Financial Analysis of Qantas Airways

VerifiedAdded on 2020/04/15

|19

|2625

|113

AI Summary

This assignment requires a detailed financial analysis of Qantas Airways, examining its financial statements in accordance with the Australian Accounting Standards Board (AASB). It involves evaluating different elements of the financial pronouncements, analyzing key themes in financial reporting, and understanding the relationship between accounting methods and decision-making. The analysis should cover aspects like revenue and expenses, assets and liabilities, earnings per share growth, and compliance with AASB standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

University Name

Student Name

Authors’ Note

Contemporary Issues in Accounting

University Name

Student Name

Authors’ Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The present study evaluates the present-day issues in the area of accounting that indicates

towards exploration of diverse difficult notions of accounting along with well as stratagems

and comprehending a wide range of issues with special orientation to the functionalities of

Qantas Airways. Again, this study also aims to present an investigative perceptive of

efficiency of Qantas Airways to meet the obligations of the conceptual framework-CF of

Australian Accounting Standards Board. Thus, the study takes into account analysis of

specific objectives of the CF, criteria for identification of accounting items in financial

reports and examines fundamental along with enhancing characteristics of the strategy.

CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The present study evaluates the present-day issues in the area of accounting that indicates

towards exploration of diverse difficult notions of accounting along with well as stratagems

and comprehending a wide range of issues with special orientation to the functionalities of

Qantas Airways. Again, this study also aims to present an investigative perceptive of

efficiency of Qantas Airways to meet the obligations of the conceptual framework-CF of

Australian Accounting Standards Board. Thus, the study takes into account analysis of

specific objectives of the CF, criteria for identification of accounting items in financial

reports and examines fundamental along with enhancing characteristics of the strategy.

3

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Analysis of satisfaction of the objectives of the conceptual framework....................................4

Examination as regards meeting recognition criteria in the financial report.............................5

Analysis of financial reports as regards relevance as well as faithful representation................7

Critical analysis of fundamental qualitative enhancing features of financial report..................7

Analytical evaluation of enhancing qualitative characteristic of financial report......................8

Conclusion................................................................................................................................10

References................................................................................................................................11

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Analysis of satisfaction of the objectives of the conceptual framework....................................4

Examination as regards meeting recognition criteria in the financial report.............................5

Analysis of financial reports as regards relevance as well as faithful representation................7

Critical analysis of fundamental qualitative enhancing features of financial report..................7

Analytical evaluation of enhancing qualitative characteristic of financial report......................8

Conclusion................................................................................................................................10

References................................................................................................................................11

4

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The present study presents a thorough illustration of diverse systems and methods of

accounting that can subsequently help in the process of, monitoring, examining, controlling

as well as directing business functions with special orientation to the operations of the

business concern Qantas Airways. In essence, Qantas Airways can be considered as the

largest airline of Australia when considered from the perspective of the fleet size,

international flights as well as worldwide destinations. Qantas Airways is the flag carrier of

Australia that necessarily possesses the overall share of approximately 65% of the domestic

market particularly in Australia and carries around 14.9% of passengers drifting both to and

fro from Australia.

Essentially, the current study intends to a present analytical findings of diverse notions of

dimensions that can help in pointing out the requirements of analysing the compliance

towards diverse regulations and objectives of conceptual framework, analysis of extent of

meeting the requirements of recognition criteria in the financial reports of Qantas, analysis of

fundamental qualitative and enhancing facets of financial reports.

Analysis of satisfaction of the objectives of the conceptual framework

The conceptual framework necessarily refers to the intentions along with the principles of

particularly general purpose financial reporting. As such, the conceptual framework is an

effective instrument that can help the board of the corporation in developing financial

standards based on themes and notions (Gelmini et al. 2015). Essentially, the conceptual

framework can help preparers of general purpose financial reports to design effective and at

once reliable stratagems of accounting whilst financial standard can approve the process of

adoption of specific accounting scheme.

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The present study presents a thorough illustration of diverse systems and methods of

accounting that can subsequently help in the process of, monitoring, examining, controlling

as well as directing business functions with special orientation to the operations of the

business concern Qantas Airways. In essence, Qantas Airways can be considered as the

largest airline of Australia when considered from the perspective of the fleet size,

international flights as well as worldwide destinations. Qantas Airways is the flag carrier of

Australia that necessarily possesses the overall share of approximately 65% of the domestic

market particularly in Australia and carries around 14.9% of passengers drifting both to and

fro from Australia.

Essentially, the current study intends to a present analytical findings of diverse notions of

dimensions that can help in pointing out the requirements of analysing the compliance

towards diverse regulations and objectives of conceptual framework, analysis of extent of

meeting the requirements of recognition criteria in the financial reports of Qantas, analysis of

fundamental qualitative and enhancing facets of financial reports.

Analysis of satisfaction of the objectives of the conceptual framework

The conceptual framework necessarily refers to the intentions along with the principles of

particularly general purpose financial reporting. As such, the conceptual framework is an

effective instrument that can help the board of the corporation in developing financial

standards based on themes and notions (Gelmini et al. 2015). Essentially, the conceptual

framework can help preparers of general purpose financial reports to design effective and at

once reliable stratagems of accounting whilst financial standard can approve the process of

adoption of specific accounting scheme.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

CONTEMPORARY ISSUES IN ACCOUNTING

In essence, analysis of the financial declarations of Qantas Airways reflects conformation

with the regulations of “Australian Accounting Standards Board (AASB) - Conceptual

Framework (CF)”. This assists to gain comprehensive understanding regarding intent of

pecuniary statements, different qualitative uniqueness that subsequently institutes the efficacy

of financial pronouncements. Nonetheless, there are different elements of statements that can

help users to utilize the information to arrive at decisions regarding purchasing, selling or

holding equity, debt instruments and settling loans else wise credit (Harris and Roach 2013).

Thus, in this way the pecuniary statement meets the requirements and objectives of

particularly financial regulation. There are diverse items of financial declaration that consists

of assets as well as liabilities including both current and non-current. Thus, primary users of

the information of Qantas Airways can get to know about resources of the business concern

and evaluate prospects of the firm regarding upcoming flows of cash in the upcoming period.

This too assists in the process of evaluating efficacy as well as efficiency of management in

discharging responsibilities (McCombs 2017).

Examination as regards meeting recognition criteria in the financial report of Qantas

Airways

The evaluation of financial statements includes analysis of consolidated financial assertions

of particularly the firm Qantas Airways that essentially refers to general purpose financial

reports (GPFR). The GPFR of the firm are prepared in accordance to the directives of the

AASB and the “Corporation Act 2001”. Apart from this, the business concern prepares as

well as presents financial information in line with regulations of International Accounting

Standards Board (IASB) along with the International Financial Reporting Standards (IFRS)

(Deegan 2013).

Assets:

CONTEMPORARY ISSUES IN ACCOUNTING

In essence, analysis of the financial declarations of Qantas Airways reflects conformation

with the regulations of “Australian Accounting Standards Board (AASB) - Conceptual

Framework (CF)”. This assists to gain comprehensive understanding regarding intent of

pecuniary statements, different qualitative uniqueness that subsequently institutes the efficacy

of financial pronouncements. Nonetheless, there are different elements of statements that can

help users to utilize the information to arrive at decisions regarding purchasing, selling or

holding equity, debt instruments and settling loans else wise credit (Harris and Roach 2013).

Thus, in this way the pecuniary statement meets the requirements and objectives of

particularly financial regulation. There are diverse items of financial declaration that consists

of assets as well as liabilities including both current and non-current. Thus, primary users of

the information of Qantas Airways can get to know about resources of the business concern

and evaluate prospects of the firm regarding upcoming flows of cash in the upcoming period.

This too assists in the process of evaluating efficacy as well as efficiency of management in

discharging responsibilities (McCombs 2017).

Examination as regards meeting recognition criteria in the financial report of Qantas

Airways

The evaluation of financial statements includes analysis of consolidated financial assertions

of particularly the firm Qantas Airways that essentially refers to general purpose financial

reports (GPFR). The GPFR of the firm are prepared in accordance to the directives of the

AASB and the “Corporation Act 2001”. Apart from this, the business concern prepares as

well as presents financial information in line with regulations of International Accounting

Standards Board (IASB) along with the International Financial Reporting Standards (IFRS)

(Deegan 2013).

Assets:

6

CONTEMPORARY ISSUES IN ACCOUNTING

The assets of Qantas Airways are reflected in terms of Australian dollars that is necessarily

the functional currency of the corporation. Nevertheless, the procedure of analysis of assets

mentioned in financial assertions reflect the fact that assets can be classified as “held for sale”

enumerated at low value of the recognized cost compared to the fair values after deduction of

the cost borne for sales. Detailed analysis of report also replicates that net defined

assets/resources of Qantas Airways is necessarily presented at the fair value of planned

assets only after the deduction of specific obligation at current value (Williams 2014). The

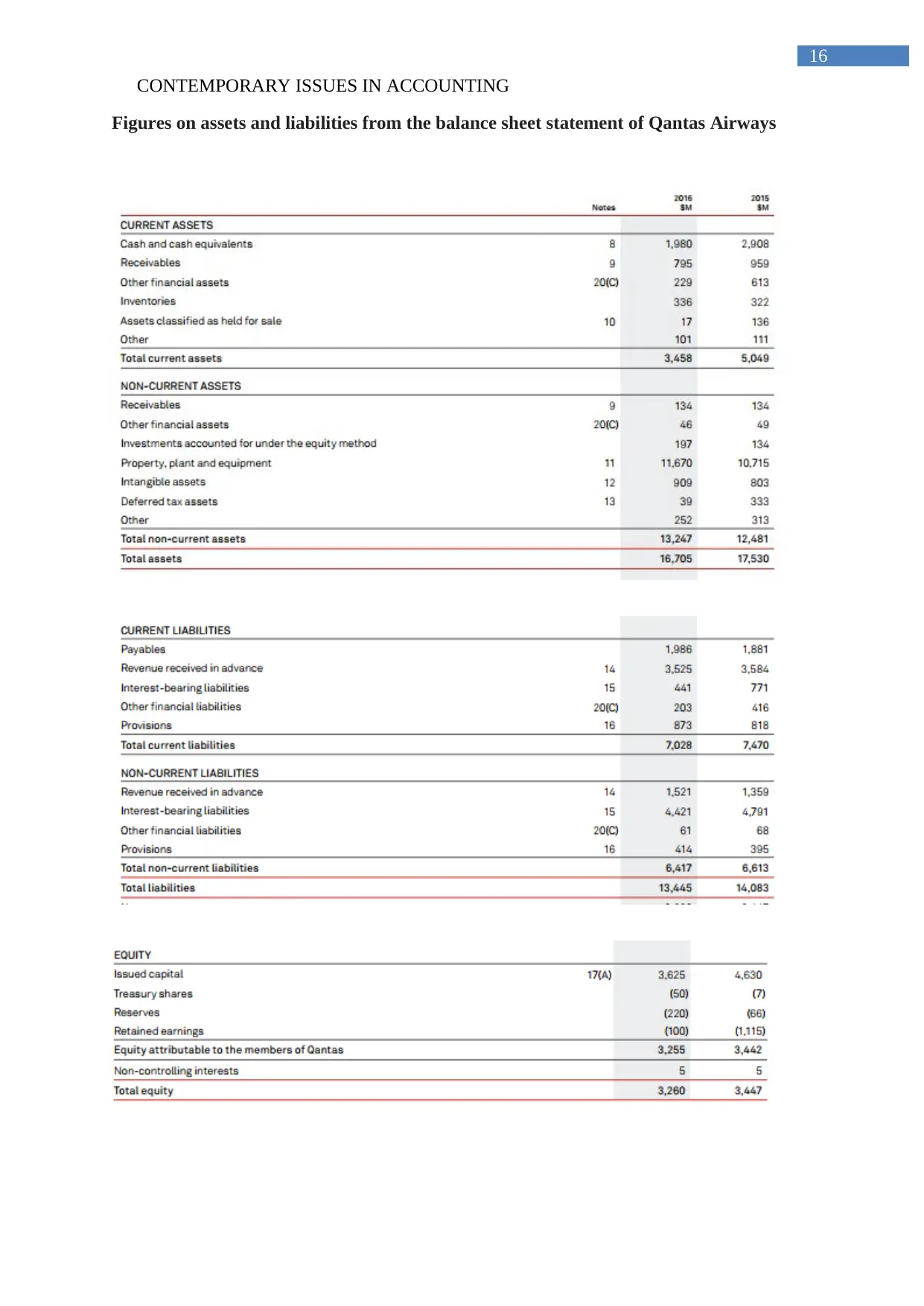

annual report for the financial year 2016 declares the asset worth $13445 million.

Liabilities:

As mentioned in the financial declaration of the firm Qantas Airways, the overall liabilities

are hereby presented to be worth $13445 million during FY2016. Particularly, the balance

sheet statement of Qantas Airways presents liabilities (counting both current as well as non-

current ones) that can be utilized for financing different functionalities and deals involved in

carrying out the operations of the firm. Analysis of financial assertions replicate the fact that

liability is presented at the historical cost and thereafter valued at the operational currency

that is necessarily reflected in terms of Australian Dollar (Goodwin et al. 2016). In addition

to this, net defined liability of the firm is measured at the fair value of specific plan liabilities

after deduction of current value of defined benefit requirements.

Equity: A detailed study of balance sheet replicates that the equity possessed by the

shareholders is presented to be $3260 m during FY 2016. As mentioned in the annual

assertions of Qantas, the derivatives mentioned therein are calculated at fair values by using

mainly the firm’s earnings and expenses. Thus, it can be mentioned that Qantas makes use of

different models particularly for measuring derivatives that necessarily have the need to

follow the process of calculation at fair value (Biondi and Lapsley 2014).

CONTEMPORARY ISSUES IN ACCOUNTING

The assets of Qantas Airways are reflected in terms of Australian dollars that is necessarily

the functional currency of the corporation. Nevertheless, the procedure of analysis of assets

mentioned in financial assertions reflect the fact that assets can be classified as “held for sale”

enumerated at low value of the recognized cost compared to the fair values after deduction of

the cost borne for sales. Detailed analysis of report also replicates that net defined

assets/resources of Qantas Airways is necessarily presented at the fair value of planned

assets only after the deduction of specific obligation at current value (Williams 2014). The

annual report for the financial year 2016 declares the asset worth $13445 million.

Liabilities:

As mentioned in the financial declaration of the firm Qantas Airways, the overall liabilities

are hereby presented to be worth $13445 million during FY2016. Particularly, the balance

sheet statement of Qantas Airways presents liabilities (counting both current as well as non-

current ones) that can be utilized for financing different functionalities and deals involved in

carrying out the operations of the firm. Analysis of financial assertions replicate the fact that

liability is presented at the historical cost and thereafter valued at the operational currency

that is necessarily reflected in terms of Australian Dollar (Goodwin et al. 2016). In addition

to this, net defined liability of the firm is measured at the fair value of specific plan liabilities

after deduction of current value of defined benefit requirements.

Equity: A detailed study of balance sheet replicates that the equity possessed by the

shareholders is presented to be $3260 m during FY 2016. As mentioned in the annual

assertions of Qantas, the derivatives mentioned therein are calculated at fair values by using

mainly the firm’s earnings and expenses. Thus, it can be mentioned that Qantas makes use of

different models particularly for measuring derivatives that necessarily have the need to

follow the process of calculation at fair value (Biondi and Lapsley 2014).

7

CONTEMPORARY ISSUES IN ACCOUNTING

Inventory: The financial position of Qantas Airways together with efficiency level if firm

can be gauged from the analysis of inventory. The inventory is registered to be $336 m

during FY 2016 up from $322 m in FY 2015. This enhancement in inventory can replicate

the lack of efficiency of the corporation to handle the inventory of the firm Qantas Airways to

control the inventory and might possibly decline the competitive position of the corporation

(Andon et al. 2015).

Accounts Receivable as well as Provisions for bad debt and provision for doubtful debt

As mentioned in the yearly consolidated report of the corporation, accounts receivables of

Qantas Airways are recorded to be $795 million in the financial year 2016. The receivables

counting both the current and non-current receivables declined to $929 million during FY

2016 from $1093 million during FY2015. Evaluation of Qantas Airway’s financial

pronouncements of corporation assists in comprehending non-current receivables. The

declaration hereby helps in analysing the information on declining receivables. The

receivables are necessarily recorded at fair values and enumerated at amortised cost using

interest method after deduction of outlays of the firm for impairments. There is an optimal

framework for capital simultaneously lessening the debt level and enhancing liquidity that

directed the way towards return enhancement (Ferguson et al. 2014).

Analysis of financial reports as regards relevance as well as faithful representation

The fundamental characteristics of effectual financial information contain relevance as well

as faithful representation of company’s pecuniary information.

As correctly mentioned by Yao et al. (2015), relevance of financial information refers to

pecuniary information that indicates towards variance in diverse decisions made by different

CONTEMPORARY ISSUES IN ACCOUNTING

Inventory: The financial position of Qantas Airways together with efficiency level if firm

can be gauged from the analysis of inventory. The inventory is registered to be $336 m

during FY 2016 up from $322 m in FY 2015. This enhancement in inventory can replicate

the lack of efficiency of the corporation to handle the inventory of the firm Qantas Airways to

control the inventory and might possibly decline the competitive position of the corporation

(Andon et al. 2015).

Accounts Receivable as well as Provisions for bad debt and provision for doubtful debt

As mentioned in the yearly consolidated report of the corporation, accounts receivables of

Qantas Airways are recorded to be $795 million in the financial year 2016. The receivables

counting both the current and non-current receivables declined to $929 million during FY

2016 from $1093 million during FY2015. Evaluation of Qantas Airway’s financial

pronouncements of corporation assists in comprehending non-current receivables. The

declaration hereby helps in analysing the information on declining receivables. The

receivables are necessarily recorded at fair values and enumerated at amortised cost using

interest method after deduction of outlays of the firm for impairments. There is an optimal

framework for capital simultaneously lessening the debt level and enhancing liquidity that

directed the way towards return enhancement (Ferguson et al. 2014).

Analysis of financial reports as regards relevance as well as faithful representation

The fundamental characteristics of effectual financial information contain relevance as well

as faithful representation of company’s pecuniary information.

As correctly mentioned by Yao et al. (2015), relevance of financial information refers to

pecuniary information that indicates towards variance in diverse decisions made by different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CONTEMPORARY ISSUES IN ACCOUNTING

users. Evaluation of pecuniary information in Qantas’s report can help in comprehending

variances in various economic decisions and this has both a predictive together with the

confirmatory value. Again, faithful representation replicates diverse economic events

expressed in specific numerical presentation along with supporting literature.

Critical analysis of fundamental qualitative enhancing features of financial report

The elementary qualitative characteristics of effectual financial information provided in the

financial assertion comprises of relevance as well as faithful representation of specific

pecuniary information.

Relevance: As rightly indicated by Laing and Perrin (2014), relevance of particularly

financial information can help in presenting variances in economic decisions of diverse users

if it has specific predictive value. Evaluation of financial information provided in the report

can also help in presenting a variance in the economic decisions and in addition to this the

same also has certain predictive value besides confirmatory value.

Faithful representation: Yao et al. (2015) assert that faithful representation also helps in

reflecting economic incidents expressed in literature and numbers. However, in order to be

effectual, pecuniary information necessarily has the need to be enough pertinent and at the

same time need to have faithful representation. Thorough analysis of financial

pronouncements of the corporation evidently states about consumer confidence, economic

fundamentals of Australia, worldwide growth facets and information on trading partners

together with the global forces. Apart from this, financial assertions of the corporation Qantas

Airways also concisely presets all the appropriate financial performance both in numbers as

well literature.

CONTEMPORARY ISSUES IN ACCOUNTING

users. Evaluation of pecuniary information in Qantas’s report can help in comprehending

variances in various economic decisions and this has both a predictive together with the

confirmatory value. Again, faithful representation replicates diverse economic events

expressed in specific numerical presentation along with supporting literature.

Critical analysis of fundamental qualitative enhancing features of financial report

The elementary qualitative characteristics of effectual financial information provided in the

financial assertion comprises of relevance as well as faithful representation of specific

pecuniary information.

Relevance: As rightly indicated by Laing and Perrin (2014), relevance of particularly

financial information can help in presenting variances in economic decisions of diverse users

if it has specific predictive value. Evaluation of financial information provided in the report

can also help in presenting a variance in the economic decisions and in addition to this the

same also has certain predictive value besides confirmatory value.

Faithful representation: Yao et al. (2015) assert that faithful representation also helps in

reflecting economic incidents expressed in literature and numbers. However, in order to be

effectual, pecuniary information necessarily has the need to be enough pertinent and at the

same time need to have faithful representation. Thorough analysis of financial

pronouncements of the corporation evidently states about consumer confidence, economic

fundamentals of Australia, worldwide growth facets and information on trading partners

together with the global forces. Apart from this, financial assertions of the corporation Qantas

Airways also concisely presets all the appropriate financial performance both in numbers as

well literature.

9

CONTEMPORARY ISSUES IN ACCOUNTING

Analytical evaluation of enhancing qualitative characteristic of financial report

Laing and Perrin (2014) mention that the enhancing qualitative enhancing characteristics of

financial report include comparability, understandability, timeliness as well as verifiability.

Comparability: As correctly mentioned by Andon et al. (2015), comparability refers to

specific information as regards a reporting entity that can necessarily assist diverse users to

detect and realize different similarities as well as dissimilarities among diverse accounting

items. In actual fact, the assessment of the functions as well as operations assists in

comparative assessment of financial information and evaluation of the entire set and

worldwide operating environment. Essentially, the figures for diverse metrics namely

operating margin, growth of the revenue, global capacity and many others for diverse time

period aid in information comparability.

Verifiability: Laing and Perrin (2014) assert that verifiability aids on presupposing users that

information replicates faithfully particular economic incidence that it purports to replicate.

Again, the financial information of the corporation inevitably abides by the directives of the

Corporation Act (2001) as well as the listing regulations stipulated under the ASX-

Australian Stock Exchange. Financial assertion of the corporation replicates the fact that

administration of the firm Qantas Airways has adopted the stratagem of presenting

disclosures that consequently can help financiers of the corporation to assess financial

condition of the firm. As such, the continuous disclosures pronounced by the firm in the

annual report can also aid in the process of augmentation of confidence among financiers by

maintaining transparency, reliability along with integrity of the corporation’s operations

together with the financial statement of Qantas Airways.

Timeliness: This indicates towards available information that needs to be accessible to

decision makers in time for influencing their decisions.

CONTEMPORARY ISSUES IN ACCOUNTING

Analytical evaluation of enhancing qualitative characteristic of financial report

Laing and Perrin (2014) mention that the enhancing qualitative enhancing characteristics of

financial report include comparability, understandability, timeliness as well as verifiability.

Comparability: As correctly mentioned by Andon et al. (2015), comparability refers to

specific information as regards a reporting entity that can necessarily assist diverse users to

detect and realize different similarities as well as dissimilarities among diverse accounting

items. In actual fact, the assessment of the functions as well as operations assists in

comparative assessment of financial information and evaluation of the entire set and

worldwide operating environment. Essentially, the figures for diverse metrics namely

operating margin, growth of the revenue, global capacity and many others for diverse time

period aid in information comparability.

Verifiability: Laing and Perrin (2014) assert that verifiability aids on presupposing users that

information replicates faithfully particular economic incidence that it purports to replicate.

Again, the financial information of the corporation inevitably abides by the directives of the

Corporation Act (2001) as well as the listing regulations stipulated under the ASX-

Australian Stock Exchange. Financial assertion of the corporation replicates the fact that

administration of the firm Qantas Airways has adopted the stratagem of presenting

disclosures that consequently can help financiers of the corporation to assess financial

condition of the firm. As such, the continuous disclosures pronounced by the firm in the

annual report can also aid in the process of augmentation of confidence among financiers by

maintaining transparency, reliability along with integrity of the corporation’s operations

together with the financial statement of Qantas Airways.

Timeliness: This indicates towards available information that needs to be accessible to

decision makers in time for influencing their decisions.

10

CONTEMPORARY ISSUES IN ACCOUNTING

Understandability: Evaluation of financial pronouncements helps in reflecting notes to

financial declarations and significant accounting policies that again can augment

understandability (Yao et al. 2015). The process of preparations together with presentation of

financial assertions of the corporation also follow particular conceptual framework of mainly

conceptual framework of AASB. Subsequently, this can help in acquiring clear understanding

regarding entire process of measurement of different accounting items in the financial

pronouncements. Investors can also examine effectiveness of corporation in utilizing the

report presented using standards of AASB. Maintenance of adherence to standards and

guiding principles can therefore help in enumeration, averting efforts to deliberate

misstatements and certify steadiness of financial information.

Conclusion

The above mentioned study helps in evaluating different items of financial pronouncements

of Qantas Airways and different themes of financial measurements. Apart from this, the

current study helps in understanding specific issues related to enumeration of pecuniary

declarations in terms of AASB. Moreover, this study also helps in gaining understanding

regarding nature of relation between system of measurement and provision of different

decisions.

CONTEMPORARY ISSUES IN ACCOUNTING

Understandability: Evaluation of financial pronouncements helps in reflecting notes to

financial declarations and significant accounting policies that again can augment

understandability (Yao et al. 2015). The process of preparations together with presentation of

financial assertions of the corporation also follow particular conceptual framework of mainly

conceptual framework of AASB. Subsequently, this can help in acquiring clear understanding

regarding entire process of measurement of different accounting items in the financial

pronouncements. Investors can also examine effectiveness of corporation in utilizing the

report presented using standards of AASB. Maintenance of adherence to standards and

guiding principles can therefore help in enumeration, averting efforts to deliberate

misstatements and certify steadiness of financial information.

Conclusion

The above mentioned study helps in evaluating different items of financial pronouncements

of Qantas Airways and different themes of financial measurements. Apart from this, the

current study helps in understanding specific issues related to enumeration of pecuniary

declarations in terms of AASB. Moreover, this study also helps in gaining understanding

regarding nature of relation between system of measurement and provision of different

decisions.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

CONTEMPORARY ISSUES IN ACCOUNTING

References

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage

assets problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Ferguson, A., Pündrich, G. and Raftery, A., 2014. Auditor industry specialization, service

bundling, and partner effects in a mining-dominated city. Auditing: A Journal of Practice &

Theory, 33(3), pp.153-180.

Gelmini, L., Bavagnoli, F., Comoli, M. and Riva, P., 2015. Waiting for Materiality in the

Context of Integrated Reporting: Theoretical Challenges and Preliminary Empirical Findings.

In Sustainability Disclosure: State of the Art and New Directions(pp. 135-163). Emerald

Group Publishing Limited.

Goodwin, J., Atilgan, Y., Simsir, S.A. and Ahmed, K., 2016. Investor reaction to accounting

misstatements under IFRS: Australian evidence.

Harris, J.M. and Roach, B., 2013. Environmental and natural resource economics: A

contemporary approach. ME Sharpe.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Laing, G.K. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB

116 non-current asset measurement models. International Journal of Critical

Accounting, 6(5-6), pp.509-519.

CONTEMPORARY ISSUES IN ACCOUNTING

References

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage

assets problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Ferguson, A., Pündrich, G. and Raftery, A., 2014. Auditor industry specialization, service

bundling, and partner effects in a mining-dominated city. Auditing: A Journal of Practice &

Theory, 33(3), pp.153-180.

Gelmini, L., Bavagnoli, F., Comoli, M. and Riva, P., 2015. Waiting for Materiality in the

Context of Integrated Reporting: Theoretical Challenges and Preliminary Empirical Findings.

In Sustainability Disclosure: State of the Art and New Directions(pp. 135-163). Emerald

Group Publishing Limited.

Goodwin, J., Atilgan, Y., Simsir, S.A. and Ahmed, K., 2016. Investor reaction to accounting

misstatements under IFRS: Australian evidence.

Harris, J.M. and Roach, B., 2013. Environmental and natural resource economics: A

contemporary approach. ME Sharpe.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial

accounting. Pearson Higher Education AU.

Laing, G.K. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB

116 non-current asset measurement models. International Journal of Critical

Accounting, 6(5-6), pp.509-519.

12

CONTEMPORARY ISSUES IN ACCOUNTING

McCombs, M., 2017. Contemporary public opinion: Issues and the news. Routledge.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Journal of Contemporary Accounting &

Economics. Journal of Contemporary Accounting & Economics, 11, pp.31-45.

CONTEMPORARY ISSUES IN ACCOUNTING

McCombs, M., 2017. Contemporary public opinion: Issues and the news. Routledge.

Williams, J., 2014. Financial accounting. McGraw-Hill Higher Education.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Journal of Contemporary Accounting &

Economics. Journal of Contemporary Accounting & Economics, 11, pp.31-45.

13

CONTEMPORARY ISSUES IN ACCOUNTING

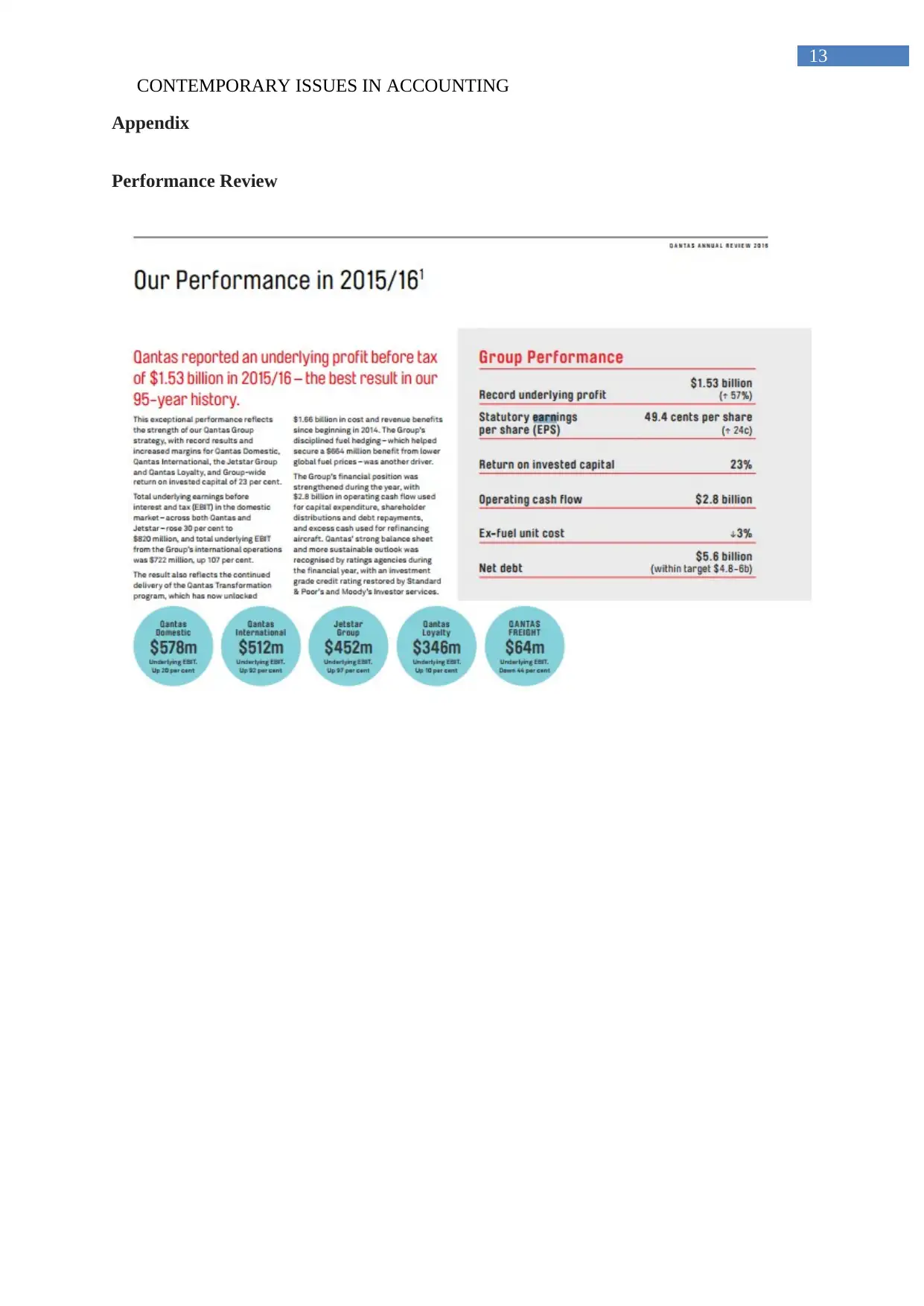

Appendix

Performance Review

CONTEMPORARY ISSUES IN ACCOUNTING

Appendix

Performance Review

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

CONTEMPORARY ISSUES IN ACCOUNTING

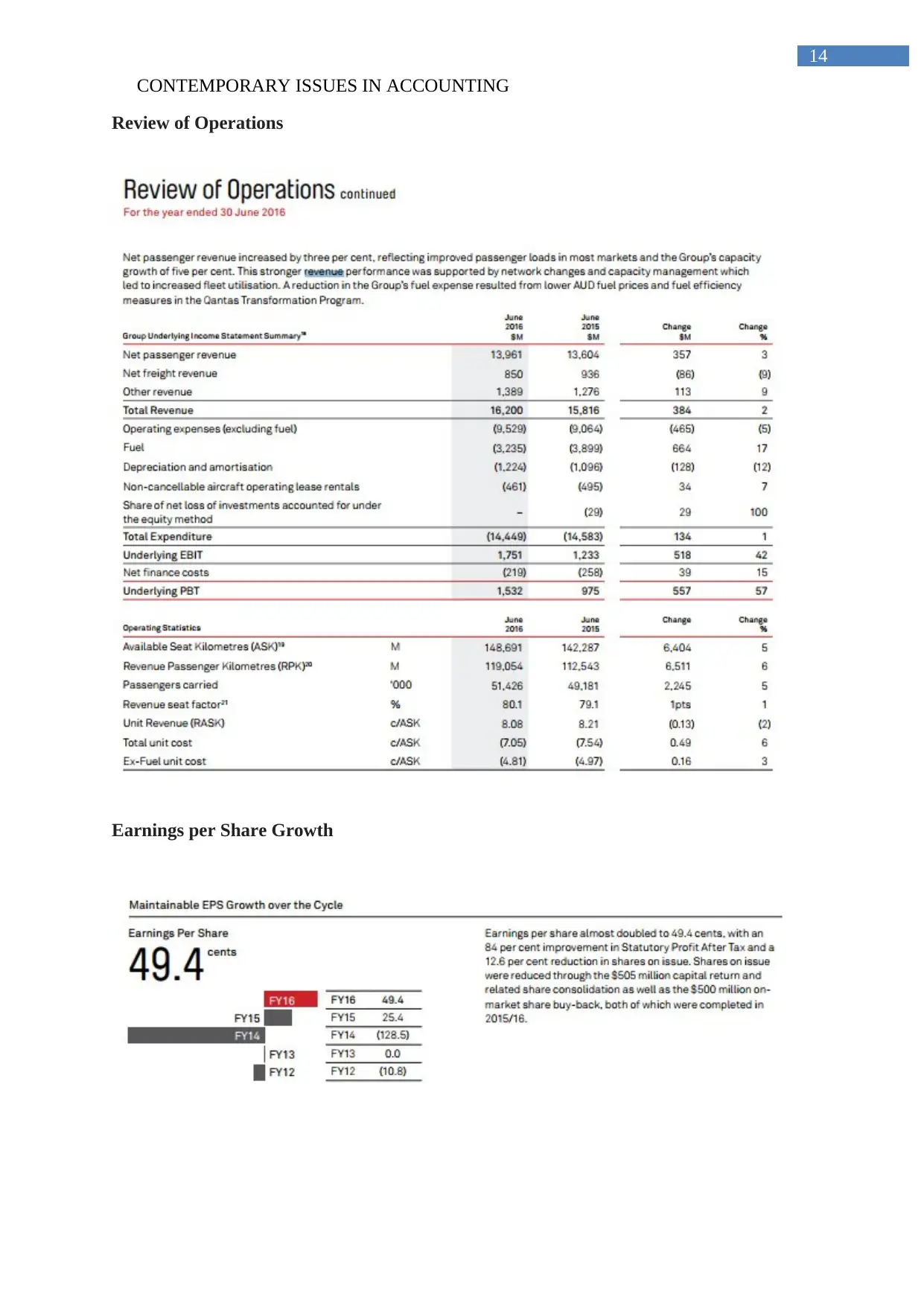

Review of Operations

Earnings per Share Growth

CONTEMPORARY ISSUES IN ACCOUNTING

Review of Operations

Earnings per Share Growth

15

CONTEMPORARY ISSUES IN ACCOUNTING

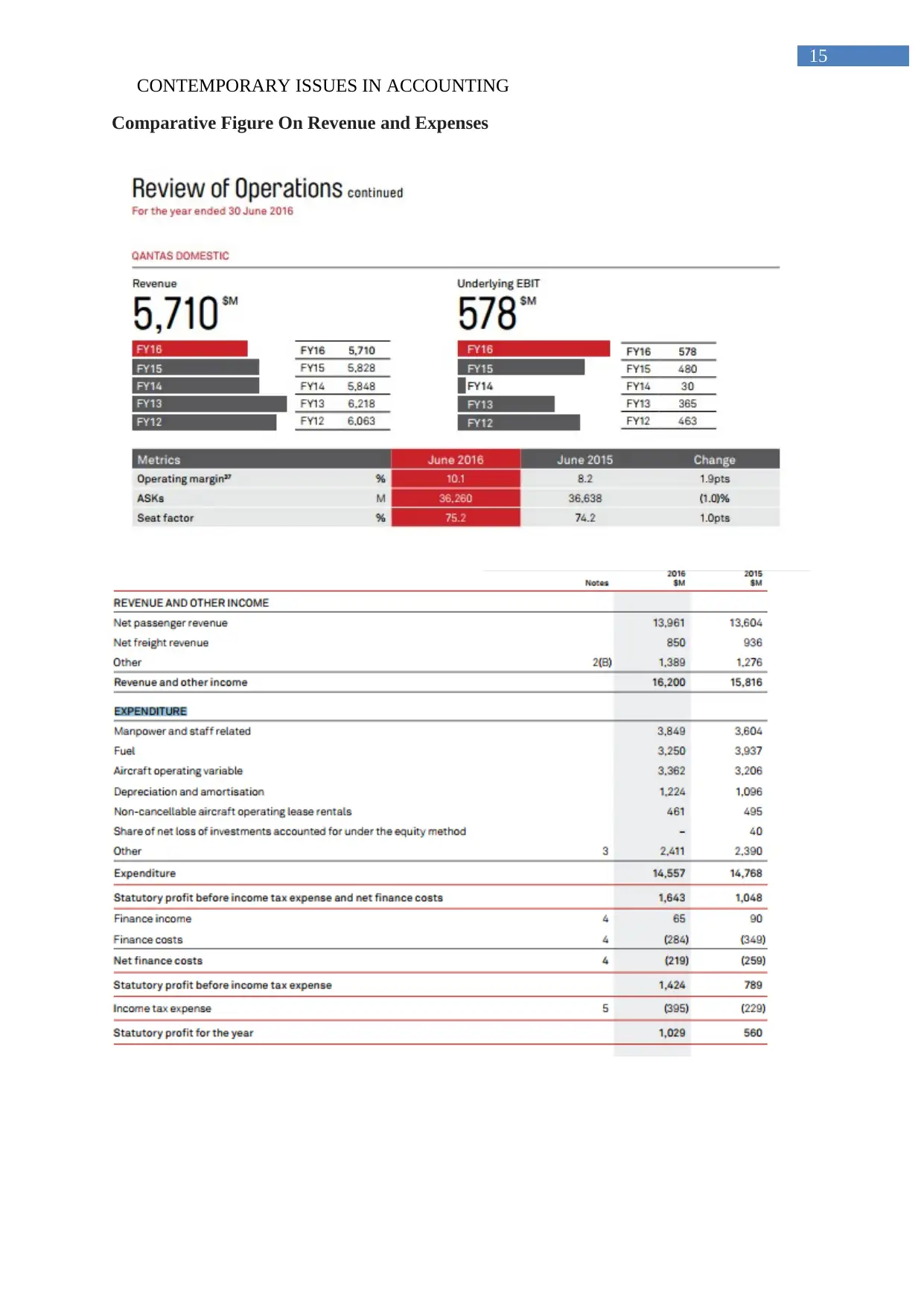

Comparative Figure On Revenue and Expenses

CONTEMPORARY ISSUES IN ACCOUNTING

Comparative Figure On Revenue and Expenses

16

CONTEMPORARY ISSUES IN ACCOUNTING

Figures on assets and liabilities from the balance sheet statement of Qantas Airways

CONTEMPORARY ISSUES IN ACCOUNTING

Figures on assets and liabilities from the balance sheet statement of Qantas Airways

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

CONTEMPORARY ISSUES IN ACCOUNTING

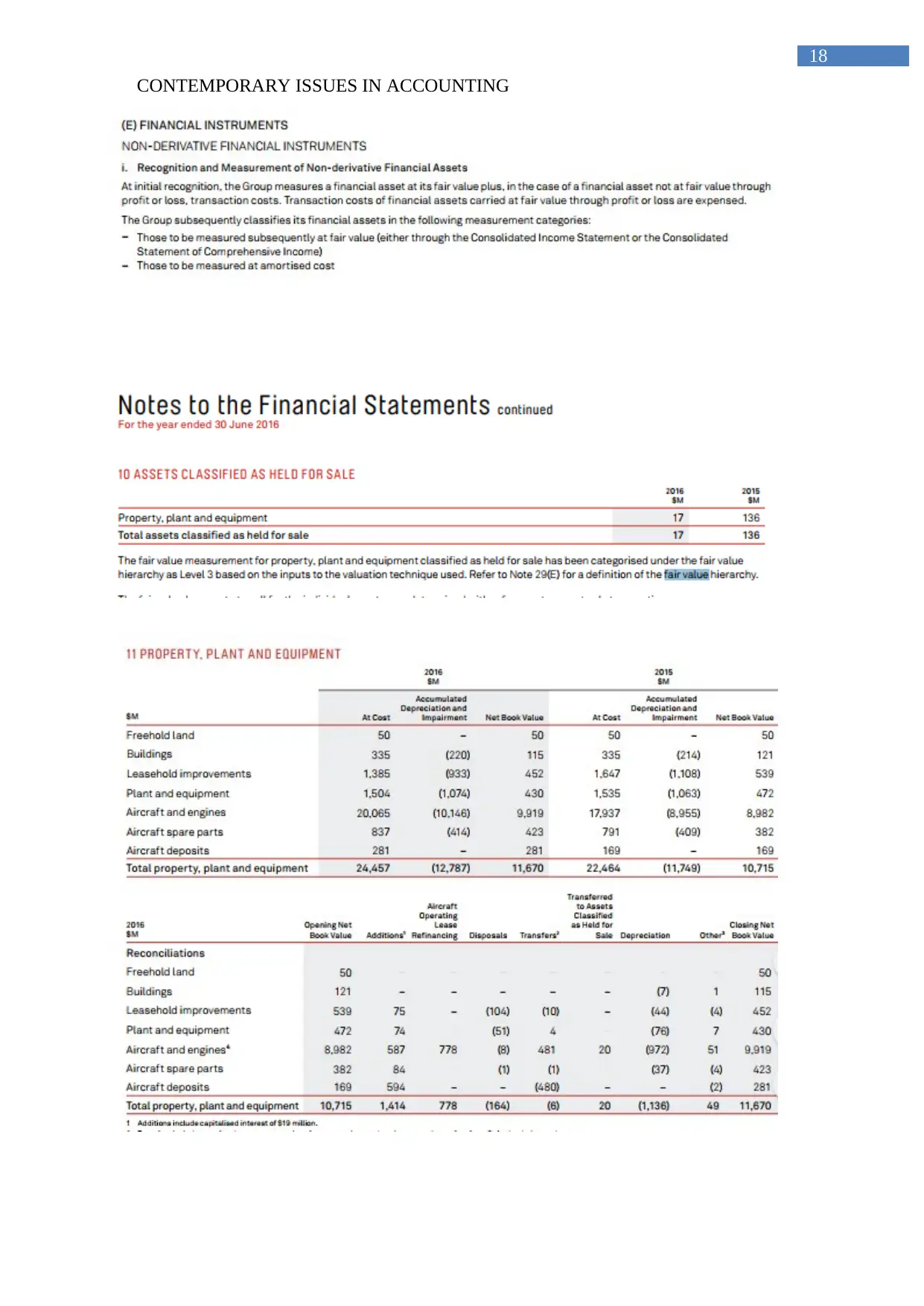

Statement of Compliance

Basis of Preparation

Recognition

CONTEMPORARY ISSUES IN ACCOUNTING

Statement of Compliance

Basis of Preparation

Recognition

18

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

19

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.