Contemporary Business Environment

VerifiedAdded on 2023/01/10

|16

|3895

|24

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Contemporary Business

Environment

Environment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. How have average house prices in the UK changed over the period from 2009 to 2019.....................3

2. What are the economic determinates of the changes............................................................................7

3. How has government action over the period 2009-2019 affected the UK housing market?.................9

4. Predict what would be the impact of COVID – 19 on UK housing market........................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................13

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

1. How have average house prices in the UK changed over the period from 2009 to 2019.....................3

2. What are the economic determinates of the changes............................................................................7

3. How has government action over the period 2009-2019 affected the UK housing market?.................9

4. Predict what would be the impact of COVID – 19 on UK housing market........................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................13

INTRODUCTION

In present era, Business environment emergence of variables like individual employees,

competition, government legislation and so forth, the market climate continues to evolve with the

flow of time. Contemporary business environment pertains to present-day circumstances as well

as concepts inside of global business environment. It describes the specific prototype system that

evaluates commercial enterprise as an accessible advisement to the organizational process. It

defines company with a changing dynamics to be macro alongside micro and macro environment

(Bergman and Foxon, 2018). The UK social housing contains private-owned and inhabited

apartment complexes, private-rented and decided to rent lodging by local authorities, and real

estate attempted by property developers. For privately investment home, property is leased by

the owner in a brief tenancy arrangement, generally for six weeks, although it can be extended.

Renters usually charge a set rent but there may be other compensation intervals. This report

contains of UK housing market situation from 2009 to 2019 and identify economic determinates

that changes the economic market. Along with, government action taken for UK housing market

that impact on the market and predict the impact of Covid-19 on UK housing market.

MAIN BODY

1. How have average house prices in the UK changed over the period from 2009 to 2019

UK annual rise in house prices declined to just 1.2 per cent in May. This indicates the

initial rate of growth since January 2013. It is motivated, in part, by the market in London that

average house price growth rates have been adverse for 15 straight years now. In May, London's

yearly household debt rate fell to -4.4 per cent, the smallest although the economic meltdown

unfolded in August 2009. Even so, close examination of the data reveals that while many other

areas of the world continue to develop considerable quantities house price growth levels there is

strong evidence of increased actual housing market depreciation once overall inflation is

compensated for.

In present era, Business environment emergence of variables like individual employees,

competition, government legislation and so forth, the market climate continues to evolve with the

flow of time. Contemporary business environment pertains to present-day circumstances as well

as concepts inside of global business environment. It describes the specific prototype system that

evaluates commercial enterprise as an accessible advisement to the organizational process. It

defines company with a changing dynamics to be macro alongside micro and macro environment

(Bergman and Foxon, 2018). The UK social housing contains private-owned and inhabited

apartment complexes, private-rented and decided to rent lodging by local authorities, and real

estate attempted by property developers. For privately investment home, property is leased by

the owner in a brief tenancy arrangement, generally for six weeks, although it can be extended.

Renters usually charge a set rent but there may be other compensation intervals. This report

contains of UK housing market situation from 2009 to 2019 and identify economic determinates

that changes the economic market. Along with, government action taken for UK housing market

that impact on the market and predict the impact of Covid-19 on UK housing market.

MAIN BODY

1. How have average house prices in the UK changed over the period from 2009 to 2019

UK annual rise in house prices declined to just 1.2 per cent in May. This indicates the

initial rate of growth since January 2013. It is motivated, in part, by the market in London that

average house price growth rates have been adverse for 15 straight years now. In May, London's

yearly household debt rate fell to -4.4 per cent, the smallest although the economic meltdown

unfolded in August 2009. Even so, close examination of the data reveals that while many other

areas of the world continue to develop considerable quantities house price growth levels there is

strong evidence of increased actual housing market depreciation once overall inflation is

compensated for.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

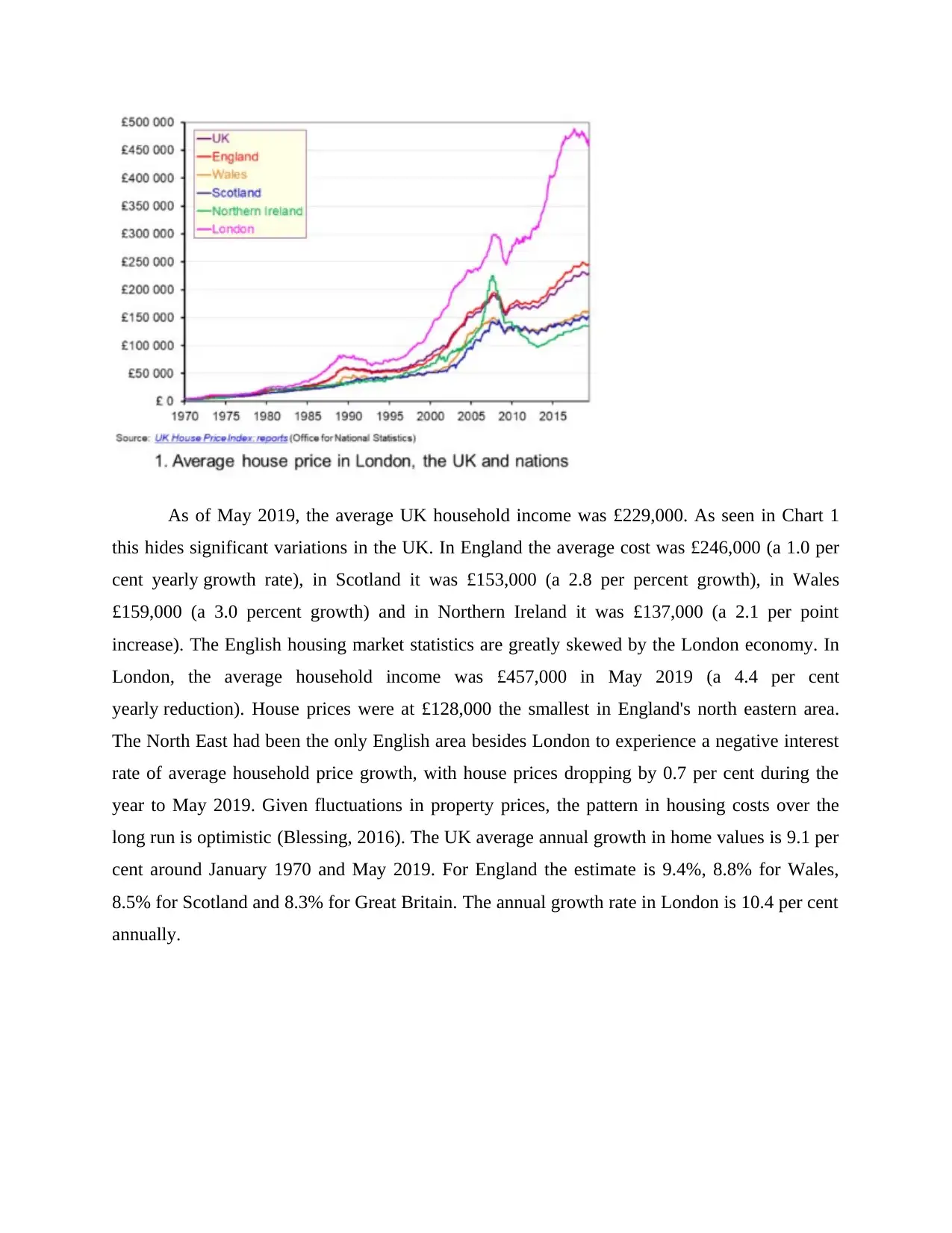

As of May 2019, the average UK household income was £229,000. As seen in Chart 1

this hides significant variations in the UK. In England the average cost was £246,000 (a 1.0 per

cent yearly growth rate), in Scotland it was £153,000 (a 2.8 per percent growth), in Wales

£159,000 (a 3.0 percent growth) and in Northern Ireland it was £137,000 (a 2.1 per point

increase). The English housing market statistics are greatly skewed by the London economy. In

London, the average household income was £457,000 in May 2019 (a 4.4 per cent

yearly reduction). House prices were at £128,000 the smallest in England's north eastern area.

The North East had been the only English area besides London to experience a negative interest

rate of average household price growth, with house prices dropping by 0.7 per cent during the

year to May 2019. Given fluctuations in property prices, the pattern in housing costs over the

long run is optimistic (Blessing, 2016). The UK average annual growth in home values is 9.1 per

cent around January 1970 and May 2019. For England the estimate is 9.4%, 8.8% for Wales,

8.5% for Scotland and 8.3% for Great Britain. The annual growth rate in London is 10.4 per cent

annually.

this hides significant variations in the UK. In England the average cost was £246,000 (a 1.0 per

cent yearly growth rate), in Scotland it was £153,000 (a 2.8 per percent growth), in Wales

£159,000 (a 3.0 percent growth) and in Northern Ireland it was £137,000 (a 2.1 per point

increase). The English housing market statistics are greatly skewed by the London economy. In

London, the average household income was £457,000 in May 2019 (a 4.4 per cent

yearly reduction). House prices were at £128,000 the smallest in England's north eastern area.

The North East had been the only English area besides London to experience a negative interest

rate of average household price growth, with house prices dropping by 0.7 per cent during the

year to May 2019. Given fluctuations in property prices, the pattern in housing costs over the

long run is optimistic (Blessing, 2016). The UK average annual growth in home values is 9.1 per

cent around January 1970 and May 2019. For England the estimate is 9.4%, 8.8% for Wales,

8.5% for Scotland and 8.3% for Great Britain. The annual growth rate in London is 10.4 per cent

annually.

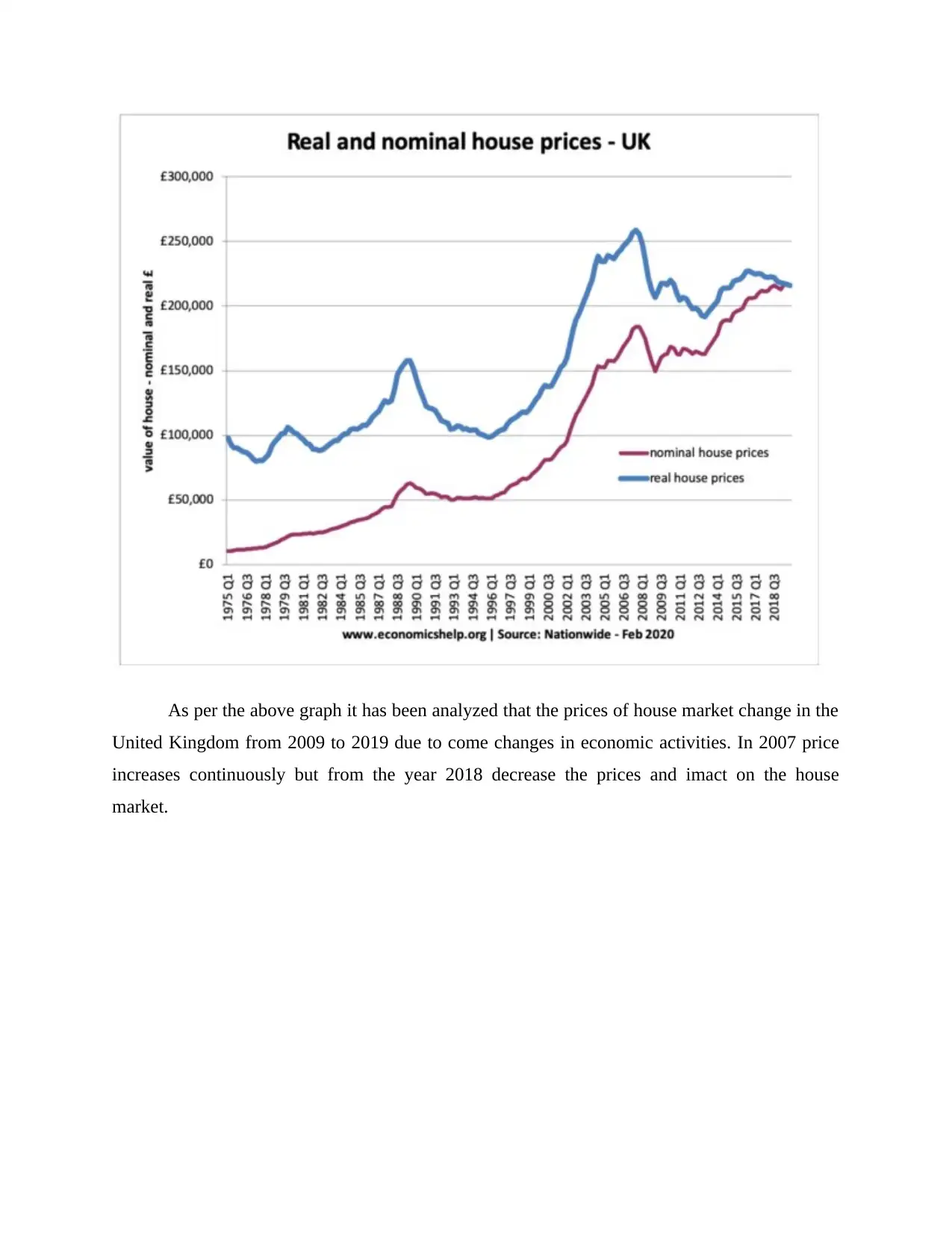

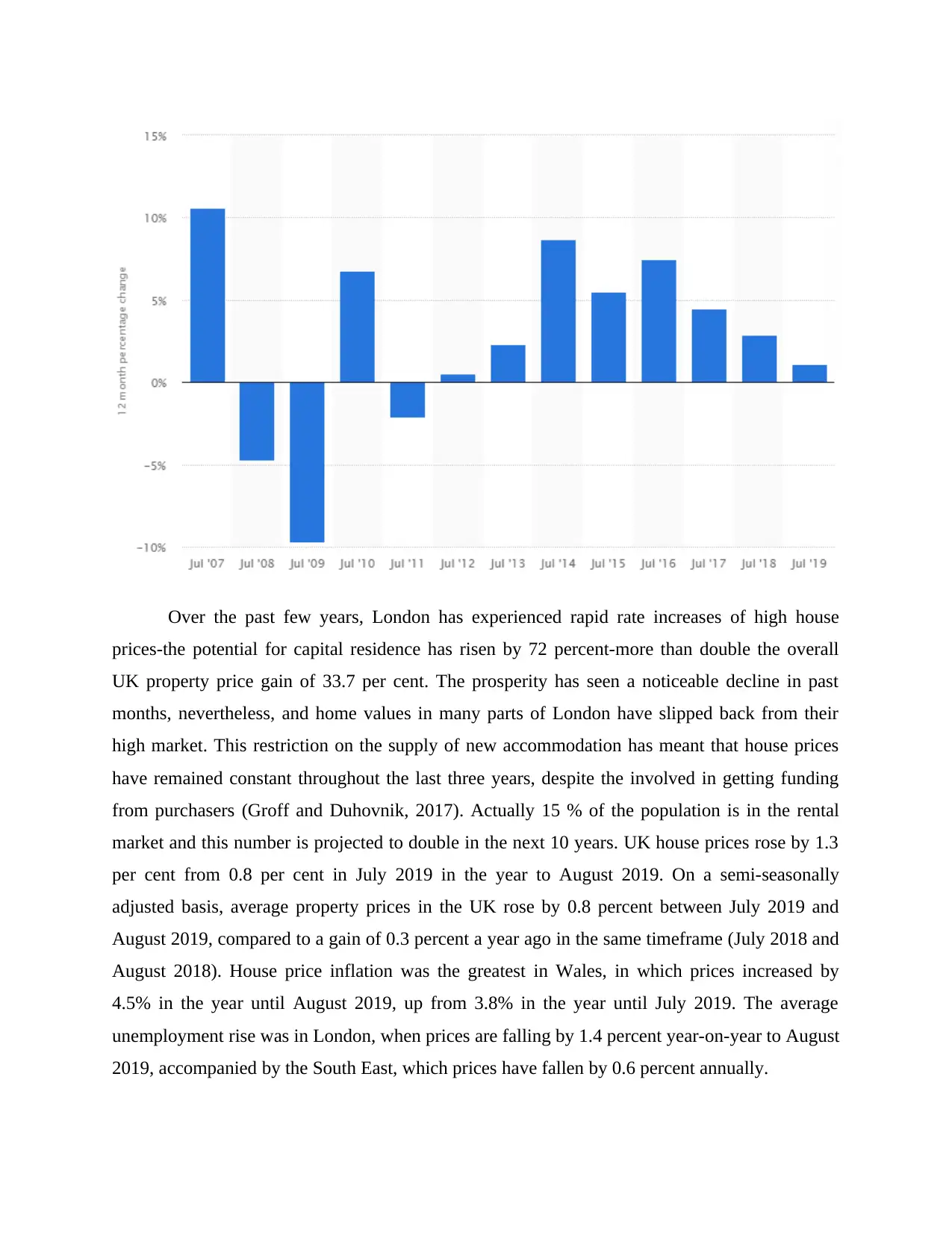

As per the above graph it has been analyzed that the prices of house market change in the

United Kingdom from 2009 to 2019 due to come changes in economic activities. In 2007 price

increases continuously but from the year 2018 decrease the prices and imact on the house

market.

United Kingdom from 2009 to 2019 due to come changes in economic activities. In 2007 price

increases continuously but from the year 2018 decrease the prices and imact on the house

market.

Over the past few years, London has experienced rapid rate increases of high house

prices-the potential for capital residence has risen by 72 percent-more than double the overall

UK property price gain of 33.7 per cent. The prosperity has seen a noticeable decline in past

months, nevertheless, and home values in many parts of London have slipped back from their

high market. This restriction on the supply of new accommodation has meant that house prices

have remained constant throughout the last three years, despite the involved in getting funding

from purchasers (Groff and Duhovnik, 2017). Actually 15 % of the population is in the rental

market and this number is projected to double in the next 10 years. UK house prices rose by 1.3

per cent from 0.8 per cent in July 2019 in the year to August 2019. On a semi-seasonally

adjusted basis, average property prices in the UK rose by 0.8 percent between July 2019 and

August 2019, compared to a gain of 0.3 percent a year ago in the same timeframe (July 2018 and

August 2018). House price inflation was the greatest in Wales, in which prices increased by

4.5% in the year until August 2019, up from 3.8% in the year until July 2019. The average

unemployment rise was in London, when prices are falling by 1.4 percent year-on-year to August

2019, accompanied by the South East, which prices have fallen by 0.6 percent annually.

prices-the potential for capital residence has risen by 72 percent-more than double the overall

UK property price gain of 33.7 per cent. The prosperity has seen a noticeable decline in past

months, nevertheless, and home values in many parts of London have slipped back from their

high market. This restriction on the supply of new accommodation has meant that house prices

have remained constant throughout the last three years, despite the involved in getting funding

from purchasers (Groff and Duhovnik, 2017). Actually 15 % of the population is in the rental

market and this number is projected to double in the next 10 years. UK house prices rose by 1.3

per cent from 0.8 per cent in July 2019 in the year to August 2019. On a semi-seasonally

adjusted basis, average property prices in the UK rose by 0.8 percent between July 2019 and

August 2019, compared to a gain of 0.3 percent a year ago in the same timeframe (July 2018 and

August 2018). House price inflation was the greatest in Wales, in which prices increased by

4.5% in the year until August 2019, up from 3.8% in the year until July 2019. The average

unemployment rise was in London, when prices are falling by 1.4 percent year-on-year to August

2019, accompanied by the South East, which prices have fallen by 0.6 percent annually.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Above statistical results, the average price changes over the period from 2009 to 2019

reflect that. In 2009, the average home price at the UK's Wembley site was £254,920 and it now

exceeded £464,591 in 2020. Improvements in the UK average home price about 82 percent

which is very big and it means that the housing sector is rising strong and also has significant

opportunities. This is also noticed that property are the biggest investment choice for potential

earnings as it is commonly analyzed that property prices increase quickly before some significant

factor affects the country like Brexit or COVID-19 currently (Igbinakhase and Naidoo, 2019).

2. What are the economic determinates of the changes

The long-term increase in property prices is induced by property prices that outstrips

supply. It has been approximated * that 175,000 additional houses per year will be constructed to

meet the projected level of housing demand. As mentioned previously, new developments are

involved in just about 5 per cent of commercial properties. The residential demand is

characterized by the state of the economy, interest rates, real revenue, and relative population

alterations. Along with those demand-side variables, the quantity supplied will decide housing

costs. The house prices are dictated by supply and demand. When demand increases (shift to the

right) or if supply drops (shift to the left), house prices will rise in equilibrium. Furthermore, the

quantity supplied will decline if demand declines or if supply increases. So, in the 2000s, the

home values grow so high, but drop in 2008. The causes for this lie predominantly in rising

property prices (Jacobs and Manzi, 2019). There are different factors that are listed in the

following which have influenced housing demand;

Demand side factors

reflect that. In 2009, the average home price at the UK's Wembley site was £254,920 and it now

exceeded £464,591 in 2020. Improvements in the UK average home price about 82 percent

which is very big and it means that the housing sector is rising strong and also has significant

opportunities. This is also noticed that property are the biggest investment choice for potential

earnings as it is commonly analyzed that property prices increase quickly before some significant

factor affects the country like Brexit or COVID-19 currently (Igbinakhase and Naidoo, 2019).

2. What are the economic determinates of the changes

The long-term increase in property prices is induced by property prices that outstrips

supply. It has been approximated * that 175,000 additional houses per year will be constructed to

meet the projected level of housing demand. As mentioned previously, new developments are

involved in just about 5 per cent of commercial properties. The residential demand is

characterized by the state of the economy, interest rates, real revenue, and relative population

alterations. Along with those demand-side variables, the quantity supplied will decide housing

costs. The house prices are dictated by supply and demand. When demand increases (shift to the

right) or if supply drops (shift to the left), house prices will rise in equilibrium. Furthermore, the

quantity supplied will decline if demand declines or if supply increases. So, in the 2000s, the

home values grow so high, but drop in 2008. The causes for this lie predominantly in rising

property prices (Jacobs and Manzi, 2019). There are different factors that are listed in the

following which have influenced housing demand;

Demand side factors

Economic growth: Better standards of living encourage people to afford more and to

invest money. Many years ago people use 3 times the income to get a loan ratio. For instance, if

a individual makes £30,000 the financial institution will be running £90,000. Hence rising

revenues cause house rate to rise. The ratio of housing costs to wages, although, can vary

significantly. For instance, the ratio of property prices to earnings rose significantly between

1995 and 2007. When the economy is down and higher unemployment, there will be a big

decrease in the quantity for home ownership.

Income: In the 2007 appealing was a time for increasingly growing revenues. The

financial system was beginning to experience a "boom" in economic policy most residents

decided to spend their extra money on accommodation; even first purchase a house or move to a

better one. Most people believed their salaries would keep on increasing and therefore were

willing to expand economically in the brief period by purchasing an expensive property,

optimistic their monthly repayments would become much more manageable with term. In

comparison, there were cycles of depression in 2008/09, with increasing unemployment and

either declining, or wages increasing far more gradually. Citizens were much less positive in

their money to afford huge sums (Kim and Lim, 2016).

Demographic factors: An increasing proportion of homes have been in the UK. When

the average family size decreases and there are much more individual people who are living

independently, the majority of houses will grow faster than the national. If we research the UK

population map, earnings rates have declined to 16 or 17, indicating that more workers spend and

become autonomous. This freedom gives rise to the buyers of homes. Housing demand in the

UK has risen for a plethora of purposes, such as: a rise in rates of divorce eventually increased

pressure for respective bedrooms.

Consumer confidence: Consumers are more likely to taking out costly loans throughout

periods of strong consumer trust in order to be able to afford a house. 100 percent mortgage rates

and involvement only housing loans have been quite prevalent in the period 2001-07. Consumers

were positive more about property beginning in the recent 1900s and so taking out investments

with a greater ratio of debt to profits. In the fast 00s, the economic expansion gives these people

sufficient incentive to speak out loans at rising interest rates. Even though joblessness was close

invest money. Many years ago people use 3 times the income to get a loan ratio. For instance, if

a individual makes £30,000 the financial institution will be running £90,000. Hence rising

revenues cause house rate to rise. The ratio of housing costs to wages, although, can vary

significantly. For instance, the ratio of property prices to earnings rose significantly between

1995 and 2007. When the economy is down and higher unemployment, there will be a big

decrease in the quantity for home ownership.

Income: In the 2007 appealing was a time for increasingly growing revenues. The

financial system was beginning to experience a "boom" in economic policy most residents

decided to spend their extra money on accommodation; even first purchase a house or move to a

better one. Most people believed their salaries would keep on increasing and therefore were

willing to expand economically in the brief period by purchasing an expensive property,

optimistic their monthly repayments would become much more manageable with term. In

comparison, there were cycles of depression in 2008/09, with increasing unemployment and

either declining, or wages increasing far more gradually. Citizens were much less positive in

their money to afford huge sums (Kim and Lim, 2016).

Demographic factors: An increasing proportion of homes have been in the UK. When

the average family size decreases and there are much more individual people who are living

independently, the majority of houses will grow faster than the national. If we research the UK

population map, earnings rates have declined to 16 or 17, indicating that more workers spend and

become autonomous. This freedom gives rise to the buyers of homes. Housing demand in the

UK has risen for a plethora of purposes, such as: a rise in rates of divorce eventually increased

pressure for respective bedrooms.

Consumer confidence: Consumers are more likely to taking out costly loans throughout

periods of strong consumer trust in order to be able to afford a house. 100 percent mortgage rates

and involvement only housing loans have been quite prevalent in the period 2001-07. Consumers

were positive more about property beginning in the recent 1900s and so taking out investments

with a greater ratio of debt to profits. In the fast 00s, the economic expansion gives these people

sufficient incentive to speak out loans at rising interest rates. Even though joblessness was close

to zero, buyers trusted their income. This faith is clearly articulated in the late 00s rise of

property sector.

Cost of mortgages: The mortgage rates in the early 1990's were lower than they are now.

That means the people were able to pay bigger mortgage and therefore be able to purchase more

large properties. Yet interest rates on mortgages now had risen. Many households find it hard to

make tax property, and let them take on a larger mortgage. Broadly speaking, interest rates have

gone up again in 2003, again fueling demand for homes. Although as interest rates slowly raised

over the period from 2004 to 2007 they did not come close to the level that had been reached as

before. Nonetheless, by 2008/09 elevated housing prices were incredibly competitive for many

citizens but this was another key contributor to the eventual drop in housing market.

Availability of mortgage finance: When we take a look at the 70s 80s of the modern

period the lending community was not very popular, there was a spike in the amount of mortgage

loans later due to higher commercial banks & competitive pressures with privatization of the

banking industry. Items such as cost only, personality-certification loans and mortgage up to 6

times income allowed individuals to exchange more loans, while growing property prices.

Nonetheless, the number of housing products available in the market dropped mostly during

credit crisis of 2008 due to a shortage of funding in the financial markets. Definitely this

financial crisis has proven a significant fall in property prices (Mussa, Nwaogu and Pozo, 2017).

Supply side factors: Supply of housing is set in the short term, since constructing

housing takes some time. And demand impacts prices rather than supply in the immediate future

Nevertheless, if housing stock is relatively elastic than production rises will lead to a significant

rate hike. The basic principles of heredity above give us a better idea that housing construction

rates are constant due to its slow rate, and display no variance whatsoever. Such conditions are

not fulfilled by the present scenario, as unemployment has forced the commodity prices to rise

exponentially and property values to grow.

Supply of new house: A fall in demand will bring higher prices on the UK housing

market and a further hand-output excess will force down costs. For instance, an approximate

700,000 new houses were built in the Irish housing boom from 1996-2006. The housing sector

crashed at any moment; the business sector had a structural excessive-supply. UK house prices

property sector.

Cost of mortgages: The mortgage rates in the early 1990's were lower than they are now.

That means the people were able to pay bigger mortgage and therefore be able to purchase more

large properties. Yet interest rates on mortgages now had risen. Many households find it hard to

make tax property, and let them take on a larger mortgage. Broadly speaking, interest rates have

gone up again in 2003, again fueling demand for homes. Although as interest rates slowly raised

over the period from 2004 to 2007 they did not come close to the level that had been reached as

before. Nonetheless, by 2008/09 elevated housing prices were incredibly competitive for many

citizens but this was another key contributor to the eventual drop in housing market.

Availability of mortgage finance: When we take a look at the 70s 80s of the modern

period the lending community was not very popular, there was a spike in the amount of mortgage

loans later due to higher commercial banks & competitive pressures with privatization of the

banking industry. Items such as cost only, personality-certification loans and mortgage up to 6

times income allowed individuals to exchange more loans, while growing property prices.

Nonetheless, the number of housing products available in the market dropped mostly during

credit crisis of 2008 due to a shortage of funding in the financial markets. Definitely this

financial crisis has proven a significant fall in property prices (Mussa, Nwaogu and Pozo, 2017).

Supply side factors: Supply of housing is set in the short term, since constructing

housing takes some time. And demand impacts prices rather than supply in the immediate future

Nevertheless, if housing stock is relatively elastic than production rises will lead to a significant

rate hike. The basic principles of heredity above give us a better idea that housing construction

rates are constant due to its slow rate, and display no variance whatsoever. Such conditions are

not fulfilled by the present scenario, as unemployment has forced the commodity prices to rise

exponentially and property values to grow.

Supply of new house: A fall in demand will bring higher prices on the UK housing

market and a further hand-output excess will force down costs. For instance, an approximate

700,000 new houses were built in the Irish housing boom from 1996-2006. The housing sector

crashed at any moment; the business sector had a structural excessive-supply. UK house prices

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

have approached 15 per cent, and prices have fallen as competitors from manufacturing are

going to rise. Housing stocks, by comparison, have fallen behind UK demand. UK house rates

won't fall as often as they did with a recession in Ireland and significantly improved quickly as a

result of continuing financial crunch.

Supply and price: When the house price increases the provided amount will rise as well.

There are three reasons for this: As firm production is expanded, they are likely to discover that,

more than a certain point of performance, prices are growing faster and faster. Residential

contractor in that situation planned to develop ever more homes. The greater the real estate

market value, the more financially viable it is to do company in the property market. Therefore,

housing agent would be motivated to sell more houses by moving from the less lucrative sector

of renting. With time, if the home price stays strong, potential people are willing to start up

company, but if the income does not rise, people would not be able to purchase a house

(Nijskens, Lohuis, Hilbers and Heeringa, 2019).

3. How has government action over the period 2009-2019 affected the UK housing market?

The UK social housing contains private-owned and inhabited apartment complexes,

private-rented and decided to rent lodging by local councils, and real estate attempted by private

landlords. For personal investment home, property is leased by the owner in a brief tenancy

arrangement, generally for six weeks, although it can be extended. Renters usually charge a set

rent but there may be other compensation intervals. There are mentioned various action that

taken by the government during to 2009 to 2019 such as:

Fiscal and monetary policy: A few of the observations suggested that the Bank of

England has an obligation to improve real estate values. This will require rise in interest rates to

discourage loan withdrawals. Furthermore, the Bank of England is primarily responsible for

market and economic development. The purpose of winning the property market isn't money

creation. If home values need to be promoted by the Bank of England, this may communicate

with the productivity expansion (Norris and Byrne, 2018).

Government subsidies: Additional cash expenditure on subsidies the 'private' house prices

could substantially boost requirement. In the past few years, housing associations have gone out

of fashion due to the govt's effort to sell off council housing and cut down on public

going to rise. Housing stocks, by comparison, have fallen behind UK demand. UK house rates

won't fall as often as they did with a recession in Ireland and significantly improved quickly as a

result of continuing financial crunch.

Supply and price: When the house price increases the provided amount will rise as well.

There are three reasons for this: As firm production is expanded, they are likely to discover that,

more than a certain point of performance, prices are growing faster and faster. Residential

contractor in that situation planned to develop ever more homes. The greater the real estate

market value, the more financially viable it is to do company in the property market. Therefore,

housing agent would be motivated to sell more houses by moving from the less lucrative sector

of renting. With time, if the home price stays strong, potential people are willing to start up

company, but if the income does not rise, people would not be able to purchase a house

(Nijskens, Lohuis, Hilbers and Heeringa, 2019).

3. How has government action over the period 2009-2019 affected the UK housing market?

The UK social housing contains private-owned and inhabited apartment complexes,

private-rented and decided to rent lodging by local councils, and real estate attempted by private

landlords. For personal investment home, property is leased by the owner in a brief tenancy

arrangement, generally for six weeks, although it can be extended. Renters usually charge a set

rent but there may be other compensation intervals. There are mentioned various action that

taken by the government during to 2009 to 2019 such as:

Fiscal and monetary policy: A few of the observations suggested that the Bank of

England has an obligation to improve real estate values. This will require rise in interest rates to

discourage loan withdrawals. Furthermore, the Bank of England is primarily responsible for

market and economic development. The purpose of winning the property market isn't money

creation. If home values need to be promoted by the Bank of England, this may communicate

with the productivity expansion (Norris and Byrne, 2018).

Government subsidies: Additional cash expenditure on subsidies the 'private' house prices

could substantially boost requirement. In the past few years, housing associations have gone out

of fashion due to the govt's effort to sell off council housing and cut down on public

accommodation. Though these were council properties in the post - war period that gave a

substantial boost to the UK residential housing stock. Clear policy expenditure motivates

electorate to anticipate more and they are being stopped by increasing expenditure.

Restriction on construction: Constraints on drawing up proposals in the UK are very

strong. This will be better for the vendors to ease the lot of regulations and try to make the

operation more efficient. This can imply a reduction in the total area of shielded greenbelt land.

This can also necessitate the regulations that domestic-builders should appreciate to be

simplified. This can lead to major local issues as people start talking about the unnecessary

development, population growth and lack of green spaces. Another option will be to add capital

to build new homes for suitable areas of greenbelt and agricultural land (Ruiz and Vargas-Silva,

2018).

4. Predict what would be the impact of COVID – 19 on UK housing market

Housing is a field of vital importance to the business. This supports massive amounts of

people locally and globally, and contributes for a major percentage of GDP income. In

econometrics people are called upon to design guide of market forces to recognize pricing

practices and cost increases. The UK housing sector is typically recognized as the source of

many systemic problems and from both the owner-occupied and rental sector there is a systemic

scarcity of seam allowance. Policy actions boost the result for customers and manufacturers or

may lead to cases of disappointment by governments. This is a strong market for application of

AS micro theory. In order to usefully speculate about the impact of COVID-19 on UK housing,

one needs to have a good conceptual knowledge of how our home values operate and what

factors alter them. Given the intense uncertainties about the disease outbreak's effect and

development, everything in this blog is speculation in some way but we expect educated

hypothesis. A latest research paper analyzing the effects of digital outbreaks in Amsterdam and

Paris on property prices and rentals noticed only comparatively short-lived and localized housing

market declines and lower impact on rentals than on incomes (Schaltegger and Burritt, 2017).

Although helpful, they are tentative in attempting to create clear conclusions from historical

precedents like these. Measures to combat the spreading of coronavirus have plunged Britain's

housing sector into deep freezing, and it is impossible to have improved in the next year.

Although British citizens can still travel in the midst of purchasing a home, estate browsing was

substantial boost to the UK residential housing stock. Clear policy expenditure motivates

electorate to anticipate more and they are being stopped by increasing expenditure.

Restriction on construction: Constraints on drawing up proposals in the UK are very

strong. This will be better for the vendors to ease the lot of regulations and try to make the

operation more efficient. This can imply a reduction in the total area of shielded greenbelt land.

This can also necessitate the regulations that domestic-builders should appreciate to be

simplified. This can lead to major local issues as people start talking about the unnecessary

development, population growth and lack of green spaces. Another option will be to add capital

to build new homes for suitable areas of greenbelt and agricultural land (Ruiz and Vargas-Silva,

2018).

4. Predict what would be the impact of COVID – 19 on UK housing market

Housing is a field of vital importance to the business. This supports massive amounts of

people locally and globally, and contributes for a major percentage of GDP income. In

econometrics people are called upon to design guide of market forces to recognize pricing

practices and cost increases. The UK housing sector is typically recognized as the source of

many systemic problems and from both the owner-occupied and rental sector there is a systemic

scarcity of seam allowance. Policy actions boost the result for customers and manufacturers or

may lead to cases of disappointment by governments. This is a strong market for application of

AS micro theory. In order to usefully speculate about the impact of COVID-19 on UK housing,

one needs to have a good conceptual knowledge of how our home values operate and what

factors alter them. Given the intense uncertainties about the disease outbreak's effect and

development, everything in this blog is speculation in some way but we expect educated

hypothesis. A latest research paper analyzing the effects of digital outbreaks in Amsterdam and

Paris on property prices and rentals noticed only comparatively short-lived and localized housing

market declines and lower impact on rentals than on incomes (Schaltegger and Burritt, 2017).

Although helpful, they are tentative in attempting to create clear conclusions from historical

precedents like these. Measures to combat the spreading of coronavirus have plunged Britain's

housing sector into deep freezing, and it is impossible to have improved in the next year.

Although British citizens can still travel in the midst of purchasing a home, estate browsing was

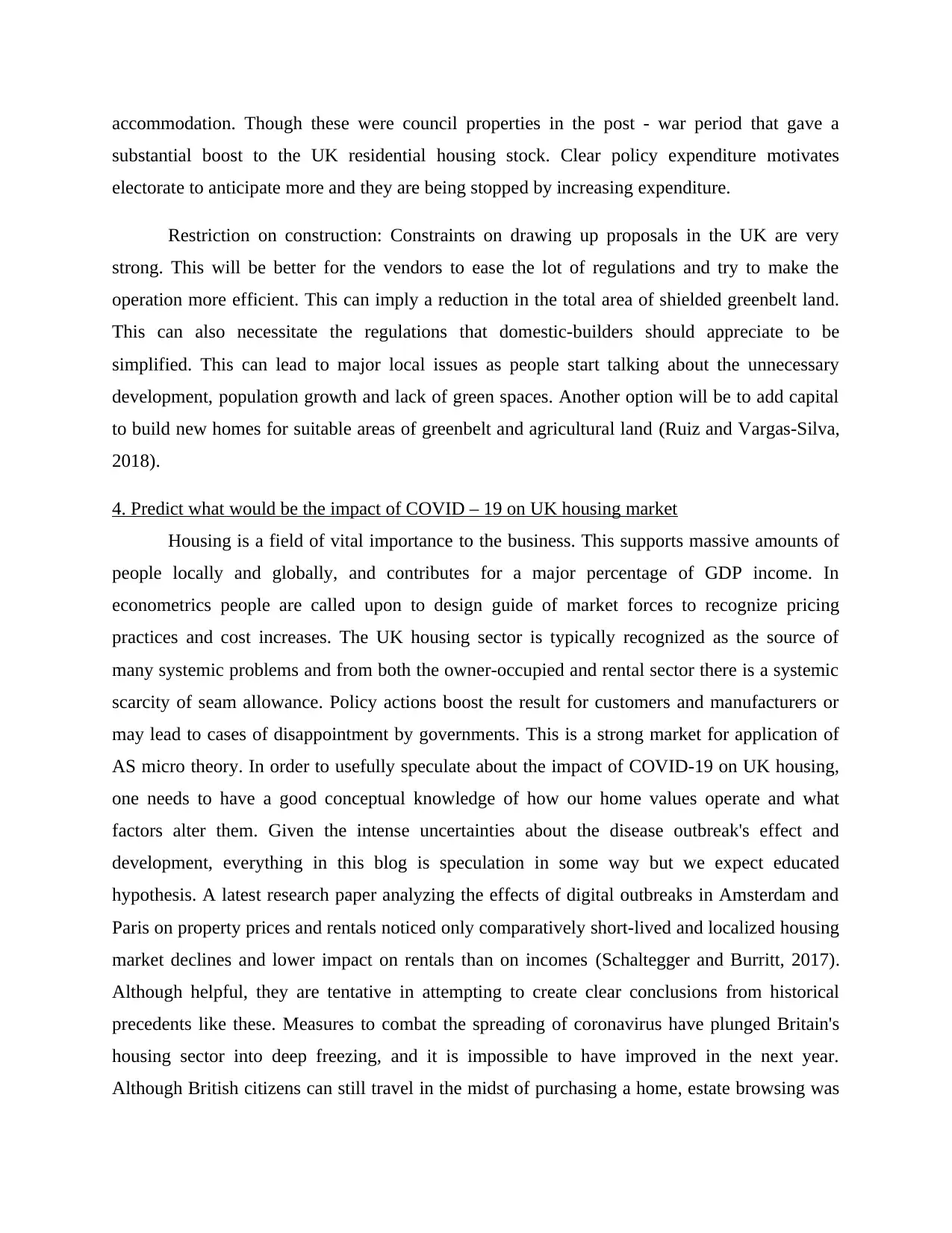

stopped and the premises of mortgage brokers permanently closed as result of broader-ranging

steps to eliminate COVID-19 infections. House prices and development had gathered since

before the beginning of 2020, supported by decreased Brexit and political instability, but this

pattern has went rapidly downwards (Wu and Li, 2018).

In order to effectively speculate about both the impact of the COVID-19 pandemic on the

Uk property market, one needs a decent empirical knowledge as to how our house prices operate

and what factors are causing them to shift. Given the immense unpredictability exploring the

effects and transformation of the COVID-19 pandemic, anybody in this website is conjecture in

certain context, but we hope pure conjecture. And it's the first sign of what the COVID-19 crisis

is going to do with the housing sector. It will create instability even in the brief period:

purchasing and sale will all but end (Stephens, 2019). Even so, they have already-Zoopla

announced a 40 percent decrease in inquiries even in early march.

steps to eliminate COVID-19 infections. House prices and development had gathered since

before the beginning of 2020, supported by decreased Brexit and political instability, but this

pattern has went rapidly downwards (Wu and Li, 2018).

In order to effectively speculate about both the impact of the COVID-19 pandemic on the

Uk property market, one needs a decent empirical knowledge as to how our house prices operate

and what factors are causing them to shift. Given the immense unpredictability exploring the

effects and transformation of the COVID-19 pandemic, anybody in this website is conjecture in

certain context, but we hope pure conjecture. And it's the first sign of what the COVID-19 crisis

is going to do with the housing sector. It will create instability even in the brief period:

purchasing and sale will all but end (Stephens, 2019). Even so, they have already-Zoopla

announced a 40 percent decrease in inquiries even in early march.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

It has been concluded, according to the aforementioned article, that UK house prices are

being adjusted due to numerous difficulties. There are growing economic factors influencing the

average prices that are both cutting and rising. Sometimes policymakers pick multiple measures

and bring in place successful regulation that influences the average house prices. This industry is

dropping due to Corona virus and rates are deducing in the industry.

It has been concluded, according to the aforementioned article, that UK house prices are

being adjusted due to numerous difficulties. There are growing economic factors influencing the

average prices that are both cutting and rising. Sometimes policymakers pick multiple measures

and bring in place successful regulation that influences the average house prices. This industry is

dropping due to Corona virus and rates are deducing in the industry.

REFERENCES

Books and Journal

Bergman, N. and Foxon, T. J., 2018. Reorienting Finance Towards Energy Efficiency: The Case

of UK Housing.

Blessing, A., 2016. Repackaging the poor? Conceptualising neoliberal reforms of social rental

housing. Housing Studies. 31(2). pp.149-172.

Groff, M. Z. and Duhovnik, M., 2017. Corporate Financial Reporting in Slovenia: Historical

Development, Contemporary Challenges and Policy Implications. Economic and

Business Review for Central and South-Eastern Europe. 19(3). pp.325-419.

Igbinakhase, I. and Naidoo, V., 2019. Global Leadership Competencies and Orientations:

Theory, Practice, And Future Implications. In Contemporary Multicultural Orientations

And Practices for Global Leadership (pp. 59-79). IGI Global.

Jacobs, K. and Manzi, T., 2019. Conceptualising ‘financialisation’: governance, organisational

behaviour and social interaction in UK housing. International Journal of Housing Policy,

pp.1-19.

Kim, J.R. and Lim, G., 2016. Fundamentals and rational bubbles in the Korean housing market:

A modified present-value approach. Economic Modelling, 59, pp.174-181.

Mussa, A., Nwaogu, U. G. and Pozo, S., 2017. Immigration and housing: A spatial econometric

analysis. Journal of Housing Economics. 35. pp.13-25.

Nijskens, R., Lohuis, M., Hilbers, P. and Heeringa, W., 2019. Hot Property: The Housing

Market in Major Cities (p. 221). Springer Nature.

Norris, M. and Byrne, M., 2018. Housing market (in) stability and social rented housing:

comparing Austria and Ireland during the global financial crisis. Journal of Housing and

the Built Environment. 33(2). pp.227-245.

Ruiz, I. and Vargas-Silva, C., 2018. Differences in labour market outcomes between natives,

refugees and other migrants in the UK. Journal of Economic Geography, 18(4), pp.855-

885.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Stephens, M., 2019. Social rented housing in the (DIS) United Kingdom: Can different social

housing regime types exist within the same nation state?. Urban Research &

Practice. 12(1). pp.38-60.

Wu, Y. and Li, Y., 2018. Impact of government intervention in the housing market: evidence

from the housing purchase restriction policy in China. Applied Economics. 50(6). pp.691-

705.

Books and Journal

Bergman, N. and Foxon, T. J., 2018. Reorienting Finance Towards Energy Efficiency: The Case

of UK Housing.

Blessing, A., 2016. Repackaging the poor? Conceptualising neoliberal reforms of social rental

housing. Housing Studies. 31(2). pp.149-172.

Groff, M. Z. and Duhovnik, M., 2017. Corporate Financial Reporting in Slovenia: Historical

Development, Contemporary Challenges and Policy Implications. Economic and

Business Review for Central and South-Eastern Europe. 19(3). pp.325-419.

Igbinakhase, I. and Naidoo, V., 2019. Global Leadership Competencies and Orientations:

Theory, Practice, And Future Implications. In Contemporary Multicultural Orientations

And Practices for Global Leadership (pp. 59-79). IGI Global.

Jacobs, K. and Manzi, T., 2019. Conceptualising ‘financialisation’: governance, organisational

behaviour and social interaction in UK housing. International Journal of Housing Policy,

pp.1-19.

Kim, J.R. and Lim, G., 2016. Fundamentals and rational bubbles in the Korean housing market:

A modified present-value approach. Economic Modelling, 59, pp.174-181.

Mussa, A., Nwaogu, U. G. and Pozo, S., 2017. Immigration and housing: A spatial econometric

analysis. Journal of Housing Economics. 35. pp.13-25.

Nijskens, R., Lohuis, M., Hilbers, P. and Heeringa, W., 2019. Hot Property: The Housing

Market in Major Cities (p. 221). Springer Nature.

Norris, M. and Byrne, M., 2018. Housing market (in) stability and social rented housing:

comparing Austria and Ireland during the global financial crisis. Journal of Housing and

the Built Environment. 33(2). pp.227-245.

Ruiz, I. and Vargas-Silva, C., 2018. Differences in labour market outcomes between natives,

refugees and other migrants in the UK. Journal of Economic Geography, 18(4), pp.855-

885.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Stephens, M., 2019. Social rented housing in the (DIS) United Kingdom: Can different social

housing regime types exist within the same nation state?. Urban Research &

Practice. 12(1). pp.38-60.

Wu, Y. and Li, Y., 2018. Impact of government intervention in the housing market: evidence

from the housing purchase restriction policy in China. Applied Economics. 50(6). pp.691-

705.

Online

Average UK house prices. 2018. https://pearsonblog.campaignserver.co.uk/tag/house-price-

inflation/

<https://realty.economictimes.indiatimes.com/news/industry/coronavirus-brings-uk-housing-

market-to-near-standstill-rics/75072418>

< https://www.bbc.com/news/business-52977890>

Average UK house prices. 2018. https://pearsonblog.campaignserver.co.uk/tag/house-price-

inflation/

<https://realty.economictimes.indiatimes.com/news/industry/coronavirus-brings-uk-housing-

market-to-near-standstill-rics/75072418>

< https://www.bbc.com/news/business-52977890>

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.