

The importance of Corporate Social Responsibility (CSR), in reference to the vitality of

enabling firms to achieve their financial objectives, has been postulated for decades now.

According to research done by Bellantuono, Pontrandolfo & Scozzi (2016), CSR is fundamental

in enabling a company to enhance its Corporate Financial Performance (CFP) and to be

competitive in any market. In that case, there are a lot of competing theories that purpose to

develop a significant explanation of the varied connections between the CSR and CFP. When a

CONTEMPORARY ACCOUNTING THEORY 4

specific company can be evaluated based on these varied connections, theories linking the CSR

and CFP can be used to explain the varied connections between the two concepts.

The ideology of CSR enables a firm to become morally accountable to the community

within which it operates. Moreover, the concepts forces companies to go beyond attaining their

own goals or making profits with the involvement of their key partners and relevant stakeholders

(Biondi, L., & Bracci, 2018). As presented by Carnevale & Mazzuca (2012), companies should

embrace the idea of becoming socially accountable for practical and moral reasons, which are

acted upon using a socially accountable posture that allows firms to boost their financial

performance in a competitive market. In that case, all the activities that purpose to bring out the

concept of CSR can the availed by competent workers, recognized companies reputation,

enhanced financial markets and satisfied clients. All these assure a company of boosting its

financial performance, which also guarantees sustainability.

Nonetheless, social obligations significantly involve some financial burdens that can

potentially affect the company’s profits and its comparative corporate performances. In that case,

various have presented the trade-off hypothesis that provides an explanation of the negative

connection between financial performances of a company and CSR (Ceulemans, Lozano &

Alonso-Almeida, 2015). With this linkage assumption, firms are able to display effective social

credentials experience that decline the stock prices in reference to what the market recommends

as an average. According to Stacchezzini, Melloni & Lai (2016), the concept of CSR is

applicable as an organizational strategy that contributes to the frameworks that boost the

competitive advantage of a given firm. An analysis by Loh, Thomas & Wang (2017), concerns

the implications of CSR of the company’s competiveness and shows that CSR should not be

considered as an ‘adventure’ for a firm’s management board. However, the concept can be

specific company can be evaluated based on these varied connections, theories linking the CSR

and CFP can be used to explain the varied connections between the two concepts.

The ideology of CSR enables a firm to become morally accountable to the community

within which it operates. Moreover, the concepts forces companies to go beyond attaining their

own goals or making profits with the involvement of their key partners and relevant stakeholders

(Biondi, L., & Bracci, 2018). As presented by Carnevale & Mazzuca (2012), companies should

embrace the idea of becoming socially accountable for practical and moral reasons, which are

acted upon using a socially accountable posture that allows firms to boost their financial

performance in a competitive market. In that case, all the activities that purpose to bring out the

concept of CSR can the availed by competent workers, recognized companies reputation,

enhanced financial markets and satisfied clients. All these assure a company of boosting its

financial performance, which also guarantees sustainability.

Nonetheless, social obligations significantly involve some financial burdens that can

potentially affect the company’s profits and its comparative corporate performances. In that case,

various have presented the trade-off hypothesis that provides an explanation of the negative

connection between financial performances of a company and CSR (Ceulemans, Lozano &

Alonso-Almeida, 2015). With this linkage assumption, firms are able to display effective social

credentials experience that decline the stock prices in reference to what the market recommends

as an average. According to Stacchezzini, Melloni & Lai (2016), the concept of CSR is

applicable as an organizational strategy that contributes to the frameworks that boost the

competitive advantage of a given firm. An analysis by Loh, Thomas & Wang (2017), concerns

the implications of CSR of the company’s competiveness and shows that CSR should not be

considered as an ‘adventure’ for a firm’s management board. However, the concept can be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 5

regarded as a strategy that can be used to attain corporate strategies, which might cause a

negative impact on the firm’s competitive advantage if not properly implemented.

According to Timbate & Park (2018), competitive advantage presents companies with the

capacity to outperform their competitors with effective differentiation from various strategic

rival actions. The connection between the firms’ internal resources and the external environment

result in positive financial results according to proven key performance indicators. In that case,

the strategic application of social accountability is beneficial to the company since it enhances

client loyalty, future income, quality products, new potential markets and productivity channels.

Generally, CSR is important since it is the main source that assures a firm of establishing

completive advantage in the market. Organizational contributions to CSR can be viewed by

financial analysts as an investment strategy that is enjoyed or consumed by individuals, with

reference to cost sharing (Soyka, 2013). In that case, firms should consider investing in CSR,

despite the cost, since it advantageous when it comes to boosting a company’s financial

performance.

Sustainability Reporting in View of Corporate Social Responsibility

When the concept of CSR is properly incorporated in a company, there are a lot of

benefits that can be realized. According to Pérez-López, Moreno-Romero & Barkemeyer (2013),

embracing CSR enables a firm to increase its value to the company’s key stakeholders, in

addition to boosting customer loyalty, credibility, boosting market shares and enhancing

sustainability growth. In the view of CSR, sustainability reporting considers fours four

fundamental components: legal, economic, philanthropic and ethical accountability, which allow

a firm to meets all its obligations to the community where the company it situated (Sutopo, Kot,

Adiati & Ardila, 2018). The essence of CSR is considered in the balancing of various

regarded as a strategy that can be used to attain corporate strategies, which might cause a

negative impact on the firm’s competitive advantage if not properly implemented.

According to Timbate & Park (2018), competitive advantage presents companies with the

capacity to outperform their competitors with effective differentiation from various strategic

rival actions. The connection between the firms’ internal resources and the external environment

result in positive financial results according to proven key performance indicators. In that case,

the strategic application of social accountability is beneficial to the company since it enhances

client loyalty, future income, quality products, new potential markets and productivity channels.

Generally, CSR is important since it is the main source that assures a firm of establishing

completive advantage in the market. Organizational contributions to CSR can be viewed by

financial analysts as an investment strategy that is enjoyed or consumed by individuals, with

reference to cost sharing (Soyka, 2013). In that case, firms should consider investing in CSR,

despite the cost, since it advantageous when it comes to boosting a company’s financial

performance.

Sustainability Reporting in View of Corporate Social Responsibility

When the concept of CSR is properly incorporated in a company, there are a lot of

benefits that can be realized. According to Pérez-López, Moreno-Romero & Barkemeyer (2013),

embracing CSR enables a firm to increase its value to the company’s key stakeholders, in

addition to boosting customer loyalty, credibility, boosting market shares and enhancing

sustainability growth. In the view of CSR, sustainability reporting considers fours four

fundamental components: legal, economic, philanthropic and ethical accountability, which allow

a firm to meets all its obligations to the community where the company it situated (Sutopo, Kot,

Adiati & Ardila, 2018). The essence of CSR is considered in the balancing of various

CONTEMPORARY ACCOUNTING THEORY 6

stakeholders’ interests, which is purposed to meet their individual needs whereas putting aside

any possible negative environmental implications in the general community. In that regard, the

success of a firm’s business is never considered in terms of its economic indicators only, but also

its approach based on social performance and environmental indicators that avails the necessity

to expand the present model of sustainability reporting.

Sustainability reporting, as a significant element of CSR in the global, has been embraced

for decades now. Under the influence of the EU financial directives, sustainability reporting has

been termed significant from the 20th century in Europe (Loprevite, Ricca & Rupo, 2018). The

introduction of global institutions and organization in competitive fields, such as IFAC, LASB

and IOSCO, has resulted from the necessity to launch an effective and efficient system that

makes it possible for companies to evaluate their finances in the present-day business

environment. In Australia, the major regulations concerning sustainability reporting frameworks

are preceded in accounting and auditing laws. These guidelines are applicable in the fields to

financial reporting of all the ASX-listed companies based on International Accounting Standards

(IASs). Generally, by enabling auditing and accounting laws to take action, Australia accepted

the direct application of International Accounting Standards. On global perspective, Serbia

accepted the application of the guidelines in 2003, whereby companies were presented with the

required to apply the relevant IASs (Maj, 2018). However, the auditing and accounting laws of

2006 excluded minor companies from the necessity of applying the IASs. However, the laws

reviewed in 2013 narrowed the group companies, which reflectively obliged major entities and

ASX-listed companies to apply IFRS.

stakeholders’ interests, which is purposed to meet their individual needs whereas putting aside

any possible negative environmental implications in the general community. In that regard, the

success of a firm’s business is never considered in terms of its economic indicators only, but also

its approach based on social performance and environmental indicators that avails the necessity

to expand the present model of sustainability reporting.

Sustainability reporting, as a significant element of CSR in the global, has been embraced

for decades now. Under the influence of the EU financial directives, sustainability reporting has

been termed significant from the 20th century in Europe (Loprevite, Ricca & Rupo, 2018). The

introduction of global institutions and organization in competitive fields, such as IFAC, LASB

and IOSCO, has resulted from the necessity to launch an effective and efficient system that

makes it possible for companies to evaluate their finances in the present-day business

environment. In Australia, the major regulations concerning sustainability reporting frameworks

are preceded in accounting and auditing laws. These guidelines are applicable in the fields to

financial reporting of all the ASX-listed companies based on International Accounting Standards

(IASs). Generally, by enabling auditing and accounting laws to take action, Australia accepted

the direct application of International Accounting Standards. On global perspective, Serbia

accepted the application of the guidelines in 2003, whereby companies were presented with the

required to apply the relevant IASs (Maj, 2018). However, the auditing and accounting laws of

2006 excluded minor companies from the necessity of applying the IASs. However, the laws

reviewed in 2013 narrowed the group companies, which reflectively obliged major entities and

ASX-listed companies to apply IFRS.

CONTEMPORARY ACCOUNTING THEORY 7

Theories Explaining the Essence of Sustainability Reporting

Two theories: Institutional and Legitimacy explain the essence of sustainability reporting in

Australian companies. The Institutional Theory (IT), according to Graymore (2014), considered

companies to be in a closed system that makes them depend on themselves, which terms their

existence in an institutional environment. However, following the acceptance of the institutional

environment for rims, the IT attain a preeminent rule that enabled companies to comprehend the

present phenomenon in the evaluating the sustainability of their business (Wang, 2017). In that

case, IT has been applied in the analysis and study of accounting practices in a firm. Through the

evaluation of the key reasons for adopting the relevant accounting practices, the factors

influencing social choices can be realized. The key indicator of IT is that companies operate

within a social framework, which allows corporate practices to be investigated based on the

application of social norms and rules of acceptable behaviors in the community within which a

company operates (Kim, Shin, Shin & Park, 2019). Resultantly, social reality is considered as a

tile of social conduct. Firms focus on institutional pressure for transition due to the necessity to

boost their sustainability, legitimacy, survival tactics and resources.

On the other hand, the Legitimacy Theory (LT) is termed as an explanatory framework that

enables firms to protect and manage their image. The LT process is related to the IT since it

recommends that institutionalization of the relevant normative ethics is an incorporated social

framework for corporate behaviors of firms. Gavana, Gottardo & Moisello (2016) argue that the

compliance with norms created by institutions, established for significant period of time, leads to

the establishment of institutional legitimacy. The LT process is obliged to boost the legitimacy of

the present social ethical system. These analysts evaluate, in their analysis, various individuals

who have applied the LT in the attempt to elaborate the concern behind voluntary firms’

Theories Explaining the Essence of Sustainability Reporting

Two theories: Institutional and Legitimacy explain the essence of sustainability reporting in

Australian companies. The Institutional Theory (IT), according to Graymore (2014), considered

companies to be in a closed system that makes them depend on themselves, which terms their

existence in an institutional environment. However, following the acceptance of the institutional

environment for rims, the IT attain a preeminent rule that enabled companies to comprehend the

present phenomenon in the evaluating the sustainability of their business (Wang, 2017). In that

case, IT has been applied in the analysis and study of accounting practices in a firm. Through the

evaluation of the key reasons for adopting the relevant accounting practices, the factors

influencing social choices can be realized. The key indicator of IT is that companies operate

within a social framework, which allows corporate practices to be investigated based on the

application of social norms and rules of acceptable behaviors in the community within which a

company operates (Kim, Shin, Shin & Park, 2019). Resultantly, social reality is considered as a

tile of social conduct. Firms focus on institutional pressure for transition due to the necessity to

boost their sustainability, legitimacy, survival tactics and resources.

On the other hand, the Legitimacy Theory (LT) is termed as an explanatory framework that

enables firms to protect and manage their image. The LT process is related to the IT since it

recommends that institutionalization of the relevant normative ethics is an incorporated social

framework for corporate behaviors of firms. Gavana, Gottardo & Moisello (2016) argue that the

compliance with norms created by institutions, established for significant period of time, leads to

the establishment of institutional legitimacy. The LT process is obliged to boost the legitimacy of

the present social ethical system. These analysts evaluate, in their analysis, various individuals

who have applied the LT in the attempt to elaborate the concern behind voluntary firms’

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 8

disclosures. In their analysis, it is evident that the LT allows firms to progressively assure that

they’ve operated within the community limits and norms. In that regard, a social agreement is

evident between the individuals and companies affected by a firm’s operations (Capaldi, 2016).

Moreover, conformity with the relevant social connections put more emphasis on the social

legitimacy of firms, which convince the general public of the importance of enhancing and

supporting survival perspectives.

Part B: Application of Theoretical Knowledge to Explain Reporting Practices

QUB History, Ownership, Governance and Financial Performance

The Qube Holdings Ltd (QUB) is a recognized infrastructure and logistic company

situated in Australia. The company was established in 2010 following the KFM Diversified

Infrastructure and Logistics Fund acquiring the Kaplan Equity and rebranding to QUB. After the

acquisition, the holding became a standard operating from before being branded as the Qube

Logistics. QUB’s governance is focused on establishing systems, synergies and frameworks in

the entire firm to establishing common goals. As for financial performance, the QUB attains an

average of 1.7% of daily earnings for the time recorded and ended on 31st December, 2018. The

financial performance of the QUB is evaluated based on five organizational units: Bulk, Ports,

property, Strategic Assets and Infrastructure. With reference to the units, four points can be

obtained to signify the financial performance of the company. These are:

Statutory income, which increased 5% to $837 million

Statutory EBITDA boosted 20.2% to $93 million

Statutory NPAT went up 36% to $61million

Statutory EPS amortization gone up 30% to 4.3% per share.

disclosures. In their analysis, it is evident that the LT allows firms to progressively assure that

they’ve operated within the community limits and norms. In that regard, a social agreement is

evident between the individuals and companies affected by a firm’s operations (Capaldi, 2016).

Moreover, conformity with the relevant social connections put more emphasis on the social

legitimacy of firms, which convince the general public of the importance of enhancing and

supporting survival perspectives.

Part B: Application of Theoretical Knowledge to Explain Reporting Practices

QUB History, Ownership, Governance and Financial Performance

The Qube Holdings Ltd (QUB) is a recognized infrastructure and logistic company

situated in Australia. The company was established in 2010 following the KFM Diversified

Infrastructure and Logistics Fund acquiring the Kaplan Equity and rebranding to QUB. After the

acquisition, the holding became a standard operating from before being branded as the Qube

Logistics. QUB’s governance is focused on establishing systems, synergies and frameworks in

the entire firm to establishing common goals. As for financial performance, the QUB attains an

average of 1.7% of daily earnings for the time recorded and ended on 31st December, 2018. The

financial performance of the QUB is evaluated based on five organizational units: Bulk, Ports,

property, Strategic Assets and Infrastructure. With reference to the units, four points can be

obtained to signify the financial performance of the company. These are:

Statutory income, which increased 5% to $837 million

Statutory EBITDA boosted 20.2% to $93 million

Statutory NPAT went up 36% to $61million

Statutory EPS amortization gone up 30% to 4.3% per share.

CONTEMPORARY ACCOUNTING THEORY 9

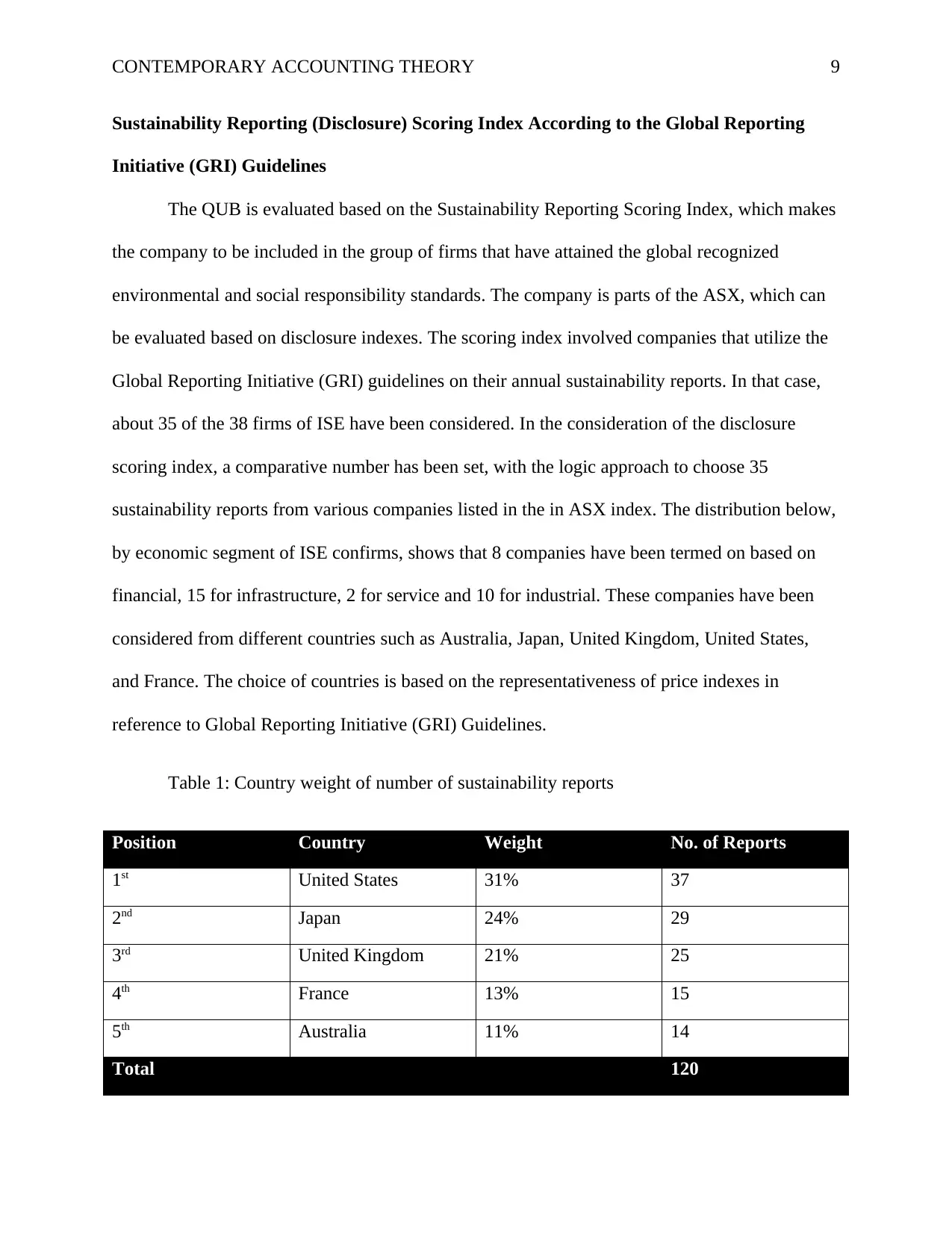

Sustainability Reporting (Disclosure) Scoring Index According to the Global Reporting

Initiative (GRI) Guidelines

The QUB is evaluated based on the Sustainability Reporting Scoring Index, which makes

the company to be included in the group of firms that have attained the global recognized

environmental and social responsibility standards. The company is parts of the ASX, which can

be evaluated based on disclosure indexes. The scoring index involved companies that utilize the

Global Reporting Initiative (GRI) guidelines on their annual sustainability reports. In that case,

about 35 of the 38 firms of ISE have been considered. In the consideration of the disclosure

scoring index, a comparative number has been set, with the logic approach to choose 35

sustainability reports from various companies listed in the in ASX index. The distribution below,

by economic segment of ISE confirms, shows that 8 companies have been termed on based on

financial, 15 for infrastructure, 2 for service and 10 for industrial. These companies have been

considered from different countries such as Australia, Japan, United Kingdom, United States,

and France. The choice of countries is based on the representativeness of price indexes in

reference to Global Reporting Initiative (GRI) Guidelines.

Table 1: Country weight of number of sustainability reports

Position Country Weight No. of Reports

1st United States 31% 37

2nd Japan 24% 29

3rd United Kingdom 21% 25

4th France 13% 15

5th Australia 11% 14

Total 120

Sustainability Reporting (Disclosure) Scoring Index According to the Global Reporting

Initiative (GRI) Guidelines

The QUB is evaluated based on the Sustainability Reporting Scoring Index, which makes

the company to be included in the group of firms that have attained the global recognized

environmental and social responsibility standards. The company is parts of the ASX, which can

be evaluated based on disclosure indexes. The scoring index involved companies that utilize the

Global Reporting Initiative (GRI) guidelines on their annual sustainability reports. In that case,

about 35 of the 38 firms of ISE have been considered. In the consideration of the disclosure

scoring index, a comparative number has been set, with the logic approach to choose 35

sustainability reports from various companies listed in the in ASX index. The distribution below,

by economic segment of ISE confirms, shows that 8 companies have been termed on based on

financial, 15 for infrastructure, 2 for service and 10 for industrial. These companies have been

considered from different countries such as Australia, Japan, United Kingdom, United States,

and France. The choice of countries is based on the representativeness of price indexes in

reference to Global Reporting Initiative (GRI) Guidelines.

Table 1: Country weight of number of sustainability reports

Position Country Weight No. of Reports

1st United States 31% 37

2nd Japan 24% 29

3rd United Kingdom 21% 25

4th France 13% 15

5th Australia 11% 14

Total 120

CONTEMPORARY ACCOUNTING THEORY 10

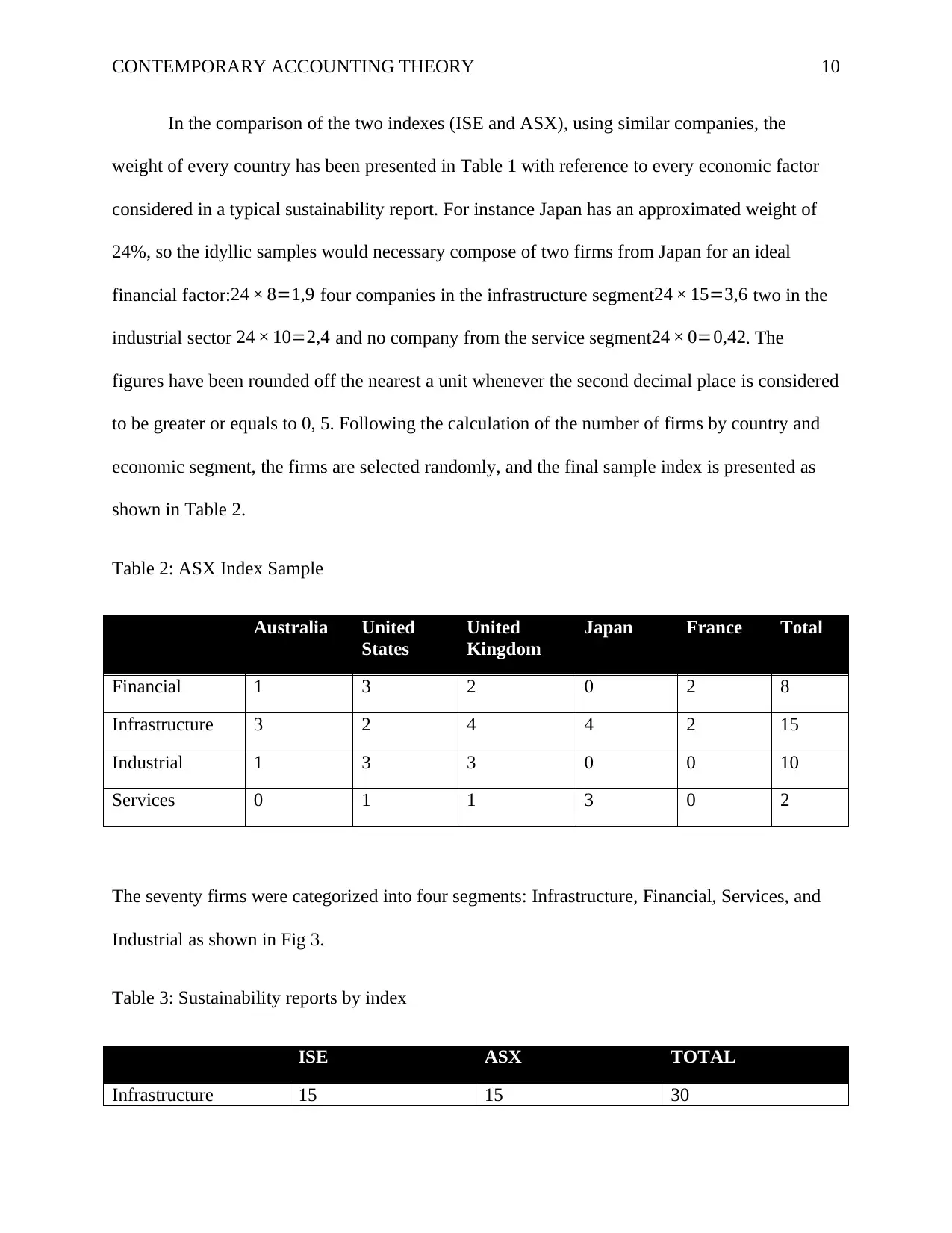

In the comparison of the two indexes (ISE and ASX), using similar companies, the

weight of every country has been presented in Table 1 with reference to every economic factor

considered in a typical sustainability report. For instance Japan has an approximated weight of

24%, so the idyllic samples would necessary compose of two firms from Japan for an ideal

financial factor:24 × 8=1,9 four companies in the infrastructure segment 24 × 15=3,6 two in the

industrial sector 24 × 10=2,4 and no company from the service segment 24 × 0=0,42. The

figures have been rounded off the nearest a unit whenever the second decimal place is considered

to be greater or equals to 0, 5. Following the calculation of the number of firms by country and

economic segment, the firms are selected randomly, and the final sample index is presented as

shown in Table 2.

Table 2: ASX Index Sample

Australia United

States

United

Kingdom

Japan France Total

Financial 1 3 2 0 2 8

Infrastructure 3 2 4 4 2 15

Industrial 1 3 3 0 0 10

Services 0 1 1 3 0 2

The seventy firms were categorized into four segments: Infrastructure, Financial, Services, and

Industrial as shown in Fig 3.

Table 3: Sustainability reports by index

ISE ASX TOTAL

Infrastructure 15 15 30

In the comparison of the two indexes (ISE and ASX), using similar companies, the

weight of every country has been presented in Table 1 with reference to every economic factor

considered in a typical sustainability report. For instance Japan has an approximated weight of

24%, so the idyllic samples would necessary compose of two firms from Japan for an ideal

financial factor:24 × 8=1,9 four companies in the infrastructure segment 24 × 15=3,6 two in the

industrial sector 24 × 10=2,4 and no company from the service segment 24 × 0=0,42. The

figures have been rounded off the nearest a unit whenever the second decimal place is considered

to be greater or equals to 0, 5. Following the calculation of the number of firms by country and

economic segment, the firms are selected randomly, and the final sample index is presented as

shown in Table 2.

Table 2: ASX Index Sample

Australia United

States

United

Kingdom

Japan France Total

Financial 1 3 2 0 2 8

Infrastructure 3 2 4 4 2 15

Industrial 1 3 3 0 0 10

Services 0 1 1 3 0 2

The seventy firms were categorized into four segments: Infrastructure, Financial, Services, and

Industrial as shown in Fig 3.

Table 3: Sustainability reports by index

ISE ASX TOTAL

Infrastructure 15 15 30

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONTEMPORARY ACCOUNTING THEORY 11

Financial 8 8 16

Services 2 2 4

Industrial 10 10 20

Total 35 35 70

The Extent and Quality of Sustainability Reporting of the QUB against the Sustainability

Reporting (Disclosure) Scoring Index Above

Financial:

As for the financial indicator of the QUB, the company has expects NPATA for the

2H19, which is fundamentally greater compared to the period recorded in 2018. However, the

recording it likely to be lower compared to the financial result 1H19. This financial recording is

focused due to expected slowdowns in the volume growth of containers; include the seasonality

of organizational activities. The company’s financial year 2019 guide has not changed in the

sustainability report (Fordham & Robinson, 2018). However, cube still purposes to achieve a

significant growth in the net earnings and revenue from the respective operational divisions. The

main sectors of growth for the 1H19 are recorded from property division and infrastructure,

which underlie total revenue of 10%.

Industrial:

The QUB is committed to developing its industrial works, whereas minimizing its

environmental impacts through the use of infrastructure and technology, which monitor, reduce

and manage emissions during the undertaking of industrial activities. The company’s contractors

Financial 8 8 16

Services 2 2 4

Industrial 10 10 20

Total 35 35 70

The Extent and Quality of Sustainability Reporting of the QUB against the Sustainability

Reporting (Disclosure) Scoring Index Above

Financial:

As for the financial indicator of the QUB, the company has expects NPATA for the

2H19, which is fundamentally greater compared to the period recorded in 2018. However, the

recording it likely to be lower compared to the financial result 1H19. This financial recording is

focused due to expected slowdowns in the volume growth of containers; include the seasonality

of organizational activities. The company’s financial year 2019 guide has not changed in the

sustainability report (Fordham & Robinson, 2018). However, cube still purposes to achieve a

significant growth in the net earnings and revenue from the respective operational divisions. The

main sectors of growth for the 1H19 are recorded from property division and infrastructure,

which underlie total revenue of 10%.

Industrial:

The QUB is committed to developing its industrial works, whereas minimizing its

environmental impacts through the use of infrastructure and technology, which monitor, reduce

and manage emissions during the undertaking of industrial activities. The company’s contractors

CONTEMPORARY ACCOUNTING THEORY 12

and suppliers are also committed to boosting the environmental in a manner that embraces a

sustainable approach to develop the application of assets in the entire business (Harjoto, 2017).

The QUB workforce is determine to launch and apply innovative measures for the purpose of

optimizing assets and developing processes that are meant to enhance efficiency, operations,

safety and environmental outcomes during industrial operations (Herbas, Frank & Arandia,

2018). Some of the initiatives that assure sustainable approach include: the change of volume

from road to rail, which is focused to reduce the trucks on roads. The main focus for this is to

enable a long-lasting sustainability approach.

Infrastructure:

The QUB is focused on developing its infrastructure activities, like the Moorebank Logistic

Park, which is purposed to deliver sustainable construction activities, and materials used to

manage various infrastructure activities. The purpose for this is to minimize the resource

consumption and optimizing the efficiency of resources in minimizing its impact to the

environment (Ross, 2017). This is attained through the application of alternative materials that

have lower embodied emission content. Favorable re-application of waste produce emitted from

demolition of on-site structures is another key alternative that lowers the emission of harmful

products to the environment.

Services:

The QUB offers its services in the strategic manners, which makes the company to be

Australia’s leading logistic firm in the importation and exportation of supply chains. The

program of the services enables the company to develop a sustainable approach that assures the

safety of its customers, not only enhancing financial performance. Therefore the company

and suppliers are also committed to boosting the environmental in a manner that embraces a

sustainable approach to develop the application of assets in the entire business (Harjoto, 2017).

The QUB workforce is determine to launch and apply innovative measures for the purpose of

optimizing assets and developing processes that are meant to enhance efficiency, operations,

safety and environmental outcomes during industrial operations (Herbas, Frank & Arandia,

2018). Some of the initiatives that assure sustainable approach include: the change of volume

from road to rail, which is focused to reduce the trucks on roads. The main focus for this is to

enable a long-lasting sustainability approach.

Infrastructure:

The QUB is focused on developing its infrastructure activities, like the Moorebank Logistic

Park, which is purposed to deliver sustainable construction activities, and materials used to

manage various infrastructure activities. The purpose for this is to minimize the resource

consumption and optimizing the efficiency of resources in minimizing its impact to the

environment (Ross, 2017). This is attained through the application of alternative materials that

have lower embodied emission content. Favorable re-application of waste produce emitted from

demolition of on-site structures is another key alternative that lowers the emission of harmful

products to the environment.

Services:

The QUB offers its services in the strategic manners, which makes the company to be

Australia’s leading logistic firm in the importation and exportation of supply chains. The

program of the services enables the company to develop a sustainable approach that assures the

safety of its customers, not only enhancing financial performance. Therefore the company

CONTEMPORARY ACCOUNTING THEORY 13

continues to invest in its community, by applying key strategic programs and initiatives like

creating an environment where customers see various career chances by internal promotion and

to management and supervisor roles. Moreover, the company continues to develop and enhance

its online professional development framework via consistent application over various divisions

in performance organization delivery systems.

Conclusion

In conclusion, CSR is a strategic concept that allows companies to employ philanthropy

and programs used to enhance accountability in the community within which a firm operates.

Just like CSR is important for the society, this concept has a significant impact on the firm’s

financial performance. Activities involved in demonstrating CSR are useful in developing the

strategic bond between the company and its employees, which boosts the morale of workers to

work towards achieving the company’s strategic plans. CSR is important since it is the main

source that assures a firm of inaugurating completive advantage in the market. Organizational

contributions to CSR can be viewed by financial analysts as an investment strategy that is

enjoyed or consumed by individuals, with reference to cost-sharing. In that case, firms should

consider investing in CSR, despite the cost, since it advantageous when it comes to boosting a

corporation’s financial performance.

continues to invest in its community, by applying key strategic programs and initiatives like

creating an environment where customers see various career chances by internal promotion and

to management and supervisor roles. Moreover, the company continues to develop and enhance

its online professional development framework via consistent application over various divisions

in performance organization delivery systems.

Conclusion

In conclusion, CSR is a strategic concept that allows companies to employ philanthropy

and programs used to enhance accountability in the community within which a firm operates.

Just like CSR is important for the society, this concept has a significant impact on the firm’s

financial performance. Activities involved in demonstrating CSR are useful in developing the

strategic bond between the company and its employees, which boosts the morale of workers to

work towards achieving the company’s strategic plans. CSR is important since it is the main

source that assures a firm of inaugurating completive advantage in the market. Organizational

contributions to CSR can be viewed by financial analysts as an investment strategy that is

enjoyed or consumed by individuals, with reference to cost-sharing. In that case, firms should

consider investing in CSR, despite the cost, since it advantageous when it comes to boosting a

corporation’s financial performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTEMPORARY ACCOUNTING THEORY 14

References

Bellantuono, N., Pontrandolfo, P., & Scozzi, B. (2016). Capturing the Stakeholders’ View in

Sustainability Reporting: A Novel Approach. Sustainability, 8(4), 379. doi:

10.3390/su8040379

Biondi, L., & Bracci, E. (2018). Sustainability, Popular and Integrated Reporting in the Public

Sector: A Fad and Fashion Perspective. Sustainability, 10(9), 3112. doi:

10.3390/su10093112

Capaldi, N. (2016). New (Other?) Directions in Corporate Social Responsibility. International

Journal Of Corporate Social Responsibility, 1(1). doi: 10.1186/s40991-016-0005-5

Carnevale, C., & Mazzuca, M. (2012). Sustainability Reporting and Varieties of Capitalism.

Sustainable Development, 22(6), 361-376. doi: 10.1002/sd.1554

Ceulemans, K., Lozano, R., & Alonso-Almeida, M. (2015). Sustainability Reporting in Higher

Education: Interconnecting the Reporting Process and Organisational Change

Management for Sustainability. Sustainability, 7(7), 8881-8903. doi:

10.3390/su7078881

Fordham, A., & Robinson, G. (2018). Mapping meanings of corporate social responsibility – an

Australian case study. International Journal Of Corporate Social Responsibility, 3(1).

doi: 10.1186/s40991-018-0036-1

Gavana, G., Gottardo, P., & Moisello, A. (2016). Sustainability Reporting in Family Firms: A

Panel Data Analysis. Sustainability, 9(1), 38. doi: 10.3390/su9010038

Graymore, M. (2014). Sustainability Reporting: An Approach to Get the Right Mix of Theory

and Practicality for Local Actors. Sustainability, 6(6), 3145-3170. doi:

10.3390/su6063145

References

Bellantuono, N., Pontrandolfo, P., & Scozzi, B. (2016). Capturing the Stakeholders’ View in

Sustainability Reporting: A Novel Approach. Sustainability, 8(4), 379. doi:

10.3390/su8040379

Biondi, L., & Bracci, E. (2018). Sustainability, Popular and Integrated Reporting in the Public

Sector: A Fad and Fashion Perspective. Sustainability, 10(9), 3112. doi:

10.3390/su10093112

Capaldi, N. (2016). New (Other?) Directions in Corporate Social Responsibility. International

Journal Of Corporate Social Responsibility, 1(1). doi: 10.1186/s40991-016-0005-5

Carnevale, C., & Mazzuca, M. (2012). Sustainability Reporting and Varieties of Capitalism.

Sustainable Development, 22(6), 361-376. doi: 10.1002/sd.1554

Ceulemans, K., Lozano, R., & Alonso-Almeida, M. (2015). Sustainability Reporting in Higher

Education: Interconnecting the Reporting Process and Organisational Change

Management for Sustainability. Sustainability, 7(7), 8881-8903. doi:

10.3390/su7078881

Fordham, A., & Robinson, G. (2018). Mapping meanings of corporate social responsibility – an

Australian case study. International Journal Of Corporate Social Responsibility, 3(1).

doi: 10.1186/s40991-018-0036-1

Gavana, G., Gottardo, P., & Moisello, A. (2016). Sustainability Reporting in Family Firms: A

Panel Data Analysis. Sustainability, 9(1), 38. doi: 10.3390/su9010038

Graymore, M. (2014). Sustainability Reporting: An Approach to Get the Right Mix of Theory

and Practicality for Local Actors. Sustainability, 6(6), 3145-3170. doi:

10.3390/su6063145

CONTEMPORARY ACCOUNTING THEORY 15

Harjoto, M. (2017). Corporate social responsibility and corporate fraud. Social Responsibility

Journal, 13(4), 762-779. doi: 10.1108/srj-09-2016-0166

Herbas Torrico, B., Frank, B., & Arandia Tavera, C. (2018). Corporate social responsibility in

Bolivia: meanings and consequences. International Journal Of Corporate Social

Responsibility, 3(1). doi: 10.1186/s40991-018-0029-0

Kim, Shin, Shin, & Park. (2019). Organizational Slack, Corporate Social Responsibility,

Sustainability, and Integrated Reporting: Evidence from Korea. Sustainability, 11(16),

4445. doi: 10.3390/su11164445

Loh, L., Thomas, T., & Wang, Y. (2017). Sustainability Reporting and Firm Value: Evidence

from Singapore-Listed Companies. Sustainability, 9(11), 2112. doi: 10.3390/su9112112

Loprevite, S., Ricca, B., & Rupo, D. (2018). Performance Sustainability and Integrated

Reporting: Empirical Evidence from Mandatory and Voluntary Adoption Contexts.

Sustainability, 10(5), 1351. doi: 10.3390/su10051351

Maj, J. (2018). Embedding Diversity in Sustainability Reporting. Sustainability, 10(7), 2487. doi:

10.3390/su10072487

Pérez-López, D., Moreno-Romero, A., & Barkemeyer, R. (2013). Exploring the Relationship

between Sustainability Reporting and Sustainability Management Practices. Business

Strategy And The Environment, 24(8), 720-734. doi: 10.1002/bse.1841

Ross, D. (2017). A research-informed model for corporate social responsibility: towards

accountability to impacted stakeholders. International Journal Of Corporate Social

Responsibility, 2(1). doi: 10.1186/s40991-017-0019-7

Harjoto, M. (2017). Corporate social responsibility and corporate fraud. Social Responsibility

Journal, 13(4), 762-779. doi: 10.1108/srj-09-2016-0166

Herbas Torrico, B., Frank, B., & Arandia Tavera, C. (2018). Corporate social responsibility in

Bolivia: meanings and consequences. International Journal Of Corporate Social

Responsibility, 3(1). doi: 10.1186/s40991-018-0029-0

Kim, Shin, Shin, & Park. (2019). Organizational Slack, Corporate Social Responsibility,

Sustainability, and Integrated Reporting: Evidence from Korea. Sustainability, 11(16),

4445. doi: 10.3390/su11164445

Loh, L., Thomas, T., & Wang, Y. (2017). Sustainability Reporting and Firm Value: Evidence

from Singapore-Listed Companies. Sustainability, 9(11), 2112. doi: 10.3390/su9112112

Loprevite, S., Ricca, B., & Rupo, D. (2018). Performance Sustainability and Integrated

Reporting: Empirical Evidence from Mandatory and Voluntary Adoption Contexts.

Sustainability, 10(5), 1351. doi: 10.3390/su10051351

Maj, J. (2018). Embedding Diversity in Sustainability Reporting. Sustainability, 10(7), 2487. doi:

10.3390/su10072487

Pérez-López, D., Moreno-Romero, A., & Barkemeyer, R. (2013). Exploring the Relationship

between Sustainability Reporting and Sustainability Management Practices. Business

Strategy And The Environment, 24(8), 720-734. doi: 10.1002/bse.1841

Ross, D. (2017). A research-informed model for corporate social responsibility: towards

accountability to impacted stakeholders. International Journal Of Corporate Social

Responsibility, 2(1). doi: 10.1186/s40991-017-0019-7

CONTEMPORARY ACCOUNTING THEORY 16

Soyka, P. (2013). The International Integrated Reporting Council (IIRC) Integrated Reporting

Framework: Toward Better Sustainability Reporting and (Way) Beyond. Environmental

Quality Management, 23(2), 1-14. doi: 10.1002/tqem.21357

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability management.

Journal Of Cleaner Production, 136, 102-110. doi: 10.1016/j.jclepro.2016.01.109

Sutopo, B., Kot, S., Adiati, A., & Ardila, L. (2018). Sustainability Reporting and Value

Relevance of Financial Statements. Sustainability, 10(3), 678. doi: 10.3390/su10030678

Timbate, L., & Park, C. (2018). CSR Performance, Financial Reporting, and Investors’

Perception on Financial Reporting. Sustainability, 10(2), 522. doi: 10.3390/su10020522

Wang, M. (2017). The Relationship between Firm Characteristics and the Disclosure of

Sustainability Reporting. Sustainability, 9(4), 624. doi: 10.3390/su9040624

Soyka, P. (2013). The International Integrated Reporting Council (IIRC) Integrated Reporting

Framework: Toward Better Sustainability Reporting and (Way) Beyond. Environmental

Quality Management, 23(2), 1-14. doi: 10.1002/tqem.21357

Stacchezzini, R., Melloni, G., & Lai, A. (2016). Sustainability management and reporting: the

role of integrated reporting for communicating corporate sustainability management.

Journal Of Cleaner Production, 136, 102-110. doi: 10.1016/j.jclepro.2016.01.109

Sutopo, B., Kot, S., Adiati, A., & Ardila, L. (2018). Sustainability Reporting and Value

Relevance of Financial Statements. Sustainability, 10(3), 678. doi: 10.3390/su10030678

Timbate, L., & Park, C. (2018). CSR Performance, Financial Reporting, and Investors’

Perception on Financial Reporting. Sustainability, 10(2), 522. doi: 10.3390/su10020522

Wang, M. (2017). The Relationship between Firm Characteristics and the Disclosure of

Sustainability Reporting. Sustainability, 9(4), 624. doi: 10.3390/su9040624

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.