Contemporary Issues in Accounting: Wesfarmers Limited Financial Report

VerifiedAdded on 2023/06/14

|16

|2380

|116

Report

AI Summary

This report provides an overview of contemporary issues in accounting, focusing on the general purpose financial reporting objectives and their application to Wesfarmers Limited. It examines the adequacy of information for the target audience, recognition criteria for financial statement elements (assets, liabilities, equity, revenues, and expenses), and fundamental and enhancing qualitative characteristics of financial reporting. The report concludes that Wesfarmers Limited complies with the objectives of general purpose financial reporting and exhibits fundamental qualitative characteristics regarding financial reporting.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary issues in accounting

Name of the student

Name of the university

Subject code

Subject title

Assignment title

Trimester number

Student ID

Author note

Contemporary issues in accounting

Name of the student

Name of the university

Subject code

Subject title

Assignment title

Trimester number

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The main objective of the general purpose financial reporting is to form the foundations for

the conceptual framework along with various other aspects of framework that flows from

that. Further, its objective is to deliver the financial information regarding the reporting

company that can be useful to the potential and existing lenders, investors and creditors for

making the decisions regarding the company’s resources. It is further directed to the users

who deliver the resources to the reporting company.

CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The main objective of the general purpose financial reporting is to form the foundations for

the conceptual framework along with various other aspects of framework that flows from

that. Further, its objective is to deliver the financial information regarding the reporting

company that can be useful to the potential and existing lenders, investors and creditors for

making the decisions regarding the company’s resources. It is further directed to the users

who deliver the resources to the reporting company.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

1. General purpose financial reporting objectives..................................................................3

2. Adequate information for target audience of financial report............................................3

2.1 Useful information...........................................................................................................3

2.2 Assessment of amount and timing...................................................................................4

2.3 Organizational resources..................................................................................................4

3. Recognition criteria for financial statement elements........................................................4

3.1 Recognition of assets........................................................................................................5

3.2 Recognition for liabilities.................................................................................................6

3.3 Recognition for equity......................................................................................................7

3.4 Revenues..........................................................................................................................8

3.5 Expenses...........................................................................................................................8

4. Fundamental qualitative characteristics.................................................................................9

4.1 Relevance.........................................................................................................................9

4.2 Materiality......................................................................................................................10

4.3 Faithful representation...................................................................................................10

5. Enhancing qualitative characteristics...................................................................................10

5.1 Comparability.................................................................................................................10

5.2 Verifiability....................................................................................................................11

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

1. General purpose financial reporting objectives..................................................................3

2. Adequate information for target audience of financial report............................................3

2.1 Useful information...........................................................................................................3

2.2 Assessment of amount and timing...................................................................................4

2.3 Organizational resources..................................................................................................4

3. Recognition criteria for financial statement elements........................................................4

3.1 Recognition of assets........................................................................................................5

3.2 Recognition for liabilities.................................................................................................6

3.3 Recognition for equity......................................................................................................7

3.4 Revenues..........................................................................................................................8

3.5 Expenses...........................................................................................................................8

4. Fundamental qualitative characteristics.................................................................................9

4.1 Relevance.........................................................................................................................9

4.2 Materiality......................................................................................................................10

4.3 Faithful representation...................................................................................................10

5. Enhancing qualitative characteristics...................................................................................10

5.1 Comparability.................................................................................................................10

5.2 Verifiability....................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

5.3 Timeliness......................................................................................................................12

5.4 Understandability...........................................................................................................12

Conclusion................................................................................................................................12

References................................................................................................................................13

CONTEMPORARY ISSUES IN ACCOUNTING

5.3 Timeliness......................................................................................................................12

5.4 Understandability...........................................................................................................12

Conclusion................................................................................................................................12

References................................................................................................................................13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The conceptual framework for the general purpose financial reporting is applicable to

the annual reporting of the company for the period starting on or after 1st July 2014. It

considers the amendment made till 4th June 2014 and prepared on 15th March 2016 by staffs

of AASB (Australian Accounting Standards Board). The compilation is not the separate

framework that is issued by AASB rather it is the representation of framework that is

amended by the other pronouncements.

1. General purpose financial reporting objectives

Wesfarmers Limited is for profit, limited by Share Company that is domiciled and

incorporated in Australia. The company’s shares are traded in the Australian Securities

exchange (Cajaiba-Santana 2014). It has been observed from the annual report of the

company that the financial report of the company is prepared as per the general purpose

reporting standard and in accordance with the Corporation Act 2001, International Financial

Reporting standard and other pronouncements of Australian Accounting Standard Board.

Further, the company adopted all the amended and new Accounting Standards and various

interpretations released by AASB (Wesfarmers.com.au 2018).

2. Adequate information for target audience of financial report

2.1 Useful information

As per the conceptual framework requirement the reporting entity must provide the

useful information to assist the users in taking major decisions. It has been observed from the

financial statement of Wesfarmers that all the required and necessary information is provided

in the financial report of the company (Cheng et al. 2014). Further, as per the requirement of

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The conceptual framework for the general purpose financial reporting is applicable to

the annual reporting of the company for the period starting on or after 1st July 2014. It

considers the amendment made till 4th June 2014 and prepared on 15th March 2016 by staffs

of AASB (Australian Accounting Standards Board). The compilation is not the separate

framework that is issued by AASB rather it is the representation of framework that is

amended by the other pronouncements.

1. General purpose financial reporting objectives

Wesfarmers Limited is for profit, limited by Share Company that is domiciled and

incorporated in Australia. The company’s shares are traded in the Australian Securities

exchange (Cajaiba-Santana 2014). It has been observed from the annual report of the

company that the financial report of the company is prepared as per the general purpose

reporting standard and in accordance with the Corporation Act 2001, International Financial

Reporting standard and other pronouncements of Australian Accounting Standard Board.

Further, the company adopted all the amended and new Accounting Standards and various

interpretations released by AASB (Wesfarmers.com.au 2018).

2. Adequate information for target audience of financial report

2.1 Useful information

As per the conceptual framework requirement the reporting entity must provide the

useful information to assist the users in taking major decisions. It has been observed from the

financial statement of Wesfarmers that all the required and necessary information is provided

in the financial report of the company (Cheng et al. 2014). Further, as per the requirement of

5

CONTEMPORARY ISSUES IN ACCOUNTING

AASB the company prepared income statement, statement of comprehensive income, balance

sheet, cash flow statement and statement of changes in equity to provide detail information

regarding the financial performance of the company.

2.2 Assessment of amount and timing

Another requirement of the conceptual framework is to present the information in

timely manner so that the users can assess and compare the data with previous years. It has

been identified that the financial statement of the company has been prepared for 1 year

period ending 30th June 2017 (De Villiers, Rinaldi and Unerman 2014). In addition to this the

financial information for the year ended 30th June 2016 also provided so that the users can

compare the current year data with the previous year.

2.3 Organizational resources

The 3rd requirement of the conceptual framework is to provide information regarding

the resources of the company and the sources from where the resources are obtained. It is

observed that as per the requirement of AASB the company clearly mentioned the source of

the resources in their financial statement and the disclosure notes associated with the

financial report (Morioka and De Carvalho 2016).

Therefore, it can be stated that all the requirements of conceptual framework are

followed by Wesfarmers Limited in concise manner.

3. Recognition criteria for financial statement elements

Recognition is the procedure of incorporating an item in the income statement or

balance sheet that fulfils the definition of element and criteria of recognition. It includes the

description of item in monetary amount as well as in words that is included in the income

statement or balance sheet. The item shall be recognized if –

CONTEMPORARY ISSUES IN ACCOUNTING

AASB the company prepared income statement, statement of comprehensive income, balance

sheet, cash flow statement and statement of changes in equity to provide detail information

regarding the financial performance of the company.

2.2 Assessment of amount and timing

Another requirement of the conceptual framework is to present the information in

timely manner so that the users can assess and compare the data with previous years. It has

been identified that the financial statement of the company has been prepared for 1 year

period ending 30th June 2017 (De Villiers, Rinaldi and Unerman 2014). In addition to this the

financial information for the year ended 30th June 2016 also provided so that the users can

compare the current year data with the previous year.

2.3 Organizational resources

The 3rd requirement of the conceptual framework is to provide information regarding

the resources of the company and the sources from where the resources are obtained. It is

observed that as per the requirement of AASB the company clearly mentioned the source of

the resources in their financial statement and the disclosure notes associated with the

financial report (Morioka and De Carvalho 2016).

Therefore, it can be stated that all the requirements of conceptual framework are

followed by Wesfarmers Limited in concise manner.

3. Recognition criteria for financial statement elements

Recognition is the procedure of incorporating an item in the income statement or

balance sheet that fulfils the definition of element and criteria of recognition. It includes the

description of item in monetary amount as well as in words that is included in the income

statement or balance sheet. The item shall be recognized if –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

The particular item has a value or cost that can be reliably measured, and

It is apparent that the future economic benefits, if any related to the item will flow

from or to the entity.

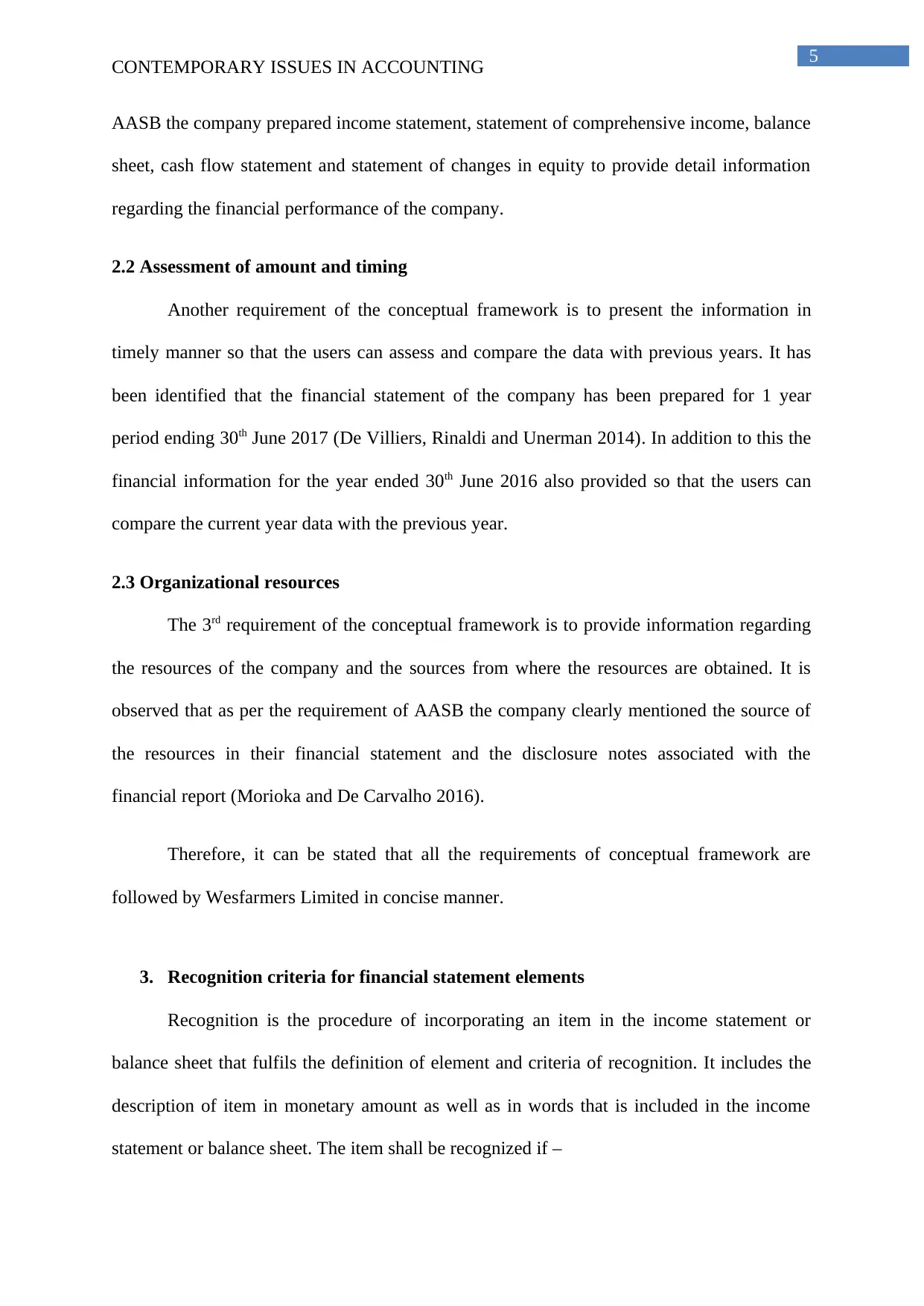

3.1 Recognition of assets

Assets are recognized under the balance sheet if it is apparent that the future economic

benefits, if any related to the asset will flow from or to the entity. It has been identified from

the balance sheet of the company that the company has various assets that are segregated

under current assets and non-current assets. Carrying value of the plant, property and

equipment are measured at the cost of asset reduced by impairment and depreciation. Further

the asset’s cost is inclusive of the cost of replacing that is eligible for capitalisation and cost

involved in major inspections (Wesfarmers.com.au 2018)..

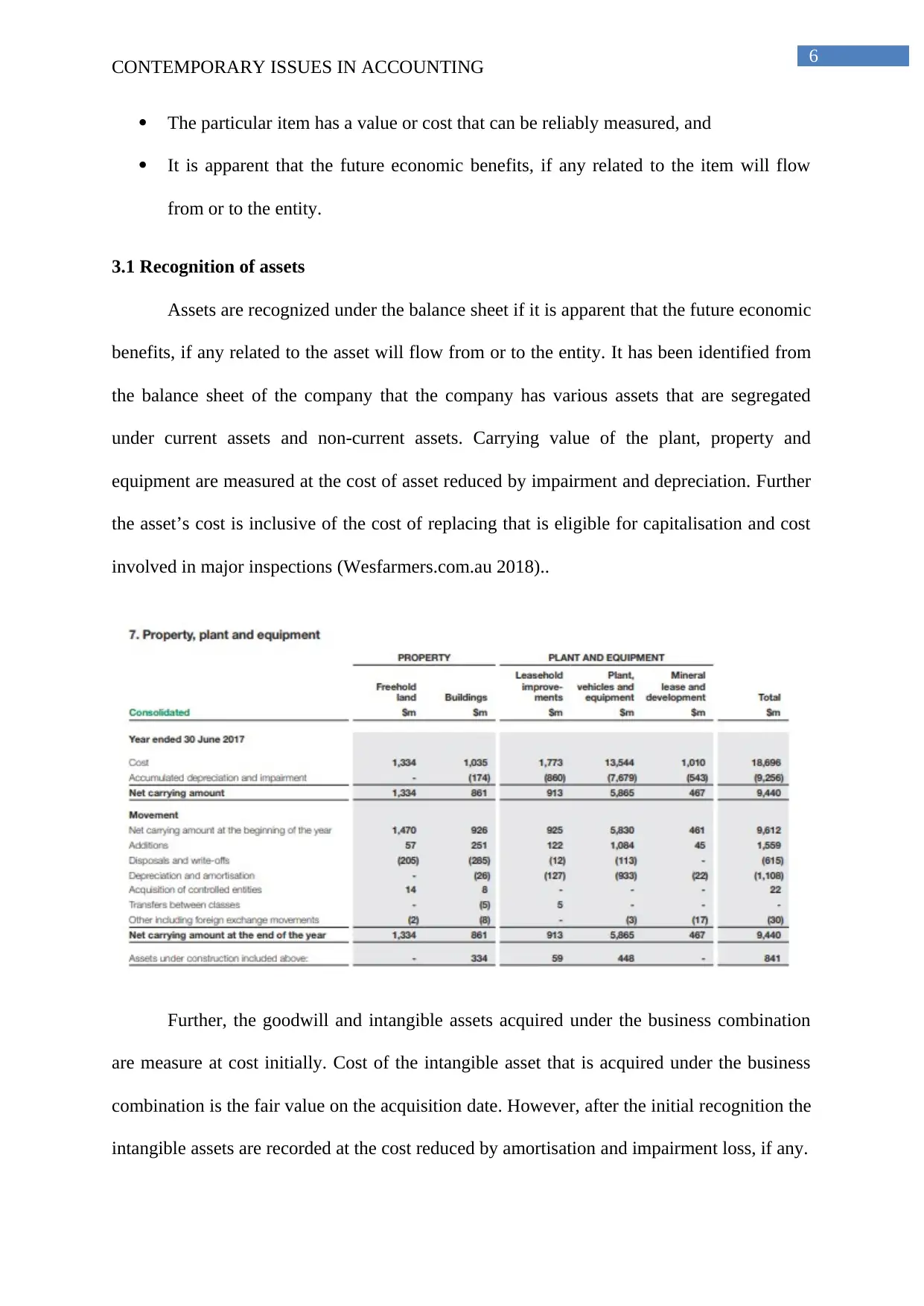

Further, the goodwill and intangible assets acquired under the business combination

are measure at cost initially. Cost of the intangible asset that is acquired under the business

combination is the fair value on the acquisition date. However, after the initial recognition the

intangible assets are recorded at the cost reduced by amortisation and impairment loss, if any.

CONTEMPORARY ISSUES IN ACCOUNTING

The particular item has a value or cost that can be reliably measured, and

It is apparent that the future economic benefits, if any related to the item will flow

from or to the entity.

3.1 Recognition of assets

Assets are recognized under the balance sheet if it is apparent that the future economic

benefits, if any related to the asset will flow from or to the entity. It has been identified from

the balance sheet of the company that the company has various assets that are segregated

under current assets and non-current assets. Carrying value of the plant, property and

equipment are measured at the cost of asset reduced by impairment and depreciation. Further

the asset’s cost is inclusive of the cost of replacing that is eligible for capitalisation and cost

involved in major inspections (Wesfarmers.com.au 2018)..

Further, the goodwill and intangible assets acquired under the business combination

are measure at cost initially. Cost of the intangible asset that is acquired under the business

combination is the fair value on the acquisition date. However, after the initial recognition the

intangible assets are recorded at the cost reduced by amortisation and impairment loss, if any.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

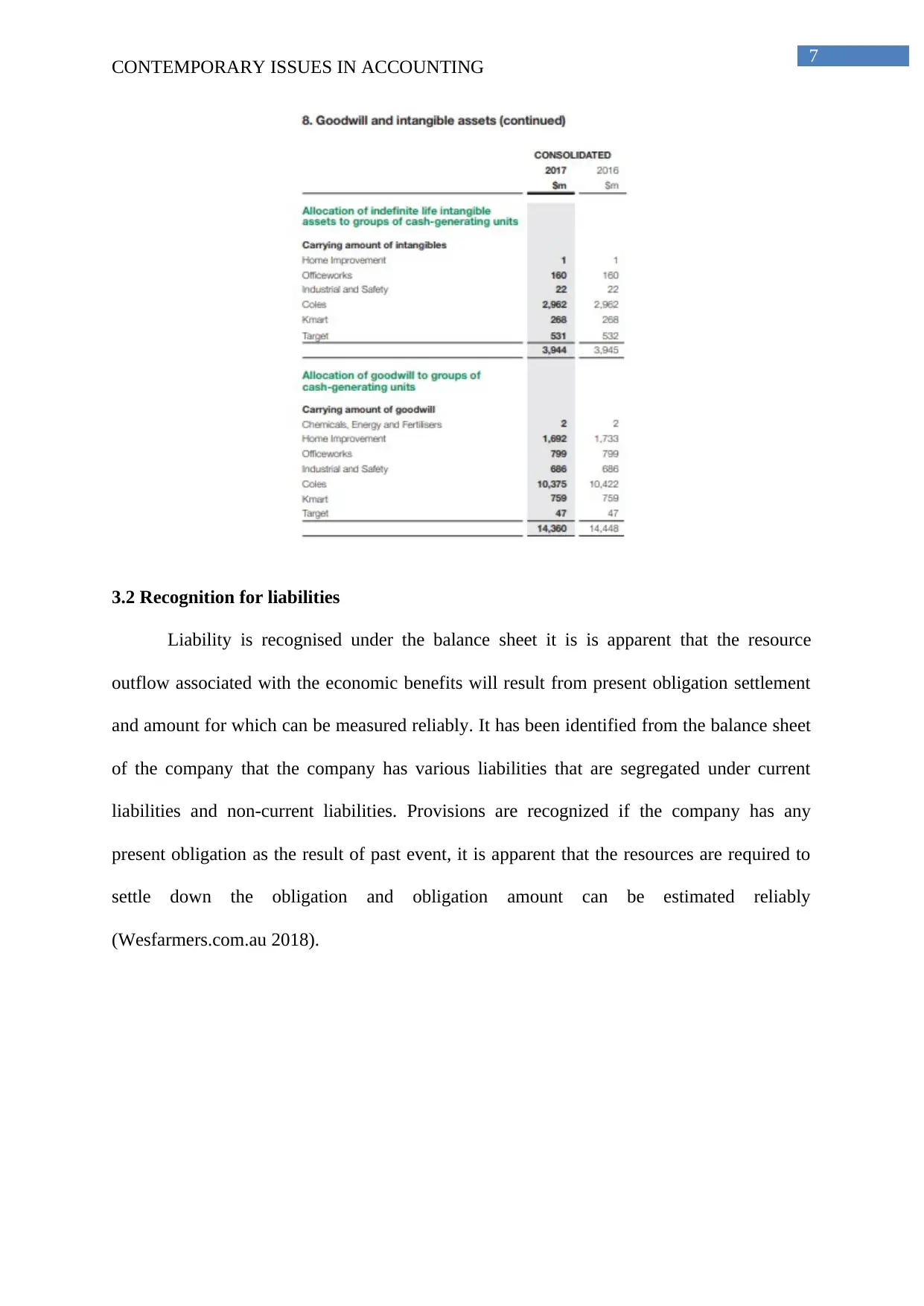

3.2 Recognition for liabilities

Liability is recognised under the balance sheet it is is apparent that the resource

outflow associated with the economic benefits will result from present obligation settlement

and amount for which can be measured reliably. It has been identified from the balance sheet

of the company that the company has various liabilities that are segregated under current

liabilities and non-current liabilities. Provisions are recognized if the company has any

present obligation as the result of past event, it is apparent that the resources are required to

settle down the obligation and obligation amount can be estimated reliably

(Wesfarmers.com.au 2018).

CONTEMPORARY ISSUES IN ACCOUNTING

3.2 Recognition for liabilities

Liability is recognised under the balance sheet it is is apparent that the resource

outflow associated with the economic benefits will result from present obligation settlement

and amount for which can be measured reliably. It has been identified from the balance sheet

of the company that the company has various liabilities that are segregated under current

liabilities and non-current liabilities. Provisions are recognized if the company has any

present obligation as the result of past event, it is apparent that the resources are required to

settle down the obligation and obligation amount can be estimated reliably

(Wesfarmers.com.au 2018).

8

CONTEMPORARY ISSUES IN ACCOUNTING

Further, the provision towards employee benefits states long service entitlements for

leave, annual leave and the incentives accrued by the employees.

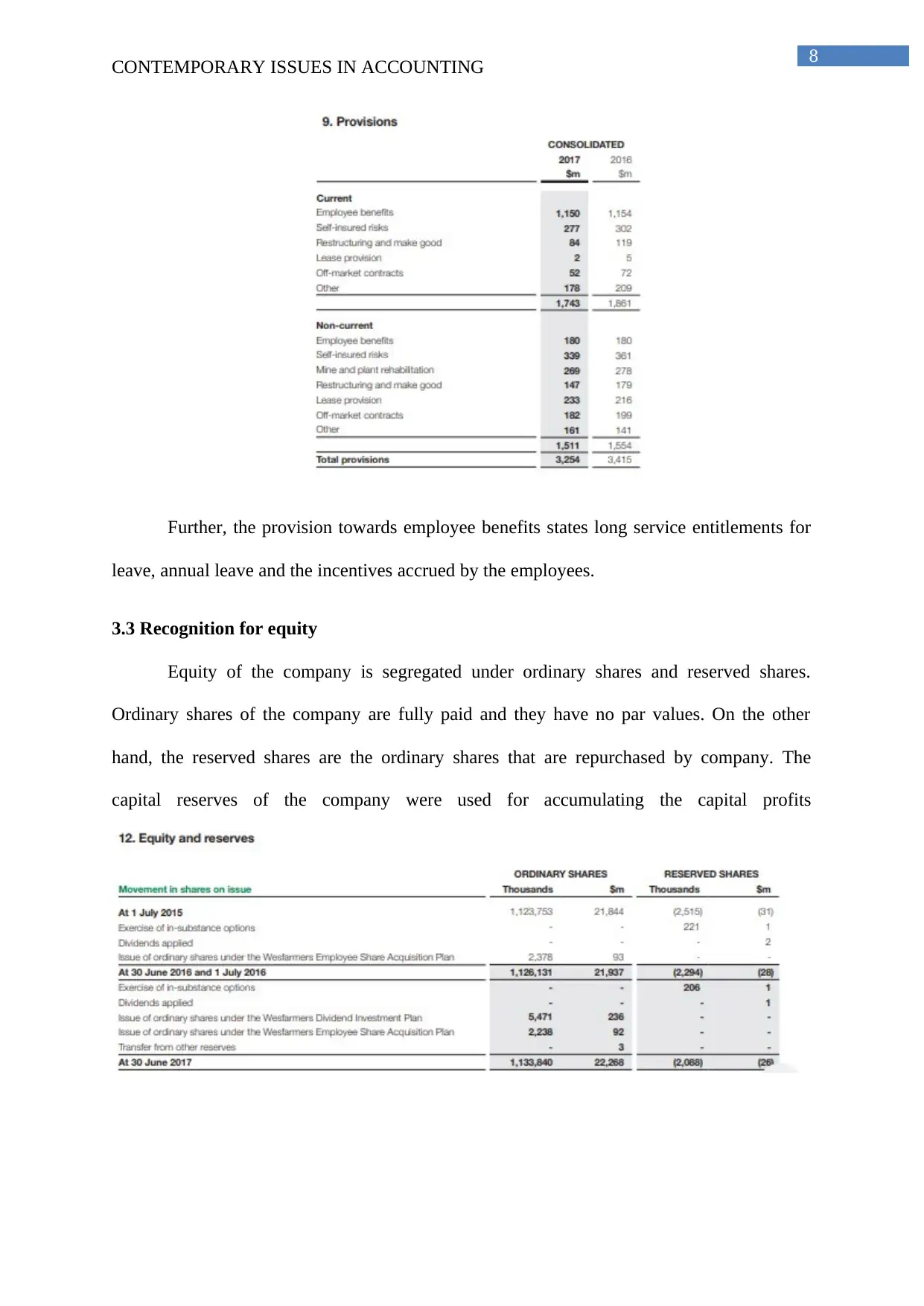

3.3 Recognition for equity

Equity of the company is segregated under ordinary shares and reserved shares.

Ordinary shares of the company are fully paid and they have no par values. On the other

hand, the reserved shares are the ordinary shares that are repurchased by company. The

capital reserves of the company were used for accumulating the capital profits

CONTEMPORARY ISSUES IN ACCOUNTING

Further, the provision towards employee benefits states long service entitlements for

leave, annual leave and the incentives accrued by the employees.

3.3 Recognition for equity

Equity of the company is segregated under ordinary shares and reserved shares.

Ordinary shares of the company are fully paid and they have no par values. On the other

hand, the reserved shares are the ordinary shares that are repurchased by company. The

capital reserves of the company were used for accumulating the capital profits

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

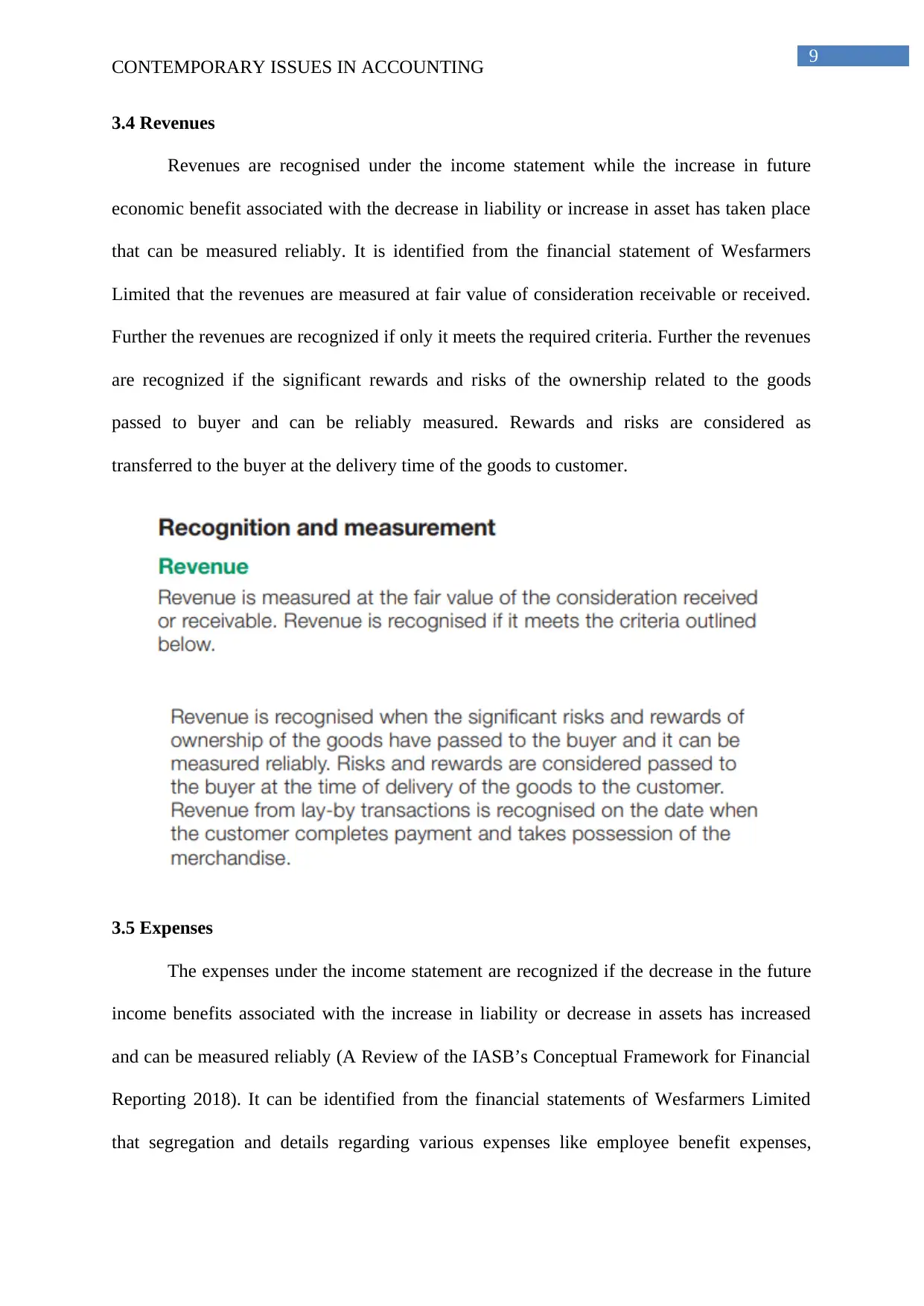

3.4 Revenues

Revenues are recognised under the income statement while the increase in future

economic benefit associated with the decrease in liability or increase in asset has taken place

that can be measured reliably. It is identified from the financial statement of Wesfarmers

Limited that the revenues are measured at fair value of consideration receivable or received.

Further the revenues are recognized if only it meets the required criteria. Further the revenues

are recognized if the significant rewards and risks of the ownership related to the goods

passed to buyer and can be reliably measured. Rewards and risks are considered as

transferred to the buyer at the delivery time of the goods to customer.

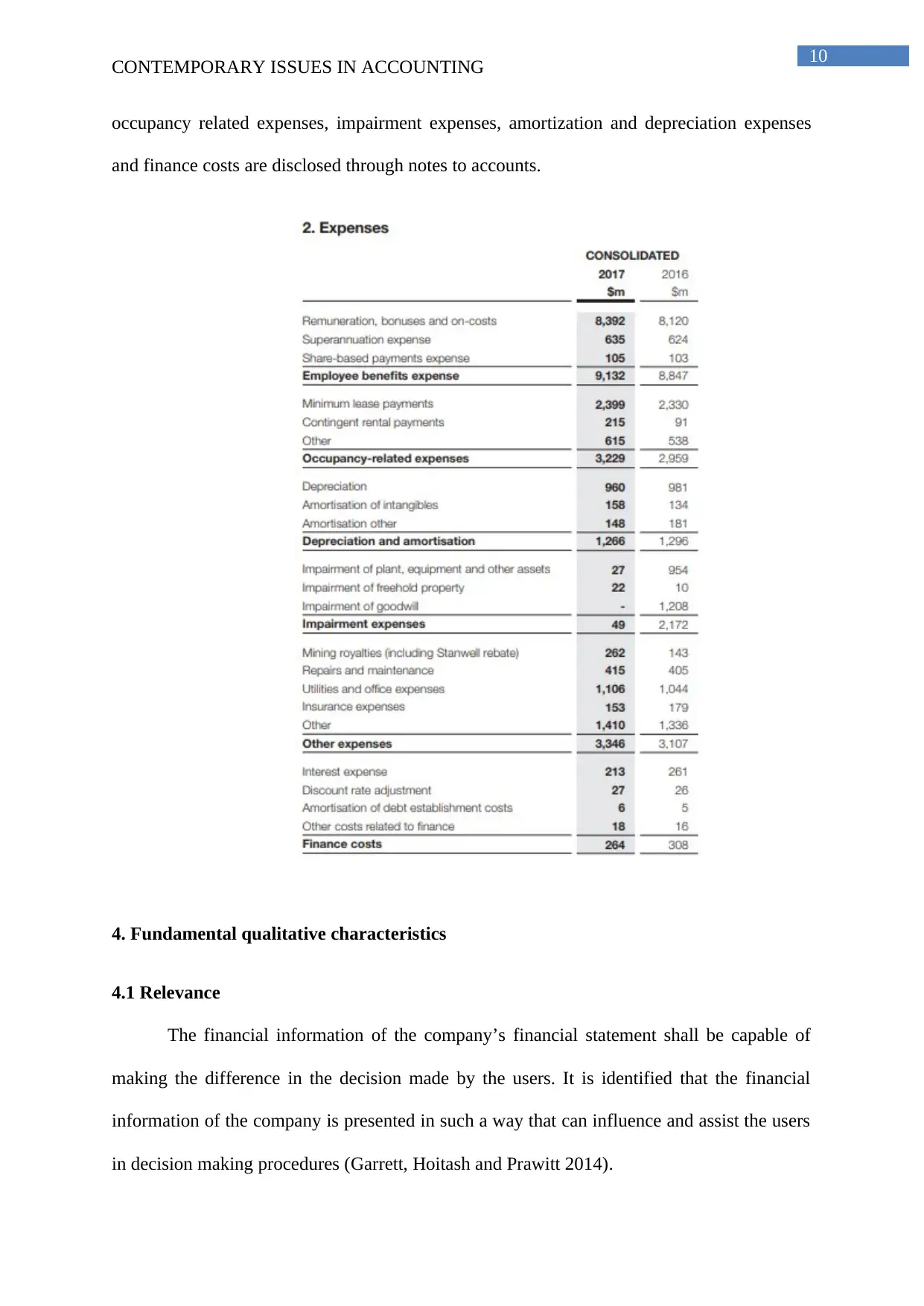

3.5 Expenses

The expenses under the income statement are recognized if the decrease in the future

income benefits associated with the increase in liability or decrease in assets has increased

and can be measured reliably (A Review of the IASB’s Conceptual Framework for Financial

Reporting 2018). It can be identified from the financial statements of Wesfarmers Limited

that segregation and details regarding various expenses like employee benefit expenses,

CONTEMPORARY ISSUES IN ACCOUNTING

3.4 Revenues

Revenues are recognised under the income statement while the increase in future

economic benefit associated with the decrease in liability or increase in asset has taken place

that can be measured reliably. It is identified from the financial statement of Wesfarmers

Limited that the revenues are measured at fair value of consideration receivable or received.

Further the revenues are recognized if only it meets the required criteria. Further the revenues

are recognized if the significant rewards and risks of the ownership related to the goods

passed to buyer and can be reliably measured. Rewards and risks are considered as

transferred to the buyer at the delivery time of the goods to customer.

3.5 Expenses

The expenses under the income statement are recognized if the decrease in the future

income benefits associated with the increase in liability or decrease in assets has increased

and can be measured reliably (A Review of the IASB’s Conceptual Framework for Financial

Reporting 2018). It can be identified from the financial statements of Wesfarmers Limited

that segregation and details regarding various expenses like employee benefit expenses,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

occupancy related expenses, impairment expenses, amortization and depreciation expenses

and finance costs are disclosed through notes to accounts.

4. Fundamental qualitative characteristics

4.1 Relevance

The financial information of the company’s financial statement shall be capable of

making the difference in the decision made by the users. It is identified that the financial

information of the company is presented in such a way that can influence and assist the users

in decision making procedures (Garrett, Hoitash and Prawitt 2014).

CONTEMPORARY ISSUES IN ACCOUNTING

occupancy related expenses, impairment expenses, amortization and depreciation expenses

and finance costs are disclosed through notes to accounts.

4. Fundamental qualitative characteristics

4.1 Relevance

The financial information of the company’s financial statement shall be capable of

making the difference in the decision made by the users. It is identified that the financial

information of the company is presented in such a way that can influence and assist the users

in decision making procedures (Garrett, Hoitash and Prawitt 2014).

11

CONTEMPORARY ISSUES IN ACCOUNTING

4.2 Materiality

Information will be material if misstating or omitting it can have an influence on the

decisions taken by the users of financial statement. It is found from the annual report of the

company that the material items have been properly recognized in the financial statement of

the company and the notes associated with it. Further, no material misstatements were found

in the financial statement of the company (Kogan, Sudit and Vasarhelyi 2018).

4.3 Faithful representation

The financial statement to be useful shall not only state the relevant phenomena, but it

shall also represent faithfully. It is identified from the financial statement of the company that

it represents the true and fair view of the company’s financial position and financial

performances as on 30th June 2017 (Zhang and Andrew 2014).

5. Enhancing qualitative characteristics

5.1 Comparability

It is the qualitative characteristic that allows the users to recognize and understand the

similarities and differences among the items. It has been identified that the company

presented the major information in graphs and tables and compared it with the previous year.

Therefore, the users can compare the data and take their decisions accordingly.

CONTEMPORARY ISSUES IN ACCOUNTING

4.2 Materiality

Information will be material if misstating or omitting it can have an influence on the

decisions taken by the users of financial statement. It is found from the annual report of the

company that the material items have been properly recognized in the financial statement of

the company and the notes associated with it. Further, no material misstatements were found

in the financial statement of the company (Kogan, Sudit and Vasarhelyi 2018).

4.3 Faithful representation

The financial statement to be useful shall not only state the relevant phenomena, but it

shall also represent faithfully. It is identified from the financial statement of the company that

it represents the true and fair view of the company’s financial position and financial

performances as on 30th June 2017 (Zhang and Andrew 2014).

5. Enhancing qualitative characteristics

5.1 Comparability

It is the qualitative characteristic that allows the users to recognize and understand the

similarities and differences among the items. It has been identified that the company

presented the major information in graphs and tables and compared it with the previous year.

Therefore, the users can compare the data and take their decisions accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

![Report: Contemporary Issues in Accounting - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fzz%2F9509ff46c136422d929242036a52e1cb.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.