Analysis of Webjet's Financial Reporting: Conceptual Framework

VerifiedAdded on 2023/06/09

|15

|2314

|446

Report

AI Summary

This report provides a comprehensive analysis of Webjet Limited's financial reporting practices, focusing on its adherence to the Australian Accounting Standards Board (AASB) conceptual framework. The report begins with an executive summary, followed by an introduction outlining the objectives of the analysis. The core of the report examines the general purpose financial reporting objectives, recognition criteria for assets, liabilities, equity, revenue, and expenses, and the qualitative characteristics of financial reporting as applied by Webjet. The analysis draws on Webjet's 2017 Annual Report to illustrate the company's compliance with AASB guidelines. The report concludes with recommendations for maintaining compliance and avoiding accounting issues. The report is structured to provide a clear understanding of Webjet's financial reporting in accordance with the conceptual framework.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

From the analysis part of the report, it can be seen that Webjet adheres to the guidelines and

principles of AASB conceptual framework in order to prepare and present the financial

statements. Thus, full compliance of Webjet can be seen with the conceptual framework

objectives, criteria to recognize financial aspects and both fundamental and enhancing qualitative

characteristics.

Executive Summary

From the analysis part of the report, it can be seen that Webjet adheres to the guidelines and

principles of AASB conceptual framework in order to prepare and present the financial

statements. Thus, full compliance of Webjet can be seen with the conceptual framework

objectives, criteria to recognize financial aspects and both fundamental and enhancing qualitative

characteristics.

2CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

General Purpose Financial Reporting Objectives............................................................................3

Recognition Criteria.........................................................................................................................6

Qualitative Characteristics of Financial Reporting........................................................................10

Conclusion and Recommendations................................................................................................11

References......................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................3

General Purpose Financial Reporting Objectives............................................................................3

Recognition Criteria.........................................................................................................................6

Qualitative Characteristics of Financial Reporting........................................................................10

Conclusion and Recommendations................................................................................................11

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The objective of this report is to take into consideration the major aspects of accounting

conceptual framework for the companies operating in Australia. For the purpose of this report,

Webjet Limited (Webjet) is taken into consideration. It needs to be mentioned that Webjet is a

major online travel agency (OTA) having operation in the regions of both Australian and New-

Zealand. The company is well-known for its online travel tools and technology

(webjetlimited.com, 2018). This particulr report can be segregated into three major parts. The

main area of focus of the first part is to analyze the general purpose financial reporting

objectives. The aim of the second part is to analyze the adherence of Webjet with the recognition

criteria of conceptual framework. The last part emphasizes on the qualitative characteristics of

financial reporting.

General Purpose Financial Reporting Objectives

In Australia, the presence of the Conceptual Framework of Australian Accounting

Standard Board (AASB) can be seen that provides the companies with the required rules and

regulations for financial reporting and it is the responsibility of the companies to follow all these

rules and regulations of AASB conceptual framework (aasb.gov.au, 2018). This is also

applicable for Webjet. AASB conceptual framework has certain objectives that Webjet is needed

to take into consideration and the following discussion shows them:

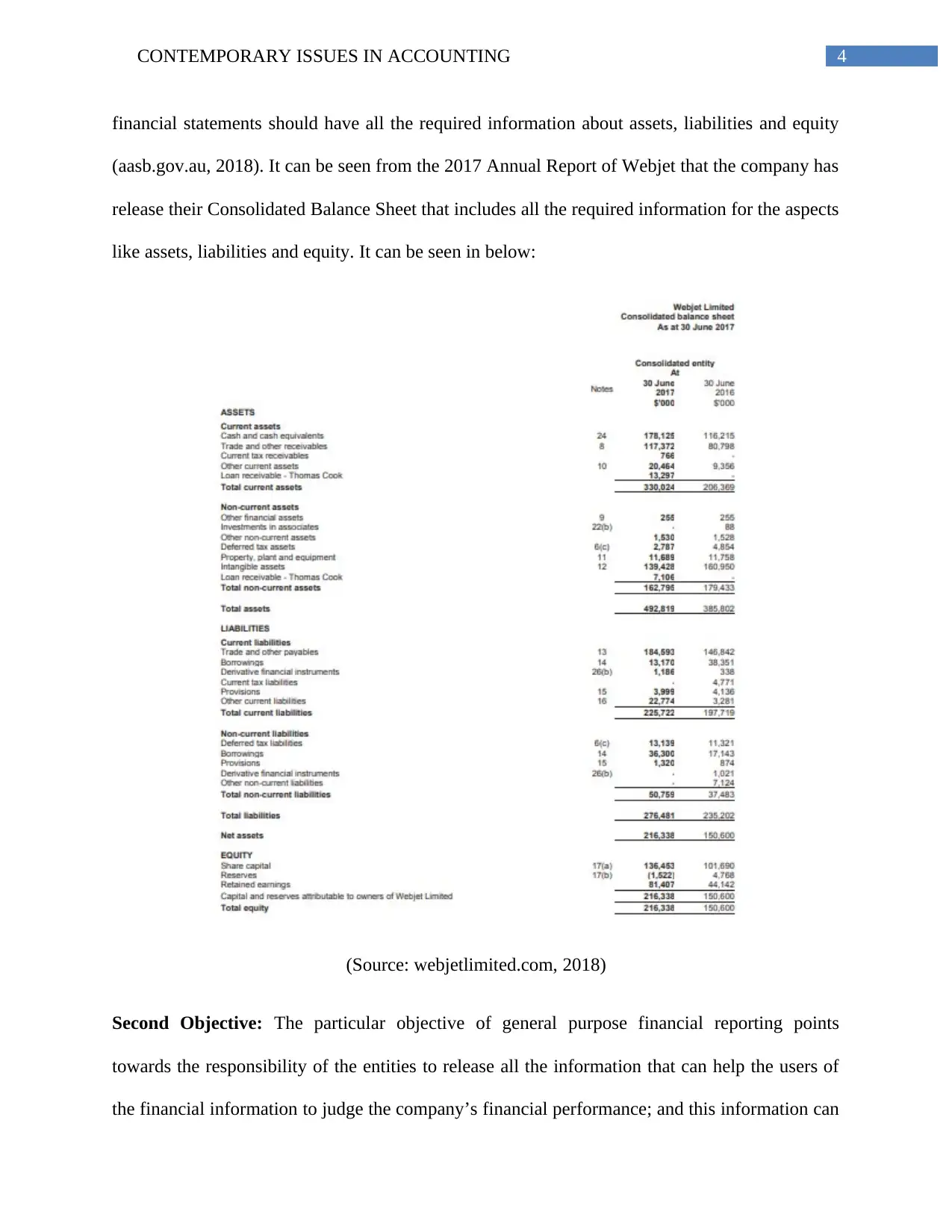

First Objective: This particular aim of general purpose financial reporting states that the

financial statements of the business organizations must contain the information that helps the

users of the financial information in assessing the current financial position. It implies that the

Introduction

The objective of this report is to take into consideration the major aspects of accounting

conceptual framework for the companies operating in Australia. For the purpose of this report,

Webjet Limited (Webjet) is taken into consideration. It needs to be mentioned that Webjet is a

major online travel agency (OTA) having operation in the regions of both Australian and New-

Zealand. The company is well-known for its online travel tools and technology

(webjetlimited.com, 2018). This particulr report can be segregated into three major parts. The

main area of focus of the first part is to analyze the general purpose financial reporting

objectives. The aim of the second part is to analyze the adherence of Webjet with the recognition

criteria of conceptual framework. The last part emphasizes on the qualitative characteristics of

financial reporting.

General Purpose Financial Reporting Objectives

In Australia, the presence of the Conceptual Framework of Australian Accounting

Standard Board (AASB) can be seen that provides the companies with the required rules and

regulations for financial reporting and it is the responsibility of the companies to follow all these

rules and regulations of AASB conceptual framework (aasb.gov.au, 2018). This is also

applicable for Webjet. AASB conceptual framework has certain objectives that Webjet is needed

to take into consideration and the following discussion shows them:

First Objective: This particular aim of general purpose financial reporting states that the

financial statements of the business organizations must contain the information that helps the

users of the financial information in assessing the current financial position. It implies that the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

financial statements should have all the required information about assets, liabilities and equity

(aasb.gov.au, 2018). It can be seen from the 2017 Annual Report of Webjet that the company has

release their Consolidated Balance Sheet that includes all the required information for the aspects

like assets, liabilities and equity. It can be seen in below:

(Source: webjetlimited.com, 2018)

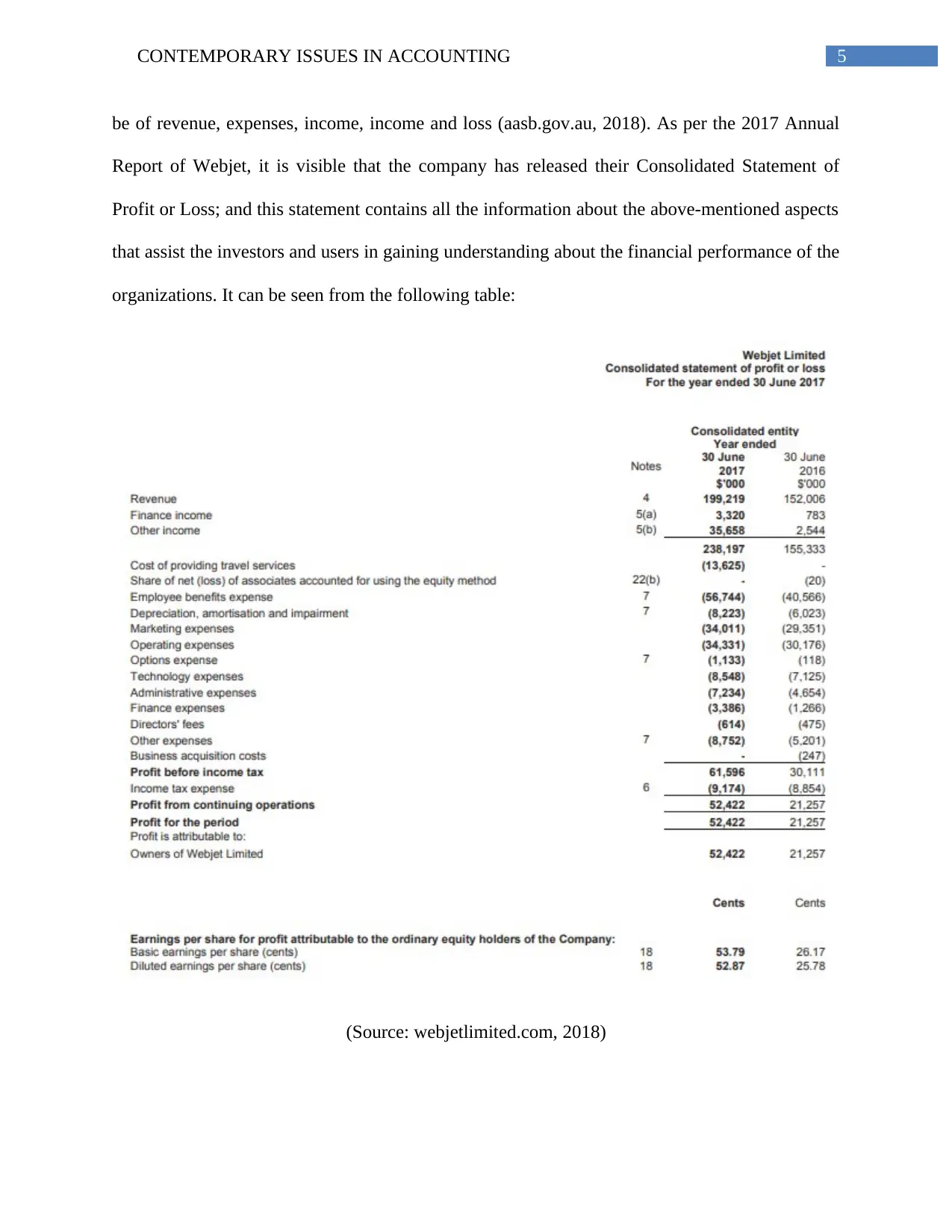

Second Objective: The particular objective of general purpose financial reporting points

towards the responsibility of the entities to release all the information that can help the users of

the financial information to judge the company’s financial performance; and this information can

financial statements should have all the required information about assets, liabilities and equity

(aasb.gov.au, 2018). It can be seen from the 2017 Annual Report of Webjet that the company has

release their Consolidated Balance Sheet that includes all the required information for the aspects

like assets, liabilities and equity. It can be seen in below:

(Source: webjetlimited.com, 2018)

Second Objective: The particular objective of general purpose financial reporting points

towards the responsibility of the entities to release all the information that can help the users of

the financial information to judge the company’s financial performance; and this information can

5CONTEMPORARY ISSUES IN ACCOUNTING

be of revenue, expenses, income, income and loss (aasb.gov.au, 2018). As per the 2017 Annual

Report of Webjet, it is visible that the company has released their Consolidated Statement of

Profit or Loss; and this statement contains all the information about the above-mentioned aspects

that assist the investors and users in gaining understanding about the financial performance of the

organizations. It can be seen from the following table:

(Source: webjetlimited.com, 2018)

be of revenue, expenses, income, income and loss (aasb.gov.au, 2018). As per the 2017 Annual

Report of Webjet, it is visible that the company has released their Consolidated Statement of

Profit or Loss; and this statement contains all the information about the above-mentioned aspects

that assist the investors and users in gaining understanding about the financial performance of the

organizations. It can be seen from the following table:

(Source: webjetlimited.com, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

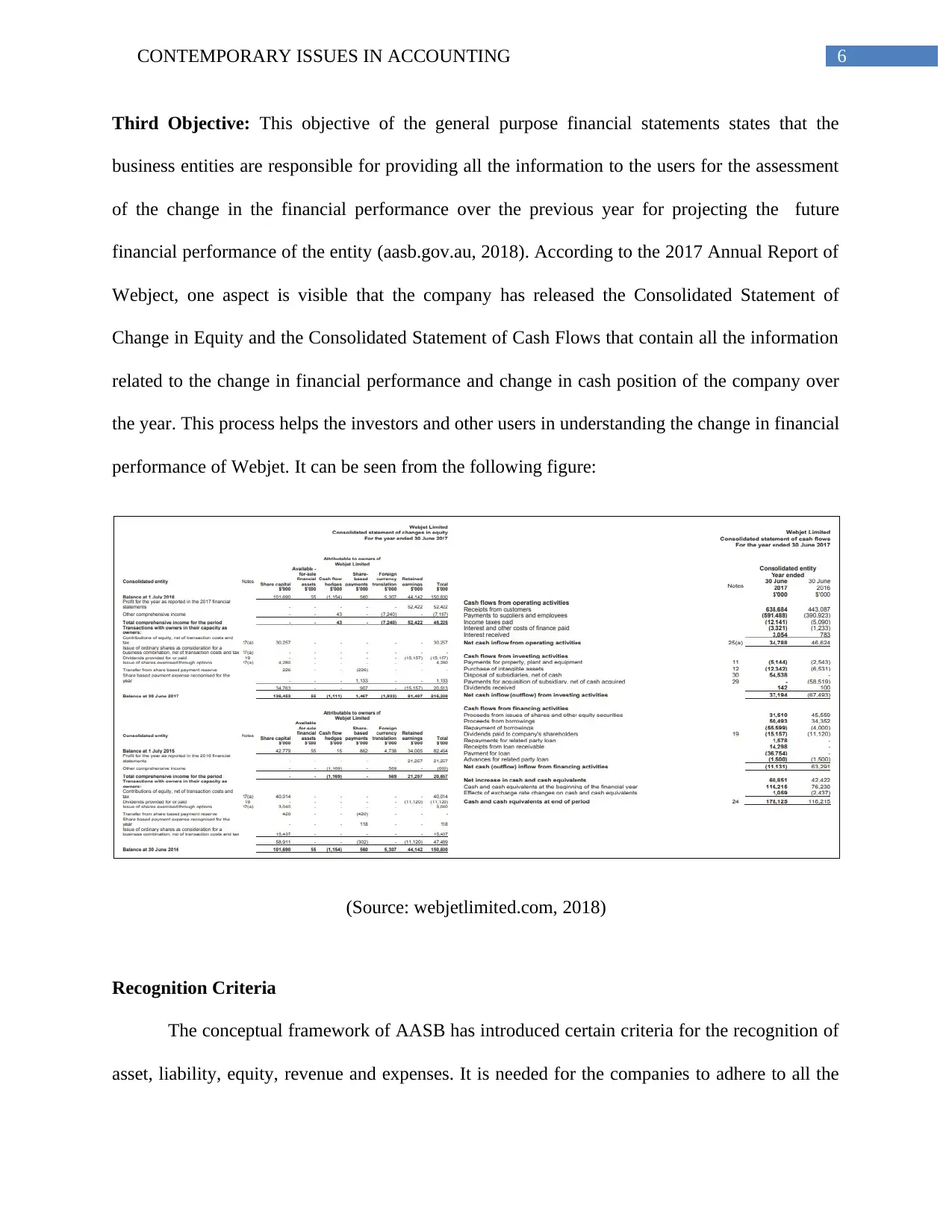

Third Objective: This objective of the general purpose financial statements states that the

business entities are responsible for providing all the information to the users for the assessment

of the change in the financial performance over the previous year for projecting the future

financial performance of the entity (aasb.gov.au, 2018). According to the 2017 Annual Report of

Webject, one aspect is visible that the company has released the Consolidated Statement of

Change in Equity and the Consolidated Statement of Cash Flows that contain all the information

related to the change in financial performance and change in cash position of the company over

the year. This process helps the investors and other users in understanding the change in financial

performance of Webjet. It can be seen from the following figure:

(Source: webjetlimited.com, 2018)

Recognition Criteria

The conceptual framework of AASB has introduced certain criteria for the recognition of

asset, liability, equity, revenue and expenses. It is needed for the companies to adhere to all the

Third Objective: This objective of the general purpose financial statements states that the

business entities are responsible for providing all the information to the users for the assessment

of the change in the financial performance over the previous year for projecting the future

financial performance of the entity (aasb.gov.au, 2018). According to the 2017 Annual Report of

Webject, one aspect is visible that the company has released the Consolidated Statement of

Change in Equity and the Consolidated Statement of Cash Flows that contain all the information

related to the change in financial performance and change in cash position of the company over

the year. This process helps the investors and other users in understanding the change in financial

performance of Webjet. It can be seen from the following figure:

(Source: webjetlimited.com, 2018)

Recognition Criteria

The conceptual framework of AASB has introduced certain criteria for the recognition of

asset, liability, equity, revenue and expenses. It is needed for the companies to adhere to all the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

recognition criteria at the time to recognize the above-mentioned financial aspects. This aspect is

also applicable for the financial reporting of Webjet and these are shown below:

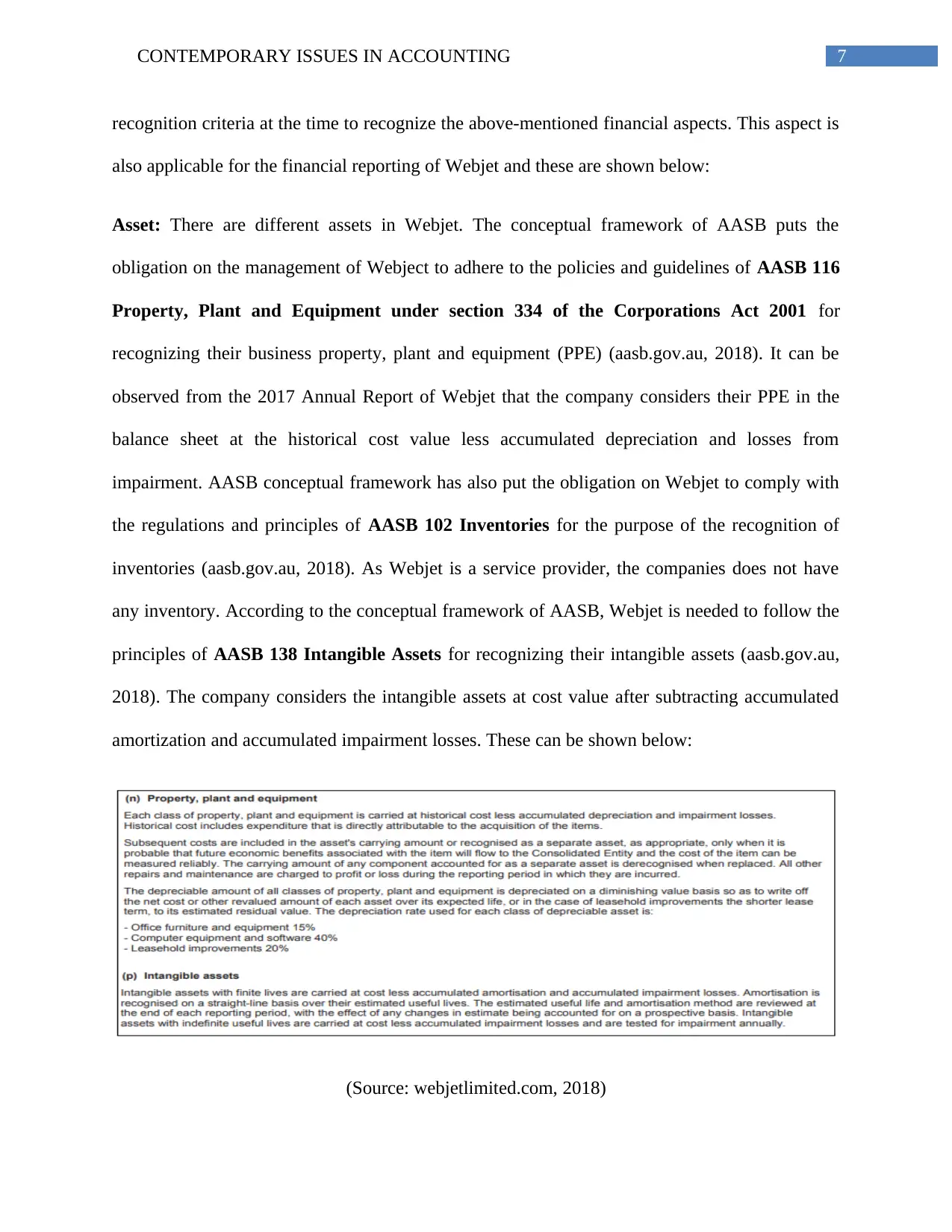

Asset: There are different assets in Webjet. The conceptual framework of AASB puts the

obligation on the management of Webject to adhere to the policies and guidelines of AASB 116

Property, Plant and Equipment under section 334 of the Corporations Act 2001 for

recognizing their business property, plant and equipment (PPE) (aasb.gov.au, 2018). It can be

observed from the 2017 Annual Report of Webjet that the company considers their PPE in the

balance sheet at the historical cost value less accumulated depreciation and losses from

impairment. AASB conceptual framework has also put the obligation on Webjet to comply with

the regulations and principles of AASB 102 Inventories for the purpose of the recognition of

inventories (aasb.gov.au, 2018). As Webjet is a service provider, the companies does not have

any inventory. According to the conceptual framework of AASB, Webjet is needed to follow the

principles of AASB 138 Intangible Assets for recognizing their intangible assets (aasb.gov.au,

2018). The company considers the intangible assets at cost value after subtracting accumulated

amortization and accumulated impairment losses. These can be shown below:

(Source: webjetlimited.com, 2018)

recognition criteria at the time to recognize the above-mentioned financial aspects. This aspect is

also applicable for the financial reporting of Webjet and these are shown below:

Asset: There are different assets in Webjet. The conceptual framework of AASB puts the

obligation on the management of Webject to adhere to the policies and guidelines of AASB 116

Property, Plant and Equipment under section 334 of the Corporations Act 2001 for

recognizing their business property, plant and equipment (PPE) (aasb.gov.au, 2018). It can be

observed from the 2017 Annual Report of Webjet that the company considers their PPE in the

balance sheet at the historical cost value less accumulated depreciation and losses from

impairment. AASB conceptual framework has also put the obligation on Webjet to comply with

the regulations and principles of AASB 102 Inventories for the purpose of the recognition of

inventories (aasb.gov.au, 2018). As Webjet is a service provider, the companies does not have

any inventory. According to the conceptual framework of AASB, Webjet is needed to follow the

principles of AASB 138 Intangible Assets for recognizing their intangible assets (aasb.gov.au,

2018). The company considers the intangible assets at cost value after subtracting accumulated

amortization and accumulated impairment losses. These can be shown below:

(Source: webjetlimited.com, 2018)

8CONTEMPORARY ISSUES IN ACCOUNTING

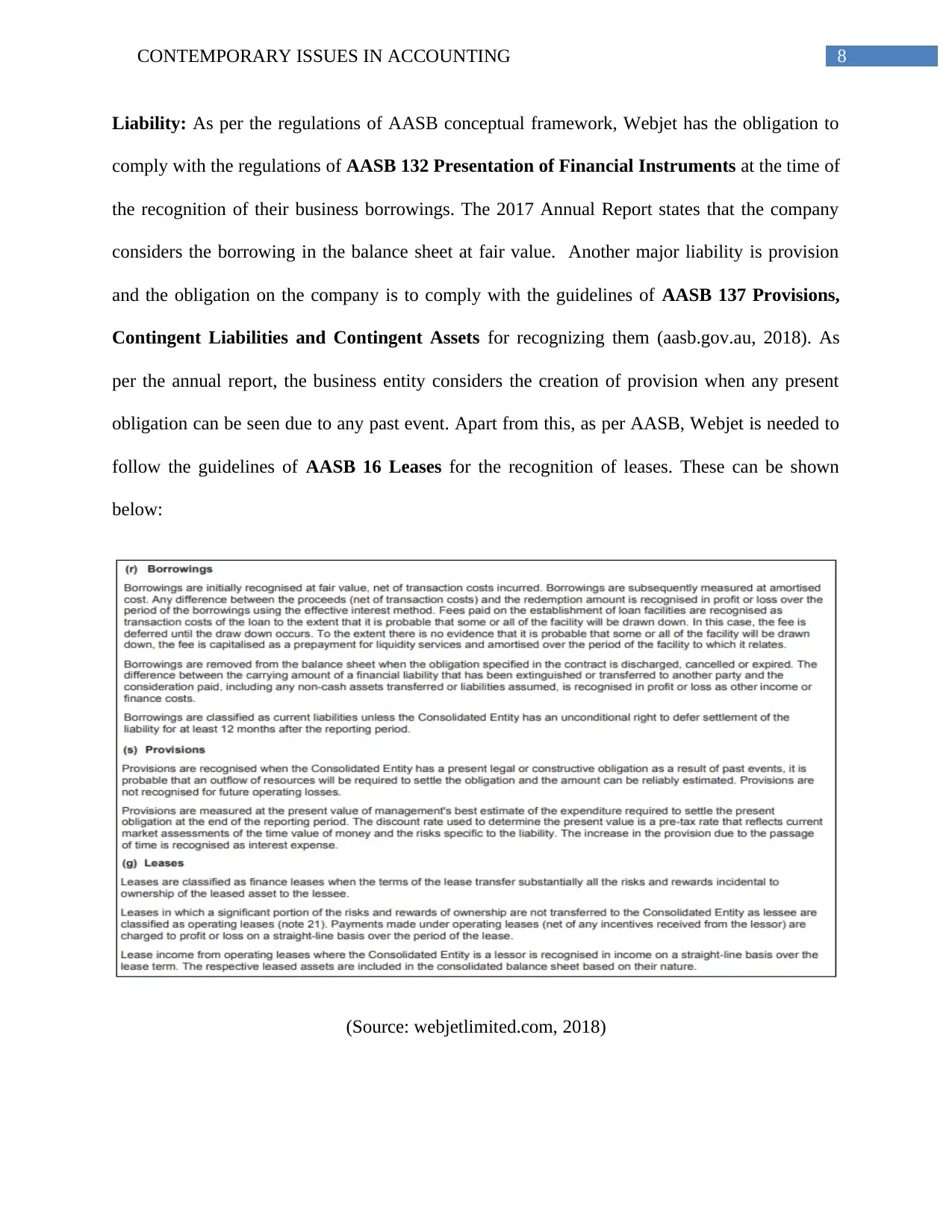

Liability: As per the regulations of AASB conceptual framework, Webjet has the obligation to

comply with the regulations of AASB 132 Presentation of Financial Instruments at the time of

the recognition of their business borrowings. The 2017 Annual Report states that the company

considers the borrowing in the balance sheet at fair value. Another major liability is provision

and the obligation on the company is to comply with the guidelines of AASB 137 Provisions,

Contingent Liabilities and Contingent Assets for recognizing them (aasb.gov.au, 2018). As

per the annual report, the business entity considers the creation of provision when any present

obligation can be seen due to any past event. Apart from this, as per AASB, Webjet is needed to

follow the guidelines of AASB 16 Leases for the recognition of leases. These can be shown

below:

(Source: webjetlimited.com, 2018)

Liability: As per the regulations of AASB conceptual framework, Webjet has the obligation to

comply with the regulations of AASB 132 Presentation of Financial Instruments at the time of

the recognition of their business borrowings. The 2017 Annual Report states that the company

considers the borrowing in the balance sheet at fair value. Another major liability is provision

and the obligation on the company is to comply with the guidelines of AASB 137 Provisions,

Contingent Liabilities and Contingent Assets for recognizing them (aasb.gov.au, 2018). As

per the annual report, the business entity considers the creation of provision when any present

obligation can be seen due to any past event. Apart from this, as per AASB, Webjet is needed to

follow the guidelines of AASB 16 Leases for the recognition of leases. These can be shown

below:

(Source: webjetlimited.com, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

Equity: The AASB conceptual framework puts the obligation on Webjet to follow the principles

of AASB 132 Financial Instruments: Presentation to recognize equity (aasb.gov.au, 2018).

According to the policy of the company, Webjet takes into account the fully paid ordinary shares

as equity.

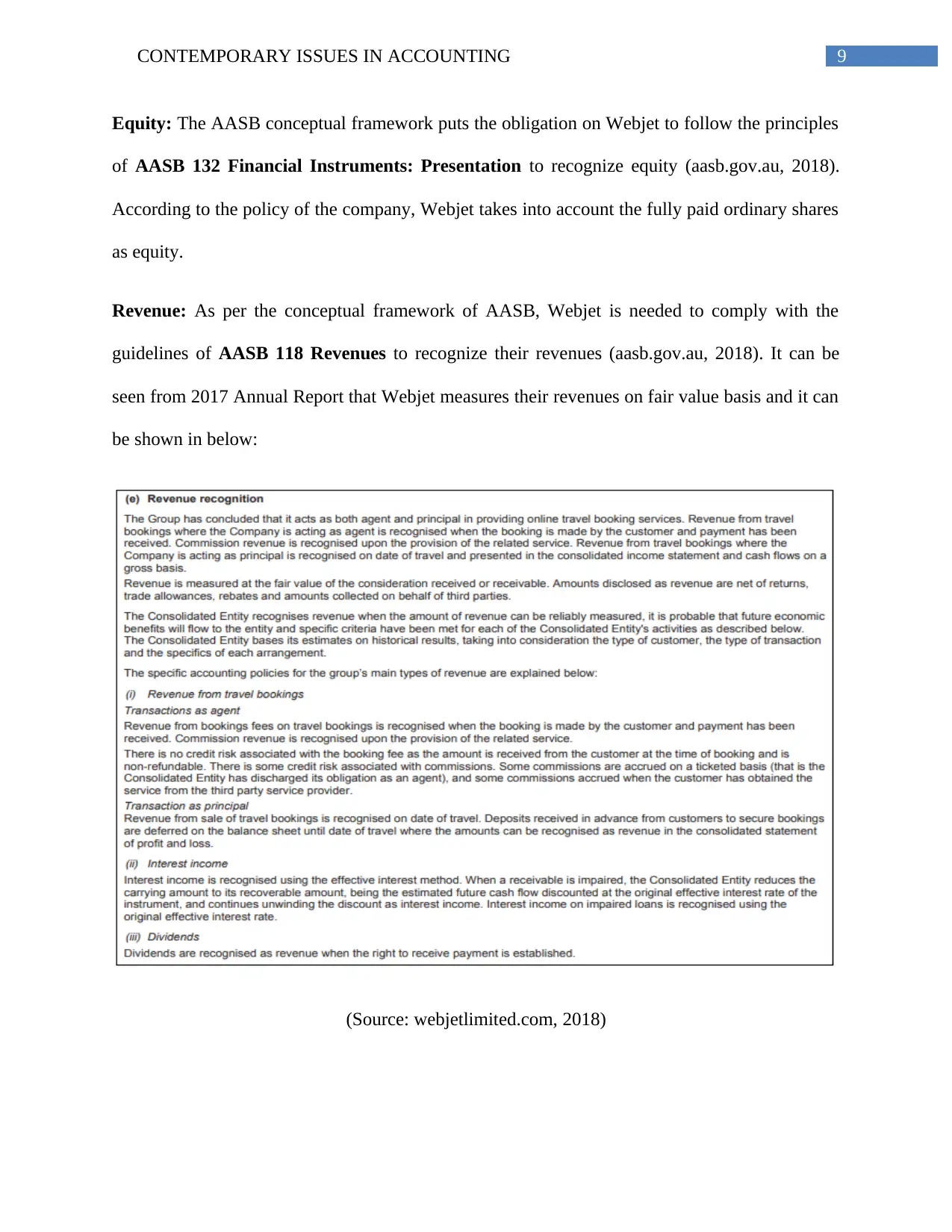

Revenue: As per the conceptual framework of AASB, Webjet is needed to comply with the

guidelines of AASB 118 Revenues to recognize their revenues (aasb.gov.au, 2018). It can be

seen from 2017 Annual Report that Webjet measures their revenues on fair value basis and it can

be shown in below:

(Source: webjetlimited.com, 2018)

Equity: The AASB conceptual framework puts the obligation on Webjet to follow the principles

of AASB 132 Financial Instruments: Presentation to recognize equity (aasb.gov.au, 2018).

According to the policy of the company, Webjet takes into account the fully paid ordinary shares

as equity.

Revenue: As per the conceptual framework of AASB, Webjet is needed to comply with the

guidelines of AASB 118 Revenues to recognize their revenues (aasb.gov.au, 2018). It can be

seen from 2017 Annual Report that Webjet measures their revenues on fair value basis and it can

be shown in below:

(Source: webjetlimited.com, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

Expenses: AASB conceptual framework states that it is needed for the companies for the

recognition of expenses at the time of the outflow of future economic benefit from the company

(aasb.gov.au, 2018). Some of the major expenses head for Webjet are lease expenses, taxation

expenses, employee benefit expenses and others.

Qualitative Characteristics of Financial Reporting

According to AASB conceptual framework, financial information of the business entities

should have the qualitative characteristics of financial reporting so that they can become more

useful for the users. They are discussed below:

Fundamental Qualitative Characteristics: Relevance and Faithful Representation are two

fundamental qualitative characteristics of financial information (Lawrence 2013). It can be seen

from 2017 Annual Report of Webjet that the financial statements of the company contain the

financial information for the year of 2017 and 2016; and it indicates towards the attempt of the

company to provide their users with the most relevant financial information for the purpose of

their investment decision-making process. It can be observed at the same time that Webjet

adheres to the principles of AASB, Corporations Act 2001, IFRS and IASB that ensures the true

and faithful representation of the financial statements of the company (Barth, 2013).

Enhancing Qualitative Characteristics: Comparability, Verifiability, Timeliness and

Understandability are for enhancing qualitative characteristics of financial reporting (Tayeh, Al-

Jarrah and Tarhini 2015). It needs to be mentioned that Webjet has provided their financial

information in the way so that the users can compare them with other corporations and the

different timeline of Webjet. For this reason, Webjet provides the financial information of the

previous year in present financial statements (Zeff, 2013). After that, the noted to the financial

Expenses: AASB conceptual framework states that it is needed for the companies for the

recognition of expenses at the time of the outflow of future economic benefit from the company

(aasb.gov.au, 2018). Some of the major expenses head for Webjet are lease expenses, taxation

expenses, employee benefit expenses and others.

Qualitative Characteristics of Financial Reporting

According to AASB conceptual framework, financial information of the business entities

should have the qualitative characteristics of financial reporting so that they can become more

useful for the users. They are discussed below:

Fundamental Qualitative Characteristics: Relevance and Faithful Representation are two

fundamental qualitative characteristics of financial information (Lawrence 2013). It can be seen

from 2017 Annual Report of Webjet that the financial statements of the company contain the

financial information for the year of 2017 and 2016; and it indicates towards the attempt of the

company to provide their users with the most relevant financial information for the purpose of

their investment decision-making process. It can be observed at the same time that Webjet

adheres to the principles of AASB, Corporations Act 2001, IFRS and IASB that ensures the true

and faithful representation of the financial statements of the company (Barth, 2013).

Enhancing Qualitative Characteristics: Comparability, Verifiability, Timeliness and

Understandability are for enhancing qualitative characteristics of financial reporting (Tayeh, Al-

Jarrah and Tarhini 2015). It needs to be mentioned that Webjet has provided their financial

information in the way so that the users can compare them with other corporations and the

different timeline of Webjet. For this reason, Webjet provides the financial information of the

previous year in present financial statements (Zeff, 2013). After that, the noted to the financial

11CONTEMPORARY ISSUES IN ACCOUNTING

statements of Webjet provide the users with the scope to verify the used accounting assumptions

and estimates of the financial statements. Moreover, Webjet releases the financial statements on

quarterly, half-yearly and annual basis that maintains timeliness of their financial information.

Most importantly, Webjet provides all the needed justification and clarification of the accounting

treatments in the notes to the financial statements that help the users in gaining understanding

about various accounting and financial treatments in the annual reports (Henderson, et al. 2015).

Conclusion and Recommendations

It can be observed from the above discussion that Webjet has fully complied with all the

requirements of the conceptual framework of AASB. The presence of the compliance of Webjet

with the objective of conceptual framework is evident in the financial statements of the

company. After that, Webjet does not have any issue in the recognition and recoding of asset,

liability, equity, revenue and expense as the company has fully followed all the recognition

criteria provided by AASB Conceptual Framework. Lastly, it can also be seen that the financial

information provided by Webjet has presence of both the fundamental and enhancing

characteristics in them. Thus, the recommendation for all the companies is to keep complying

with all the requirement and characteristics of conceptual framework so that accounting issues

can be avoided.

statements of Webjet provide the users with the scope to verify the used accounting assumptions

and estimates of the financial statements. Moreover, Webjet releases the financial statements on

quarterly, half-yearly and annual basis that maintains timeliness of their financial information.

Most importantly, Webjet provides all the needed justification and clarification of the accounting

treatments in the notes to the financial statements that help the users in gaining understanding

about various accounting and financial treatments in the annual reports (Henderson, et al. 2015).

Conclusion and Recommendations

It can be observed from the above discussion that Webjet has fully complied with all the

requirements of the conceptual framework of AASB. The presence of the compliance of Webjet

with the objective of conceptual framework is evident in the financial statements of the

company. After that, Webjet does not have any issue in the recognition and recoding of asset,

liability, equity, revenue and expense as the company has fully followed all the recognition

criteria provided by AASB Conceptual Framework. Lastly, it can also be seen that the financial

information provided by Webjet has presence of both the fundamental and enhancing

characteristics in them. Thus, the recommendation for all the companies is to keep complying

with all the requirement and characteristics of conceptual framework so that accounting issues

can be avoided.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.