Contemporary Development - Aviva Insurance UK

VerifiedAdded on 2022/08/31

|14

|4134

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: MANAGEMENT 0

CONTEMPORARY

DEVELOPMENT

CONTEMPORARY

DEVELOPMENT

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT 1

Contents

Introduction: Aviva Insurance UK........................................................................................................2

Pestle analysis of Aviva insurance company.........................................................................................2

Impact of climate change on insurance company..................................................................................5

Aviva Insurance Company action on climate change............................................................................5

Recommendations.................................................................................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

Contents

Introduction: Aviva Insurance UK........................................................................................................2

Pestle analysis of Aviva insurance company.........................................................................................2

Impact of climate change on insurance company..................................................................................5

Aviva Insurance Company action on climate change............................................................................5

Recommendations.................................................................................................................................8

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Appendix.............................................................................................................................................13

MANAGEMENT 2

Introduction: Aviva Insurance UK

Aviva is found to be the biggest insurance company with over 15.5 million customers.

It offers a wide range of life insurance as well as non-life insurance services to families,

individuals, as well as business clients. The portfolio of insurance services includes travel

insurance, car insurance, home insurance, personal accident insurance, term life insurance,

whole life insurance, health insurance, employee benefits as well as critical illness insurance.

At the same time, it also offers retirement solutions, saving plans, investment portfolio plans.

The company sells markets as well as ensure the distribution of its insurance products

through direct and online, brokers, financial advisors and corporate partners. Aviva receives

around ten million calls from its customer service division every year. Aviva gives emphasis

on few elements in order to gain the best customer satisfaction. It tends to offer everything

from health and life insurance to pension plans and general insurance. This is something that

keeps it apart from other competitors. It also puts digital first in convenient, simple and easy

way. it also chooses its products and market carefully in order to provide the best experience

and value to the customers.

It plays the most significant role in order to assess the climate risk in insurance sector.

It also encourages businesses to increase the delivery of UN sustainable development goals.

Tackling climate change is the most significant aspect of business organisation. Insurance

industries are also required to effectively work on climate change issues in order to work for

environmental protection and their welfare. Similarly, Aviva Insurance is also working on

several aspects of climate change. The initiatives taken by Aviva insurance for climate

change are discussed in the paper. Afterwards, recommendations are provided that will help

in improving the climate change initiative of the company.

Pestle analysis of Aviva insurance company

Politics factors: In March 2019, UK was forecast to leave the European Union. UK

government has taken this step for minimising the adverse impact of uncertainty. High level

of uncertainty is also seen in the insurance market of UK. Due to this policy, Aviva has

transferred some of its insurance policies into the Aviva insurance Ireland DAC. Aviva has

Introduction: Aviva Insurance UK

Aviva is found to be the biggest insurance company with over 15.5 million customers.

It offers a wide range of life insurance as well as non-life insurance services to families,

individuals, as well as business clients. The portfolio of insurance services includes travel

insurance, car insurance, home insurance, personal accident insurance, term life insurance,

whole life insurance, health insurance, employee benefits as well as critical illness insurance.

At the same time, it also offers retirement solutions, saving plans, investment portfolio plans.

The company sells markets as well as ensure the distribution of its insurance products

through direct and online, brokers, financial advisors and corporate partners. Aviva receives

around ten million calls from its customer service division every year. Aviva gives emphasis

on few elements in order to gain the best customer satisfaction. It tends to offer everything

from health and life insurance to pension plans and general insurance. This is something that

keeps it apart from other competitors. It also puts digital first in convenient, simple and easy

way. it also chooses its products and market carefully in order to provide the best experience

and value to the customers.

It plays the most significant role in order to assess the climate risk in insurance sector.

It also encourages businesses to increase the delivery of UN sustainable development goals.

Tackling climate change is the most significant aspect of business organisation. Insurance

industries are also required to effectively work on climate change issues in order to work for

environmental protection and their welfare. Similarly, Aviva Insurance is also working on

several aspects of climate change. The initiatives taken by Aviva insurance for climate

change are discussed in the paper. Afterwards, recommendations are provided that will help

in improving the climate change initiative of the company.

Pestle analysis of Aviva insurance company

Politics factors: In March 2019, UK was forecast to leave the European Union. UK

government has taken this step for minimising the adverse impact of uncertainty. High level

of uncertainty is also seen in the insurance market of UK. Due to this policy, Aviva has

transferred some of its insurance policies into the Aviva insurance Ireland DAC. Aviva has

MANAGEMENT 3

stated that its locally regulated business in Europe has been prepared to minimise the

potential impact of operations.

Economic factors: the UK is seen to be the most developed and prosperous country in the

world. The people living in the UK enjoy a high standard of living as compared to other

countries. UK economy also works favourably for Insurance companies. In addition to this,

UK economy is also dominated by the service sector by comprising 80 per cent stake in the

GDP. The UK holds the fourth biggest insurance market it is found that economic climate is

putting then positive impact on the insurance companies. As compared to this, regulations

with Brexit remains the greatest concern for it, due to the recent economic uncertainty,

several brokers are taking steps in securing the future of the business.

Social factors: Due to the increasing shift of people on long term plan, Aviva and Pension

UK has done the deal with prudential retirement for the long reinsurance transaction. It has

stated that pension insurers are regularly seeking to manage their capital and risk with long

reinsurance agreements. Demand is also increasing due to the increasing affordability of the

pension risk transfer by reflecting enhanced insurer capacity and attractive pricing. Therefore,

the leading pension schemes are taking benefit of the favourable environment by transferring

risk (Insurance Business UK, 2018). In addition to this, the changing demand of customers

toward automation has forced the Aviva to meet their demand. Due to this, Aviva has also

created an automated system by matching the skills of employees. In the area of pension also,

Aviva has made the 40 per cent increase in efficiency since implementing the Low-code

platform.

Technological factor:

Digital first strategy: Mobile, online and tablet has enhanced the customer experience.

Due to this, Aviva digital first strategy has given the emphasis on being the digital disruptor

and bringing improvement in customer experience through digital technologies. By following

this strategy, Aviva is collaborating and recruiting the innovators, data scientists, start-ups

and entrepreneurs. By the year 2016, Aviva had around 7.5 million of users registered on the

digital platforms. In addition to this, Aviva also entered in “digital insurance joint venture”

with the tenant and Hill house in Hong Kong. It will see insurance products and solutions

online. By effectively tapping the market as per changing demand and needs of the

customers, Aviva is able to maintain its unique position in the market.

stated that its locally regulated business in Europe has been prepared to minimise the

potential impact of operations.

Economic factors: the UK is seen to be the most developed and prosperous country in the

world. The people living in the UK enjoy a high standard of living as compared to other

countries. UK economy also works favourably for Insurance companies. In addition to this,

UK economy is also dominated by the service sector by comprising 80 per cent stake in the

GDP. The UK holds the fourth biggest insurance market it is found that economic climate is

putting then positive impact on the insurance companies. As compared to this, regulations

with Brexit remains the greatest concern for it, due to the recent economic uncertainty,

several brokers are taking steps in securing the future of the business.

Social factors: Due to the increasing shift of people on long term plan, Aviva and Pension

UK has done the deal with prudential retirement for the long reinsurance transaction. It has

stated that pension insurers are regularly seeking to manage their capital and risk with long

reinsurance agreements. Demand is also increasing due to the increasing affordability of the

pension risk transfer by reflecting enhanced insurer capacity and attractive pricing. Therefore,

the leading pension schemes are taking benefit of the favourable environment by transferring

risk (Insurance Business UK, 2018). In addition to this, the changing demand of customers

toward automation has forced the Aviva to meet their demand. Due to this, Aviva has also

created an automated system by matching the skills of employees. In the area of pension also,

Aviva has made the 40 per cent increase in efficiency since implementing the Low-code

platform.

Technological factor:

Digital first strategy: Mobile, online and tablet has enhanced the customer experience.

Due to this, Aviva digital first strategy has given the emphasis on being the digital disruptor

and bringing improvement in customer experience through digital technologies. By following

this strategy, Aviva is collaborating and recruiting the innovators, data scientists, start-ups

and entrepreneurs. By the year 2016, Aviva had around 7.5 million of users registered on the

digital platforms. In addition to this, Aviva also entered in “digital insurance joint venture”

with the tenant and Hill house in Hong Kong. It will see insurance products and solutions

online. By effectively tapping the market as per changing demand and needs of the

customers, Aviva is able to maintain its unique position in the market.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT 4

Investment data analytics for the consumer insights: data analytics help in a long way

for understanding the customers. Most of the customers hold different insurance products that

help insurers in assessing the risk of individual. At the same time, Aviva has also made

investment in areas of weather analytics solutions and predictive analytics such as flood

mapping.

Legal factors: In UK, GDPR that is general data protection regulation has been brought

mainly in the insurance and finance sector. Research has shown that 54 per cent of the

businesses have made changes due to GDPR. GDPR also plays significant role in the Aviva

insurance company. For example: if any person will buy the product from its website or any

other channel, it will ask for the payment information. It also asks for personal information

when an individual applies for a policy. For this, it started using the underwriting engine that

takes account of information including postcode, address, age and other relevant information.

It has also stated that at the time of carrying out the health and travel policy it tends to use the

personal information to underwrite, arrange, or manage the policy as well as preventing fraud

(Rose, 2013).

Environmental factors: due to the increasing concern of the customers as well as government

on the environment, it becomes essential for the organisation to take environmental measures.

Similarly, Aviva has also assigned the investment of around £1.8 billion of the new

investment in solar, wind, energy, and biomass efficiency. Besides this, Aviva also holds

around £3 billion in the green bonds for supporting the transition in becoming a low carbon

economy. The chief of Aviva has stated that sustainability should be treated as a competitive

sport. Not only this, Aviva with the help of Climate Care tends to give emphasis on the

household energy saving technologies. For example Aviva has done the significant

investment in “Treadle Pump Project” that empowers the smallholder in developing country

named India to purchase affordable and simple pumps. This project also helps in tackling the

rural poverty by enabling the farmers in increasing yield. In this way, Aviva insurance is

taking several initiatives not only in UK but also in other countries (Geneva Association,

2014).

Investment data analytics for the consumer insights: data analytics help in a long way

for understanding the customers. Most of the customers hold different insurance products that

help insurers in assessing the risk of individual. At the same time, Aviva has also made

investment in areas of weather analytics solutions and predictive analytics such as flood

mapping.

Legal factors: In UK, GDPR that is general data protection regulation has been brought

mainly in the insurance and finance sector. Research has shown that 54 per cent of the

businesses have made changes due to GDPR. GDPR also plays significant role in the Aviva

insurance company. For example: if any person will buy the product from its website or any

other channel, it will ask for the payment information. It also asks for personal information

when an individual applies for a policy. For this, it started using the underwriting engine that

takes account of information including postcode, address, age and other relevant information.

It has also stated that at the time of carrying out the health and travel policy it tends to use the

personal information to underwrite, arrange, or manage the policy as well as preventing fraud

(Rose, 2013).

Environmental factors: due to the increasing concern of the customers as well as government

on the environment, it becomes essential for the organisation to take environmental measures.

Similarly, Aviva has also assigned the investment of around £1.8 billion of the new

investment in solar, wind, energy, and biomass efficiency. Besides this, Aviva also holds

around £3 billion in the green bonds for supporting the transition in becoming a low carbon

economy. The chief of Aviva has stated that sustainability should be treated as a competitive

sport. Not only this, Aviva with the help of Climate Care tends to give emphasis on the

household energy saving technologies. For example Aviva has done the significant

investment in “Treadle Pump Project” that empowers the smallholder in developing country

named India to purchase affordable and simple pumps. This project also helps in tackling the

rural poverty by enabling the farmers in increasing yield. In this way, Aviva insurance is

taking several initiatives not only in UK but also in other countries (Geneva Association,

2014).

MANAGEMENT 5

Impact of climate change on insurance company

It is true that the physical effect of climate change put the impact on value of all

classes of assets. However, there is no such particular mechanism to price carbon. Climate

change put a significant impact on the business model of Aviva. The next impact of climate

change is on the Aviva insurance business where company serves the 33 million customers.

It is found that ability of global insurance industry in making the social risk is threatened by

climate change. It is also said that the industry must make use of the risk management expert

to convince the policymakers. Insurance provides a significant role in providing support to

people in time of need. Due to this, it put pressure on the insurance companies to help society

in adapting and becoming more resilient to the changes related to climate change. Concerning

climate change, Aviva has stated that climate change effects directly affect its business. This

also presents a risk to financial stability over the decades.

If company is not able to adapt to climate change, it might affect the corporate debt,

equity, real estate, sovereign debt, as well as infrastructure assets. Insurance company is on

the front line in the battle against climate change. They have to pay more to the policyholders

as extreme weather such as drought, flooding, heatwaves, as well as storms become more

frequent. Insurance companies also have to face several significant losses as climate change

directly hit the company they invest in. The impact of climate change risk is proving to be

growing reality for the insurance sector. Aviva decision-making also impacted due to weather

related financial regulatory, losses and technological changes, health impacts, liability risks.

In this way, it can be stated that tackling climate change has become a necessity. Financial

sector is therefore required to develop the instruments and approaches for making

environment finance a major priority.

Aviva Insurance Company action on climate change

Firstly, Aviva anticipates the unmitigated climate related risk by presenting the threat

to financial stability. It is also taking action today to measure, identify, measure, monitor as

well as report the climate related opportunities and risk. Aviva has also made significant

investment of around £4.4 billion since 2015 in the green assets. At the same time, it

Impact of climate change on insurance company

It is true that the physical effect of climate change put the impact on value of all

classes of assets. However, there is no such particular mechanism to price carbon. Climate

change put a significant impact on the business model of Aviva. The next impact of climate

change is on the Aviva insurance business where company serves the 33 million customers.

It is found that ability of global insurance industry in making the social risk is threatened by

climate change. It is also said that the industry must make use of the risk management expert

to convince the policymakers. Insurance provides a significant role in providing support to

people in time of need. Due to this, it put pressure on the insurance companies to help society

in adapting and becoming more resilient to the changes related to climate change. Concerning

climate change, Aviva has stated that climate change effects directly affect its business. This

also presents a risk to financial stability over the decades.

If company is not able to adapt to climate change, it might affect the corporate debt,

equity, real estate, sovereign debt, as well as infrastructure assets. Insurance company is on

the front line in the battle against climate change. They have to pay more to the policyholders

as extreme weather such as drought, flooding, heatwaves, as well as storms become more

frequent. Insurance companies also have to face several significant losses as climate change

directly hit the company they invest in. The impact of climate change risk is proving to be

growing reality for the insurance sector. Aviva decision-making also impacted due to weather

related financial regulatory, losses and technological changes, health impacts, liability risks.

In this way, it can be stated that tackling climate change has become a necessity. Financial

sector is therefore required to develop the instruments and approaches for making

environment finance a major priority.

Aviva Insurance Company action on climate change

Firstly, Aviva anticipates the unmitigated climate related risk by presenting the threat

to financial stability. It is also taking action today to measure, identify, measure, monitor as

well as report the climate related opportunities and risk. Aviva has also made significant

investment of around £4.4 billion since 2015 in the green assets. At the same time, it

MANAGEMENT 6

welcomes the suggestions of “Financial stability board task force on the TCFD that is climate

related financial disclosures.” Aviva is also developing the climate VAR (value at risk)

measure in conjunction with UNEP FI (UN Environment Programme Finance Initiative

Investor Pilot Project. this tends to enable the investors to measure the significant business

impact of the climate related opportunities and risks on their corporate bond investment and

equity. Aviva has also extended this measure with the qualification expert consultancy and

risk management named Elseware to cover the classes of other assets (Brigham, Kiosse &

Otley, 2010).

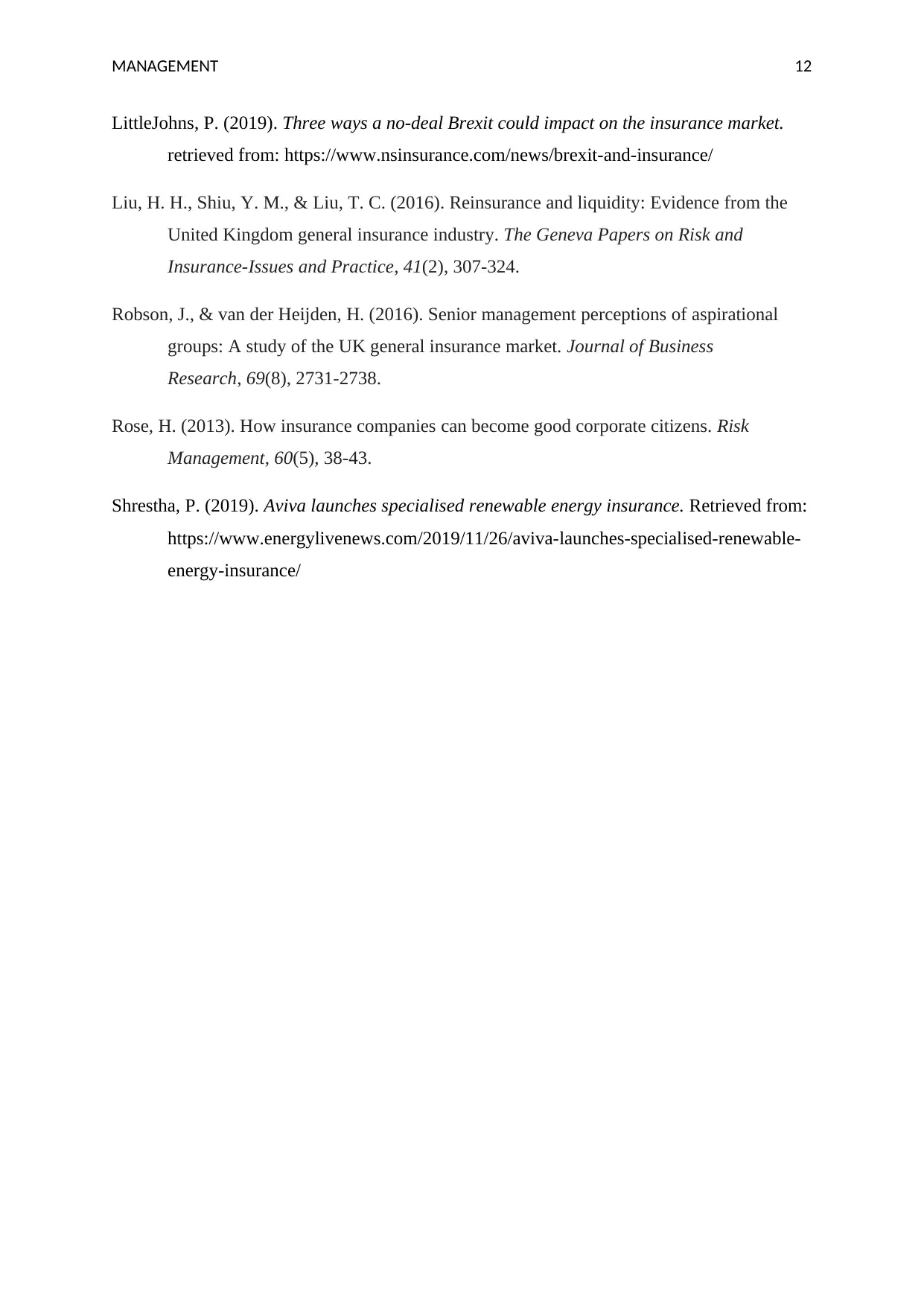

The same climate VAR measure provides the forward looking and holistic approach

view of the climate related transition, opportunities, and physical risk to the business of

Aviva. Transition risk and opportunities include the projected cost of the policy action that

has the objective to limit the emission of greenhouse gas. Besides this, physical risk includes

the financial impact of climate change with the help of extreme weather.

For supporting this initiative, an internal interdisciplinary team has been created with

the representation from business to manage the daily projects. Besides this, it has also

established the expert pane to challenge and review the major assumptions made in

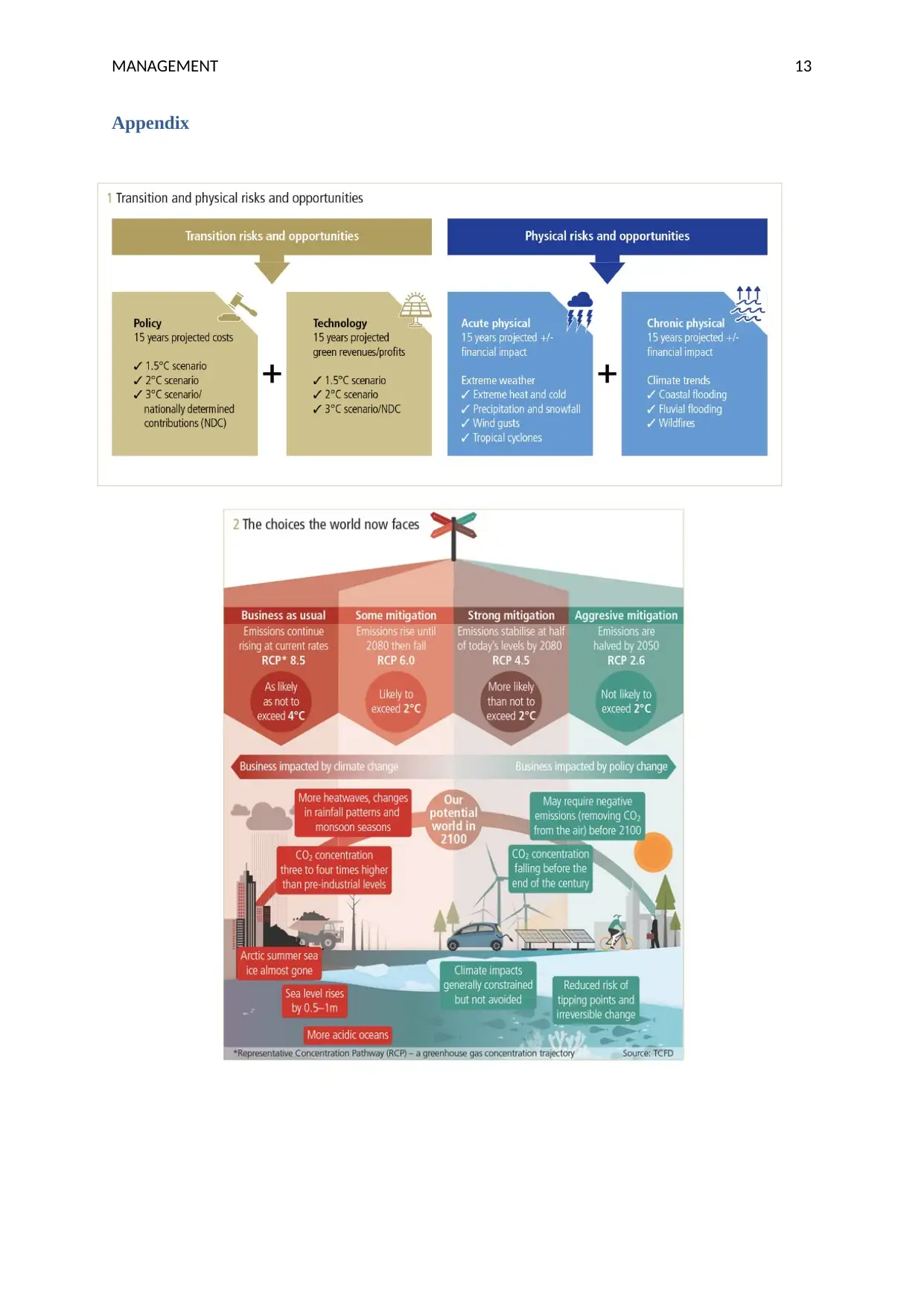

development, selection and modelling of the scenarios. Four scenarios have been identified in

respect to climate change. Every identified scenario describes the greenhouse future as well

as some other pollutants (LittleJohns, 2019).

It is found that every scenario tends to assume the gradual path where temperature

increases slowly but the policy of climate ramped up in different speeds with high degree of

coordination. In the special report of IPCC, it is indicated that the need to take action is to

keep the warming below the temperature of 1.5°C. Industry is required to slash the CO2

emission by 65 to 90 per cent by 2050 (Gurenko, 2015).

Climate neutral programme has also helped the Aviva in offsetting its carbon

emission through climate care projects. Climate Neutral Now is community of organisations

across the world to become climate neutral. Aviva is one such organisation who is part of the

campaign. Other firms such as Adidas and Microsoft are not taking any action but insisting

other firms take several measures (Robson & van der Heijden, 2016). Through the

collaboration of London Benchmarking Group, it has also provided new ways to measure the

social impact of carbon related projects. This tool has also assisted the Aviva to highlight that

its programme has helped around 1.1 million people. This has helped the Aviva to win

welcomes the suggestions of “Financial stability board task force on the TCFD that is climate

related financial disclosures.” Aviva is also developing the climate VAR (value at risk)

measure in conjunction with UNEP FI (UN Environment Programme Finance Initiative

Investor Pilot Project. this tends to enable the investors to measure the significant business

impact of the climate related opportunities and risks on their corporate bond investment and

equity. Aviva has also extended this measure with the qualification expert consultancy and

risk management named Elseware to cover the classes of other assets (Brigham, Kiosse &

Otley, 2010).

The same climate VAR measure provides the forward looking and holistic approach

view of the climate related transition, opportunities, and physical risk to the business of

Aviva. Transition risk and opportunities include the projected cost of the policy action that

has the objective to limit the emission of greenhouse gas. Besides this, physical risk includes

the financial impact of climate change with the help of extreme weather.

For supporting this initiative, an internal interdisciplinary team has been created with

the representation from business to manage the daily projects. Besides this, it has also

established the expert pane to challenge and review the major assumptions made in

development, selection and modelling of the scenarios. Four scenarios have been identified in

respect to climate change. Every identified scenario describes the greenhouse future as well

as some other pollutants (LittleJohns, 2019).

It is found that every scenario tends to assume the gradual path where temperature

increases slowly but the policy of climate ramped up in different speeds with high degree of

coordination. In the special report of IPCC, it is indicated that the need to take action is to

keep the warming below the temperature of 1.5°C. Industry is required to slash the CO2

emission by 65 to 90 per cent by 2050 (Gurenko, 2015).

Climate neutral programme has also helped the Aviva in offsetting its carbon

emission through climate care projects. Climate Neutral Now is community of organisations

across the world to become climate neutral. Aviva is one such organisation who is part of the

campaign. Other firms such as Adidas and Microsoft are not taking any action but insisting

other firms take several measures (Robson & van der Heijden, 2016). Through the

collaboration of London Benchmarking Group, it has also provided new ways to measure the

social impact of carbon related projects. This tool has also assisted the Aviva to highlight that

its programme has helped around 1.1 million people. This has helped the Aviva to win

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 7

“UNFCCC Momentum” for the change award. Climate care has also Aviva in

communicating its positive outcomes to the stakeholders with confidence and clarity.

Employees also stated that Aviva is making a positive contribution to the world. In this way,

Aviva has worked with the development and climate experts for its carbon related

programme.

It has also designed the integrated package for supporting the large renewable energy

companies across the world launched by Aviva. Renewable energy of Aviva tends to cover

the insurance of companies who have operation in the overseas and home markets that

include technologies such as solar power, onshore wind farms, as well as battery storage.

Through this, commercial customers will be easily able to get the single package of insurance

for covering the whole lifecycle in areas such as operation, construction, marine project,

terrorism as well as third party liability. It is one such initiative taken by Aviva for supporting

actions to contribute toward the UK target of “net zero emission” by 2050. In order to

manage climate change, Aviva has also set the objective to cut its emission by 70 per cent by

2030. In the starting of 2019, Aviva UK excited the operational fossil fuel market to tackle

climate change (Infopro, 2016).

In addition to the above concerns, Aviva Company is also doing disinvestment

wherever it is necessary. The disinvestment in unnecessary is helping it focus on the core

areas. Therefore, the output by those is helping it in bringing growth in the right manner. In

the year 2015, Aviva has identified that around 40 companies are making their business

revenue from coal mining. It continuously engages with those companies of engaging them

for transition. It is also supporting them to reduce greenhouse gas emission (Liu Shiu & Liu,

2016). For the global brokers and its commercial clients, Aviva has introduced new or

modified insurance packages. These modified packages are helping it in moving on the right

direction that ultimately helps the company in achieving success and growth. It is also taking

significant set up in its commitment by bringing the special renewable energy proposition by

proving the insurance solutions for renewable energy related risk. It has however stated that

this is small set up in its sustainability journey. However, it is already working with the

largest clients and brokers to ensure that they will remain as the partner of choice (Shrestha,

2019).

In every scenario, the impact of insurance liability is more limited as compared to

investment return. In spite of this, there is potential for some impact on the pensions and life

“UNFCCC Momentum” for the change award. Climate care has also Aviva in

communicating its positive outcomes to the stakeholders with confidence and clarity.

Employees also stated that Aviva is making a positive contribution to the world. In this way,

Aviva has worked with the development and climate experts for its carbon related

programme.

It has also designed the integrated package for supporting the large renewable energy

companies across the world launched by Aviva. Renewable energy of Aviva tends to cover

the insurance of companies who have operation in the overseas and home markets that

include technologies such as solar power, onshore wind farms, as well as battery storage.

Through this, commercial customers will be easily able to get the single package of insurance

for covering the whole lifecycle in areas such as operation, construction, marine project,

terrorism as well as third party liability. It is one such initiative taken by Aviva for supporting

actions to contribute toward the UK target of “net zero emission” by 2050. In order to

manage climate change, Aviva has also set the objective to cut its emission by 70 per cent by

2030. In the starting of 2019, Aviva UK excited the operational fossil fuel market to tackle

climate change (Infopro, 2016).

In addition to the above concerns, Aviva Company is also doing disinvestment

wherever it is necessary. The disinvestment in unnecessary is helping it focus on the core

areas. Therefore, the output by those is helping it in bringing growth in the right manner. In

the year 2015, Aviva has identified that around 40 companies are making their business

revenue from coal mining. It continuously engages with those companies of engaging them

for transition. It is also supporting them to reduce greenhouse gas emission (Liu Shiu & Liu,

2016). For the global brokers and its commercial clients, Aviva has introduced new or

modified insurance packages. These modified packages are helping it in moving on the right

direction that ultimately helps the company in achieving success and growth. It is also taking

significant set up in its commitment by bringing the special renewable energy proposition by

proving the insurance solutions for renewable energy related risk. It has however stated that

this is small set up in its sustainability journey. However, it is already working with the

largest clients and brokers to ensure that they will remain as the partner of choice (Shrestha,

2019).

In every scenario, the impact of insurance liability is more limited as compared to

investment return. In spite of this, there is potential for some impact on the pensions and life

MANAGEMENT 8

businesses due to the changes in mortality rates in varied scenarios. General insurance

liability is also limited due to the short term nature of business. The physical effect of climate

change will also result in more risk. Aviva will regularly incorporate and develop the climate

VAR into the overall strategy focusing on the impact of climate related opportunities and

risks. In UK more than 400 employees have at least signed up the car share programme.

Aviva has also come up with the electric charging vehicle at the eight different locations of

UK.

In the September 2018, Aviva insurance has also launched the WBA (World

benchmarking alliance) as its founding partner with the United Nations and Index Initiatives

at the General assembly of UN (Crick, Jenkins & Surminski, 2018). The initiative has also

been funded by the Dutch, UK and Danish government by publishing transparent and free

benchmark ranking companies on the contribution toward achievement of SDGs (Sustainable

development goals). This will increase the accountability and transparency for business

related to SDGs. The main objective of this is to empower the investors, consumers, civil

society and government organisations by providing them insight and data that shows the

company performance relate to SDGs.

In addition to the above actions, Aviva Insurance also uses detailed topographical data

in assessing different flood risks for those houses that are at the top of hills. As an insurer,

Aviva also engages in the price differentiation from the insurance of property (Keskitalo,

Vulturius & Scholten, 2014).

Recommendations

Firstly, it is suggested to insurance industry for continuing to institutionalise the

climate change as major business issue as well as expanding its contribution toward the

building of financial resilience to climate risk. It should also explore the ways for supporting

the decarbonised infrastructure and climate resilient through the underwriting, industry risk

management and investment function. It is also suggested to review the integrate and sound

public authority risk management strategy. The effective coordination of the dissemination of

the data can be easily integrated and interpreted into the decision-0making process of private

and public stakeholders as well as should be used by insurer in appropriate insurance cover.

In addition to this, the monitoring of the implementation of adaptation strategies as well as

businesses due to the changes in mortality rates in varied scenarios. General insurance

liability is also limited due to the short term nature of business. The physical effect of climate

change will also result in more risk. Aviva will regularly incorporate and develop the climate

VAR into the overall strategy focusing on the impact of climate related opportunities and

risks. In UK more than 400 employees have at least signed up the car share programme.

Aviva has also come up with the electric charging vehicle at the eight different locations of

UK.

In the September 2018, Aviva insurance has also launched the WBA (World

benchmarking alliance) as its founding partner with the United Nations and Index Initiatives

at the General assembly of UN (Crick, Jenkins & Surminski, 2018). The initiative has also

been funded by the Dutch, UK and Danish government by publishing transparent and free

benchmark ranking companies on the contribution toward achievement of SDGs (Sustainable

development goals). This will increase the accountability and transparency for business

related to SDGs. The main objective of this is to empower the investors, consumers, civil

society and government organisations by providing them insight and data that shows the

company performance relate to SDGs.

In addition to the above actions, Aviva Insurance also uses detailed topographical data

in assessing different flood risks for those houses that are at the top of hills. As an insurer,

Aviva also engages in the price differentiation from the insurance of property (Keskitalo,

Vulturius & Scholten, 2014).

Recommendations

Firstly, it is suggested to insurance industry for continuing to institutionalise the

climate change as major business issue as well as expanding its contribution toward the

building of financial resilience to climate risk. It should also explore the ways for supporting

the decarbonised infrastructure and climate resilient through the underwriting, industry risk

management and investment function. It is also suggested to review the integrate and sound

public authority risk management strategy. The effective coordination of the dissemination of

the data can be easily integrated and interpreted into the decision-0making process of private

and public stakeholders as well as should be used by insurer in appropriate insurance cover.

In addition to this, the monitoring of the implementation of adaptation strategies as well as

MANAGEMENT 9

their effect on the vulnerability is suggested to disseminate the best practice as well as taking

corrective measures (Ansah & Sorooshian, 2019). It is true that the impact of climate change

risk is proving to be growing reality for the insurance sector. Due to this, insurance

companies decision-making also impacted due to weather losses and technological changes,

health impacts, as well as liability risks.

In addition to this, it is also recommended to Policymakers for incentivising institutional

investment in the green bond. It will also be better to create a green bind framework. Aviva

insurance should also work more on the business coalitions for enacting legislation in

reducing the greenhouse gases. By sponsoring the research, it can work on reducing the

carbon emission especially in developing countries. Contribution is also made toward

renewable energy projects and reforestation. By providing several benefits, employees can

also be encouraged to adopt green policies (Crichton, 2018).

Aviva can give more emphasis on offering discounts to its customers who invest in

their self protection. For example, people, who take steps in protecting their house from

wildfire, will be given discount. This will help it in contributing to the environment and will

bring positive image for the organisation. Aviva can also increase its investment in energy

deficiency and low carbon energy technology. Transport and building will also require to

shift heavily toward green electricity (BPA Worldwide, 2017). Aviva Investor Climate

Transition Equity Fund that is supported by £100 million seed investment from the Aviva

France. The fund will, however, need a long term and good investment approach in order to

address climate change mitigation.

their effect on the vulnerability is suggested to disseminate the best practice as well as taking

corrective measures (Ansah & Sorooshian, 2019). It is true that the impact of climate change

risk is proving to be growing reality for the insurance sector. Due to this, insurance

companies decision-making also impacted due to weather losses and technological changes,

health impacts, as well as liability risks.

In addition to this, it is also recommended to Policymakers for incentivising institutional

investment in the green bond. It will also be better to create a green bind framework. Aviva

insurance should also work more on the business coalitions for enacting legislation in

reducing the greenhouse gases. By sponsoring the research, it can work on reducing the

carbon emission especially in developing countries. Contribution is also made toward

renewable energy projects and reforestation. By providing several benefits, employees can

also be encouraged to adopt green policies (Crichton, 2018).

Aviva can give more emphasis on offering discounts to its customers who invest in

their self protection. For example, people, who take steps in protecting their house from

wildfire, will be given discount. This will help it in contributing to the environment and will

bring positive image for the organisation. Aviva can also increase its investment in energy

deficiency and low carbon energy technology. Transport and building will also require to

shift heavily toward green electricity (BPA Worldwide, 2017). Aviva Investor Climate

Transition Equity Fund that is supported by £100 million seed investment from the Aviva

France. The fund will, however, need a long term and good investment approach in order to

address climate change mitigation.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT 10

Conclusion

In the limelight of above discussion, it can be concluded that Aviva Insurance is

working well in the UK by providing several services as per the changing need of the

customers. It has also started digital platform due to the changing need of the customers.

Aviva has also made significant investment of around £4.4 billion since 2015 in the green

assets. In addition to this, it is also investing in several projects to bring the positive impact of

climate change on society as well as on the insurance industry. Aviva has introduced new or

modified insurance packages. These modified packages will definitely help Aviva in going to

the right direction. The increasing climate change problem also requires several changes.

Therefore, it is suggested to make the best use of computer models. Those persons should be

hired who have the best knowledge about research and forecasting the weather effectively.

By doing this, it can also assist the people regarding climate changes. As a result, it will

ultimately help the company in achieving success and growth. Aviva gives emphasis on the

different customers' needs related to health and life insurance to pension.

Conclusion

In the limelight of above discussion, it can be concluded that Aviva Insurance is

working well in the UK by providing several services as per the changing need of the

customers. It has also started digital platform due to the changing need of the customers.

Aviva has also made significant investment of around £4.4 billion since 2015 in the green

assets. In addition to this, it is also investing in several projects to bring the positive impact of

climate change on society as well as on the insurance industry. Aviva has introduced new or

modified insurance packages. These modified packages will definitely help Aviva in going to

the right direction. The increasing climate change problem also requires several changes.

Therefore, it is suggested to make the best use of computer models. Those persons should be

hired who have the best knowledge about research and forecasting the weather effectively.

By doing this, it can also assist the people regarding climate changes. As a result, it will

ultimately help the company in achieving success and growth. Aviva gives emphasis on the

different customers' needs related to health and life insurance to pension.

MANAGEMENT 11

References

Ansah, R. H., & Sorooshian, S. (2019). Green economy: Private sectors’ response to climate

change. Environmental Quality Management, 28(3), 63-69.

BPA Wolrdwide. (2017). Aviva joins UN climate change campaign. Retrieved from:

https://www.insurancebusinessmag.com/uk/news/environmental/aviva-joins-un-

climate-change-campaign-65075.aspx

Brigham, M., Kiosse, P. V., & Otley, D. (2010). ‘One Aviva, Twice the Value’: Connecting

Sustainability at Aviva plc. In Accounting for Sustainability (pp. 209-232). Routledge.

Crichton, D. (2018). The role of private insurance companies in managing flood risks in the

UK and Europe. In Urban flood management (pp. 83-100). CRC Press.

Crick, F., Jenkins, K., & Surminski, S. (2018). Strengthening insurance partnerships in the

face of climate change–insights from an agent-based model of flood insurance in the

UK. Science of the total environment, 636, 192-204.

Crick, F., Jenkins, K., & Surminski, S. (2018). Strengthening insurance partnerships in the

face of climate change–insights from an agent-based model of flood insurance in the

UK. Science of the total environment, 636, 192-204.

Geneva Association. (2014). The insurance industry and climate change-Contribution to the

global debate. The Geneva Reports, 2(1), 1-152.

Gurenko, E. N. (2015). Climate change and insurance: Disaster risk financing in developing

countries (Vol. 6, No. 6). Routledge.

Infopro. (2019). Navigating the impact of climate risk on financial stability. Retrieved from:

https://www.risk.net/risk-management/7147136/navigating-the-impact-of-climate-

risk-on-financial-stability

Keskitalo, E. C. H., Vulturius, G., & Scholten, P. (2014). Adaptation to climate change in the

insurance sector: examples from the UK, Germany and the Netherlands. Natural

Hazards, 71(1), 315-334.

References

Ansah, R. H., & Sorooshian, S. (2019). Green economy: Private sectors’ response to climate

change. Environmental Quality Management, 28(3), 63-69.

BPA Wolrdwide. (2017). Aviva joins UN climate change campaign. Retrieved from:

https://www.insurancebusinessmag.com/uk/news/environmental/aviva-joins-un-

climate-change-campaign-65075.aspx

Brigham, M., Kiosse, P. V., & Otley, D. (2010). ‘One Aviva, Twice the Value’: Connecting

Sustainability at Aviva plc. In Accounting for Sustainability (pp. 209-232). Routledge.

Crichton, D. (2018). The role of private insurance companies in managing flood risks in the

UK and Europe. In Urban flood management (pp. 83-100). CRC Press.

Crick, F., Jenkins, K., & Surminski, S. (2018). Strengthening insurance partnerships in the

face of climate change–insights from an agent-based model of flood insurance in the

UK. Science of the total environment, 636, 192-204.

Crick, F., Jenkins, K., & Surminski, S. (2018). Strengthening insurance partnerships in the

face of climate change–insights from an agent-based model of flood insurance in the

UK. Science of the total environment, 636, 192-204.

Geneva Association. (2014). The insurance industry and climate change-Contribution to the

global debate. The Geneva Reports, 2(1), 1-152.

Gurenko, E. N. (2015). Climate change and insurance: Disaster risk financing in developing

countries (Vol. 6, No. 6). Routledge.

Infopro. (2019). Navigating the impact of climate risk on financial stability. Retrieved from:

https://www.risk.net/risk-management/7147136/navigating-the-impact-of-climate-

risk-on-financial-stability

Keskitalo, E. C. H., Vulturius, G., & Scholten, P. (2014). Adaptation to climate change in the

insurance sector: examples from the UK, Germany and the Netherlands. Natural

Hazards, 71(1), 315-334.

MANAGEMENT 12

LittleJohns, P. (2019). Three ways a no-deal Brexit could impact on the insurance market.

retrieved from: https://www.nsinsurance.com/news/brexit-and-insurance/

Liu, H. H., Shiu, Y. M., & Liu, T. C. (2016). Reinsurance and liquidity: Evidence from the

United Kingdom general insurance industry. The Geneva Papers on Risk and

Insurance-Issues and Practice, 41(2), 307-324.

Robson, J., & van der Heijden, H. (2016). Senior management perceptions of aspirational

groups: A study of the UK general insurance market. Journal of Business

Research, 69(8), 2731-2738.

Rose, H. (2013). How insurance companies can become good corporate citizens. Risk

Management, 60(5), 38-43.

Shrestha, P. (2019). Aviva launches specialised renewable energy insurance. Retrieved from:

https://www.energylivenews.com/2019/11/26/aviva-launches-specialised-renewable-

energy-insurance/

LittleJohns, P. (2019). Three ways a no-deal Brexit could impact on the insurance market.

retrieved from: https://www.nsinsurance.com/news/brexit-and-insurance/

Liu, H. H., Shiu, Y. M., & Liu, T. C. (2016). Reinsurance and liquidity: Evidence from the

United Kingdom general insurance industry. The Geneva Papers on Risk and

Insurance-Issues and Practice, 41(2), 307-324.

Robson, J., & van der Heijden, H. (2016). Senior management perceptions of aspirational

groups: A study of the UK general insurance market. Journal of Business

Research, 69(8), 2731-2738.

Rose, H. (2013). How insurance companies can become good corporate citizens. Risk

Management, 60(5), 38-43.

Shrestha, P. (2019). Aviva launches specialised renewable energy insurance. Retrieved from:

https://www.energylivenews.com/2019/11/26/aviva-launches-specialised-renewable-

energy-insurance/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT 13

Appendix

Appendix

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.