University Financial Accounting: Consolidation and Goodwill Analysis

VerifiedAdded on 2023/06/10

|11

|1400

|222

Homework Assignment

AI Summary

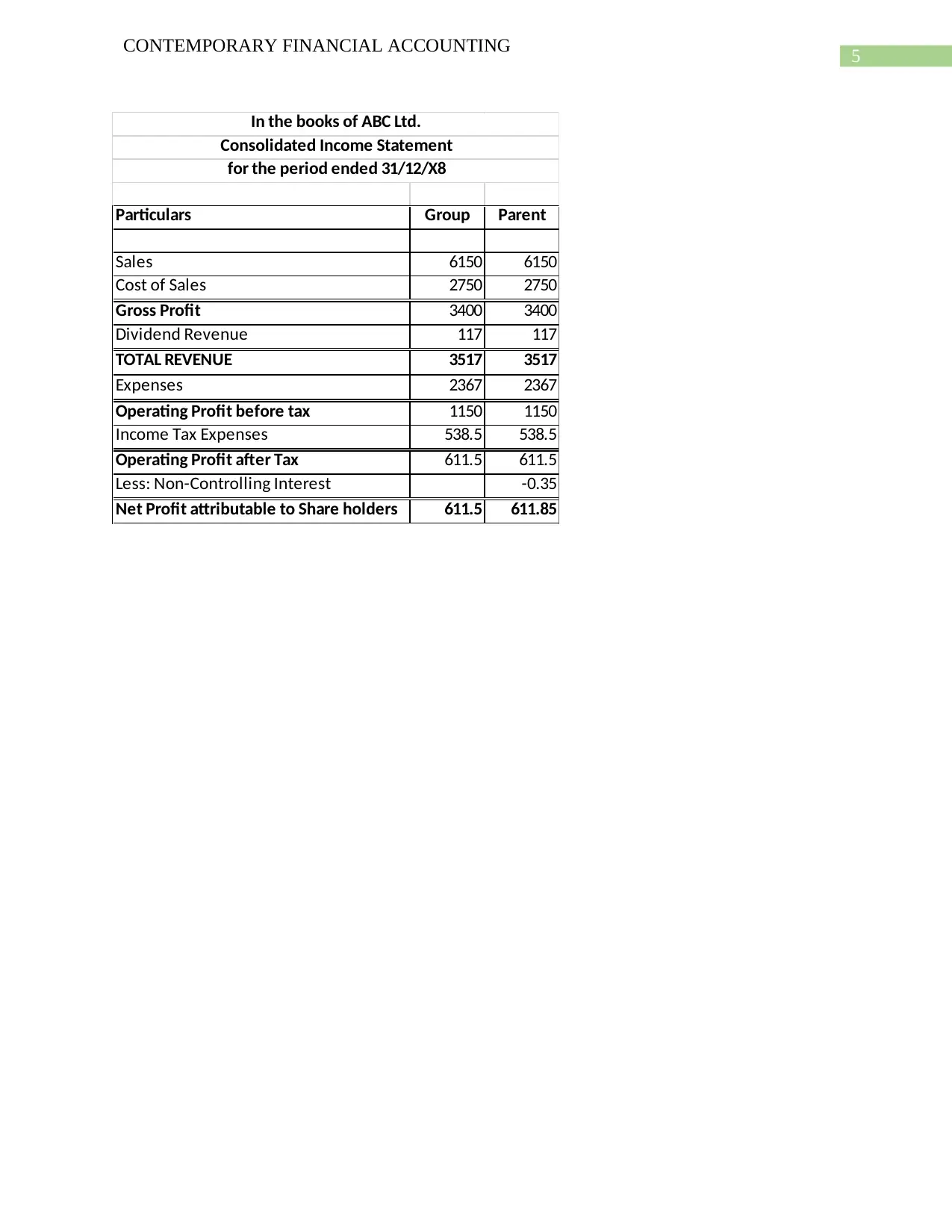

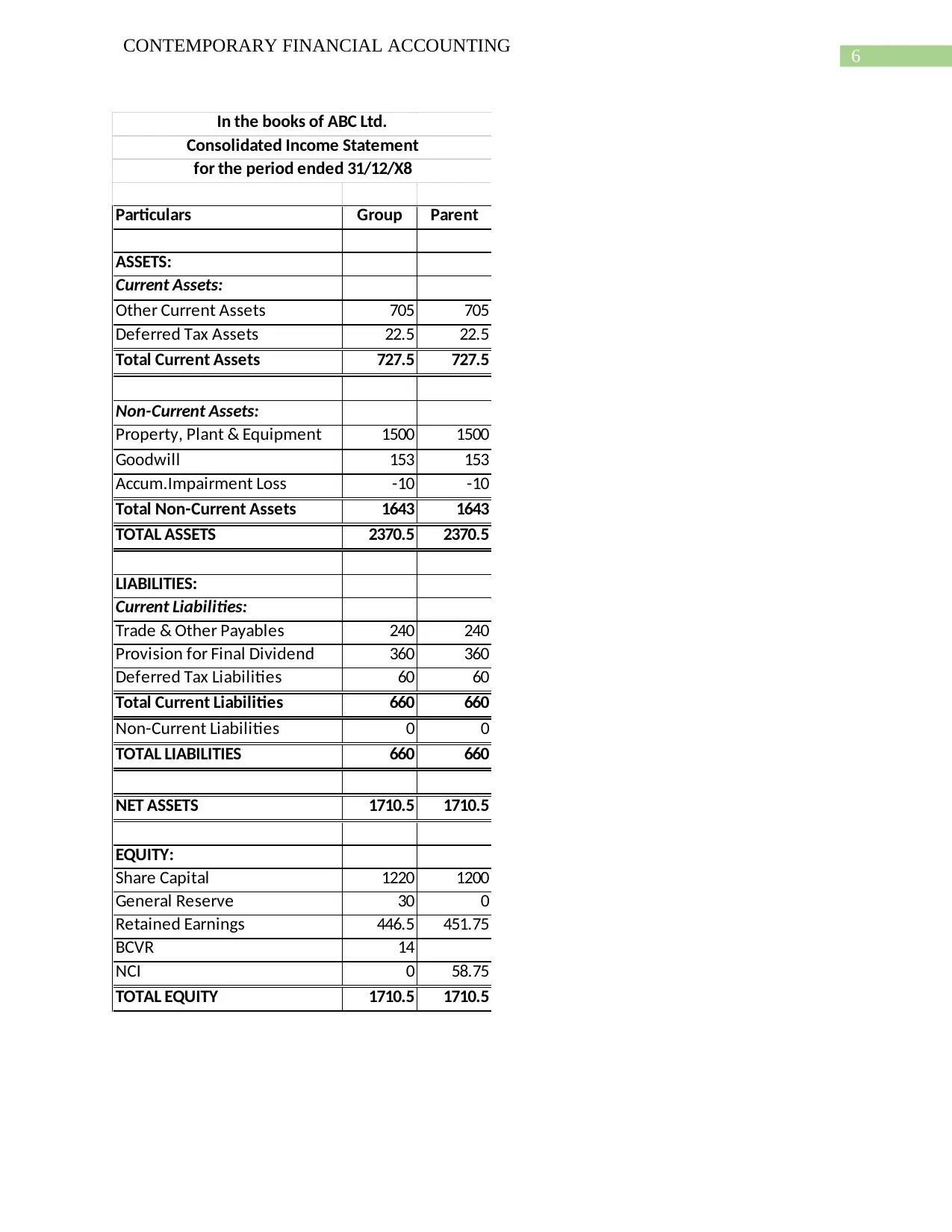

This financial accounting assignment addresses the consolidation of financial statements, specifically focusing on the acquisition of a subsidiary and the subsequent accounting for goodwill. The solution begins with journal entries to record the initial investment, followed by an acquisition analysis determining the fair value of net identifiable assets and liabilities. It includes detailed workings for the consolidated income statement, balance sheet, and retained earnings, reflecting adjustments for intercompany transactions and non-controlling interests. Furthermore, the assignment explores and compares the partial and full goodwill methods, detailing their application under IFRS and US GAAP, along with their respective advantages and disadvantages, with a focus on the recognition of controlling and non-controlling interests. Finally, the solution provides consolidated financial statements for the parent company, ABC Ltd. including a consolidated income statement and a consolidated balance sheet.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.